Location Based Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 70.08 Billion |

| Market Size (2031) | USD 210.54 Billion |

| Growth Rate (2026 - 2031) | 24.62% CAGR |

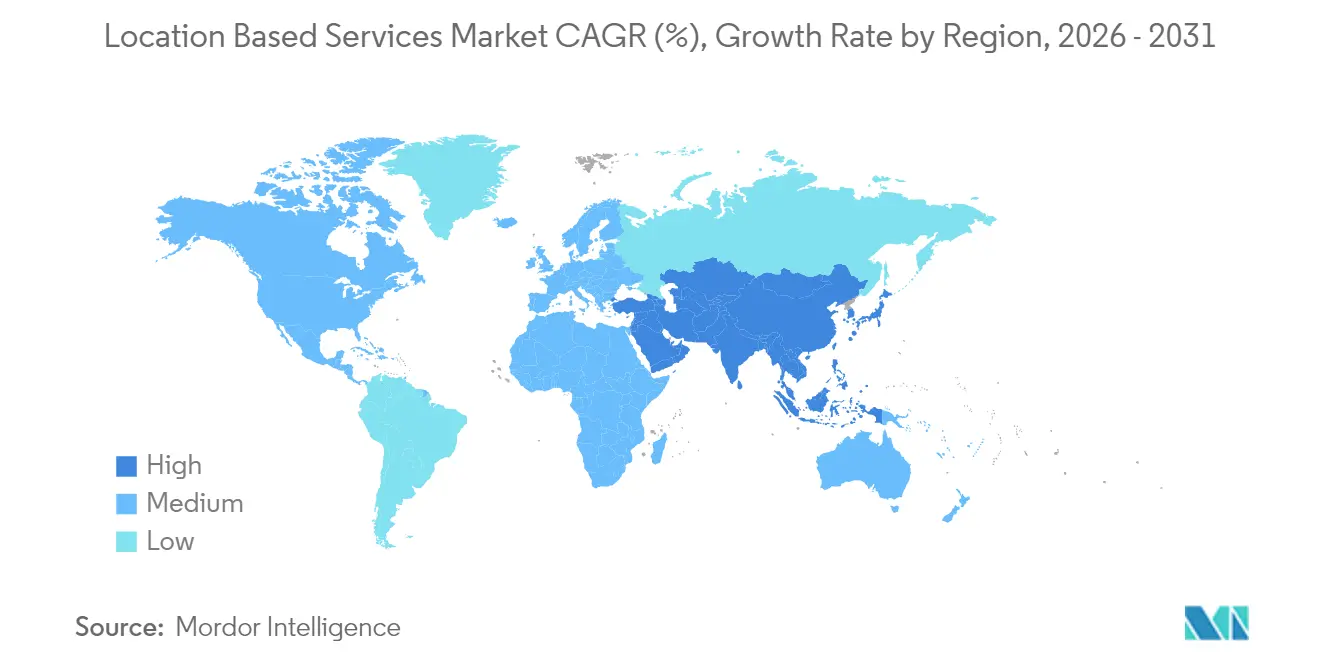

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Location Based Services Market Analysis by Mordor Intelligence

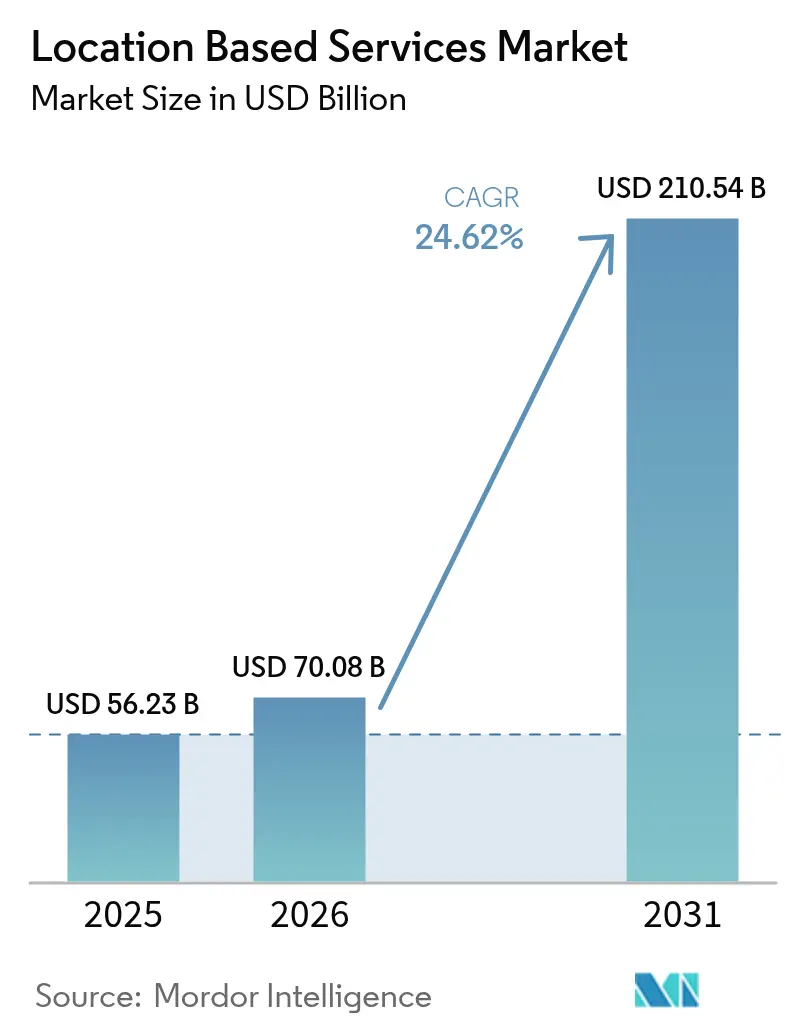

The location-based services market size was valued at USD 56.23 billion in 2025 and estimated to grow from USD 70.08 billion in 2026 to reach USD 210.54 billion by 2031, at a CAGR of 24.62% during the forecast period (2026-2031). This brisk trajectory stems from 5G network-slicing deployments that guarantee sub-meter accuracy, mandatory emergency-call regulations that enforce Advanced Mobile Location, and the rise of digital-twin logistics hubs that depend on real-time location systems. Intensifying hyper-local advertising budgets, centimeter-grade satellite augmentation, and AI-driven indoor positioning all expand addressable use cases, prompting enterprises to embed location intelligence across marketing, safety, and industrial automation workflows. Market participants therefore focus on multi-modal positioning engines that blend GPS, UWB, BLE, Wi-Fi FTM, and sensor fusion to deliver seamless indoor-outdoor coverage. Mergers, high-value partnerships, and compliance spending drive consolidation, while privacy regulation shapes commercial models toward explicit-consent engagement.

Key Report Takeaways

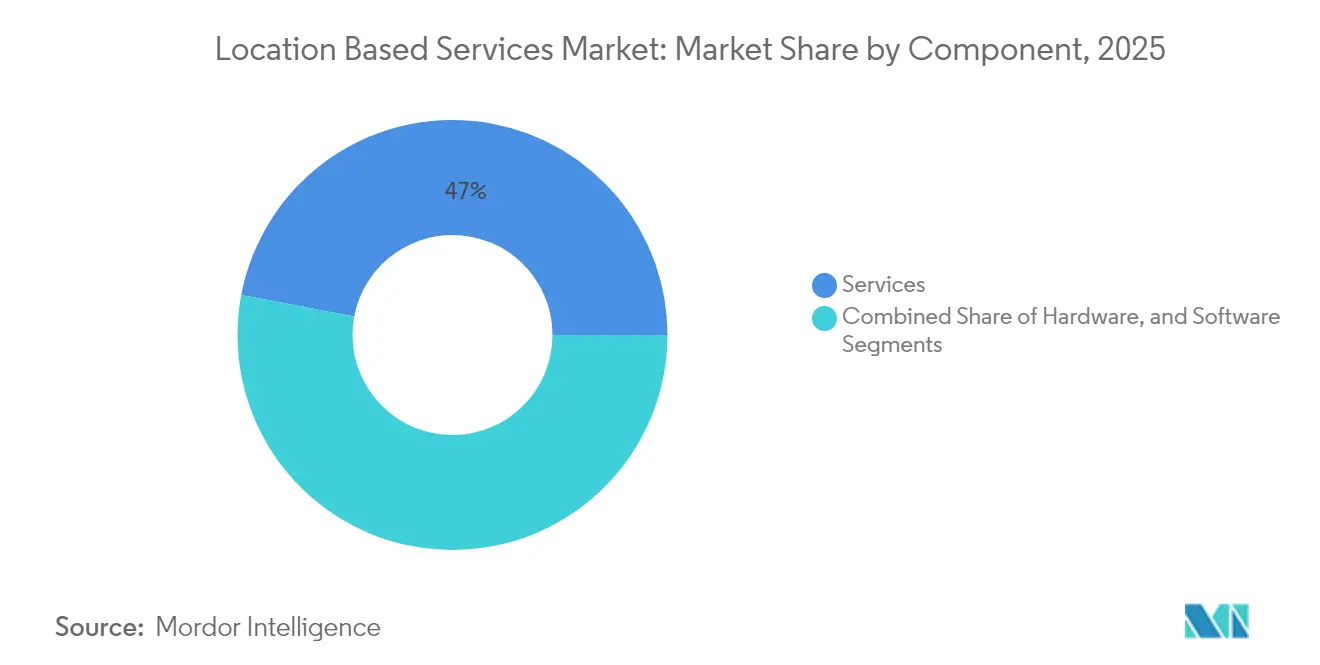

- By component, services held 47.02% of location-based services market share in 2025; software is forecast to post a 26.05% CAGR through 2031.

- By location type, outdoor applications accounted for 67.94% of the location-based services market size in 2025, whereas indoor positioning is projected to climb at a 27.45% CAGR to 2031.

- By core technology, GPS/A-GPS commanded 46.92% of the location-based services market share in 2025; UWB is forecast to post a 27.12% CAGR through 2031.

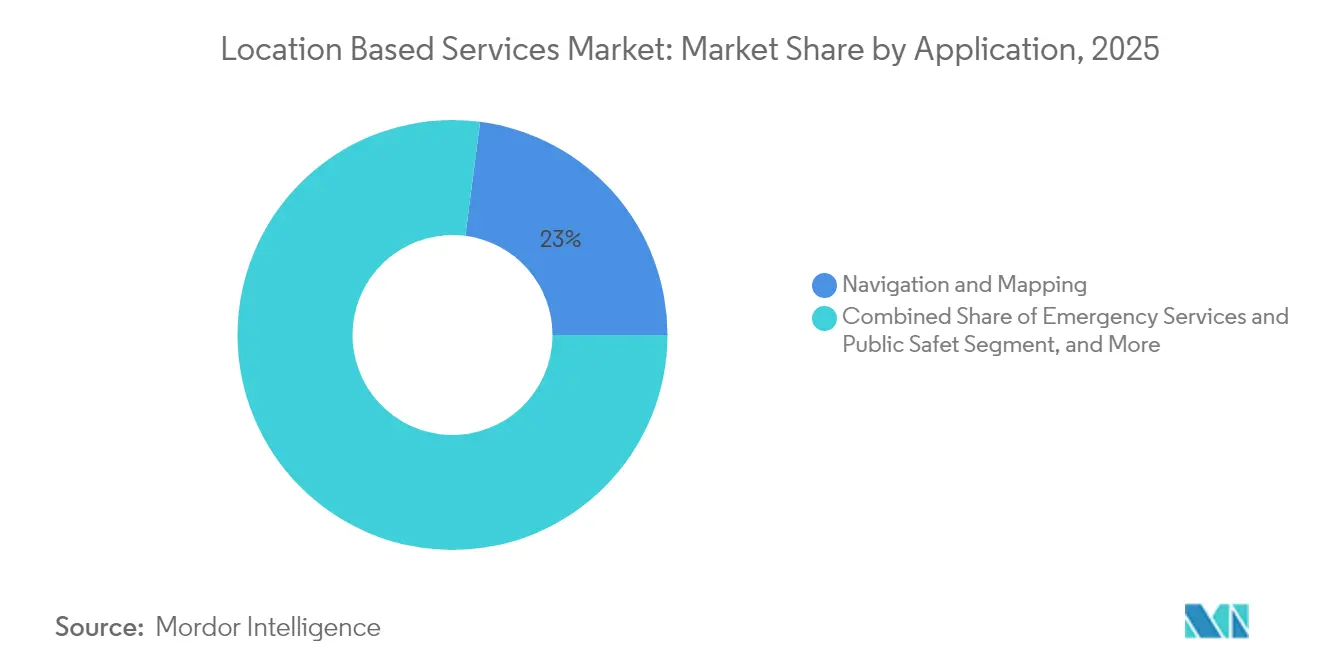

- By application, Navigation and Mapping commanded 22.95% of 2025 revenue, while Location-Based Advertising and Promotion is pacing the fastest at a 27.98% CAGR through 2031.

- By end-user industry, Transportation and Logistics held 22.31% share in 2025; healthcare and life sciences recorded the highest growth outlook at 25.94% CAGR between 2026 and 2031.

- By geography, North America commanded 36.35% of 2025 revenue, while Asia-Pacific is pacing the fastest at a 25.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Location Based Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosion of hyper-local advertising budgets | +4.2% | Global, with North America leading | Medium term (2-4 years) |

| Mandates for e-911 and AML emergency accuracy in OECD markets | +3.8% | OECD countries, EU mandatory since 2022 | Short term (≤ 2 years) |

| Rise of indoor positioning via BLE, UWB and sensor fusion | 5.1% | Global, concentrated in urban centers | Medium term (2-4 years) |

| 5G network slicing enabling sub-meter latency LBS | 4.7% | Asia-Pacific core, spill-over to North America and EU | Long term (≥ 4 years) |

| Proliferation of 'digital twin' logistics hubs needing RTLS | 3.9% | Global, industrial clusters priority | Medium term (2-4 years) |

| Satellite-based augmentation (SBAS, multi-GNSS) for cm-grade precision | 3.8% | Global, aviation and agriculture focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Explosion of hyper-local advertising budgets

Marketers plan to allocate 20%-plus of budgets to local campaigns in 2025, up from 46% in 2024, as geofencing proves effective for foot-traffic uplift. Google Maps already monetizes USD 11.1 billion annually through ad placements. Retailers adopting location-triggered push notifications report sharp increases in in-store conversions, validating the revenue-expansion thesis. Greater location granularity also supports dynamic creative optimization, letting brands tailor messages to micro-markets. As a result, the location-based services market gains sustained demand from advertising technology platforms, publishers, and brands eager to link online intent with offline purchase paths.

Mandates for e-911 and AML emergency accuracy in OECD markets

The European Electronic Communications Code requires AML on all smartphones, delivering caller coordinates within 50 m for 87% of emergencies [1]ETSI, “Advanced Mobile Location Standard Now Mandatory on All European Smartphones for Emergency Calls,” etsi.org. The UK experience shows a 4,000-fold accuracy boost versus Cell-ID, cutting response times and potentially saving 7,500 lives over 10 years. More than 30 nations have adopted AML, while the US is tightening E-911 vertical-accuracy rules. Telcos must therefore upgrade positioning cores and hand-off APIs, fueling spending on hybrid GNSS, Wi-Fi, and sensor-assisted solutions. Compliance budgets directly expand the location-based services market as operators embed advanced location middleware within network cores and end-user apps.

Rise of Indoor Positioning via BLE, UWB and Sensor Fusion

UWB achieves sub-30 cm accuracy in 95% of industrial trials through time-of-arrival and angle-of-arrival techniques. BLE beacons deliver 92.7% dynamic floor-level precision in multi-story atria. Combining Wi-Fi FTM, UWB, and inertial sensors further suppresses drift, ensuring reliable navigation inside hospitals, airports, and factories. Hospitals deploying RTLS solutions cut search time for wheelchairs and beds, improving patient throughput, as demonstrated at Oulu University Hospital. These results illustrate why indoor accuracy advances are central to unlocking asset-tracking, way-finding, and AR-commerce opportunities across the location-based services market.

5G Network Slicing Enabling Sub-meter Latency LBS

3GPP Release 18 introduces bandwidth aggregation and carrier-phase analytics, enabling sub-meter outdoor positioning [2] Ericsson, “5G Advanced Positioning in 3GPP Release 18,” ericsson.com. Network slices grant guaranteed latency and QoS for mission-critical localization, such as autonomous drones and remote surgery. Demonstrations in commercial standalone 5G networks show indoor accuracies of 2-3 m when fused with BIM data. Operators see a USD 100 billion healthcare revenue pool tied to 5G location services by 2026. These capabilities encourage industrial enterprises to procure slice-backed RTLS, amplifying demand within the location-based services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened consumer push-back on location privacy | -2.8% | Global, strongest in EU and California | Short term (≤ 2 years) |

| Regulatory fragmentation (GDPR, CCPA, India DPDP Act) | -3.2% | Global, varying compliance requirements | Medium term (2-4 years) |

| Indoor mapping standardisation lag increases integration cost | -2.1% | Global, concentrated in urban centers | Medium term (2-4 years) |

| RF-signal multipath and interference in dense urban cores | -1.9% | Global, metropolitan areas priority | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened consumer push-back on location privacy

Surveys show 71% of users will only share location after explicit consent. GDPR mandates data-minimization, while CCPA imposes opt-out mechanics, reducing always-on tracking coverage by up to 30%. India’s DPDP Act introduces extra consent layers, compelling providers to invest in differential-privacy and federated-learning models that add engineering cost. These shifts slow data-collection velocity, tempering certain advertising revenue streams inside the location-based services market.

Regulatory fragmentation (GDPR, CCPA, India DPDP Act)

Cross-border data-transfer constraints require localized data centers, inflating infrastructure bills by 15-25% for multi-region operators. Conflicting rules—GDPR’s erasure right versus CCPA portability—drive parallel compliance stacks that drain 20-30% of developer bandwidth. Smaller vendors face disproportionate cost burdens, encouraging acquisitions by capital-rich incumbents. The compliance drag therefore modestly suppresses the CAGR of the location-based services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Propel Adoption

Services represented 47.02% of 2025 revenue as enterprises outsourced design, deployment, and support to managed-service experts. Software, however, is forecast to log a 26.05% CAGR, underscoring how AI analytics convert raw pings into business actions. Large 3PLs integrating digital-twin command centers illustrate why turnkey suites attract premium subscriptions. Meanwhile, hardware growth stays positive as UWB anchors and BLE gateways proliferate in healthcare campuses.

The location-based services market size for software subscriptions climbs steadily as Mapbox’s MapGPT and TomTom’s Azure integrations let automakers push over-the-air upgrades without refreshing on-board units. Service integrators bundle hardware, cloud dashboards, and analytics, ensuring lower total cost of ownership for clients and reinforcing recurring-revenue visibility.

By Location Type: Indoor Momentum Builds

Outdoor positioning still dominates owing to mature GNSS ecosystems, yet indoor deployments are scaling fast. The location-based services market share for outdoor stood at 67.94% in 2025; indoor positioning is tracking a 27.45% CAGR through 2031, suggesting convergence down the line. Hospitals, malls, and airports deploy BLE and UWB tags to cut asset-search cycles and guide visitors, inching the indoor slice toward parity with outdoor during the forecast horizon.

Hybrid solutions hand-off seamlessly between GPS, 5G, Wi-Fi, and Bluetooth, preserving user experience. Standardisation consortia continue refining accuracy benchmarks, which should trim calibration costs and unlock pent-up demand, expanding the overall location-based services market.

By Core Technology: UWB Ascends

GPS/A-GPS commanded 46.92% of 2025 value; Ultra-Wideband is the fastest mover at 27.12% CAGR thanks to centimeter-level accuracy that suits robotics, warehousing, and secure-access applications. Wi-Fi FTM remains popular for cost-effective indoor fixes, while BLE gains uptake in energy-sensitive devices. 5G Advanced positioning will further compress error margins, challenging satellite reliance in urban cores and propelling multi-sensor fusion sales within the location-based services market.

RFID and NFC technologies serve specialized applications in asset tracking and contactless interactions, particularly in logistics and retail environments where short-range positioning suffices for inventory management and customer engagement. The convergence of multiple positioning technologies creates hybrid solutions that optimize accuracy and reliability across different use cases, with sensor fusion techniques combining Wi-Fi Fine Time Measurement (FTM), UWB, and Inertial Measurement Units (IMU) to reduce positioning errors through maximum likelihood estimation

By Application: Advertising Overtakes Navigation

Navigation and mapping retained the largest absolute revenue at 22.95% in 2025, yet location-based advertising and promotions sprint ahead at 27.98% CAGR as retailers pivot toward location-triggered offers. Asset-tracking remains essential for logistics compliance. Emergency services modules enjoy stable demand under AML mandates, while gaming and AR unlock new monetization after landmark deals such as the USD 3.5 billion Niantic acquisition.

Social media and engagement platforms increasingly integrate location features to enhance user experiences and enable targeted content delivery, while the convergence of artificial intelligence and location services creates new application categories that combine real-time positioning with predictive analytics. The shift toward contextual location services reflects changing user expectations for privacy-preserving applications that activate location features only when explicitly requested, rather than continuous background tracking that raises privacy concerns.

By End-user Industry: Healthcare Leads Growth

Transportation and logistics accounted for 22.31% of 2025 turnover, but healthcare is scaling fastest at 25.94% CAGR as hospitals invest in patient flow optimisation and asset safety. Retail leverages geofencing to cut card-false-decline rates by 30%. Manufacturing taps private 5G RTLS for automated guided vehicles, while government agencies embed AML for public safety, reinforcing cross-sector revenue diversity inside the location-based services market.

Manufacturing and industrial applications benefit from private 5G networks that enable precise asset tracking and automation, while telecom and IT services sectors integrate location capabilities into network optimization and customer service applications.

Geography Analysis

North America generated the largest slice at 36.35% in 2025 on the back of AML-ready smartphone penetration and robust cloud infrastructure. High-value contracts such as HERE Technologies’ USD 1 billion AWS alliance illustrate the region’s scale. Federal E-911 deadlines ensure continuous operator investment, while automotive OEMs trial lane-level HD maps for Level-3 autonomy.

Asia-Pacific is the fastest-growing at 25.17% CAGR, with unique mobile subscribers on track to hit 2.1 billion by 2030 and contribute USD 880 billion to GDP . Standalone 5G rollouts in China, Korea, and Japan foster network-based positioning APIs; SBAS constellations such as GAGAN complement GNSS for precision farming. Governments champion data-governance frameworks that balance innovation with privacy, encouraging domestic ecosystem formation and enlarging the location-based services market size across the region.

Europe maintains steady momentum through stringent privacy leadership that nurtures consumer trust. AML has been mandatory on all smartphones since 2022, catalyzing backend upgrades among carriers and PSAPs. An emerging crop of privacy-focused startups employs differential-privacy to meet GDPR, enriching service diversity. Southern and Eastern European cities trial U-Space corridors requiring reliable drone positioning, adding a new adjacency.South America and Middle East and Africa remain nascent but promising. Brazil adopts SBAS for aviation, while Gulf smart-city programs deploy BLE m-commerce beacons in mega-malls. African regional aviation bodies collaborate on SatNav-Africa SBAS, sowing foundational infrastructure for future precision-agriculture and transport services. Collectively these initiatives broaden the geographic footprint of the location-based services market.

Mordor Intelligence provides coverage of the location based services market across other key regional markets, including Middle East and Africa, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Arab Emirates, Nigeria, Japan, India, France, Canada, Germany, and Spain incorporating local coverage and market participation, as required.

Regulatory Landscape

Regulation for location-based services is tightening around two core themes, emergency-location performance and the lawful processing of sensitive location data. In the United States, FCC activity around Next Generation 911 (NG911) and location-based routing continues to push actionable vertical-location delivery (including HAE and AGL formats) to Public Safety Answering Points, with Federal Register rulemaking activity in 2025 and deployment deadlines for z-axis or dispatchable-location capabilities for nationwide CMRS providers by April 2025. In parallel, enforcement scrutiny around how carriers and platforms handle location data is increasing, reinforced by a June 2026 US Supreme Court decision upholding FCC authority to issue fines tied to mishandling of customer location information under Section 222 of the Communications Act.

In Europe, privacy and data-minimization obligations under GDPR continue to shape consent-led commercial models, while AI governance adds another requirement set for location-driven AI systems. Regulation (EU) 2024/1689 (EU AI Act) becomes fully applicable on August 2, 2026, raising expectations around training-data quality, data governance, and bias controls for high-risk AI uses that can intersect with geospatial and location analytics. For LBS providers operating globally, these overlaps between telecom rules, privacy laws, and AI governance increase compliance engineering, documentation, and audit readiness as part of product delivery.

Value Chain Analysis

The location-based services value chain starts with positioning and context signals (GNSS/GPS and A-GPS, cellular and 5G positioning, Wi-Fi FTM, BLE, UWB, and sensor data), along with foundational geospatial content such as maps, POIs, and indoor maps. These inputs feed into location platforms and middleware that provide APIs, SDKs, and geospatial databases, then into application layers for navigation and mapping, advertising and promotion, emergency services, and asset and fleet tracking. System integrators and managed service providers package deployment, calibration, and ongoing operations, especially for enterprise indoor RTLS in healthcare, logistics, and industrial campuses.

Downstream performance depends on data quality, coverage, and the ability to maintain accuracy in GNSS-challenged environments such as dense urban cores and indoors. This pushes the ecosystem toward multi-modal and visual approaches. Recent capability moves reflect the direction of travel: Niantic Spatial launched VPS 2.0 in April 2026 to deliver centimeter-level positioning using visual cues rather than GPS, and HERE Technologies announced HERE Location Reasoning in May 2026 to offload spatial computation for more deterministic, location-aware AI outcomes. These additions expand the platform layer by widening the toolset available to developers beyond radio-only positioning, while improving reliability of location-aware automation in supply-chain and robotics use cases.

Competitive Landscape

The location-based services market features moderate concentration. Platform giants Google, Apple, and Microsoft bundle mapping SDKs into OS ecosystems, securing default positioning channels. Specialized firms HERE, TomTom, and Mapbox compete on neutral-platform HD maps and developer tooling. Strategic alliances dominate: HERE’s USD 1 billion AWS pact scales AI streaming maps; TomTom renews Azure Maps integration through 2030; Mapbox pairs with Hyundai AutoEver for immersive 3D navigation in next-generation infotainment.

M&A accelerates: Powerfleet bought Fleet Complete for USD 200 million to deepen telematics, Viavi acquired Spirent for USD 1.3 billion to boost PNT test capabilities, and LocationMind purchased Irys for US expansion. Patent filings cover hybrid GNSS-cellular positioning with transactional overlays, underscoring IP differentiation.

Indoor-position leaders IndoorAtlas, Sewio Networks, and Pointr harness magnetic-field mapping and UWB to challenge outdoor incumbents. Startups focusing on privacy-preserving analytics gain traction amid tightening regulation, while chip vendors including Qualcomm and Silicon Labs embed low-power ranging engines into IoT SoCs.

Location Based Services Industry Leaders

Google LLC (Alphabet Inc.)

Apple Inc.

Cisco Systems, Inc.

IBM Corporation

HERE Global B.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opening is forming at the intersection of high-precision positioning and AI-native experiences, where enterprises look for deterministic, auditable outcomes rather than best-effort coordinates. HERE Technologies introduction of HERE Location Reasoning in May 2026 highlights demand for geospatial grounding that converts location queries into structured execution flows for AI, which aligns with operational needs in logistics control towers and digital-twin environments that consume real-time location streams. The opportunity is strongest for vendors that can combine mapping, rules, and real-time telemetry into enterprise-grade location decisioning, particularly where workflows require traceability under privacy and emerging AI governance.

Resilient positioning for autonomy and last-mile operations is another practical use-case area, especially where GPS degrades. Niantic Spatial commercialization of visual positioning with deployments tied to delivery robotics, alongside its April 2026 VPS 2.0 launch, points to active pull for centimeter-level alternatives supporting urban navigation, robotics, and AR. In public safety, ongoing NG911 location-based routing work and the standardization of vertical location reporting expand demand for hybrid stacks that deliver dispatchable, actionable location to PSAPs. Providers that integrate GNSS, Wi-Fi, and sensor fusion with compliance-ready interfaces stand to benefit from this work.

Recent Industry Developments

- April 2026: Cisco documented AnyLocate capabilities in Catalyst 9800 Series Wireless Controller software (IOS XE 26.1.x), combining UWB with Wi-Fi Fine Time Measurement to support indoor wayfinding and asset tracking. The update places enterprise Wi-Fi infrastructure in the role of a sensor fabric for location intelligence, reducing reliance on standalone positioning gateways and accelerating indoor LBS deployments across campuses and buildings.

- July 2025: Uber partnered with Baidu to deploy driverless vehicles globally using Apollo Go. The collaboration connects a large ride-hailing platform with an autonomous mobility stack, lifting the emphasis on reliable, real-time positioning and mapping for scaled deployments across multiple geographies.

- January 2024: HERE Technologies unveiled a USD 1 billion collaboration with AWS to deliver AI-powered live-streaming maps aimed at automating enterprise workflows. By scaling cloud-native map streaming and tooling, the partnership reinforces the platform layer that many LBS applications rely on for routing, geofencing, and real-time contextualization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid and free location-based services delivered through software and supporting services that use a device or asset location to trigger actions, content, navigation, analytics, or alerts across indoor and outdoor settings.

Scope exclusions: We exclude pure satellite navigation hardware sales when it is not bundled with an ongoing software or service revenue stream.

Segmentation Overview

- By Component

- Hardware

- Software

- Services

- By Location Type

- Indoor

- Outdoor

- By Core Technology

- GPS / A-GPS

- Wi-Fi and WLAN Triangulation

- Bluetooth Low Energy (BLE)

- Ultra-Wideband (UWB)

- RFID and NFC

- By Application

- Navigation and Mapping

- Location-Based Advertising and Promotion

- Asset and Fleet Tracking

- Emergency Services and Public Safety

- Gaming and Augmented Reality

- Social Media and Engagement

- By End-user Industry

- Retail and FMCG

- Transportation and Logistics

- Healthcare and Life Sciences

- Telecom and IT Services

- Oil, Gas and Energy

- Government and Public Sector

- Manufacturing and Industrial

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the demand and policy context for location-aware apps. We referred to public sources such as FCC E911 and location accuracy updates, US FTC privacy guidance, and European Commission privacy and consent guidance, alongside standards bodies including 3GPP and IEEE for positioning-related releases.

We also used sources such as ITU indicators on mobile broadband, the World Bank for macro and digitization signals, and peer-reviewed papers that track indoor positioning performance and adoption. Company filings, product documentation, and investor materials were checked to understand how revenue is recognized across software, services, and related enablement. To reduce missed players and to validate revenue ranges, we relied on paid subscriptions for company financials and intelligence, news and financials, and patent databases. These examples are not exhaustive, and many other public sources were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming which parts of location-based services are actually monetized, and how pricing shifts with accuracy, latency, and privacy requirements. We spoke with solution owners, telecom and platform stakeholders, system integrators, and enterprise buyers across APAC, EMEA, and the Americas so desk research assumptions could be tested and corrected before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | APAC: 44% |

| Mid tier: 54% | Functional/Unit leaders: 38% | EMEA: 32% |

| Smaller Players: 14% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

Sizing used a top-down build where mobile broadband users and connected device footprints were translated into addressable use cases, then filtered by penetration across application types such as navigation, proximity marketing, and fleet and asset tracking. To keep totals realistic, we corroborated the outputs with selective bottom-up approximations using sampled vendor revenues, channel checks in managed services, and simple ASP x volume logic for location transactions where pricing is visible.

Key inputs tracked include smartphone and mobile internet penetration, 4G and 5G coverage progression, indoor positioning adoption in large venues and logistics sites, advertising spend shifting to hyperlocal formats, and regulatory signals such as emergency location requirements that can accelerate usage. For forecasting, scenario analysis was run around privacy and consent enforcement, 5G rollout pace, and enterprise deployment cycles, then reconciled with the consensus ranges we heard from practitioners. Where bottom-up checks were thin for smaller providers, ranges were inferred from comparable offerings and then tightened using regional adoption indicators.

Data Validation & Update Cycle

Outputs were checked against independent signals such as device shipment trends, telecom coverage metrics, and enterprise deployment activity, and variances were investigated before sign-off. When a driver moved too fast for a single assumption to hold, for example a step-change in privacy rules or a material technology shift in indoor accuracy, we re-contacted sources to re-test the input.

Each dataset and calculation pass goes through multi-step analyst review so that unit logic, currency treatment, and growth rates stay consistent across regions and years. Reports are refreshed annually, and interim updates are completed when major events materially change adoption or pricing. Before delivery, a final review pass is done so clients receive the most current view available.

Mordor Intelligence's Location Based Services Market Size Compared With Other Published Estimates

Published market values for location-based services often differ because firms do not count the same revenue streams, and they also use different base years and growth paths. Differences also show up when one study bundles adjacent markets into the same number, which can make growth appear higher than what buyers can actually capture.

Standalone real-time location systems deployments sold as facility infrastructure projects are treated outside Mordor Intelligence's scope unless they are monetized as part of an ongoing location-based service offering, which reduces overlap with broader tracking markets. Other gaps usually come from how indoor versus outdoor use cases are weighted, whether hyperlocal advertising is counted net or gross, and how quickly ASPs are assumed to rise with 5G-driven accuracy gains and privacy compliance costs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 56.23 B (2025) | |

| Global Advisory A | USD 44.64 B (2025) | Uses a slower uplift path into 2026-2033 and appears to apply more conservative penetration for enterprise indoor and logistics use cases, which reduces the near-term addressable pool. |

| Industry Publisher B | USD 31.17 B (2025) | Shows internal inconsistency across sections for 2025-2026, and the smaller 2025 value likely reflects a narrower application set or a tighter monetization filter that excludes some managed and analytics-related revenue. |

The comparison suggests the spread is mainly driven by what is included as monetized service revenue versus adjacent infrastructure, and by how quickly adoption is assumed to scale in enterprise and advertising-led use cases. By tying the model to observable adoption indicators and then pressure-testing it with interviews, the final figure stays explainable and repeatable even when inputs vary by region and application.

Key Questions Answered in the Report

What is driving the rapid expansion of the location-based services market?

Growth stems from 5G positioning accuracy, AML emergency mandates, and rising hyper-local advertising budgets, pushing the market toward a 24.62% CAGR to 2031.

Which segment of the location-based services market is growing fastest?

Indoor positioning is projected to rise at a 27.45% CAGR as BLE and UWB deliver sub-meter accuracy inside hospitals, malls, and factories.

How large is the location-based services market size for software solutions?

Software revenue is expected to climb sharply within overall market size, aided by AI analytics that transform raw pings into actionable intelligence.

Why is Asia-Pacific considered the most promising geography?

Standalone 5G rollouts, SBAS initiatives, and a forecast 2.1 billion mobile-subscriber base fuel a 25.17% CAGR, the highest globally.

Page last updated on: