Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.32 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 2.69 Billion |

| Growth Rate (2026 - 2031) | 2.50% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Russia Hair Care Market Analysis by Mordor Intelligence

The Russia hair care market size in 2026 is estimated at USD 2.38 billion, growing from 2025 value of USD 2.32 billion with 2031 projections showing USD 2.69 billion, growing at 2.50% CAGR over 2026-2031. Domestic producers have replaced many existing multinationals, sustaining core demand. At the same time, e-commerce platforms are expanding product accessibility across Russia's vast geography. In line with global wellness trends, demand is rising for plant-based, paraben-free, and sulfate-free hair care products, driven by increasing health and sustainability awareness. Technological advancements are introducing innovative formulations focused on volumizing, color protection, and damage repair, appealing to urban consumers. Additionally, growing awareness among men about personal grooming and hair health is expanding the market's reach, which has traditionally centered on women. The Russian hair care sector is benefiting from active influencer marketing, a recovery in beauty salon visits, and increased interest in premium and natural products. The "Chestny ZNAK" regulatory digitization system is compelling manufacturers to improve traceability, though it also raises compliance costs. Despite challenges such as currency volatility and a high 21% prime rate, which drive up raw material and financing expenses, the Russian hair care market continues to attract brand innovation and capital investment.

Key Report Takeaways

- By product type, shampoo led with 41.05% of the Russian Hair Care market share in 2025. Hair styling products are projected to log the fastest 2.92% CAGR through 2031.

- By category, synthetic/conventional items captured 71.60% share of the Russian Hair Care market size in 2025, while natural/organic is set to expand at a 3.02% CAGR through 2031.

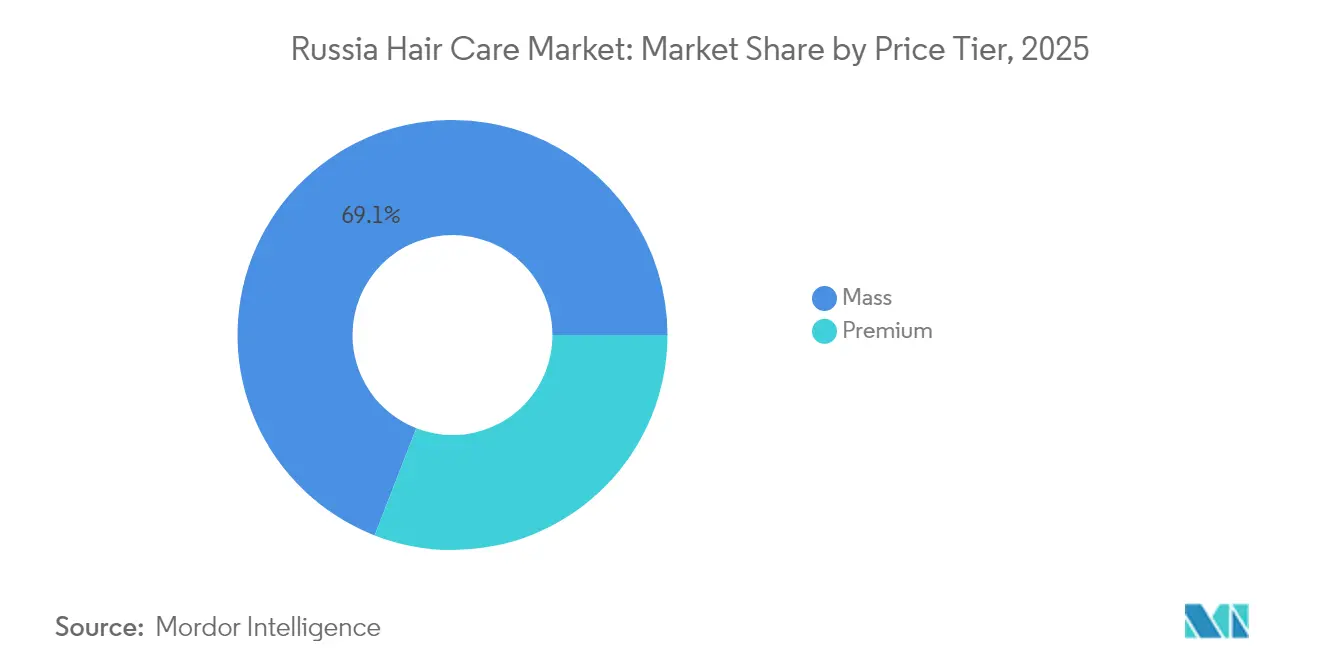

- By price tier, mass products retained a 69.10% share in 2025; premium is forecast to post a 3.46% CAGR out to 2031.

- By channel, supermarkets/hypermarkets held 37.10% revenue in 2025, whereas online retail will advance at a 4.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Russia Hair Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing hair problems among millennials | +0.8% | National, especially Moscow and St. Petersburg | Medium term (2-4 years) |

| Greater demand for premium and customized hair care | +0.6% | Large cities, expanding to regional centers | Long term (≥ 4 years) |

| Rising demand for natural/organic formulations | +0.5% | Nationwide, higher in affluent regions | Medium term (2-4 years) |

| Influence of social media and celebrity endorsements | +0.4% | National, strongest among urban Gen Z | Short term (≤ 2 years) |

| Product innovation and packaging | +0.3% | Premium segments in major cities | Medium term (2-4 years) |

| Viral micro-influencer campaigns | +0.2% | Urban areas via digital platforms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing hair problems among millennials

Russian millennials are the key drivers of growth in the specialized hair care market. This demand is primarily influenced by factors such as urban pollution, work-related stress, and changing dietary habits. According to the Russian Federal State Statistics Service, the 35-39 age group is the largest demographic in Russia in 2024, comprising 6.29 million males and 6.49 million females[1]Source: Russian Federal State Statistics Service, "Population of the Russian Federation by Gender and Age", rosstat.gov.ru. This group’s increasing focus on scalp health has led to higher spending on treatments for thinning hair, dandruff, and damage repair. The prevalence of these issues among millennials has resulted in a greater willingness to invest in hair care, boosting sales and encouraging brands to enhance their marketing efforts and expand product portfolios. Younger consumers, in particular, are leaning towards premium products, often trying high-end solutions that deliver targeted results for specific hair and scalp concerns. Domestic brands like Time To Grow, which specializes in trichological solutions, are leveraging this trend and have expanded their clinical partnership network throughout 2024. Additionally, social media significantly amplifies awareness of hair health, driving demand for scientifically-formulated products tailored to individual needs, moving away from generic care routines.

Greater demand for premium and customized hair care

Russian consumers continue to favor premium hair care products despite economic challenges, reflecting a broader trend of selective premiumization in the retail sector. The premium segment has achieved a 3.57% CAGR, surpassing the overall market growth, as consumers increasingly prioritize quality over quantity in discretionary spending. This trend is supported by a rise in Russia's average monthly income per capita, which increased from RUB 53,579 in 2023 to RUB 63,090 in 2024[2]Source: Russian Federal State Statistics Service, "Federal State Statistics Service", rosstat.gov.ru, according to the Russian Federal State Statistics Service. Customization trends are evident through salon-exclusive professional lines and direct-to-consumer brands offering personalized formulations. The growing demand for premium and customized hair care drives market value growth beyond the average rate, fosters innovation, reshapes consumer expectations, and creates new opportunities. Both established and emerging brands are capitalizing on this trend with differentiated, high-value, and personalized offerings. The launch of Hardy Professional, a premium Russian brand, in late 2024 highlights domestic manufacturers' recognition of this opportunity. Additionally, the EAEU Technical Regulation TR CU 009/2011 reinforces premium positioning by emphasizing quality assurance requirements.

Rising demand for natural/organic formulations

In Russia, consumers are increasingly prioritizing products with natural ingredients and sustainable packaging, reflecting a broader shift towards environmental consciousness. This change has driven the natural/organic category to achieve a compound annual growth rate (CAGR) of 3.11%. Educated urban consumers, in particular, are becoming more skeptical of synthetic chemicals, further fueling this trend. Domestic brands are capitalizing on this demand by incorporating locally sourced botanical ingredients such as sea-buckthorn, birch extract, and thermal waters into their products, which helps them differentiate in the market. Faberlic, a prominent Russian manufacturer, has strategically focused on plant-extract formulations and maintains halal certification, enabling it to cater to a diverse range of consumer preferences. Additionally, the trend is supported by import substitution dynamics, as consumers increasingly explore domestic alternatives to international organic brands that were previously available. Compliance with EAEU regulatory standards ensures product safety while reinforcing claims of natural positioning, further strengthening consumer trust in these offerings.

Influence of social media and celebrity endorsements

Following restrictions on traditional media, digital marketing channels have become the key drivers of brand awareness and purchasing decisions in Russia's hair care market. With high connectivity, influencer reviews, tutorials, and testimonials now reach vast audiences instantly, strengthening brand loyalty and increasing demand for both premium and trending products. In 2023, approximately 92% of Russians were online[3]Source: World Bank, Individuals using the Internet (% of population) - Russian Federation", worldbank.org, and this growing internet penetration has significantly enhanced the impact of social media and celebrity endorsements on the hair care sector. Russians actively use social platforms, resulting in record-high brand visibility and consumer engagement. Platforms like YouTube and Instagram play a crucial role, with beauty influencers shaping consumer preferences and driving rapid product adoption through effective campaigns. Korean cosmetics brands illustrate this trend by collaborating with over 200 local beauty influencers through distribution partnerships to engage the MZ generation. Additionally, micro-influencer campaigns are proving highly effective for niche products, enabling smaller brands to compete with established players through authentic endorsements. This strategy's effectiveness is further amplified by Russia's growing e-commerce infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic sanctions constraining multinational investment | -0.7% | National, premium segments | Long term (≥ 4 years) |

| Counterfeit proliferation on online channels | -0.4% | Major e-commerce hubs | Medium term (2-4 years) |

| Rising raw-material costs | -0.5% | National | Short term (≤ 2 years) |

| Competition from at-home hair solutions | -0.3% | Urban and regional | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic sanctions constraining multinational investment

International sanctions have transformed the competitive landscape, driving major multinationals to either exit Russia or significantly scale back their operations. L'Oréal has limited its activities to its Kaluga manufacturing plant while halting retail expansion. Similarly, Unilever continues to supply essential products locally but has stopped making new investments. These restrictions have disrupted the supply of premium imported goods and restricted access to advanced formulation technologies. At the same time, they have created opportunities for domestic manufacturers and Asian suppliers, particularly from India and China, to capture market share. Parallel import mechanisms have mitigated some availability issues, albeit at higher costs due to complex logistics and currency volatility. The long-term effects will depend on geopolitical developments and potential changes to sanctions.

Rising raw material costs

Hair care manufacturers are facing mounting challenges as inflationary pressures and supply chain disruptions drive up input costs. Russia, which relies heavily on imports for its cosmetic raw materials, is particularly affected. In 2024, the situation is exacerbated by a 6.4% depreciation of the ruble against major currencies, significantly increasing the cost of imports. Additionally, interest rates have surged further, inflating financing expenses for manufacturers. A critical issue lies in sourcing specialized ingredients, such as silicones, where domestic production falls short of meeting cosmetic-grade requirements. To address this, companies like Russo Chemie have expanded their supplier networks to include Asian alternatives. However, this strategy introduces new challenges, including inconsistencies in product quality and longer lead times, which complicate operations. These constraints are putting pressure on profit margins across all price segments. Despite this, premium brands demonstrate a higher degree of pricing flexibility, enabling them to better absorb these escalating costs compared to other segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Dominance Faces Styling Innovation

Shampoo continues to lead the market, holding a 41.05% share in 2025. Shampoos fulfill universal needs such as cleansing and scalp health, appealing to all demographics, regardless of gender, age, or hair type. Additionally, the market's segmentation into anti-dandruff, cosmetic, dry, and herbal/organic shampoos caters to specific and growing consumer demands. On the other hand, hair styling products represent the fastest-growing category, achieving a 2.92% CAGR through 2031, driven by increased style awareness and the influence of professional salons on consumer preferences. Consumers are increasingly opting for premium conditioners, particularly those offering intensive repair for damaged hair. Millennials, dealing with stress-related hair issues, are turning to hair loss treatments, with brands like Time To Grow expanding their trichological product lines. While hair colorants face competition from professional salons, they remain relevant by emphasizing the convenience of at-home use.

The growth of the styling segment reflects lifestyle changes, as Russian consumers, inspired by social media, embrace diverse hair textures and styles. Brands like SEKTA have expanded their styling portfolios, introducing multifunctional products that combine treatment benefits with styling hold and texture. Urban professionals, often short on time, are driving demand for niche products like dry shampoos and leave-in treatments. Compliance with EAEU Technical Regulation TR CU 009/2011 ensures product safety across all categories while fostering innovation in formulations that distinguish premium products from mass-market alternatives.

By Category: Synthetic Dominance Challenged by Natural Growth

Synthetic and conventional formulations hold a 71.60% market share in 2025, highlighting their affordability and established consumer trust. Synthetic hair care products are generally more budget-friendly than natural or organic alternatives, making them accessible to a broader range of income groups. However, natural and organic products are experiencing significant growth, with a projected 3.02% CAGR through 2031. This trend reflects a gradual shift in consumer preferences toward ingredient transparency and environmental sustainability. The natural segment benefits from the use of domestic botanical resources and the incorporation of traditional Russian remedies into modern formulations. Established brands like Natura Siberica have built credibility in this space, while newer players focus on locally-sourced ingredients to differentiate themselves from imported products.

Digital platforms are accelerating consumer education, driving the adoption of natural products, particularly among millennials who prioritize ingredient safety and environmental impact in their purchasing decisions. While the synthetic category retains advantages in affordability and consistent performance, key factors for mass-market penetration, hybrid formulations are gaining traction. These blends combine the performance of synthetics with the appeal of natural ingredients. Additionally, Rospotrebnadzor has increased its oversight of cosmetic marketing claims, ensuring authentic natural positioning and preventing misleading communications.

By Price Tier: Mass Appeal Persists as Premium Accelerates

Mass-market products hold a 69.10% share in 2025, highlighting their importance to price-sensitive consumers dealing with economic uncertainties. At the same time, premium offerings are set to grow at a 3.46% CAGR through 2031, as affluent consumers increasingly value quality over cost. This dynamic reflects broader trends in Russian retail, where mid-market products face challenges from both ends of the spectrum. The mass segment capitalizes on domestic manufacturing and simplified formulations, maintaining affordability despite rising input costs. Retailers like L'Etoile are expanding their premium Korean brand portfolios to attract consumers willing to trade up for superior formulations.

Premium growth is driven by salon-exclusive professional lines, imported specialty brands, and domestic innovations targeting specific hair concerns. The segment's stability during economic downturns underscores its appeal to loyal users who view hair care as a necessity rather than a luxury. Mandatory product marking requirements, set to begin in 2025, may disproportionately affect smaller premium brands due to compliance costs, potentially consolidating market share among well-established players with greater resources.

By Distribution Channel: Digital Transformation Accelerates Traditional Decline

In 2025, supermarkets and hypermarkets hold a 37.10% share of the distribution market due to their convenience and extensive product offerings. These outlets provide a comprehensive range of hair care products, including shampoos, conditioners, treatments, and styling aids, enabling shoppers to purchase hair care items alongside groceries and daily essentials. This one-stop shopping experience drives frequent purchases. Online retail stores are experiencing the fastest growth, with a 4.14% CAGR projected through 2031, reflecting the rapid adoption of digital platforms by Russian consumers. This growth is primarily driven by the dominance of marketplaces like Wildberries and Ozon. Specialty stores face challenges from both the efficiency of hypermarkets and the growing preference for online shopping. On the other hand, convenience stores remain significant for impulse buys and urgent needs.

The expansion of e-commerce is extending beyond major cities, fostering growth in regional markets, particularly in online FMCG purchases. This shift is providing smaller cities, previously underserved by specialty retailers, with greater access to premium brands. Other channels, such as direct sales and professional salons, continue to thrive by offering personalized service and expert advice, advantages that online platforms cannot fully replicate. However, the mandatory digital marking requirements under the "Chestny ZNAK" system will impact all distribution channels. Smaller retailers, in particular, may face difficulties complying with these traceability standards due to limited technological resources.

Geography Analysis

Russia's hair care market demonstrates significant regional concentration, with Moscow and St. Petersburg leading in premium product consumption despite representing only 15% of the national population. Affluent consumers in the capital region, supported by higher disposable incomes and exposure to global beauty trends through digital platforms, drive demand for imported and premium domestic brands. Regional markets are growing at a faster pace, aided by the expansion of e-commerce distribution networks and a gradual increase in local purchasing power. The Krasnodar region, in particular, is experiencing dynamic growth, driven by the rise in beauty salon establishments and the expansion of spa resorts fueled by tourism development.

The Siberian and Far Eastern regions offer untapped potential for hair care brands willing to invest in distribution infrastructure and adapt products to suit local climate conditions. Consumers in these areas prefer practical and affordable solutions to address the effects of harsh weather on hair health. The mandatory product marking system, set to be implemented in 2025, may initially challenge remote regions due to technological infrastructure gaps. However, government support for digital transformation is expected to gradually resolve these issues. Currency fluctuations impact regional markets differently, with border regions experiencing higher price volatility due to cross-border trade dynamics. Economic development disparities across Russian regions create distinct consumer segments, necessitating tailored marketing strategies and product positioning. Urban centers focus on convenience and premium offerings, while smaller cities prioritize value and multifunctional products. Regional regulatory compliance remains consistent under federal oversight by Rospotrebnadzor, although local market dynamics influence enforcement priorities and consumer education initiatives.

Competitive Landscape

The Russian hair care market has shifted to a more moderately fragmented landscape, largely due to the exit of major international players following sanctions. Now, domestic manufacturers find themselves in competition with Asian suppliers. This shift has paved the way for nimble brands that swiftly adapt to evolving consumer tastes and regulatory landscapes. The market has seen a notable decrease in concentration, with no single entity holding more than a 15% share. This democratization allows smaller brands to carve out regional niches and establish a strong foothold. In this dynamic environment, technology adoption stands out as a pivotal differentiator, especially in areas like e-commerce, digital marketing, and supply chain management.

Key players in the Russian hair care arena encompass L'Oreal SA, Natura Siberica, Estel Professional, Unilever PLC, and Procter Gamble Company. While hair wash products dominate, hair masks have also found favor among Russian women, who typically lean towards products with natural ingredients. Recently, brands emphasizing natural and organic formulations have surged in popularity. Notable names like Natura Siberica, Organic Shop, and White Agafia have made their mark with products such as Natura Siberica's Northern Cloudberry Shampoo, Organic Shop's Golden Orchid Color Conditioner, and Natura Siberica's Fresh Spa Birch Tree Strengthening Shampoo. These key players are not resting on their laurels; they're pushing for larger market shares through relentless product innovation and significant investments in research and development, especially for niche offerings. Given these dynamics, the industry's competitive rivalry is poised to remain high in the coming years.

New entrants are shaking up the status quo, harnessing direct-to-consumer strategies and the power of social media to upend traditional distribution models. Korean brands, for instance, have adeptly navigated the market, leveraging influencer collaborations and a strong marketplace presence. Yet, opportunities abound, especially in professional salon channels, organic formulations, and specialized treatments targeting hair loss and scalp health. Domestic players are not just participants but innovators, as evidenced by patent filings. Companies like Faberlic, for instance, boast over 34 patents and churn out 200+ unique formulas each year. However, the path isn't without hurdles. Regulatory compliance under EAEU standards poses challenges for newcomers, simultaneously fortifying the position of established players with their robust quality systems.

Russia Hair Care Industry Leaders

-

L'Oréal S.A.

-

Unilever PLC

-

Natura Siberica

-

Estel Professional

-

The Procter and Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: HanKook Cosmetics, a leading name in the Korean cosmetics industry, has established a distribution partnership with BerryLink to expand into the Russian market. The company is utilizing the reach of over 200 local beauty influencers to connect with the MZ generation, promoting Olive Young brands such as Tonefit Sun and Ours.

- January 2024: The Love Co., an Indian beauty brand, has entered the Russian market by partnering with Kristina Bykova. The brand introduced specialized skincare and hair treatments designed for Russian consumers, which are distributed through Wildberries and Ozon marketplaces.

- December 2022: In Russia, Nomica, a new line of hair products, was launched. The brand claimed that its functional formulae address the specific needs of different hair types while maintaining the product's natural beauty.

- October 2022: Henkel unveiled its new hair care brand, SalonLab and Me, introduced a trio of products: a shampoo, conditioner, and hair mask.

Russia Hair Care Market Report Scope

Hair care is an umbrella term for various aspects of hygiene and cosmetology that affect hair that grows on the scalp.

The Russian Hair Care Market is Segmented by Product Type (Shampoo, Conditioner, Hair Loss Treatment Products, Hair Colorants, Hair Styling Products, Perms and Relaxants, and Other Product Types), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Pharmacies/Drug Stores, Online Retail Stores, and Other Distribution Channels). The report offers market size and values in (USD Million) during the forecast years for the above segments.

By Product Type

| Shampoo |

| Conditioner |

| Hair Loss Treatment Products |

| Hair Colorants |

| Hair Styling Products |

| Other Product Types |

By Category

| Synthetic/Conventional |

| Natural /Organic |

By Proce Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarkets/ Hypermarkets |

| Specialty Stores |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Shampoo |

| Conditioner | |

| Hair Loss Treatment Products | |

| Hair Colorants | |

| Hair Styling Products | |

| Other Product Types | |

| By Category | Synthetic/Conventional |

| Natural /Organic | |

| By Proce Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarkets/ Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Russia Hair Care market in 2026?

The market is valued at USD 2.38 billion in 2026 and is projected to grow at a 2.50% CAGR to 2031.

Which product category holds the biggest share?

Shampoo remains the largest segment with 41.05% revenue in 2025.

What drives premium hair-care demand in Russia?

Affluent urban consumers seek quality formulations and salon-grade customization, pushing the premium tier to a 3.46% CAGR.

How fast is online sales of hair care expanding?

Online retail is the fastest channel, expected to post a 4.14% CAGR through 2031 as platforms like Wildberries and Ozon scale nationwide.

Page last updated on: