Headless Commerce Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 6.17 Billion |

| Growth Rate (2026 - 2031) | 20.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Headless Commerce Platform Market Analysis by Mordor Intelligence

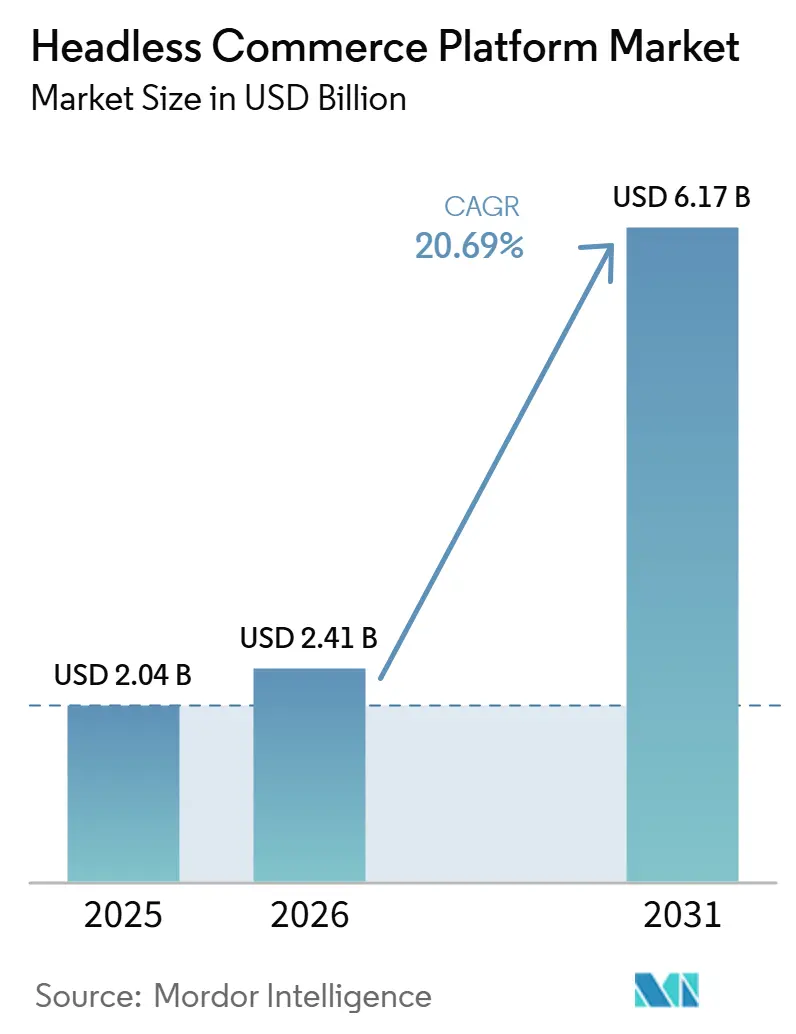

The headless commerce platform market size is expected to increase from USD 2.04 billion in 2025 to USD 2.41 billion in 2026 and reach USD 6.17 billion by 2031, growing at a CAGR of 20.69% over 2026-2031. The headless commerce platform market is moving forward as enterprises and mid-sized brands replace tightly coupled commerce stacks with API-first systems that let them update the storefront without rewriting the commerce core. This shift matters because faster launches, easier channel expansion, and deeper AI integration now depend on flexible architecture rather than on isolated front-end redesign work. The current revenue mix still reflects enterprise buying patterns, with software leading current spend while services grow quickly, as deployment, integration, and customization remain demanding. The headless commerce platform market is also expanding beyond early enterprise adopters, as hybrid deployments gain traction and SMEs enter through more guided implementation paths. Competition is now centered on AI-ready platform design, reusable integrations, and lower deployment friction, which is pushing vendors to compete on operating flexibility as much as on storefront performance.

Key Report Takeaways

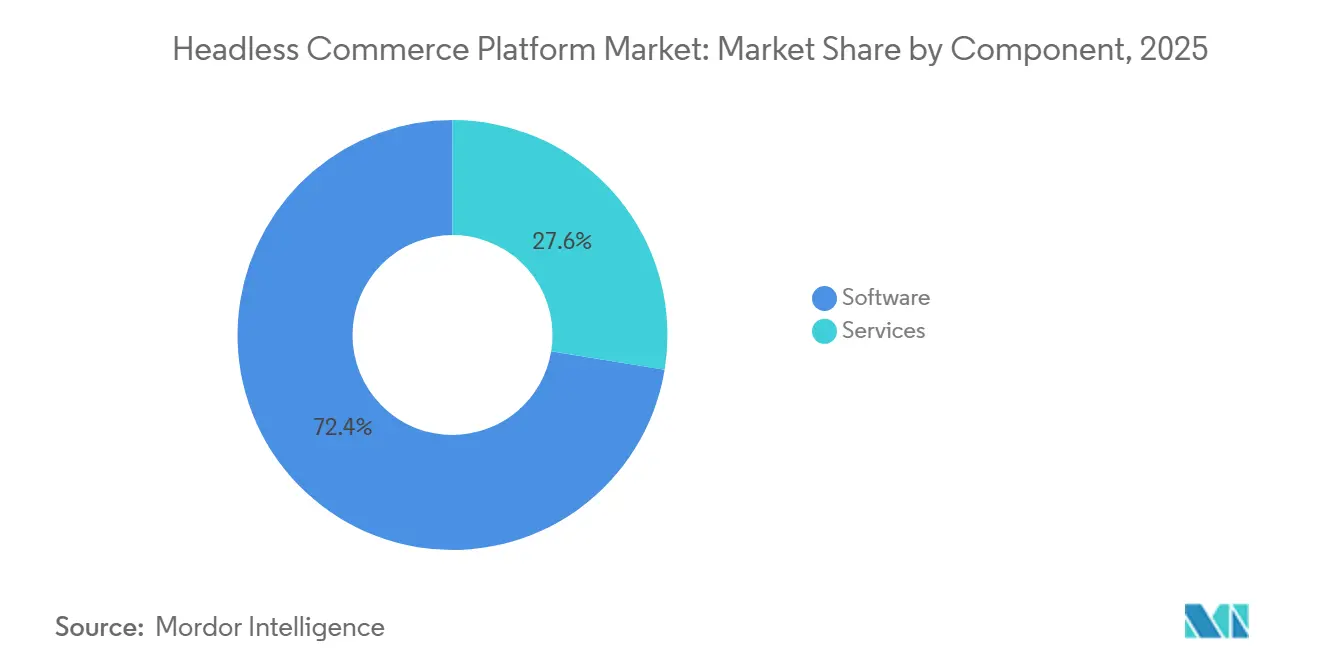

- By component, software held a 72.41% share of the headless commerce platform market in 2025, while services are projected to expand at a 23.84% CAGR through 2031.

- By deployment mode, cloud-based deployment held 68.19% share in 2025, while hybrid deployment is projected to expand at a 22.63% CAGR through 2031.

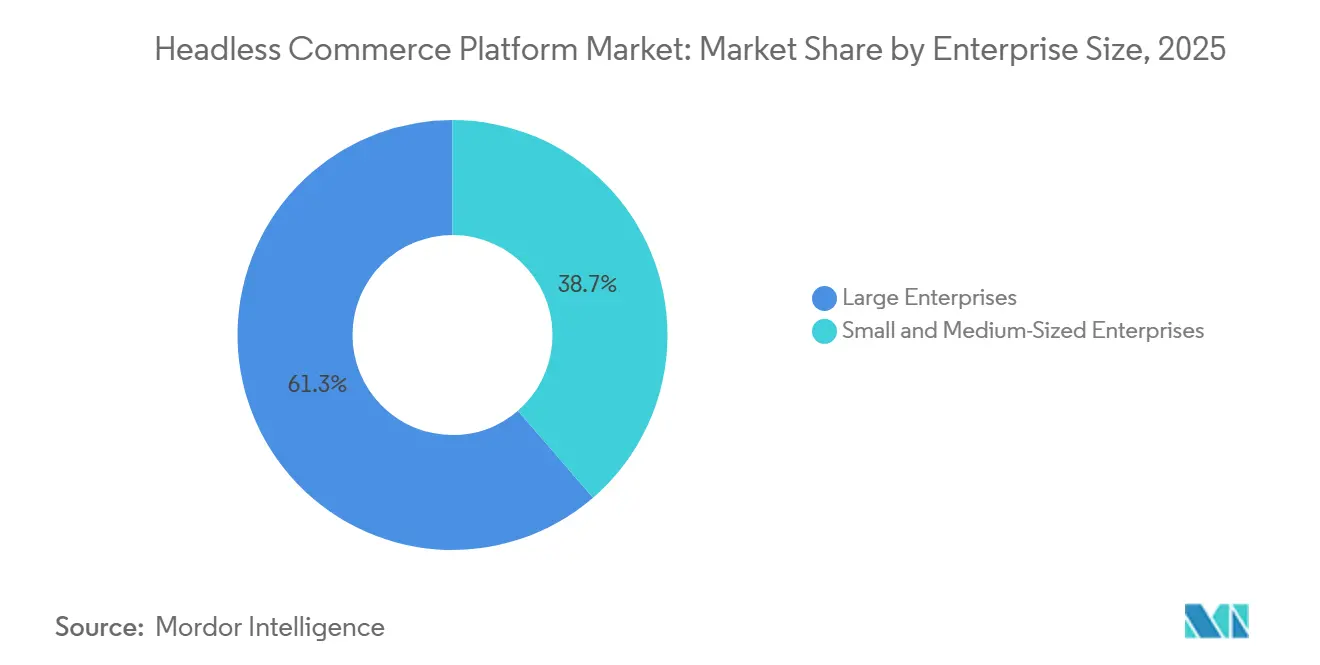

- By enterprise size, large enterprises held 61.34% share of the headless commerce platform market in 2025, while SMEs are projected to expand at a 24.17% CAGR through 2031.

- By application, retail and e-commerce accounted for 34.82% of the market share in 2025, while direct-to-consumer commerce is projected to expand at a 26.43% CAGR through 2031.

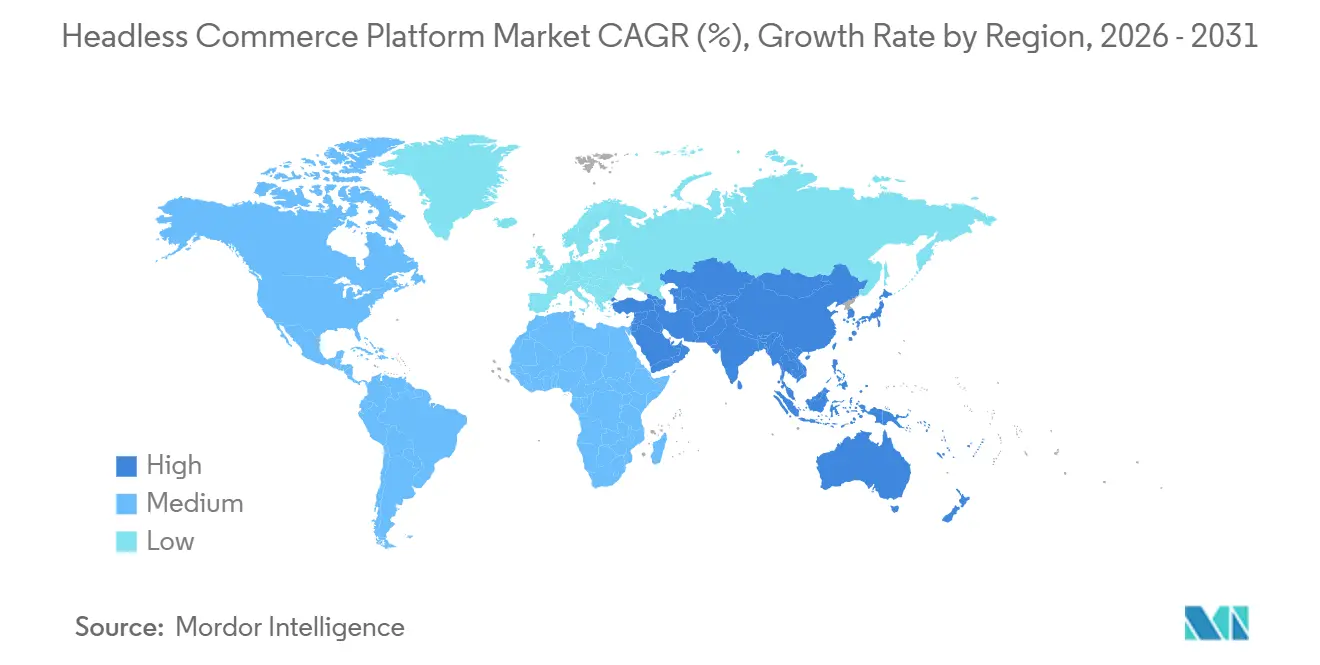

- By geography, North America held 36.71% share of the headless commerce platform market in 2025, while Asia-Pacific is projected to expand at a 25.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Headless Commerce Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Omnichannel Customer Experiences | +4.2% | Global | Short term (≤ 2 years) |

| Accelerated Shift Toward API-First Commerce Architectures | +3.6% | Global | Short term (≤ 2 years) |

| Adoption of Composable Commerce and Microservices | +3.1% | North America and EU | Medium term (2-4 years) |

| AI-Driven Personalization and Real-Time Merchandising | +2.5% | Global | Medium term (2-4 years) |

| Enterprise Migration Away from Monolithic Commerce Stacks | +2.0% | North America and EU | Medium term (2-4 years) |

| Expansion of Headless Commerce Into B2B and D2C Use Cases | +1.7% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Omnichannel Customer Experiences

Consistent delivery across websites, mobile apps, in-store kiosks, social channels, and voice interfaces has become a basic operating requirement for modern commerce teams, which is raising demand for systems that can serve multiple touchpoints from a single back-end logic layer. Traditional monolithic platforms often force companies to add middleware to keep inventory, pricing, catalog content, and personalization aligned across channels, which slows and costs more each new channel launch. In the headless commerce platform market, decoupled architecture addresses this problem by enabling the same commerce engine to support different front-end experiences without requiring repeated back-end rework. That matters because channel expansion is no longer a one-time digital program; it is a continuous operating process that requires rapid content changes, campaign launches, and interface updates across customer touchpoints. The result is that omnichannel demand is pushing the headless commerce platform market toward solutions that shorten launch cycles, limit technical debt, and maintain consistent core commerce operations even as customer interaction points multiply.

Accelerated Shift Toward API-First Commerce Architectures

API-first design has moved from a developer preference to a formal buying requirement, as enterprises seek commerce systems that integrate cleanly with content, search, payments, tax, logistics, and analytics tools. The MACH Alliance reported in 2026 that 92% of surveyed organizations had implemented or were actively adopting composable technology, indicating that API-first planning has moved deeply into mainstream enterprise roadmaps.[1]MACH Alliance, “Enterprise Technology Report: AI: From Pilot to Production,” MACH Alliance, machalliance.org That level of adoption indicates that the headless commerce platform market is no longer being shaped by niche experimentation, as architecture flexibility is now directly tied to integration speed and operating readiness for future digital programs. commercetools reinforced this position in June 2026 when it linked Autonomous Commerce to real-time AI activity across pricing, inventory, and personalization, showing that machine-led commerce operations depend on an API-native foundation. In the headless commerce platform market, companies that delay API-first adoption not only accept slower integration times but also reduce their ability to deploy AI-driven commerce processes at scale.[2]commercetools, “commercetools Introduces ‘Autonomous Commerce’,” commercetools, commercetools.com

Adoption of Composable Commerce and Microservices

Composable commerce is gaining ground because it allows companies to assemble a best-fit stack rather than forcing every commerce function into one bundled suite. A 2025 study in the International Journal of Research Trends and Innovations described migrating from Oracle Commerce to a MACH-based, composable architecture using commercetools, resulting in 60% faster deployment cycles and a 45% reduction in operational costs.[3]International Journal of Research Trends and Innovations, “Composable Commerce at Scale: Architecting Future Proof Digital Platforms,” International Journal of Research Trends and Innovations, doi.org The same study cited a 22% increase in mobile conversions and a 35% reduction in infrastructure incidents after the composable migration, underscoring why architecture choice is being evaluated as a commercial performance issue rather than an internal technology preference. The MACH Alliance also reported in 2026 that 78% of organizations with fully implemented composable foundations achieved measurable AI ROI, compared with 13% in early planning stages. In the headless commerce platform market, this blend of faster deployment, lower operating friction, and stronger AI readiness continues to support microservices adoption among enterprise buyers.

AI-Driven Personalization and Real-Time Merchandising

AI personalization is now a practical buying priority because merchants want storefronts and product experiences that respond to live catalog, pricing, inventory, and behavioral signals with minimal latency. Headless design meets this requirement by exposing structured commerce data through APIs, making it easier for AI systems to read and act on current information. Elastic Path released AI-optimized Product Experience Manager data feeds in December 2025, enabling merchants to expose products, price books, bundles, and promotions to AI answer engines without custom API development.[4]Elastic Path, “Elastic Path Makes Product Catalogs AI-Ready With Data Structured for Programmatic Consumption,” Elastic Path, elasticpath.com commercetools made a similar case in June 2026, presenting Autonomous Commerce as the operating layer for AI agents making real-time decisions across pricing, inventory, campaigns, and personalization. This is pushing the headless commerce platform market toward vendors that can combine performance, clean data structures, and secure AI permissions inside a single operating model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity With Legacy Systems | -2.5% | Global | Short term (≤ 2 years) |

| Shortage Of Specialized API and Front-End Engineering Talent | -2.1% | Global | Medium term (2-4 years) |

| Elevated Total Cost of Ownership for Custom Builds | -1.5% | North America and EU | Medium term (2-4 years) |

| Security, Data Governance, and Compliance Execution Gaps | -1.2% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Systems

Legacy ERP, order management, product information, and customer data systems were often not built for API interaction, so many headless projects become more difficult to implement than they appeared during initial planning. Once teams begin mapping live workflows, data inconsistencies, undocumented process dependencies, and version conflicts tend to surface, stretching project timelines and increasing delivery risk. In the headless commerce platform market, this makes adoption easier for organizations with cleaner architecture and more difficult for businesses with a large installed base of older transactional systems. The problem is especially serious in manufacturing and distribution settings, where deeply embedded back-end systems cannot be replaced within a single budget cycle, even when the front end clearly needs modernization. Integration friction does not weaken the long-term case for headless architecture, but it does keep deployment cycles long and sustains demand for consulting, systems integration, and custom support.

Shortage of Specialized API and Front-End Engineering Talent

Headless deployment requires API design, front-end framework skills, DevOps discipline, and commerce process knowledge within the same delivery environment, and that combination is difficult to hire for in most markets. The challenge is sharper for smaller buyers because one poor hiring decision, one delayed agency handoff, or one weak integration design can remove much of the speed benefit that headless migration is supposed to deliver. In the headless commerce platform market, the talent gap keeps implementation risk elevated, even as software licensing becomes easier to access through packaged cloud offerings. Vendors are responding with more guided tooling and reusable development paths, but these measures still depend on sound technical oversight and do not eliminate the need for experienced architectural decisions. The result is a slower first-time adoption curve for some buyers and continued reliance on specialist partners to deliver production-grade storefronts and integrations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platform Dominance Masks A Services-Led Growth Dynamic

Software held 72.41% of the headless commerce platform market share in 2025, while services are projected to expand at a 23.84% CAGR through 2031. That mix reflects the strength of recurring platform subscriptions among API-native vendors, especially in enterprise deployments where the commerce engine is treated as a strategic system rather than as a simple storefront tool. It also shows that buyers still commit the largest budgets to the core software layer before they refine how delivery, orchestration, and optimization work around it. In the headless commerce platform market, software remains the largest revenue pool because it anchors the long-term relationship between platform vendors and merchants.

Services are growing faster because implementation consulting, systems integration, customization, and ongoing managed support continue well after the initial launch. This pattern suggests that many projects in the headless commerce platform market are still architecture transformations rather than straightforward software installations, and that keeps external expertise closely tied to the buying cycle. The present growth rate also shows that customers are still paying for the effort required to connect content, catalog, checkout, tax, and operational systems into a stable working environment. The headless commerce platform industry, therefore, remains shaped by a dual revenue structure in which software captures the largest installed base, while services expand with each new deployment, migration, and enhancement cycle.

By Deployment Mode: Hybrid Architectures Bridge Cloud Ambition And Data Sovereignty

Cloud-based deployment accounted for 68.19% of the headless commerce platform market size in 2025, while hybrid deployment is projected to grow at a 22.63% CAGR through 2031. Leading vendors have built their offerings primarily as managed cloud services, which explains why cloud deployment accounts for the largest share of current revenue. This model appeals to merchants that want faster scaling, reduced infrastructure management, and easier access to frequent feature updates without maintaining a large internal hosting stack. At the same time, on-premises deployment remains relevant where internal controls, established IT policies, or legacy system dependencies still outweigh the speed advantages of a full cloud move.

Hybrid deployment is growing faster because many enterprises want front-end flexibility without shifting every core system and every sensitive dataset into a single outside cloud environment. WEBSALE positions German-hosted, API-first commerce around data sovereignty, which shows that hosting location and data residency have become direct buying factors in parts of Europe. In the headless commerce platform market, hybrid architecture suits organizations that want the benefits of composable storefronts while keeping selected processes close to existing internal systems. That makes hybrid less of a temporary compromise and more of a durable operating model for multinational retailers, regulated sectors, and companies moving through a multi-stage modernization plan.

By Enterprise Size: Large Enterprises Anchor Revenue While SME Adoption Reshapes The Addressable Market

Large enterprises held 61.34% of the market in 2025, while SMEs are projected to expand at a 24.17% CAGR through 2031. Early adoption favored larger organizations because they had the budget, engineering depth, and internal integration capacity needed for complex headless migration programs. That first-mover advantage still shapes current revenue concentration, especially where retailers and manufacturers run layered commerce, content, order, and customer systems across several regions and channels. VTEX reported 3,100 active online stores across 44 countries, serving 2,200 B2C and B2B customers as of December 31, 2025, demonstrating the scale already operating on leading headless platforms.

SMEs are growing faster because deployment tooling, managed hosting, and composable starter patterns are lowering the time and effort needed to launch modern storefronts. In the headless commerce platform market, smaller brands are not entering through lighter versions of enterprise transformation; they are entering through more packaged, more guided, and less engineering-heavy delivery paths. This expands the addressable base beyond companies that can fund long migration cycles and large architecture teams, an important shift for how the category grows from here. It also changes vendor strategy because success increasingly depends on reducing implementation friction while preserving the flexibility that made headless attractive to larger buyers in the first place.

By Application: Retail And E-Commerce Leads, But Direct-To-Consumer Commerce Is The Structural Growth Engine

Retail and e-commerce accounted for 34.82% of the headless commerce platform market size in 2025, while direct-to-consumer commerce is projected to expand at a 26.43% CAGR through 2031. Retail remains the largest application because multi-channel merchants manage large catalogs, seasonal demand shifts, and frequent merchandising changes that expose the limits of monolithic systems. Direct-to-consumer is expanding faster because brands want stronger control over customer data, presentation, and margin capture outside marketplace intermediaries. In the headless commerce platform market, this keeps demand closely tied to the broader move toward owned digital channels and more direct brand-customer relationships.

B2B commerce, marketplace commerce, and other applications together accounted for 65.18% of the market in 2025, indicating that adoption has already spread far beyond consumer storefront modernization alone. Procurement portals, brand-direct ordering flows, and marketplace operations all benefit from a unified back end that can serve different buying journeys without rebuilding core logic for every use case. Marketplace activity is especially important because it requires a single product and inventory system to support owned storefronts, third-party selling points, and social commerce endpoints simultaneously. That breadth of application keeps the headless commerce platform market focused on orchestration, extensibility, and channel-level flexibility rather than on website presentation alone.

Geography Analysis

North America accounted for 36.71% of the headless commerce platform market share in 2025. The region leads because it combines technology-forward retailers, a mature SaaS ecosystem, and an early willingness among enterprises to fund API-first commerce modernization. Vendor presence also reinforces this position, since several leading platform developers built strong commercial footprints in the United States before expanding globally. That concentration of platform expertise supports partner ecosystems, implementation talent, and enterprise sales capacity in the region. Canada and Mexico remain smaller than the United States, but they continue to add relevance in cross-border commerce and regional digital expansion programs.

Europe is the second-largest regional market, with Germany, the United Kingdom, and France standing out as the main demand centers. Spryker has built its offer around complex B2B catalog, aftermarket, and marketplace use cases, and its 2025 product update added a unified AI layer with stronger B2B capabilities. WEBSALE also highlights German-hosted, API-first commerce that addresses data sovereignty needs, showing that regulatory and hosting requirements still shape purchase decisions in parts of the region. South America shows meaningful adoption through Brazil, while Argentina and the rest of South America remain earlier-stage opportunities as digital commerce penetration continues to build.

Asia-Pacific is projected to expand at a 25.92% CAGR through 2031, making it the fastest-growing regional segment in the headless commerce platform market. Growth is being supported by digital commerce expansion across China, India, Southeast Asia, and Japan, where brands need front ends that can change quickly across devices, channels, and content formats. The region also benefits from a leapfrog pattern because many retailers are building modern commerce stacks without the same depth of legacy platform commitments seen in some Western markets. That shortens the path from digital expansion plans to actual headless deployment, especially for mobile-first and content-commerce heavy models. The Middle East and Africa remain smaller in present revenue terms, yet Saudi Arabia and the UAE are building stronger multi-channel retail capacity while Nigeria and South Africa anchor a gradual but expanding adoption base.

Competitive Landscape

The headless commerce platform market remains moderately fragmented, with a small top tier of API-native vendors holding outsized influence in enterprise buying while a longer tail of composable specialists, open-source platforms, and regional providers contests the rest of the field. commercetools, VTEX, and BigCommerce form the clearest top cluster because they combine established customer bases, ecosystem reach, and visible product road maps tied to AI-led commerce operations. commercetools strengthened that position in June 2026 when it introduced Autonomous Commerce and unveiled Sphere, framing AI agents as active participants in pricing, inventory, campaign management, and personalization. VTEX also entered 2026 with meaningful scale, reporting 3,100 active online stores across 44 countries for 2,200 B2C and B2B customers as of the end of 2025. These positions matter because enterprise buyers in the headless commerce platform market increasingly want vendors that can support both channel flexibility and large operational footprints.

Spryker and Elastic Path compete from more specialized positions where complex catalogs, buyer-specific pricing, procurement workflows, and broad composability requirements are more important than mass merchant scale. Spryker’s Summer 2025 product release strengthened B2B features and added a unified AI layer, which supports its standing in industrial and aftermarket commerce environments. Elastic Path expanded its intelligent commerce platform in November 2025 with native advanced search, content management, and hosted front-end services, reducing the third-party work required to complete a full stack. Earlier, in April 2025, Elastic Path launched an AI-ready B2B commerce solution optimized for Model Context Protocol, extending its platform toward subscription handling, rules-based promotions, and AI-assisted B2B workflows. These moves show that competition in the headless commerce platform market is shifting from simple decoupled delivery toward broader AI-ready composable stacks that can support more of the operating environment.

The field still leaves room for open-source entrants, front-end composition tools, and developer-led alternatives to pressure the mid-market and innovation edge of the category. VTEX’s 2025 acquisition of Weni expanded its platform with AI-powered customer experience and conversational service capabilities, which signals that vendors are moving beyond storefront infrastructure into adjacent operating layers. That direction suggests future advantage will depend on data control, partner ecosystem depth, and secure AI permissions as much as on storefront speed alone. The headless commerce platform market therefore remains competitive, but leadership is increasingly defined by which vendors can reduce implementation friction while extending the platform into AI-led commerce workflows.

Headless Commerce Platform Industry Leaders

commercetools GmbH

BigCommerce Holdings, Inc.

VTEX

Spryker Systems GmbH

Elastic Path Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: commercetools introduced Autonomous Commerce and unveiled the Sphere platform on June 9, 2026, defining AI agents as active real-time participants in commerce operations including dynamic pricing, inventory reordering, campaign management, and personalization. Sphere powers over USD 100 billion in annualized GMV at under 60 milliseconds average response time, providing the headless, API-first foundation for enterprise AI agent deployment at scale.

- December 2025: Elastic Path released AI-optimized Product Experience Manager data feeds in general availability on December 9, 2025, enabling merchants to expose structured products, price books, bundles, and promotions to AI answer engines including ChatGPT and Perplexity for agentic and conversational commerce channels.

- November 2025: Elastic Path expanded its intelligent commerce platform with native advanced search, content management, and hosted frontend services on November 12, 2025. The additions reduced third-party dependencies required for a complete headless commerce stack and embedded AI across the full commerce layer in alignment with Elastic Path's Intelligent Commerce platform vision.

- April 2025: Elastic Path launched the first AI-ready B2B commerce solution optimized for Model Context Protocol on April 24, 2025, introducing an AI Product Chatbot, subscription management, rules-based promotions, and sales rep tooling. MCP support enables AI agents to interact efficiently with complex B2B buying workflows, including subscriptions and digital product entitlements.

Global Headless Commerce Platform Market Report Scope

The headless commerce platform market refers to the ecosystem of software solutions and associated services that enable the decoupling of the frontend presentation layer (the "head") from the backend ecommerce functionality (the "body"), such as product information management, cart, and checkout processes. By utilizing APIs to communicate between these two layers, headless commerce platforms allow businesses to deliver highly customized, fast, and seamless shopping experiences across multiple digital touchpoints including web, mobile applications, social media, IoT devices, and in-store kiosks without being restricted by the limitations of a traditional monolithic backend. The market encompasses cloud-based, on-premise, and hybrid deployment models, catering to organizations ranging from large enterprises to small and medium-sized enterprises. These platforms are utilized across various applications such as B2B commerce, direct-to-consumer (D2C) retail, and marketplace commerce to provide the agility needed to rapidly adapt to evolving consumer expectations, integrate emerging technologies, and scale digital commerce operations efficiently.

The Headless Commerce Platform Market Report is Segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Application (Retail and E-Commerce, B2B Commerce, Direct-to-Consumer Commerce, Marketplace Commerce, and Others), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small And Medium-Sized Enterprises |

| Retail and E-Commerce |

| B2B Commerce |

| Direct-to-Consumer Commerce |

| Marketplace Commerce |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Software | ||

| Services | |||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small And Medium-Sized Enterprises | |||

| By Application | Retail and E-Commerce | ||

| B2B Commerce | |||

| Direct-to-Consumer Commerce | |||

| Marketplace Commerce | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the headless commerce platform market?

The headless commerce platform market stands at USD 2.41 billion in 2026 and is projected to reach USD 6.17 billion by 2031 at a CAGR of 20.69%.

Which deployment model is growing fastest through 2031?

Hybrid deployment is the fastest-growing mode, with a projected 22.63% CAGR, even though cloud-based deployment held the largest 68.19% share in 2025.

Why do large enterprises still lead spending on headless commerce platforms?

Large enterprises held 61.34% share in 2025 because they were earlier adopters and had the budgets, engineering depth, and integration capacity required for complex migrations.

Which application area is expanding the fastest?

Direct-to-consumer commerce is growing the fastest at a 26.43% CAGR, while retail and e-commerce remained the largest application with 34.82% share in 2025.

Which region leads revenue and which one grows the fastest?

North America led with 36.71% share in 2025, while Asia-Pacific is projected to post the fastest growth at a 25.92% CAGR through 2031.

How are leading vendors competing in 2026?

Vendors are competing through AI-ready platform design, broader composable stacks, and tools that lower deployment friction. commercetools, VTEX, Spryker, and Elastic Path are all extending beyond storefront delivery into AI-led operating workflows.

Page last updated on: