Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.65 Trillion |

| Market Size (2031) | USD 2.51 Trillion |

| Growth Rate (2026 - 2031) | 8.78% CAGR |

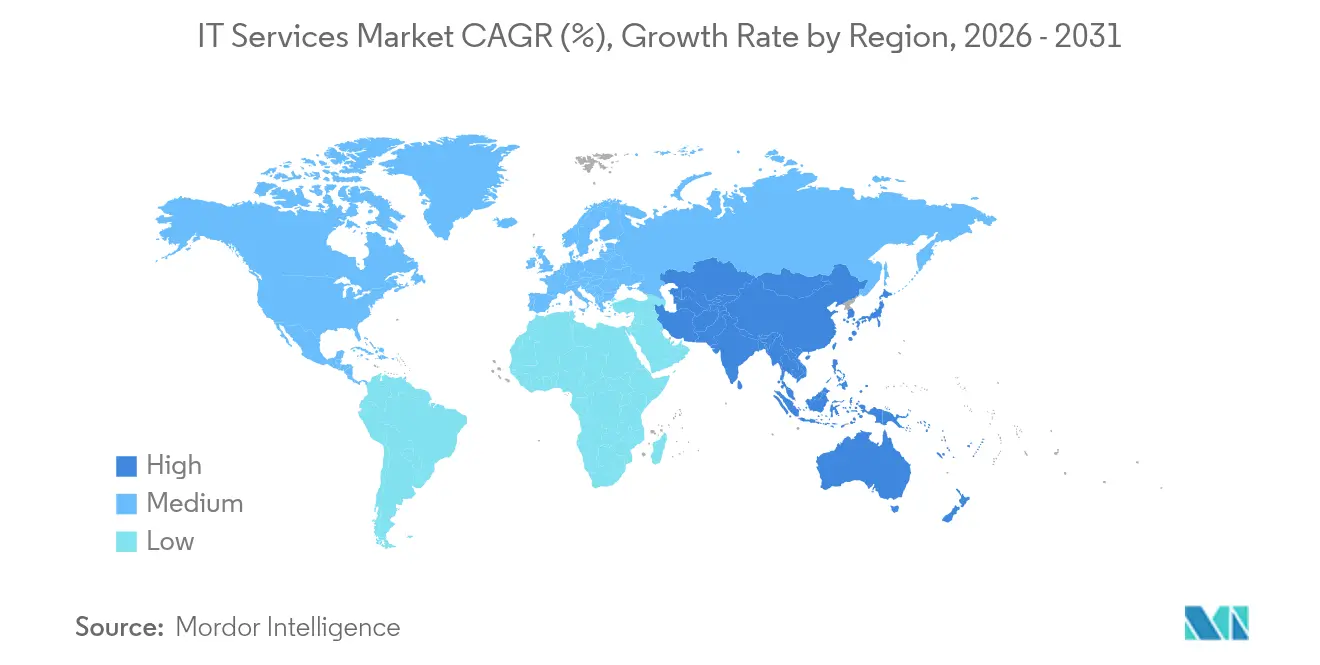

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

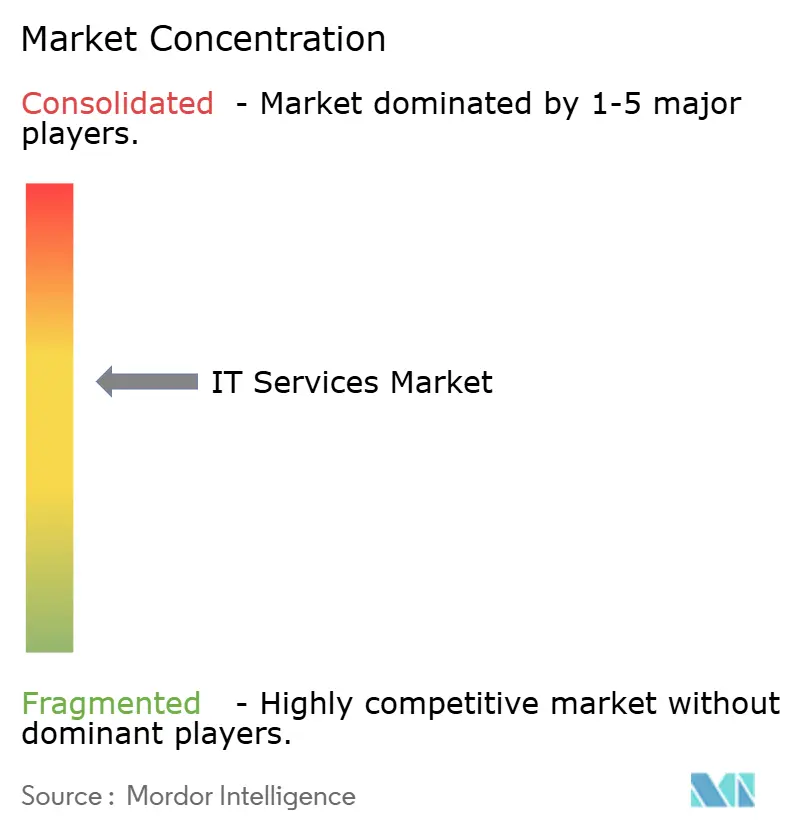

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IT Services Market Analysis by Mordor Intelligence

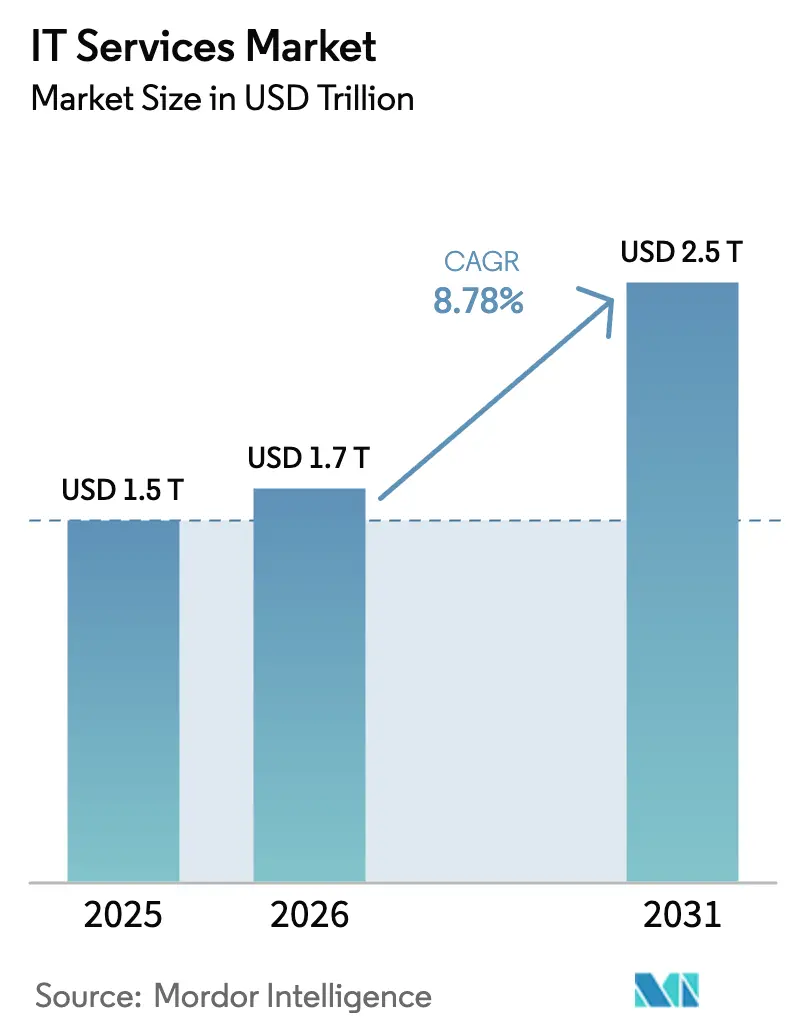

The IT Services Market size is estimated at USD 1.65 trillion in 2026, and is expected to reach USD 2.51 trillion by 2031, at a CAGR of 8.78% during the forecast period (2026-2031).

Robust digital-transformation agendas, an upswing in enterprise artificial-intelligence adoption, and rising cloud-native migrations are expanding addressable demand. Spending momentum is strongest in banking and healthcare, where 2024 outlays jumped 8.7% and 15% respectively as institutions modernized legacy cores. Providers able to bundle consulting, implementation, and managed services around hybrid-cloud and AI workloads capture premium contracts, while price-sensitive outsourcing engagements continue to anchor large-scale delivery pipelines. Heightened consolidation—including multibillion-dollar acquisitions—shows that scale, vertical depth, and intellectual-property differentiation are now decisive in winning enterprise renewals.

Key Report Takeaways

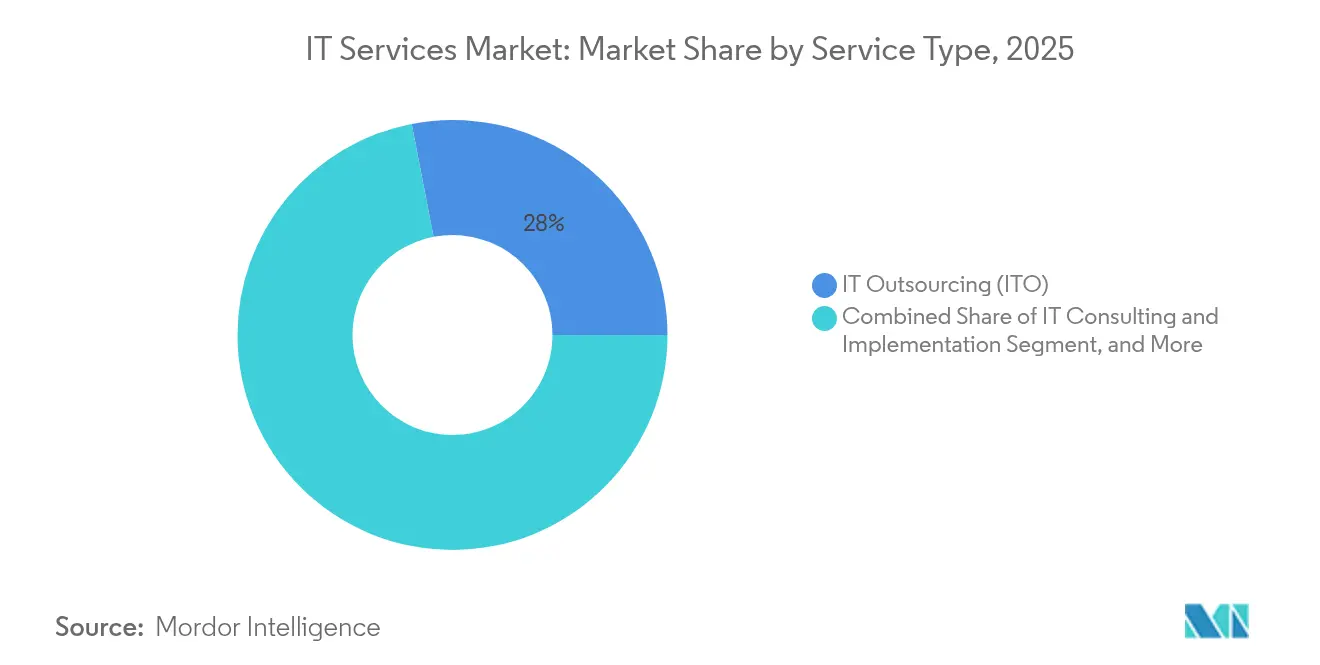

- By service type, IT Outsourcing led with a 28.04% revenue share in 2025; Managed Security Services is advancing at a 12.18% CAGR through 2031.

- By end-user enterprise size, Large Enterprises held 69.42% of the IT services market share in 2025, while Small and Medium Enterprises are expanding at an 10.92% CAGR to 2031.

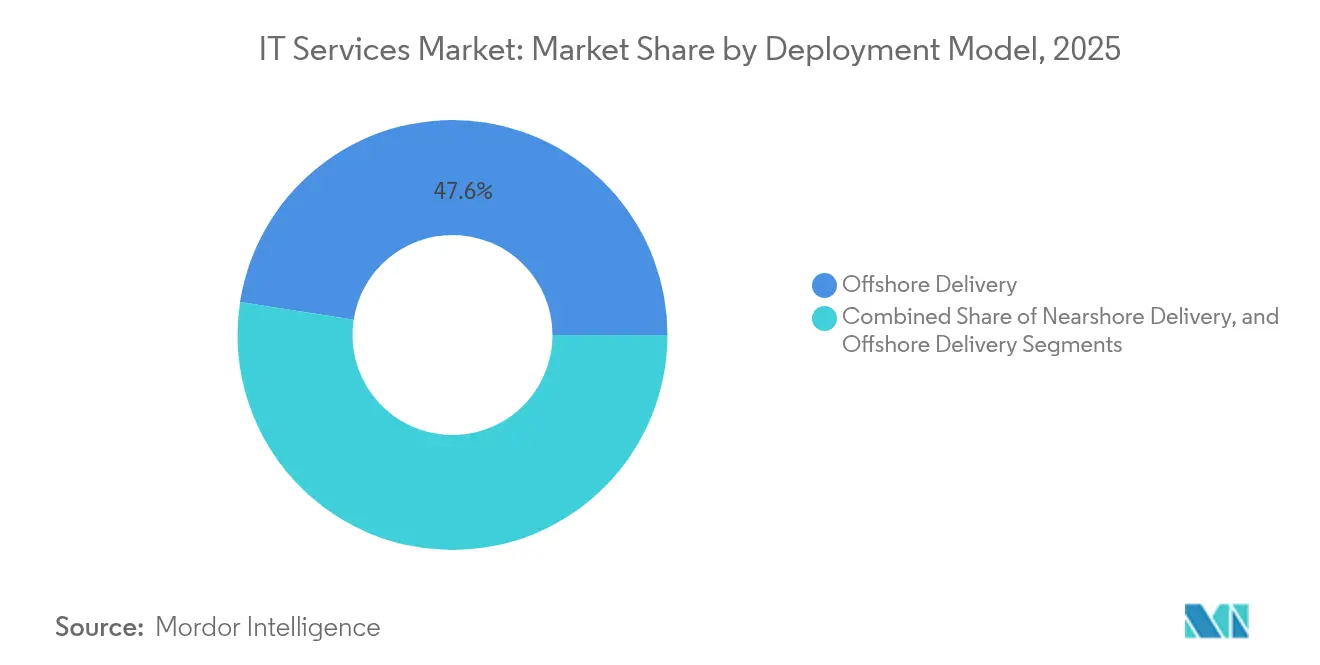

- By deployment model, Offshore Delivery accounted for 47.55% share of the IT services market size in 2025; Nearshore Delivery records the fastest 10.18% CAGR through 2031.

- By end-user vertical, Banking, Financial Services, and Insurance captured 24.38% share of the IT services market size in 2025; Healthcare and Life-Sciences is growing at an 11.02% CAGR to 2031.

- By geography, North America commanded 37.05% revenue in 2025; Asia-Pacific is set to post the highest 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation acceleration | +2.1% | Global, especially North America and Europe | Medium term (2–4 years) |

| Hybrid-cloud migration boom | +1.8% | North America, Europe core; Asia-Pacific expansion | Long term (≥ 4 years) |

| Escalating cyber-threat landscape | +1.4% | Global, acute in BFSI and healthcare | Short term (≤ 2 years) |

| Enterprise AI and analytics spend surge | +1.9% | North America, Europe primary; Asia-Pacific emerging | Medium term (2–4 years) |

| Vertical-specific cloud platforms adoption | +1.2% | Global, sector-specific regional patterns | Long term (≥ 4 years) |

| Sustainability-driven Green-IT audits | +0.8% | EU and North America, global spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-transformation acceleration post-COVID-19

Multi-cloud adoption has crossed 87% of enterprises, while 51% are funding cloud-native modernization tracks that bundle application refactoring, AI services and data platforms. The Global IT services market now rewards providers that master container orchestration, micro-services and DevOps over simple lift-and-shift migration. DXC Technology’s “Cloud Right” approach enabled Ocean Network Express to achieve zero-downtime migration, showcasing how vendors move from infrastructure caretakers to strategic business partners. Revenue pools are shifting toward advisory and managed cloud operations layers that demand both deep technical credentials and sector insight. These engagements, typically structured around shared service-level outcomes, lift provider stickiness and unit economics. Skills scarcity in Kubernetes, site reliability engineering and FinOps is further buoying service rates, underscoring why cloud-first programmes add the highest positive delta to long-run growth.

Hybrid-cloud migration boom

Global cloud-ERP outlays are on track to nearly double between 2022 and 2027 as enterprises pursue workload portability and regulatory compliance.[1]IBM Institute for Business Value, “The Enterprise Guide to AI Governance,” ibm.com European firms directed EUR 489.8 billion (USD 553.5 billion) to IT services in 2025, with 45% tagged for cloud initiatives. Multi-cloud strategies help organizations avert vendor lock-in, yet they impose governance complexity that drives demand for advisory and optimization services. Data sovereignty mandates heighten the need for region-specific hosting footprints, bolstering nearshore and onshore engagements. Providers offering certified cloud architects and managed FinOps talent are capturing high-margin contracts across the IT services market.

Escalating cyber-threat landscape

Average breach costs are projected to hit USD 4.45 million in 2025, and cybercrime losses are set to reach USD 10.5 trillion annually.[2]Patrick Castillo, “Cybersecurity Compliance in 2025: Preparing for New Regulations,” ntiva.com Regulatory frameworks like the EU’s DORA require auditable cyber-resilience, pushing enterprises toward third-party managed security. Zero-Trust architectures and AI-enabled threat-hunting have moved from best practices to mandatory controls. Providers specializing in security operations, incident response, and compliance management report record pipelines, with double-digit growth consistently outpacing the broader IT services market.

Enterprise AI and analytics spend surge

Global AI expenditure is heading toward USD 826.7 billion by 2030 as executive teams weaponize data for competitive gain. In banking, 77% of leaders deem generative AI deployment-ready. Over half of large enterprises have instituted AI governance boards, signaling that ethical, legal, and operational oversight is now a board-level agenda item. Consulting firms that fuse data-science talent with risk and compliance know-how are uniquely positioned to shepherd complex enterprise rollouts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Service-price commoditization pressure | -1.3% | Global, especially offshore hubs | Short term (≤ 2 years) |

| Global talent shortage and attrition | -1.8% | North America, Europe primary; Asia-Pacific secondary | Medium term (2–4 years) |

| Data-sovereignty geopolitical barriers | -0.9% | EU and Asia-Pacific compliance-driven | Long term (≥ 4 years) |

| Scope-3 carbon-reporting compliance costs | -0.6% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Service-price commoditization pressure

Automation and offshore scale have erased entry barriers for common help-desk and infrastructure tasks, compressing margins in traditional outsourcing. Clients increasingly demand outcome-based billing, compelling vendors to prove tangible business impact. Smaller rivals undercut pricing, which accelerates consolidation among incumbents able to cross-sell premium consulting and security offerings. The resulting shake-out is likely to realign the competitive order within the IT services market over the next two years.

Global talent shortage and attrition

Demand for AI engineers, cloud architects, and security analysts outstrips supply across major economies. Attrition spiked in 2024, forcing leading players to announce workforce realignments while chasing niche experts at premium salaries. Elevated wage inflation threatens profitability and slows project kickoff times, curbing near-term revenue realization. Vendors are ramping up reskilling programs and opening satellite delivery centers in tier-2 cities to tap untapped talent pools, yet structural shortages persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Security Services Drive Premium Growth

Managed Security Services is growing at a 12.18% CAGR, the steepest rate across the IT services market. Enterprises accept that specialized providers outperform internal teams in threat detection and incident response, prompting long-term outsourcing contracts that include continuous compliance monitoring. IT Outsourcing retains the largest 28.04% revenue position due to entrenched cost-optimization mandates. However, margin compression in commoditized workstreams is pushing vendors to package outsourcing with consulting to protect pricing. Cloud and Platform Services benefit from surging hybrid-cloud adoption; projects frequently bundle ERP modernization with data-integration layers, supporting cross-selling momentum.

Demand dynamics also favor Business Process Outsourcing, especially in finance, HR, and industry-specific back-office workflows where robotic process automation amplifies efficiency gains. IT Consulting revenues rise on complexity: organizations need guidance to harmonize AI, edge computing, and vertical clouds. Vendors that deliver reference architectures, accelerated migration toolkits, and domain-centric solutions increase wallet share across the IT services market.

By End-User Enterprise Size: SMEs Accelerate Digital Adoption

Small and Medium Enterprises register an 10.92% CAGR through 2031, reflecting democratized access to cloud-delivered ERP, CRM, and cybersecurity bundles. Consumption-based pricing allows SMEs to deploy capabilities historically reserved for large corporations, compressing deployment timelines from months to weeks. Compliance burdens in healthcare and financial services incentivize SMEs to engage external specialists rather than build in-house controls, expanding addressable revenue for managed-service partners.

Large Enterprises still command 69.42% revenue, underpinned by sprawling legacy estates that demand long-duration transformation roadmaps. Hybrid models blending internal centers of excellence with targeted external expertise prevail, securing high-value contracts for niche providers. Enterprise buyers increasingly list sustainability credentials and carbon-reporting readiness in RFPs, offering differentiation avenues for providers that track Scope-3 emissions across the IT services market.

By Deployment Model: Nearshore Gains Strategic Advantage

Offshore Delivery leads with 47.55% revenue thanks to mature delivery ecosystems in India and the Philippines that enable labor arbitrage without compromising quality. Yet Nearshore Delivery posts a faster 10.18% CAGR as enterprises weigh geopolitical risk, time-zone overlap, and data-sovereignty constraints. Latin America and Eastern Europe see expanding captive centers and vendor investments aimed at de-risking concentrated supply chains.

Onshore Delivery, while costlier, retains relevance for projects demanding strict regulatory adherence or classified data handling. Government agencies and highly regulated industries favor domestically located personnel cleared under local regulations. Vendors that maintain balanced global-nearshore-onshore footprints offer flexible resourcing models, strengthening competitiveness across the IT services market.

By End-User Vertical: Healthcare Leads Digital Transformation

Healthcare and Life-Sciences accelerate at an 11.02% CAGR, fastest among verticals, as providers digitize electronic health records, tele-health, and diagnostics analytics. Regulatory mandates on data interoperability and patient privacy generate continuous demand for integration and security consulting. BFSI holds a 24.38% share of the IT services market size owing to vast modernization budgets and stringent cyber-resilience rules.

Manufacturing invests in Industry 4.0 platforms connecting factory floors to analytics hubs, requiring specialized OT-IT convergence expertise. Retail focuses on real-time inventory visibility and personalized commerce journeys, while Telecom and Media seek 5G deployment support and content-delivery optimization. Energy and Utilities prioritize grid automation and sustainability reporting, creating a wide spectrum of opportunities for multi-disciplinary service vendors.

Geography Analysis

North America represents 37.05% of 2025 revenue, steered by USD 2.7 trillion in enterprise tech spending and early-adopter behavior toward AI and cloud platforms. Federal mandates requiring AI governance boards have institutionalized demand for strategic advisory and implementation services. Canada advances digital-government programs and natural-resource automation, whereas Mexico’s nearshore proposition attracts U.S. firms seeking cultural affinity and IP protection.

Asia-Pacific records the highest 11.12% CAGR through 2031. China scales smart-city pilots and green-manufacturing upgrades, India leverages its delivery-hub heritage while expanding domestic demand, and ASEAN economies close infrastructure gaps to support cross-border e-commerce and fintech growth. Japan and South Korea funnel investments into advanced manufacturing and telecom, spurring niche consulting around 5G and edge computing. Australia and New Zealand, despite mature IT spend, continue prioritizing cybersecurity and cloud compliance in banking and government.

Europe allocates EUR 489.8 billion (USD 553.5 billion) to IT services in 2025, 45% of which funds cloud programs. Regulatory frameworks—GDPR, DORA, and NIS2—propel security and compliance spend, ensuring consistent engagement pipelines for qualified providers. Germany spearheads manufacturing digitization, the United Kingdom leads in financial services transformation, and France, Italy, and Spain scale cloud-ERP rollouts. Eastern Europe develops as both a nearshore delivery basin and a consumer of modernization services, strengthening ecosystem depth across the IT services market.

Competitive Landscape

The IT services market exhibits moderate concentration, with leading players pursuing scale and vertical depth via acquisitions. Capgemini’s USD 3.3 billion purchase of WNS expanded process capabilities in key verticals, while Cognizant’s USD 1.3 billion Belcan takeover bolstered engineering services. IBM’s USD 6.4 billion HashiCorp deal fortified multi-cloud management offerings, underscoring infrastructure orchestration as a competitive battleground.

Technology fusion is the core differentiator: 55% of enterprises now maintain an AI governance board, and vendors that productize AI accelerators or compliance toolkits gain a big advantage.[4]IBM Corporation, “IBM Completes Acquisition of HashiCorp,” ibm.com White-space opportunities arise in quantum-readiness consulting, sustainability analytics, and automated regulatory reporting, domains where smaller specialists can outmaneuver generalists.

Pricing models evolve toward outcomes; clients demand commitments on efficiency gains or revenue lifts. Vendors build cross-functional squads mixing data scientists, industry SMEs, and change-management consultants to satisfy this pivot. Market share shifts will likely hinge on the agility with which providers retool delivery models, reskill talent, and monetize intellectual property across the IT services market.

IT Services Industry Leaders

Accenture plc

IBM (Technology & Consulting Services)

Tata Consultancy Services Ltd.

Cognizant Technology Solutions Corp.

Capgemini SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Charter Communications agreed to acquire Cox Communications for USD 34.5 billion, aiming for USD 500 million in annual synergies.

- January 2025: Omnicom completed its USD 13 billion takeover of Interpublic Group, enhancing data-driven marketing capabilities.

- December 2024: Capgemini finalized its USD 3.3 billion WNS acquisition, broadening business-process services depth.

- November 2024: IBM closed its USD 6.4 billion HashiCorp acquisition, strengthening hybrid-cloud toolchains.

Global IT Services Market Report Scope

IT services apply technical and business expertise to assist organizations in creating, managing, and optimizing their information and business processes. The scope of the market is considered by service type, size, end-user industry, and geographical analysis throughout the forecast period. The scope of the study considered was project-oriented (integration, consulting application, and development), managed services (application ma nagement, outsourcing, and infrastructure services), and support services (hardware and software and IT knowledge) while evaluating the market size.

The IT services market is segmented by service type (professional (system integration and consulting) and managed services), size (small and medium enterprises and large enterprises), end-user industry (BFSI, telecommunication, healthcare, retail, manufacturing, government, and other end-user industries), and by geography (North America [United States and Canada], Europe [Germany, United Kingdom, and France], Asia-Pacific [China, Japan, India, Singapore, Indonesia, Malaysia, Vietnam, and Thailand], Latin America, and Middle East and Africa). The market sizes and forecasts are provided for a value of USD for all the above segments.

By Service Type

| IT Consulting and Implementation |

| IT Outsourcing (ITO) |

| Business Process Outsourcing (BPO) |

| Managed Security Services |

| Cloud and Platform Services |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

By Deployment Model

| Onshore Delivery |

| Nearshore Delivery |

| Offshore Delivery |

By End-user Vertical

| BFSI |

| Manufacturing |

| Government and Public Sector |

| Healthcare and Life-Sciences |

| Retail and Consumer Goods |

| Telecom and Media |

| Logistics and Transport |

| Energy and Utilities |

| Other End-user Verticals |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Service Type | IT Consulting and Implementation | ||

| IT Outsourcing (ITO) | |||

| Business Process Outsourcing (BPO) | |||

| Managed Security Services | |||

| Cloud and Platform Services | |||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Deployment Model | Onshore Delivery | ||

| Nearshore Delivery | |||

| Offshore Delivery | |||

| By End-user Vertical | BFSI | ||

| Manufacturing | |||

| Government and Public Sector | |||

| Healthcare and Life-Sciences | |||

| Retail and Consumer Goods | |||

| Telecom and Media | |||

| Logistics and Transport | |||

| Energy and Utilities | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the IT services market in 2026?

The IT services market size is valued at USD 1.65 trillion in 2026, with a projected 8.78% CAGR to 2031.

Which service type is expanding fastest?

Managed Security Services posts the highest 12.18% CAGR as enterprises outsource cyber-resilience.

What region shows the strongest growth?

Asia-Pacific leads with an 11.12% CAGR through 2031, driven by rapid digitization and government tech investment.

How are SMEs influencing demand?

SMEs grow at an 10.92% CAGR by adopting subscription-based cloud and security services that lower entry barriers.

What is driving nearshore delivery adoption?

Enterprises seek time-zone alignment, data-sovereignty compliance, and geopolitical risk mitigation, pushing nearshore models to a 10.18% CAGR.

Why is AI governance important to buyers?

Over 55% of large firms have AI governance boards, making advisory on compliance, ethics, and risk essential in service proposals.

Page last updated on: