Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 20.12 Billion |

| Market Size (2026) | USD 20.98 Billion |

| Market Size (2031) | USD 25.9 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Hair Care Market Analysis by Mordor Intelligence

United States hair care market size in 2026 is estimated at USD 20.98 billion, growing from 2025 value of USD 20.12 billion with 2031 projections showing USD 25.9 billion, growing at 4.29% CAGR over 2026-2031. This growth highlights a shift in the market, where innovation, specialized therapeutic products, and online sales are becoming more important than simply increasing the volume of products sold. Companies are focusing on creating unique products with personalized formulations, advanced delivery systems, and seamless integration of physical and digital shopping experiences to stand out in the market. The market is also seeing a growing demand for products that offer therapeutic benefits, use transparent and safe ingredients, and follow sustainable practices. As a result, competition in the market is no longer just about securing shelf space in stores. Instead, it is influenced by factors such as strong research and development capabilities, compliance with regulatory standards, and the ability to generate demand through influencers and digital platforms. The competitive landscape shows moderate consolidation, with the top 5 multinational companies holding a significant share of the market. However, smaller niche brands are continuing to disrupt the market by introducing innovative and unique products that cater to specific consumer needs.

Key Report Takeaways

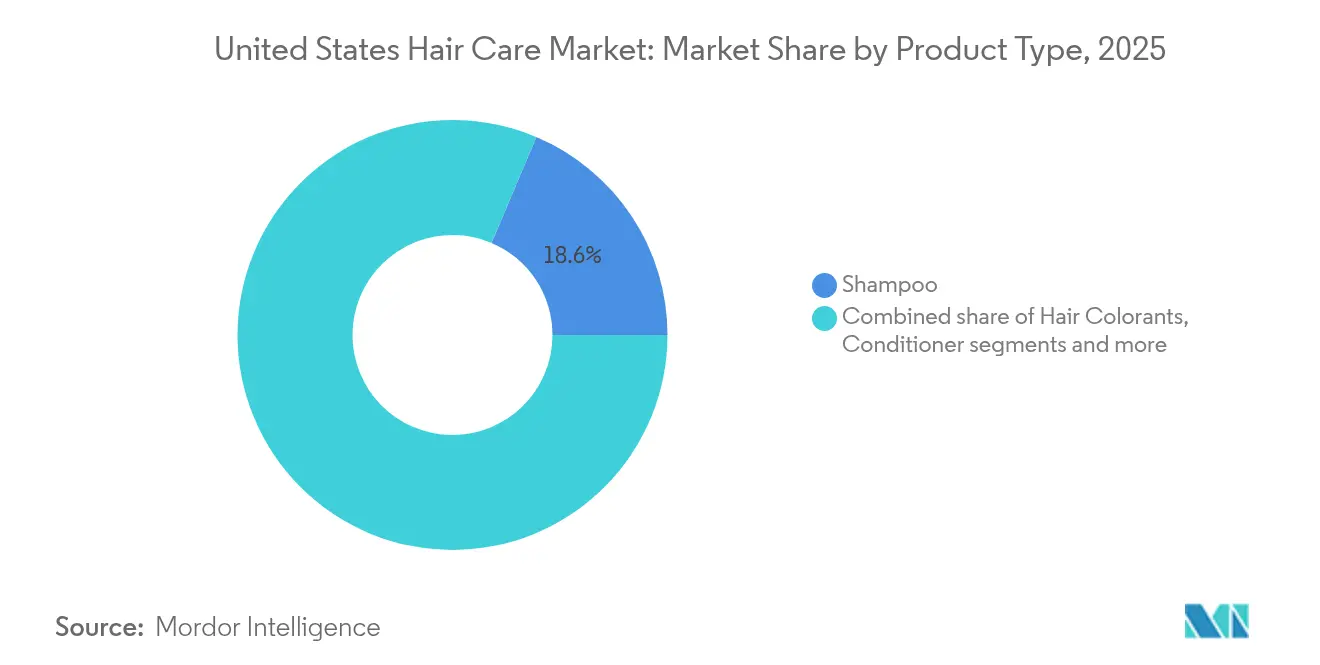

- By product type, shampoo accounted for an 18.62% share of the United States hair care market size in 2025, while hair loss treatment products are forecast to grow at a 6.11% CAGR through 2031.

- By nature, conventional/synthetic lines held an 86.08% share of the United States hair care market size in 2025; natural/organic offerings are advancing at a 6.75% CAGR to 2031.

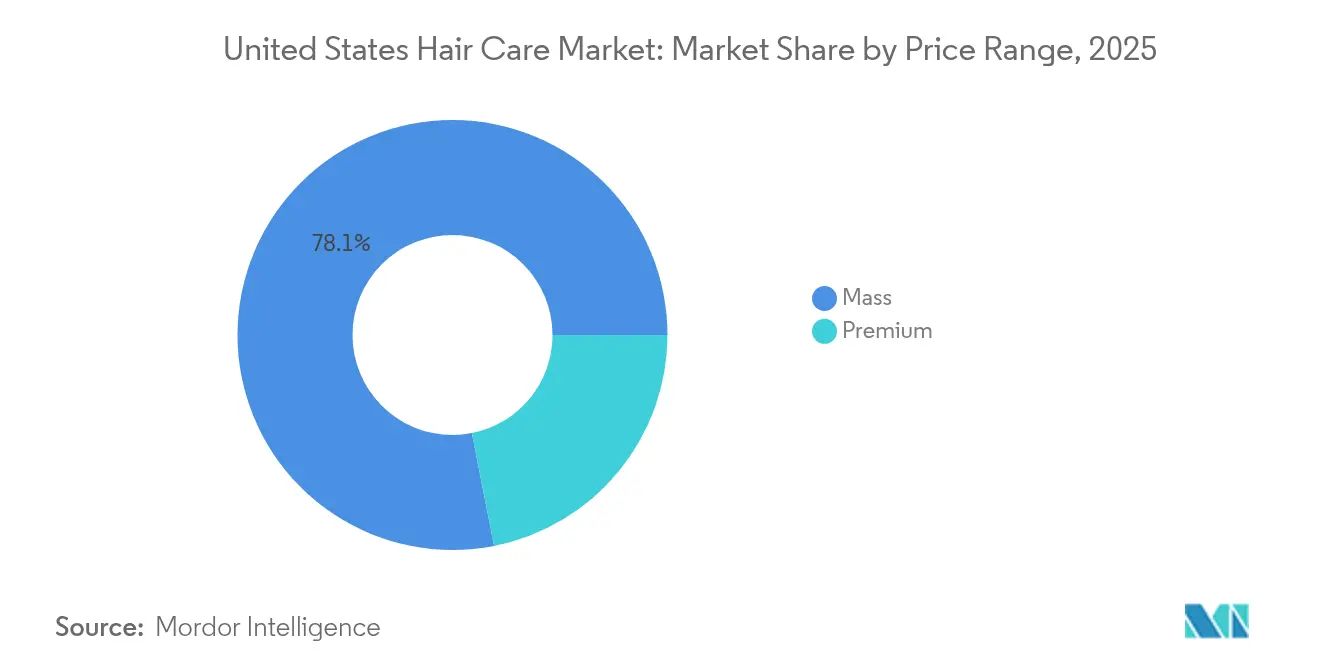

- By price range, mass products dominated with 78.10% of the United States hair care market share in 2025, yet premium items are set to expand at a 5.74% CAGR to 2031.

- By distribution channel, supermarkets/hypermarkets led with 31.05% of the United States hair care market share in 2025, whereas online stores are rising at a 5.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Hair Care Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for products catering to ethnic and textured hair | +0.8% | National, concentrated in diverse metropolitan areas | Medium term (2-4 years) |

| Growing demand for multi-functional and damage repair products | +0.7% | National, stronger in premium retail channels | Short term (≤ 2 years) |

| Advancements in product formulation technologies | +0.6% | National, led by innovation hubs | Long term (≥ 4 years) |

| Increasing awareness of male grooming | +0.5% | National, accelerated in urban markets | Medium term (2-4 years) |

| Impact of social media and beauty influencers | +0.4% | National, strongest among Gen Z and Millennials | Short term (≤ 2 years) |

| Growing emphasis on scalp health | +0.3% | National, premium and specialty channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for multi-functional and damage repair products

Demand for multi-functional and damage-repair hair care solutions is becoming a key factor driving the United States hair care market. Women are increasingly looking for products that simplify their routines by addressing hydration, repair, and scalp care in a single solution. According to the National Council on Aging, as of April 2025, United States women experiencing hair loss are willing to spend up to USD 5,000 on treatments, showcasing the emotional importance of hair care and the readiness to invest in effective products[1]Source: National Council on Aging, "Hair Loss: Causes, Types, and Other Facts", ncoa.org. In response, brands are launching innovative products to meet these needs. For example, on March 25, 2024, Dove launched its scalp + hair therapy collection, a premium 6-product range developed through 65 years of Dove research and dermatological expertise. The collection claims that 89% of women experienced thicker and stronger hair after using the Dove Fullness Restore Scalp Serum, which is part of the line. This product line focuses on enhancing scalp health and improving hair density by incorporating ingredients like niacinamide, peptides, and zinc.

Increasing awareness of male grooming

Awareness of male grooming is growing rapidly, driving significant growth in the United States hair care market. Men are increasingly adopting hair care routines to address issues like hair loss, curl care, and beard maintenance. According to the American Hair Loss Association, around two-thirds of American men experience some level of hair loss by the age of 35, and this figure rises to approximately 85% by the age of 50[2]Source: American Hair Loss Association, "Men’s Hair Loss", americanhairloss.org. This concern has led to a rising demand for specialized products. For example, BosleyMD offers shampoos, conditioners, and scalp therapies made with botanical ingredients as alternatives to minoxidil-based treatments. Similarly, Kérastase homme provides high-end, salon-quality products focused on strengthening hair and improving scalp health. These solutions combine luxury with proven clinical benefits, encouraging more men to invest in hair care. As a result, the availability of such targeted products is expanding men’s involvement in the hair care market and diversifying consumer demand across the United States.

Growing emphasis on scalp health

Scalp health is becoming an essential focus as consumers increasingly recognize its importance in achieving overall hair wellness. Many now treat scalp care as an extension of skincare, incorporating ingredients like probiotics, salicylic acid, and zinc pyrithione, which are known for their benefits in promoting follicular health. According to the National Alopecia Areata Foundation, nearly 7 million people in the United States have experienced alopecia areata or are likely to at some point, with approximately 700,000 currently affected as of 2025. This highlights the growing demand for both medical and cosmetic solutions[3]Source: National Alopecia Areata Foundation, "Alopecia Areata", naaf.org. Traditional practices such as therapeutic oiling, commonly seen among black and South Asian communities, are gaining popularity in mainstream markets. These practices not only address scalp health but also create opportunities for routine-based products, further driving demand in the United States hair-care market.

Impact of social media and beauty influencers

Social media and beauty influencers are significantly influencing the United States hair-care market, changing how consumers discover, evaluate, and purchase products. With 239 million social media users in the United States as of 2025, according to World Population Review, digital platforms have become a powerful tool for shaping consumer behavior[4]Source: World Population Review, "Social Media Users by Country 2025", worldpopulationreview.com. Tutorials, product reviews, and viral trends on platforms like Instagram, TikTok, and YouTube encourage consumers to try new products and make quicker purchasing decisions. Consumers now expect greater transparency from brands, including clear ingredient lists and ethical practices. Celebrity-led product launches, such as Blake Lively’s blake brown, demonstrate how personal branding can turn online followers into loyal customers. For both established companies and emerging brands, collaborating with influencers and leveraging digital storytelling are now essential strategies to build brand awareness, foster trust, and compete effectively in the dynamic United States hair-care market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growth of counterfeit products | -0.4% | National, concentrated in e-commerce channels | Short term (≤ 2 years) |

| Growing preference for traditional at-home hair care practices | -0.3% | National, stronger in diverse communities | Medium term (2-4 years) |

| Challenges in meeting regulatory standards for imported products | -0.2% | National, affecting international brands | Short term (≤ 2 years) |

| Concerns over health and safety of chemical-based items | -0.2% | National, premium and natural segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing preference for traditional at-home hair care practices

The increasing popularity of traditional at-home hair care routines is slowing the growth of the United States hair-care market, as more consumers opt for natural, time-tested methods over commercial products. According to NSF Org, 74% of Americans prioritize organic ingredients in personal care items, highlighting a strong preference for do-it-yourself (DIY) solutions or simpler, natural formulations[5]Source: NSF Org, "74% of Consumers Consider Organic Ingredients Important in Personal Care Products," nsf.org. Home remedies like coconut oil treatments, shea butter applications, and herbal rinses are gaining traction due to their affordability, accessibility, and perceived effectiveness, especially during periods of economic uncertainty. This shift is challenging commercial brands to adapt by creating products with transparent ingredient lists, straightforward formulations, and clear advantages over homemade alternatives. At the same time, brands must continue to innovate and differentiate their offerings to remain competitive in this evolving market.

Concerns over health and safety of chemical-based items

Concerns about the safety of chemical-based hair-care products are slowing the growth as consumers are becoming more cautious about the ingredients used in these products. Chemicals like parabens, sulfates, phthalates, and formaldehyde-releasing preservatives have faced increasing scrutiny from both regulators and the public. The Food and Drug Administration, under the Modernization of Cosmetics Regulation Act (MoCRA), is actively monitoring reports of adverse effects linked to such ingredients. Growing awareness of potential risks, such as scalp irritation, hair thinning, and other long-term health issues, has led to a surge in demand for “clean,” organic, and dermatologist-approved alternatives. As a result, brands are under pressure to reformulate their products or introduce new lines that are free from harmful chemicals. However, meeting these demands involves additional costs for compliance, testing, and certification, which can extend development timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Solutions Drive Growth

Shampoo remains a key product in the United States hair-care market, accounting for a 18.62% portion of revenue in 2025. As an everyday essential, it enjoys consistent demand across households, though its growth is limited due to widespread market penetration. Conditioners and styling products also play an important role, as they are integral to daily hair maintenance and enhancing appearance. These categories collectively contribute to the market's stability by addressing routine consumer needs and preferences, ensuring steady performance over time.

On the other hand, hair-loss treatment products are emerging as the fastest-growing segment, with a projected growth rate of 6.11% CAGR through 2031. Factors such as stress, aging, and hormonal changes are driving an increase in hair-thinning issues, leading to higher demand for specialized solutions. Innovations in scalp treatments, DHT-blocking products, and premium restorative formulas are further boosting this segment. This trend reflects a shift in consumer focus from basic maintenance to targeted, performance-driven products, positioning hair-loss treatments as a key driver of growth in the market.

By Nature: Clean Beauty Momentum Accelerates

Conventional/synthetic hair-care products continue to dominate the United States market in 2025, making up 86.08% of sales. These products remain popular due to their affordability, consistent performance, and widespread availability across retail channels like supermarkets, drugstores, and online platforms. Consumers often stick to these options because of their familiarity, trusted brands, and appealing features such as pleasant fragrances and effective results. This segment’s accessibility and affordability ensure it remains a staple for a broad range of customers, maintaining its stronghold in the market.

On the other hand, natural and organic hair-care products are rapidly gaining traction, with a projected growth rate of 6.75% CAGR through 2031, outpacing the overall market. Increasing consumer awareness about the benefits of clean and sustainable products is driving demand, especially among younger and environmentally conscious buyers. These products emphasize plant-based ingredients, eco-friendly packaging, and safety, which resonate with consumers seeking healthier and more ethical choices. As a result, brands focusing on transparency and sustainability are experiencing higher customer loyalty, signaling a shift in consumer preferences toward wellness-oriented and environmentally responsible hair-care solutions.

By Price Range: Premium Segment Captures Value

Mass-market hair care products continued to dominate the market in 2025, contributing 78.10% share of revenue. These products are widely available in grocery stores, drugstores, and other retail outlets, making them easily accessible to a broad range of consumers. Their affordability and family-sized packaging make them a practical choice for households looking for cost-effective solutions. Well-known brands and consistent product quality have helped maintain customer loyalty, ensuring these products remain a staple in the market. This segment’s strong presence highlights its importance in meeting everyday hair care needs for the majority of consumers.

On the other hand, premium hair care products are emerging as a key growth area, with sales expected to grow at a 5.74% CAGR through 2031. These products attract consumers willing to spend more for advanced formulations, salon-quality results, and scientifically proven benefits. Premium offerings often include features like multi-functional benefits, high-performance ingredients, and luxurious experiences, appealing to urban and digitally savvy shoppers. The rise of influencer marketing and compelling brand stories has further boosted the appeal of premium products, driving a shift in consumer preferences. This trend indicates a growing demand for high-value, performance-driven hair care solutions in the market.

By Distribution Channel: Digital Transformation Reshapes Retail

Supermarkets/hypermarkets remained the primary sales channels for hair-care products in 2025 with 31.05% share in the total revenue, driven by their convenience and wide product availability. These stores attract a large number of shoppers who prefer purchasing hair-care items along with their regular groceries. Promotions, discounts, and prominent in-store displays further encourage impulse purchases, helping these outlets maintain their strong position in the market. Their ability to offer a variety of products at competitive prices makes them a preferred choice for many consumers.

Meanwhile, online retail is emerging as the fastest-growing sales channel, with sales expected to grow at a 5.83% CAGR through 2031. E-commerce platforms provide convenience, home delivery, and access to a wider range of products, including premium and niche brands that may not be available in physical stores. Subscription models and personalized recommendations also enhance the online shopping experience. Specialty beauty stores are gaining traction by offering hybrid options like buy-online-pick-up-in-store and real-time inventory updates. These trends highlight the increasing importance of digital and omnichannel strategies in shaping the future of hair-care product distribution in the United States.

Geography Analysis

The United States hair care market shows diverse demand patterns across different regions. Coastal metropolitan areas, with higher incomes, lead in the adoption of premium hair care products. In contrast, the Sun Belt states, experiencing population growth and younger demographics, are seeing rapid growth in retail sales. These regions are driving demand for products like textured-hair solutions and UV-protection stylers. Cities with significant ethnic populations, such as Atlanta, Houston, and Los Angeles, are boosting the market for curl-focused moisturizers and edge-taming gels. Northern states, with colder climates, see higher demand for anti-static hydration products during winter, while humid southern regions favor anti-frizz and anti-humidity sprays.

Urban areas are also leading in e-commerce adoption, where same-day delivery services have become common. This trend allows brands to launch directly online without needing a physical retail presence. On the other hand, rural consumers still rely heavily on stores like Walmart and regional grocery chains, where they prefer value packs and well-known heritage brands. Retailers are adapting their strategies to cater to these differences. Urban stores often highlight premium mini-sized products and innovative displays, while suburban and rural outlets focus on bulk family-sized packs and promotional bundles to meet local preferences.

Regulations in the United States remain consistent at the federal level under Food and Drug Administration oversight, but some states, like California, have stricter rules, such as the safe cosmetics program. These state-level regulations are pushing brands to reformulate products to comply with stricter chemical guidelines and avoid creating fragmented product lines. As a result, companies must carefully plan their supply chains to address varying regional needs while adhering to regulatory requirements. The intersection of climate-driven demands, demographic trends, and regulatory changes is shaping the strategies of hair care brands across the country.

Regulatory Landscape

United States hair-care products are regulated as cosmetics under the US Food and Drug Administration (FDA) framework, and the Modernization of Cosmetics Regulation Act of 2022 (MoCRA) has increased compliance obligations for brands and manufacturers selling shampoos, conditioners, styling products, and hair colorants. Under MoCRA and related provisions (including 21 USC 364d), responsible persons must maintain records supporting adequate safety substantiation for cosmetic products, and serious adverse events must be reported to the FDA within 15 business days, reinforcing routine documentation, complaint handling, and product stewardship across mass and premium portfolios.

MoCRA implementation also formalizes transparency at the facility and product level, including facility registration with biennial renewals and cosmetic product listing, while the FDA continues to clarify expectations through guidance and oversight activity. A near-term operational anchor is the first biennial facility registration renewal cycle due July 1, 2026, which increases the importance of compliant manufacturing footprints and traceable supply chains for both domestic production and imported finished goods.

Competitive Landscape

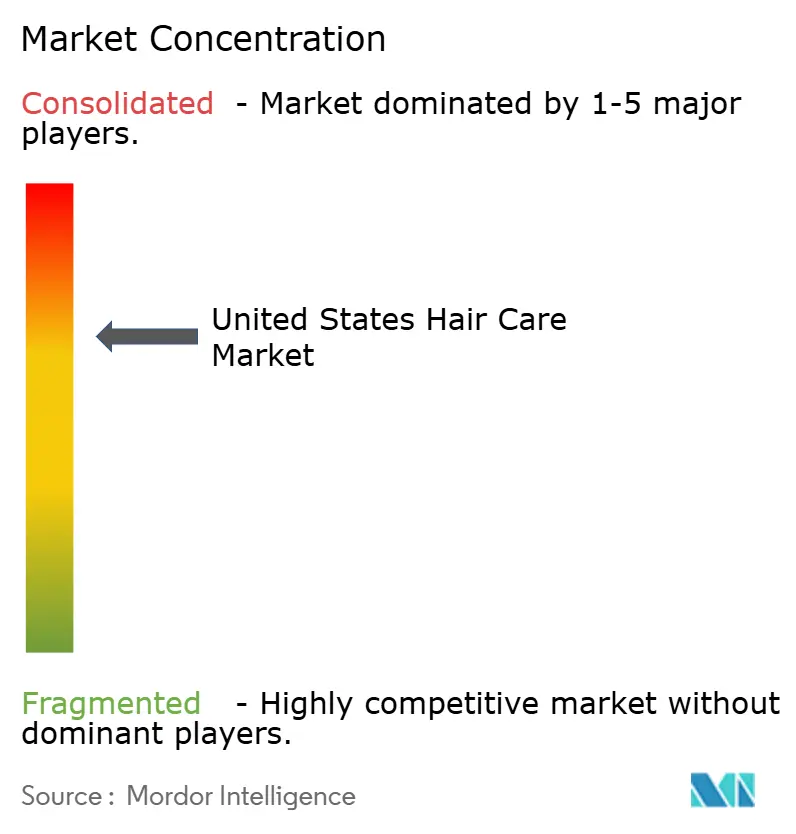

The competitive landscape in the United States hair care market is moderately concentrated, with the top five multinational companies controlling approximately 70%-80% of the market share. These large players benefit from economies of scale in manufacturing and advertising, but smaller, niche brands are disrupting the market by focusing on authenticity, innovation, and speed-to-market. For example, L’Oréal’s collaboration with Zuvi on the AirLight Pro device highlights how partnerships can create unique, patent-protected products. Major companies like Procter & Gamble, Unilever, and Henkel are also expanding their portfolios by acquiring high-growth niche brands such as Mielle Organics, Nutrafol, and eSalon, allowing them to tap into emerging segments.

Digital strategies are becoming increasingly important for companies to stay competitive. Brands are leveraging tools like AI-powered chatbots to provide personalized hair care recommendations and augmented reality features to enhance customer engagement. Social media influencers and community-driven marketing are also key components of these strategies. Additionally, regulatory compliance is becoming a critical factor as the Modernization of Cosmetics Regulation Act (MoCRA) is implemented. Larger companies with established global quality systems are better equipped to handle these changes, while smaller brands may face challenges due to rising compliance costs. Sustainability initiatives, such as using recycled materials, water-efficient formulas, and energy-saving manufacturing processes, are also gaining traction, aligning with consumer preferences and corporate Environmental, Social, and Governance (ESG) goals.

Smaller, innovative brands are standing out by focusing on science-backed formulations, cultural relevance, and personalized solutions. Products like K18’s biotech peptide, OLAPLEX’s patented molecule for hair repair, and Nutrafol’s botanical-based formulas demonstrate how intellectual property can justify premium pricing. Private equity investments are fueling research and development as well as omnichannel expansion for these brands. However, many of these smaller companies eventually become acquisition targets for larger multinationals seeking to enhance their innovation pipelines. As a result, mergers and acquisitions remain a significant trend in the United States hair care market, shaping its competitive dynamics.

United States Hair Care Industry Leaders

-

L'Oreal SA

-

Henkel AG & Co. KGaA

-

Procter & Gamble Co.

-

Kao Corporation

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

MoCRA-driven operating requirements are changing how value is created in the United States hair-care market, creating opportunities for brands that can document safety substantiation, run compliant adverse-event processes, and meet retailer expectations for traceability. As the FDA expands its ability to access records and oversee cosmetics, investments in quality systems, supplier qualification, and product information management can become commercial differentiators, particularly for fast-growing premium and online-led brands that rely on rapid innovation cycles.

Formulation and packaging innovation is also creating opportunity areas, especially in scalp-health, performance-led products and sustainability-aligned inputs that can support clean-label and environmental claims. Industry activity during 2026 points to that direction, including US-facing formulation venues showcasing bio-based and upcycled ingredient solutions for hair care. In parallel, L'Oréal has highlighted dedicated refill manufacturing capability at its Burgos facility for haircare as part of scaling refill options. Together, these developments support product roadmaps that combine efficacy cues (skinification, scalp care) with lower-impact materials and refill formats, helping brands differentiate beyond basic cleansing and conditioning.

Recent Industry Developments

- July 2026: Henkel completed its acquisition of OLAPLEX, integrating the premium hair-care brand into Henkel Consumer Brands. The acquisition increases Henkel's presence in prestige hair repair and professional-influenced routines, strengthening its position across premium channels in the United States.

- June 2025: L'Oréal finalized an agreement to acquire Color Wow, a professional hair-care brand, to strengthen L'Oréal's Professional Products Division. The transaction broadened L'Oréal's salon-adjacent portfolio and added a scaled platform in styling and frizz-control solutions popular with US consumers.

- November 2024: Vichy expanded its Dercos line into the United States with a three-step scalp care system spanning anti-dandruff cleansing, conditioning, and a salicylic acid serum. The launch reinforced scalp care as a distinct, regimen-based subcategory that bridges cosmetic and therapeutic positioning at retail.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers spending in the United States on hair care products sold through retail and professional-facing channels, counted on a value basis in USD. It includes everyday cleansing, conditioning, styling, coloring, and treatment items purchased for hair and scalp needs.

Scope exclusions: We exclude hair appliances, salon services, and prescription-only therapies, and we also exclude raw ingredients sold for manufacturing.

Segmentation Overview

-

By Product Type

- Shampoo

- Conditioner

- Hair Styling products

- Hair Colorants

- Hair Loss Treatment Products

- Other product types

-

By Nature

- Natural/Organic

- Conventional/Synthetic

-

By Price Range

- Mass

- Premium

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Drugstores/Pharmacies

- Specialty and Beauty Stores

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the demand pool and keep assumptions tied to public signals that move with hair care consumption. We reviewed sources such as the US Census Bureau (retail trade), the Bureau of Labor Statistics (CPI and personal consumption inflation signals), the FDA (cosmetics guidance and recalls), and USITC trade statistics for select hair preparations where applicable.

To connect market movement with category-level behavior, we also used company annual reports and investor presentations, major retailer category updates, and trade association publications linked to personal care. In a few cases, paid subscriptions for company financials and patent intelligence were used to confirm revenue mix hints and innovation intensity, which then informed how quickly price and mix were allowed to shift. These examples are not exhaustive, and we checked other public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were conducted with manufacturers, distributors, large retailers, and industry specialists tracking hair care category performance in the United States. Discussions focused on what is driving volume, what is driving price and mix, and how channel shifts, especially online versus store-based retail, are changing the realized value captured in the market model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 58% | Functional/Unit leaders: 40% | |

| Smaller Players: 14% | Managers: 46% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where US consumption value is reconstructed using category-level spending signals, then split using share indicators across the main hair care product baskets. After setting that core total, we corroborate it with selective bottom-up approximations, including sampled brand revenue exposure to hair care, channel checks on online assortment and pricing, and volume times average selling price logic on a few high-velocity subcategories.

Key inputs used in the model include category price inflation from CPI-type series, premiumization and pack-size shifts, e-commerce share changes, salon versus at-home usage patterns, and product mix movement across cleansing, conditioning, styling, and color. Where bottom-up views are incomplete, for example for private-label or privately held brands with limited disclosure, gaps are handled using proxy share bands validated in interviews, followed by sensitivity checks so no single assumption dominates the final total.

Forecasting uses scenario analysis supported by short-run trend smoothing. Price, mix, and channel shares are projected separately and then recombined into total value. Assumptions are adjusted only after they are tested against what interviewees expect for promotions, innovation cycles, and consumer trade-down or trade-up behavior over the forecast period.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including inflation and consumption indicators, retailer and company commentary, and the implied direction of per-capita spend. If a category or channel result looks unusual, we re-check the inputs, rerun the math with alternative assumptions, and re-contact select respondents to confirm whether the movement is real or a modeling artifact.

Before sign-off, the work is reviewed in steps so calculations, unit consistency, and year-to-year movements are checked by another analyst. The report is refreshed annually, and interim updates are made when material events occur, including major regulatory actions or sharp pricing changes. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's United States Hair Care Market Market Size Versus Other Published Estimates

Published market values for US hair care often differ, even when the product descriptions look similar, because counting rules and sales channels included can change the total by a wide margin. Differences also come from the base year selection, how inflation is carried forward, and whether the estimate is built from retail scan-style totals or from a broader consumption value view.

The table points to a major spread that is mainly explained by channel and scope choices, where some estimates focus on mass retail only and others blend in a wider set of outlets. In Mordor Intelligence's model, the value includes shampoo, conditioner, styling agents, colorants, hair oil, and other hair care types across channels such as supermarkets and hypermarkets, convenience stores, specialty stores, online retail, and other channels, which can lift the total versus narrow tracked-channel definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 20.12 B (2025) | |

| Trade Publication A | USD 11.00 B (2024) | Uses a tracked-channel retail view (MULO) centered on shampoo, conditioner, and hairstyling, which typically leaves out parts of specialty, professional, and other outlet sales, and it also uses a different base year. |

| Global Consultancy B | USD 4.61 B (2025) | Treats the market as a narrower product and revenue pool and mixes total and incremental growth framing in its public summary, which can understate the full category value when compared on a like-for-like year. |

Looking across the three values, the practical takeaway is that the year label alone is not sufficient, and inclusion rules matter more. By keeping scope tied to clear product buckets and a stated channel set, the estimate stays traceable to repeatable inputs, which helps decision-makers compare trends without mixing mismatched definitions.

Key Questions Answered in the Report

How fast will premium hair products grow in the United States hair care market through 2031?

Premium lines are forecast to post a 5.74% CAGR, well ahead of mass offerings, as consumers seek clinically proven benefits and personalized solutions.

Which product segment is expanding most rapidly?

Hair loss treatment products are projected to rise at a 6.11% CAGR, driven by aging demographics and stress-related hair issues.

What is driving the shift toward natural and organic formulas?

Ingredient transparency, perceived safety, and sustainability concerns are pushing natural/organic ranges to grow at 6.75% CAGR, outpacing synthetic lines.

How big is the online channel within United States hair care?

Online stores held 24.88% of 2025 sales and are growing at a 5.83% CAGR, fueled by convenience and influencer-led discovery.

Page last updated on: