Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.67 Billion |

| Market Size (2031) | USD 8.6 Billion |

| Growth Rate (2026 - 2031) | 8.68% CAGR |

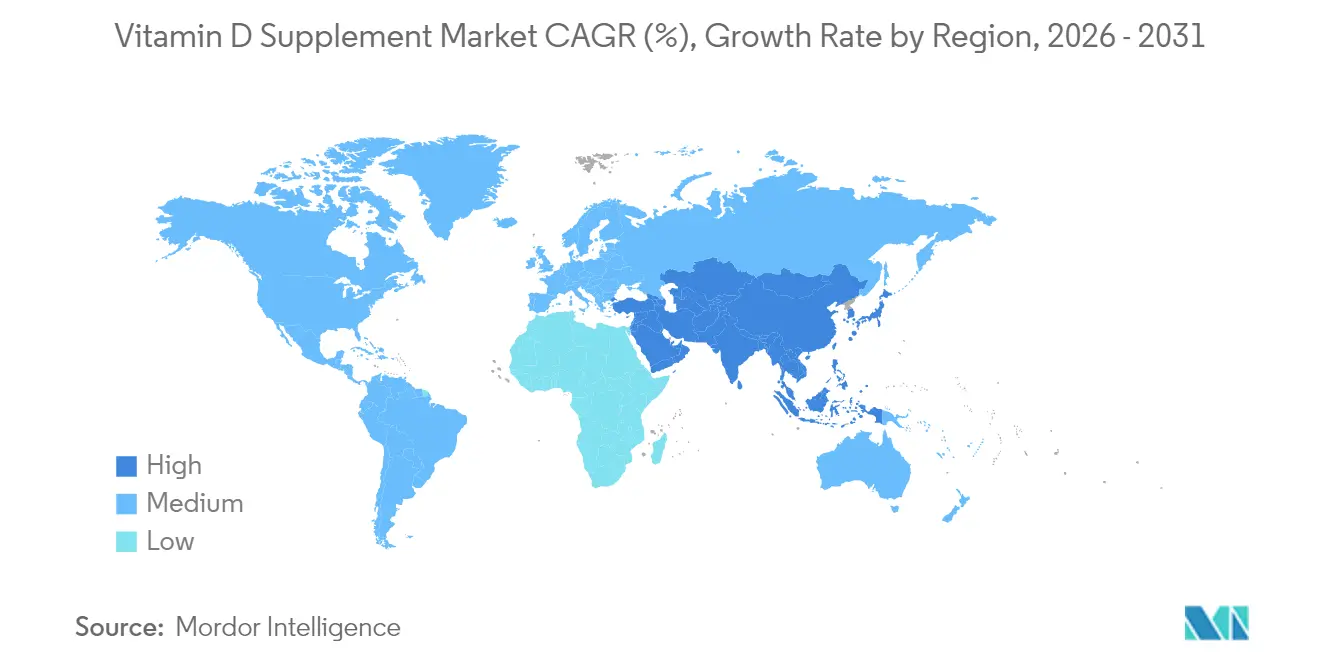

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vitamin D Supplement Market Analysis by Mordor Intelligence

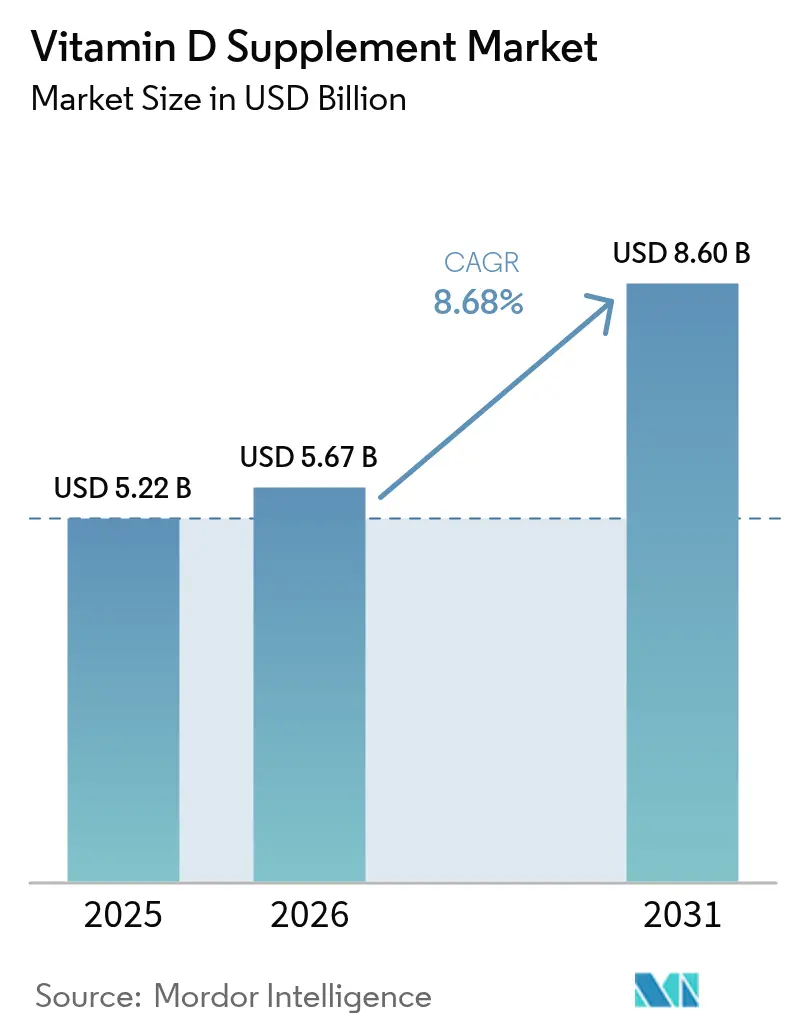

The Vitamin D Supplements market size is expected to grow from USD 5.22 billion in 2025 to USD 5.67 billion in 2026 and is forecast to reach USD 8.6 billion by 2031 at 8.68% CAGR over 2026-2031. The market demonstrates robust growth due to increasing consumer awareness regarding vitamin D deficiency and its implications for overall health. The market expansion is primarily attributed to the growing scientific evidence supporting vitamin D's crucial role in immune system modulation, cognitive function enhancement, and skeletal health maintenance. The medical community's revised guidelines advocating higher vitamin D serum levels have significantly influenced market dynamics, particularly in regions with limited sunlight exposure. Additionally, the aging population, rising prevalence of osteoporosis, and increased focus on preventive healthcare contribute substantially to market growth.

Key Report Takeaways

- By product type, vitamin D3 commanded 85.65% of the vitamin D supplements market share in 2025 while maintaining an 8.81% CAGR outlook for 2026-2031.

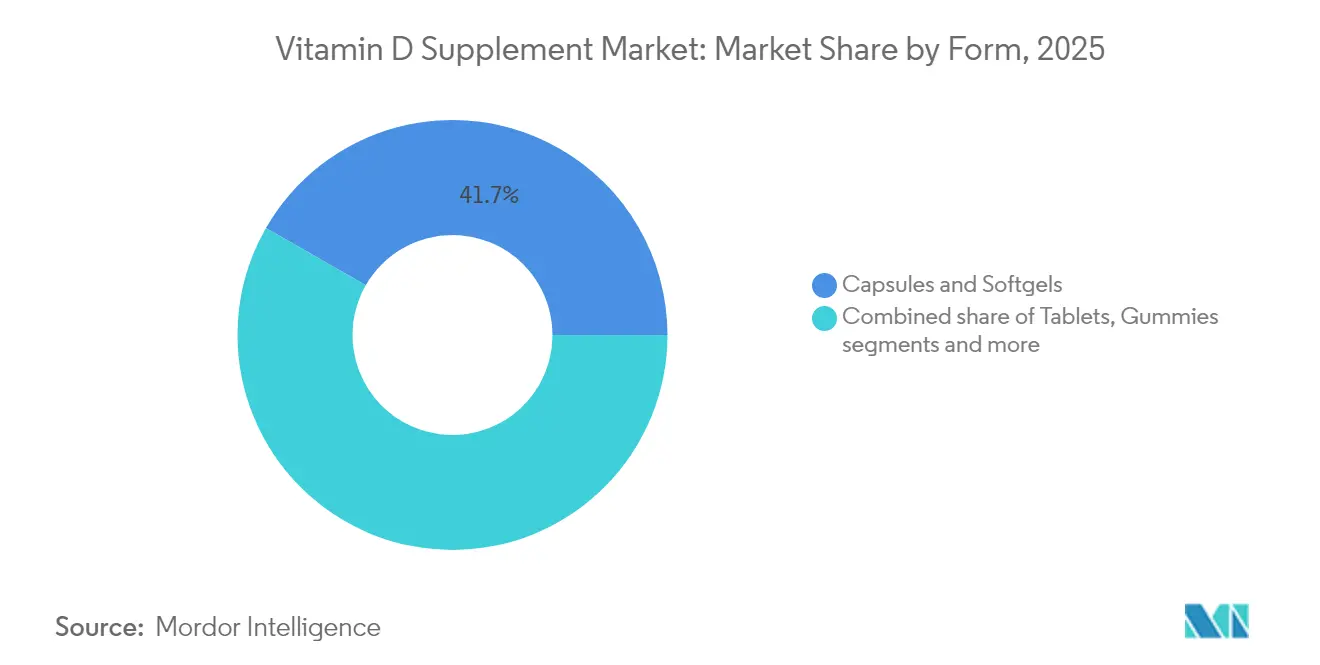

- By form, capsules and softgels held 41.72% of the vitamin D supplements market share in 2025. The gummies segment projects a CAGR of 11.92% during 2026-2031..

- By source, plant-based alternatives are expanding at a 14.6% CAGR, yet animal-derived products still represent 69.55% of the vitamin D supplements market size in 2025.

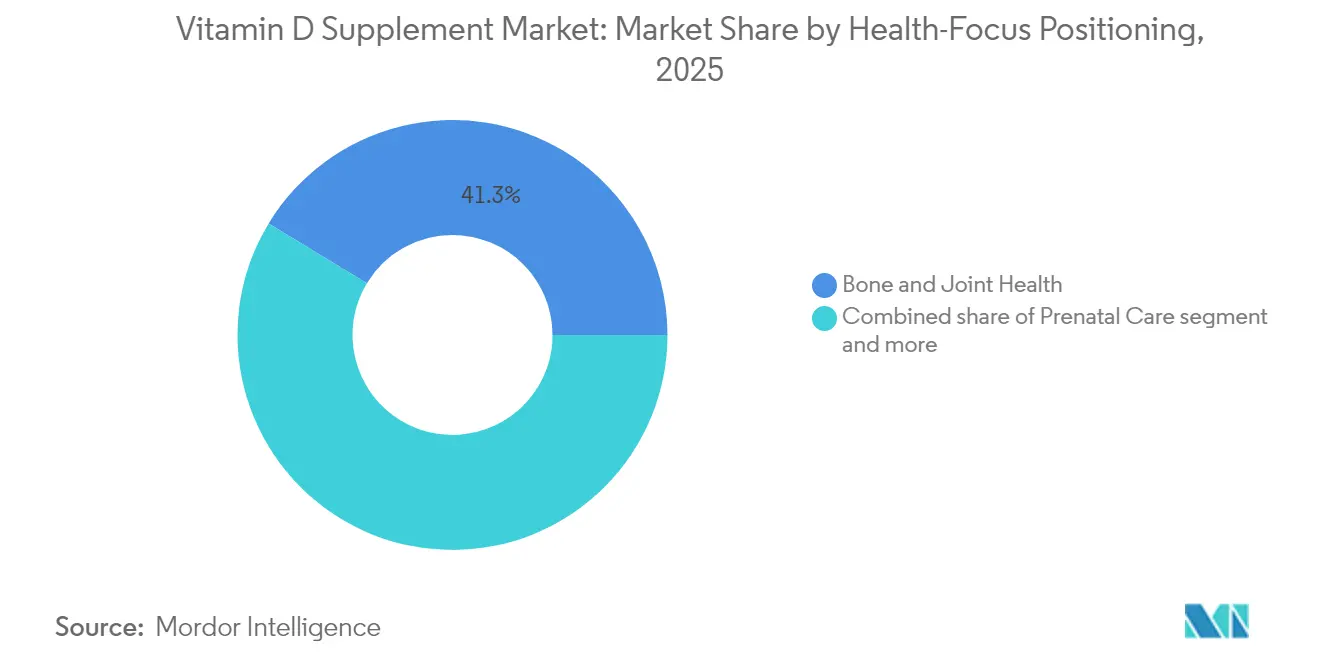

- By health-focus positioning, immune support products are growing at 11.95% CAGR, whereas bone and joint health leads with 41.33% revenue share in 2025.

- By distribution channel, specialty and health stores retained a 34.78% share in 2025, while online retail is scaling at 14.05% CAGR until 2031.

- By geography, North America captured 29.74% vitamin D supplement market share in 2025, and Asia-Pacific is set to rise at a 9.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vitamin D Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vitamin D deficiency drives global market growth and expansion | +3.2% | Global, with highest impact in Middle East, Northern Europe, India, China | Long term (≥ 4 years) |

| Growing elderly population fuels increased demand for bone health supplements worldwide | +2.1% | North America, Europe, Japan, China | Long term (≥ 4 years) |

| Medical community support and recommendations strengthen vitamin D market development | +1.7% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Pandemic-driven health concerns boost global vitamin D consumption and sales | +1.0% | Global | Short term (≤ 2 years) |

| Public health programs and educational initiatives increase vitamin D awareness globally | +0.5% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Growing consumer demand for plant-based supplements is supporting the market growth | +1.3% | Global, with stronger adoption in North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Vitamin D Deficiency Drives Global Market Growth and Expansion

The global vitamin D supplement market is experiencing significant growth, primarily driven by the widespread prevalence of vitamin D deficiency across populations and age groups. Vitamin D, which is essential for calcium absorption, immune function, and bone health, has gained increased attention as medical evidence links its deficiency to various health conditions, including osteoporosis, cardiovascular diseases, diabetes, autoimmune disorders, and compromised immunity. Modern urban lifestyles with limited sun exposure, particularly in densely populated areas and high-latitude regions, have resulted in millions of people failing to meet recommended daily vitamin D levels through natural synthesis or diet. Moreover, government agencies and international organizations have recognized vitamin D deficiency as a significant public health concern and implemented supportive measures. The National Health Service (NHS) in the United Kingdom advocates daily vitamin D supplementation, particularly during autumn and winter months. Similarly, Health Canada requires vitamin D fortification in milk and promotes supplementation, especially for older adults. These official endorsements validate the importance of vitamin D supplementation and enhance consumer confidence in supplements as a necessary health intervention.

Growing Elderly Population Fuels Increased Demand for Bone Health Supplements Worldwide

The global aging population trend is increasing the demand for vitamin D supplements, particularly those targeting bone and joint health. Research demonstrates that vitamin D supplementation in older adults supports both osteoporosis prevention and functional mobility maintenance while reducing disability risks. Companies are developing products that address bone health, mobility, and mental well-being for older consumers. The market features age-specific formulations designed to overcome absorption challenges and meet higher dosage requirements of elderly populations, establishing a premium market segment. This demographic shift is evidenced by World Bank data, which reports that the United States population aged 65 and over increased from 16.92% in 2022 to 17.43% in 2023, further accelerating the demand for specialized vitamin D supplements [1]Source: World Bank, "World Development Indicators", databank.worldbank.org.

Medical Community Support and Recommendations Strengthen Vitamin D Market Development

The medical community's evolving understanding of optimal vitamin D levels is transforming the supplement market. Research demonstrates vitamin D's importance beyond bone and calcium metabolism, prompting healthcare professionals to recommend supplementation to diverse patient groups. Medical practitioners now advise vitamin D supplements for infants, pregnant women, individuals with autoimmune disorders, metabolic syndromes, and those with limited sun exposure, in addition to traditional recommendations for the elderly and at-risk populations. This broader medical support has established vitamin D as an essential preventive health supplement. Healthcare provider recommendations have increased consumer confidence in vitamin D supplementation. Global medical organizations provide guidelines that support market growth. The Endocrine Society and the American Academy of Pediatrics (AAP) advocate vitamin D supplementation from infancy, with the AAP recommending 400 IU daily for breastfed infants to prevent rickets.[2]Source: Centers for Disease Control and Prevention (CDC), “Vitamin D and Breastfeeding”, cdc.gov .

Pandemic-Driven Health Concerns Boost Global Vitamin D Consumption and Sales

The COVID-19 pandemic increased consumer interest in immune support supplements, particularly vitamin D, following research indicating its importance in respiratory health and immune function. This increased awareness has led to lasting changes in consumer behavior, as supplementation became a regular practice rather than a temporary response to the pandemic. Consumers now view supplements as an integral part of their health maintenance routines, moving away from the previous pattern of occasional use. This shift is notable among younger consumers, who have begun incorporating vitamin D supplements into their daily routines. The pandemic also transformed purchasing patterns, with e-commerce becoming a primary distribution channel, allowing direct-to-consumer brands to expand their market presence through digital marketing and subscription services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit products impact market growth of vitamin D supplements market | -0.8% | Global, with highest impact in developing regions | Medium term (2-4 years) |

| Competition from fortified functional foods diverts consumer spending from standalone supplements | -0.5% | North America, Europe, Australia, Japan | Medium term (2-4 years) |

| High cost of premium supplements reduces affordability in low-income markets | -0.7% | Developing regions, emerging markets, rural areas | Long term (≥ 4 years) |

| Supply chain disruptions affecting raw material availability and distribution of vitamin D products | -0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Impact Market Growth of Vitamin D Supplements Market

The presence of counterfeit and substandard vitamin D supplements poses a significant market constraint by eroding consumer trust and risking negative health effects. According to the United States Pharmacopeia's 2024 policy position, the dietary supplements market expanded from 4,000 products in 1994 to approximately 80,000 products in 2024, creating substantial challenges for quality control and regulatory oversight. This market expansion has enabled some manufacturers to introduce products containing inconsistent or insufficient vitamin D levels, particularly in regions with weak regulatory enforcement. Quality issues are most evident in expanding online marketplaces, where product authenticity verification remains difficult. While the industry has implemented solutions such as blockchain traceability, authentication systems, and consumer awareness programs, these measures increase operational costs, particularly affecting smaller manufacturers. The counterfeit supplement problem is more severe in developing markets with emerging regulatory frameworks, which may restrict market growth in areas with high vitamin D deficiency rates and market expansion opportunities.

Competition From Fortified Functional Foods Diverts Consumer Spending from Standalone Supplements

The growth in vitamin D-fortified foods and beverages presents significant competition for traditional supplements by providing consumers with convenient ways to meet their nutritional needs through a regular diet. This trend is prominent in developed markets, where manufacturers incorporate vitamin D fortification to enhance product value. The 2020-2025 Dietary Guidelines for Americans recognize both fortified foods and supplements as valid sources for meeting nutritional requirements. Consumers increasingly favor obtaining nutrients through food sources, viewing fortified products as a more natural approach to nutrition compared to supplements. This preference is especially strong among health-conscious individuals who typically purchase premium supplements. In response, supplement manufacturers are focusing on distinctive advantages such as precise dosage control, specialized formulas, and enhanced absorption technologies that fortified foods cannot provide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Gummies Disrupt Traditional Delivery Methods

The form factor landscape is transforming, with gummies showing the highest growth rate at a CAGR of 11.92% from 2026-2031. However, capsules and softgels remain the market leaders, holding a 41.72% share in 2025. This evolution reflects consumer preferences for convenient and enjoyable supplement consumption methods that fit easily into daily routines. Gummies have gained particular popularity among Gen Z and Millennial consumers who seek alternatives to traditional supplements. Their appeal extends beyond taste, addressing pill fatigue and swallowing difficulties that impact supplement adherence across age groups.

Tablets retain substantial market presence due to their cost-effectiveness and stability benefits. Liquid formulations are increasing in popularity for their versatility and absorption advantages, especially in pediatric and geriatric applications. Powders have established a position in sports nutrition, frequently combined with protein and performance supplements. Innovation across form factors focuses on clean-label formulations, including reduced-sugar gummies, plant-based tablet excipients, and organic liquid formulations. This expansion of delivery formats is growing the market by attracting consumers who previously avoided supplements due to format limitations or compliance issues.

By Product Type: D3 Dominates While Expanding Applications

The vitamin D supplements market is dominated by Vitamin D3 (cholecalciferol), which accounts for 85.65% market share in 2025. The segment is expected to grow at a CAGR of 8.81% from 2026-2031. D3's market leadership is attributed to its higher bioavailability and effectiveness, as studies show it is more efficient in increasing and sustaining serum 25-hydroxyvitamin D levels compared to D2. Research indicates D3's benefits extend beyond bone health to immune function, cardiovascular health, and cognitive performance. While Vitamin D2 (ergocalciferol) remains available through prescriptions and plant-based products, its market share decreases as vegan D3 alternatives become more available.

The market shows advancement in delivery systems and formulation technologies to improve absorption and effectiveness. Companies are implementing microencapsulation techniques to enhance vitamin D3's stability and prevent degradation across various product forms. Oil-based formulations are becoming more prevalent due to their enhanced absorption characteristics. Production methods are also evolving, as demonstrated by Nutriearth's development of natural vitamin D3 oil that replicates the body's natural synthesis process without chemical extraction, which recently received marketing approval in Canada. These technological improvements are expanding D3's presence across product categories and consumer segments, supporting continued market growth despite its established market position.

By Source: Plant-Based Alternatives Reshape Market Dynamics

Animal-based vitamin D holds a 69.55% market share in 2025, while plant-based/vegan alternatives demonstrate a 14.6% CAGR from 2026-2031. This growth in plant-based options reflects consumer preferences for sustainable and ethical products, which are increasingly associated with wellness benefits. The plant-based vitamin D market is expanding beyond traditional vegan consumers to include flexitarians and health-conscious individuals. Companies like Hi-D are developing vitamin D products from UV-exposed mushrooms, providing whole-food alternatives with additional nutritional benefits.

Synthetic vitamin D maintains a market position by offering cost-effective supplementation options for price-sensitive consumers. The segment continues to improve through technological advancements that enhance product purity and reduce environmental impact. Animal-based vitamin D, while experiencing market share decline, benefits from established supply chains and consumer familiarity. Companies in this segment are implementing sustainable practices and transparent sourcing, particularly in lanolin extraction. The availability of multiple vitamin D sources enables companies to target specific consumer segments based on preferences, supporting focused brand positioning and customer retention.

By Health-Focus Positioning: Immune Support Accelerates Beyond Traditional Applications

Bone and joint health positioning maintains market dominance with a 41.33% share in 2025, while immune support emerges as the fastest-growing positioning segment, projected to grow at a 11.95% CAGR from 2026-2031. The immune support segment's growth reflects the shift in consumer perception of immune health from a seasonal concern to a year-round priority following the pandemic. Vitamin D's immune-modulating properties have gained increased recognition, particularly among younger consumers who prioritize immune resilience over bone health. The prenatal care segment, though specialized, continues to expand due to increased understanding of vitamin D's importance in maternal and infant health.

The others category includes positioning opportunities in mood support, cognitive function, and cardiovascular health, offering market differentiation potential. These segments typically feature higher price points and targeted marketing to specific health-conscious consumer groups. Companies are adopting multi-benefit positioning strategies that highlight vitamin D's multiple physiological functions, developing products that address several health outcomes. This comprehensive approach reflects consumers' understanding of interconnected health systems and positions vitamin D as a core component in overall supplementation strategies. This positioning evolution enables companies to enhance their value propositions and expand their consumer base while maintaining existing product formulations.

By Distribution Channel: Digital Transformation Reshapes Consumer Access

The vitamin D supplement distribution landscape is undergoing a structural change, with online retail achieving a 14.05% CAGR from 2026-2031. Specialty and health stores maintain market leadership with a 34.78% market share in 2025. The transition to digital channels reflects evolving consumer purchasing behavior, initially accelerated by the pandemic but maintained through operational efficiency, expanded product selection, and customized purchasing options. Online channels demonstrate strong performance for vitamin D supplements due to product uniformity, consistent purchase cycles, and recurring revenue opportunities. The distribution landscape is projected to stabilize by 2025, with natural and specialty stores, e-commerce, and mass market channels reaching equivalent market positions.

Supermarkets and hypermarkets maintain a strong market presence through integration with regular grocery shopping. These retailers are expanding their vitamin D product range to include premium formulations. Direct selling, practitioner channels, and fitness centers serve specific market segments through targeted offerings. Distribution channel diversification enables companies to implement omnichannel strategies while maintaining brand consistency. Online brands drive product innovation, while traditional retail brands emphasize in-store visibility and customer education.

Geography Analysis

North America holds 29.74% market share in 2025, supported by high consumer awareness, healthcare spending, and comprehensive regulatory standards. The region's market position stems from its adoption of innovative delivery formats and specialized formulations, particularly in direct-to-consumer channels. The United States market shows distinct segmentation across price points, with premium brands focusing on quality, bioavailability, and targeted benefits. Canada's vitamin D market is strengthened by regulatory policies ensuring product safety and efficacy, particularly during winter months with limited sunlight. The region's aging population drives demand for bone health supplements, while preventive health trends expand consumption across age groups.

Europe maintains a significant market share, with growth varying across countries based on deficiency rates, regulations, and consumer preferences. The European Union's regulatory framework guides market development while prioritizing consumer safety. The United Kingdom and Germany dominate in market value, while Nordic countries demonstrate high per capita consumption due to geographical factors and deficiency awareness. European markets show strong development in plant-based vitamin D products, reflecting consumer demand for sustainable options.

Asia-Pacific shows the highest growth rate at 9.55% CAGR from 2026-2031, driven by health awareness, increasing incomes, and recognition of vitamin D deficiency. China's market expansion is led by Caltrate through product launches and market activation. India presents growth opportunities owing to vitamin D deficiency, while Japan's market is characterized by an aging population and a focus on preventive health, supporting premium vitamin D products. Japan's elderly population segment (aged 65 years and older) constituted 29.6% of the total population in 2023, according to the World Bank . E-commerce development enhances access to international brands and specialized products. Regional manufacturers compete through locally adapted formulations, including combination supplements addressing common nutritional gaps in Asian diets.

Regulatory Landscape

Regulation of vitamin D supplements is shaped by ingredient permissibility, labeling, and safety limits, with the European Union and United States setting influential reference points. In the EU, Directive 2002/46/EC governs food supplements, and recent updates broaden allowable vitamin D sources: Commission Regulation (EU) 2025/352 added calcidiol monohydrate to the permitted vitamin D sources list for food supplements, creating a formal pathway for higher-bioavailability vitamin D forms within the supplement category. In parallel, novel food authorizations continue to define which new vitamin D sources can be marketed and under what conditions. Novel food approvals also affect product design and competitive access in Europe. Commission Implementing Regulation (EU) 2024/1052 authorized calcidiol monohydrate as a novel food with a five-year period of data protection tied to a single authorized operator, while Commission Implementing Regulation (EU) 2025/691 authorized vitamin D2 mushroom powder as a novel food with specific use restrictions, including for infants and young children. In the United States, the FDA framework for dietary supplements and related guidance, alongside enforcement of labeling and claims (including advertising oversight in practice), keeps compliance, substantiation, and quality systems central to go-to-market, while regions such as ASEAN follow general principles for maximum vitamin and mineral levels but remain fragmented at the national implementation level.

Value Chain Analysis

The vitamin D supplement value chain starts with upstream vitamin D ingredient production and then flows through formulation, packaging, and distribution into retail and practitioner channels. For vitamin D3, key raw material routes include lanolin (sheep wool grease) for conventional supply and lichen for vegan positioning, followed by UV conversion steps, purification, and stabilization into intermediate formats such as beadlets, oils, or powders that are then used by finished-product manufacturers. Large ingredient producers and integrated manufacturers, including dsm-firmenich and major Chinese producers (for example, Zhejiang Garden Biochemical High-Tech Co., Ltd., Zhejiang NHU Co., Ltd., and Xiamen Kingdomway Group Company), supply global brand owners and contract manufacturers. Midstream participants include distributors that aggregate and qualify inputs for finished-product makers, with players such as Prinova Group LLC and Barentz International B.V. supporting global reach, documentation, and lead-time management. Downstream, brand owners sell through specialty and health stores, mass retail, online platforms, and practitioner channels, with online retail increasing the importance of traceability and authenticity controls in response to counterfeit risks highlighted in the broader supplements market. Cross-border trade requirements and import scrutiny add friction in some markets (for example, India import processes involving ICEGATE/SWIFT filings and FSSAI document scrutiny), while periodic local disruptions in some producing regions can tighten availability for high-demand formats such as oils and beadlets used across capsules, softgels, and gummies.

Competitive Landscape

The vitamin D supplements market is fragmented. This structure creates a competitive environment where established pharmaceutical and consumer health companies operate alongside specialized nutrition firms and emerging wellness brands. The market dynamics allow scale advantages for industry leaders while providing innovation opportunities for agile competitors focusing on specific consumer segments or distribution channels. Major market players include Nestle S.A., Haleon plc, NOW Foods, Amway Corporation, and Herbalife Nutrition Ltd.

The competitive landscape continues to evolve through strategic partnerships. For example, Nutriearth's collaboration with AIDP Inc. for North American distribution of its natural vitamin D3 oil enables smaller innovators to access broader markets through established distribution networks. Companies differentiate themselves across the competitive spectrum, with premium brands focusing on quality credentials, specialized formulations, and enhanced bioavailability. Value-oriented players compete through cost efficiency and broad distribution. Market opportunities remain in personalized supplementation, condition-specific formulations, and innovative delivery systems that improve compliance and user experience.

Digital capabilities influence competitive dynamics, as direct-to-consumer brands use data analytics and targeted marketing to build consumer relationships outside traditional retail channels. Regulatory expertise has become a competitive advantage amid increasing global compliance requirements. The FDA's 2024 revised guidance for dietary supplements containing new dietary ingredients creates additional barriers to entry for smaller players. The market faces competition from adjacent categories, including functional foods and beverages fortified with vitamin D, requiring supplement manufacturers to demonstrate clear value propositions against these alternatives.

Vitamin D Supplement Industry Leaders

-

Nestle S.A.

-

Haleon plc

-

NOW Foods

-

Amway Corporation

-

Herbalife Nutrition Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory openings for new vitamin D forms and formats create clear whitespace for differentiation beyond standard cholecalciferol products. In the EU, Commission Regulation (EU) 2025/352 explicitly permitting calcidiol monohydrate as a vitamin D source for food supplements supports premium, bioavailability-led positioning, while novel food authorizations such as Commission Implementing Regulation (EU) 2025/691 for vitamin D2 mushroom powder expand plant-based and whole-food style claims within permitted use conditions. These approvals directly align with observed market traction for plant-based/vegan sources and faster-growing consumer-friendly delivery formats (notably gummies), giving manufacturers room to build new SKUs that are both compliant and meaningfully differentiated. Opportunities also extend into adjacent compliance-enabled routes that reshape demand signals between supplements and fortified foods. In the United States, the FDA amendment allowing vitamin D3 as a nutrient supplement in yogurt and other cultured dairy products (September 2025) reinforces competition from fortified functional foods but also increases consumer awareness and can support cross-category portfolio strategies for companies active in both supplements and nutrition. At the same time, the European Commission timetable for harmonized Maximum Permitted Levels (MPLs), including a planned public consultation in Q3 2026 with legal adoption targeted for Q1 2028, elevates demand for reformulation capability, dosage strategy, and pan-EU label readiness, which favors operators with strong regulatory and quality infrastructure and creates service opportunities for contract manufacturers and compliant ingredient suppliers.

Recent Industry Developments

- June 2026: NOW Foods partnered with LeafWorks to implement a next-generation sequencing lab at its Sparks, Nevada facility to advance botanical identity testing. While focused on botanicals, the capability supports broader supplement quality programs and strengthens supply-chain verification practices amid counterfeit and adulteration concerns across online-heavy channels.

- May 2025: Pharmavite LLC established a new manufacturing and R&D facility in New Albany, Ohio, a USD 250 million, 225,000-square-foot site with capacity for future expansion. The investment increases domestic manufacturing scale for supplements and supports faster innovation cycles and supply reliability for high-volume categories that include vitamin D.

- February 2024: Bobbie expanded into the infant nutrition category by launching two organic infant supplements, including Vitamin D Drops, broadening product portfolio and expanding channels to direct-to-consumer and specialty retailers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers retail and practitioner-sold vitamin D dietary supplements that are intended for human use and taken orally. The value includes common finished-dose forms, across channels, and it counts products containing vitamin D2 or vitamin D3.

Scope exclusions: Excludes injectable vitamin D therapies and bulk vitamin D used for animal feed, food fortification, or personal-care formulations.

Segmentation Overview

-

By Product Type

- Vitamin D2

- Vitamin D3

-

By Form

- Tablets

- Capsules and Softgels

- Gummies

- Powders

- Liquid

- Others

-

By Source

- Synthetic

- Animal-Based

- Plant-Based/Vegan

-

By Health-Focus Positioning

- Bone and Joint Health

- Immune Support

- Prenatal Care

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty and Health Stores

- Online Retailers

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the fact base and to keep assumptions realistic when data is scattered across brands and channels. We rely on public sources such as the NIH Office of Dietary Supplements and CDC nutrition-related data, along with WHO publications where deficiency guidance is referenced across countries.

To anchor supply and trade signals, we review sources such as UN Comtrade for trade flows, customs and tariff schedules where relevant, and peer-reviewed nutrition journals that report deficiency prevalence and supplementation behavior. In parallel, company annual reports, earnings transcripts, and investor presentations help map how supplement portfolios and channel mixes change over time. For spot checks, selective paid subscriptions are used for company financials and intelligence, patent databases, and shipment-level import and export views, mainly to validate directionally. These examples are not exhaustive, and many other public and reference sources were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions and fill gaps that are difficult to read from public data alone, such as price ladders by form factor and how much demand is tied to practitioner recommendations. We spoke with a mix of supplement manufacturers, ingredient distributors, pharmacy and e-commerce channel participants, and nutrition-focused professionals across major consuming regions, so the model reflects real purchase behavior rather than label claims alone.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 21% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 21% | Managers: 42% | Americas: 18% |

Market-Sizing & Forecasting

The sizing starts with a top-down build where population and adult-age mix, vitamin D deficiency prevalence, and likely supplementation rates are combined to form a demand pool, which is then converted into value using typical daily dosage ranges and average selling prices across key oral formats. Because label strengths vary widely, dosage normalization is applied so high-IU products do not inflate value without a matching price premium.

After that, selective bottom-up approximations are used as a cross-check, using sampled brand and channel price points, channel mix splits, and supplier and distributor feedback on category run rates. When a country has limited visibility, proxies are used from comparable markets based on income level, pharmacy penetration, and e-commerce share, and then adjusted through expert feedback. For forecasting, scenario analysis is used and the assumptions are guided by how fast deficiency screening, preventive health interest, and channel expansion are expected to move, followed by re-checking price progression so inflation effects are not double-counted.

Data Validation & Update Cycle

Outputs are validated in a few passes so the final numbers remain consistent with real-world signals. We compare the modeled totals against independent indicators such as supplement retail growth commentary, channel expansion signals, and trade movement patterns, and then check for outliers where implied per-capita spend looks unrealistic.

If large variances show up by country or by year, the assumptions are revisited and, where needed, respondents are re-contacted to confirm whether the issue is dosage, pricing, or channel mix. Before sign-off, a separate analyst review is completed to check formulas, unit logic, and currency conversions. The report is refreshed annually, and interim updates are made when material events can change demand or pricing, followed by a final pre-delivery pass so clients receive the latest view.

Mordor Intelligence's Vitamin D Supplements Market Size Compared Against Other Published Estimates

Published market values for vitamin D supplements can look far apart, even when the topic sounds identical, because the underlying scope and conversion steps are not aligned. Differences usually come from what gets counted as a supplement versus an ingredient, how dosage and pricing are translated into value, and how frequently the inputs are refreshed.

Bulk vitamin D used in food fortification sits outside Mordor Intelligence's scope, and this single inclusion choice explains why some published values look smaller or larger when they mix ingredients, fortified foods, and finished supplements in one total. The other common gap comes from how D2 and D3 are treated, where some sources focus only on D3, and from how currency timing and average selling price progression are applied during inflationary periods.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.22 B (2025) | |

| Industry Publisher A | USD 2.80 B (2025) | Often uses a narrower counted basket in practice, with weaker clarity on whether practitioner channels and higher-priced formats are fully captured, which can compress the value even in the same year. |

| Trade Publisher B | USD 1.50 B (2025) | Focuses on vitamin D3 supplements only, which leaves out vitamin D2 products and can also understate value if gummy, liquid, and premium strength pricing is not normalized by dose and form. |

The spread in the table is mainly explained by scope and conversion mechanics, rather than a disagreement that demand exists. When the counted product set is kept to finished oral supplements and the value is tied back to dosage-normalized consumption and format-level pricing, the total becomes easier to audit and repeat year to year.

Key Questions Answered in the Report

What is the current value of the vitamin D supplements market?

The market is valued at USD 5.67 billion in 2026 and is forecast to reach USD 8.6 billion by 2031.

Which segment holds the largest vitamin D supplements market share?

Vitamin D3 dominates with 85.65% share in 2025 because of superior bioavailability.

Why are gummies growing so quickly within the category?

Gummies alleviate pill fatigue, appeal to younger users, and post a 11.92% CAGR through 2031.

Which region is expanding the fastest?

Asia-Pacific is projected to grow at 9.55% CAGR, driven by rising deficiency awareness and e-commerce access.

Page last updated on: