Herbal Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

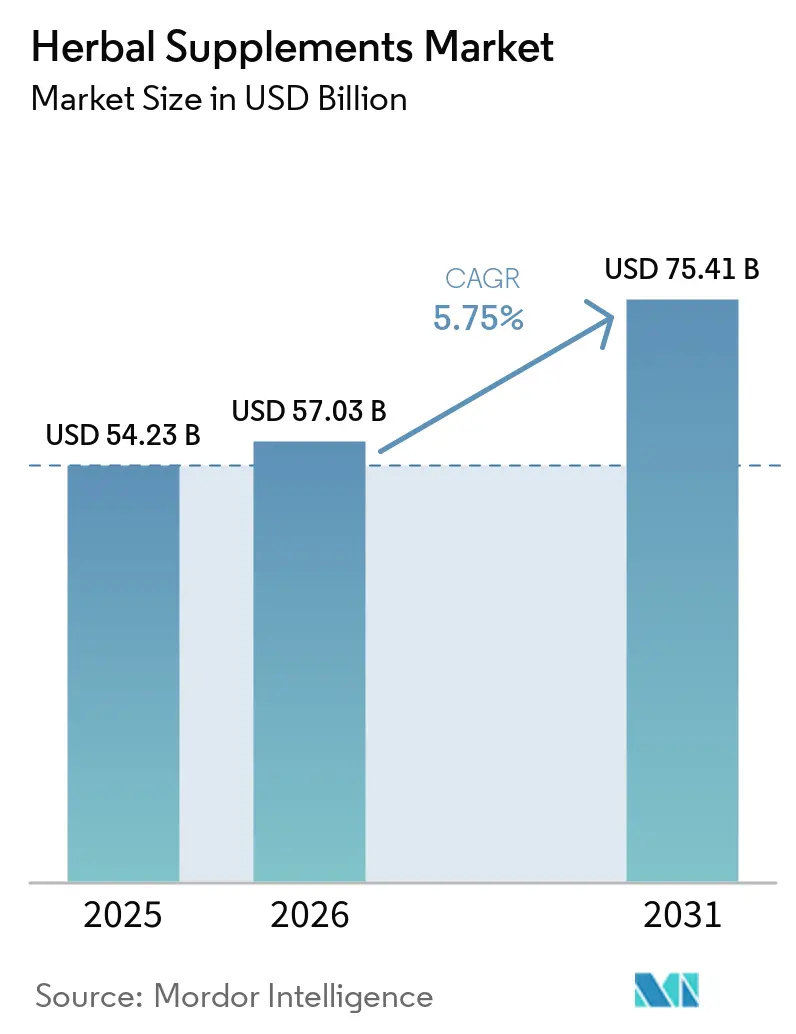

| Market Size (2026) | USD 57.03 Billion |

| Market Size (2031) | USD 75.41 Billion |

| Growth Rate (2026 - 2031) | 5.75% CAGR |

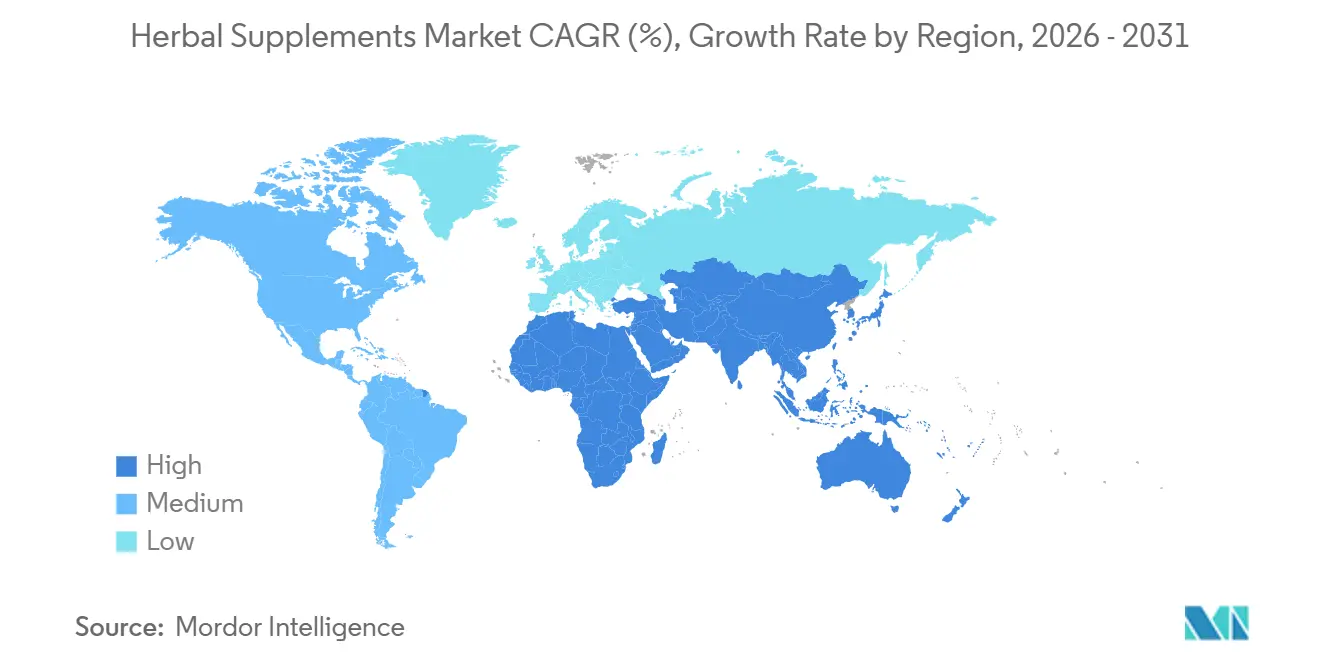

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Herbal Supplements Market Analysis by Mordor Intelligence

The herbal supplements market size is projected to expand from USD 54.23 billion in 2025 and USD 57.03 billion in 2026 to USD 75.41 billion by 2031, registering a 5.75% CAGR between 2026 and 2031. As consumer lifestyles evolve, demand in the herbal supplements market is increasingly shifting toward modern formats. Products such as gummies and chews are becoming popular, particularly among younger consumers in the Asia-Pacific region. At the same time, Europe faces regulatory fragmentation in the herbal supplements market, while globally, stricter quality standards are driving up compliance costs. This trend benefits vertically integrated players capable of ensuring traceability and managing overheads effectively. Innovations in ingredients, especially bioavailability platforms that enhance curcumin, ashwagandha, and functional mushrooms, are supporting premium pricing despite persistent raw-material volatility. Additionally, the integration of social commerce, subscription models, and network pharmacology research is accelerating product development cycles and geographic expansion, while also increasing risks for brands that fail to adapt quickly.

Key Report Takeaways

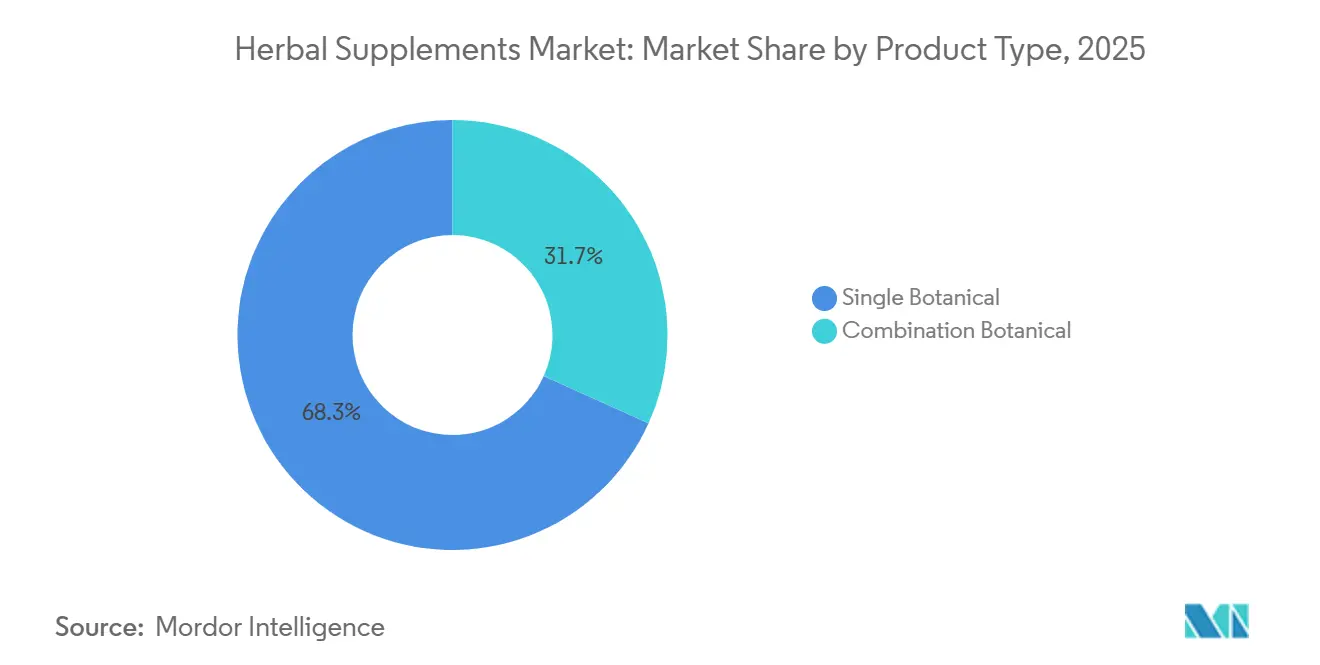

- By product type, single botanical products led with 68.27% of herbal supplements market share in 2025, while combination formulas are forecast to expand at a 6.15% CAGR through 2031.

- By form, capsules and softgels accounted for 57.86% of the herbal supplements market size in 2025, but gummies and chews are advancing at a 6.58% CAGR to 2031.

- By functionality, immune support commanded 42.03% of category spending in 2025, whereas stress, sleep, and cognitive health formulas are set to grow at a 6.35% CAGR during the same period.

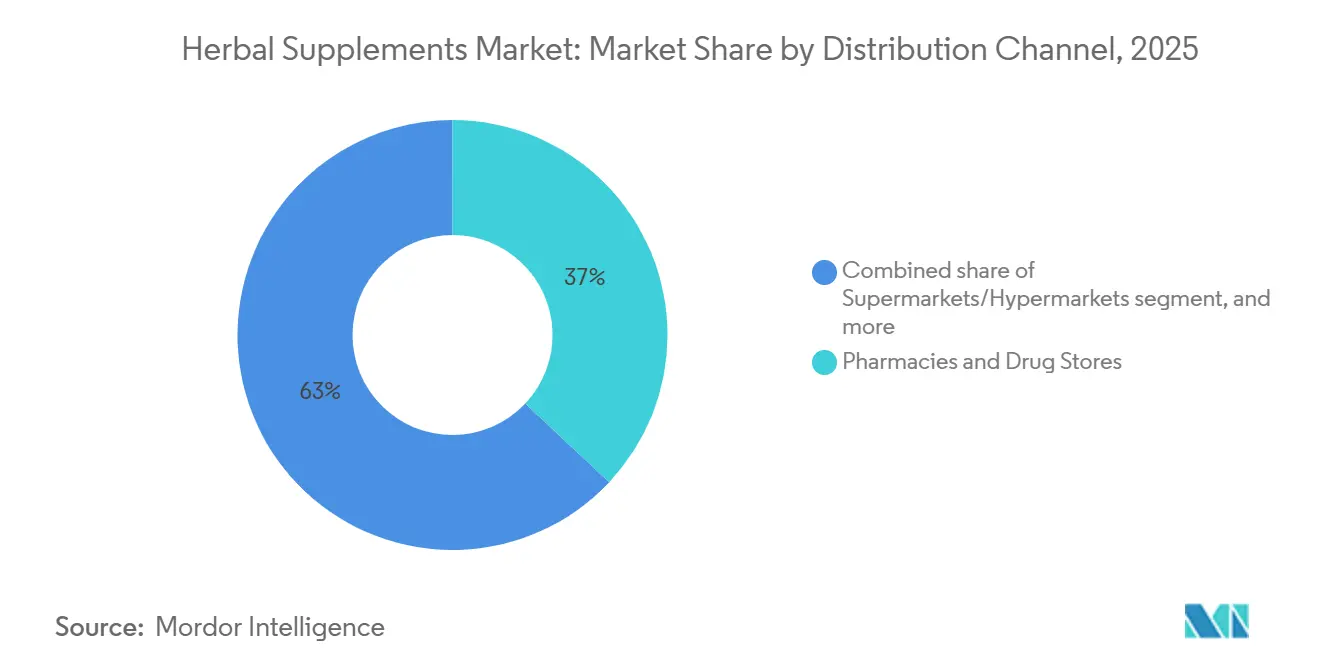

- By distribution channel, pharmacies and drug stores held 37.01% revenue share in 2025, while online retail is projected to increase at a 6.47% CAGR to 2031.

- By geography, North America captured 40.98% of global revenue in 2025, and Asia-Pacific is on track for the fastest regional growth at a 6.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Herbal Supplements Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for natural and clean-label products | +1.3% | Global, with strongest impact in North America & Europe | Long term (≥ 4 years) |

| Growth of e-commerce and digital platforms | +1.0% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Ageing populations driving preventive health spend | +0.9% | North America, Europe, Japan core markets | Long term (≥ 4 years) |

| Product innovation and personalization | +0.8% | North America & EU innovation hubs, expanding globally | Medium term (2-4 years) |

| Influence of traditional medicine systems | +0.6% | Asia-Pacific core, expanding to Western markets | Long term (≥ 4 years) |

| Technological advancements in cultivation and processing | +0.5% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Preference for natural and clean-label products

Consumer demand for transparency and natural ingredients is significantly transforming product development strategies within the herbal supplements market. This shift extends beyond ingredient sourcing to include sustainable packaging solutions, ethical harvesting practices, and a focus on environmental and social responsibility. For instance, Blackmores achieved B Corp certification in 2024, showcasing its commitment to sustainability and ethical business practices. Regulatory developments in the herbal supplements market are further accelerating the transition to natural products. The EU's Heads of Food Safety Agencies identified 117 substances for potential restriction in food supplements, compelling manufacturers to prioritize botanicals with established safety and efficacy profiles[1]Federal Office of Consumer Protection and Food Safety, "First report of the HoA Working Group "Food Supplements"", bvl.bund.de. Third-party certifications have also emerged as a critical factor for market access and consumer trust. Products with USP Verified certification, for example, enjoy an 84% trust rate among supplement users, emphasizing the growing importance of quality assurance and transparency. This increasing preference for natural formulations is driving advancements in extraction technologies, standardization processes, and clean-label solutions. These innovations enable manufacturers to deliver consistent potency, meet regulatory requirements, and align with evolving consumer expectations, positioning the industry for sustained growth.

Growth of e-commerce and digital platforms

The digital transformation of distribution has significantly reshaped the herbal supplements market, driving a notable increase in online sales. E-commerce platforms in the herbal supplements market have enabled direct-to-consumer interactions, eliminating traditional retail markups and offering personalized product recommendations tailored to individual health goals and preferences. This shift gained momentum during the COVID-19 pandemic, as consumers increasingly sought convenient and reliable access to health products. Social media platforms, particularly TikTok, have become critical in influencing consumer behavior, creating substantial product awareness and driving sales conversions. This trend is especially pronounced among younger demographics who favor natural health solutions. Additionally, digital platforms have introduced subscription-based models, which enhance customer retention and streamline predictive inventory management. These advancements address persistent supply chain challenges that have historically affected the industry. The integration of artificial intelligence into e-commerce platforms further enhances the consumer experience by enabling sophisticated product matching and delivering educational content. This empowers consumers to navigate the complex herbal supplement landscape with greater confidence and informed decision-making.

Ageing populations driving preventive health spend

Demographic shifts in the herbal supplements market in developed regions, particularly the aging population, are driving sustained demand for preventive health solutions. Herbal supplements are increasingly positioned as natural alternatives to pharmaceutical interventions, aligning with consumer preferences for holistic wellness. According to the U.S. Census Bureau, the global population aged 65 and older is projected to reach 94.7 million by 2060, significantly influencing healthcare spending on preventive measures[2]United States Census Bureau, "Measuring America's People and Economy", census.gov. This demographic transition is accompanied by growing awareness of the gut-brain axis and the critical role of microbiome health in overall well-being. Cognitive health has emerged as a high-growth segment within the preventive health market. Adaptogens, such as ashwagandha, are experiencing robust demand as consumers prioritize natural solutions for stress management and mental wellness. The aging population's preference for natural and scientifically validated products is further supported by rising disposable incomes and improved health literacy, enabling manufacturers to adopt premium pricing strategies for high-quality formulations. Additionally, the increasing pressure to contain healthcare costs is encouraging consumers to explore preventive approaches. Herbal supplements, offering cost-effective alternatives to prescription medications, are becoming a preferred choice for maintaining wellness. This trend underscores the growing importance of preventive health solutions in addressing the needs of an aging population while balancing economic considerations.

Product innovation and personalization

Innovations in delivery formats and personalized nutrition strategies are significantly transforming the herbal supplement market, broadening its appeal to a wider consumer base beyond traditional users. In the herbal supplements market, the integration of personalization technologies has enabled the development of highly targeted formulations tailored to individual genetic profiles, lifestyle factors, and specific health goals. This trend aligns with growing consumer demand, as 59% of individuals actively seek scientific validation to ensure the efficacy of supplements. Simultaneously, advancements in extraction and standardization technologies are addressing long-standing concerns about the variability of herbal supplements. These innovations ensure consistent potency and enhance bioavailability, improving product reliability and effectiveness. Emerging trends, such as synbiotic formulations that combine probiotics and prebiotics, are gaining momentum in the herbal supplements market. For instance, products like 360GUT, derived from wild thyme, have demonstrated clinical efficacy in optimizing gut microbiome health, underscoring the potential of this innovation category. Furthermore, the adoption of nanotechnology and advanced delivery systems is revolutionizing the industry by improving absorption rates and reducing dosing requirements. These advancements make herbal supplements more convenient, efficient, and appealing to consumers. Sustainability is also becoming a critical focus area, with innovations in eco-friendly packaging and carbon-neutral manufacturing processes serving as key competitive differentiators.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality control and product adulteration | -0.4% | Global, with heightened scrutiny in regulated markets | Short term (≤ 2 years) |

| Competition from conventional pharmaceuticals and other natural products | -0.3% | North America & Europe primarily | Medium term (2-4 years) |

| Supply chain vulnerabilities | -0.3% | Global, with Asia-Pacific sourcing dependencies | Short term (≤ 2 years) |

| Regulatory inconsistencies | -0.2% | EU and emerging markets primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Quality control and product adulteration

Amid rising concerns in the herbal supplements market over product quality and authenticity, the American Herbal Products Association has rolled out Good Agricultural Practices to combat contamination and adulteration. The Botanical Adulterants Prevention Program has flagged prevalent substitution and contamination in widely used ingredients, underscoring the need for advanced authentication technologies, such as blockchain-based tracking systems. Regulatory bodies are ramping up their oversight efforts. Notably, an expert group from the EU has proposed restrictions on substances, including coumarin, curcumin, and hypericum perforatum, citing safety concerns. In a move echoing this heightened regulatory vigilance across Europe, the Netherlands is launching a notification system for food supplements, classifying herbal preparations into distinct risk groups. As supply chain transparency becomes paramount for market access, companies are channeling investments into vertical integration and forging direct sourcing relationships, all in a bid to uphold product integrity and traceability.

Competition from conventional pharmaceuticals and other natural products

Pharmaceutical companies are increasingly encroaching on the herbal supplements market, bolstered by the allure of standardized potency profiles from synthetic alternatives. A case in point: Sanofi's bold USD 1 billion acquisition of Qunol in 2025 underscores the pharmaceutical sector's growing appetite for the healthy aging supplement niche, a move that infuses the segment with robust R&D resources and regulatory know-how. Meanwhile, GLP-1 supplement formulations are carving out a niche as viable substitutes for prescription weight management drugs. Companies like GNC are at the forefront, channeling investments into research aimed at crafting natural counterparts to these pharmaceutical solutions. As consumers gravitate towards integrated nutrition solutions, the landscape shifts: functional foods and beverages laced with botanical ingredients are emerging as formidable contenders to traditional supplement formats. On another front, advancements in synthetic biology and precision fermentation are making it feasible to produce nature-identical compounds en masse, posing a potential challenge to conventional botanical sourcing. Adding another layer of complexity, personalized nutrition firms are harnessing genetic testing and biomarker insights, offering tailored supplement regimens that stand in stark contrast to the traditional one-size-fits-all model.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Formulas Broaden Therapeutic Reach

In the herbal supplements market, combination formulas represented a smaller share of 2025 sales, they are anticipated to grow at a faster pace than the overall herbal supplements market, with a robust CAGR of 6.15% projected through 2031. Insights from network pharmacology indicate that piperine can enhance curcumin's bioavailability by an impressive 2000%, enabling the use of lower dosages while improving tolerability. These clinically validated synergies not only justify a price premium of 20–35% but also drive stronger consumer loyalty, as evidenced by higher repeat purchase rates compared to single-ingredient products. Leading brands like Foria Wellness leverage multi-herb blends, incorporating ingredients such as reishi, chaga, ashwagandha, and L-theanine, to position their SKUs as comprehensive wellness solutions. These products are marketed as holistic rituals designed to address multiple health concerns, including stress management, sleep enhancement, and cognitive support.

Single botanical products in the herbal supplements market, however, continue to dominate, contributing 68.27% of 2025 revenue. Their success is attributed to simpler regulatory requirements and greater consumer familiarity. For instance, psyllium emerged as the leading product in U.S. mainstream channels, generating USD 289.45 million in 2024. This performance was supported by an FDA-approved claim linking soluble fiber to heart health benefits. Despite this, the market for single botanical products faces challenges such as saturation and limited opportunities for differentiation, which have slowed growth. To address these challenges, brands are increasingly positioning these staple products as entry-level offerings, using them as a gateway to upsell consumers to more profitable combination formulas within the broader herbal supplements market.

By Form: Gummies Reshape Consumer Experience

In the herbal supplements market, gummies and chews, currently the fastest-growing delivery format, are projected to achieve a robust 6.58% CAGR, significantly transforming the value dynamics. The increasing demand for clean-label products has led manufacturers to incur 15–20% higher costs for natural colorants. Despite these added expenses, the strong sensory appeal of gummies and chews continues to drive incremental consumer purchases. This trend is particularly evident on social media platforms, where the visual aesthetics of products play a crucial role in influencing virality and consumer engagement. Additionally, the flexibility offered by micro-dosing, providing five to ten milligrams per piece, enables consumers to personalize their intake, effectively addressing the issue of pill fatigue and enhancing user convenience.

By 2025, capsules and softgels are expected to maintain a dominant 57.86% share of the herbal supplements market. Their suitability for oil-soluble active ingredients and ability to deliver higher potencies per serving make them particularly effective for ingredients such as milk thistle and berberine. However, the growing variety of stock-keeping units (SKUs) across delivery formats, including capsules, powders, gummies, and stick packs, has introduced complexities in inventory management. Brands that adopt agile forecasting methods and collaborate with reliable contract manufacturing partners are better positioned to mitigate these challenges. In contrast, smaller market entrants often face significant cash-flow constraints, especially as rising minimum order quantities add further financial pressure.

By Distribution Channel: E-Commerce Captures Data And Margin

In the herbal supplements market, online retail is expected to grow at a robust CAGR of 6.47%, surpassing the growth rate of brick-and-mortar stores and capturing a substantial share of the expanding herbal supplements market. Direct-to-consumer brands are strategically utilizing subscription-based business models, which not only increase customer lifetime value but also reduce their dependence on costly algorithm-driven advertising methods. The Asia-Pacific region is leading this shift, with online transactions accounting for 52% of the category's total in 2025. Additionally, social commerce has experienced significant growth, exceeding 50%, driven primarily by the purchasing behavior of Gen Z consumers.

Pharmacies and drug stores continue to hold a notable 37.01% of the herbal supplements market share, supported by strong consumer trust and consistent in-store foot traffic. However, their gross margins remain 15–25 percentage points lower than those of e-commerce channels, primarily due to distributor fees. To address these challenges, some pharmacies are adopting innovative approaches such as “whole-health fusion” models, where pharmacists trained in herbal medicine provide on-site consultations. While these efforts may help sustain their relevance, the slower pace of in-store operational changes compared to the rapid evolution of digital platforms limits their ability to respond effectively to emerging viral trends.

Geography Analysis

In 2025, North America maintained its position as the leading regional contributor, accounting for 40.98% of global revenue. U.S. herbal supplement sales rose to USD 13.23 billion, reflecting a 5.4% year-over-year growth. The direct-to-consumer segment experienced significant growth, reaching a 29% penetration rate, highlighting the increasing preference for online subscriptions. The FDA's 2025 approval of NMN as a dietary supplement resolved uncertainties surrounding novel ingredients. Furthermore, tariff reductions on turmeric and ginger lowered landed costs, intensifying price competition with synthetic alternatives. Canada benefits from its streamlined Natural Health Product regime, while Mexico leverages cross-border e-commerce and growing urban incomes. Retailers across North America are emphasizing third-party testing in response to past adulteration issues, pushing suppliers to obtain ISO 22000 certification to retain shelf space.

Asia-Pacific is anticipated to grow at the fastest rate in the herbal supplements market, with a projected 6.87% CAGR through 2031. China's oral plant extract sector, valued at CNY 60.2 billion (approximately USD 8.5 billion), and India's emergence as a global sourcing hub, supported by Sami-Sabinsa's USD 15 million capacity expansion, are key growth drivers. In early 2026, three major acquisitions in India underscored the trend of domestic brand consolidation. Meanwhile, social commerce platforms like Shopee and TikTok are driving demand in Southeast Asia. Japan's aging population is boosting demand for cognitive and mobility botanicals, further supported by government recognition of traditional medicine in mainstream healthcare. Although regulatory timelines vary across ASEAN countries, the overall trend of liberalization is reducing barriers for international players with region-specific products.

Europe, despite its regulatory complexities, continues to experience steady growth. The EU's Traditional Herbal Medicinal Products Directive facilitates the entry of botanical supplements with a history of traditional use. Europe's strong focus on sustainability aligns well with the values of botanical supplements, increasing demand for ethically sourced and eco-friendly products. Germany leads the European herbal supplements market, demonstrating widespread acceptance of natural health products and benefiting from a well-established retail network. Post-Brexit, the UK's regulatory landscape is ripe with opportunities for innovative botanical formulations, even those facing hurdles in other EU territories. Yet, the region grapples with challenges, notably the EU's impending 2025 ban on botanicals with hydroxyanthracene derivatives, necessitating product tweaks and supply chain realignments[3]Europe Food Safety Authority, "Comprehending the Future Prohibition of Botanicals in the EU Containing Hydroxyanthracene Derivatives in 2025", efsa.europa.eu. Meanwhile, South America and the Middle East & Africa emerge as potential hotspots, driven by a rising health consciousness and maturing retail landscapes, albeit with many markets still navigating underdeveloped regulatory terrains.

Competitive Landscape

The herbal supplements market, known for its fragmentation, boasts a multitude of regional and international players, each presenting a diverse product lineup. Prominent names in the arena include Herbalife Nutrition Ltd., Amway Corporation, Harbin Pharmaceutical Group (GNC), Dr. Willmar Schwabe GmbH & Co. KG (Nature's Way), and Kirin Holdings Company, Limited (Blackmores). This fragmentation heightens competition, resulting in price pressures and an imperative for ongoing product innovation. Many small and medium enterprises tap into local ingredients and traditional wisdom, fostering trust among niche consumers. Consequently, the market sees limited consolidation, with no single entity commanding a global dominance.

Companies are carving out competitive edges through technology adoption, channeling investments into blockchain for supply chain transparency, AI for tailored consumer experiences, and cutting-edge extraction methods to uphold product quality. The B Corp movement is emerging as a strategic differentiator, with firms like Blackmores and Gaia Herbs securing certifications to underscore their commitment to environmental and social stewardship.

Opportunities abound in areas like personalized nutrition, eco-friendly packaging, and novel delivery methods such as functional drinks and topical solutions. Noteworthy disruptors are surfacing, including firms utilizing genetic testing for tailored supplement advice and synthetic biology ventures crafting nature-equivalent compounds on a large scale. The landscape is further muddied by consolidation moves, highlighted by Nestlé Health Science's acquisition of brands from The Bountiful Company and a flurry of private equity stakes in niche botanical firms.

Herbal Supplements Industry Leaders

-

Herbalife Nutrition Ltd.

-

Amway Corporation

-

Dr. Willmar Schwabe GmbH & Co. KG (Nature's way)

-

Kirin Holdings Company, Limited. (Blackmores)

-

Harbin Pharmaceutical Group Co., Ltd (GNC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Vivazen introduced botanical gummies to expand its functional plant-based supplements portfolio. The product line features three formulations: Berry Bliss for energy and focus, Cider Crush for stress relief, and Citrus Chill for relaxation, with effects reported to begin within 20 minutes.

- February 2025: Organic India has expanded its product line with the launch of its new Regenerative Organic Certified teas and herbal supplements at Expo West. The new product line includes Neem supplements, Tulsi Holy Basil supplements, Ashwagandha supplements, and Tulsi Original Tea.

- February 2025: Blue Toad Botanicals has launched a new supplement called You’ve Got Some NERVE, which is the first product to feature Vanizem, an Aframomum melegueta extract by PLT Health Solutions. According to the company, the extract has been clinically evidenced to support measures of mood and sleep, and is featured alongside other botanicals and vitamins including NeuroAEA (Anandamide and Myristicin), Feverfew, passionflower, skullcap, NeuroAGARIC (muscimol), methylated B-complex, benfotiamine, a proprietary terpene stack, and acetyl-L-carnitine.

- December 2024: Himalaya Wellness has launched a new 28-count bottle of PartySmart, featuring a clinically tested herbal formulation. The product supports liver function during alcohol metabolism and aids in reducing acetaldehyde, a compound produced during alcohol breakdown that can cause morning-after discomfort. The single-capsule dosage, taken during alcohol consumption, aims to improve post-celebration recovery.

Global Herbal Supplements Market Report Scope

| Single Botanical |

| Combination Botanical |

| Tablets |

| Capsules/Softgels |

| Gummies/Chews |

| Powders |

| Others |

| Digestive and Gut Health |

| Stress, Sleep and Cognitive Health |

| Immune Support |

| Others |

| Pharmacies and Drug Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Single Botanical | |

| Combination Botanical | ||

| By Form | Tablets | |

| Capsules/Softgels | ||

| Gummies/Chews | ||

| Powders | ||

| Others | ||

| By Functionality/Health Benefits | Digestive and Gut Health | |

| Stress, Sleep and Cognitive Health | ||

| Immune Support | ||

| Others | ||

| By Distribution Channel | Pharmacies and Drug Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the herbal supplements market?

The herbal supplements market size reached USD 54.23 billion in 2025 and is forecast to climb to USD 69.74 billion by 2030.

Which region is growing fastest for herbal supplements?

Asia-Pacific posts the quickest growth at an expected 8.7% CAGR through 2030, fueled by integration of traditional medicine into modern wellness practices.

Which product type dominates sales?

Single botanical formulations held 68.56% of 2024 revenue due to clear regulatory pathways and strong clinical backing.

How quickly are gummy supplements expanding?

Gummies and chews are advancing at a 7.2% CAGR and already represent 34% of U.S. supplement turnover.

Page last updated on: