Vitamin Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 62.58 Billion |

| Market Size (2031) | USD 82.5 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vitamin Supplements Market Analysis by Mordor Intelligence

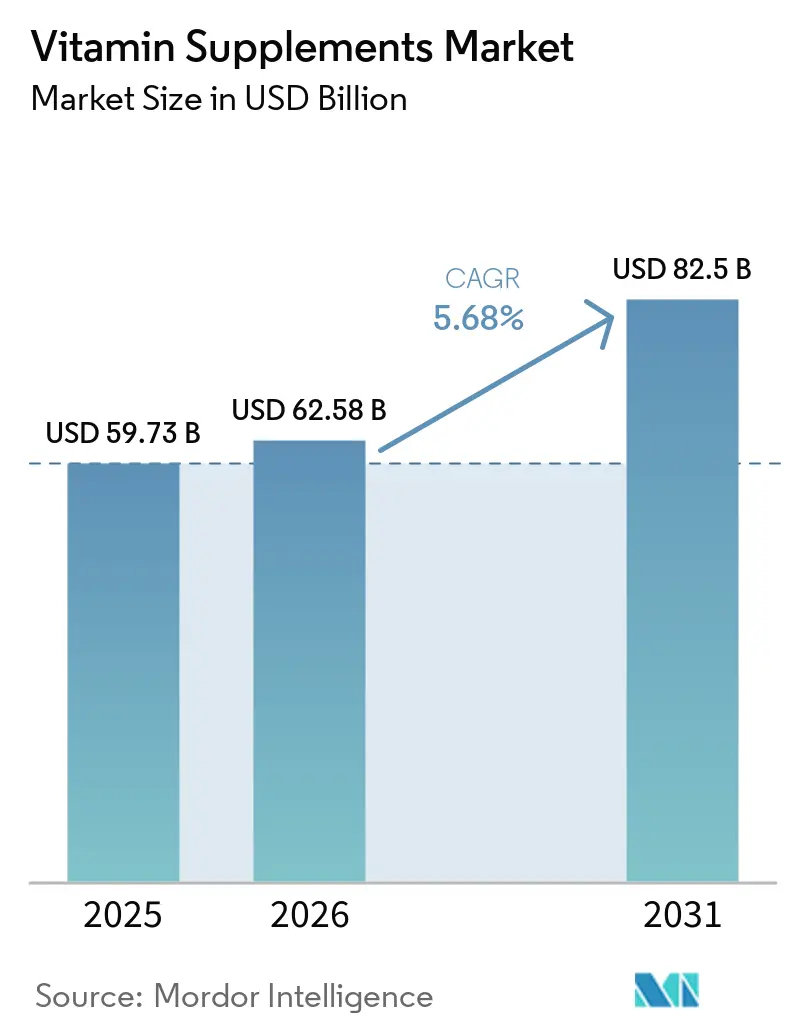

The vitamin supplements market size is expected to grow from USD 59.73 billion in 2025 to USD 62.58 billion in 2026 and is forecast to reach USD 82.50 billion by 2031 at 5.68% CAGR over 2026-2031. As consumers place greater emphasis on wellness, energy, and immune health, daily vitamin supplementation has become a regular part of proactive health management. The growing prevalence of vitamin D deficiency continues to drive market growth, but regulatory challenges and supply chain disruptions remain key concerns. The United States Food and Drug Administration's (FDA) Office of Dietary Supplement Programs (ODSP) is enhancing its regulatory framework by updating processes for New Dietary Ingredient (NDI) notifications, Generally Recognized as Safe (GRAS) pathways, and ensuring the quality of gummy supplements. A public stakeholder meeting held in March 2026 highlighted the agency's increased focus on dose consistency and contaminant testing[1]Source: Food and Drug Administration, "Public Meeting Exploring the Scope of Dietary Supplement Ingredients," fda.gov. In this evolving market environment, companies that invest in scientific validation, clear product labeling, and innovative delivery formats are well-positioned to build consumer trust and gain a competitive advantage.

Key Report Takeaways

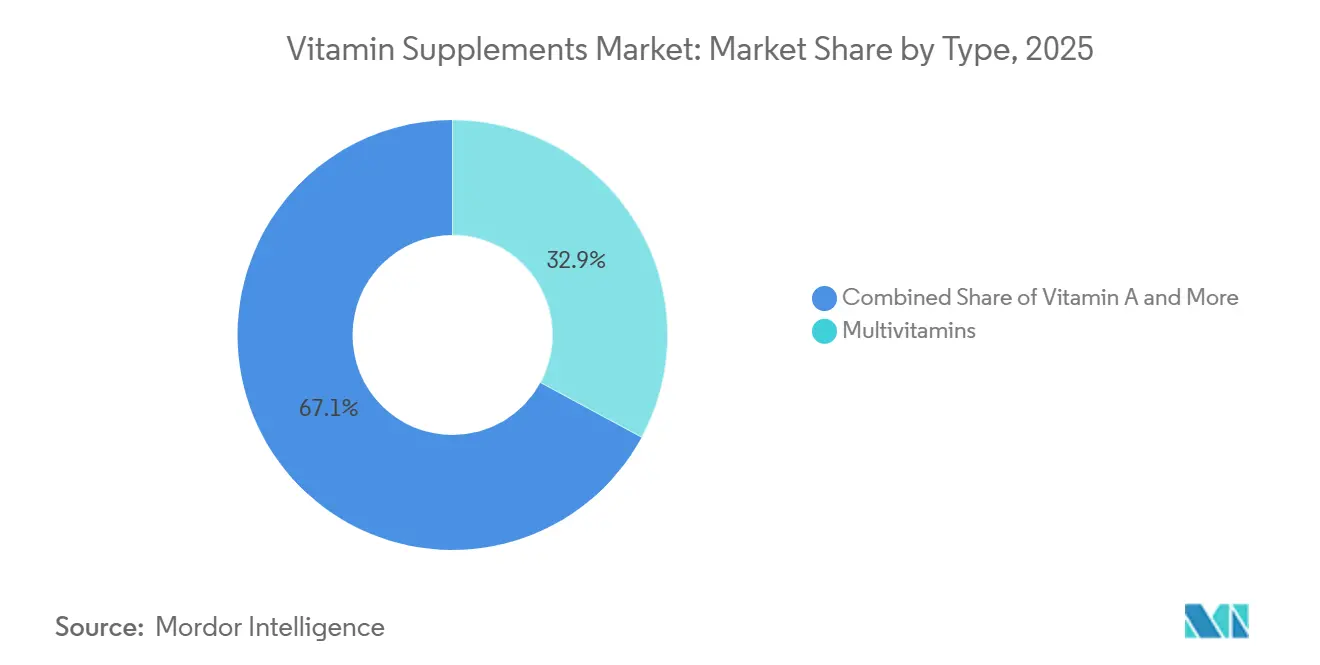

- By type, multivitamins led the vitamin supplements market with a share of 32.88%% in 2025, while Vitamin D are anticipated to register the fastest CAGR of 6.90% during 2026-2031.

- By form, tablets retained 38.21% share in 2025, whereas gummies is forecast to expand at a 7.86% CAGR through 2031.

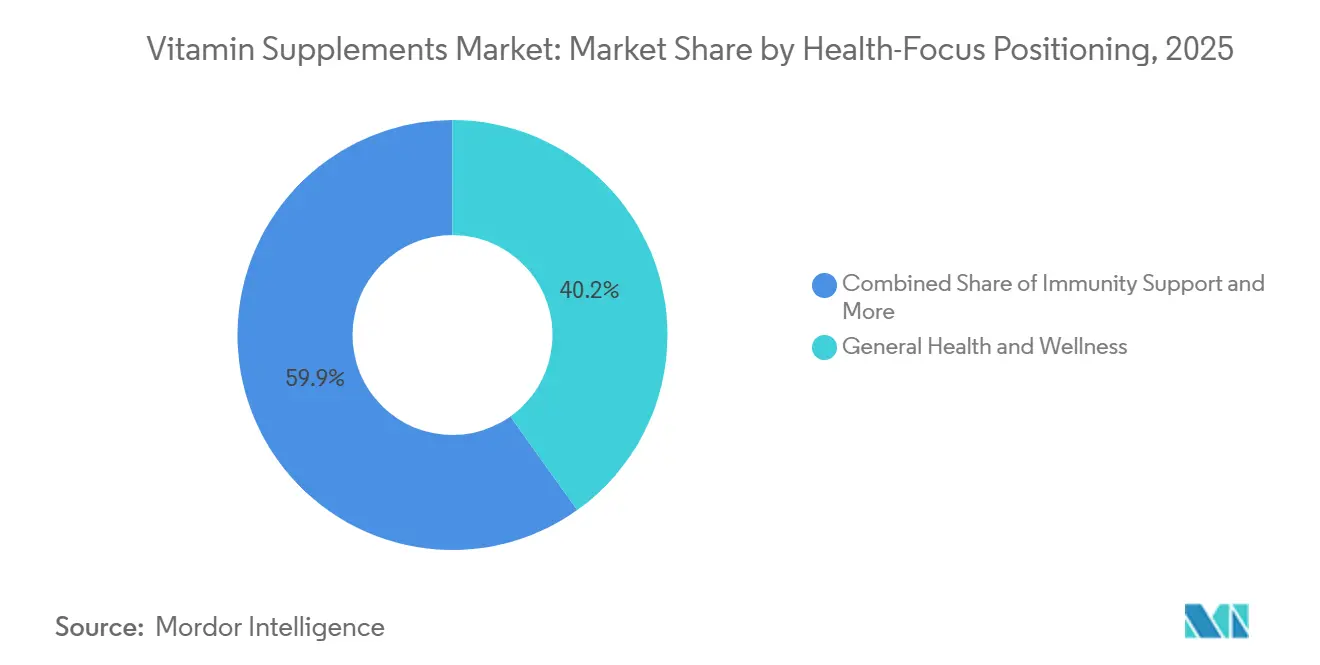

- By health-focus positioning, general health and wellness held 40.15% of 2025 revenue, but immunity support is expected to grow fastest at 6.89% through 2031.

- By distribution channel, supermarkets/hypermarkets led the vitamin supplements market with a share of 35.26% in 2025, while online retail stores is anticipated to register the fastest CAGR of 7.56% during 2026-2031.

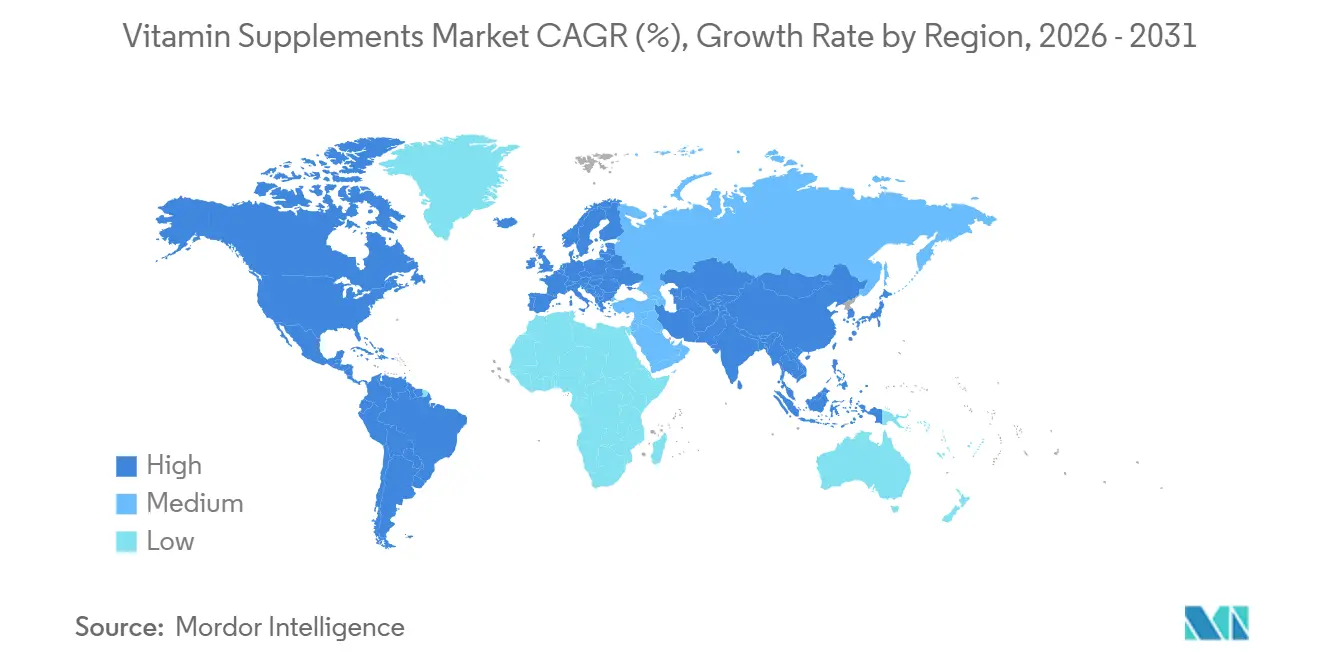

- By geography, North America led the vitamin supplements market with a share of 36.66% in 2025, while Asia-Pacific are anticipated to register the fastest CAGR of 7.24% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vitamin Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer focus on preventive healthcare and wellness | +1.5% | Global, strongest in North America, Europe, and urban Asia-Pacific | Medium term (2–4 years) |

| Micronutrient deficiency concerns strengthening vitamin demand | +1.2% | Global, with highest intensity in South Asia, Eastern Mediterranean, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Aging population supporting healthy longevity solutions | +0.9% | Japan, Germany, China, United States - key aged economies | Long term (≥ 4 years) |

| Fitness-oriented lifestyles supporting daily supplement intake | +0.7% | North America, Europe, Southeast Asia | Medium term (2–4 years) |

| Maternal and prenatal nutrition needs driving supplement adoption | +0.5% | South Asia, Southeast Asia, North America, Middle East | Medium term (2–4 years) |

| Innovation in gummies, softgels, and convenient delivery formats | +0.8% | North America, Europe, spill-over to premium Asia-Pacific segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing consumer focus on preventive healthcare and wellness

Preventive healthcare has transitioned from being a niche lifestyle choice to a core priority, significantly influencing the demand for vitamin supplements and expanding their appeal across diverse consumer segments. This shift is driven by the growing adoption of digital health tools, such as wearable devices, artificial intelligence (AI)-powered personalization platforms, and corporate wellness programs. These advancements are encouraging brands to move away from generic multivitamin offerings and focus on condition-specific solutions. The increasing preference for personalized health regimens demonstrates how digital self-care tools are shaping consumer purchasing decisions. Additionally, the introduction of glucagon-like peptide-1 (GLP-1) weight-loss medications is creating new opportunities for supplements designed to support low-calorie diets, boost energy levels, and improve digestive health. Together, these factors are redefining the market's growth trajectory, positioning vitamin supplements as integral components of modern wellness strategies rather than optional lifestyle products.

Micronutrient deficiency concerns strengthening vitamin demand

Micronutrient deficiencies are driving the global demand for vitamin supplements, as significant gaps in essential nutrients like vitamin D and vitamin B12 highlight the need for tailored solutions across various populations. In developed markets, supplements prescribed by healthcare professionals are becoming increasingly common. At the same time, regulatory organizations such as the World Health Organization (WHO) are influencing consumer behavior. For example, the WHO recommends fortifying edible oils and fats with vitamins A and D as part of public health initiatives[2]Source: World Health Organization, "WHO Guideline on fortification of edible oils and fats with vitamins A and D for public health," who.int. These efforts, combined with the recognition of widespread nutrient deficiencies, are transforming product strategies. Companies that provide clinical-grade evidence to support their claims are gaining consumer trust, commanding premium pricing, and building stronger brand loyalty. This shift is creating a clear distinction in the market's quality tiers. As a result, vitamin supplements are no longer seen as optional lifestyle products but as essential components of modern preventive healthcare.

Aging population supporting healthy longevity solutions

The aging population is driving a significant increase in demand for vitamin supplements, making the category a critical contributor to promoting healthy longevity. This trend remains consistent, showing resilience against short-term economic changes. According to the World Health Organization (WHO), the global population aged 60 and above is expected to reach 2.1 billion by 2050, doubling from its 2020 level. This demographic shift underscores the growing need for targeted nutritional solutions. Older adults face specific challenges, such as reduced absorption of vitamin B12, lower synthesis of vitamin D, and declining calcium uptake, which are driving demand for specialized supplement formulations. Additionally, increasing clinical evidence supports this trend. Peer-reviewed studies have shown that daily multivitamin use can lead to measurable reductions in biological aging markers, further encouraging adoption among seniors. In developed economies like Japan and Germany, consumers are increasingly choosing pharmaceutical-grade and premium blended supplements, reflecting a broader shift toward premiumization in the market. As longevity becomes a central focus in healthcare strategies, brands that combine scientific credibility with tailored solutions are well-positioned to capture long-term value in this growing segment. This demographic-driven growth ensures that longevity-focused supplements will remain a cornerstone of the global wellness economy for years to come.

Fitness-oriented lifestyles supporting daily supplement intake

The growing adoption of fitness culture has expanded the supplement consumer base beyond professional athletes, attracting a younger, digitally engaged audience that seamlessly incorporates daily supplementation into their wellness routines. This shift has moved supplement purchases from niche specialty stores to mainstream retail channels, with e-commerce platforms like Amazon becoming key destinations for product discovery and repeat purchases. Sports-related goals are increasingly influencing purchasing decisions, positioning supplements as everyday essentials in fitness routines rather than niche performance enhancers. Regulatory frameworks, such as the Dietary Supplement Health and Education Act (DSHEA) in the United States and the evolving Food Supplements Directive in Europe, ensure that the rising demand is met with high product standards, consumer safety, and trust. The intersection of lifestyle trends, digital accessibility, and regulatory oversight is driving sustained growth in the global fitness-oriented supplement market. As a result, vitamins and supplements are becoming an integral part of the daily lives of a new generation, solidifying their role as key components of modern wellness practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and substandard products eroding consumer confidence | −0.6% | Global, acute in e-commerce-driven markets and Middle East and Africa | Short term (≤ 2 years) |

| Preference for whole food nutrition limiting supplement reliance | −0.4% | Western Europe, health-conscious urban North America | Medium term (2–4 years) |

| Complex regulatory frameworks across international markets | −0.5% | Global cross-border trade, European Union, Asia-Pacific regulatory divergence | Long term (≥ 4 years) |

| Raw material price volatility affecting profit margins | −0.3% | Global manufacturing, Asia-Pacific sourcing hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and substandard products eroding consumer confidence

The vitamin supplements market is facing challenges as counterfeit and low-quality products erode consumer confidence, particularly on online platforms where illegitimate businesses are growing alongside legitimate direct-to-consumer sales. In response to significant Salmonella outbreaks and the discovery of advanced counterfeit operations in 2026, the United States Food and Drug Administration (FDA) has increased its oversight of dietary supplements[3]Source: Food and Drug Administration, "Dietary Supplement Inspections After Recent FDA Salmonella and Counterfeit Alerts," fda.gov. The FDA is now prioritizing proactive contaminant testing and thorough audits of suppliers handling high-risk ingredients. Additionally, the FDA's Office of Dietary Supplement Programs has flagged concerns about gummy supplements, citing issues such as inconsistent dosing, unstable ingredients, and the lack of reliable methods for detecting contaminants. At the same time, gray-market distributors are undercutting legitimate suppliers, exposing gaps in traditional procurement systems. To address these challenges and maintain trust, leading brands are adopting measures like third-party verification seals, QR-code traceability, and pharmacist endorsements. These strategies are becoming critical for protecting consumer trust and securing market share in an increasingly scrutinized environment.

Complex regulatory frameworks across international markets

Regulatory frameworks across international markets create significant challenges for the vitamin supplements industry. These regulations increase compliance costs and delay market entry, especially for smaller brands striving to compete. The United States Food and Drug Administration (FDA) is reviewing a proposed rule to eliminate the Generally Recognized as Safe (GRAS) pathway as an independent safety mechanism, which could transform how new ingredients are introduced in the United States. Similarly, the European Union's (EU) Food Supplements Directive enforces strict dosage limits, reducing opportunities for product differentiation. Managing diverse standards for labeling, permissible ingredient levels, and novel food registration across multiple jurisdictions demands significant resources. This gives multinational companies with dedicated compliance teams a clear competitive edge. For regional or domestic players, these fragmented regulations create substantial barriers to scaling operations globally. To achieve sustainable growth, businesses must focus on regulatory flexibility and invest in compliance expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Multivitamins Lead, Vitamin D Poised for a Decade of Outsized Growth

In 2025, multivitamins dominated the global vitamin supplements market with a 32.88% share. Their widespread popularity stems from their ability to cater to diverse demographics, their easy availability in mass markets, and strong endorsements from healthcare professionals. Multivitamins provide a convenient, all-in-one solution, making them particularly appealing to busy individuals who prefer a simplified approach to supplementation. This strong market position ensures that multivitamins remain a key revenue driver for the industry. Their established presence highlights their resilience, with demand supported by evolving lifestyles and a growing working-age population in emerging economies.

Meanwhile, Vitamin D is projected to be the fastest-growing segment, with a CAGR of 6.90% through 2031. This growth is driven by the global prevalence of Vitamin D deficiency. Research consistently emphasizes its essential role in maintaining bone health, strengthening the immune system, and supporting respiratory health. These findings have facilitated a shift from prescription-based sales to over-the-counter (OTC) availability, boosting both consumer adoption and healthcare provider recommendations. Additionally, the market is evolving toward advanced formulations that combine Vitamin D with complementary nutrients such as Vitamin K2, Magnesium, and Boron. This transition from single-nutrient products to scientifically validated blends positions Vitamin D as a key driver of innovation in the supplements market, with growth potential that outpaces other categories.

By Form: Tablets Dominant, Gummies Rewriting the Format Economy

In 2025, tablets remain the dominant format and accounted for 38.21% of the global vitamin supplements market. Their dominance is driven by cost-effective production, long shelf life, and precise dosing, making them a reliable choice for both health-conscious consumers and institutional buyers. Tablets continue to serve as the foundation of the category, consistently aligning with physician recommendations and building consumer trust. Their established role highlights their ability to balance affordability with effectiveness, ensuring they remain the preferred option in markets where scalability and regulatory compliance are critical.

At the same time, gummies are transforming the market as the fastest-growing segment, with a projected CAGR of 7.86% through 2031. Their rapid growth is fueled by their sensory appeal, convenience, and increased visibility on social media platforms, particularly among younger consumers and first-time supplement users. With their enjoyable taste and engaging formats, gummies have transitioned from a novelty product to a mainstream offering, driving significant investments in specialized manufacturing facilities. This shift reflects evolving consumer expectations, where supplement adherence is increasingly tied to enjoyment and seamless integration into daily routines. As gummies gain traction, they are reshaping competitive dynamics and positioning taste-driven innovation as a critical growth driver in the vitamin supplements market.

By Health-Focus Positioning: General Wellness Anchors Revenue, Immunity Support Accelerates

In 2025, the general health and wellness segment captured a significant 40.15% share of the market. This segment's dominance highlights the global popularity of multivitamins, which are often the first choice for individuals exploring dietary supplements. However, this broad appeal presents both opportunities and challenges. While it drives revenue, increasingly knowledgeable consumers are shifting toward specialized solutions, which can influence brand loyalty. The segment continues to thrive due to its relevance across various demographic groups. To sustain its leadership, companies need to balance catering to the broader market while also offering tailored products that meet evolving consumer expectations.

At the same time, the immunity support segment is witnessing rapid growth, with a projected CAGR of 6.89% through 2031. Initially positioned as a response to seasonal demand or pandemic-related concerns, immunity support has now become a consistent, year-round priority for consumers, reflecting a fundamental change in behavior. This segment benefits from strong scientific evidence and growing awareness of the critical role immune health plays in overall well-being. Its growth is further supported by advancements in innovative product formulations and regulatory approvals for immune-focused supplements. As a result, the immunity support segment is not only driving substantial growth but is also reshaping the competitive landscape, emerging as a strategic priority for companies aiming to build lasting consumer relationships.

By Distribution Channel: Supermarkets Lead by Volume, Online Retail Emerges as the Strategic Battlefield

In 2025, supermarkets and hypermarkets accounted for 35.26% of the vitamin supplements distribution market, reaffirming their position as the leading channel by volume. This dominance is driven by the routine nature of supplement purchases. Products such as multivitamins and Vitamin C, which are commonly used daily, benefit from their availability in physical stores. Strategic placement in checkout aisles further encourages impulse purchases. Recognizing this trend, major brands are expanding their presence in retail outlets, leveraging visibility to reach a broader audience. Meanwhile, specialty and health stores focus on serving premium customers. These stores build trust through endorsements from pharmacists or healthcare practitioners, which is particularly valuable for therapeutic-dose formulations that require in-store education at the point of sale.

Online retail is emerging as the fastest-growing channel, with a projected (CAGR) of 7.56% through 2031. It is quickly becoming a critical battleground for supplement brands. Features such as subscription-based models, personalized delivery services, and social commerce platforms are transforming how brands connect with consumers. Additionally, cross-border e-commerce is opening doors to global brand access. While offline channels remain dominant in markets such as the United States, e-commerce is expected to surpass them in the near future, driven by its convenience and ability to offer personalized experiences. For manufacturers, this shift highlights the importance of investing in both physical retail presence and digital capabilities. The competitive landscape increasingly favors multinational companies that can operate effectively across both channels, leaving smaller players struggling to compete with single-channel strategies.

Geography Analysis

In 2025, North America retained its position as the largest market for vitamin supplements, contributing 36.66% of global revenue. This dominance is driven by high consumer spending per capita, a well-established Dietary Supplement Health and Education Act (DSHEA) regulatory framework, and a strong culture of preventive health across all age groups. The United States leads the region, with multivitamins, Vitamin D, and Vitamin C being the most popular categories. However, growth is slowing as the market nears saturation. Canada’s efforts to enhance its natural health product regulations and Mexico’s expansion of pharmacy-channel distribution are helping sustain momentum. Still, the region reflects a mature market where achieving incremental growth is increasingly challenging.

Asia-Pacific is the fastest-growing region, with a projected CAGR of 7.24% through 2031. This growth is fueled by the rapid expansion of the middle class, changing dietary habits, and a young, working population influenced by digital wellness trends. China remains the largest contributor, while India and Southeast Asia are the fastest-growing subregions, benefiting from simplified regulations and expanding retail networks. Japan and South Korea, though mature markets, continue to see strong demand for pharmaceutical-grade formulations. Companies like Haleon are leveraging localized strategies, such as Centrum Daily Kits, to outperform standardized global product launches.

Europe presents a distinct market landscape. The European Union (EU) Food Supplements Directive and national pharmacy licensing requirements create significant barriers for generic products but reward evidence-backed brands with premium pricing opportunities. Germany leads with a pharmacy-focused model that fosters clinical trust, while the United Kingdom benefits from National Health Service (NHS)-endorsed Vitamin D programs. Southern and Eastern Europe are emerging as growth areas, driven by aging populations, increased fitness participation, and regulatory harmonization that facilitates cross-border trade. Meanwhile, South America and the Middle East and Africa (MEA) are gaining momentum through the expansion of modern retail and premium pharmacy channels, offering long-term opportunities for global companies investing in diversified regional strategies.

Competitive Landscape

The global vitamin supplements market is highly fragmented, with multinational consumer health companies competing alongside specialized nutrition firms, pharmaceutical-affiliated divisions, and numerous regional and private-label players. Industry leaders such as Haleon, Bayer, and Amway’s Nutrilite brand operate on a global scale, leveraging clinical validation programs and diversified geographic portfolios to drive growth. These companies effectively manage regional declines by expanding into high-growth markets, showcasing a competitive infrastructure advantage that mid-sized firms often lack. In recent years, strategic efforts have focused on investments in product formats, portfolio optimization, and geographic expansion, emphasizing the critical role of scale and adaptability in this fragmented market.

Opportunities are emerging at the intersection of clinical science and consumer accessibility. Multinational corporations are increasingly grounding their brands in peer-reviewed evidence, such as studies demonstrating how multivitamin use can reduce biological aging markers. This creates a clinical claims platform that smaller players find difficult to replicate. At the same time, digital-first brands are disrupting traditional distribution channels by utilizing platforms like TikTok Shop and Amazon to engage younger, digitally savvy consumers. Personalized nutrition startups are further transforming the competitive landscape by combining vitamin regimens with artificial intelligence (AI)-driven health data analytics, positioning themselves as credible, customized alternatives to standard supplements.

Regulatory compliance is becoming a critical differentiator. With increased scrutiny on good manufacturing practices and potential changes to frameworks such as the United States Generally Recognized as Safe (GRAS) pathway, ingredient suppliers with certified European manufacturing capabilities are well-positioned to stand out in the United States and specialty supplement markets. This evolving regulatory environment is expected to consolidate parts of the supply chain, creating opportunities for upstream players while raising barriers for less-resourced competitors. Overall, the competitive landscape is shaped by a combination of scale-driven incumbency, science-backed credibility, digital disruption, and regulatory agility, factors that will continue to influence market leadership in the coming years.

Vitamin Supplements Industry Leaders

-

Amway Corporation

-

Haleon plc

-

Bayer AG

-

Herbalife Nutrition Ltd.

-

Pharmavite LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Haleon announced an investment of GBP 175 million to establish a new manufacturing facility in Madhya Pradesh, India. This facility marked Haleon's first manufacturing presence in South Asia and was designed to meet local demand while supporting supply across Asia. The initiative was expected to create approximately 500 jobs. This investment reinforced Haleon's strategy of strengthening local manufacturing capabilities in rapidly expanding emerging markets, particularly where distribution had outpaced traditional import-dependent supply chains.

- April 2026: NOW Foods introduced two new gummy vitamin supplements, expanding its product portfolio. The company launched Vitamin C gummies, delivering 250 milligrams per serving with a bright, citrus orange flavor, and Vitamin D3 gummies, offering 1,000 International Units (IU) per gummy.

- April 2026: Alkem Laboratories Limited launched "A to Z Daily," a daily multivitamin supplement for adults aimed at providing comprehensive nutritional support for both the body and mind. The "A to Z Daily" tablets were formulated with 26 essential vitamins, minerals, and botanicals. Key nutrients included Vitamin B complex, Vitamin D3, Vitamin C, Zinc, and Iron, which were intended to boost energy levels, reduce fatigue, and enhance immunity. The product also incorporated clinically researched botanicals such as Ashwagandha, Bacopa monnieri (Brahmi), Panax ginseng, and the amino acid L-theanine, which were known to help manage stress and anxiety, improve sleep quality, and support cognitive function.

Global Vitamin Supplements Market Report Scope

Vitamin supplements are defined as products that provide essential organic micronutrients, vitamins, in concentrated form to support normal physiological functions when dietary intake is insufficient. They are designed to prevent or correct deficiencies, maintain health, and in some cases, enhance wellness outcomes.

The vitamin supplements market is segmented by type, form, health-focus positioning, distribution channel, and geography. By type, the market is segmented into Vitamin A, Vitamin B, Vitamin C, Vitamin D, Vitamin E, Vitamin K, and multivitamins. By form, the market is segmented into tablets, gummies, powders, capsules and softgels, liquid, and others. By health-focus positioning, the market is segmented into general health and wellness, immunity support, bone and joint health, energy and metabolism, heart health, cognitive and mental health, prenatal health, and other applications. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty and health stores, online retail stores, and other distribution channels. By Geography, the market is segmented into North America, Europe, Asia-Pacific, South America and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Vitamin A |

| Vitamin B |

| Vitamin C |

| Vitamin D |

| Vitamin E |

| Vitamin K |

| Multivitamins |

| Tablets |

| Gummies |

| Powders |

| Capsules and Softgels |

| Liquid |

| Others |

| General Health and Wellness |

| Immunity Support |

| Bone and Joint Health |

| Energy and Metabolism |

| Heart Health |

| Cognitive and Mental Health |

| Prenatal Health |

| Other Applications |

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Vitamin A | |

| Vitamin B | ||

| Vitamin C | ||

| Vitamin D | ||

| Vitamin E | ||

| Vitamin K | ||

| Multivitamins | ||

| By Form | Tablets | |

| Gummies | ||

| Powders | ||

| Capsules and Softgels | ||

| Liquid | ||

| Others | ||

| By Health-Focus Positioning | General Health and Wellness | |

| Immunity Support | ||

| Bone and Joint Health | ||

| Energy and Metabolism | ||

| Heart Health | ||

| Cognitive and Mental Health | ||

| Prenatal Health | ||

| Other Applications | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the global vitamin supplements market?

The market was valued at USD 59.73 billion in 2025 and is projected to reach USD 82.50 billion by 2031, growing at a CAGR of 5.68% between 2026 and 2031.

Which type of segment leads the market?

Multivitamins are the largest type of segment, holding 32.88% share in 2025, driven by broad consumer appeal and convenience.

Which format dominates the market?

Tablets are the dominant format, accounting for 38.21% share in 2025, favored for cost-efficiency, dosage precision, and shelf stability.

Which format is expanding fastest?

Gummies are the fastest-growing format, with a CAGR of 7.86% projected through 2031, driven by taste appeal and adoption among younger consumers.

Which regions lead and grow fastest?

North America is the largest geography with 36.66% share in 2025, while Asia-Pacific is the fastest-growing region, expected to expand at a CAGR of 7.24% through 2031 due to rising middle-class demand and digital adoption.

Which type of segment is growing fastest?

Vitamin D is the fastest-growing type segment, projected to expand at a CAGR of 6.90% from 2026 to 2031, supported by rising awareness of deficiency and its role in immunity and bone health.

Page last updated on: