Go-to-Market Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

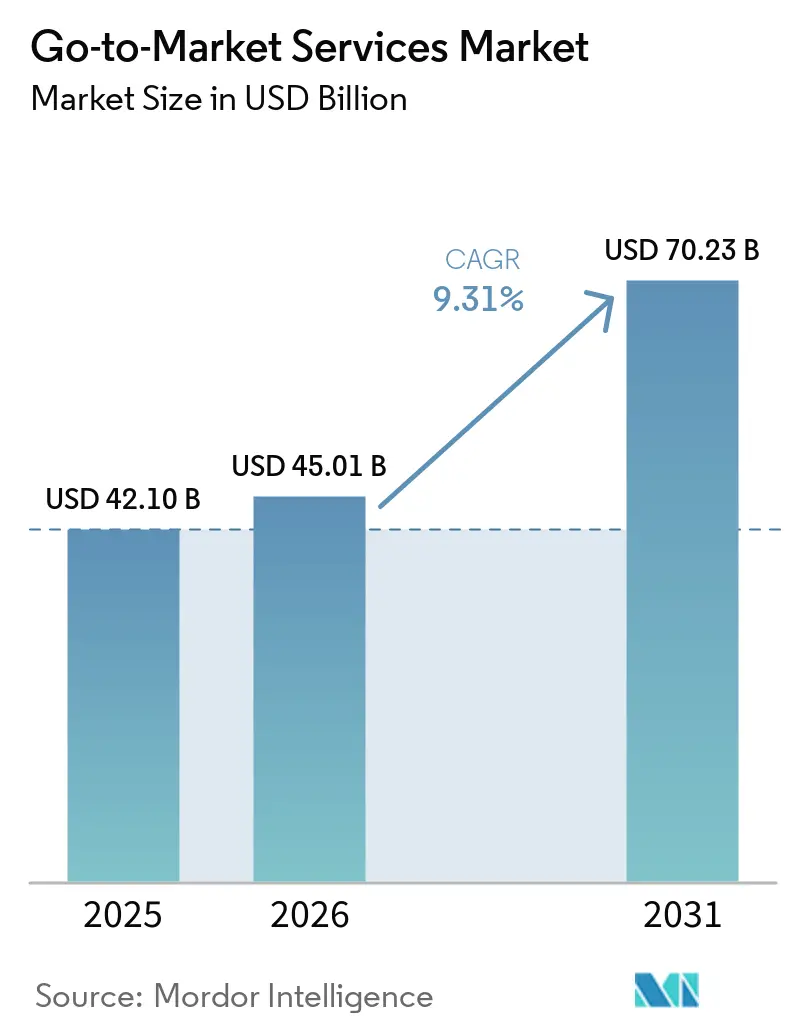

| Market Size (2026) | USD 45.01 Billion |

| Market Size (2031) | USD 70.23 Billion |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Go-to-Market Services Market Analysis by Mordor Intelligence

The go-to-market services market size is expected to increase from USD 42.1 billion in 2025 to USD 45.01 billion in 2026 and reach USD 70.23 billion by 2031, growing at a CAGR of 9.31% over 2026-2031. Growth is being supported by a broad redesign of how companies market, sell, and retain customers, as AI tools are pushing firms to connect these functions more tightly than before. Enterprises are increasingly turning to external specialists because the shift from isolated pilots to commercial AI deployment has made execution more complex, especially when technology, pricing, sales process, and customer success need to change together. The opportunity remains strong because many companies still lack the in-house capability to redesign revenue operations, localize expansion plans, and align digital and seller-led journeys consistently. Competitive pressure is also rising as large consulting networks defend their installed enterprise relationships while AI-native boutiques win work through narrower specialization, faster delivery, and more outcome-linked commercial terms. Even with budget pressure and some in-housing of execution work, demand is holding because regulatory complexity, pricing redesign, and agentic AI deployment continue to move faster than most organizations can absorb on their own.

Key Report Takeaways

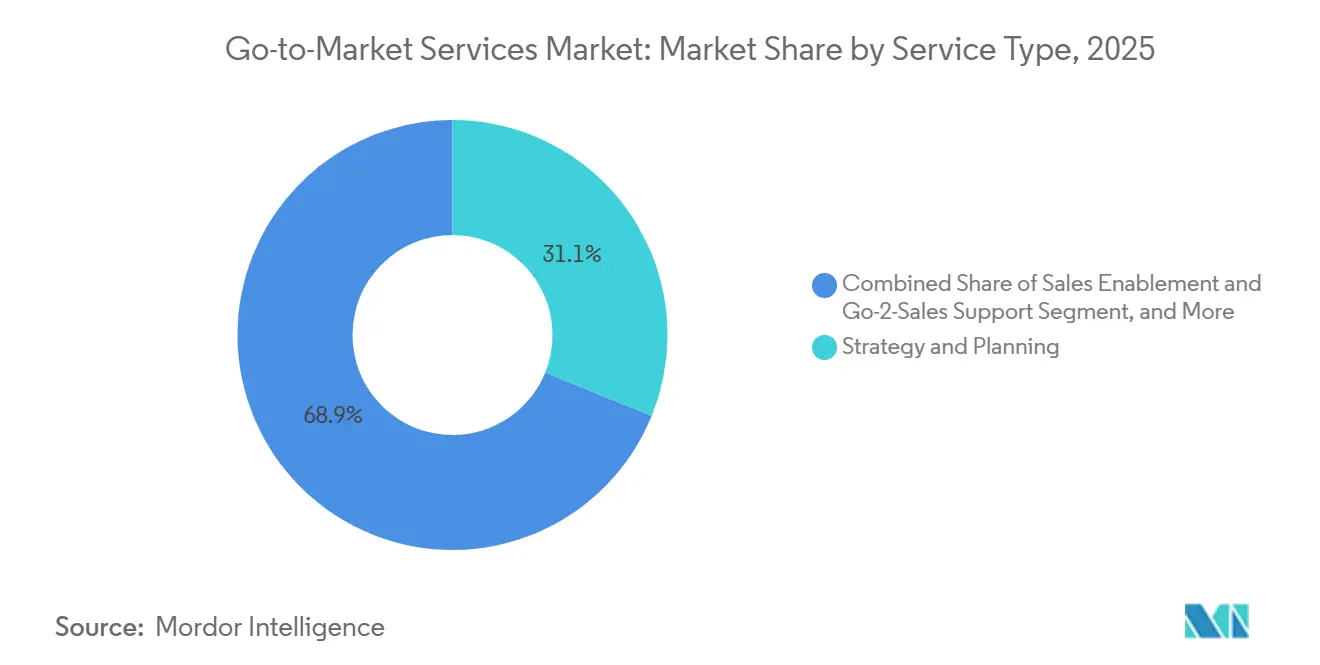

- By service type, strategy and planning accounted for 31.12% of the go-to-market services market revenue in 2025, while sales enablement and go-to-sales support are projected to expand at a 9.60% CAGR through 2031.

- By enterprise size, large enterprises accounted for 62.13% of market spending in 2025, while mid-sized enterprises are projected to record the fastest CAGR of 9.94% through 2031.

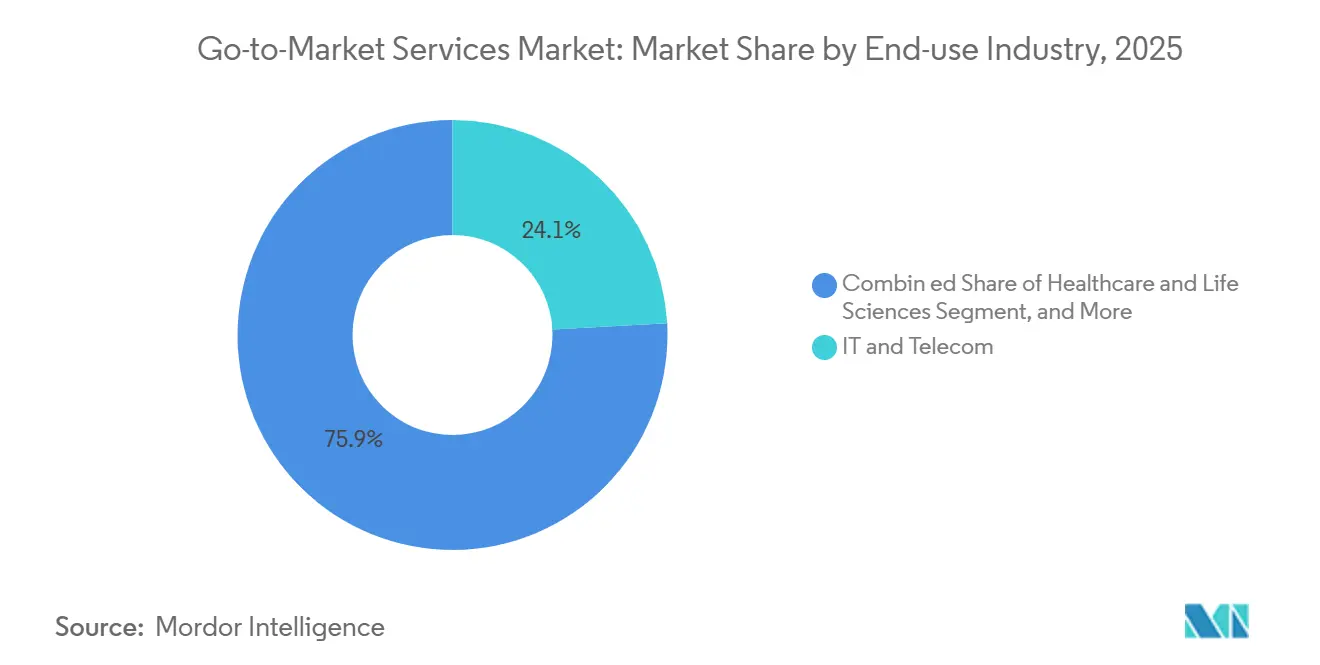

- By end-use industry, IT and telecom accounted for 24.13% of go-to-market services market revenue in 2025, while healthcare and life sciences are expected to grow at a 9.81% CAGR through 2031.

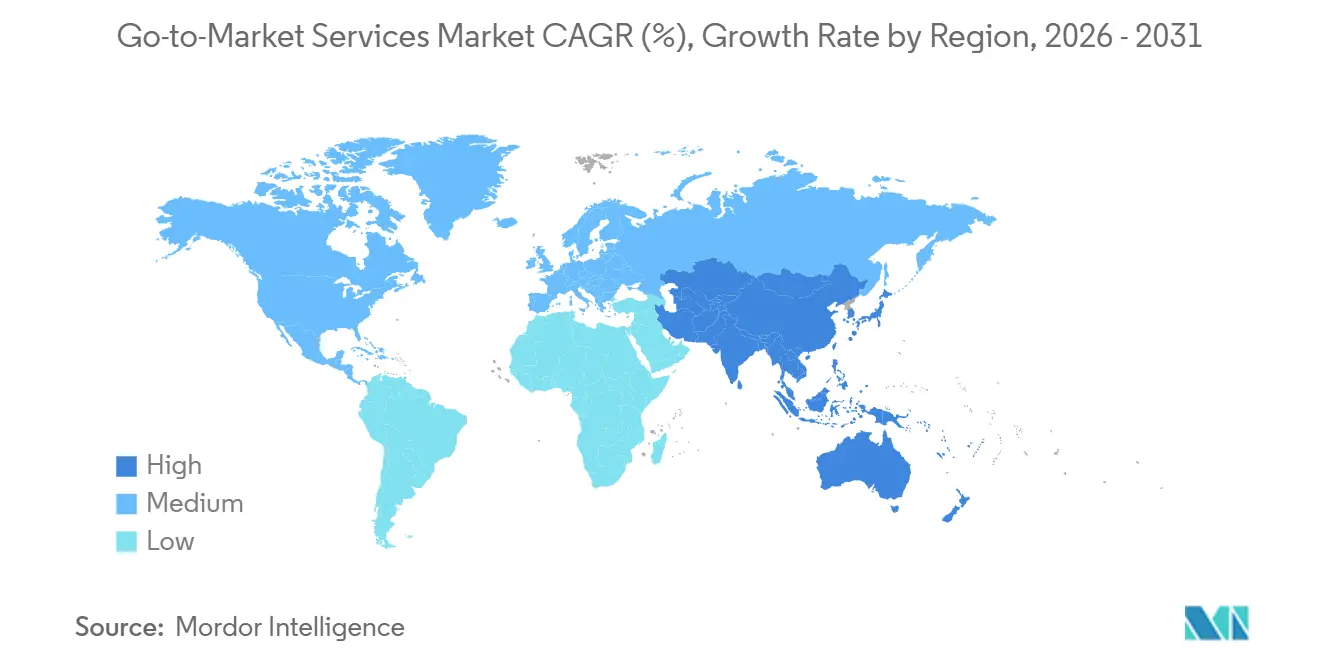

- By geography, North America accounted for 47.09% of the market value in 2025, while the Asia-Pacific is projected to grow at a 10.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Go-to-Market Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Led Sales and Marketing Transformation | +2.8% | Global | Short term (≤ 2 years) |

| Omnichannel Buying and Sales Alignment Demand | +2.2% | North America and EU | Short term (≤ 2 years) |

| Cross-Border Expansion and Localization Needs | +1.5% | APAC core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Pricing and Monetization Redesign for AI and Subscription Offers | +1.1% | Global, strongest in North America | Medium term (2-4 years) |

| Agent-Engine Optimization and Machine-Readable Offer Design | +0.6% | North America and EU | Short term (≤ 2 years) |

| Channel Governance for Hybrid Direct and Partner Routes | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Led Sales and Marketing Transformation

The go-to-market services market is being pushed forward by a deeper change than simple workflow automation, because generative and agentic AI are replacing core assumptions behind planning, engagement, and measurement. Forrester described this shift as a point where older go-to-market structures become difficult to sustain, especially when marketing, sales, and customer success still operate on separate systems and separate definitions of buyer progress. This change matters because AI-mediated buying weakens older demand metrics, which makes it harder for internal teams to defend spend using legacy activity dashboards and easier for specialist advisers to win work around measurement redesign and execution discipline. Salesforce highlighted that business leaders expect meaningful revenue gains from generative AI in commercial functions, but those gains depend on tight coordination across sales, marketing, and service, which many organizations still do not have in place.[1]Salesforce, “AI in Sales and Marketing: The Complete Guide to Alignment,” Salesforce, salesforce.com EY’s March 2026 launch of an agentic sales orchestration platform with Snowflake and Canva also showed how prospecting, pricing support, and contract automation are now being tied together in a single commercial workflow, raising the complexity of implementation.[2]EY, “EY Announces Launch of Agentic Sales Orchestration Platform to Address Enterprise AI Fragmentation,” EY, ey.com In this setting, the go-to-market services market is rewarding providers that can connect AI orchestration to real revenue operations, rather than those that only offer isolated tools or short-term experimentation support.

Omnichannel Buying and Sales Alignment Demand

The go-to-market services market is also benefiting from the fact that B2B buying is now spread across more channels, more information sources, and more moments where buyers expect continuity rather than disconnected outreach. Gartner reported in May 2026 that buyers used multiple information sources during a purchase and that 45% had used generative AI in a recent transaction, yet 69% still turned to sales representatives to validate AI-generated information at critical stages. That finding supports a simple commercial reality, digital self-service is expanding, but it does not remove the need for human validation when deals become larger, more technical, or more risky. Hokodo found that European B2B buyers wanted several distinct sales channels and expected digital experiences that were fast, simple, and accurate, which reinforces demand for GTM specialists who can rebuild channel design, data flow, and seller readiness together. Forrester had already signaled that more than half of large B2B transactions above USD 1 million would move through digital self-serve channels, which means seller-led interactions are being reserved for the points where confidence, compliance, and deal structure matter most. As a result, the go-to-market services market is seeing sustained demand for work that spans channel architecture, RevOps redesign, and front-line enablement in one connected program.

Cross-Border Expansion and Localization Needs

The go-to-market (GTM) services market gains additional support when enterprises expand across borders, because mistakes in positioning, compliance, and channel selection become more costly once companies leave familiar home markets. Accenture’s 2026 localization analysis showed that the geography of foreign direct investment has shifted meaningfully, with the Middle East and Central Asia gaining share and the Eurozone also strengthening, which signals that commercial priorities are moving beyond a simple focus on mature Western markets.[3]Accenture, “For Multinational Companies, Localization Matters More Than Ever,” Accenture, accenture.com The same research showed a surge in business partnerships across major regions, pointing to more partner-led routes to market and more complexity in channel management, distributor selection, and local execution design. This matters because translation and true commercial localization are not the same task, and providers that confuse them often fail to adapt offers, messaging, and selling motions to local buying behavior. Microsoft’s April 2025 European Digital Commitments also showed that regulatory positioning itself can shape commercial trust, especially when data residency and governance become part of the value proposition presented to public sector and regulated buyers. That dynamic is widening the role of the go-to-market (G2M) services market in APAC, Europe, and parts of the Middle East, where growth depends on local fit as much as on product quality.

Pricing and Monetization Redesign for AI and Subscription Offers

The go-to-market services market is being lifted by the need to redesign pricing models for AI-enabled products, subscription offers, and hybrid commercial structures that no longer fit older software selling assumptions. FTI Consulting noted that many companies still bundle AI and machine learning capabilities into existing offers, a practice that often weakens monetization and makes it harder to match price with delivered value. The same body of work also pointed to the growing use of hybrid pricing structures, where subscription, usage, and outcome logic are being combined in ways that require new packaging, sales narratives, and customer success models. This is creating first-time demand for advisers who can work across pricing, positioning, enablement, and performance measurement, because poor pricing design can damage margins even when demand remains strong. HubSpot’s April 2026 decision to reprice an AI resolution tool at USD 0.50 per outcome showed how quickly public pricing anchors can reset buyer expectations and shorten the response window for competitors. In practice, the G2M services market is benefiting because pricing redesign is no longer a narrow finance task and has become part of full commercial execution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Compression and Project-Based Procurement | -2.0% | Global, strongest in North America and EU | Short term (≤ 2 years) |

| In-House Martech and AI Teams Reducing Outsourced Execution | -1.4% | North America and EU | Medium term (2-4 years) |

| Data Governance and Agentic AI Readiness Gaps | -0.8% | Global | Medium term (2-4 years) |

| Channel Conflict and Discount Leakage Across Routes-to-Market | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Compression and Project-Based Procurement

The go-to-market services market continues to face pressure from tighter client spending, especially when boards demand clearer revenue outcomes while leaving operating budgets constrained. Gartner’s 2025 CMO Spend Survey showed that marketing budgets remained stalled at 7.7% of company revenue and that many chief marketing officers were being asked to do more with less. In that environment, many buyers are shifting away from open-ended retainers and toward short, milestone-based engagements that require providers to prove value faster and carry more commercial risk within the same contract.[4]Analytic Partners, “Five Forces Shaping Marketing Budget Decisions in 2026,” Financial Post, financialpost.com Analytic Partners reported in February 2026 that senior decision-makers were leaning more heavily on econometric models and commercial analytics for budget allocation, which raises the screening threshold for any GTM provider that cannot demonstrate a measurable contribution. PepsiCo reinforced the same efficiency mood when its 2025 disclosures pointed to a USD 500 million advertising reduction tied to productivity gains across spending categories. For the go-to-market services market, this does not remove demand, but it does compress deal size, lengthen approval cycles, and push vendors toward clearer ROI framing at the point of sale.

In-House Martech and AI Teams Reducing Outsourced Execution

The go-to-market services market is also being restrained by the steady expansion of internal AI and martech teams, particularly for repeatable execution work that can now be brought in-house more easily. Reuters reported in May 2026 that companies, including Kimberly-Clark, Catalyst Brands, and Target India, were using AI at Indian capability centers to bring more creative and campaign work inside the organization and cut dependence on agencies. The Conference Board also found a modest decline in outsourcing among some organizations over the prior 18 months, linked to stronger internal AI capability and the ability to automate parts of marketing and communications work. This substitution threat is most visible in tasks such as content generation, campaign activation, and recurring reporting, where internal teams can now work faster at lower marginal cost. Boston Consulting Group argued that companies pursuing in-house efficiency still need process redesign and new operating models, which means strategic and orchestration work remains harder to internalize than production work. That distinction matters because the GTM services market is likely to lose some execution-heavy mandates while retaining stronger demand for redesign, governance, and cross-functional transformation support.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Strategy And Planning Leads While Sales Enablement Accelerates

Strategy and planning services held 31.12% of the go-to-market service market share in 2025, reflecting client demand for a clear commercial foundation before moving into campaign activity or seller execution. This service group includes go-to-market strategy, market entry advisory, and positioning and messaging work, all of which gained importance as organizations adjusted to AI-supported buyer journeys and changing channel economics. Product launch and commercialization services continued to benefit from fast product cycles in technology, healthcare, and consumer goods, where delays in positioning or readiness can weaken launch results. Channel partner and distribution strategy also remained important because hybrid direct and partner structures need clear ownership rules, partner incentives, and consistent customer experience. Demand generation and lead generation stayed relevant, but AI-based internal tools created more substitution pressure in this part of the go-to-market service market than in advisory-intensive categories.

Sales enablement and go-to-sales support is projected to grow at a 9.60% CAGR through 2031, making it the fastest-growing service type in the go-to-market service market. Gartner’s buyer research found that 69% of buyers still relied on sales representatives to validate AI-generated information, which puts seller readiness at the center of commercial performance. Providers are responding with AI-assisted content libraries, real-time deal coaching, buyer intelligence tools, and manager-led adoption programs that make information more useful during live selling situations. The growth is not only driven by new software because many clients need help with behavior change, sales process design, field adoption, and measurement after they purchase new tools. This part of the go-to-market service industry is likely to gain further importance as sellers spend less time introducing basic product information and more time helping buyers make confident decisions.

By Enterprise Size: Large Enterprises Lead While Mid-Sized Buyers Expand Faster

Large enterprises accounted for 62.13% of market spending in 2025, reflecting the scale, geographic reach, and organizational complexity of their commercial transformation programs. These companies purchase the widest range of go-to-market services, including multi-country market entry support, enterprise pricing redesign, omnichannel alignment, partner strategy, and post-launch optimization. Their work often runs across multiple budget cycles and requires coordination among product, sales, marketing, finance, legal, data, and customer success teams. These requirements favor providers with established executive relationships, broad sector knowledge, and the ability to staff complex programs across regions. The current revenue structure of the go-to-market service market, therefore, remains concentrated around large clients even as other buyer groups become more active.

Mid-sized enterprises are projected to grow at a 9.94% CAGR through 2031, making them the fastest-expanding enterprise size segment in the go-to-market service market. These buyers increasingly face the same channel, pricing, data, and expansion challenges as larger companies, but their internal teams are often not designed to solve them all at once. Premier NX identified that mid-market firms with USD 50 million to USD 1 billion in revenue face a more layered, cross-functional, and technology-dependent growth environment than in earlier expansion cycles. Providers that offer modular services at lower engagement thresholds can address a group that may not need a full enterprise transformation program but still needs practical commercial support. Platform consolidation is also encouraging some mid-sized clients to simplify their martech and sales technology environments, which creates a more focused advisory task around how unified platforms support the full buyer journey.

By End-Use Industry: IT And Telecom Anchors Demand While Healthcare And Life Sciences Grows Faster

IT and telecom accounted for 24.13% of the go-to-market service market in 2025, supported by a high product launch frequency, active partner programs, and the ongoing need to maintain clear positioning in crowded technology categories. Technology vendors require recurring support because product releases, pricing structures, sales motions, and partner enablement change more often than in many other sectors. BFSI, consumer goods and beauty, and retail and e-commerce also represented substantial demand pools, but each required a different form of commercial support. Financial services buyers needed help with regulated digital sales, consumer goods and beauty companies faced fast trend cycles, and retailers needed more coordinated omnichannel experiences. Media and entertainment, automotive, education, and travel and hospitality remained smaller but relevant parts of the go-to-market service market because their commercialization barriers often involved sector-specific channels, monetization, recruitment, or recovery needs.

Healthcare and life sciences are expected to grow at a 9.81% CAGR through 2031, making them the fastest-growing end-use segment in the go-to-market services market. Bain and Company reported that 2025 was the largest year on record for pharma services deal value, indicating continued investment in the sector's commercial infrastructure. Peer-reviewed research in Drug Discovery Today found that external commercial solutions organizations are increasingly helping bridge market access, logistics, manufacturing, reimbursement, and channel challenges for cellular immunotherapy products. Regulatory expectations from the FDA, EMA, and national health agencies add complexity, as promotional plans and commercial processes must be designed within clear compliance boundaries. The go-to-market service market, therefore, has a strong opening in healthcare and life sciences, but providers need deep regulatory, clinical, and commercial knowledge to compete effectively.

Geography Analysis

North America held 47.09% of the go-to-market service market share in 2025, supported by the concentration of technology, SaaS, and business services companies that make large and frequent investments in commercial transformation. The United States remained the primary national market, while Canada and Mexico gained prominence as enterprises built integrated North American programs that still required distinct positioning, compliance, and route-to-market approaches. Forrester’s 2026 research on augmented, resilient, and collaborative GTM structures showed that US B2B leaders were investing in more fundamental commercial redesign rather than limited point-solution upgrades. Europe represented the second-largest regional opportunity, with Germany, the United Kingdom, and France serving as the main centers of demand. The EU AI Act’s phased enforcement created an additional compliance burden for AI-supported commercial programs, especially where companies must document, audit, and govern automated processes involving customers and prospects.

Asia-Pacific is projected to grow at a 10.05% CAGR through 2031, making it the fastest-growing geography in the go-to-market service market. Digital infrastructure investment, cross-border trade, and regional companies seeking international growth are increasing the need for local positioning, partner planning, and sales execution support. Reuters reported that AI productivity gains at global capability centers in India were helping multinationals internalize some routine work, but this development also expanded the pool of Indian mid-sized companies seeking external help as they pursue exports and overseas growth. China remained both a destination market and an origin for outbound expansion, creating demand for support around local messaging, regulatory navigation, and partner strategy across Southeast Asia and beyond.

Brazil’s telecommunications sector received USD 2.3 billion in foreign direct investment during the first 4 months of 2026, while the country's total foreign direct investment reached USD 77.6 billion in 2025. Brazil’s CBS and IBS indirect tax reform adds another commercial planning requirement, as pricing, invoicing, and channel economics may need to be adjusted before programs are activated. The Middle East is being supported by Saudi Arabia’s Vision 2030 programs and the UAE Digital Strategy 2025 to 2027, which are creating demand for commercial strategy, digital GTM design, and market entry support across the GCC. PRCA MENA found that 68% of agencies expected revenue growth in 2026 and 80% viewed strategic advisory as a critical growth driver, indicating continued demand for senior advisory work across the region. Africa remains at an earlier stage, but the implementation of the AfCFTA digital trade agenda is supporting the development of formal digital trade corridors and creating room for market-entry advisory across South Africa, Nigeria, and Egypt.

Competitive Landscape

The global go-to-market services market is moderately concentrated, with large professional services networks, major strategy firms, and IT services providers still controlling a meaningful share of enterprise transformation work. At the same time, the go-to-market services market is opening space for AI-native boutiques and specialist firms that compete through vertical depth, faster execution, and pricing models tied more closely to measurable outcomes. This is creating margin pressure in the mid-market, where large firms cannot always defend premium fee levels and smaller firms can tailor delivery more tightly to a client’s sales motion or pricing challenge. Accenture’s March 2026 acquisition of Faculty showed how major incumbents are using M&A to strengthen applied AI capability inside commercial transformation delivery. Capgemini’s February 2026 move to join the OpenAI Frontier Alliance and its April 2026 launch of the Google Cloud AI Enterprise Hub reflected the same direction, with leading firms embedding platform relationships and engineering capacity into the core of service delivery.

White-space demand in the go-to-market services market remains strongest in outcome-based managed services for mid-sized clients, commercialization support for regulated sectors, and cross-border programs that require both localization and AI-enabled execution. Pricing specialists such as Simon-Kucher have benefited from monetization redesign demand, especially as AI and subscription structures make packaging and willingness-to-pay questions more complex. That pattern matters because the go-to-market services market is no longer being shaped only by broad strategy mandates and is instead rewarding firms that solve specific commercial problems with execution depth. Some providers also fall outside the real boundaries of the category, as market research firms such as SIS International are more closely tied to primary intelligence work than to GTM strategy, demand creation, sales enablement, or commercialization execution. By contrast, firms such as Oliver Wyman, WPP Group, and Dentsu Group align more closely with the practical service scope of the go-to-market services market because they are closer to pricing, market entry, and channel execution needs.

Technology-enabled differentiation has become the main dividing line across the go-to-market services market, especially in the ability to connect agentic platforms, revenue intelligence, and workflow governance into one operating model. Deloitte’s April 2026 launch of an end-to-end agentic transformation practice with Google Cloud and McKinsey’s April 2026 launch of the McKinsey Google Transformation Group both showed how incumbents are moving toward tighter platform-linked execution at scale. Bain’s May 2026 investment in the OpenAI Deployment Company added another example of large firms tying themselves directly to enterprise AI rollout capacity rather than staying at the advisory layer alone. The result is a go-to-market services market where scale still matters, but the winning position increasingly depends on how well a provider can translate AI capability into measurable commercial change for each client.

Go-to-Market Services Industry Leaders

Deloitte Touche Tohmatsu Limited

Accenture plc

PricewaterhouseCoopers International Limited

Publicis Groupe S.A.

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: EY and Microsoft announced a joint investment of more than USD 1 billion over five years to launch a new initiative embedding Microsoft's Forward Deployed Engineers with EY industry professionals to scale enterprise AI transformation across change management delivery models, a direct expansion of GTM delivery capacity for large enterprise clients.

- May 2026: Bain and Company invested in the OpenAI Deployment Company, a new venture launched by OpenAI with 19 global partners designed to deploy AI across enterprises' most critical operations, extending Bain's three-year partnership with OpenAI and giving Bain portfolio companies priority access to deployment services.

- May 2026: KPMG and Anthropic announced a global alliance and launched KPMG Digital Gateway Powered by Claude, embedding Claude directly into KPMG's client delivery platform for agentic workflow development, with an initial focus on tax clients and private equity firms.

- May 2026: ZS launched ZAIDYN Medical and ZAIDYN Content, two purpose-built agentic AI application suites for life sciences commercial teams, extending its ZAIDYN® platform and reflecting recognition as a Leader in the IDC MarketScape for Life Sciences R&D Strategic Consulting 2026.

Global Go-to-Market Services Market Report Scope

The Global Go-to-Market Services Market refers to services that help companies plan and execute successful market entry and product launches across regions or countries. It includes market entry strategy, positioning, launch planning, channel strategy, messaging, and sales enablement support. The market is driven by the need to reduce launch risk, localize offerings, and accelerate revenue generation in new markets.

The Go-To-Market Services Market Report is Segmented by Service Type (Strategy and Planning, Product Launch and Commercialization, Channel Partner and Distribution Strategy, Demand Generation and Lead Generation, Sales Enablement and Go-to-Sales Support, and Others), Enterprise Size (Large Enterprises, Mid-sized Enterprises, and Small Enterprises), End-use Industry (Retail and E-commerce, Consumer Goods and Beauty, Media and Entertainment, IT and Telecom, BFSI, Healthcare and Life Sciences, Education, Travel and Hospitality, Automotive, and Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Strategy and Planning |

| Product Launch and Commercialization |

| Channel Partner and Distribution Strategy |

| Demand Generation and Lead Generation |

| Sales Enablement and Go-to-Sales Support |

| Others |

| Large Enterprises |

| Mid-sized Enterprises |

| Small Enterprises |

| Retail and E-commerce |

| Consumer Goods and Beauty |

| Media and Entertainment |

| IT and Telecom |

| BFSI |

| Healthcare and Life Sciences |

| Education |

| Travel and Hospitality |

| Automotive |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Service Type | Strategy and Planning | |

| Product Launch and Commercialization | ||

| Channel Partner and Distribution Strategy | ||

| Demand Generation and Lead Generation | ||

| Sales Enablement and Go-to-Sales Support | ||

| Others | ||

| By Enterprise Size | Large Enterprises | |

| Mid-sized Enterprises | ||

| Small Enterprises | ||

| By End-use Industry | Retail and E-commerce | |

| Consumer Goods and Beauty | ||

| Media and Entertainment | ||

| IT and Telecom | ||

| BFSI | ||

| Healthcare and Life Sciences | ||

| Education | ||

| Travel and Hospitality | ||

| Automotive | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the go-to-market service market?

The go-to-market service market is estimated at USD 45.01 billion in 2026 and is projected to reach USD 70.23 billion by 2031 at a CAGR of 9.31%.

Which service type leads current demand?

Strategy and planning led service demand with a 31.12% share in 2025 because companies needed stronger market entry, positioning, and commercial architecture before executing new sales programs.

Which service area is projected to grow the fastest?

Sales enablement and go-to-sales support is projected to grow at a 9.60% CAGR through 2031 as companies invest in seller readiness, AI-assisted content, and real-time buyer intelligence.

Why are mid-sized companies increasing their use of GTM services?

Mid-sized companies face more complex pricing, channel, data, and expansion challenges but often lack large internal teams, making modular external support more attractive.

Which end-use sector has the highest forecast growth?

Healthcare and life sciences is expected to expand at a 9.81% CAGR through 2031 because pharmaceutical, biotech, and commercial solutions firms need specialized launch, access, and compliant channel support.

Which region has the strongest growth outlook?

Asia-Pacific is projected to grow at a 10.05% CAGR through 2031, supported by digital investment, cross-border trade, and expanding demand for local market entry and partner strategy support.

Page last updated on: