Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.04 Billion |

| Market Size (2031) | USD 12.47 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

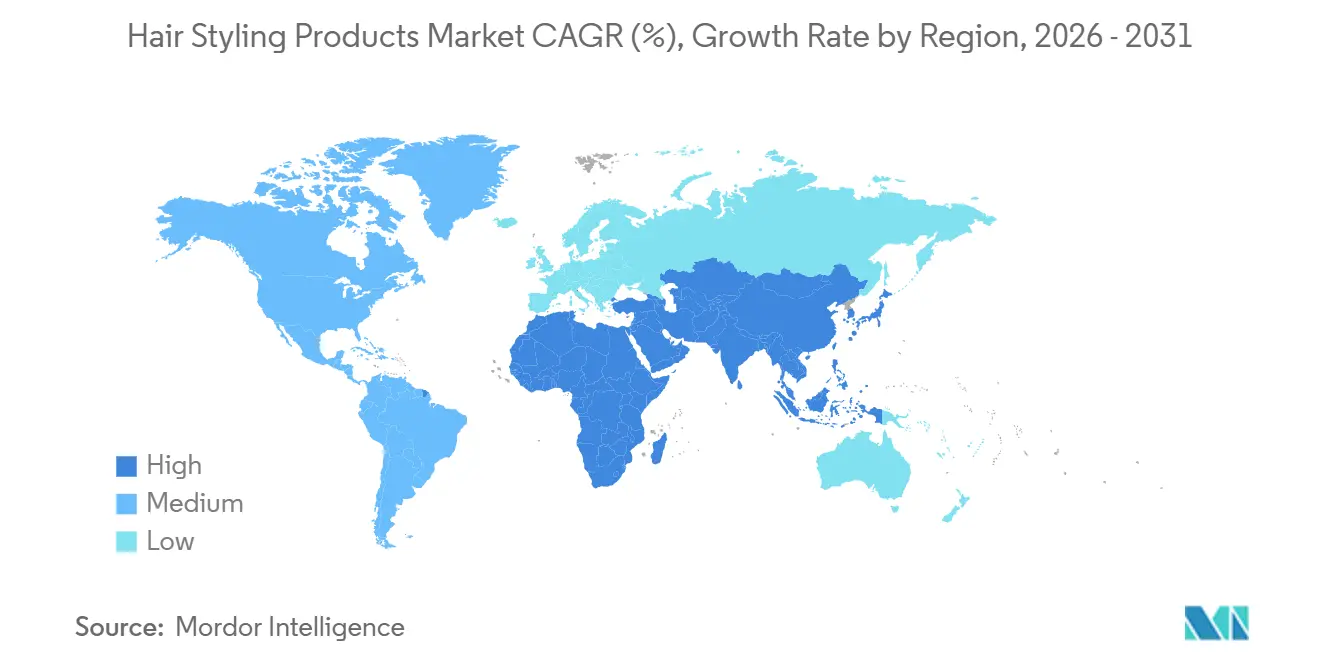

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Styling Products Market Analysis by Mordor Intelligence

The hair styling products market size is expected to grow from USD 9.96 billion in 2025 to USD 10.04 billion in 2026 and is forecast to reach USD 12.47 billion by 2031 at 4.43% CAGR over 2026-2031. Ingredient transparency, gender-inclusive positioning, and multifunctional benefits are replacing brand heritage as primary purchase drivers. Premiumization is gaining traction as younger consumers opt for products with validated performance claims, while value-oriented lines continue to dominate unit sales. In response, brands have focused on clean-label formulations, improved digital merchandising strategies, and robust omni-channel fulfillment systems to maintain sales momentum ahead of broader beauty market trends. Although regulatory changes under the Modernization of Cosmetics Regulation Act (MoCRA) have increased compliance costs for manufacturers, they have also created opportunities for early adopters to showcase ingredient safety and traceability. Digital discovery through short-form videos has accelerated the purchase process, compelling brands to align inventory data with real-time social-commerce trends. The Asia-Pacific region is experiencing the fastest growth, driven by rising affluence in tier-2 cities and social-commerce ecosystems that bypass traditional retail channels.

Key Report Takeaways

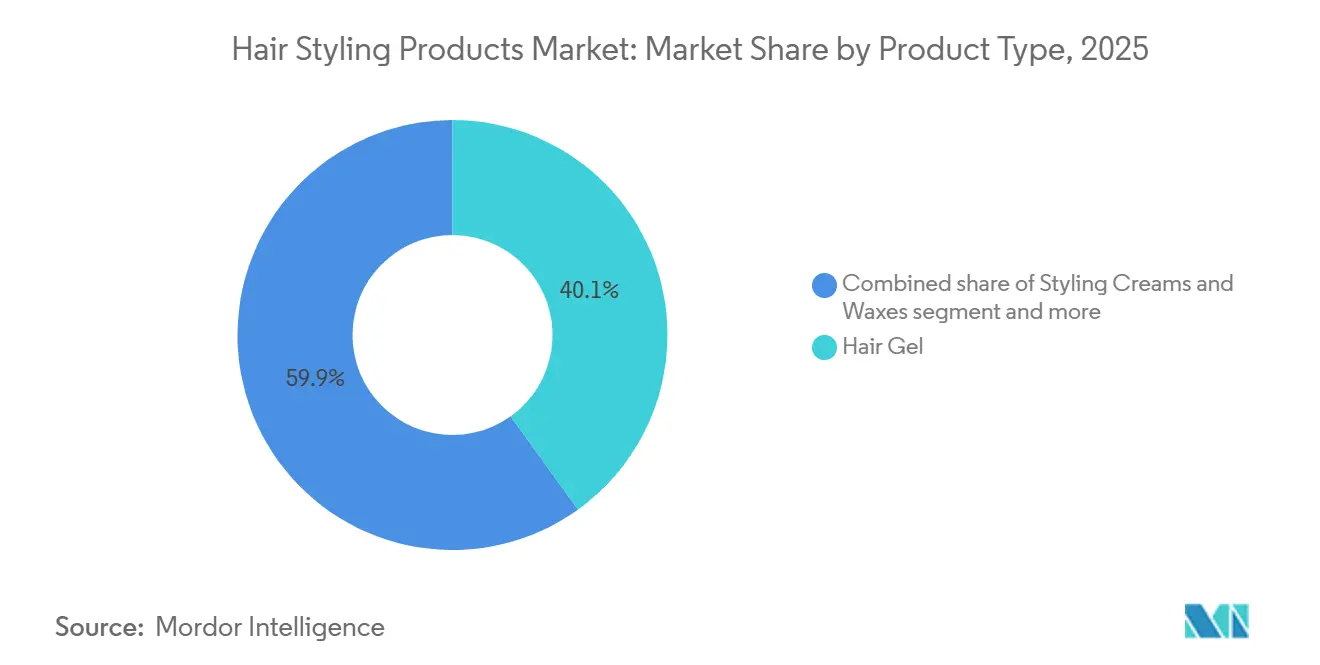

- By product type, hair gel led with 40.09% of the 2025 hair styling products market share, and styling creams and waxes are projected to rise at a 4.59% CAGR through 2031

- By nature, synthetic formulations controlled 72.90% of the 2025 value, while organic variants are projected to record the segment-high 5.80% CAGR to 2031.

- By price range, mass lines captured 78.16% of 2025 revenue; premium offerings advance fastest at 5.67% CAGR to 2031.

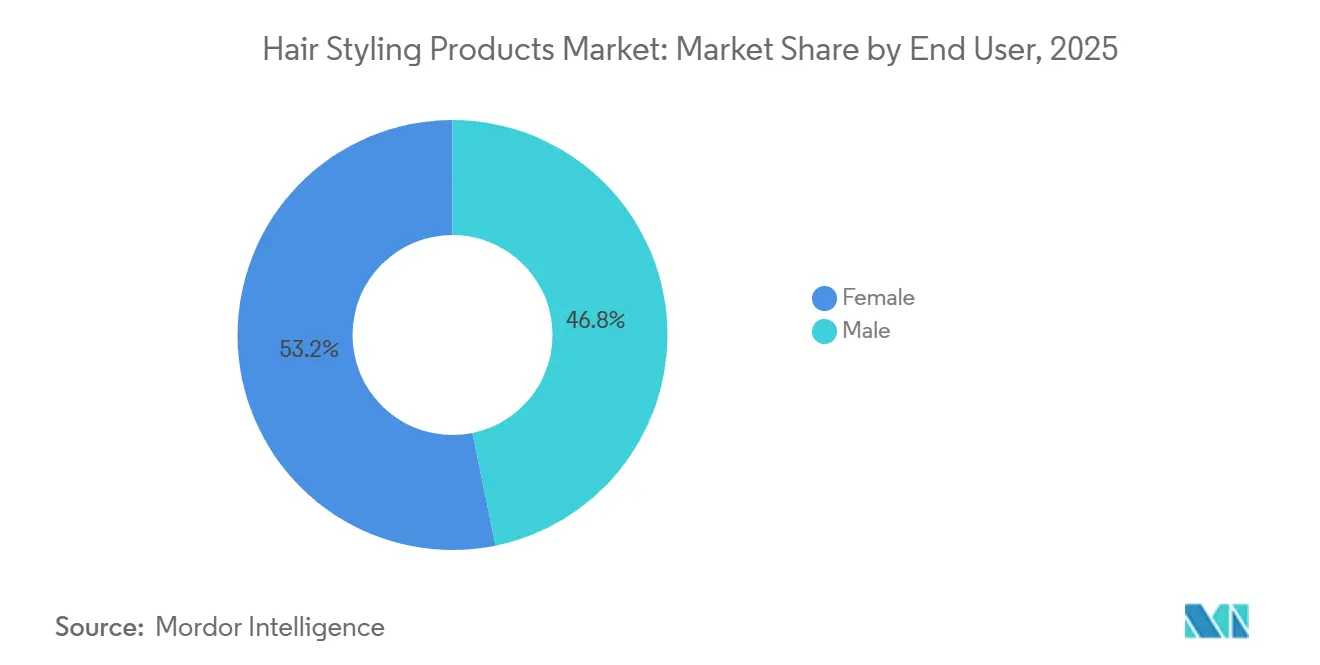

- By end user, women accounted for 53.21% demand in 2025, yet men exhibit the top CAGR at 6.11% through 2031.

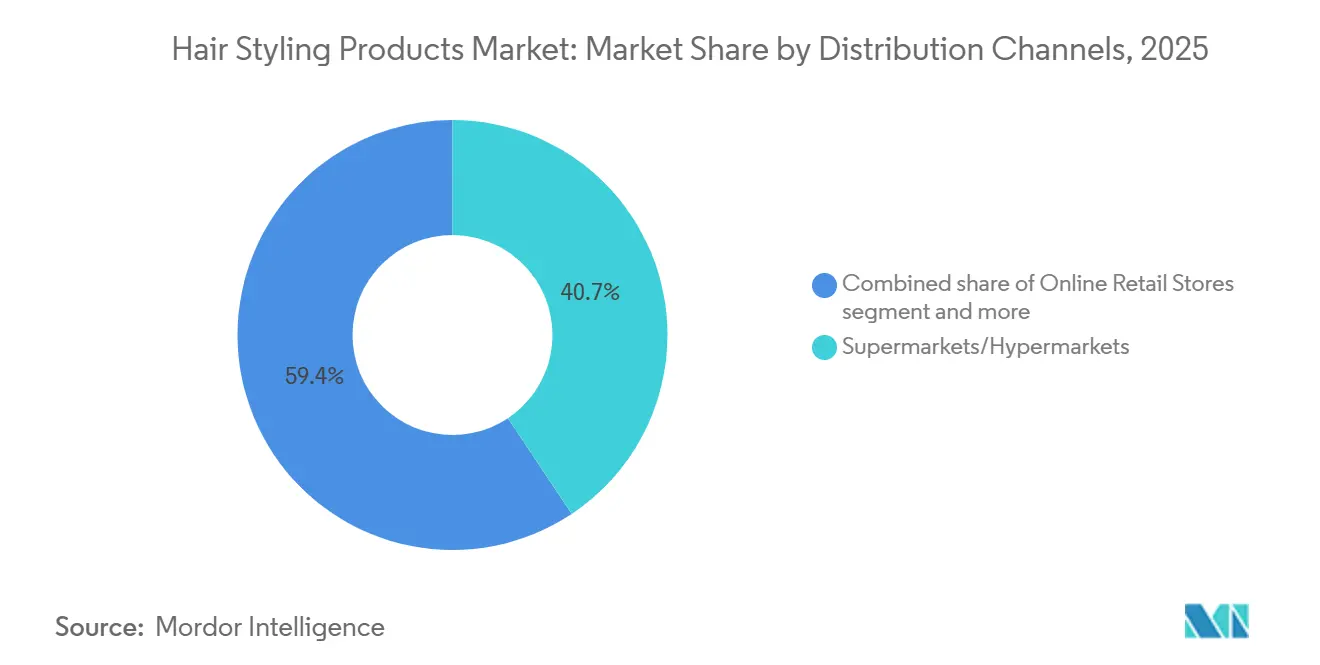

- By distribution channel, supermarkets & hypermarkets owned 40.65% of the 2025 distribution, but online retail climbs at a 6.97% CAGR to 2031.

- By geography, North America delivered 39.92% of 2025 revenue, whereas Asia-Pacific stakes the fastest 5.11% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hair Styling Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing focus on personal grooming and appearance | +0.9% | Global, with strongest uptake in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising influence of social media and beauty influencers | +1.1% | Global, particularly North America, Europe, and Asia-Pacific markets with high digital penetration | Short term (≤ 2 years) |

| Inclination towards natural and organic formulations | +0.8% | Europe and North America lead; Asia-Pacific emerging | Medium term (2-4 years) |

| Surging male grooming expenditure and awareness | +0.7% | North America, Europe, and Asia-Pacific tier-1 cities | Long term (≥ 4 years) |

| Demand for gender-neutral and inclusive products | +0.5% | North America and Europe, with gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Innovation in multifunctional styling products | +0.6% | Global, with early adoption in premium segments across all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing focus on personal grooming and appearance

The growing emphasis on personal grooming and physical appearance is a key factor driving the expansion of the global hair styling products market. Consumers across various age groups are increasingly prioritizing well-maintained hair as an essential aspect of personal identity, professionalism, and social presence. Hairstyles are now widely regarded as a form of self-expression, influenced by fashion trends, workplace norms, and cultural shifts. This change has heightened the importance of daily styling routines, boosting demand for products such as gels, mousses, sprays, serums, and heat protectants that deliver salon-quality results at home. In 2024, the average monthly expenditure on hair and beauty treatments in South Korea was KRW 35.52 thousand, according to Statistics Korea [1]Source: Statistics Korea, "Average monthly income and expenditure (whole households)", kosos.kr. This spending level underscores consumers' willingness to allocate consistent budgets for hair care and styling. It reflects a broader global trend where grooming is integrated into routine lifestyle expenses rather than being treated as discretionary. Such spending behavior indicates strong demand for both professional salon services and complementary at-home styling products. As consumers increasingly prioritize polished appearances for social media, professional settings, and personal confidence, they are more inclined to experiment with new styles, textures, and finishes. This trend drives repeat purchases and fosters innovation in multifunctional, damage-reducing, and long-lasting styling formulations.

Rising influence of social media and beauty influencers

The growing impact of social media and beauty influencers is a key factor driving the expansion of the global hairstyling products market. Platforms such as Instagram, TikTok, YouTube, and Pinterest have redefined hairstyling, turning it from a routine grooming activity into a medium for self-expression and trend adoption. Content such as tutorials, product reviews, viral challenges, and before-and-after transformations enhances visibility for styling products like gels, sprays, serums, and heat protectants, facilitating faster product discovery and reducing purchase decision timelines. According to the World Bank, 68% of the global population actively used the internet in 2024, highlighting the role of digital connectivity in amplifying the reach of beauty-related content [2]Source: World Bank, "Individuals using the Internet", worldbank.org. This connectivity allows brands to engage directly with consumers through targeted campaigns, live demonstrations, and user-generated content. Additionally, social media algorithms personalize exposure, ensuring that styling solutions designed for specific hair types, textures, and concerns reach the most relevant audiences.

Inclination towards for natural and organic formulations

The growing consumer preference for natural and organic formulations is a key factor driving the hair styling products market. With increasing awareness of ingredient safety, scalp health, and the potential for long-term hair damage, consumers are actively seeking styling products free from harsh chemicals such as parabens, sulfates, phthalates, and synthetic alcohols. Modern consumers are not only concerned with hold strength or finish but also with the impact of products on hair texture, scalp sensitivity, and overall hair health. This trend has led to a rise in demand for plant-based gels, botanical-infused serums, aloe- and flaxseed-based styling creams, and naturally derived heat protectants. A study conducted in March 2025 by NSF, a global public health and safety organization, revealed that 74% of consumers prioritize organic ingredients in personal care products [3]Source: NSF International, "2025 Consumer Insights Report: Organic Ingredients in Personal Care", nsf.org. This finding underscores the increasing importance of clean and transparent formulations in the hair styling category. Consumers are scrutinizing ingredient lists more closely and expect brands to clearly communicate information about sourcing, sustainability practices, and safety standards. In response, manufacturers are reformulating traditional styling products to include naturally derived polymers, essential oils, and biodegradable ingredients, ensuring performance is maintained while meeting consumer demand for cleaner formulations.

Surging male grooming expenditure and awareness

The increasing expenditure on male grooming and growing awareness are becoming significant qualitative growth drivers for the global hair styling products market. Historically less developed compared to the female segment, the men’s category has undergone substantial evolution due to changing social norms, heightened appearance awareness, and the acceptance of male self-care. Modern male consumers are progressively investing in hairstyling products such as pomades, clays, waxes, styling creams, and texturizing sprays to achieve polished, professional, and trend-focused looks. Grooming has expanded beyond basic upkeep to become closely associated with personal branding, workplace presence, and social media representation. The rising influence of barbershop culture, celebrity athletes, and digital influencers has further enhanced styling routines among men, promoting experimentation with fades, textured cuts, longer hairstyles, and color treatments, all of which require specialized styling products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns regarding harmful ingredients | -0.6% | Global, with heightened scrutiny in Europe and North America | Medium term (2-4 years) |

| Environmental concerns related to packaging, sprays, and aerosols | -0.5% | Europe and North America lead; Asia-Pacific emerging | Long term (≥ 4 years) |

| Regulatory pressures and stricter ingredient compliance | -0.4% | Europe, North America, and select Asia-Pacific markets | Medium term (2-4 years) |

| High price sensitivity in developing markets | -0.7% | Asia-Pacific, Middle East, Africa, and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concerns regarding harmful ingredients

Concerns regarding harmful or controversial ingredients pose a significant challenge in the hair styling products market. Increasing consumer awareness of the potential long-term effects of chemicals such as parabens, sulfates, formaldehyde-releasing preservatives, phthalates, and certain synthetic fragrances has intensified scrutiny of product labels. Hair styling products are particularly affected due to their frequent use and prolonged contact with the scalp, which raises concerns about scalp irritation, hair damage, and systemic exposure. This growing awareness has influenced purchasing behavior, with consumers increasingly researching ingredient lists, seeking third-party certifications, and preferring brands that prioritize transparency and clean-label formulations. Negative media coverage, social media discussions, and influencer advocacy for “toxic-free” beauty further amplify these concerns, potentially discouraging repeat purchases of traditional formulations. Consequently, legacy brands that continue to rely on conventional chemical-based polymers and fixatives may experience a decline in consumer trust unless reformulation efforts are clearly communicated to the market.

Environmental concerns related to packaging, sprays, and aerosols

Environmental concerns related to packaging and product delivery formats are increasingly constraining growth in the hair styling products market. Common formats such as aerosols, pump sprays, and single-use plastic containers, traditionally used in products like hairsprays, mousses, and volumizers, are under heightened scrutiny due to their environmental impact. Issues include non-recyclable components, the release of volatile organic compounds (VOCs), and greenhouse gas emissions from propellants. Both consumers and regulators are urging brands to adopt sustainable alternatives, presenting reputational and operational challenges for companies. Environmentally conscious consumers now prefer refillable packaging, biodegradable materials, and recyclable bottles, and they are more likely to shift loyalty away from brands that neglect ecological considerations. Social media campaigns, advocacy for eco-labeling, and growing public awareness of plastic pollution and climate change have intensified expectations for sustainable product design. This creates additional pressure on brands to integrate eco-friendly packaging solutions while maintaining the functional requirements of styling products, such as stability, dispensing efficiency, and shelf life.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gel Dominance Meets Cream Innovation

Hair gel accounted for 40.09% of 2025 sales, indicating a split between traditional hold-focused formulations and natural-finish alternatives. Meanwhile, styling creams and waxes are expected to grow at a CAGR of 4.59% through 2031, marking the fastest growth rate among product types. This growth is driven by rising demand for products that offer a natural finish and subtle texture, reflecting changing consumer preferences. The growing preference for creams is driven by workplace aesthetics that emphasize understated styles over high-gloss finishes, a trend further influenced by the rise of remote work and hybrid office arrangements, which have shifted grooming habits.

Other styling products, such as pomades and texturizing sprays, cater to niche demand from barbershop clients and salon professionals who prioritize versatility over mass-market offerings. These products are particularly valued for their ability to create diverse styles while maintaining professional-grade quality. The integration of styling and treatment benefits is influencing product innovation; for instance, Kao Corporation's Bioré styling gel, which incorporates ceramides for scalp hydration, reflects the growing "skinification" trend. This trend underscores the blending of cosmetic and skincare benefits in hair styling products to meet consumer expectations for multifunctionality. Adherence to ISO 22716 (Good Manufacturing Practices for Cosmetics) has become essential, with non-compliant products at risk of being removed from major retail channels, further emphasizing the importance of regulatory compliance in maintaining market presence.

By Nature: Organic Surge Challenges Synthetic Incumbents

Synthetic or conventional products are anticipated to account for 72.90% of the revenue in 2025, reflecting the cost and performance trade-offs that constrain the adoption of organic products in mass-market segments. Organic and natural formulations are projected to grow at a CAGR of 5.80% through 2031. The European Union's Ecolabel certification, which is awarded to products meeting stringent environmental criteria, has emerged as a competitive differentiator, with certified products commanding price premiums of 15% to 25%. Supply-chain constraints for certified-organic botanicals have restricted margin expansion, as ingredient costs are 40% to 60% higher than those of synthetic alternatives. Synthetic formulations continue to offer advantages in hold strength and humidity resistance, which are essential attributes for professional stylists operating in high-demand environments such as fashion shows and film sets.

The "clean beauty" movement has led to the proliferation of multiple certifications, including COSMOS, Natrue, and EWG Verified, which has created consumer confusion and diluted the impact of individual labels. Meanwhile, synthetic formulations are evolving to address safety concerns. Brands are replacing parabens with alternative preservatives such as phenoxyethanol and adopting sulfate-free surfactants that replicate the cleansing properties of natural ingredients. These developments reflect the ongoing efforts of brands to balance consumer demand for safety and sustainability with the performance and cost advantages of synthetic products.

By Price Range: Mass Holds Ground as Premium Accelerates

Mass-market products are projected to account for 78.16% of sales in 2025, while premium styling products are expected to grow at a CAGR of 5.67% through 2031. This highlights a two-tier market where brand loyalty varies significantly across income groups. Oribe's Gold Lust collection, priced between USD 50 and USD 70 per unit, experienced a 22% growth in 2025, driven by salon partnerships and influencer endorsements that position the brand as aspirational. In response, mass-market players like Unilever's TRESemmé and Procter & Gamble's Pantene have introduced "masstige" sub-brands, incorporating premium elements such as botanical extracts and minimalist packaging at more accessible price points. Price sensitivity remains a critical factor in developing markets, where local brands in countries like India, Indonesia, and Nigeria undercut multinational pricing by 30% to 40% through simplified formulations and sachet packaging.

E-commerce platforms have broadened access to premium products, with subscription services offering trial sizes that reduce the barrier to entry. For instance, Birchbox reported that 38% of its subscribers upgraded to full-size premium styling products after sampling. The middle-tier segment, comprising products priced between USD 10 and USD 25, faces margin pressures as consumers increasingly gravitate toward either value or luxury options, compelling brands to either reposition their offerings or exit the market.

By End User: Male Segment Outpaces Female Growth

Female consumers are projected to represent 53.21% of demand in 2025, reflecting consistent purchasing patterns and a broader range of product offerings. Meanwhile, male end-users are anticipated to drive a compound annual growth rate (CAGR) of 6.11% through 2031, making them the fastest-growing demographic segment. The normalization of male grooming has accelerated since the pandemic, with workplace re-entry increasing the focus on professional appearance. Gender-neutral brands, including Hairstory and Function of Beauty, have gained popularity by avoiding binary marketing and prioritizing ingredient efficacy over demographic-specific targeting.

Female consumers remain the primary demographic; however, growth in this segment has plateaued in mature markets as product penetration nears saturation. Innovation efforts are increasingly focused on addressing the needs of specific hair types, such as curly, coily, and textured hair, that have historically been underserved by mass-market formulations. Brands that do not develop male-specific formulations, such as lighter textures, faster absorption, and subtle fragrances, risk losing market share to specialists like Uppercut Deluxe and Baxter of California.

By Distribution Channels: Online Retail Disrupts Traditional Gatekeepers

Supermarkets and hypermarkets accounted for 40.65% of the distribution share in 2025, while online retail stores are projected to grow at a CAGR of 6.97% through 2031, representing the fastest-growing distribution channel. This highlights a structural shift toward direct-to-consumer and digital-first models. E-commerce platforms are streamlining the discovery-to-purchase process. However, convenience stores and specialist stores are experiencing margin pressures due to declining foot traffic. Specialty beauty retailers, such as Ulta and Sephora, are adopting omnichannel strategies that integrate in-store consultations with online fulfillment.

Supermarkets and hypermarkets continue to benefit from impulse purchasing and immediate product availability. However, their market share is diminishing as younger consumers increasingly prioritize convenience and personalized recommendations over traditional in-store browsing. Retailers like Walmart and Target have responded by expanding their beauty product assortments and collaborating with prestige brands that were previously exclusive to specialty channels. The distribution channel mix is expected to become more fragmented as brands explore innovative approaches, such as pop-up stores, vending machines, and hotel partnerships, to engage with consumers in non-traditional settings.

Geography Analysis

North America accounted for 39.92% of the projected 2025 revenue, reflecting its significant market share. However, the region's maturity is evident in its single-digit growth rates, which fall below the global average. The United States remains the largest single-country market, with states like California and New York contributing significantly to national sales due to high per-capita incomes and a dense network of salons. In Canada, bilingual labeling requirements and stricter ingredient regulations under Health Canada's Cosmetic Ingredient Hotlist have increased compliance costs, leading some smaller brands to exit the market. Mexico's market is divided, with premium imports concentrated in urban centers such as Mexico City and Monterrey, while mass-market local brands dominate rural areas.

The Asia-Pacific region is projected to grow at a 5.11% CAGR through 2031, fueled by rising middle-class incomes and the popularity of K-beauty and J-beauty trends, which emphasize minimalist aesthetics and multifunctional formulations. In China, the "skinification" trend has extended to hair care, with consumers seeking styling products that include scalp-health ingredients such as niacinamide and centella asiatica. India's market is expanding rapidly, with tier-2 cities like Pune, Jaipur, and Lucknow driving incremental demand as disposable incomes rise and grooming norms evolve. In Japan, the aging population has shifted demand toward anti-aging hair formulations, prompting companies like Kao Corporation and Shiseido to launch styling products targeting thinning and graying hair.

Europe's market is heavily influenced by the EU's REACH regulation, which restricts over 1,300 cosmetic ingredients. This regulation compels brands to reformulate products for the bloc's 27 member states, increasing R&D costs but creating a competitive advantage for compliant brands against non-compliant entrants. South America, the Middle East, and Africa remain emerging markets but are attracting increasing investment. For instance, Unilever expanded its manufacturing footprint in Brazil in 2025 to cater to the region's growing middle class. In South Africa, the market is benefiting from the increased availability and penetration of textured-hair products.

Competitive Landscape

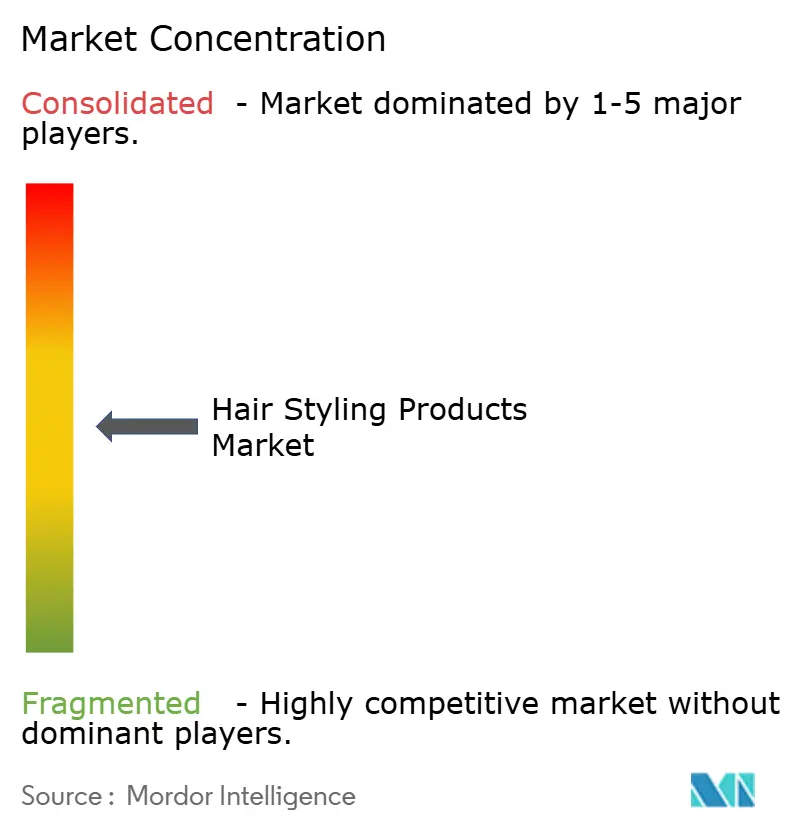

The hair styling products market exhibits moderate fragmentation, with multinational corporations such as L'Oréal, Unilever, and Procter & Gamble accounting for approximately 45% of global revenue. However, these companies face ongoing market share erosion from specialist brands that utilize salon distribution channels and influencer partnerships to bypass traditional retail models. Specialist brands are increasingly leveraging direct-to-consumer strategies and niche marketing to appeal to specific consumer segments. Strategic trends indicate a division in approach: mass-market players focus on cost leadership through vertical integration and private-label collaborations to maintain affordability, while premium brands emphasize clinical validation and sustainability credentials to support higher price points and build consumer trust.

Opportunities remain in hybrid formulations that combine styling hold with scalp-health benefits, driven by the growing trend of "skinification" in hair care, where skincare principles are applied to hair products. This trend is exemplified by Kao Corporation's patent filings for ceramide-infused styling gels, which aim to provide both styling functionality and scalp nourishment. Additionally, technology adoption is transforming competitive dynamics, with brands leveraging augmented-reality try-on tools to allow consumers to visualize product effects and AI-powered product recommendations to personalize shopping experiences. These innovations help reduce return rates and improve conversion rates, enhancing customer satisfaction and loyalty.

Regulatory compliance has become a critical factor in maintaining market presence, particularly adherence to ISO 22716 (Good Manufacturing Practices for Cosmetics) and the EU's REACH regulation. These standards ensure product safety and quality, providing a competitive advantage for compliant brands. Non-compliant brands face significant risks, including delisting from major retailers and e-commerce platforms, which can severely impact their market access. As regulatory scrutiny intensifies, companies are increasingly investing in compliance measures to safeguard their market positions and meet consumer expectations for safe and reliable products.

Hair Styling Products Industry Leaders

-

L’Oréal S.A.

-

Kao Corporation

-

Unilever PLC

-

Henkel AG and Co. KGaA

-

The Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: John Frieda, under the leadership of its parent company Kao Corporation, has undergone a significant brand refresh. This includes reformulated products, redesigned premium packaging, and enhanced fragrance technology to reinforce its position in the premium mass haircare and styling market. The relaunch features vegan formulations with fewer, more effective, and biodegradable ingredients, the elimination of harsh surfactants and preservatives, and the incorporation of DSM-Firmenich’s AuraBoost mood-enhancing fragrance technology.

- August 2024: Dyson launched its pre-style and post-style serums, incorporating chitosan, a macromolecule derived from oyster mushrooms. These serums, developed using Dyson's proprietary Triodetic technology, provide flexible hold throughout the day.

- July 2024: Henkel, a global manufacturer of industrial and consumer products, inaugurated a new beauty care production facility in Riyadh. The facility produces a variety of products under the Pert brand, including shampoos, conditioners, and specialized hair styling items, catering to the rising demand for premium personal care products in the Middle East.

Global Hair Styling Products Market Report Scope

Hair styling products refer to the products used to create different hairstyles on natural hair. These products can be used individually and also with hair styling tools. The hair styling products market is segmented into product type, distribution channel, and geography. Based on the product type, the market is segmented into hair gel, hair mousse, hairspray, styling creams and waxes, and other styling products. The market is segmented by distribution channels: convenience stores, supermarkets/hypermarkets, specialist stores, online retail stores, and other distribution channels. Further, the market is segmented geographically into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD billion).

By Product Type

| Hair Gel |

| Hair Mousse |

| Hair Spray |

| Styling Creams and Waxes |

| Other Styling Products |

By Nature

| Synthetic/Conventional |

| Organic/Natural |

By Price Range

| Mass |

| Premium |

By End User

| Male |

| Female |

By Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialist Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hair Gel | |

| Hair Mousse | ||

| Hair Spray | ||

| Styling Creams and Waxes | ||

| Other Styling Products | ||

| By Nature | Synthetic/Conventional | |

| Organic/Natural | ||

| By Price Range | Mass | |

| Premium | ||

| By End User | Male | |

| Female | ||

| By Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialist Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the hair styling products market expected to grow through 2031?

It is projected to expand at a 4.43% CAGR from 2026 to 2031, taking value from USD 10.04 billion to USD 12.47 billion.

Which product type is gaining momentum against traditional hair gel?

Styling creams and waxes are the fastest risers, advancing at a 4.59% CAGR through 2031 as consumers favor natural-finish looks.

Why is Asia-Pacific considered the key growth region?

Rising disposable income in tier-2 cities and dominant social-commerce platforms are propelling a 5.11% CAGR in the region.

What factors are pushing demand for organic hair styling formulations?

Regulatory clampdowns on controversial chemicals and consumer preference for transparent ingredient lists are driving 5.80% annual growth in organic products.

Page last updated on: