Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 7.19% CAGR |

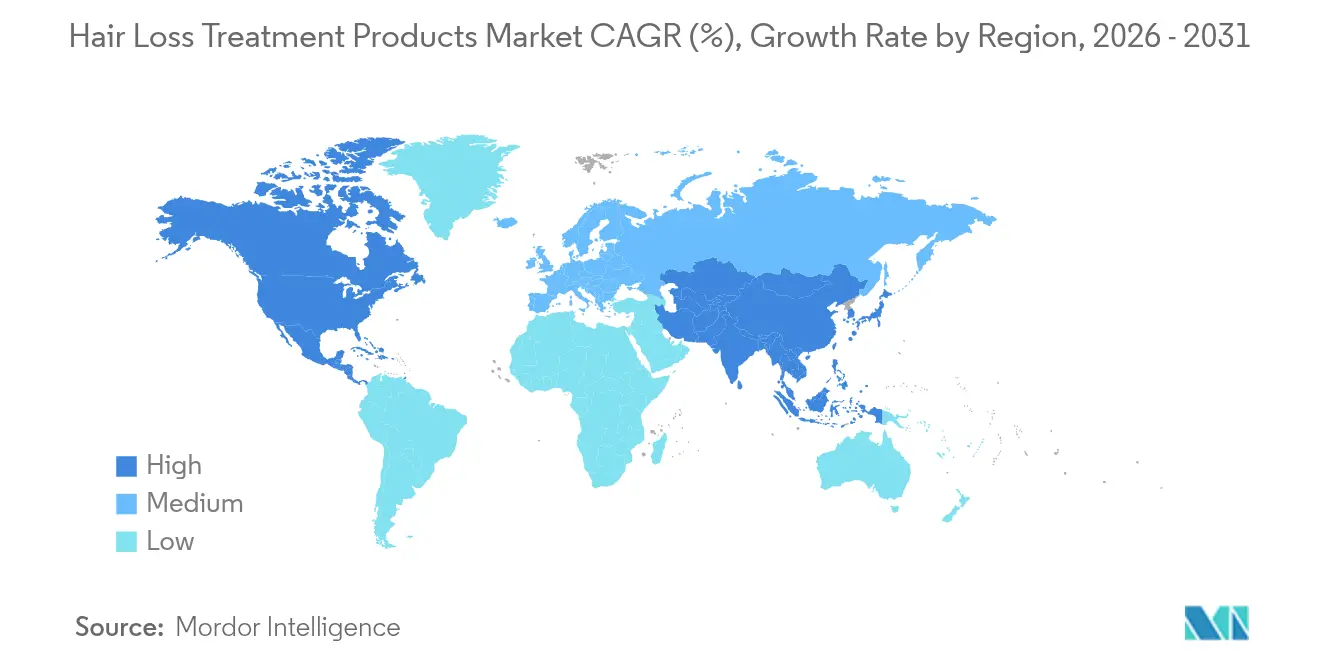

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

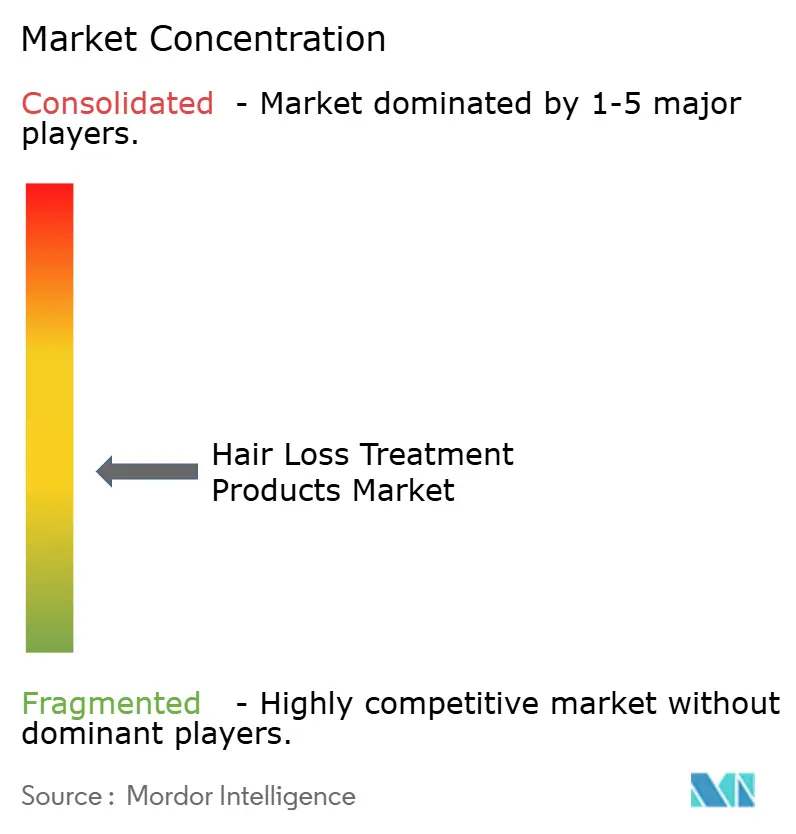

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Loss Treatment Products Market Analysis by Mordor Intelligence

Hair Loss Treatment Products Market size in 2026 is estimated at USD 3.14 billion, growing from 2025 value of USD 2.93 billion with 2031 projections showing USD 4.45 billion, growing at 7.19% CAGR over 2026-2031. This expansion reflects a confluence of demographic pressures and technological breakthroughs that are reshaping treatment paradigms across consumer segments. The FDA's approval of deuruxolitinib (Leqselvi) in July 2024 for severe alopecia areata marked a pivotal regulatory milestone, signaling heightened institutional confidence in advanced therapeutic approaches[1]Source: U.S Food & Drug Administration, "Approval of deuruxolitinib", fda.gov. North America commands early-mover advantage, yet Asia-Pacific’s youthful population, digital engagement, and innovation capacity underpin its status as the fastest-growing regional cluster. Competitive intensity is moderate; established consumer-health majors coexist alongside venture-backed biotech start-ups that deploy highly targeted delivery systems and personalized regimens. Growth opportunities increasingly concentrate around omnichannel distribution, combination therapy kits, and premium serums that promise visible results within 90 days.

Key Report Takeaways

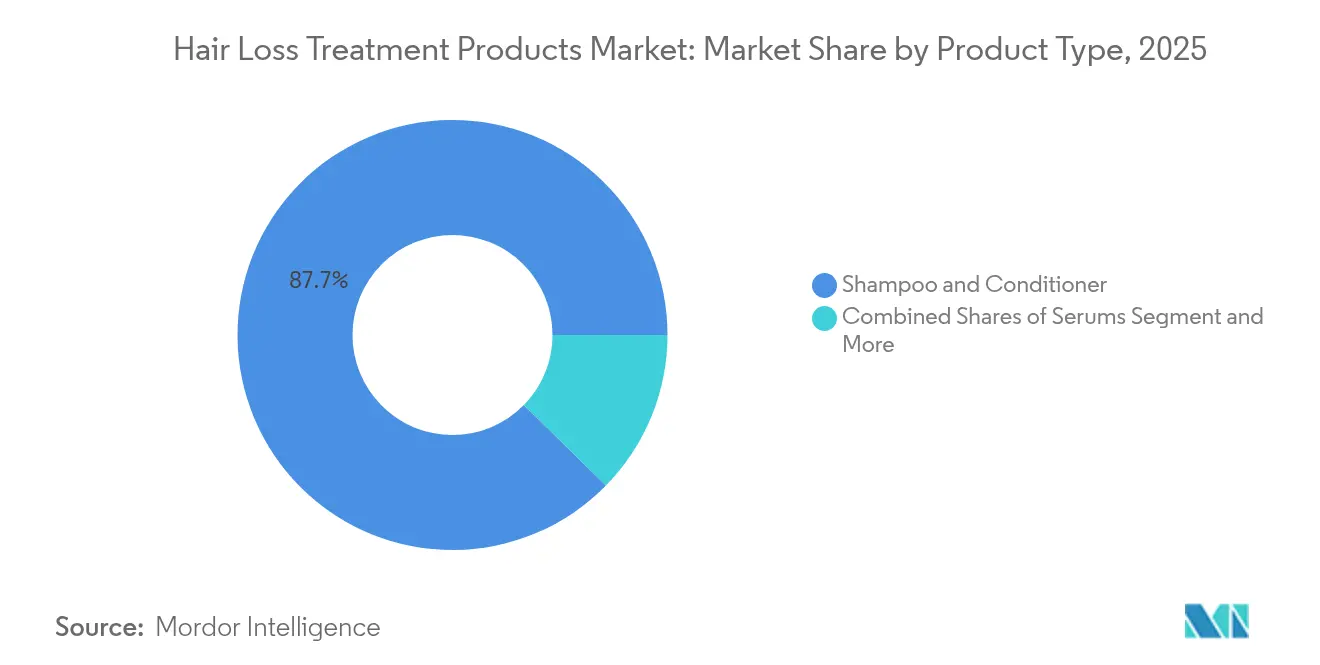

- By product type, shampoos and conditioners held 87.65% of the hair loss treatment products market share in 2025, whereas serums are forecast to advance at an 8.02% CAGR through 2031.

- By gender, female consumers accounted for 70.45% of 2025 revenue, while the same segment is projected to expand at a 9.12% CAGR to 2031.

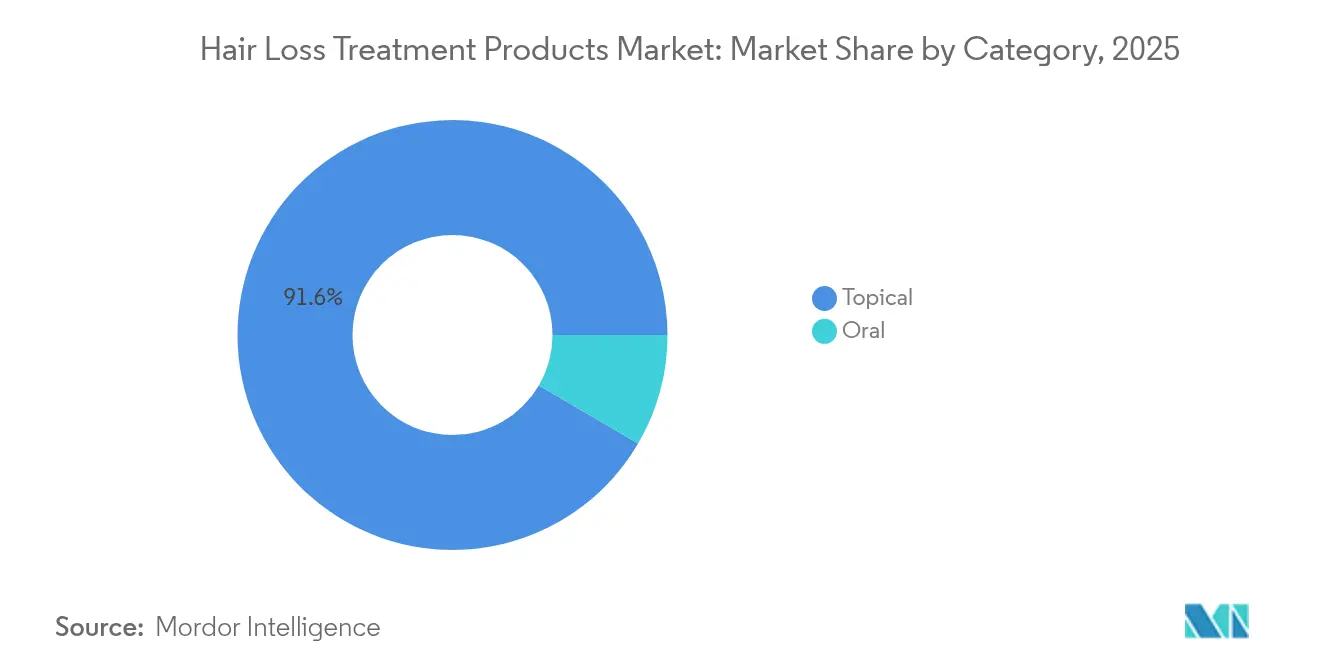

- By category, topical formulations represented 91.58% of revenue in 2025; oral supplements are expected to post an 8.55% CAGR through 2031.

- By distribution channel, health and beauty stores captured 46.10% revenue share in 2025; online retail is projected to grow at an 8.21% CAGR between 2026-2031.

- By geography, North America led with 35.62% share in 2025, while Asia-Pacific is anticipated to register a 8.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hair Loss Treatment Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population | +1.8% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Scientific and Technological Advancements | +1.2% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Influence of social media and Beauty Influencers | +0.9% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Non-invasive Alternatives Gaining Traction | +0.7% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Heightened Aesthetic Awareness | +0.6% | Global, with urban concentration | Short term (≤ 2 years) |

| Expansion of Modern Retail and E-commerce | +0.5% | Asia-Pacific and North America, spreading globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population

Demographic transitions across developed markets are fundamentally altering treatment demand patterns, with individuals aged 50+ representing the fastest-growing consumer segment. According to MedlinePlus.gov, Androgenetic alopecia, commonly recognized as male pattern baldness in men and female pattern hair loss in women, is a prevalent cause of hair loss for both genders. The aging population's higher disposable income and healthcare spending propensity drives premium product adoption, particularly in North America where consumers aged 55+ account for 40% of hair loss treatment expenditure. Recent studies indicate that age-related hormonal changes accelerate hair follicle miniaturization, creating demand for targeted therapeutic interventions beyond traditional cosmetic approaches. This demographic shift coincides with increased longevity expectations, extending the treatment duration and lifetime customer value for manufacturers.

Scientific and Technological Advancements

Biotechnology breakthroughs are revolutionizing treatment efficacy through precision delivery mechanisms and regenerative approaches. Nanotechnology platforms enable targeted follicular penetration, with recent clinical trials demonstrating 3x improved bioavailability compared to conventional topical formulations. The development of siRNA therapeutics targeting specific hair loss pathways represents a paradigm shift from symptom management to root cause intervention. Pelage Pharmaceuticals' PP405, currently in Phase 2a trials, exemplifies this approach by activating dormant hair follicle stem cells through novel signaling pathways. Advanced delivery systems, including microneedle patches loaded with growth factors and exosome-based treatments, are demonstrating measurable improvements in hair density and thickness metrics. These technological advances are supported by increased patent filings, with South Korea leading at significant share of global hair loss treatment patents in 2024, reflecting intensive R&D investment across the value chain.

Influence of Social Media and Beauty Influencers

Digital platforms are reshaping consumer awareness and treatment adoption patterns, with user-generated content driving a siginificant share of growth in scalp care product demand during 2024. Social media influencers are normalizing hair loss discussions, particularly among younger demographics who previously avoided treatment seeking. The mainstreaming of minoxidil usage through influencer endorsements has expanded the addressable market beyond traditional clinical settings, with direct-to-consumer brands capturing significant market share. Beauty influencers' emphasis on preventive care is driving early intervention trends, with consumers in their 20s and 30s representing the fastest-growing treatment initiation segment. Platform-specific content strategies, including before-and-after documentation and treatment journey sharing, are creating authentic peer-to-peer recommendations that surpass traditional advertising effectiveness. This influence extends globally, with Asian markets showing particularly strong correlation between social media engagement and treatment adoption rates.

Non-invasive Alternatives Gaining Traction

Consumer preference shifts toward non-surgical interventions are accelerating adoption of topical and device-based treatments over invasive procedures. The FDA's approval of low-level laser therapy devices, including HairMax's expanded product line with 510(k) clearance, validates non-invasive efficacy claims and reduces treatment barriers. Clinical evidence supporting combination therapies, including microneedling with topical actives, demonstrates comparable results to surgical interventions at significantly lower cost and risk profiles. Recent studies indicate that 78% of consumers prefer topical treatments over surgical options when efficacy data supports comparable outcomes. Device-based treatments, including LED therapy and radiofrequency systems, are gaining acceptance through clinical validation and improved accessibility. The integration of at-home treatment devices with professional monitoring through telemedicine platforms is creating hybrid care models that combine convenience with clinical oversight.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of Counterfeit and Unsafe Products | -0.8% | Global, highest in emerging markets | Short term (≤ 2 years) |

| Regulatory Hurdles and Approval Delays | -0.6% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Potential Side Effects | -0.4% | Global, with regional variation in reporting | Medium term (2-4 years) |

| Variable Product Effectiveness | -0.3% | Global, with higher impact in price-sensitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prevalence of Counterfeit and Unsafe Products

Market proliferation of unregulated formulations undermines consumer confidence and creates safety concerns that constrain legitimate market growth. Counterfeit products, particularly prevalent in online marketplaces, often contain undisclosed active ingredients or harmful substances that can cause adverse reactions. Regulatory agencies report increasing seizures of fake hair loss treatments, with the FDA issuing multiple warnings about unapproved products containing prescription-strength ingredients without proper labeling. The challenge is particularly acute in emerging markets where regulatory oversight may be limited and price sensitivity drives consumers toward unverified alternatives. Consumer education initiatives and enhanced supply chain verification are becoming critical for maintaining market integrity and protecting brand reputation across legitimate manufacturers.

Regulatory Hurdles and Approval Delays

Complex approval processes for novel therapeutic approaches create market entry barriers and delay innovation commercialization. The FDA's stringent requirements for demonstrating both safety and efficacy extend development timelines and increase costs for manufacturers pursuing advanced formulations. International regulatory harmonization remains incomplete, requiring separate approval processes across major markets and creating additional complexity for global product launches. Recent regulatory developments, including the FDA's guidance on combination products and the EMA's centralized approval pathway, aim to streamline processes while maintaining safety standards. However, the evolving regulatory landscape for biotechnology-based treatments continues to create uncertainty for investment decisions and product development timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoos Dominate While Serums Drive Innovation

Shampoo and conditioner products command 87.65% market share in 2025, reflecting their role as entry-level treatments and daily-use convenience for consumers seeking hair health maintenance. This dominance stems from established distribution networks, consumer familiarity, and integration into existing hair care routines without requiring behavioral changes. However, serums represent the fastest-growing segment at 8.02% CAGR through 2031, driven by targeted therapeutic formulations and premium positioning that appeals to treatment-focused consumers. The serum category benefits from advanced delivery technologies, including nanotechnology platforms and bioactive compounds that demonstrate measurable efficacy improvements over traditional formulations.

Other product categories, encompassing oils, gummies, and tablets, maintain steady growth trajectories supported by consumer preference for diverse treatment modalities and combination therapy approaches. The FDA's oversight of dietary supplements through the Dietary Supplement Health and Education Act provides regulatory framework for oral formulations, while topical oils benefit from natural ingredient trends and minimal processing appeals. Recent product launches, including Orthomol Hair Solution's introduction in German pharmacies with Baicapil complex, demonstrate continued innovation across traditional product categories. Manufacturing advances in encapsulation technology and sustained-release formulations are enhancing product efficacy across all categories, with impact on oral supplements and specialized topical treatments.

By Gender: Female Segment Leads Growth Despite Male Foundation

Female consumers represent 70.45% market share in 2025 and demonstrate the highest growth potential at 9.12% CAGR through 2031, reflecting evolving beauty standards and reduced stigma around hair loss treatment seeking. Social media influence plays a particularly strong role in female segment expansion, with beauty influencers normalizing hair loss discussions and promoting preventive care approaches. The female segment benefits from broader product variety, including cosmetically elegant formulations and multi-benefit products that address hair health alongside other beauty concerns. Clinical research indicates that female pattern hair loss affects in most of the women by age 50, creating substantial addressable market expansion as awareness increases.

Male consumers maintain significant market presence despite lower growth rates, with established treatment patterns and higher acceptance of pharmaceutical interventions. The male segment demonstrates stronger preference for clinically proven treatments, including FDA-approved medications and device-based therapies. Recent trends indicate increasing male adoption of comprehensive hair care routines, influenced by social media content and changing grooming standards. User-generated content on platforms like TikTok and Instagram is driving male engagement with hair loss topics, creating opportunities for brands to expand their male-focused product lines and marketing approaches.

By Category: Topical Applications Lead While Oral Supplements Gain Momentum

Advanced delivery systems are revolutionizing topical treatment efficacy, with topical applications maintaining 91.58% market share in 2025 through superior convenience and targeted action. Recent technological developments include microneedle patches loaded with growth factors, nanotechnology-enhanced penetration systems, and time-release formulations that extend active ingredient availability. The topical category benefits from consumer preference for localized treatment without systemic exposure, reducing concerns about side effects associated with oral medications. Clinical trials demonstrate that combination topical therapies, including minoxidil with complementary actives, achieve superior results compared to monotherapy approaches.

Oral supplements represent the fastest-growing category at 8.55% CAGR through 2031, driven by systemic approach benefits and convenience for consumers seeking comprehensive hair health support. The oral segment includes both prescription medications and dietary supplements, with growing clinical evidence supporting nutritional interventions for hair loss prevention and treatment. Recent research indicates that specific nutrient combinations, including biotin, zinc, and specialized amino acids, demonstrate measurable improvements in hair density and growth rates. Regulatory frameworks for dietary supplements continue evolving, with the FDA providing guidance on structure-function claims and labeling requirements that support market growth while ensuring consumer safety.

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

Health and beauty stores maintain 46.10% market share in 2025, leveraging professional consultation services and product demonstration capabilities that online channels cannot replicate. These traditional retailers benefit from established relationships with healthcare professionals and ability to provide personalized recommendations based on individual hair loss patterns. However, online retail stores demonstrate the strongest growth trajectory at 8.21% CAGR through 2031, driven by convenience, privacy, and direct-to-consumer brand proliferation. The digital channel expansion reflects changing consumer preferences for discreet purchasing and access to broader product selections not available in physical stores.

Supermarkets and hypermarkets serve as important accessibility channels for entry-level products, while other distribution channels, including dermatology clinics and specialty medical retailers, cater to prescription and professional-grade treatments. The integration of omnichannel strategies allows consumers to research online while purchasing in-store, creating hybrid shopping experiences that combine digital convenience with physical product interaction. Recent developments include telemedicine consultations linked to e-commerce platforms, enabling professional guidance for online purchases and improving treatment outcomes through proper product selection and usage monitoring.

Geography Analysis

North America commands 35.62% market share in 2025, supported by advanced healthcare infrastructure, high disposable income, and established treatment acceptance patterns. The region benefits from robust regulatory frameworks that ensure product safety while facilitating innovation, with the FDA's approval pathways supporting both pharmaceutical and device-based treatments. Recent regulatory developments, including the FDA's approval of deuruxolitinib for alopecia areata, demonstrate continued innovation in prescription treatments. Consumer awareness levels remain high, supported by healthcare professional education and direct-to-consumer marketing that normalizes treatment seeking behavior.

Asia-Pacific emerges as the fastest-growing region at 8.78% CAGR through 2031, driven by rising disposable income, increasing aesthetic awareness, and expanding healthcare access. The region demonstrates strength in technology adoption, with South Korea leading global patent filings at a significanr share of hair loss treatment innovations in 2024. Consumer preferences in Asia-Pacific markets favor natural ingredients and traditional medicine integration, creating opportunities for products that combine modern technology with botanical actives. China and India represent the largest growth opportunities within the region, supported by urbanization trends and evolving beauty standards that prioritize hair health and appearance.

Europe maintains steady growth supported by established healthcare systems and regulatory harmonization through the European Medicines Agency. The region demonstrates strong preference for clinically validated treatments and sustainable product formulations, with increasing demand for environmentally conscious packaging and ingredient sourcing. South America and Middle East and Africa represent emerging opportunities with growing middle-class populations and increasing healthcare spending, though market development remains constrained by economic factors and limited distribution infrastructure in some areas.

Regulatory Landscape

Regulation for hair loss treatment products is shaped by product classification across cosmetics, drugs, and medical devices. In the United States, rules differentiate cosmetics from drugs that claim to treat or prevent hair loss; under 21 CFR 310.527, OTC drug products for hair growth or hair loss prevention require robust evidentiary support, which constrains consumer claims while guiding parallel development of prescription therapies. The approval of deuruxolitinib (Leqselvi) in 2024 illustrates a higher-evidence pathway for therapeutic claims.

Internationally, EU MDR 2017/745 Annex XVI can pull certain cosmetic devices into medical-device oversight when risk profiles align, affecting at-home scalp-technology commercialization. In China, NMPA requires clinical testing and proof of efficacy for higher-risk functional claims, raising compliance for global brands. In the United States, state-level activity toward scalp cooling coverage, such as West Virginia HB 4089 in March 2026, signals ongoing policy alignment around medically associated hair loss support that intersects consumer channels.

Competitive Landscape

The hair loss treatment products market exhibits moderate fragmentation, creating opportunities for both established pharmaceutical companies and emerging biotechnology firms to capture market share through differentiated approaches. Strategic patterns reveal increasing investment in advanced delivery technologies and combination therapies, with companies pursuing vertical integration to control formulation development and manufacturing quality.

Major players leverage extensive distribution networks and brand recognition, while smaller firms focus on niche segments and innovative formulations that address specific consumer needs. Patent portfolios play crucial roles in competitive positioning, with companies like Olaplex demonstrating how proprietary bond-building technology can create sustainable competitive advantages across product categories. Pelage Pharmaceuticals' USD 14 million funding round in 2024 exemplifies investor confidence in regenerative medicine approaches targeting dormant hair follicle stem cells. Regulatory compliance frameworks, particularly FDA oversight for pharmaceutical products and device classifications, create barriers to entry while ensuring product safety and efficacy standards.

Technology adoption serves as a primary differentiation mechanism, with companies investing in nanotechnology platforms, bioactive delivery systems, and personalized treatment approaches. Recent SEC filings indicate substantial R&D investments across the sector, with biotechnology companies raising significant funding to advance clinical trials and regulatory approvals. Opportunities exist in personalized medicine approaches, combination therapy optimization, and emerging markets where treatment access remains limited by economic and infrastructure constraints.

Hair Loss Treatment Products Industry Leaders

-

The Procter & Gamble Company

-

L'Oréal S.A.

-

Unilever

-

Pierre Fabre Laboratories

-

Estée Lauder Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities exist at the intersection of prescription-grade innovation, evidence-backed cosmetic formulations, and non-invasive device-enabled regimens. Sun Pharmaceutical's LEQSELVI (deuruxolitinib) launch in the United States in 2025, following FDA approval, expands dermatologist-mediated access and supports adjacent demand for supportive scalp-care and cosmetic options. AbbVie's April 2026 FDA application for upadacitinib (RINVOQ) for adults and adolescents with severe alopecia areata expands the late-stage development footprint and creates whitespace for consumer-health brands to align topical and cosmetic adjunct products with medically managed journeys.

In mass and premium consumer lanes, clinical and AI-enabled substantiation differentiates products. Peer-reviewed randomized controlled trials published in April 2026 for a wearable electrotrichogenic device and for an AI-developed multi-target cosmetic hair tonic illustrate product development routes that pair measurable endpoints with consumer-friendly formats. Shampoos and conditioners remain the dominant entry point by value in 2025, while brands extending routines into scalp-focused systems with credible testing capture consumer interest in non-invasive solutions.

Recent Industry Developments

- May 2026: L'Oréal S.A. launched the L'Oréal Paris Elvive Collagen Peptide + Lifter collection exclusively at Walmart on May 1, 2026, targeting hair volumization with a skinification-led positioning. The exclusive retail tie-up strengthens mass-channel visibility and encourages regimen-based purchasing across complementary SKUs. It also intensifies competitive pressure in scalp and hair-fiber care systems where brands blend cosmetic benefits with treatment-adjacent claims.

- July 2025: Sun Pharmaceutical Industries Limited launched LEQSELVI (deuruxolitinib) in the United States for adults with severe alopecia areata after FDA approval. The rollout expands access to prescription options for severe cases and supports adjacent demand for supportive scalp-care and cosmetic camouflage products.

- July 2024: The U.S. FDA approved deuruxolitinib (Leqselvi) for severe alopecia areata. This milestone validated drug-lane approaches and influenced R&D and portfolio prioritization alongside consumer-oriented topical and device solutions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers retail and pharmacy hair loss treatment products sold for managing hair thinning and hair fall, across topical, oral, and supportive product formats, counted as manufacturer level revenue in USD.

Scope exclusions (for clarity): Surgical hair transplant procedures, in-clinic regenerative services, and general cosmetic hair styling products that do not claim hair loss treatment are not counted.

Segmentation Overview

-

By Product Type

- Shampoo and Conditioner

- Serums

- Others

-

By Gender

- Male

- Female

-

By Category

- Topical

- Oral

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a fact base on hair loss prevalence, treatment seeking behavior, and the regulated product landscape, so our model inputs do not float without real world anchors. Public sources that shaped assumptions include US FDA documentation for approvals and labeling updates, US CDC materials for population level trends, WHO health indicators, and national statistics agencies for age and gender splits by country.

We also reviewed company annual reports and investor presentations to understand portfolio mix, geographic exposure, and how firms describe category growth. This was followed by cross-checking with reputable press and association sites that track dermatology and consumer health trends. Where available, we used paid database subscriptions for company financials and intelligence, news and financials, patent databases, and an import-export shipment level database to sanity-check trade-exposed categories in selected markets. These examples are not exhaustive, and many other public sources were referenced for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk sources cannot fully answer, especially how demand is split between topical regimens, oral therapies, and supportive products, and how pricing moves by channel. We spoke with a mix of manufacturers, distributors, dermatology focused stakeholders, and retail channel participants across APAC, EMEA, and the Americas. We then re-checked key assumptions when we saw outliers in growth or pricing patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 19% | APAC: 40% |

| Mid tier: 44% | Functional/Unit leaders: 33% | EMEA: 36% |

| Smaller Players: 19% | Managers: 48% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that links adult population by age band to hair loss incidence indicators, then estimates the share actively using treatment products. That usage pool is translated into annual spending using typical regimen frequency and average selling price by format. To keep the model grounded, we also build selective bottom-up checks using supplier revenue signals, channel checks in pharmacy and online retail, and sampled price points multiplied by realistic volume ranges, then adjust totals when the two views do not reconcile.

Inputs that materially move the model include age and gender mix, penetration of topical versus oral regimens, average pack size and repurchase cadence, share of online retail in category sales, and pricing differences between mass and premium serums and shampoos. Forecasts lean on multivariate regression so growth is tied to observable drivers such as population aging, disposable income direction, and retail channel mix shifts. Scenario analysis is applied when regulation or new approvals can change adoption timing. When granular country detail is thin, we fill gaps using proxy markets with similar demographics and channel structure, and we only scale after experts confirm the proxy is reasonable.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, so the final number is not driven by one dataset or one assumption. Variance checks are run at regional and category levels, and any sharp jumps are traced back to a specific input such as ASP changes, penetration swings, or channel mix shifts before sign-off.

A second analyst reviews the logic and the math, and follow-up calls are triggered if an assumption changes the market meaningfully or conflicts with multiple interview notes. The model is refreshed annually, with interim updates when material events occur, and a final pre-delivery sweep is done to ensure the latest public data and pricing direction are reflected.

Mordor Intelligence's Hair Loss Treatment Products Market Size Versus Other Published Estimates

Different published market sizes for hair loss treatment products can appear far apart because each source draws the line around a different product set, then applies its own pricing and channel assumptions. The starting year and the way currency is normalized can also shift the headline number, even when the discussion is centered on the same countries.

The biggest gap drivers here are whether vitamins and supplements are counted as core treatment, whether cosmetic shampoos are included without a treatment claim, and whether the estimate mixes consumer products with clinical procedures. Another common difference comes from how price progression is handled, since some sources uplift ASPs broadly while others keep prices flatter and let volume carry more of the change. Refresh timing can also leave new approvals under-reflected.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.14 B (2026) | |

| Global Publisher A | USD 9.50 B (2024) | Uses an earlier base year and a broader consumer basket that explicitly includes vitamins and supplements alongside shampoos and conditioners, which can pull in maintenance and wellness spending beyond treatment-focused products. |

| Industry Report B | USD 12.00 B (2030) | Carries forward the same broad scope into the forecast period and applies a relatively smooth CAGR path, which can mask near-term shifts from channel mix and regulated therapy adoption in specific regions. |

The spread across sources is mainly explained by scope and timing, not by one simple math difference. When the product basket is restricted to treatment-claimed formats and the channel and pricing inputs are rechecked with field feedback, the result stays closer to the measurable demand pool, which is the modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the 2026 value of the hair loss treatment products market?

The market is valued at USD 3.14 billion in 2026 and is set to grow steadily at a 7.19% CAGR.

Which region is growing fastest?

Asia-Pacific posts the highest projected CAGR of 8.78% through 2031 owing to rising disposable income and strong digital engagement.

Which product type currently holds the largest share?

Shampoos and conditioners dominate with 87.65% of 2025 revenue, reflecting widespread daily-use habits.

Why are serums gaining momentum?

Serums use peptide, nanotechnology, and stem-cell actives that deliver targeted penetration and visible results, fueling an 8.02% CAGR forecast.

Page last updated on: