Service Delivery Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.42 Billion |

| Market Size (2031) | USD 10.6 Billion |

| Growth Rate (2026 - 2031) | 7.40% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

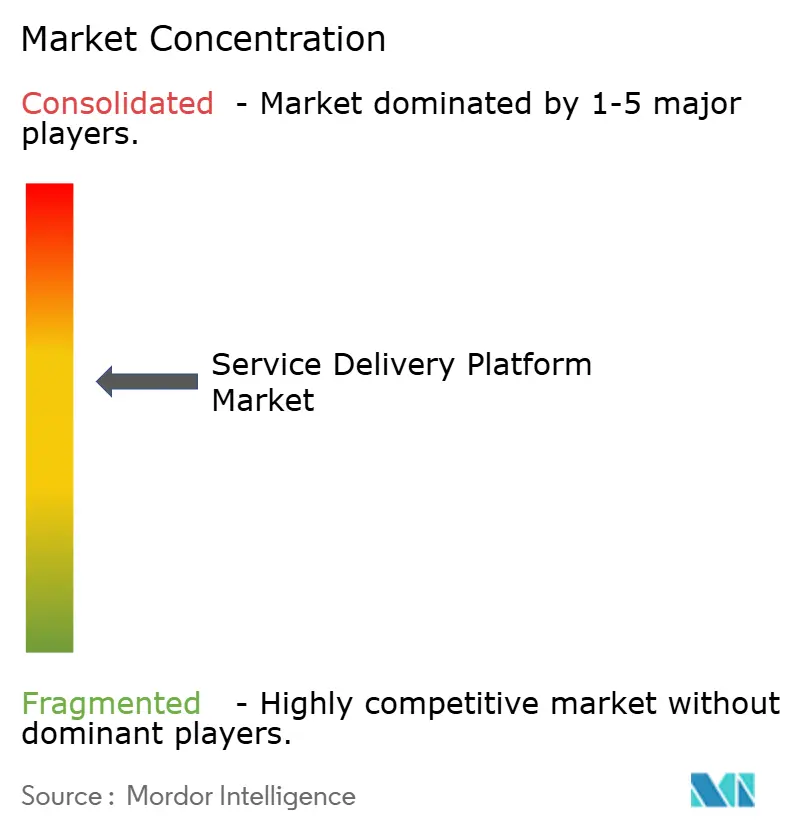

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Service Delivery Platform Market Analysis by Mordor Intelligence

The service delivery platform market size is expected to grow from USD 6.91 billion in 2025 to USD 7.42 billion in 2026 and is forecast to reach USD 10.6 billion by 2031 at 7.40% CAGR over 2026-2031. 5G standalone deployments, cloud-native transformation strategies and the urgent replacement of legacy OSS/BSS stacks combine to pull capital toward platform modernization. Operators are investing in microservices architectures that shorten release cycles, enable network slicing, and monetize low-latency enterprise use cases. Software-defined agility is further amplified by private-5G adoption in industrial campuses and by rising demand for hyper-personalized consumer propositions. Competitive intensity is rising as hyperscale cloud providers, traditional network vendors and niche software specialists converge on the same opportunity set, forcing consolidation, partnerships and open-API strategies.

Key Report Takeaways

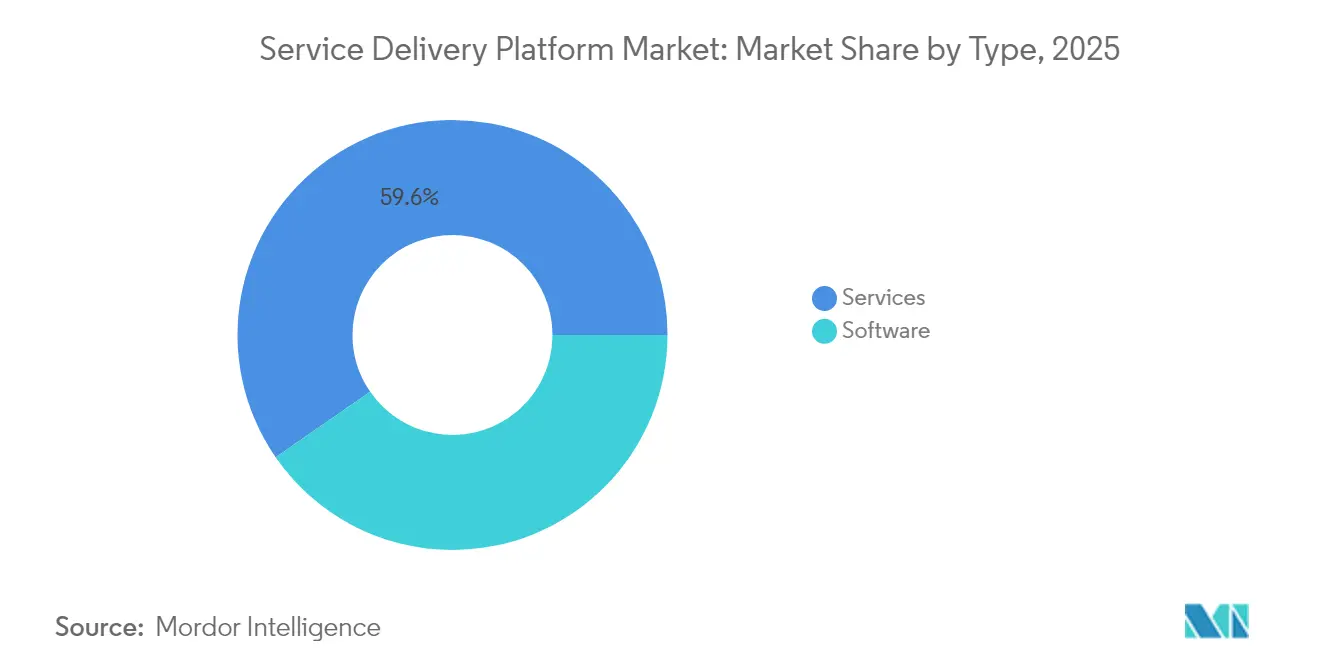

- By type, services captured 59.62% of service delivery platform market share in 2025, while software is expanding at an 11.25% CAGR through 2031.

- By deployment mode, the cloud segment led with a 62.55% revenue share in 2025 and is accelerating at a 13.85% CAGR to 2031.

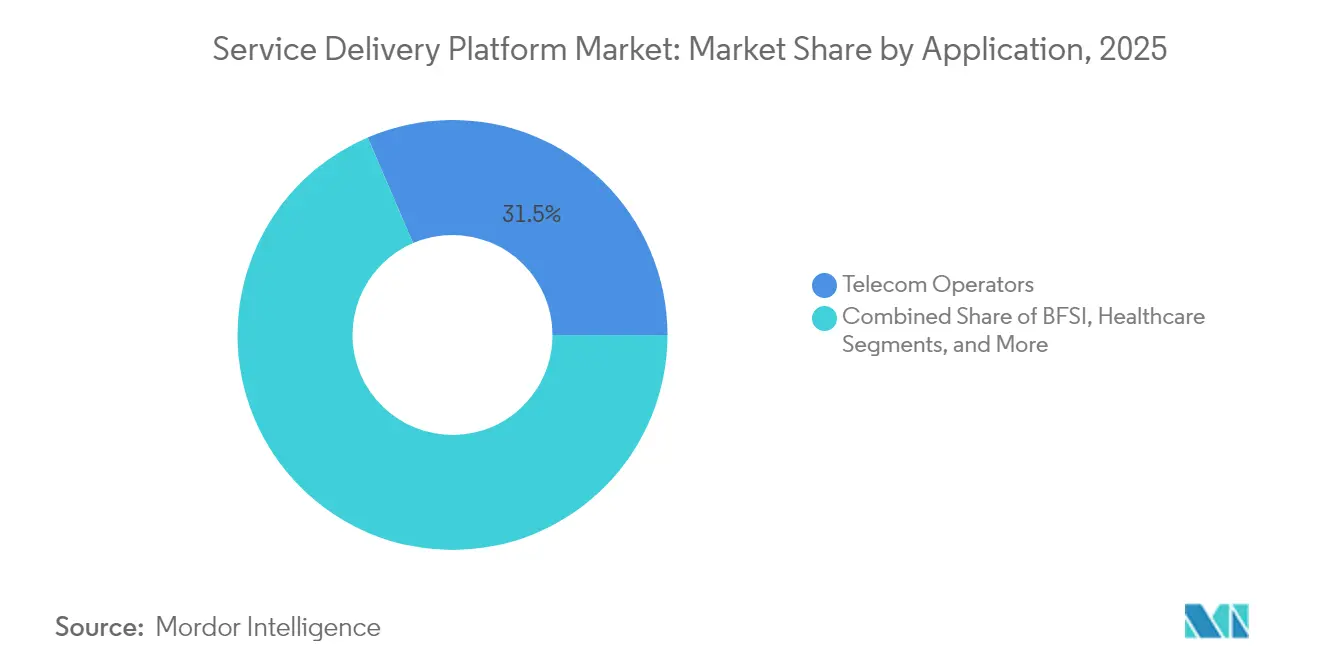

- By application, telecom operators accounted for 31.45% of the service delivery platform market size in 2025, whereas healthcare is projected to post the fastest 12.25% CAGR through 2031.

- By network type, wireless platforms dominated with 70.90% share in 2025 and are forecast to advance at a 11.75% CAGR over the outlook period.

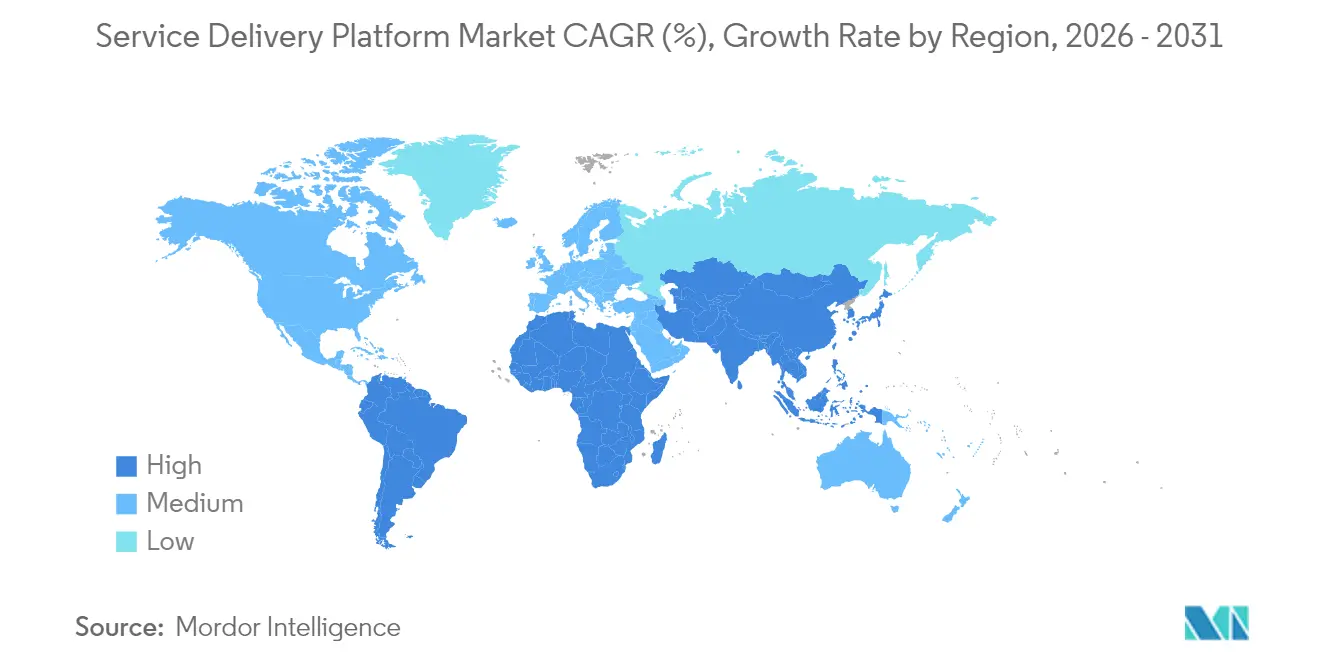

- By geography, North America held 31.20% of the service delivery platform market in 2025, yet Asia-Pacific is poised to generate the highest 13.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Service Delivery Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-outs driving flexible service orchestration | +2.1% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Cloud-native transformation among telecom operators | +1.8% | North America, Europe | Long term (≥ 4 years) |

| Demand for digital BSS and hyper-personalised services | +1.5% | Developed markets worldwide | Medium term (2-4 years) |

| IoT proliferation requiring scalable service management | +1.3% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Microservices and containerisation adoption | +1.0% | Cloud-mature markets globally | Medium term (2-4 years) |

| Network slicing and private-5G monetisation | +0.9% | North America, Europe, select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Roll-outs Driving Flexible Service Orchestration

Standalone 5G build-outs obligate operators to adopt orchestration layers that allocate network resources in milliseconds and expose capabilities through open APIs. Ericsson estimates network slicing alone can unlock USD 200 billion in new value, underscoring why Singtel commercialised consumer slicing in 2024 to create premium 5G+ tiers [1]Ericsson Research Team, “200 Billion Reasons to Explore Network Slicing,” Ericsson, ericsson.com. Global mobile core spending jumped 32% year-over-year in Q1 2025 as carriers moved workloads onto cloud-native cores. Service-based architecture inherently suits microservices, and platform vendors are embedding policy engines that monetise latency, bandwidth and security guarantees. The service delivery platform market therefore captures demand for intent-based orchestration that links 5G radio resources to enterprise SLAs. As more slices go live in healthcare, logistics and media, revenue opportunities will multiply and platform scalability will become a competitive determinant.

Cloud-native Transformation Among Telecom Operators

Hyperscale alliances are recasting telco IT roadmaps. Vodafone’s decade-long USD 1.5 billion pact with Microsoft targets 300 million subscribers across Europe and Africa, shifting workloads to Azure and embedding DevOps practices that shrink release cycles from months to weeks. Telefónica Germany migrated 45 million users to a cloud-native 5G core without service disruption, evidencing maturity of containerised network functions. Continuous integration and automated testing now underpin rapid feature activation, while dynamic resource scaling improves cost discipline. Vendors are responding with SaaS delivery models and pay-as-you-grow licensing, expanding the addressable service delivery platform market. Over the long term, cloud-first strategies will make telcos less dependent on proprietary hardware and more agile in launching cross-vertical propositions.

Demand for Digital BSS and Hyper-personalised Services

Customer experience differentiation hinges on real-time charging, convergent billing and AI-driven targeting. Nuuday cut product launch times and operating expenses by deploying Netcracker’s cloud BSS/OSS suite. Indosat Ooredoo Hutchison onboarded 100 million subscribers onto a digital monetisation platform in just 18 days, demonstrating execution speed achievable with microservices. AI models surface contextual offers, boosting ARPU and reducing churn. As telcos evolve into digital ecosystems curating fintech, cloud gaming and IoT services, scalable BSS engines become foundational. This demand channel widens the service delivery platform market by tying monetisation logic directly into service orchestration layers.

IoT Proliferation Requiring Scalable Service Management

Billions of connected assets across factories, logistics corridors and smart cities necessitate device-agnostic lifecycle control. EdgeIQ’s Symphony platform showcases DeviceOps functions spanning provisioning, firmware updates and policy enforcement. Private-5G pilots in automotive plants highlight the need for edge orchestration that processes sensor data locally while integrating with central policy engines. Predictive maintenance, real-time quality control and autonomous guided vehicles each depend on deterministic throughput and latency parameters. Platforms that mesh 5G, MEC and AI workflows therefore secure a pivotal role in industrial digitalisation, reinforcing long-run demand in the service delivery platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX to modernise legacy OSS/BSS | −1.2% | Emerging markets worldwide | Short term (≤ 2 years) |

| Cyber-security and data-privacy concerns | −0.8% | Europe, North America | Medium term (2-4 years) |

| Vendor lock-in in cloud-SDP ecosystems | −0.6% | Multi-vendor global deployments | Long term (≥ 4 years) |

| Shortage of DevOps / cloud-native talent | −0.5% | Asia-Pacific and other emerging regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX to Modernise Legacy OSS/BSS

The upfront investment to replace mainframe-era stacks deters many mid-tier and emerging-market operators from full-scale digitalisation. Airtel Sri Lanka’s transformation trimmed operating IT spend by 80% but required phased capital injections and specialist consulting support [2]Light Reading Staff, “How Airtel Sri Lanka Revamped Its BSS,” Light Reading, lightreading.com. Smaller carriers often resort to overlay approaches that leave core silos intact, tempering immediate platform revenues. While cloud subscription models soften balance-sheet pressure, integration complexity still commands sizeable professional services budgets. As a result, near-term adoption curves can flatten, moderating the overall service delivery platform market CAGR by an estimated −1.2 percentage points.

Cyber-security and Data-privacy Concerns

Expanded threat surfaces accompany multicloud architectures, and regulators are tightening compliance screws. Thales reports that 81% of telcos remain uneasy about 5G security posture, citing proliferation of SaaS endpoints. The UK’s Telecoms Security Act imposes 258 individual controls, pushing operators to audit code pipelines, strengthen supply-chain transparency and segment networks. European data-localisation laws force complex multi-region deployment blueprints that can inflate cost and delay roll-outs. Heightened scrutiny obliges vendors to harden platforms against DDoS, API abuse and insider threats, adding overhead and lengthening procurement cycles, which collectively shave an estimated −0.8 percentage points off forecast growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Software Adoption Outpaces Services

Software revenue in the service delivery platform market is climbing at an 11.25% CAGR, eclipsing the headline growth rate as operators migrate from proprietary appliances to API-centric orchestration suites. Services still generated 59.62% of 2025 turnover, reflecting ongoing demand for integration, migration, and managed operations. Vendors allocate substantial R&D—Huawei alone spent USD 24.8 billion in 2024—toward AI, analytics, and low-code tooling that compress service innovation timelines.

Platform software enables composable microservices that abstract network complexity and promote partner onboarding. Projects such as Nexign’s framework cut integration windows from three months to barely four weeks, allowing MegaFon to roll out 170-plus offers swiftly . Professional services remain indispensable during legacy cut-over phases and DevOps enablement. Taken together, software gains will steadily lift the service delivery platform market share of modular, license-based products.

By Deployment Mode: Cloud Dominance Reinforces Agility

Cloud implementations contributed 62.55% of global revenue in 2025 and are increasing at a 13.85% CAGR as carriers de-risk capital commitments and pursue elastic scaling. The cloud-first trajectory is evidenced by T-Mobile migrating its prepaid BSS onto AWS to cut hardware overhead and improve uptime.

Hybrid blueprints are emerging in financial services and public-sector contexts where data residency rules mandate on-premise control planes. Vendor toolkits now automate CI/CD pipelines and provide zero-touch network function upgrades, further tilting preference toward cloud. Consequently, the service delivery platform market size attributed to cloud deployments is expected to eclipse USD 5.4 billion before 2031.

By Application: Healthcare Sets the Pace

Telecom operators commanded 31.45% of 2025 spending; nonetheless, healthcare applications are projected to record a market-leading 12.25% CAGR on the back of telemedicine, electronic health record integration and remote diagnostics. Platforms such as HealthNXT synthesise patient data flows, shaping holistic care journeys and lowering administrative friction.

Banks and insurers digitise customer onboarding and fraud detection, leveraging convergent charging engines to embed financial products inside connectivity bundles. Government digital-service agendas and retail omnichannel strategies add further momentum. Collectively, cross-vertical uptake enlarges the service delivery platform market size and diversifies revenue streams away from pure connectivity.

By Network Type: Wireless Leads Value Creation

Wireless architectures delivered 70.90% of 2025 revenue and are pacing at a 11.75% CAGR as millimeter-wave 5G, private networks and network slicing mature. Enterprises such as Tesla deploy dedicated 5G systems to automate robotics and autonomous vehicles across plants, stimulating demand for ultra-reliable low-latency communication layers.

Wireline fibre continues to underpin backhaul and edge interconnect but yields slower incremental growth. Fixed-mobile convergence strategies, illustrated by KPN’s product bundles, drive integrated orchestration requirements. As virtualised RAN and open RAN proliferate, seamless coordination between radio and core domains will crystallise, consolidating wireless networks’ primacy within overall platform spending.

Geography Analysis

North America retained 31.20% of revenue in 2025, buoyed by aggressive 5G roll-out timetables, supportive spectrum policy and deep cloud expertise. Large-scale mergers such as Verizon’s USD 20 billion Frontier acquisition and Charter’s USD 34.5 billion Cox purchase expand fibre footprints and stimulate end-to-end platform consolidation. T-Mobile’s joint venture with KKR to gain Metronet accelerates integrated fixed-wireless propositions. Regulatory focus on supply-chain security and submarine cable oversight creates parallel compliance consulting demand, shaping vendor service portfolios in the region.

Asia-Pacific is forecast to generate a 13.65% CAGR, the fastest worldwide, as operators pivot toward beyond-connectivity revenue that already formed 19.9% of H1-2024 takings. China Mobile and China Unicom channel scale advantages into cloud, video and industrial digital services. StarHub’s Cloud Infinity programme leverages multi-cloud orchestration with AWS, Google Cloud and Nokia to deliver sub-10 millisecond latency for enterprise workloads, illustrating architectural innovation. National digital-economy policies funnel incentives toward private 5G and smart-manufacturing roll-outs, reinforcing regional momentum.

Europe represents a mature, regulation-heavy environment where the EU’s AI Act and data-sovereignty mandates influence architectural choices. Vodafone’s Azure partnership exemplifies long-term capital commitment to cloud-native transformation across several national markets. The UK Telecoms Security Act compels tier-1 operators to implement 258 cybersecurity controls, prompting accelerated platform upgrades. Although South America and the Middle East and Africa start from lower baselines, rising mobile penetration and government digitalisation agendas signal vibrant future demand for agile service delivery frameworks.

Regulatory Landscape

Service delivery platforms sit at the intersection of telecom security, cloud assurance, and data governance, with compliance obligations increasingly shaped by security codes and cloud control frameworks rather than telecom-only rules. In the United Kingdom, the Telecommunications (Security) Act has been operationalized through a detailed control set, and in June 2026 the UK government published a draft revised Telecommunications Security Code of Practice. The update reinforces expectations around secure design, supply-chain assurance, and operational controls that affect SDP procurement requirements and audit readiness.

Technical standards bodies are also tightening the baseline for interoperability and assurance in orchestration-centric architectures. The German Federal Office for Information Security (BSI) released the C5:2026 cloud computing compliance catalog, incorporating new requirements aligned to European cloud certification work (EUCS). This affects cloud-hosted SDP deployments used by telecom operators and adjacent verticals with data-residency needs. In parallel, ITU-T Recommendations such as Q.4142 (June 2024) and Y.3046 (September 2024) set reference requirements for service orchestration and service-aware networking, giving cross-vendor teams a shared technical vocabulary for compliance mapping in multi-domain service delivery.

Value Chain Analysis

The SDP value chain starts with core technology inputs, including cloud infrastructure, Kubernetes/container platforms, databases, security tooling, and telecom network functions and mediation. It then moves into platform software and integration layers such as service orchestration, policy control, charging and billing, API exposure, and analytics or AI, along with assurance capabilities. Network OEMs and OSS/BSS vendors typically package these functions as suites, while hyperscale cloud providers supply carrier-grade cloud primitives and managed services. Systems integrators and managed service providers handle migration, integration, and run operations. Downstream, communications service providers and enterprises use SDPs to launch and monetize digital services, often through B2B2X models that include application partners, CPaaS providers, and industry solution specialists.

Interface and ecosystem alignment increasingly relies on industry specifications, including GSMA Operator Platform requirements (OPG.02) and TM Forum frameworks such as the GB1067 Ecosystem Reference Architecture. These frameworks influence how vendors expose APIs and onboard partners. Constraints are concentrated in specialized silicon and electronics supply as more service delivery shifts to cloud-native cores, edge, and high-capacity transport. Lead-time pressure for advanced networking components has been amplified by tariff-driven component uncertainty (Supplyframe Commodity IQ, April 2025) and logistics disruption, including Gulf shipping rerouting that has caused multi-week delays for semiconductors and telecom-critical electronics (June 2026). These frictions increase the appeal of software-first deployments and phased modernization programs that reduce dependence on tightly constrained hardware refresh cycles.

Competitive Landscape

The service delivery platform market shows moderate fragmentation, with top vendors collectively controlling less than 50% of global revenue. Traditional equipment suppliers Huawei, Ericsson, and Nokia leverage long-standing operator relationships, yet they increasingly coexist with agile OSS/BSS pure-plays, hyperscale cloud providers, and vertical-specific specialists. Nokia’s USD 2.3 billion purchase of Infinera boosts integrated optical-to-cloud capabilities and highlights a strategy to embed transport intelligence inside platform portfolios [4]Semiconductor Today Editorial, “Nokia to Acquire Infinera for USD 2.3 Billion,” Semiconductor Today, semiconductor-today.com.

Hyperscalers pursue similar ground: Microsoft divested Metaswitch to Alianza to streamline focus while still embedding Azure Operator Nexus as a carrier-grade cloud fabric. Ericsson finalised the USD 6.2 billion Vonage acquisition to fuse CPaaS assets with 5G network APIs, enabling developers to build low-latency applications that monetise network quality attributes. Meanwhile, SaaS disruptors such as Amdocs MVNO&GO promise to launch virtual operators in weeks, further compressing time-to-revenue.

Strategic alliances and ecosystem openness dictate competitive advantage. API-first software houses win niche vertical deals while systems integrators provide multicloud orchestration and security assurance. Over the medium term, differentiation will pivot on AI-driven automation, zero-touch operations and ability to monetise network exposure functions, reshaping market share trajectories and merger appetites.

Service Delivery Platform Industry Leaders

Huawei Technologies Co., Ltd.

Nokia Corporation

Ericsson AB

Cisco Systems, Inc.

Amdocs Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operator and enterprise modernization programs are creating whitespace for SDPs that combine orchestration with AI-enabled operations and monetization, while maintaining interoperability with open interface programs. TM Forum activity in June 2026, including the launch of an AI-native Open Digital Architecture (ODA) roadmap and the release of an Agentic AI-Native BSS guidebook (GB1082 v2.0.0) with Huawei at the DTW 2026 Global Summit, offers a practical base for vendors to productize standards-aligned building blocks. This includes Open APIs, composable BSS/OSS, and intent-driven automation, which can reduce integration friction across multi-vendor stacks.

A second opportunity area is the shift of service delivery and network automation into public cloud and enterprise workflow ecosystems, expanding the buyer set beyond telecom IT into platform engineering and operations teams. In June 2026, Nokia expanded its collaboration with AWS to host its Autonomous Networks Fabric on AWS, linking closed-loop automation and AI tooling to cloud infrastructure. At the same time, Aria Systems and ServiceNow launched an agentic BSS offering in June 2026, pointing to an integration path where SDPs connect with enterprise workflow platforms to unify service fulfillment, customer operations, and monetization. Together, these moves reinforce demand for cloud-hosted, API-first platforms that can bridge telco-grade assurance with enterprise automation, especially where data residency and security controls shape deployment blueprints.

Recent Industry Developments

- July 2026: Activeport launched its Global Edge platform internationally and reported contracts with Spark (New Zealand) and ViewQwest (Singapore). The move broadens access to edge and connectivity-enabled service delivery capabilities across multiple operator footprints, supporting B2B service enablement models that depend on consistent orchestration across geographies.

- June 2026: Nokia and Amazon Web Services expanded their collaboration to deliver autonomous networks, positioning Nokia's Autonomous Networks Fabric on AWS and connecting it with cloud AI services such as Amazon Bedrock and Amazon SageMaker. The announcement reinforces public-cloud-based delivery for automation and orchestration workloads, influencing SDP architecture choices toward cloud-native deployments and AI-assisted operations.

- April 2026: Albion and Tecnotree partnered to deliver a next-generation value-added services platform for TELUS in North America, combining Tecnotree's digital platform with managed services from Albion. This strengthens the role of packaged platforms plus services in accelerating time-to-market for new propositions, while highlighting continued operator spend on modernization and monetization layers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from service delivery platforms that help service providers and enterprises create, orchestrate, deliver, and manage digital services across networks, devices, and channels, including platform software and related implementation and support services.

Scope exclusions: This sizing excludes pure network hardware, standalone OSS or BSS tools that do not perform SDP functions, and general IT outsourcing that is not tied to SDP deployments.

Segmentation Overview

- By Type

- Software

- Services

- By Deployment Mode

- On-Premise

- Cloud

- By Application

- Telecom Operators

- BFSI

- Media and Entertainment

- Healthcare

- Retail and E-commerce

- Government and Public Sector

- Others

- By Network Type

- Wireless

- Wireline

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a clean fact base on telecom and enterprise digital service delivery activity, plus the policy and technology shifts that change SDP demand. Public sources such as International Telecommunication Union indicators, OECD telecom and broadband statistics, World Bank digital adoption series, U.S. FCC publications, and Eurostat ICT usage datasets help anchor subscriber, traffic, and connectivity context that supports realistic adoption assumptions.

We also review company annual reports, investor presentations, product documentation, and credible press coverage to understand how platforms are packaged, priced, and sold (license, subscription, or managed service). Where needed, we use paid databases for company financials and intelligence, and patent databases to spot where feature development is accelerating. The desk sources cited here are illustrative only, and many other public references were used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions on adoption, pricing, and deployment mix, because these details vary by operator maturity and enterprise IT priorities. We speak with platform providers, system integrators, telecom operators, and large enterprise buyers across APAC, EMEA, and the Americas so the model can reflect regional rollout timing and procurement cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 46% |

| Mid tier: 42% | Functional/Unit leaders: 39% | EMEA: 29% |

| Smaller Players: 19% | Managers: 47% | Americas: 25% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where telecom and enterprise digital service activity is reconstructed into an addressable demand pool and then filtered through SDP adoption and spend intensity by region. To keep totals realistic, we corroborate results with selective bottom-up checks such as sampled vendor revenue disclosures, channel conversations on typical deal sizes, and a simple ASP times deployment volume approximation for key use cases.

Key model inputs include cloud versus on-premise deployment mix, 5G and network modernization rollout pace, digital service launch frequency, number of enterprise service workflows being automated, and typical contract duration and renewal behavior. When primary feedback shows gaps in smaller-country visibility, we apply peer-market proxies tied to connectivity and IT spend indicators, then adjust based on regional maturity.

For forecasting, scenario analysis is used because adoption can accelerate or slow down with budget cycles and modernization programs. The scenarios are anchored to interview consensus on rollout timing and then checked against observable indicators like connectivity expansion and enterprise cloud adoption trends.

Data Validation & Update Cycle

Validation is done by triangulating multiple outputs and checking whether the implied spend per operator or per enterprise aligns with what respondents describe as feasible budgets. Outliers are reviewed for unit mistakes, currency timing, or double counting between platform software and services, and then the assumptions are reworked until the variance is explainable.

A second analyst reviews the logic, inputs, and conversions before sign-off, and any large changes trigger follow-up questions to selected interviewees. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass so clients receive the most current view.

Mordor Intelligence's Service Delivery Platform Market Estimate Compared With Other Published Estimates

Published market values for service delivery platforms often differ because authors pick different boundaries and timing assumptions, then apply different ways of converting deployments into revenue. Differences also come from whether services are treated as part of SDP revenues, how cloud subscriptions are annualized, and whether the base year reflects an unusually strong or weak spending cycle.

In this study, the spread is mainly explained by whether adjacent monetization and generic cloud application platform revenues are included, plus the use of a 2026 current-year anchor with an explicit split of software and related services that is validated through operator and enterprise buying checks, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.42 B (2026) | |

| Global Consultancy A | USD 6.54 B (2024) | Uses an earlier base year and a broader definition that can blend SDP with wider digital service enablement stacks, which can shift revenue recognition and reduce comparability to a pure SDP scope. |

| Industry Publisher B | USD 7.49 B (2024) | Keeps 2024 as the base year and applies a higher growth path, which may assume faster cloud subscription ramp and earlier 5G-led adoption than what interview-based rollout timing suggests. |

Taken together, the comparison shows that year selection and what gets counted as SDP versus adjacent platforms drive most of the variance. By tying the estimate to clear deployment and pricing variables, then re-checking them with real buyer and supplier feedback, the final number stays traceable and repeatable for planning decisions.

Key Questions Answered in the Report

What is the current size of the service delivery platform market?

The service delivery platform market size reached USD 7.42 billion in 2026 and is forecast to climb to USD 10.6 billion by 2031.

Which deployment model is growing fastest?

Cloud-based deployment leads with a 13.85% CAGR thanks to elastic scaling, lower hardware costs and DevOps-enabled agility.

Why is healthcare the fastest-growing application segment?

Telemedicine, unified patient-journey orchestration and regulatory pushes for interoperable systems are propelling healthcare demand at a 12.25% CAGR.

How does 5G slicing affect service delivery platforms?

Slicing requires real-time orchestration and monetisation of differentiated network attributes, expanding platform functionality and revenue potential.

Page last updated on: