Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.33 Billion |

| Market Size (2031) | USD 18.79 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

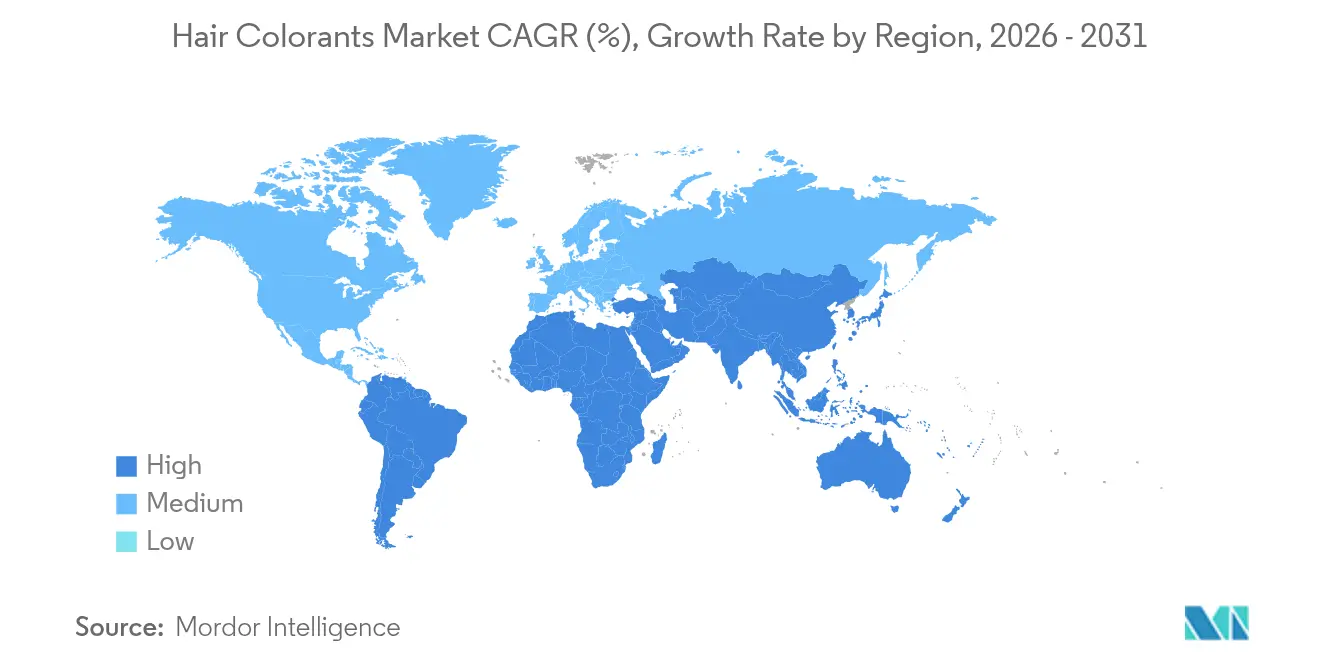

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

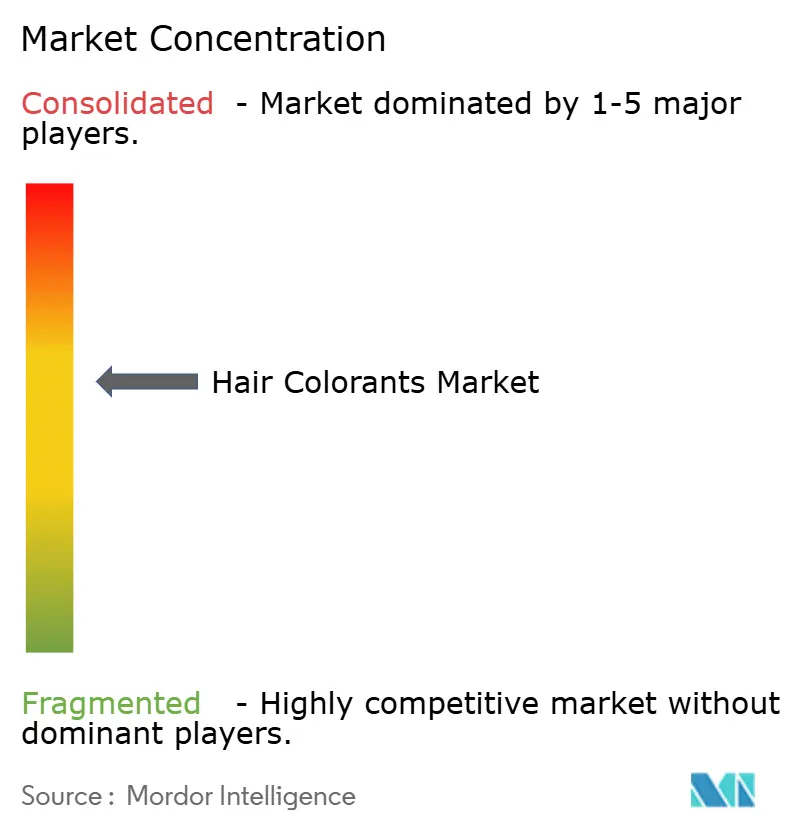

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hair Colorants Market Analysis by Mordor Intelligence

Hair colorants market size in 2026 is estimated at USD 15.33 billion, growing from 2025 value of USD 14.72 billion with 2031 projections showing USD 18.79 billion, growing at 4.15% CAGR over 2026-2031. Two distinct consumer demands are shaping this trend: older consumers are focusing on grey coverage, while younger ones are leaning towards bold, short-cycle styles. Innovations like ammonia-free products, quick shade turnovers influenced by social media, and a blend of online and offline retailing are driving both volume and value growth. Europe sees a consistent rise in premium products, supported by a strong preference for high-quality formulations and brand loyalty among consumers. Meanwhile, Asia Pacific benefits from a growing salon infrastructure, increasing disposable incomes, and a surge in digital commerce, leading to even higher gains. While established players bolster their advantages in research, regulatory matters, and salon distribution, niche newcomers are successfully drawing in a digitally-savvy audience by leveraging targeted marketing strategies and unique product offerings, resulting in a moderate competitive intensity.

Key Report Takeaways

- By product type, Permanent Colorants held 48.62% of the 2025 hair colorants market share and Highlighters are forecast to expand at a 9.29% CAGR between 2026-2031.

- By category, Mass products captured 68.78% of 2025 revenue while Premium offerings are expected to register a 10.52% CAGR through 2031.

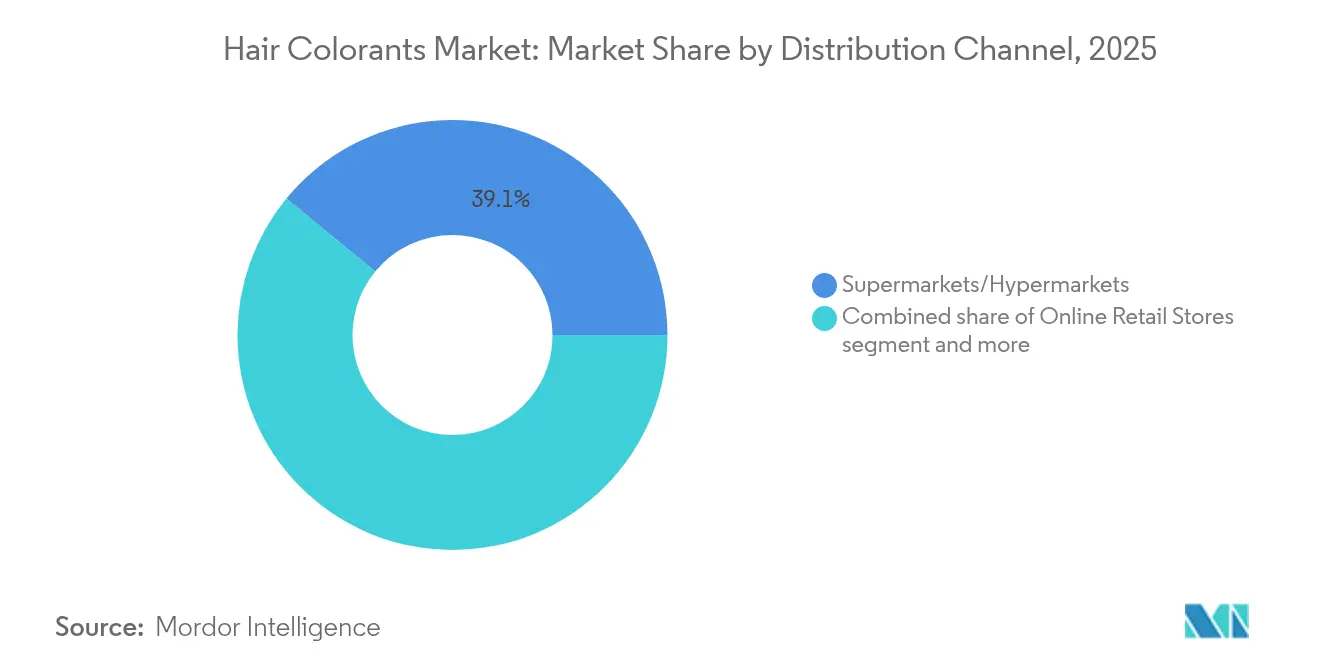

- By distribution channel, Supermarkets/Hypermarkets commanded 39.05% of 2025 sales, and Online Retail Stores are projected to grow at a 6.76% CAGR to 2031.

- By geography, Europe accounted for 32.45% of 2025 value and Asia Pacific is poised to advance at a 7.85% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hair Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demographic shift – grey-coverage demand surge | +1.2% | North America, Europe, East Asia | Long term (≥ 4 years) |

| Social-media fueled fashion experimentation | +0.8% | North America, Europe, expanding Asia Pacific | Short term (≤ 2 years) |

| Innovation in ammonia-free and natural dyes | +0.6% | Europe, North America | Medium term (2-4 years) |

| Expansion of salon networks in emerging markets | +0.9% | Asia Pacific core, spill-over Latin America and MEA | Medium term (2-4 years) |

| At-home AI shade-matching adoption | +0.4% | North America, Europe, urban Asia Pacific | Short term (≤ 2 years) |

| Rise of gender-neutral inclusive color lines | +0.3% | North America, Europe, selective global cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demographic shift – grey-coverage demand surge

By 2040, projections indicate that 22.7% of Canada's residents will be aged 65 and older. This demographic increasingly favors professional services and premium at-home kits, seeking assurances of full coverage, longevity, and scalp safety. In response, formulators are incorporating bond-building agents to mitigate chemical stress, ensuring that products cater to the specific needs of aging hair, such as reduced elasticity and increased fragility. Hairdressers are championing subscription-based touch-up services, offering convenience and consistent results to maintain customer satisfaction. Amid intensified safety scrutiny, compliance with ISO 22716 emerges as a trust signal, reinforcing consumer confidence and bolstering brand loyalty among older buyers. As a result, while niche color trends may waver, permanent oxidative systems continue to hold steady in volume due to their reliability and effectiveness. Manufacturers adept at harmonizing low-odor chemistry with deep penetration technology stand poised to tap into this structurally expanding and increasingly discerning user base.

Social-media fueled fashion experimentation

Platforms like TikTok have accelerated color fads, shrinking their timelines from seasons to mere weeks. This shift has intensified the demand for semi-permanent and highlight formats, which allow for quicker changes and align with the fast-paced preferences of younger consumers. In the U.S., 40% of adults aged 18-22 show a keen interest in gender-neutral color cosmetics, underscoring a wider trend towards inclusive beauty that resonates with evolving societal values. Generative AI-driven virtual try-on tools are alleviating user hesitations by enabling them to visualize results before making a commitment, thereby enhancing consumer confidence and driving purchase decisions. The swift rise of digital trends is pushing supply chains to adapt, leading to smaller batch runs with a wider shade variety to meet diverse consumer demands. This agility is especially beneficial for firms that utilize flexible manufacturing cells, allowing them to respond quickly to market shifts. Retailers are capitalizing on these rapid cycles, rolling out limited-edition drops that transition from social media previews to checkouts in just days, creating a sense of urgency and exclusivity among consumers.

Innovation in ammonia-free and natural dyes

Driven by regulatory mandates and consumer health concerns, investments are surging into oil-delivery systems and monoethanolamine-based solutions. These innovations aim to eliminate ammonia while maintaining color integrity, addressing growing consumer demand for safer and more sustainable hair color products. L’Oréal's cutting-edge iNOA technology boasts a 60% oil content, facilitating pigment diffusion with reduced odor and irritation, setting a benchmark for innovation in the hair color market. The European Commission's nod in 2024 to HC Red No. 18, allowing concentrations of up to 1.5%, underscores a growing endorsement for next-gen molecules, reflecting the regulatory push for advanced and compliant formulations. Concurrently, research delves into plant-derived anthocyanins, eyeing rich burgundy shades that cater to the rising preference for natural ingredients. However, challenges like batch consistency and fade resistance persist, requiring further technological advancements. Brands touting dermatology-tested credentials are increasingly securing prime placements in upscale chains and niche salons, as consumers prioritize safety and efficacy in their purchasing decisions.

Expansion of salon networks in emerging markets

In Asia Pacific, the urban middle class is increasingly turning to professional services, prompting global players to acquire local distributors and franchise operators. For instance, L’Oréal's acquisition of CONCEPT JP in 2025 not only brought 11 professional stores and 16 express sites in Quebec but also bolstered SalonCentric's regional presence, enabling the company to strengthen its supply chain and service capabilities. Across Southeast Asia, similar acquisitions are extending reach into tier-two cities, where salon density is still emerging, creating opportunities for market penetration and customer base expansion. This network expansion is also enhancing training opportunities, equipping stylists with advanced coloring techniques, bond-repair recommendations, and the ability to deliver premium services that meet evolving consumer expectations. Moreover, in countries like India and Indonesia, where matching undertones is vital, local shade customization ensures cultural relevance, catering to diverse preferences and maintaining brand loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and allergy concerns over dye chemicals | -0.7% | Global focus in Europe and North America | Long term (≥ 4 years) |

| Stringent global ingredient regulations | -0.5% | EU leadership, global adoption | Medium term (2-4 years) |

| Supply-chain risk for key dye intermediates | -0.4% | Asia-centered production nodes | Short term (≤ 2 years) |

| Counterfeit and return fraud on e-commerce channels | -0.2% | High online penetration markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health and allergy concerns over dye chemicals

PPD, a recognized sensitizer, has been flagged by the nonprofit MADE SAFE as a primary allergen responsible for contact dermatitis. This chemical is commonly used in hair dyes and other cosmetic products, making its regulation critical for consumer safety. In the United Arab Emirates, regulatory inspections discovered multiple retail products surpassing permissible PPD limits, highlighting oversight deficiencies and the need for stricter enforcement. Meanwhile, New York State's revelation of counterfeit cosmetics laced with heavy metals has further eroded consumer confidence, raising concerns about the safety of unregulated products[1]Source : The New York State Department of State," Fake Cosmetics and their Health Risks", dos.ny.gov. As a result, consumers are increasingly gravitating towards certified PPD-free products and botanical-based kits, which are perceived as safer alternatives. However, the transition is tempered by premium pricing and a restricted range of shades, limiting the pace of adoption despite growing awareness of potential health risks.

Stringent global ingredient regulations

In 2024, the EU's Rapid Alert System for dangerous non-food products recorded over 1,000 notifications related to cosmetics, with hair dyes being a significant focus due to concerns over potential health risks and regulatory scrutiny. Meanwhile, the U.S. Modernization of Cosmetics Regulation Act (MoCRA) mandates adverse-event reporting and facility registration, creating additional financial and operational burdens for smaller brands that often lack the resources of larger companies[2]Source: Food and Drug Administration,"Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", fda.gov. In China, the evolving CSAR regime has introduced distinct filing rules for special-use colorants, requiring companies to maintain parallel formulation portfolios to meet compliance standards. While global players navigate this intricate and dynamic regulatory landscape with dedicated compliance teams, startups frequently resort to outsourcing compliance tasks, which increases costs and extends time-to-market, potentially impacting their competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Permanent Colorants underpin value while Highlighters accelerate rotation

Permanent colorants dominate the global hair color market, maintaining a commanding share of 48.62% in 2025, underscoring consumers’ consistent preference for long-lasting color solutions that reduce the need for frequent maintenance. This category remains the backbone of the industry, especially as demographic aging trends continue to increase demand for reliable grey coverage. Innovation in formulations has strengthened its position, with brands like CHI Color Express introducing ammonia-free systems that deliver 100% grey coverage in just 10 minutes, catering to consumers seeking both efficiency and gentler chemistry. The segment is further bolstered by the fact that permanent oxidative dyes account for nearly 70-80% of hair coloring products sold in European markets as regulated under Regulation (EC) No 1223/2009. Despite its stronghold, the category faces growing scrutiny from health-conscious consumers who are cautious about conventional chemical systems, pressuring manufacturers to develop safer and more natural alternatives. Nevertheless, the durability and effectiveness of permanent colorants continue to secure their leading role in the hair coloring landscape.

Highlighters stand out as the fastest-growing segment, projected to expand at a 9.29% CAGR through 2031, driven by changing consumer behavior and evolving beauty trends. Social media has been instrumental in fueling experimentation, with younger demographics embracing bold, unconventional looks that temporary color solutions can provide. Unlike permanent products, highlighters appeal to consumers who do not want long-term commitments and instead seek playful options that align with fast-moving fashion and cultural trends. This trend resonates particularly well during festivals, lifestyle events, and casual experimentation, reflecting the demand for spontaneity in beauty routines. The rise of digital influencers and viral beauty trends has created a strong pull for these products, making them highly visible and aspirational. As a result, highlighters are expected to sustain robust growth, carving out a dynamic space in the market by addressing the need for creative self-expression without the permanence of chemical-intensive systems.

By Category: Mass keeps volume leadership while Premium stretches margin horizons

In 2025, mass ranges dominated unit sales, accounting for 68.78%. This trend is largely driven by value pricing strategies that resonate with supermarket shoppers, bolstering brand loyalty among cost-conscious families. Retailers often combine multi-pack promotions with loyalty discounts, a tactic that not only boosts sales but also secures shelf space in the face of competition from private labels. Meanwhile, updates to product formulations lean towards subtle fragrance adjustments and the addition of new shades, avoiding drastic changes in chemistry to maintain cost efficiency.

On the other hand, premium product lines are set to experience a robust growth rate of 10.52% CAGR. These products are increasingly appealing to aspirational consumers who associate higher prices with salon-quality results. Features like gluten-free labels, eco-friendly aluminum packaging, and silicone-free formulas resonate with the modern wellness narrative. Additionally, subscription services offer tailored formulations every six weeks, a strategy that not only stabilizes revenue but also reduces customer turnover. Retail strategies favor specialty chains, where trained consultants emphasize usage techniques to enhance product effectiveness.

By Distribution Channel: Physical mass retail steadies totals as digital channels scale faster

Supermarkets and hypermarkets dominate the market with a 39.05% share. Their widespread presence allows for quick access to routine purchases, and color charts in the aisles boost impulse buying by helping customers visualize their choices. Additionally, these stores often provide a tactile shopping experience, enabling consumers to compare products directly. Brand partners fund end-cap merchandising, curating shade clusters to combat option fatigue and ensure a streamlined shopping experience. Furthermore, the ability to physically browse a wide range of products in one location makes supermarkets and hypermarkets a preferred choice for many consumers, especially for last-minute or unplanned purchases.

Online retail stores are witnessing the fastest growth, boasting a 6.76% CAGR. Features like high-resolution images, live shade consultations, and bundled shipping deals turn casual browsing into multi-kit purchases by offering convenience and personalization. Some retailers utilize AI chatbots to suggest color care routines tailored to individual preferences, enhancing cross-sell rates and improving customer satisfaction. With shipment tracking and simple reordering options, user loyalty increases significantly. This digital model allows smaller indie brands to thrive by bypassing the high costs associated with traditional shelf-placement fees, leveling the playing field in a competitive market. Additionally, the flexibility of online platforms enables retailers to offer frequent promotions, exclusive online-only products, and subscription models, further driving customer engagement and retention.

Geography Analysis

In 2025, Europe commanded a dominant 32.45% share of the hair colorants market, underscoring the deep-rooted salon traditions in nations like Germany, France, Italy, and the UK. Brands, responding to stringent EU cosmetic regulations, are continuously refining formulations, often eliminating contentious additives and shifting towards eco-friendly packaging. With rising disposable incomes and a cultural focus on appearance, there's a steadfast demand for premium products. Notably, Eastern Europe, with countries like Poland and Romania, is witnessing a shift as consumers transition from natural dyes to oxidative systems. However, this growth is tempered by economic fluctuations that heighten price sensitivity.

Asia Pacific is on a rapid ascent, boasting a projected CAGR of 7.85% through 2031. Urbanization in China and India is driving more frequent salon visits. Meanwhile, the rise of digital commerce is enabling brands to launch directly to consumers, sidestepping traditional distributors. Platforms like Chinese livestream shopping are not just showcasing trends but are also bolstering repeat purchases, especially for temporary and semi-permanent products. In Vietnam and Indonesia, government-backed vocational programs are broadening the pool of certified stylists, inadvertently boosting the demand for professional coloring services. Yet, brands must navigate challenges like currency volatility and fluctuating import tariffs, necessitating nimble pricing strategies to fend off competition from local brands.

North America, while mature, is a hotbed of innovation, with product development increasingly leaning towards inclusivity and clean-label narratives. The region's hair colorants market is buoyed by a surge in subscription services, delivering tailored kits every six weeks. Regulatory shifts, particularly under MoCRA in Canada and the U.S., are pushing for transparent labeling. Major multinationals are seizing this as an opportunity to bolster consumer trust. Meanwhile, Latin America and the Middle East and Africa are emerging markets, characterized by youthful populations and a burgeoning influencer culture. While certain Sub-Saharan markets grapple with infrastructure challenges that hinder penetration, the Gulf Cooperation Council countries are witnessing a surge in organized retail, paving the way for premium product opportunities.

Regulatory Landscape

Hair colorants sit under cosmetics frameworks that increasingly rely on ingredient-by-ingredient safety conclusions and post-market oversight. In the European Union, Regulation (EC) No 1223/2009 remains the core rulebook, and Commission Regulation (EU) 2026/909 adopted in April 2026 updated requirements for substances used in cosmetic products, including several hair dyes. The SCCS issued negative safety opinions on Basic Blue 99 and Basic Brown 16 in February 2026, leading to reformulation and portfolio-management considerations for brands selling across Europe.

In the United States, FDA oversight of cosmetic hair colorants is shaped by MoCRA, which requires facility registration, serious adverse event reporting, and safety substantiation for hair coloring preparations. Across Asia, filing and standards regimes add localization needs, including China’s CSAR pathways and technical guidance updates for hair dye cosmetics research and quality control, reinforcing the need for parallel formulations, documentation readiness, and stronger supplier qualification for dye intermediates and finished products sold across multiple jurisdictions.

Competitive Landscape

The hair colorants market exhibits moderate concentration with established multinational corporations competing alongside specialized regional players and emerging direct-to-consumer brands.Multinational giants like L’Oréal, Henkel, Coty, and Kao command nearly 60% of the global revenue. These incumbents harness integrated research and development centers and global supply chains, reaping economies of scale from pigment synthesis to the final packaged goods. They are also quick to patent innovative delivery mechanisms, including cartridge-based applicators and amino-acid bonding agents, fortifying their technological edge and creating significant barriers for new entrants.

Through strategic acquisitions, these firms bolster their distribution in burgeoning markets and amplify their influence in professional channels. A case in point is L’Oréal’s 2025 expansion of SalonCentric in Canada, a move underscoring vertical consolidation and aligning with its prior Asian endeavors to onboard salon educators. Such expansions not only enhance market penetration but also strengthen relationships with professional stakeholders, ensuring a steady demand for their products. Concurrently, ingredient powerhouses like Givaudan are broadening their horizons by acquiring specialists in finished products, diversifying their revenue streams and expediting brand formulation cycles. This downstream integration allows them to cater to a wider range of clients, from large-scale manufacturers to niche brands, while reducing dependency on traditional revenue sources.

New-age direct-to-consumer brands are carving a niche with hyper-personalized quizzes, vegan endorsements, and community-centric narratives that strike a chord with Gen Z. These brands leverage digital platforms to build direct relationships with consumers, fostering loyalty and engagement. While these brands collaborate with contract manufacturers to maintain an asset-light model, they grapple with escalating regulatory challenges that tend to favor their better-capitalized counterparts. Moreover, partnerships with AR technology providers offer a unique edge, enabling immersive shopping experiences and personalized product recommendations. However, these partnerships necessitate consistent capital investment to keep pace with evolving user expectations and technological advancements, making it challenging for smaller players to sustain long-term competitiveness.

Hair Colorants Industry Leaders

-

Henkel AG & Co. KGaA

-

L'Oréal S.A

-

Revlon Inc.

-

Kao Corporation

-

Wella Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory change and safety scrutiny are creating room for compliant dye molecules, gentler systems, and clearer substantiation packages that can be carried across channels, both salon and at-home. The European Commission’s April 2026 Regulation (EU) 2026/909 and the SCCS safety opinions in February 2026 raise the bar for reformulation toolkits, including alternative colorants, stabilizers, and delivery systems, and for brands able to document safety substantiation at scale.

China’s 2026 standards work program and technical guidance (NMPA project plan and NIFDC guidelines released in 2026) point to a more structured pathway for ingredient listing and test expectations, which supports opportunities for companies that build China-ready dossiers and maintain localized shade portfolios. North America is also seeing capability and capacity moves, including Alfaparf Group’s July 2026 purchase of a manufacturing facility in Lincoln, Rhode Island to enhance professional hair color and developer production, with operations ramping afterward. Upstream, ingredient makers are investing in natural color capability, including Sensient Technologies starting an expansion of its St. Louis natural color production facility in March 2026 as part of a USD 250 million investment, which helps shape brand roadmaps that reduce reliance on synthetic dyes and broaden clean-label color options where allowed.

Recent Industry Developments

- July 2026: Henkel AG & Co. KGaA successfully closed its acquisition of OLAPLEX after fulfilling closing conditions. The deal strengthens Henkel's position in premium hair care attached to coloring routines, expanding access to bond-building and damage-mitigation claims that influence colorant purchase decisions. It also increases portfolio breadth for cross-selling across professional and consumer channels.

- March 2026: Sensient Technologies started an expansion of its St. Louis natural color production facility as part of a USD 250 million investment, signaling intensified focus on clean-label and natural color capabilities for the hair colorants market.

- January 2024: Wella Company introduced Clairol's first bonding-focused at-home hair color range, bringing bond-protecting technology into a mainstream consumer format. This expanded the competitive benchmark for at-home kits toward damage reduction alongside coverage and shade performance, pushing peers to pair color with repair-oriented claims and ingredients.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers products that change or enhance hair color, including both consumer and professional use. We measure it as the value of product sales across retail and salon-linked channels at the global level.

Scope exclusions: Hair care items without a coloring function, such as shampoos, conditioners, and styling products, are excluded even if they claim shine or tone benefits.

Segmentation Overview

-

By Product Type

- Bleachers

- Highlighters

- Permanent Colorants

- Semi-Permanent Colorants

- Temporary Colorants

-

By Category

- Mass

- Premium

-

By Distribution Channel

-

Supermarkets/Hypermarkets

- Health and Beauty Stores

- Online Retail Stores

- Other Distribution Channels

-

Supermarkets/Hypermarkets

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work begins with mapping what counts as a hair colorant and what does not, then aligning that definition with how sales flow through stores, online channels, and professional channels. We rely on public and official sources such as US Food and Drug Administration cosmetics guidance, the European Commission and ECHA for ingredient and safety references, and US International Trade Commission data for trade direction checks where hair preparations are reported.

To ground the model, we also review company annual reports, investor presentations, and earnings transcripts to understand how brands describe category performance and pricing moves. Patents and peer-reviewed papers provide supporting signals for formulation shifts such as ammonia-free systems and long-wear claims, which can alter mix and average selling prices over time. Paid subscriptions for company financials, news, and patent databases are used selectively to speed up cross-checks and to keep timelines consistent. The sources listed here are illustrative and not exhaustive, since we use additional references for collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from interviews and structured surveys with hair colorant manufacturers, distributors, retailers, and salon-side stakeholders. These interviews helped confirm channel splits and real world price ladders. Since this is a global market, we also validate differences in shade adoption cycles, promotion intensity, and regulatory constraints across major regions, so the final assumptions do not reflect a single geography.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 14% | APAC: 47% |

| Mid tier: 49% | Functional/Unit leaders: 30% | EMEA: 33% |

| Smaller Players: 17% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

Sizing uses a top-down approach. Consumer spend signals and category mix indicators are used to reconstruct regional demand for hair coloring products, then filtered through product type and channel splits. To keep the totals practical, we corroborate the outcome with selective bottom-up approximations such as sampled price points across key channels, a limited supplier and distributor roll up, and volume-to-value checks using typical pack sizes.

The model is driven by variables such as permanent versus semi-permanent versus temporary mix, salon versus at-home contribution, the pace of gray coverage demand in older cohorts, fashion shade turnover in younger cohorts, and average selling price progression by mass versus premium positioning. Where country-level data is thin, we handle gaps by using proxy indicators from similar markets with close income levels and beauty retail penetration, then stress testing those proxies with expert feedback. For forecasting, we use multivariate regression with scenario checks, where price inflation, premiumization, online share shifts, and regional adoption trends are treated as key explanatory variables and tuned to what interviewees expect for the next few years.

Data Validation & Update Cycle

Validation happens in layers. We reconcile totals to independent signals such as public company commentary on category growth, trade movement direction, and channel-level expansion patterns. When a value looks off, the assumptions are rechecked, outliers are traced back to the input, and the analyst team reviews the logic before sign off.

We also compare the model against adjacent indicators, including changes in beauty retail traffic, salon service recovery, and reported pricing actions, and we tighten assumptions when the narrative and numbers do not match. Reports are refreshed annually, with interim updates triggered when material events occur, including major regulatory changes, sharp currency moves, or step changes in input costs. Before delivery, a final update pass is completed so clients receive the most current version available at that time.

Mordor Intelligence's Hair Colorants Market Size Versus Other Published Estimates

Published market sizes for hair coloring often do not align, even when they sound similar. Different publishers draw the product line differently and choose different base years. Variations also come from how pricing is treated, how salon use is counted, and how quickly the model is refreshed when demand patterns change.

Hair dye products discussed as a wider "hair color" category (including some hair color products beyond classic colorants) sit outside Mordor Intelligence's scope, which is one reason the table figures differ. For the remaining gap, the difference is typically explained by whether estimates include salon services versus only product sales, whether they apply strong premiumization and online mix shifts to average selling prices, and how currency conversion timing is handled for multi-region totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.33 B (2026) | |

| Global Consultancy A | USD 29.77 B (2026) | Uses a broader hair color definition that can extend beyond colorants, and it also blends professional and at-home use in a way that can pull in non-comparable value pools when summarizing global totals. |

| Industry Publisher B | USD 27.40 B (2025) | Anchors the size on a different base year and a wider product grouping, and the price build often assumes faster premium mix expansion without enough cross checks at the product type and channel level. |

Looking across the three figures, the largest swings are explained by how tightly the product definition is kept to colorants, and whether the write up mixes in adjacent hair color product buckets. By keeping inputs tied to product sales by type, channel, and region, and by checking the outcome against observed pricing and mix signals, the estimate remains easier to reproduce and interpret for demand planning and go-to-market actions.

Key Questions Answered in the Report

What is the current value of the hair colorants market?

The market is valued at USD 15.33 billion in 2026.

How fast is the market expected to grow through 2031?

The market is projected to advance at a 4.15% CAGR over 2026-2031.

Which product type generates the highest revenue?

Permanent Colorants account for 48.62% of 2025 sales.

Which region is poised for the fastest expansion?

Asia Pacific is forecast to grow at a 7.85% CAGR to 2031.

What distribution channel is expanding the quickest?

Online Retail Stores are projected to increase at a 6.76% CAGR between 2026-2031.

Page last updated on: