Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.32 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

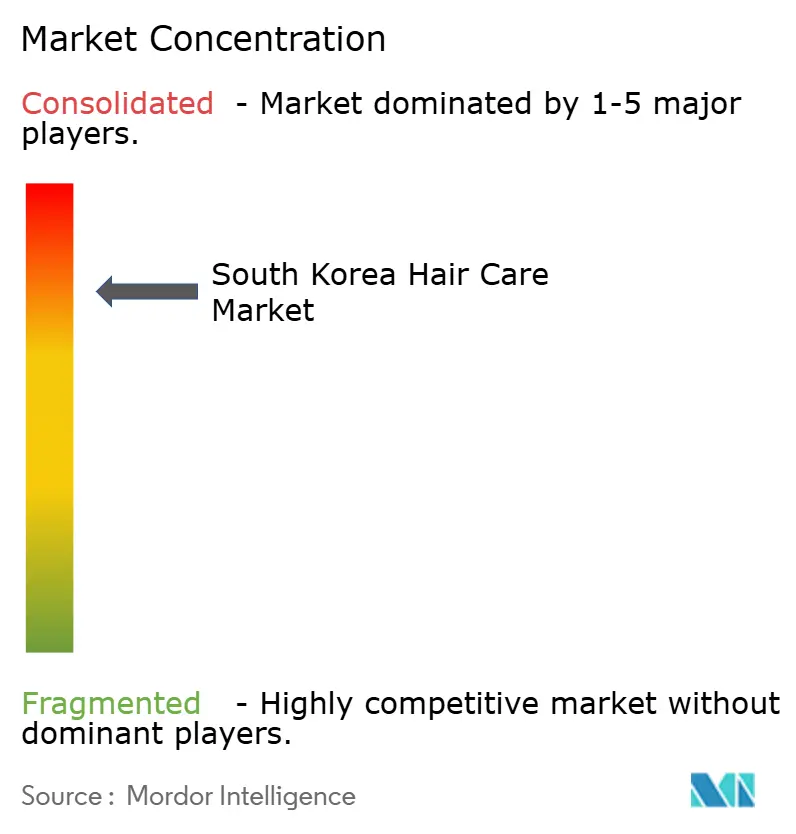

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Hair Care Market Analysis by Mordor Intelligence

The South Korea hair care market size was valued at USD 1.32 billion in 2025 and estimated to grow from USD 1.39 billion in 2026 to reach USD 1.81 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031). South Korean shoppers have begun treating the scalp as an extension of facial skin, which is pushing brands to embed microbiome-friendly actives, AI diagnostics, and genetic personalization into everyday wash-off formulas. Younger adults now initiate 70% of hair-loss treatments, amplifying preventive demand and accelerating patent activity that gives domestic suppliers a major share of global filings. Online retail already commands more than three-fifths of sales and continues to expand on the back of mobile purchasing, live-commerce, and cross-border tourism, while clean-label expectations are reshaping ingredient strategies after the 2025 ISO 16128 shift. Merger and acquisition worth KRW 3.176 trillion in 2025 compressed the value chain, allowing cash-rich conglomerates and private-equity funds to lock in ODM capacity, packaging technology, and salon assets, thereby tightening competitive barriers for indie challengers.

Key Report Takeaways

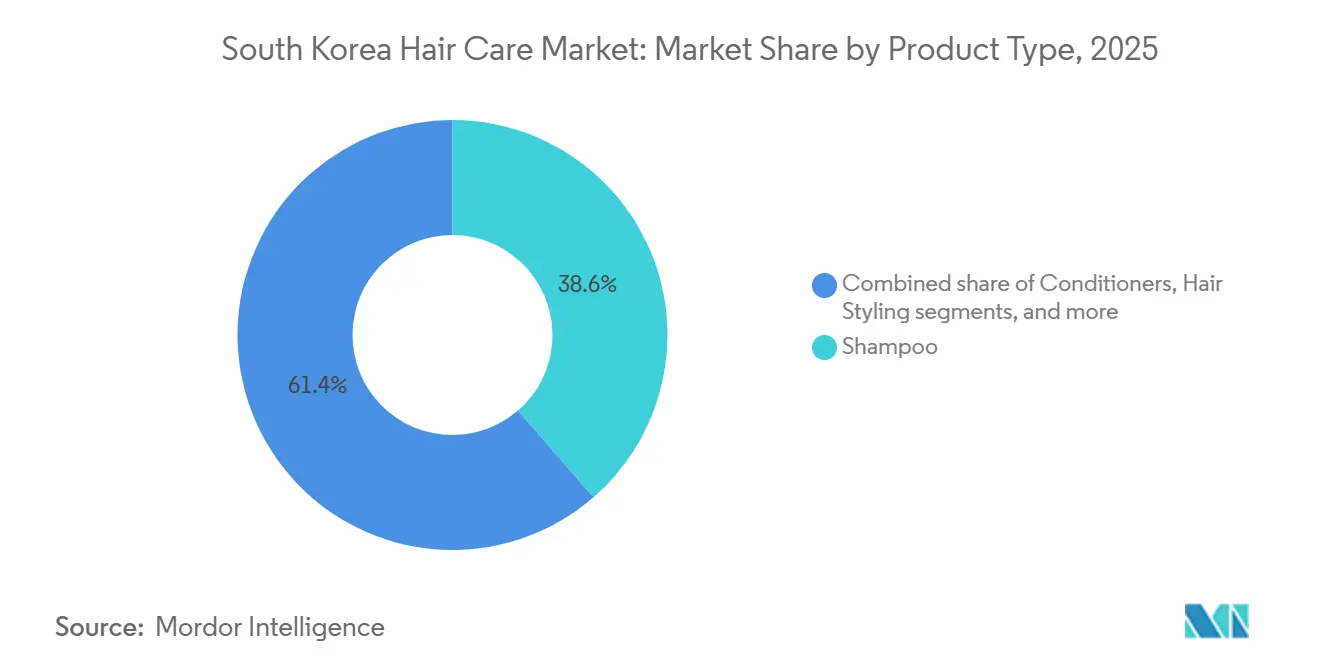

- By product category, shampoo led with 38.62% of South Korea hair care market share in 2025, whereas hair styling products are projected to advance at a 6.10% CAGR to 2031.

- By category, mass products held 72.74% of 2025 revenue, while premium offerings are forecast to expand at a 6.72% CAGR through 2031.

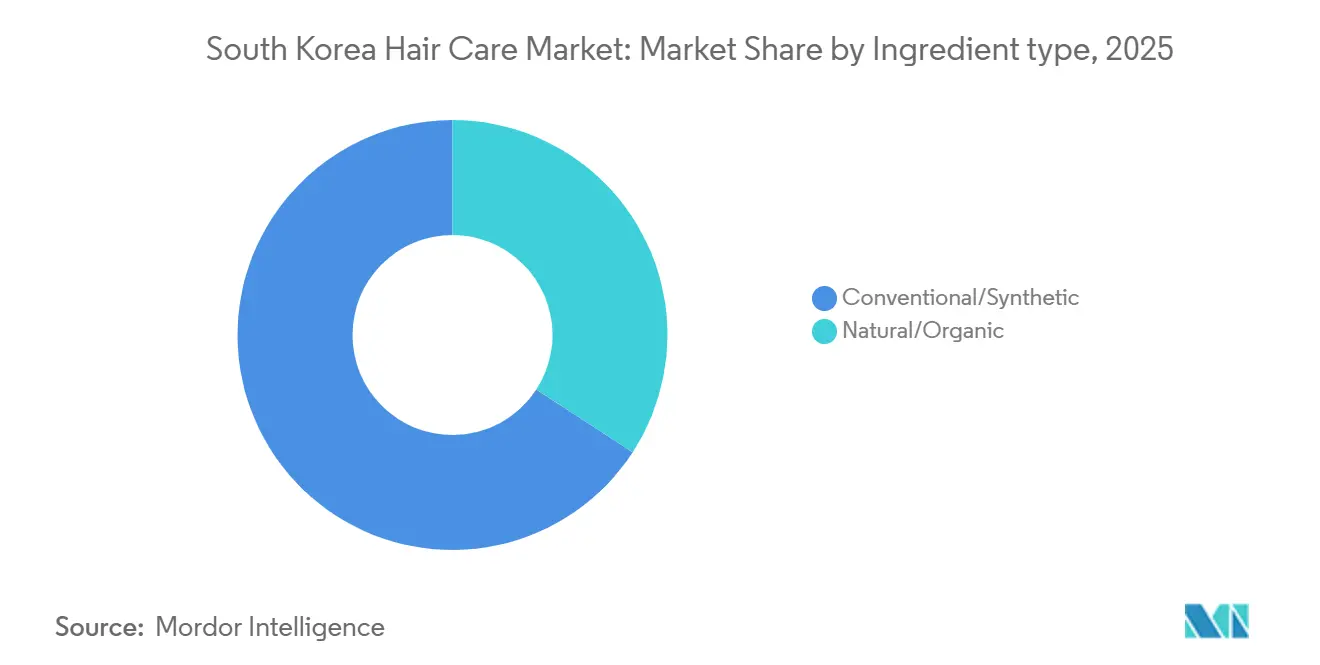

- By ingredient type, conventional formulations accounted for 65.82% of sales in 2025, yet natural and organic lines are expected to grow at a 7.08% CAGR during 2026-2031.

- By distribution channel, online retail stores captured 61.12% of sales in 2025 and are set to record a 7.39% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Hair Care Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT CAGR FORECASTS | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Influence of social media and celebrity endorsement | +1.2% | National, with spillover to global K-beauty markets | Short term (≤ 2 years) |

| Strong demand for products formulated with clean label ingredients | +1.0% | National, with early adoption in Seoul metropolitan area | Medium term (2-4 years) |

| Rising awareness of scalp health | +0.8% | National, with higher penetration in urban centers | Medium term (2-4 years) |

| Growing demand for personalized hair care solutions | +0.7% | National, concentrated in tech-savvy demographics | Long term (≥ 4 years) |

| Growth of men’s grooming segment | +0.6% | National, with accelerated growth in major cities | Medium term (2-4 years) |

| Rapid expansion of e-commerce and D2C channels | +0.9% | National, with rural market penetration increasing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Influence of social media and celebrity endorsement

Instagram and Facebook have become the primary platforms for users, from teenagers to those in their 40s, to discover hair care products, significantly influencing their purchase intentions. Data from 2024, released by South Korea's Ministry of Science and ICT, reveals that 41% of South Koreans engage with social network services over 20 times a week[1]Ministry of Science and ICE, " 2024 Survey on Internet Usage", msit.go.kr. Across various platforms, consumers are increasingly drawn to online content, where celebrity endorsements and influential marketing play a pivotal role in capturing their attention. This evolution marks a significant shift from conventional advertising methods. Research highlights the importance of content uniqueness and strong community connections, especially among K-beauty creators, in shaping the emotional expectations of global consumers. Trends from South Korea's social media are swiftly gaining worldwide attention, underscoring the global resonance of Korean fashion and beauty content. The rise of live commerce, intertwined with social media, is reshaping purchasing behaviors, enabling real-time interactions between buyers and sellers, something traditional e-commerce struggles to achieve. This dynamic not only enriches the shopping journey but also empowers brands to present their products in a more engaging and customized way, amplifying consumer interest and driving conversions.

Strong demand for products formulated with clean label ingredients

Consumer behavior has pivoted towards ingredient-centric purchasing, a shift propelled by platforms like Hwahae that champion detailed ingredient analysis and consumer education. Concurrently, the Ministry of Food and Drug Safety has intensified its regulatory scrutiny, banning ingredients such as hydroquinone, select parabens, triclosan, and benzophenone, citing health and environmental concerns. This regulatory landscape favors companies that swiftly pivot, reformulating with safer alternatives. This is evident in the rising popularity of ingredients like Centella Asiatica, Niacinamide, and Mugwort in hair care. Consumers are now willing to pay a premium for clean-label products, signaling a lifestyle shift where beauty purchases resonate with broader health and environmental values. Established manufacturers are pouring investments into sourcing natural ingredients and ensuring transparent labeling. This trend also carves out opportunities for smaller brands that can showcase superior ingredient safety profiles.

Rising awareness of scalp health

As the environment changes and issues like dandruff and greasy scalps become more prevalent, consumers in the country are becoming increasingly aware of scalp health. This growing awareness is driving demand for specialized scalp management products and programs that cater to individual needs. Companies that can scientifically validate their treatments for specific scalp concerns stand to gain significantly, as consumers are actively seeking solutions backed by research and proven results. Leading this movement, Kolmar Korea has introduced AI-driven diagnostic tools that identify 16 variants of androgenetic alopecia through scalp biomarkers, offering a more precise approach to addressing scalp issues. The intensified emphasis on scalp health highlights the importance of trichologist expertise and specialized scalp care services, as consumers increasingly value professional guidance. To succeed in this burgeoning market, hair care brands are urged to invest in educational initiatives, such as awareness campaigns and informative content, and establish professional collaborations with experts to build trust and credibility.

Growing demand for personalized hair care solutions

Brands harness consumer data, ingredient science, and agile manufacturing to create solutions tailored to individual hair types, scalp conditions, and styling preferences. This trend reflects a broader consumer push for personalization across various product categories. Younger demographics, in particular, now view customization as a standard expectation rather than an added luxury. Although the economic model for personalized hair care requires substantial upfront investments in technology and data systems, it presents brands with an opportunity to gain a competitive advantage. By doing so, they can secure customer loyalty and justify premium pricing. Companies that skillfully embrace personalization not only enhance customer lifetime value but also benefit from reduced acquisition costs, driven by increased satisfaction and organic word-of-mouth referrals.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECASTS | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Health concerns over chemical ingredients | -0.5% | National, with heightened sensitivity in urban markets | Medium term (2-4 years) |

| Proliferation of counterfeit products | -0.3% | National, concentrated in online marketplaces | Short term (≤ 2 years) |

| High market saturation and brand competition | -0.4% | National, particularly intense in premium segments | Long term (≥ 4 years) |

| Stringent regulations on ingredients | -0.2% | National, with compliance costs affecting smaller players | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns over chemical ingredients

In response to rising concerns over chemical ingredient safety, the Ministry of Food and Drug Safety has taken decisive regulatory actions. Recently, they enforced the removal of PABA-containing products from e-commerce platforms, citing potential risks of liver and kidney damage[2]Ministry of Food and Drug Safety, "PABA-Containing Hair, Skin, and Nail Products Removed in South Korea's E-Commerce", mfds.go.kr. South Korea's regulatory stance has grown more precautionary, often setting standards that are stricter than many global counterparts. Notably, the country has implemented bans on substances like formaldehyde, coal tar dyes, and certain UV filters. Such stringent measures pose challenges for manufacturers, especially those catering to both domestic and international markets, as they grapple with compliance costs and the need for reformulation. While the push for ingredient transparency has empowered consumers, it has also heightened anxieties surrounding chemical safety. This heightened concern can influence purchasing decisions, even for ingredients that have received regulatory approval. As a result, companies find themselves in a delicate balancing act: meeting efficacy demands while addressing safety perceptions. This often necessitates substantial Research and Development investments to craft alternative formulations that uphold product performance without compromising on safety concerns.

Proliferation of counterfeit products

The Ministry of Food and Drug Safety actively combats counterfeit and non-compliant products on e-commerce platforms, underscoring the persistent challenge of upholding product integrity in the digital marketplace. While the swift expansion of online sales channels has opened doors for legitimate brands, it has equally paved the way for counterfeit products, jeopardizing brand reputation and eroding consumer trust. The global reach of e-commerce complicates enforcement, necessitating collaboration among domestic regulators, international customs, and platform operators to effectively counteract counterfeit distribution. In this landscape, consumer education is paramount; buyers must hone their skills to discern authentic products and validate seller credentials. Premium brands, often commanding higher prices, bear the brunt of this counterfeit surge, as fraudsters keenly target products with pronounced price disparities between genuine and fake versions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shampoo Dominance Faces Styling Innovation

In 2025, shampoo dominates the market with a commanding 38.62% share, highlighting its essential role in daily hair care across all demographics. Its widespread usage stems from its fundamental role in maintaining hair hygiene and health, making it a staple product in personal care routines. Hair styling products, however, are rapidly gaining ground, boasting a 6.10% CAGR projected through 2031. This growth is driven by evolving consumer preferences for versatile styling and the global hair fashion industry's nod to K-beauty trends. The rising popularity of the styling segment reflects a broader lifestyle evolution, with consumers increasingly valuing products that enable quick style transitions for diverse occasions. This trend gains significance in today's world, where remote work and an amplified social media presence heighten the demand for at-home styling. Additionally, the increasing availability of innovative styling products, such as heat protectants and multi-functional sprays, further supports this segment's growth.

Conditioners and hair colorants maintain a steady demand as established segments, but the "other product types" category is buzzing with innovation. This evolving segment now encompasses scalp treatments, hair masks, and specialized serums, tackling concerns that go beyond basic cleansing and conditioning. These products address issues such as scalp health, hair damage repair, and hydration, catering to a growing consumer base seeking targeted solutions. Moreover, the fusion of hair care with skincare principles has ushered in treatments that apply the same scientific attention to hair and scalp as is standard in facial skincare. This trend reflects a shift towards holistic hair care, where consumers prioritize products that combine functionality with advanced formulations to achieve healthier and more manageable hair.

By Category: Premium Segment Drives Value Growth

In 2025, mass products command a dominant 72.74% share of the market, highlighting South Koreans' value-driven purchasing habits, irrespective of their income levels. These products cater to a broad audience by offering affordability and functionality, making them a staple in the daily lives of consumers. On the other hand, premium products are charting a growth path, expanding at a notable 6.72% CAGR. This trajectory indicates a pronounced shift towards premiumization, with consumers prioritizing quality, efficacy, and brand prestige, often at the expense of price considerations. This evolution resonates with the nation's economic journey, where rising disposable incomes are increasingly directed towards high-end personal care products, reflecting a growing willingness to invest in superior offerings.

The rise of the premium segment underscores a discerning consumer base eager to invest in products that deliver tangible results or unique experiences. This shift is driven by heightened awareness of product benefits, increased exposure to global beauty trends, and a desire for self-care indulgence. Brands like MEDIPEEL are capitalizing on this trend, with their 'Extra Super 9 Plus Glow Lifting Wrapping Mask' selling over 200,000 units monthly, and their pore care line boasting annual sales exceeding USD 7.83 million in 2024. Additionally, the premium segment benefits from K-beauty's global reputation, as international recognition of Korean beauty innovations amplifies domestic demand for premium products. This global acclaim not only enhances consumer trust but also reinforces the perception of premium products as aspirational and worth the investment.

By Ingredient Type: Natural Transition Accelerates

In 2025, the conventional/synthetic ingredient segment commands a significant 65.82% market share. Meanwhile, the natural/organic segment is on an upward trajectory, boasting a 7.08% CAGR from 2026 to 2031. This evolving landscape underscores a shift in consumer preferences, largely influenced by a growing awareness of ingredient safety and environmental issues. Notably, the surge in the natural segment is driven by a rising appetite for vegan hair care products, especially among the youth. Consumers are increasingly prioritizing products that align with their values, such as sustainability and cruelty-free practices, further fueling the demand for natural and organic alternatives.

Responding to this trend, South Korean manufacturers are turning to plant-based substitutes. They're replacing traditional synthetic ingredients with innovations like jojoba-based silicones and plant-derived keratin. These alternatives not only cater to consumer demand but also align with global sustainability goals, making them a strategic choice for manufacturers. A testament to this industry shift is Dooricosmetics, heralded as Korea's inaugural traditional oriental herbal hair care brand. They've embraced this evolution, infusing herbal extracts and patented components into their vegan-certified offerings. Furthermore, the Ministry of Food and Drug Safety (MFDS) has set forth regulations governing natural and organic cosmetics. These encompass detailed directives on ingredient sourcing and labeling, offering a structured pathway for product development in this burgeoning segment, as highlighted by the U.S. Department of Commerce.

By Distribution Channel: Digital Platforms Reshape Retail Landscape

In 2025, online retail stores are set to command a dominant 61.12% share of South Korea's hair care market distribution, boasting the highest projected CAGR of 7.39% through 2031. This digital shift has revolutionized the way consumers explore and buy hair care products, with social media and e-commerce platforms emerging as pivotal sources for product insights and purchasing choices. The convenience of online shopping, coupled with the availability of detailed product reviews and personalized recommendations, has further fueled this growth, making it a preferred channel for a wide range of consumers.

Specialty stores continue to play a vital role, especially for premium and professional products. However, they're increasingly embracing online channels and digital tools to bolster their physical presence. These stores are leveraging omnichannel strategies to provide a seamless shopping experience, combining the tactile benefits of in-store shopping with the convenience of online platforms. Niche and emerging brands find particular advantage in the e-commerce landscape, allowing them to connect with targeted consumer segments more efficiently than through traditional retail avenues. This digital edge has ushered in fresh avenues for market innovation, hastened product development timelines, and refined consumer engagement tactics throughout the hair care sector. Additionally, the integration of advanced analytics and AI-driven tools is enabling brands to better understand consumer preferences and tailor their offerings accordingly, further driving growth in the market.

Geography Analysis

The South Korean hair care market benefits from a densely populated urban corridor where 50% of residents live in the Seoul metropolitan region. High smartphone penetration, exceeding 95% simplifies mobile engagement, allowing brands to test innovations in Seoul’s trend-sensitive districts before scaling nationally, according to the Statistics Korea data from 2023. Provincial cities such as Busan, Daegu, and Gwangju form secondary consumption centers, each exhibiting nuanced preferences shaped by local culture and climate. Busan’s coastal humidity increases interest in anti-frizz and UV-protection SKUs, while inland Daegu’s dry winters support hydrating scalp tonics.

Uniform broadband coverage and robust courier networks diminish access disparities, enabling rural shoppers to receive next-day deliveries for niche products once confined to flagship Seoul boutiques. Government investment in fifth-generation networks further expands live-commerce reach, fostering real-time interactions between countryside audiences and urban influencers. Tourism flows re-open, and duty-free channels inside Incheon International Airport become live showrooms where foreign visitors trial hair care innovations before exporting them abroad. Although domestic consumption anchors demand, export-oriented brands incorporate feedback from Chinese, Japanese, and Southeast Asian tourists to fine-tune scent profiles and packaging languages.

Geo-economic strategies also matter; firms position distribution centers near ports to streamline order fulfillment for both domestic and overseas markets. Environmental regulations vary slightly by municipality, influencing ingredient disclosures or plastic use thresholds. Seoul’s “Zero Waste” pilot prompts city-wide adoption of refill stations, nudging brands to test circular packaging. Lessons learned in the capital’s regulatory sandbox often inform nationwide rollouts, illustrating the feedback loop between local governance and market behavior in the South Korean hair care market.

Regulatory Landscape

South Korea hair care products are regulated under the Cosmetics Act, with oversight by the Ministry of Food and Drug Safety (MFDS). Hair care items positioned as functional cosmetics (for example, products tied to hair color change or other defined functions) face MFDS examination or reporting requirements tied to safety and efficacy, alongside compliance with MFDS-administered safety standards and functional-cosmetic evaluation rules that govern ingredient restrictions and product testing expectations.

Recent updates add compliance pressure and also streamline certain pathways. In December 2025, MFDS Notification No. 2025-88 revised the Regulation on Evaluation of Functional Cosmetics, adding "solids" to exempted product types for efficacy data submission to speed access for qualifying formats. In May 2026, Amendment No. 21709 to the Cosmetics Act was promulgated, introducing rules for transparency around AI-generated cosmetics advertisements, with enforcement taking effect in November 2026, pushing brands and platforms to tighten claim substantiation and disclosure practices in digital and live-commerce environments.

Competitive Landscape

The South Korean hair care market shows high concentration, with domestic companies Amorepacific Corporation and LG Household and Health Care Ltd of LG Corp. as the primary market leaders. These companies maintain their positions through aggressive promotional activities while competing against international brands. The market has seen increased competition from brands such as Nature Republic, which has gained market share through product expansion and consumer-friendly packaging.

Hyundai Pharm's launch of Dexnoxyl, South Korea's inaugural over-the-counter hair-loss remedy, underscores the evolving competitive landscape as more pharmaceutical firms make their market entry. This development highlights the growing interest of pharmaceutical companies in diversifying their product portfolios to cater to consumer health needs. Companies are increasingly leveraging technology, particularly AI-driven personalization and diagnostic features, to carve out a distinct edge in the market. These advancements enable businesses to offer tailored solutions, enhancing customer satisfaction and driving market growth.

At CES 2025, Amorepacific showcased its tech prowess, unveiling the Wanna-Beauty AI for bespoke product suggestions and an AI-driven Skin Analysis and Care Solution, developed in collaboration with Samsung. The Wanna-Beauty AI leverages advanced algorithms to analyze consumer preferences and recommend products tailored to individual needs, while the AI Skin Analysis and Care Solution provides precise skin diagnostics and customized care plans. By prioritizing personalization via data analytics and AI, companies can now craft products that cater to unique consumer needs, reshaping the competitive landscape and setting new benchmarks for innovation in the market.

South Korea Hair Care Industry Leaders

-

Amorepacific Corporation

-

LG Corporation

-

Kao Corporation

-

The Procter & Gamble Company

-

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Scalp care and hair-loss adjacent claims continue to pull more R&D and funding into hair care, creating whitespace for functional, skinification-led products and supporting tools. South Korea held 42.9% (576 cases) of global patent applications for hair loss cosmetics between 2002 and 2023, reinforcing the country as an innovation base for hair-loss cosmetics and related actives. In March 2026, scalp care brand Refield (Konstant) secured KRW 11 billion in Series B funding led by Korea Investment Partners, with participation from Amorepacific, Hana Ventures, and KT Investment, signaling active capital formation around scalp-health propositions that can be scaled through online-first distribution.

Beauty-tech enablement is becoming more explicit in industry and government activity, widening opportunities in AI-led diagnostics, claims support, and manufacturing automation that translate into differentiated hair care programs and higher-value bundles (device plus topical regimen). MFDS held discussions in May 2026 with beauty companies on AI-based skin and scalp analysis and related regulatory improvements, aligning product development with clearer compliance expectations for tech-assisted personalization. On the supply side, ODM and ingredient ecosystems are building hair care-specific capabilities, illustrated by Kolmar Korea expanding its haircare R&D workforce by about 40% in 2025 to strengthen functional hair product development, while a phased cosmetics safety assessment system is being prepared for implementation starting in 2028, incentivizing earlier investment in safety dossiers, substantiation, and compliant digital claims workflows.

Recent Industry Developments

- July 2026: Kao Corporation announced the Liese hair color series featuring its newly developed H-Linx TECH, with a rollout across seven Asian countries and regions starting in August 2026. The move extends a Japan-origin brand into a broader regional footprint, increasing competitive intensity in colorants and damage-care positioning for South Korea-relevant assortments.

- March 2026: Amorepacific reported developing a novel peptide (Tripeptide-132) using AI and molecular modeling to reinforce hair keratin, with findings published in the International Journal of Cosmetic Science. The work strengthens the companys hair science credentials and supports premium, scalp-and-hair longevity narratives that can be commercialized across mass and premium lines.

- August 2024: LG Household and Health Care announced development of the Ultra Atomizing Hairbrush, a smart device that uses sensors to adjust leave-in treatment application based on brushing patterns. This highlights growing device-plus-formula ecosystems in hair care and builds a pathway for personalized routines that integrate diagnostics and dosing.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers the consumer purchase value of hair care products sold in South Korea across everyday cleansing, conditioning, styling, coloring, and related hair care needs, measured across offline and online channels.

Scope exclusions: This sizing does not include in-salon hair services or procedures, and it also excludes devices such as dryers, irons, and electric trimmers.

Segmentation Overview

-

Product Type

- Shampoo

- Conditioner

- Hair Colorants

- Hair Styling Products

- Other Product Types

-

Category

- Premium Products

- Mass Products

-

Ingredient Type

- Natural and Organic

- Conventional/Synthetic

-

Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with setting a clear market boundary and building context that could be checked and repeated. We used public sources for macro anchors and trade direction, such as Statistics Korea (KOSIS), the Korea Customs Service, and the Bank of Korea, to align inflation and currency timing that affect USD normalization.

To keep category assumptions realistic, we reviewed guidance from the Ministry of Food and Drug Safety on relevant product and claim classifications, and we used trade bodies such as KOTRA and KITA to map the broader beauty pipeline. Company annual reports, investor presentations, and reputable press were used to track channel shifts and pricing tiers. When disclosures were limited, we supplemented with selective paid subscriptions for company financials and intelligence plus patent databases. The desk sources listed here are illustrative only, and we used many additional references for data collection, cross-checking, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating what actually sells in South Korea, how products are priced, and how the channel mix is shifting. These points can materially change the final market value, so we spoke with manufacturers, distributors, retail and e-commerce leaders, and category managers. Follow-up checks were used to confirm assumptions on premium versus mass split, online share, and the adoption curve of natural and organic positioning in hair care.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 16% | |

| Mid tier: 48% | Functional/Unit leaders: 38% | |

| Smaller Players: 22% | Managers: 46% |

Market-Sizing & Forecasting

Sizing used a top-down and bottom-up logic. We reconstructed South Korea consumer spend patterns and category weights into a hair care demand pool, then refined those inputs using product and channel shares validated through interviews. We also corroborated outputs with selective bottom-up approximations, such as sampled price-per-unit times estimated unit movement by channel, plus supplier-and-distributor roll-ups where disclosures allow, to keep totals realistic.

The model inputs include indicators such as online retail share of hair care sales, premium versus mass price gaps, product mix across shampoo, conditioner, styling products, and colorants, and the expected shift toward natural and organic offerings. Trade signals and currency timing were used mainly as reasonableness checks rather than direct proxies for consumption, because imported and locally produced products can behave differently in a given year. For forecasting, we applied scenario analysis using short trend models. Growth direction was guided by channel expansion, pricing progression, and category trading-up, then adjusted based on what primary respondents expected for promotions and portfolio changes. When company-level revenue splits were unavailable, we handled gaps with conservative allocation rules tied to observable channel presence and product positioning, followed by re-checks with interviewees.

Data Validation & Update Cycle

Results were validated through multiple checks. We started with internal consistency tests across product totals, channel totals, and implied pricing, then compared outputs against macro trends and trade direction. If an output looked off, we reopened the underlying assumptions and reworked the calculations, and re-contacted respondents when variance could change the market total or trend line.

Before sign-off, the model and narrative go through a multi-step analyst review so the final market value can be traced back to clear inputs and calculation steps. Reports are refreshed annually, with interim updates when material events occur, such as sharp pricing shifts, channel shocks, or policy changes that affect product claims. Right before delivery, an analyst runs a final pass so clients receive the most current view available at that time.

Mordor Intelligence's South Korea Hair Care Market Market Sizing Compared With Other Published Estimates

Published market values for South Korea hair care do not always match, and the spread typically comes from differences in what is counted as hair care, which year is used as the base, and how pricing and channel mix are handled.

The table shows a noticeable gap versus larger figures. In Mordor Intelligence's model, the total is limited to retail hair care product sales in South Korea (such as shampoo, conditioner, styling products, hair colorants, and similar items) tracked by distribution channel, rather than including salon services or hair devices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.32 B (2025) | |

| Global Consultancy A | USD 2.50 B (2024) | Uses a different base year and a broader basket that can pull in specialized scalp and hair loss treatment groupings, and then applies generalized channel assumptions that may not reflect South Korea online and offline splits. |

| Industry Databook B | USD 3.00 B (2022) | Anchors the series on an earlier year and uses a higher-level split (conventional versus organic), which can leave room for adjacent personal care items to be captured inside hair care totals. |

Across the three figures, the biggest drivers are base-year timing and category inclusions, followed by how pricing is carried forward and how channel weights are applied. When the scope is kept product-led and channel-led, and when assumptions are rechecked during refresh cycles, it becomes easier to replicate the steps and explain year-to-year changes to decision-makers.

Key Questions Answered in the Report

How fast will premium hair products grow in South Korea by 2031?

Premium offerings are projected to rise at a 6.72% CAGR between 2026 and 2031.

Which channel sells the most hair care products to Korean consumers?

Online retail stores already hold 61.12% of 2025 sales and remain the fastest-growing outlet at a 7.39% CAGR.

What drives young Koreans to invest in scalp-care solutions?

Early hair-loss concerns, AI diagnostics, and genetic tests make preventive scalp care routine for consumers in their 20s and 30s.

Are Natural and Organic formulas gaining ground?

Yes, they will expand at a 7.08% CAGR after ISO 16128 replaced state certification and lowered entry costs for clean-label brands.

Page last updated on: