Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Hair Care Market Analysis by Mordor Intelligence

The Canadian hair care market size was valued at USD 1.59 billion in 2025 and estimated to grow from USD 1.66 billion in 2026 to reach USD 2.05 billion by 2031, at a CAGR of 4.32% during the forecast period (2026-2031). This growth is primarily attributed to increasing consumer awareness regarding personal grooming and hygiene, coupled with the rising demand for innovative, sustainable, and natural hair care products. The market includes a diverse range of offerings such as shampoos, conditioners, hair oils, serums, hair masks, and styling products, catering to the varying needs of consumers across different demographics and hair types. Also, the growing influence of social media platforms has played a pivotal role in shaping consumer preferences, with trends such as DIY hair care routines and the use of organic ingredients gaining traction. Additionally, the expansion of e-commerce channels has enhanced the accessibility of hair care products, enabling consumers to explore a broader range of options and make informed purchasing decisions. Key players in the market are focusing on product innovation, introducing advanced formulations that address specific concerns such as hair fall, dandruff, and scalp health.

Key Report Takeaways

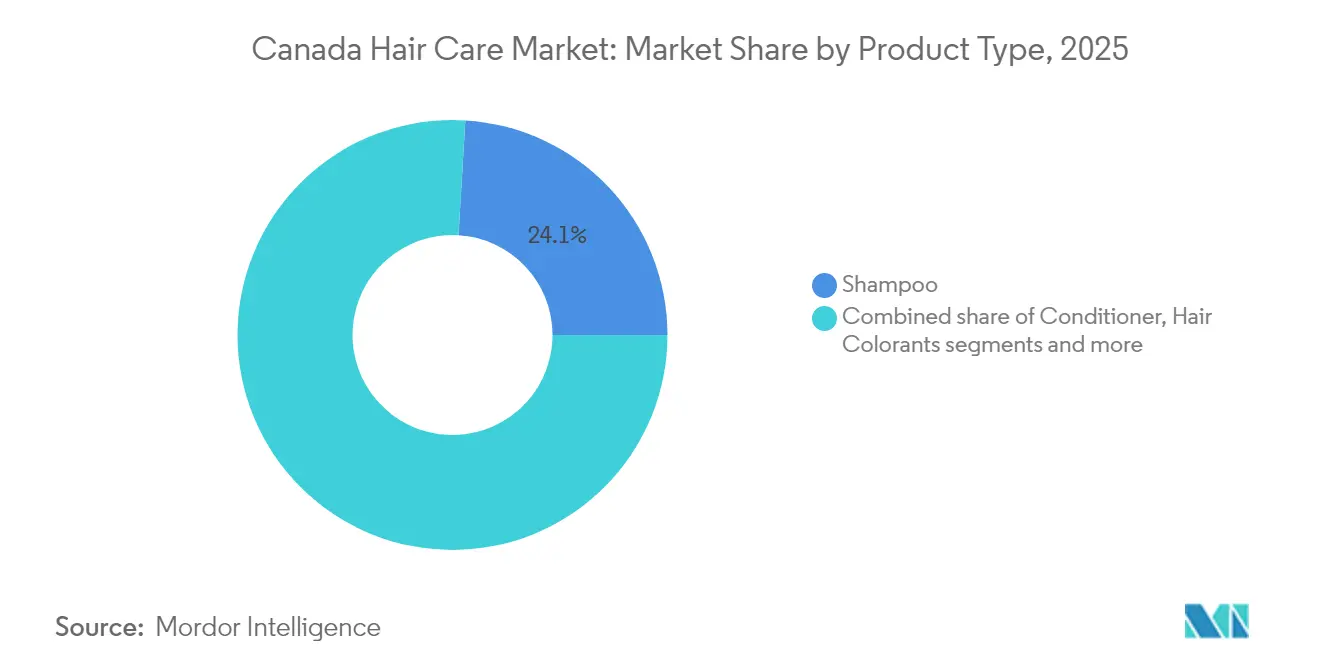

- By product type, shampoo retained 24.05% revenue share of the Canadian hair care market in 2025, while hair styling products are projected to expand at a 5.08% CAGR to 2031.

- By category, mass products held 74.90% of the Canadian hair care market size in 2025; premium products are forecast to advance at a 5.55% CAGR through 2031.

- By ingredient type, conventional/synthetic formulas captured 65.10% of the Canadian hair care market size in 2025, whereas natural and organic products are growing at a 6.12% CAGR.

- By distribution channel, specialty stores led with 33.85% revenue share in 2025, but online retail stores are on track for a 6.92% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multicultural demographic fueling textured-hair and protective-style products | +0.8% | National, concentrated in Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Aging population increasing demand for hair health products | +0.6% | National, highest in Atlantic provinces | Long term (≥ 4 years) |

| Growing demand for natural and organic hair care products | +0.7% | National, urban-centric adoption | Short term (≤ 2 years) |

| Growing consumer awareness of personal grooming | +0.5% | Urban centers, Greater Toronto Area, Lower Mainland | Medium term (2-4 years) |

| Surge in demand for clean label ingredient products | +0.4% | National, premium market segments | Short term (≤ 2 years) |

| Technological innovations in product formulations | +0.3% | National, early adoption in major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multicultural demographic fueling textured-hair and protective-style products

The multicultural demographic in Canada is significantly driving the demand for textured-hair and protective-style products. The diverse population has led to an increased need for specialized hair care products catering to various hair textures and protective styling needs. The growing awareness and availability of such products are further fueling this demand, making it a key driver in the market. Additionally, the increasing representation of diverse hair types in media and advertising has encouraged consumers to embrace their natural hair textures, further boosting the demand for these products. Government initiatives promoting multiculturalism and inclusivity have also played a role in supporting the growth of this segment. For instance, the Canadian Multiculturalism Act emphasizes the importance of cultural diversity, indirectly influencing consumer preferences and market trends. As a result, manufacturers are focusing on innovation and product development to meet the unique needs of this diverse consumer base, contributing to the overall growth of the market.

Aging population increasing demand for hair health products

The aging population in Canada is driving significant growth in the demand for hair health products. Statistics Canada reported that approximately 7.6 million Canadians were aged 65 and older as of 2023, representing nearly one-fifth (18.9%) of the total population [1]Source: Statistique Canada, “The older people are all right”, statcan.gc.ca. This demographic increasingly seeks solutions for age-related hair concerns, including thinning, graying, and hair loss, which has fueled the demand for specialized hair care products. Companies are actively introducing a variety of offerings, such as shampoos, conditioners, serums, and treatments, specifically designed to address these issues. Additionally, older consumers are prioritizing premium and natural hair care solutions, demonstrating a willingness to invest in products that enhance hair health and address aesthetic needs. This trend is expected to significantly influence the Canadian Hair Care Market during the forecast period as the aging population continues to expand and emphasize personal care.

Growing demand for natural and organic hair care products

The growing demand for natural and organic hair care products is a significant driver of the Canadian hair care market. Consumers are increasingly seeking products free from harmful chemicals, such as parabens and sulfates, and are opting for formulations that include natural ingredients like plant extracts, essential oils, and organic compounds. This shift is driven by rising awareness of the potential health and environmental benefits associated with natural and organic products. Additionally, the trend aligns with the broader consumer preference for sustainable and eco-friendly products, further boosting the demand in this segment. Manufacturers are responding by expanding their product portfolios to include certified organic and natural hair care solutions, catering to the evolving preferences of Canadian consumers. The increasing availability of such products across various distribution channels, including online platforms, specialty stores, and supermarkets, is further fueling market growth.

Growing consumer awareness of personal grooming

Consumers in Canada are increasingly prioritizing personal grooming, which is driving the growth of the hair care market. Rising awareness about maintaining hair health, coupled with the influence of social media and beauty trends, has led to a surge in demand for hair care products. According to Statistique Canada, the average spending on personal care, including hair care, reached CAD 1,860 in 2023, marking a 30.1% increase from 2021 [2]Source: Statistique Canada, “Survey of Household Spending, 2023”, statcan.gc.ca. This growth was largely fueled by higher spending on hair care products. Additionally, the growing availability of innovative and customized hair care solutions is further encouraging consumers to invest in grooming products. This trend is particularly prominent among younger demographics, who are more inclined toward experimenting with new products and styles to enhance their appearance. The increasing disposable income and the willingness to spend on premium and organic hair care products are also contributing to the market's expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.3% | National, heightened in urban areas | Short term (≤ 2 years) |

| Proliferation of counterfeit products | -0.2% | National, concentrated in online channels | Medium term (2-4 years) |

| Potential side effects or allergies from certain hair care products | -0.2% | National, regulatory focus areas | Short term (≤ 2 years) |

| High cost of hair styling products and salon services | -0.4% | National, economic sensitivity varies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns over chemical ingredients

Increasing awareness about the potential health risks associated with chemical ingredients in hair care products is acting as a major market restraint in the market. Consumers are becoming more cautious about the long-term effects of synthetic chemicals, such as sulfates, parabens, and silicones, which are commonly found in shampoos, conditioners, and styling products. These ingredients are often linked to issues like scalp irritation, hair damage, and even more severe health concerns when used over extended periods. For instance, sulfates, while effective in creating lather, can strip the scalp of natural oils, leading to dryness and irritation. Similarly, parabens, widely used as preservatives, have been associated with potential hormonal disruptions, raising significant concerns among health-conscious consumers. This growing awareness has led to a shift in consumer preferences, with many opting for natural, organic, and chemical-free alternatives. Products labeled as "paraben-free," "sulfate-free," or "natural" are gaining traction, as consumers increasingly scrutinize ingredient lists before making purchasing decisions.

Proliferation of counterfeit products

The proliferation of counterfeit products poses a significant restraint on the Canadian hair care market. Counterfeit goods, often sold at lower prices, undermine the sales of genuine products, impacting the revenue of established brands. These fake products not only erode brand reputation but also raise concerns about consumer safety, as they may contain harmful or unregulated ingredients. The availability of counterfeit hair care items through online platforms and unauthorized retail channels further exacerbates the issue. This challenge compels manufacturers and stakeholders to invest in anti-counterfeiting measures, such as advanced packaging technologies and authentication systems, to protect their products and maintain consumer trust. However, these efforts increase operational costs, adding another layer of complexity to the market dynamics. The widespread presence of counterfeit products also creates a trust deficit among consumers, as they may find it increasingly difficult to differentiate between authentic and fake products. This lack of confidence can lead to reduced brand loyalty and a shift in purchasing behavior, with consumers opting for alternative or lower-cost options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Specialized Solutions Reshape Category Dynamics

In 2025, shampoo holds a dominant 24.05% share of the Canadian hair care market, underscoring its pivotal role in maintaining hair health and hygiene. The product's widespread adoption is attributed to its essential nature in daily grooming routines and the continuous innovations catering to specific hair types and concerns, such as dandruff, dryness, and hair fall. Additionally, the growing demand for natural and organic shampoos has further propelled its market share, as consumers increasingly prioritize products with clean and sustainable ingredients. The segment's strong performance reflects its ability to adapt to evolving consumer preferences and its indispensable position in the hair care regimen.

However, from 2026 to 2031, hair styling products are expected to outpace other segments, registering a robust CAGR of 5.08%. This growth is fueled by the rising popularity of hairstyling among Canadian consumers, who are becoming more experimental with their looks. Social media platforms play a significant role in shaping styling trends, with influencers and brands driving demand for innovative products like texturizing sprays, gels, and heat protectants. Furthermore, the increasing availability of professional-grade styling products for at-home use has expanded the consumer base, contributing to the segment's rapid growth. As a result, hair styling products are emerging as a key growth driver within the Canadian hair care market.

By Category: Premium Segment Outpaces Market Growth

In 2025, mass products dominate the Canadian hair care market, holding a substantial 74.90% share. This dominance can be attributed to their affordability, widespread availability, and appeal to a broad consumer base. Mass products cater to diverse hair care needs, offering a variety of shampoos, conditioners, and styling products at competitive prices. The segment benefits from strong distribution networks, including supermarkets, hypermarkets, and online platforms, ensuring easy accessibility for consumers across the country. Additionally, frequent promotional activities and discounts further bolster the demand for mass hair care products in Canada.

Yet, from 2026 to 2031, the premium segment is set to experience vigorous growth, projected at a CAGR of 5.55%. This growth is driven by increasing consumer preference for high-quality, specialized hair care solutions and a growing focus on personal grooming. Premium products often feature advanced formulations, natural ingredients, and targeted benefits, appealing to consumers willing to invest in superior hair care. The rise of e-commerce platforms and direct-to-consumer channels has also facilitated the accessibility of premium brands, contributing to their expanding market share. Furthermore, the influence of social media and endorsements by beauty influencers are playing a significant role in driving awareness and demand for premium hair care products in Canada.

By Distribution Channel: Specialty Stores Dominates, Online Retail Stores Accelerates

In 2025, specialty stores command a dominant 33.85% share of the Canadian hair care market, owing to their tailored product offerings and personalized customer service. These stores cater to niche consumer demands by providing a curated selection of high-quality products, often including premium and professional-grade options. Their ability to offer expert advice and foster customer loyalty further strengthens their position in the market. Additionally, the in-store experience provided by specialty stores, such as product demonstrations and consultations, enhances customer engagement and satisfaction. The growing preference for exclusive and specialized products among consumers continues to drive the prominence of this segment.

Meanwhile, online retail stores are witnessing the fastest expansion, boasting a 6.92% CAGR from 2026 to 2031. The convenience of online shopping, coupled with a wide range of product availability and competitive pricing, drives this growth. Additionally, advancements in e-commerce platforms and targeted marketing strategies are enabling online retailers to capture a growing share of the Canadian hair care market. The increasing adoption of mobile shopping and digital payment methods further accelerates the growth of this segment. Furthermore, the integration of artificial intelligence and personalized recommendations in online platforms is enhancing the shopping experience for consumers.

By Ingredient Type: Natural Formulations Gain Market Share

In 2025, conventional/synthetic ingredients dominate the Canadian hair care market, holding a significant 65.10% share. These formulations are widely preferred due to their cost-effectiveness, availability, and proven efficacy in addressing various hair care needs, such as cleansing, conditioning, and styling. The extensive use of synthetic ingredients in mass-market products and their ability to deliver consistent results have contributed to their strong market presence. Additionally, the established supply chain and manufacturing processes for synthetic ingredients further bolster their dominance in the market. However, growing concerns over the long-term effects of synthetic chemicals on hair and scalp health may pose challenges to this segment in the future.

Conversely, natural and organic formulations are gaining traction in the Canadian hair care market, driven by increasing consumer awareness and demand for sustainable and chemical-free products. From 2026 to 2031, this segment is projected to grow at a robust CAGR of 6.12%, outpacing the conventional segment. Consumers are increasingly seeking products with plant-based, eco-friendly ingredients that align with their health and environmental values. This shift is further supported by advancements in natural ingredient processing and the introduction of innovative formulations that cater to diverse hair care needs while maintaining a focus on sustainability. Additionally, government regulations promoting the use of natural ingredients and eco-friendly practices are expected to further drive growth in this segment.

Geography Analysis

Canada's diverse geography shapes its hair care market, influencing both consumer preferences and product demand. Urban centers like Toronto, Montreal, and Vancouver, known for their multicultural populations, lead the charge in adopting innovative hair care solutions. These cities showcase a rising demand for products tailored to various hair textures and specific concerns. Their dynamic retail infrastructure not only introduces new products but also ensures brands meet the evolving needs of Canada's diverse demographic segments. Consequently, these urban hubs are pivotal in steering Canada's overall market dynamics. According to ITC Trade Map, the import value of hair care preparation solutions in Canada increased from USD 588,325 thousand in 2021 to USD 749,712 thousand in 2024 , reflecting the growing demand for such products.

Canada's multicultural population significantly influences its hair care market. Urban centers, rich in ethnic diversity, push brands to craft specialized products catering to unique hair care needs. For example, those with curly or textured hair often seek hydration and curl definition, while straight or fine hair consumers lean towards volumizing or strengthening solutions. This nuanced demand has driven brands to innovate and broaden their portfolios, championing inclusivity and effectiveness. Moreover, the multicultural influence extends beyond product formulations; brands are increasingly prioritizing representation and diversity in their marketing strategies to better connect with their audience.

Moreover, Canada's vast geography and varying climate conditions further shape consumer preferences in the hair care market. Coastal regions, characterized by high humidity, drive demand for anti-frizz and humidity-resistant products, while the drier prairies see a preference for moisturizing and hydrating formulations. Seasonal changes also play a role, with consumers adjusting their hair care routines to address weather-related challenges such as dryness in winter or increased oiliness in summer. These geographical and climatic factors compel brands to consider regional variations when developing and distributing their products, ensuring they meet the specific needs of consumers across the country. This alignment with local preferences underscores the importance of geography in shaping the Canadian hair care market.

Regulatory Landscape

Hair care products sold as cosmetics in Canada are regulated by Health Canada under the Food and Drugs Act and the Cosmetic Regulations (CRC, c. 869). Companies must comply with ingredient and labeling rules (including INCI ingredient naming), and manufacturers and importers are required to submit a Cosmetic Notification Form (CNF) to Health Canada within 10 days of first sale. Non-compliant products can face enforcement actions, including stopping sale, especially when ingredients conflict with the Cosmetic Ingredient Hotlist (prohibited or restricted substances). Cosmetics are explicitly excluded from the Canada Consumer Product Safety Act, keeping primary oversight within Health Canada’s cosmetics framework.

Regulatory requirements have tightened around transparency and ingredient disclosure. Health Canada’s public consultation on proposed updates to the Cosmetic Ingredient Hotlist (initiated in November 2025) closed on February 17, 2026, which reinforces the need for ongoing reformulation and compliance monitoring as Hotlist entries evolve. Fragrance allergen disclosure provisions tied to amended regulations (SOR/2024-63) also took effect on April 12, 2026, increasing packaging and supply-chain information demands for products using fragrance mixtures, including fragranced shampoos, conditioners, and styling products.

Competitive Landscape

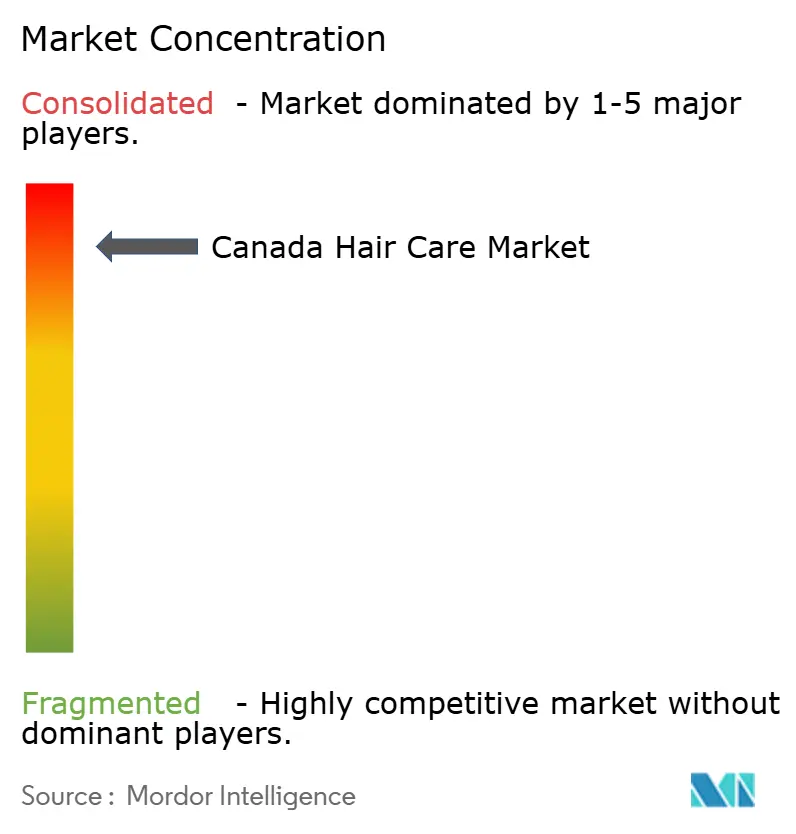

The Canadian hair care market is characterized by a highly concentrated competitive landscape. This indicates a dominant presence of multinational corporations such as L'Oréal, Procter & Gamble Company, and Unilever Plc, which collectively control a significant share of the market. These established players benefit from extensive distribution networks, strong brand equity, and economies of scale, enabling them to maintain their leadership positions. However, the market is witnessing a shift as emerging digital-native brands challenge traditional hierarchies. These new entrants are leveraging direct-to-consumer strategies and social media platforms to build brand awareness and engage with consumers more effectively, disrupting the status quo in the process.

To maintain their competitive edge, established players are increasingly focusing on vertical integration and portfolio optimization. For instance, L'Oréal has strategically divested Carol's Daughter to concentrate on its core brands, ensuring a more streamlined and focused product portfolio. These actions highlight the ongoing efforts of major players to adapt to changing consumer preferences and market dynamics while reinforcing their dominance in the industry.

Despite the stronghold of multinational corporations, the rise of digital-native brands signifies a growing trend of innovation and agility within the market. These brands are capitalizing on the increasing consumer demand for personalized and sustainable hair care solutions. By utilizing data-driven insights and engaging directly with their target audience, they are carving out a niche in the competitive landscape. This evolving dynamic underscores the importance of adaptability and innovation for both established players and new entrants in the Canadian hair care market, as they navigate the challenges and opportunities presented by this rapidly changing industry.

Canada Hair Care Industry Leaders

L’Oréal S.A.

Unilever PLC

Henkel AG & Co. KGaA

Procter & Gamble Company

Kao Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ingredient and labeling changes are creating near-term room for brands that can operationalize transparency at scale, particularly in fragranced hair care, where disclosure requirements add complexity to legacy formulations and supplier documentation. With fragrance allergen disclosure provisions taking effect on April 12, 2026, compliance-ready product architecture (traceable fragrance components, standardized INCI labeling, and faster CNF workflows within the 10-day window after first sale) can act as a differentiator for both mass and premium lines.

Retail execution and service enablement provide another route to differentiation. Shoppers Drug Mart’s rollout of a spa-grade Skin Analysis Tool across beauty departments (April 2026) and the L’Oreal Canada and Shoppers Drug Mart multi-brand fragrance refill fountain pilot (May 2026) indicate retailer investment in in-store personalization and refill models, which can support regimen-building for scalp health and styling routines. In parallel, expanding e-commerce and specialty channels in Canada support brands that bundle targeted solutions (for textured hair, aging-related thinning, and clean-label preferences) with education, authenticity controls, and traceable sourcing to reduce counterfeit-related friction in online channels.

Recent Industry Developments

- June 2026: SalonCentric Canada (a subsidiary of L’Oreal Canada) signed a definitive agreement to acquire the assets of Cantin Beaute, a professional products distributor in Quebec with 25 stores. The deal expands SalonCentric’s physical footprint and improves access to salon-professional distribution, supporting faster reach for professional-grade hair care and styling portfolios in Canada.

- June 2025: Po Athletic introduced Endless Summer, a natural shampoo and conditioner developed in collaboration with Olympian Summer McIntosh and manufactured in Canada. The launch adds momentum to domestically made, natural-positioned hair care offerings aimed at performance and lifestyle use cases.

- January 2024: Vegamour expanded distribution in Canada by launching in 114 Sephora stores and on Sephora Canada’s e-commerce platform. This broadened access for hair wellness products through a major specialty retailer, reinforcing Sephora’s role as a scaling channel for premium and treatment-led hair care.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Canada hair care market is defined as the value of hair care products sold in Canada across retail channels, covering everyday cleansing, conditioning, coloring, styling, and treatment needs for consumers.

Scope exclusions: Salon services and hair-cutting services are excluded, and only product sales value is counted.

Segmentation Overview

- By Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

- By Category

- Premium Products

- Mass Products

- By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

- By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by building a clean view of Canada category demand and the shopper environment, before the model is finalized. We typically lean on public sources such as Statistics Canada for consumer and retail context, the Government of Canada customs trade tables for import and export signals, and industry association publications that describe category direction and channel shifts.

To keep assumptions realistic, we also review sources such as company annual reports and investor presentations for category commentary, product mix, and pricing actions, along with credible press and retailer communications that signal promotions and shelf resets. In parallel, a paid subscription covering company financials and another covering shipment-level trade flows are used selectively to cross-check value ranges and spot breaks in trend. The desk sources listed here are illustrative only, and many other public and paid references are also used during data collection and validation.

Primary Interviews and Surveys

Primary work is used to pressure-test what we saw in published data, especially on pricing progression, channel share changes, and how mass and premium mixes are moving in Canada. We speak with a spread of manufacturers, distributors, retailers, and industry specialists, and we also include viewpoints from different functions so assumptions are not built from a single lens.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | |

| Mid tier: 52% | Functional/Unit leaders: 29% | |

| Smaller Players: 14% | Managers: 57% |

Market-Sizing & Forecasting

Sizing is built using a mix of top-down and bottom-up checks so the final value stays explainable and repeatable. The top-down view is reconstructed from Canada demand signals that reflect how much hair care is being bought through key channels, and then aligned to category splits such as mass versus premium and natural versus conventional where evidence supports it. After that, selective bottom-up approximations are used to corroborate the totals, using sampled price points by product type and channel checks, followed by adjustments when the implied spending pattern looks unrealistic.

Inputs that are tracked in the model include retail sales movement by channel (especially online versus store-based), average price and promotion intensity signals, trade flow direction for packaged beauty products, consumer spending and inflation context, and the mix shift between core care items and styling or treatment products. When data is missing for smaller sub-categories, we fill gaps with conservative share assumptions that are then verified in interviews, and we avoid forcing precision that the evidence cannot support.

For forecasting, we use scenario analysis anchored to a base case, because category growth is heavily influenced by price, promotions, and mix, which can change quickly. The forward view is then stress-tested using primary feedback on expected pricing behavior, premiumization pace, and the stability of demand across channels.

Data Validation & Update Cycle

Validation happens in layers so a single weak signal does not steer the final output. Model totals are triangulated against independent metrics such as category-level retail momentum, implied per-capita spend direction, and trade-based value signals, and then unusual jumps are reviewed before analyst sign-off.

If a large variance appears by product type or channel, follow-up calls are triggered to re-check the assumption and confirm if the change is real or a data timing issue. Reports are refreshed annually, and interim updates are made when there is a material event that can shift pricing, distribution, or category demand. Before delivery, the full model is re-run once more so clients receive the most current view.

Mordor Intelligence's Canada Hair Care Market Market Estimate Compared With Other Published Estimates

It is common to see different Canada hair care market values across published sources, even when the topic name looks the same. The differences usually come from what is counted as hair care, what year is treated as the base, and how pricing and channel shifts are translated into value.

Key gap drivers for this market tend to be whether premium and mass are both included with the same definition, whether hair treatments and oils are grouped broadly or narrowly, and how online sales are handled when promotions are frequent. Currency timing can also move the reported USD value, and some sources apply an aggressive price path without doing enough checks against retail movement signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.59 B (2025) | |

| Global Publisher A | USD 1.23 B (2024) | Uses an earlier base year and a tighter product basket, which can understate value when newer treatment formats and higher price points are growing. |

| Industry Publisher B | USD 4.07 B (2024) | Likely applies a broader personal care or salon-adjacent scope, and may also be mixing retail product sales with other spending, which inflates the total versus a product-only definition. |

Retail channel trend checks, category mix signals, and trade-based value direction are the evidence points that keep Mordor Intelligence tied to a product-sales-only scope for Canada, which helps reduce over-counting when adjacent beauty spend is blended into hair care. The spread in the table mainly reflects scope boundaries and base-year choices, and our approach keeps the final number traceable to clear demand and pricing drivers.

Key Questions Answered in the Report

What is the projected value of the Canada hair care market by 2031?

The Canada hair care market is forecast to reach USD 2.05 billion by 2031, growing at a 4.32% CAGR.

Which product category is expanding fastest?

Hair styling products lead growth with a projected 5.08% CAGR between 2026 and 2031.

How large is the premium segment compared with mass products?

Mass lines held 74.90% share in 2025, while premium offerings are expanding faster at a 5.55% CAGR.

Which sales channel is growing most quickly?

Online retail stores show the highest growth trajectory at a 6.92% CAGR, driven by virtual consultations and social-media influence.

Page last updated on: