Cardiovascular Health Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

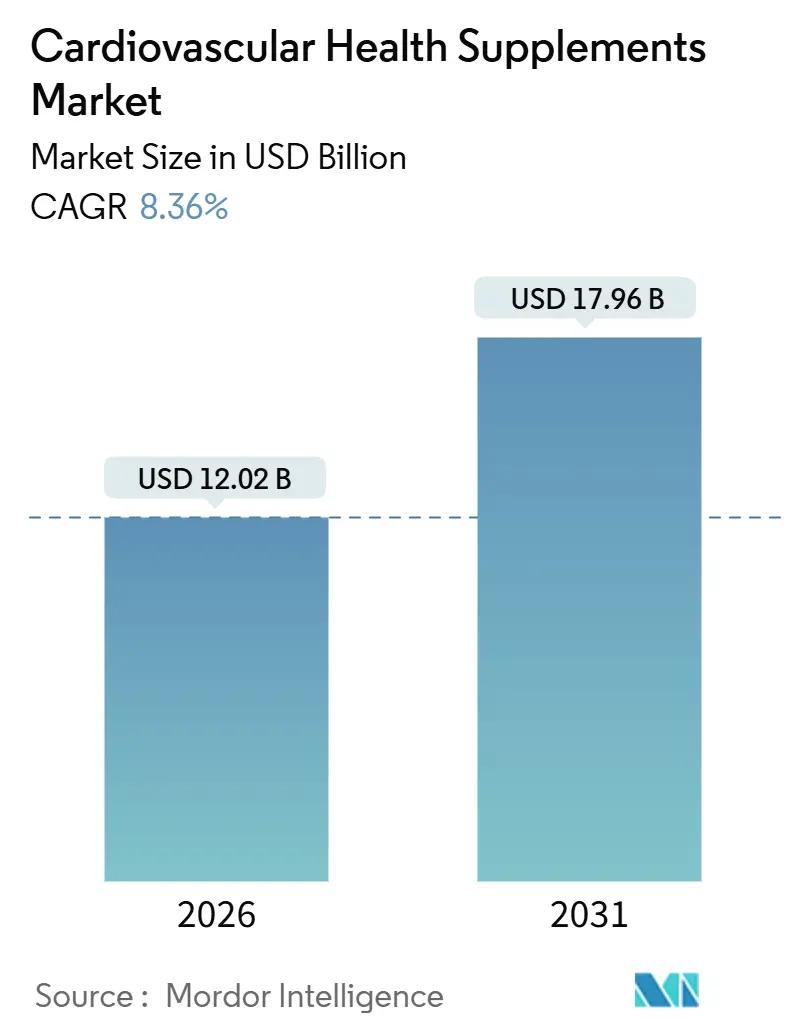

| Market Size (2026) | USD 12.02 Billion |

| Market Size (2031) | USD 17.96 Billion |

| Growth Rate (2026 - 2031) | 8.36% CAGR |

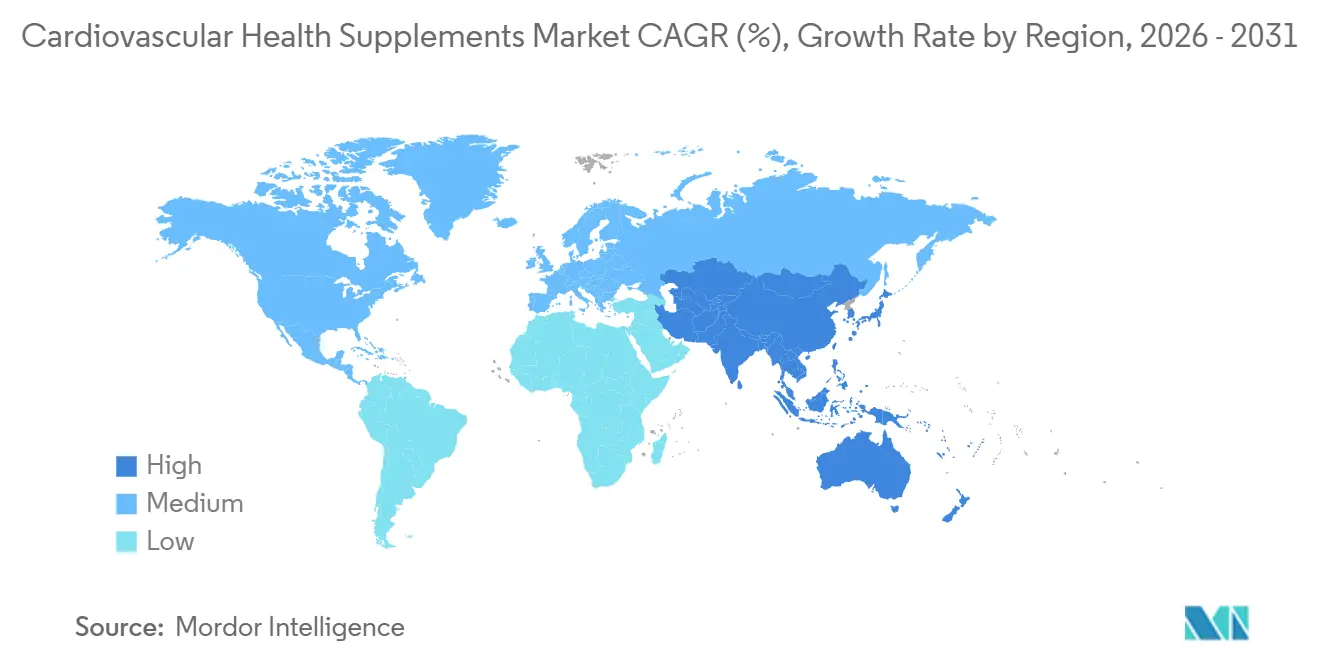

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cardiovascular Health Supplements Market Analysis by Mordor Intelligence

The Cardiovascular Health Supplements Market size is estimated at USD 12.02 billion in 2026, and is expected to reach USD 17.96 billion by 2031, at a CAGR of 8.36% during the forecast period (2026-2031).

Strong demand arises from aging populations, greater acceptance of preventive care, and a steady pipeline of peer-reviewed studies clarifying dose–response relationships for omega-3, CoQ10, and magnesium. Sustained innovation in bioavailability technologies, the rapid adoption of e-commerce subscription plans, and policy moves that emphasize chronic-disease mitigation further amplify expansion. Competitive intensity stays moderate because multinational pharmaceutical companies and digitally native brands pursue different playbooks, yet both converge on clinically validated, sustainably sourced ingredients. Together, these forces position the cardiovascular health supplements market for durable, mid-single-digit volume gains and steady premiumization as consumers trade up to evidence-backed formulations.

Key Report Takeaways

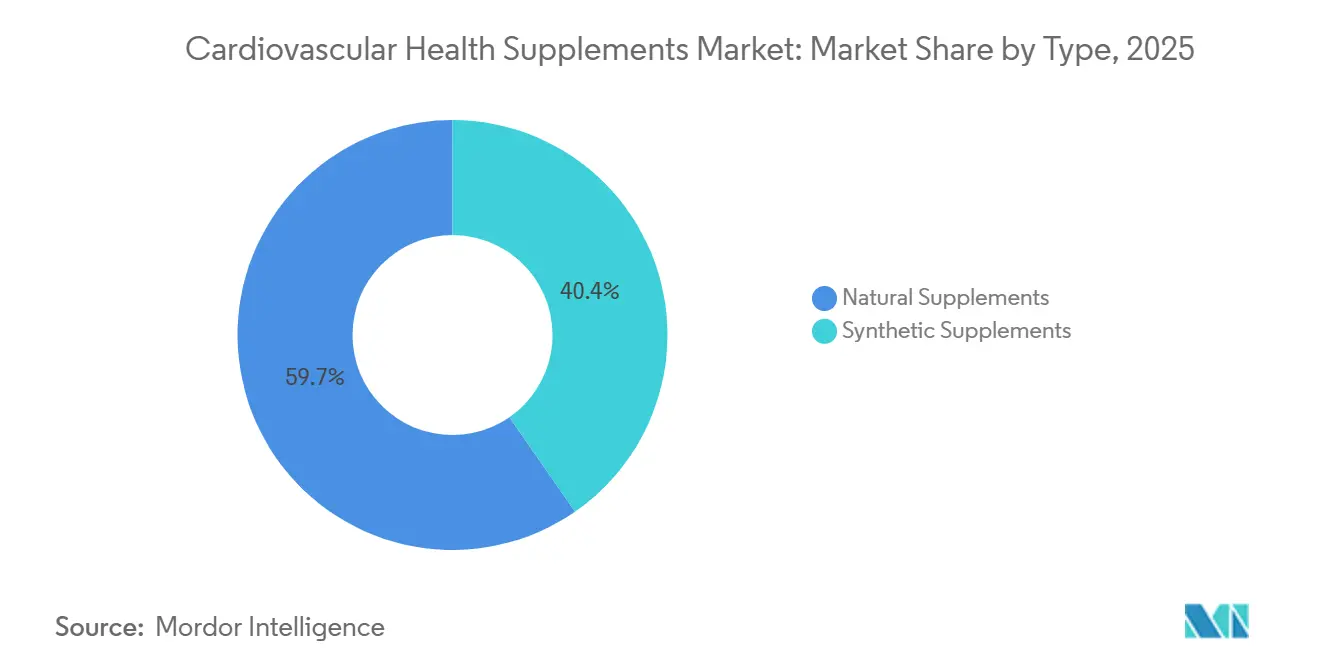

- By type, natural supplements led with a 59.65% share in 2025, whereas synthetic variants are forecast to register a 10.45% CAGR through 2031.

- By ingredient, vitamins and minerals accounted for a 42.45% share in 2025; omega fatty acids are set to grow at a 10.55% CAGR to 2031.

- By form, capsules captured 31.45% of the market in 2025, while softgels are on track for a 10.76% CAGR through 2031.

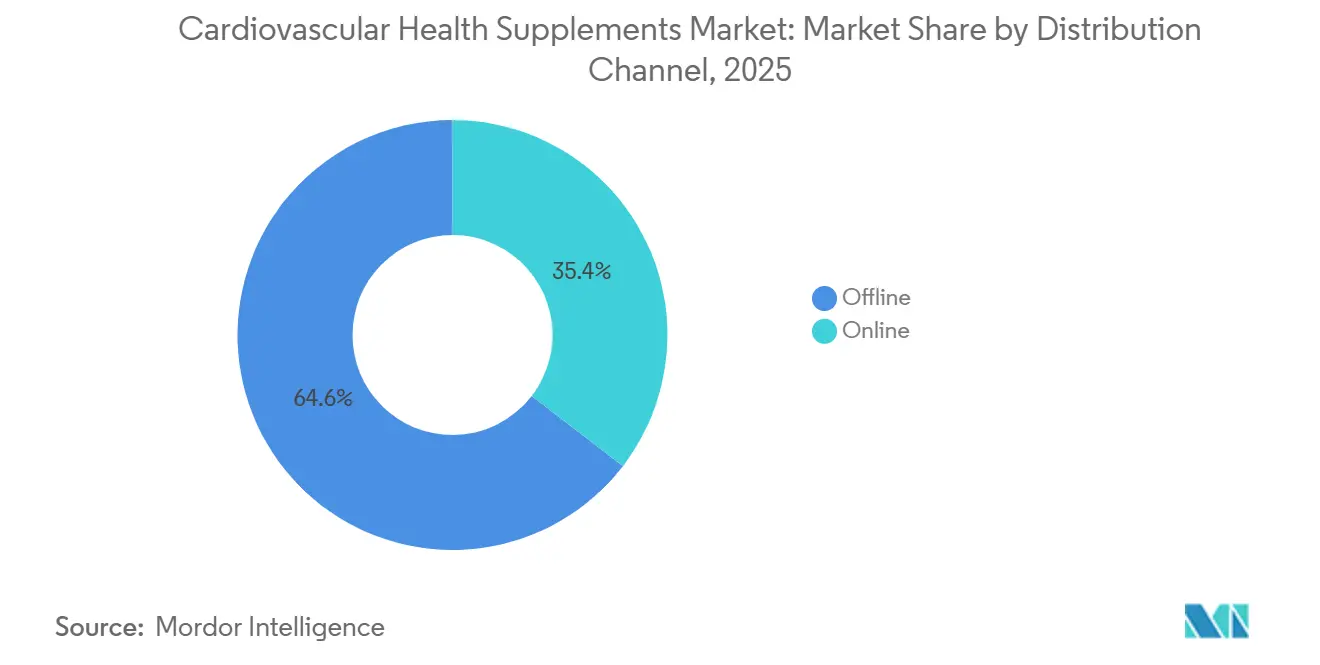

- By distribution channel, offline outlets commanded a 64.56% share in 2025; online platforms will advance at an 11.65% CAGR through 2031.

- By end user, adults aged 18-64 years held 58.65% share in 2025, and athletes plus fitness enthusiasts will post an 11.32% CAGR to 2031.

- By geography, North America dominated with a 42.48% share in 2025; Asia-Pacific will deliver the fastest 9.54% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cardiovascular Health Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular diseases | +1.8% | Global, highest burden in North America, Europe, emerging Asia-Pacific | Long term (≥ 4 years) |

| Growing consumer focus on preventive care | +1.5% | North America and Europe lead, urban Asia-Pacific catching up | Medium term (2-4 years) |

| Aging population and longevity trends | +1.4% | Global, especially Japan, Germany, Italy, China | Long term (≥ 4 years) |

| Expansion of personalized nutrition | +0.9% | North America and Western Europe, affluent Asia-Pacific | Medium term (2-4 years) |

| Clinical validation of bioavailability tech | +0.7% | Global, earliest uptake in North America and Europe | Medium term (2-4 years) |

| Integration into telehealth cardiac care | +0.6% | North America and Europe, pilot programs in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular Diseases

Cardiovascular disease caused 19.8 million deaths worldwide in 2023 and generated 437 million disability-adjusted life years, making it the leading global killer. In the United States, heart disease accounted for 680,981 deaths in 2023, while 5% of adults live with coronary heart disease. Modifiable risks—high systolic blood pressure, elevated LDL cholesterol, poor diet, and physical inactivity—drive 79.6% of cardiovascular DALYs. This burden keeps clinicians and patients searching for adjunct therapies that address those variables, underpinning durable demand for products in the cardiovascular health supplements market. Brands that can guarantee purity and dose precision for omega-3s, plant sterols, and CoQ10 align with evidence-based guidelines and secure hospital formulary adoption.

Growing Consumer Focus on Preventive Healthcare

Following the pandemic, preventive self-care surged: 57.6% of U.S. adults reported supplement use in 2017-2018, and 21.8% of seniors specifically took omega-3 products. Multiple-product stacking is standard, with 24.9% of older consumers using 4 or more supplements simultaneously[1]National Institutes of Health, “Dietary Supplement Use in U.S. Adults 2017-2018,” nih.gov. Subscription programs that bundle EPA-dominant omega-3s, CoQ10, magnesium, and plant sterols suit this habit by lowering unit prices, simplifying reordering, and supporting adherence. Rising health literacy and disposable income among urban professionals reinforce willingness to pay for clinically substantiated formulations, maintaining momentum for the cardiovascular health supplements market.

Aging Population and Longevity Trends

The global population aged 60 and over will reach 1.4 billion by 2030 and 2.1 billion by 2050, with 80% of the growth in low- and middle-income economies[2]United Nations, “World Population Ageing 2025 Highlights,” un.org. Age-related vascular stiffening and mitochondrial decline spur interest in nutrients that support nitric-oxide synthesis, antioxidant protection, and energy metabolism. CoQ10 supplementation yields a 5.6-percentage-point boost in left-ventricular ejection fraction among heart-failure patients. Magnesium intakes of 300-400 mg per day improve endothelial function and marginally reduce blood pressure, covering common deficits in older adults. Such findings broaden the cardiovascular health supplements market, as governments such as China promote proactive aging strategies under the Healthy China 2030 initiative.

Expansion of Personalized Nutrition Platforms

North American and European telehealth providers now combine lipid panels, genetic data, and wearable metrics to calibrate supplement regimens. APIs link supplement refills to blood-pressure dashboards, automating dose tweaks and adherence nudges. These data-driven services push clinically verified EPA, CoQ10, and magnesium into subscription models, elevating average order values and reducing dropout. Companies that integrate into remote cardiac-rehab software tap a new institutional revenue stream, deepening the cardiovascular health supplements market’s penetration into traditional healthcare pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexity and labeling gaps | -0.8% | Global, pronounced differences between FDA and EFSA | Long term (≥ 4 years) |

| Limited high-quality evidence for botanicals | -0.6% | Global, especially affects novel ingredients | Medium term (2-4 years) |

| Sustainability constraints on marine omega-3 | -0.4% | Global, supply pressure in Peru, Chile, Norway | Medium term (2-4 years) |

| Counterfeit proliferation in e-commerce | -0.3% | Global, unregulated marketplaces bear highest incidence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Complexity and Labeling Disparities

U.S. supplements fall under the Dietary Supplement Health and Education Act, allowing structure-function claims without pre-market FDA approval, while Europe’s Regulation 1924/2006 demands rigorous dossiers for any health statement[3]U.S. Food and Drug Administration, “DSHEA Overview,” fda.gov. Divergent daily-value units, allergen rules, and ingredient nomenclature force multinational brands to maintain region-specific SKUs, inflating inventory and compliance costs. Smaller entrants often forgo cross-border expansion, narrowing consumer choice and slightly capping the cardiovascular health supplements market growth trajectory.

Limited High-Quality Clinical Evidence for Certain Ingredients

Omega-3, plant sterols, and CoQ10 enjoy solid clinical foundations, but many botanicals lack randomized, placebo-controlled trials. The STRENGTH study delivered null cardiovascular results for high-dose EPA + DHA blends, provoking debates about formulation specificity. Vitamin D and B-complex trials produce inconsistent endpoints, weakening marketing claims and risking regulatory action. Evidence gaps hinder novel product launches and keep retail buyers conservative about shelf allocations, creating a mild drag on the cardiovascular health supplements market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Pharmaceutical-Grade Synthetics Gain Traction

Synthetic formulations will expand at a 10.45% CAGR through 2031, outpacing the natural segment that held a 59.65% share in 2025. In revenue terms, the synthetic slice of the cardiovascular health supplements market is projected to grow from USD 4.8 billion in 2026 to roughly USD 7.9 billion by 2031, as standardized doses resonate with physicians who value prescription-like purity. The REDUCE-IT trial, which used 4 g per day of icosapent ethyl, showcased a 25% reduction in major adverse cardiovascular events and validated the therapeutic promise of highly purified EPA. Natural products continue to appeal to consumers wary of “chemical” inputs, yet clinical endorsements and insurance reimbursement tilt hospital formularies toward synthetics.

Natural supplements retain dominance thanks to century-old fish-oil traditions and growing interest in plant-based extractions such as algal EPA-DHA, garlic, and hawthorn. Hybrid portfolios that combine certified-organic raw materials with precision-manufactured synthetics enable major suppliers to reach both audiences and hedge against regulatory shifts. Regional nuances matter: natural extracts lead in Southeast Asia, where acceptance of traditional medicine is high, whereas synthetic EPA gains traction in the United States through prescription channels like Vascepa. The cardiovascular health supplements market share for synthetic products could reach 45% in hospital pharmacies by 2031, assuming guideline adoption remains on course.

By Ingredient: Omega Fatty Acids Accelerate on Evidence Wave

Vitamins and minerals commanded a 42.45% slice of the cardiovascular health supplements market in 2025, but omega fatty acids are forecast to record a 10.55% CAGR through 2031, the sharpest among all ingredient groups. Global omega-3 sales are expected to rise from USD 3.3 billion in 2026 to USD 5.4 billion in 2031, representing nearly 30% of the cardiovascular health supplements market size at the end of the period. High-EPA formulations outperform blends containing substantial DHA, as suggested by contrasting outcomes in the REDUCE-IT and STRENGTH studies.

Beyond EPA, CoQ10 continues a steady climb, supported by data showing a 5.6-point ejection-fraction gain in heart-failure populations. Plant sterols lower LDL by roughly 10% at 2-3 g per day and are eligible for qualified health claims in both the United States and Europe. Lesser-known botanicals like grape-seed extract struggle for shelf space because randomized trials remain scarce. Ingredient diversification thus clusters around well-validated actives, a trend that tightens links between supplement brands and pharmaceutical contract research organizations.

By Form: Softgels Optimize Lipophilic Uptake

Capsules held the largest 31.45% share in 2025, yet softgels are on course for a 10.76% CAGR as consumers seek better absorption of fat-soluble CoQ10 and vitamin K2. Re-esterified triglyceride omega-3 delivered in softgels raises the red-blood-cell omega-3 index more rapidly than identical doses packed in standard capsules, a benefit highlighted in multiple crossover trials. Enhanced uptake shortens time to measurable biomarker shifts, an outcome that resonates with data-driven users who monitor lipid panels via app integrations.

Tablets remain relevant for bulk multivitamin blends that prioritize cost efficiency over absorption speed. Liquids and chewables cater to pediatric and geriatric segments who struggle with swallowing, though they constitute a small revenue slice. Innovative vendors experiment with stick-pack powders containing micro-encapsulated lipids that disperse into water, giving athletes a portable option that mixes easily with workout beverages. Form choice increasingly serves as a branding lever rather than a mere packaging decision.

By Distribution Channel: Online Models Reshape Access

Offline stores owned 64.56% share in 2025, but online sales will post an 11.65% CAGR, making e-commerce the fastest channel through 2031. Direct-to-consumer brands wield auto-refill mechanisms that align shipment frequency with 30-day dose cycles, dampening the 3.6% cost-related nonadherence rate among older adults. Algorithmic recommendation engines upsell complementary nutrients, elevating annual order values.

Pharmacies maintain high levels of trust and remain the go-to venue for prescription-strength EPA and pharmacist-recommended plant sterols. Mass retailers appeal to price-sensitive shoppers, while specialty health stores court organic and non-GMO buyers. Hybrid strategies flourish: leading pharmacy chains offer click-and-collect, allowing shoppers to order online and pick up in-store, which blends the immediacy of brick-and-mortar with digital convenience. Regulatory agencies now spot-audit warehouse stocks of major marketplaces, nudging platforms toward stricter third-party seller vetting.

By End User: Athletic Demand Blurs Performance and Prevention

Adults aged 18-64 years contributed 58.65% of 2025 revenue, yet the athlete and fitness category will notch an 11.32% CAGR, reflecting rising interest in endothelial-support nutrients that double as workout aids. Studies demonstrate that 300 mg magnesium daily improves vascular function and lowers diastolic blood pressure, benefits prized by endurance runners seeking efficient oxygen delivery. Beetroot-based nitric oxide boosters crossover from sports nutrition to cardiovascular wellness, creating hybrid positioning opportunities.

Geriatric consumers sustain predictable demand driven by statin-associated CoQ10 depletion and rising hypertension prevalence. Pediatric use remains limited; in the absence of strong evidence, parents prefer dietary interventions over supplements. End-user messaging now segments by health objective: elite performance, active aging, or risk mitigation. Brands that tailor dose form, flavor, and subscription cadence to these motivations capture superior lifetime value.

Geography Analysis

North America dominated the cardiovascular health supplements market with a 42.48% share in 2025, a lead anchored by high supplement literacy and robust healthcare expenditure. U.S. adults allocate disposable income to self-directed prevention, and 21.8% of seniors already use omega-3 products. Clinical trial density in the region yields a steady stream of peer-reviewed endorsements that bolster pharmacist recommendations and hospital formulary inclusion. Canada shows similar behavioral patterns, while Mexico’s middle-class expansion is driving the launch of new pharmacy chains that stock U.S.-origin products.

Europe posts stable yet slower growth, hampered slightly by EFSA’s stringent claim requirements. Germany and Italy see elevated CoQ10 adoption due to statin co-prescription, whereas the United Kingdom favors plant sterols sold in grocery pharmacies. Consumer attitudes skew toward natural and organic, allowing brands that demonstrate Marine Stewardship Council certification to charge higher shelf prices.

Asia-Pacific will be the engine of incremental volume, logging a 9.54% CAGR through 2031. China’s Healthy China 2030 policy amplifies public education on dietary lipids, and e-commerce giants plug heart-health packs into livestream shopping events. Japan’s super-aged population continues to prioritize endothelial support, while South Korea’s biotech parks churn out fermentation-based algal oils to feed regional vegan demand. India sees urban upper-middle-class households embrace imported omega-3 and magnesium, but local producers lead in herbal blends melded with traditional Ayurvedic botanicals. Southeast Asian markets benefit from gradual ASEAN labeling harmonization, which trims port bottlenecks for multinational entrants.

South America and the Middle East & Africa remain niche but promising. Brazil’s elevated cardiovascular mortality rates have elevated public discourse around omega-3, and pharmacy chains are investing in private-label fish oil lines. Among Gulf Cooperation Council members, high per-capita income underpins demand for premium, purity-verified products, though import duties and hot-climate shipping constraints raise landed costs. African expansion is constrained by lower purchasing power and limited cold-chain logistics, prompting most brands to pilot only in South Africa and Kenya for now.

Competitive Landscape

The global market exhibits moderate concentration, with key players leveraging distinct strategies to maintain their competitive edge. Abbott, Bayer, Pfizer, and Nestlé Health Science capitalize on their established distribution networks and significant clinical research budgets to secure prominent end-cap displays in national pharmacy chains. In contrast, Nordic Naturals, Thorne, and NOW prioritize third-party testing and ingredient transparency to strengthen their presence among specialty retailers and practitioners. Direct-to-consumer leaders drive subscription retention rates above 65% by employing high-frequency digital campaigns, A/B-tested landing pages, and biomarker-based personalization.

Investment trends are shifting toward bioavailability technologies and sustainable sourcing solutions. BASF’s introduction of nano-emulsified omega-3 targets brands catering to athletic recovery, while DSM-Firmenich’s integration of telehealth services positions it as a strategic formulation partner rather than a commodity supplier. Algal-fermentation startups are attracting venture capital due to the appeal of vegan EPA-DHA, which mitigates risks associated with fishery quotas. To address counterfeit risks on gray-market platforms, established players are adopting blockchain batch tracking and in-package NFC tags, enabling consumers to verify product authenticity via smartphone applications.

Partnerships are expanding across the value chain, enabling greater operational efficiency. Contract development organizations now offer turnkey liposomal and self-emulsifying drug-delivery systems, allowing smaller brands to compete effectively without investing in manufacturing infrastructure. In Northern Europe and parts of North America, Marine Stewardship Council certification has become a critical standard, benefiting early adopters such as Nordic Naturals. Additionally, consolidation activity is expected to increase as pharmaceutical majors explore subscription-based business models that provide direct patient insights and diversify revenue streams.

Cardiovascular Health Supplements Industry Leaders

Abbott Laboratories

Bayer AG

Pfizer Inc.

Nestlé Health Science

DSM-Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: NRoute, one of the leading health and fitness supplement companies, launched Heartisafe, its latest innovation designed to support and enhance cardiovascular health. The new supplement features a potent proprietary blend of Fruitflow—a patented tomato extract and Grape Seed Extract.

- June 2025: Melody, a modern wellness brand offering clean, nature-based formulas launched Heart Tune, a new heart health supplement designed to support cardiovascular function with simplicity and science-backed ingredients. Now available on melodywellness.com, Amazon, and Walmart.

Global Cardiovascular Health Supplements Market Report Scope

As per scope of the report, cardiovascular health supplements are dietary products designed to support heart health by improving circulation, reducing cholesterol, and maintaining blood pressure. They often contain ingredients like omega-3 fatty acids, vitamins, and minerals. These supplements aim to promote overall heart wellness and prevent cardiovascular diseases.

The Cardiovascular Health Supplements Market is Segmented by Type (Natural Supplements and Synthetic Supplements), Ingredient (Vitamins & Minerals, Omega Fatty Acids, Herbs & Botanicals, Coenzyme Q10, Plant Sterols, and Other Ingredients), Form (Tablets, Capsules, Softgels, Liquid, Powder, and Other Forms), Distribution Channel (Offline and Online), End User (Adults 18-64 Years, Geriatric Population 65+ Years, Pediatric & Adolescents, and Athletes & Fitness Enthusiasts), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Natural Supplements |

| Synthetic Supplements |

| Vitamins & Minerals |

| Omega Fatty Acids |

| Herbs & Botanicals |

| Coenzyme Q10 (CoQ10) |

| Plant Sterols |

| Other Ingredients |

| Tablets |

| Capsules |

| Softgels |

| Liquid |

| Powder |

| Other Forms |

| Offline | Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets | |

| Specialty Health Stores | |

| Online | E-Commerce Marketplaces |

| Brand-owned Web Stores & Subscriptions |

| Adults (18-64 Years) |

| Geriatric Population (65+ Years) |

| Pediatric & Adolescents |

| Athletes & Fitness Enthusiasts |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Natural Supplements | |

| Synthetic Supplements | ||

| By Ingredient | Vitamins & Minerals | |

| Omega Fatty Acids | ||

| Herbs & Botanicals | ||

| Coenzyme Q10 (CoQ10) | ||

| Plant Sterols | ||

| Other Ingredients | ||

| By Form | Tablets | |

| Capsules | ||

| Softgels | ||

| Liquid | ||

| Powder | ||

| Other Forms | ||

| By Distribution Channel | Offline | Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets | ||

| Specialty Health Stores | ||

| Online | E-Commerce Marketplaces | |

| Brand-owned Web Stores & Subscriptions | ||

| By End User | Adults (18-64 Years) | |

| Geriatric Population (65+ Years) | ||

| Pediatric & Adolescents | ||

| Athletes & Fitness Enthusiasts | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cardiovascular health supplements market in 2031?

It is expected to reach USD 17.96 billion, expanding from USD 12.02 billion in 2026 at an 8.36% CAGR.

Which ingredient segment will see the fastest growth through 2031?

Omega fatty acids will grow at a 10.55% CAGR, outpacing vitamins, minerals, and botanicals.

Why are softgels gaining share over capsules?

Softgels improve absorption of lipophilic actives like EPA and CoQ10, enabling lower doses and better compliance, which drives a 10.76% CAGR for the format.

Which region will deliver the highest growth rate?

Asia-Pacific is forecast to post a 9.54% CAGR due to Healthy China 2030 initiatives, aging populations, and strong e-commerce uptake.

How are online channels affecting market dynamics?

E-commerce subscriptions reduce nonadherence and boost personalized bundles, leading online sales to grow at an 11.65% CAGR through 2031.

What major restraint could limit market expansion?

Divergent global regulations and inconsistent labeling standards raise compliance costs and slow new-product rollouts, subtracting roughly 0.8 percentage points from the forecast CAGR.

Page last updated on: