Sports Supplement Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

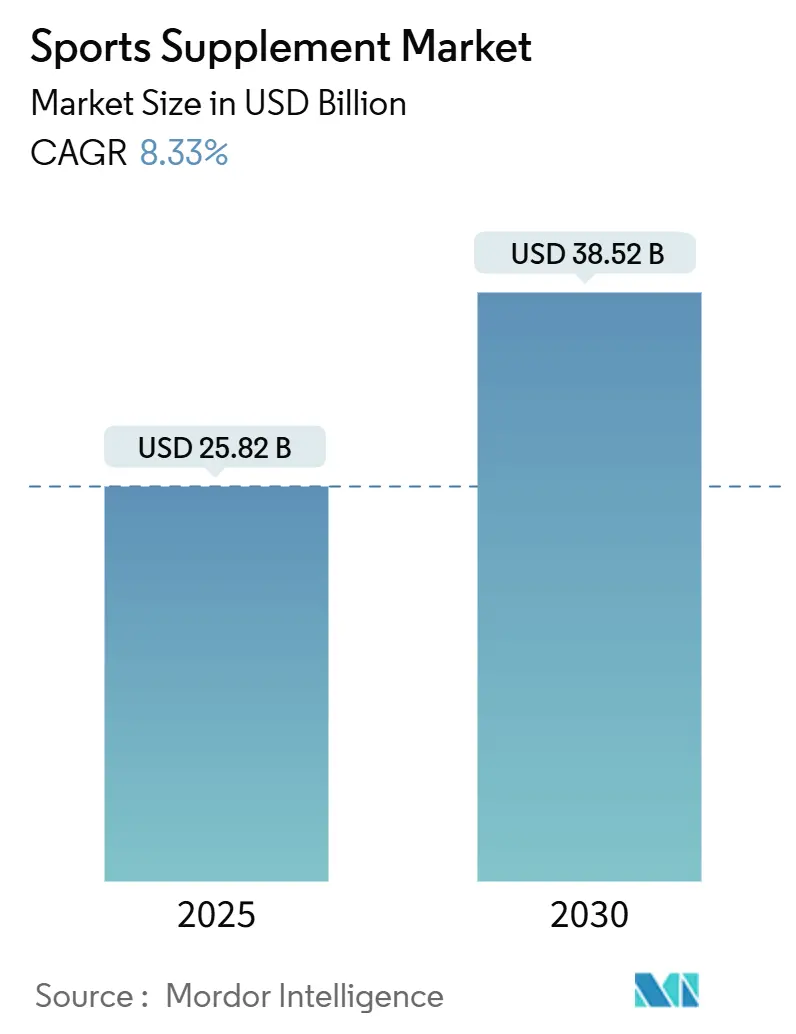

| Market Size (2025) | USD 25.82 Billion |

| Market Size (2030) | USD 38.52 Billion |

| Growth Rate (2025 - 2030) | 8.33% CAGR |

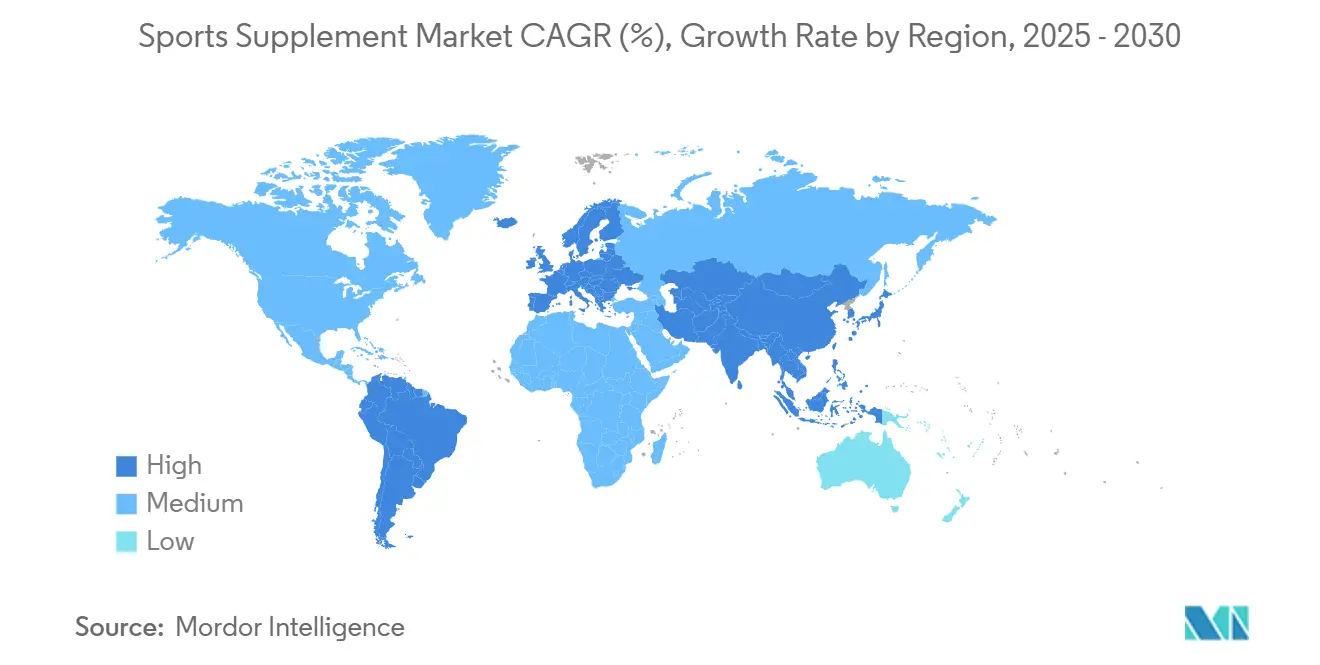

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sports Supplement Market Analysis by Mordor Intelligence

The sports supplement market size reached USD 25.82 billion in 2025 and is projected to climb to USD 38.52 billion by 2030, expanding at an 8.33% CAGR over the forecast period. This growth is attributed to increasing fitness adoption, scientific support for plant-based proteins, and the growing role of digital commerce driven by influencers. The shift toward natural, organic, and plant-based ingredients is appealing to health-conscious consumers. Enhanced regulations and quality certifications are strengthening consumer confidence and driving market expansion. Furthermore, advancements in precision nutrition, which incorporate biomarker data into product formulations, are enabling the development of premium product tiers. North America, supported by high disposable incomes and a mature gym culture, holds the largest share of the sports supplement market. On the other hand, the Asia-Pacific region is experiencing the fastest growth, fueled by urban millennials focusing their discretionary spending on wellness. The competitive landscape is moderately intense; global players prioritize ingredient innovation and acquisitions, while digital-native disruptors capitalize on direct-to-consumer models to capture niche markets.

Key Report Takeaways

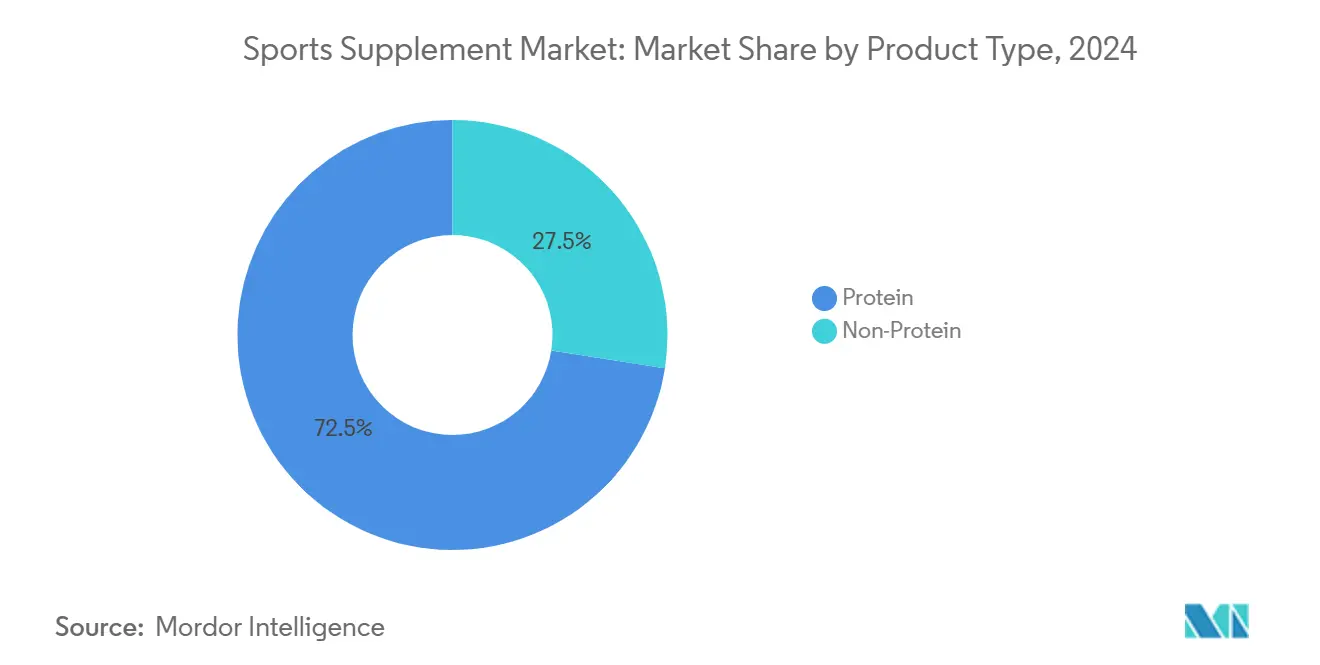

- By product type, protein supplements held 72.53% of sports supplement market share in 2024; non-protein products are forecast to accelerate at a 9.80% CAGR through 2030.

- By source, animal-based offerings captured 68.94% of the sports supplement market size in 2024, while plant-based formats are projected to advance at a 9.23% CAGR to 2030.

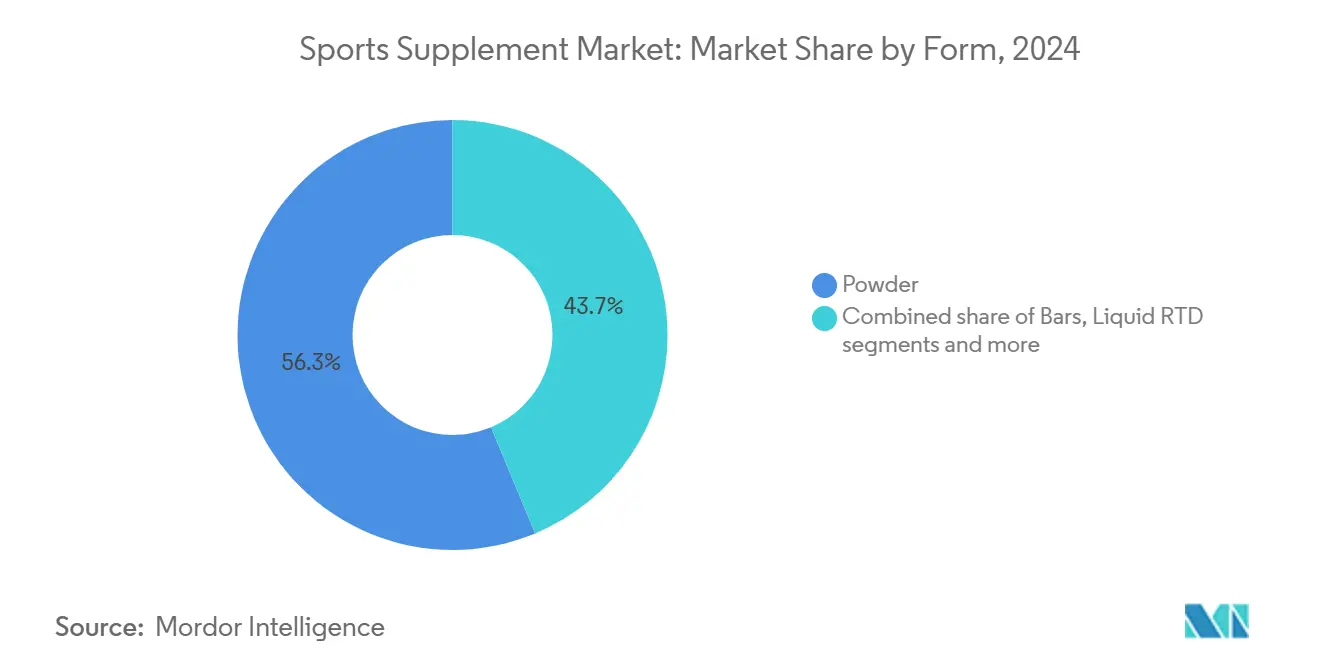

- By form, powder formulations led with 56.28% revenue share in 2024; liquid RTD lines are expected to post the highest 8.96% CAGR over 2025-2030.

- By distribution channel, supermarkets and hypermarkets accounted for 42.71% of 2024 sales, whereas online retail is slated to expand at a 10.18% CAGR during the forecast period.

- By geography, North America contributed 38.26% of global 2024 sales; Asia-Pacific is anticipated to grow the fastest at a 9.56% CAGR through 2030.

Global Sports Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fitness club and gym membership boom | +1.8% | Global; strongest in North America and urban Asia-Pacific | Medium term (2-4 years) |

| Rising plant-based protein popularity | +1.5% | Global; early uptake in North America and Europe | Long term (≥ 4 years) |

| Increasing health and fitness awareness | +2.1% | Global; peak in developed markets | Long term (≥ 4 years) |

| Influence of social media and fitness influencers | +1.9% | Global; deepest impact in North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Scientific advances and product innovations | +1.2% | Global; North America and Europe | Medium term (2-4 years) |

| Personalized biomarker-driven protein mixes | +0.8% | North America, Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fitness club and gym membership boom

The democratization of fitness culture has widened the use of sports supplements, expanding their appeal from elite athletes to everyday fitness enthusiasts. As gym memberships rise, more individuals are turning to supplements—such as protein powders, pre-workouts, BCAAs, and recovery drinks—to boost physical performance and support muscle growth. In 2024, 77 million Americans, representing 25% of those aged six and older, were members of gyms, studios, or other fitness facilities, according to the Health and Fitness Association (HFA)[1]Source: Health and Fitness Association, "One in Four Americans Belonged to a Gym in 2024", www.healthandfitness.org. Including both members and non-members, the total number of fitness facility users reached nearly 96 million, equating to approximately one in three Americans (31.0%). The increase in fitness club memberships has directly driven the adoption of supplements, as gym environments promote performance nutrition and validate product effectiveness. This trend has particularly benefited the protein powder and pre-workout segments, which align with the resistance training routines increasingly favored by recreational users. Additionally, the growing popularity of functional fitness and high-intensity interval training has heightened demand for recovery-focused supplements, such as branched-chain amino acids and creatine formulations, designed for non-competitive athletes seeking to enhance performance. Regular gym-goers often incorporate sports supplements into their routines, sustaining demand and driving market growth.

Rising plant-based protein popularity

The efficacy of plant-based protein supplements demonstrates that they can achieve muscle protein synthesis rates comparable to whey protein when formulated appropriately. The FDA's GRAS (Generally Recognized as Safe) notifications for innovative plant proteins, including pea, rice, and hemp, have significantly expanded the range of formulation possibilities. In 2024, Americans spent USD 8.1 billion on plant-based foods, with USD 450 million allocated to protein liquids and powders, according to the Good Food Institute[2]Source: Good Food Institute, "U.S. retail market insights for the plant-based industry", www.gfi.org. Additionally, advancements in precision fermentation technologies now allow for the production of complete amino acid profiles, which were previously attainable only through animal-based sources. This growing trend is not limited to vegan consumers but also appeals to flexitarians and environmentally conscious athletes, driving market growth by creating new demand rather than merely replacing existing products. Moreover, regulatory compliance frameworks, such as the ISO 14001 environmental management standards, are increasingly influencing procurement strategies among institutional buyers, including sports teams and corporate wellness programs, further shaping the market landscape.

Influence of social media and fitness influencers

Fitness influencers, through their personal endorsements and visible results, connect with followers more genuinely than traditional advertisements. This connection builds stronger trust and increases the likelihood of followers trying the recommended supplements. However, the impact of these influencers stems from complex factors such as source credibility, physical appeal, and content quality, rather than simple celebrity endorsements. Their content educates large audiences on the benefits of nutrition, exercise, and supplements, encouraging broader participation in physical activities and supplement usage. In 2024, the International Telecommunication Union reported that global internet users reached 5.5 billion[3]Source: International Telecommunication Union, "Internet use", www.itu.int, highlighting the significant internet penetration driving social media engagement. Nevertheless, the transient nature of social media content complicates regulatory oversight, as traditional advertising standards struggle to address platforms like Instagram Stories and TikTok promotions. Recognizing the higher return on investment, companies are increasingly directing their marketing budgets toward creator partnerships, shifting away from conventional advertising methods.

Scientific advances and product innovations

Advancements in nutritional science have led to formulations featuring optimized protein blends, bioavailable ingredients, and targeted amino acid ratios, which significantly enhance muscle recovery, endurance, and performance. Brands are utilizing AI, machine learning, and DNA testing to develop nutrition plans and supplements tailored to individual genetics, metabolism, and fitness goals. This personalized approach strengthens consumer trust and adherence. Precision nutrition is driving innovation in the sports supplement market, with biomarker-driven formulations enabling customized protein and micronutrient recommendations based on unique metabolic profiles. Key developments include FrieslandCampina's fermented gut-muscle axis solution, designed to modulate the microbiome for improved muscle function, and Vitamin Shoppe's NovaQSpheres encapsulation technology, which enhances creatine stability and bioavailability. Additionally, AI applications in supplement personalization analyze genetic polymorphisms to predict individual responses to creatine supplementation. Clinical evidence highlights that genetic profiles significantly influence muscle mass gains and injury prevention outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying global regulatory scrutiny | -1.4% | Global; strictest in EU, rising in Asia-Pacific | Medium term (2-4 years) |

| Ultra-processed food backlash | -0.9% | North America, Europe | Long term (≥ 4 years) |

| Side effects and health risks | -0.7% | Global; amplified in developed markets | Short term (≤ 2 years) |

| High cost and affordability concerns | -1.1% | Emerging Asia-Pacific, Latin America, Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying global regulatory scrutiny

Regulatory authorities across the globe are increasingly intensifying their oversight of sports supplements. The European Food Safety Authority has imposed restrictions on 117 substances and updated its guidance to ensure more rigorous substantiation of health claims. In Canada, Health Canada's supplemented foods regulations now require novel food assessments for innovative ingredients. While these regulations create compliance challenges for emerging formulations, they are expected to enhance product safety and efficacy standards. Similarly, the FDA continues to enforce GRAS (Generally Recognized as Safe) notification requirements for novel proteins and functional ingredients. Although this enforcement increases development costs for manufacturers, it significantly enhances the credibility of products in the market. These evolving regulatory frameworks provide an advantage to established manufacturers with well-developed compliance infrastructures, while simultaneously creating significant barriers for smaller players who may lack the necessary regulatory expertise.

Ultra-processed food backlash

Consumers are becoming increasingly skeptical of ultra-processed foods, and this sentiment is now extending to sports supplements. Concerns about artificial additives, excessive processing, and a shift away from whole food-based nutrition are driving this trend. Ready-to-drink formulations and highly processed protein bars are particularly impacted, creating significant opportunities for minimally processed alternatives and products with clean-label positioning. Health experts are actively challenging the generalized health claims promoted by non-expert influencers, which could lead to a decline in consumer trust toward supplement marketing. In response, companies are implementing measures to enhance transparency, such as obtaining third-party testing certifications, providing detailed ingredient sourcing disclosures, and showcasing their commitment to product integrity and ethical manufacturing practices.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Protein Segments Drive Innovation

Protein supplements hold a commanding market share of 72.53% in 2024, highlighting their widespread consumer acceptance and well-documented effectiveness in supporting muscle protein synthesis and recovery. This dominance reflects their established role in fitness and health regimens. However, non-protein categories are experiencing a faster growth trajectory, with a strong compound annual growth rate (CAGR) of 9.80% anticipated through 2030. This growth is primarily driven by the increasing mainstream adoption of creatine, which was previously limited to elite athletic circles. Creatine monohydrate, in particular, has seen significant revenue growth on a global scale. The U.S. market is a key contributor to this trend, as creatine usage expands to include women, older adults, and applications targeting cognitive health. Within the protein segment, whey and casein proteins continue to lead in technical performance for muscle synthesis. However, plant-based protein alternatives, when formulated with complete amino acid profiles, are demonstrating comparable efficacy, making them a viable option for consumers seeking non-animal-based solutions.

BCAA supplements are encountering market saturation as scientific research increasingly supports the use of complete protein sources over isolated amino acids for achieving optimal training adaptations. Creatine, on the other hand, benefits from its FDA GRAS-approved status (GRN No. 931) and an extensive safety record supported by over 680 clinical trials, positioning it for sustained growth in the functional foods and beverages market. The product landscape is evolving with the introduction of diverse formats, including ready-to-drink (RTD) creatine beverages, gummies, and encapsulated beadlets. These innovations address consumer preferences for improved palatability and convenience, which have historically been barriers to broader adoption. This diversification is expected to further drive creatine's market penetration and appeal across various consumer demographics.

By Source: Plant-based Acceleration Challenges Animal Dominance

Animal-based supplements hold a 68.94% market share in 2024, driven by their superior amino acid profiles and consumers' long-standing preference for whey protein. These animal proteins provide essential amino acids and bioactive compounds, offering health benefits such as joint and skin support through collagen. On the other hand, plant-based supplements are experiencing significant growth, with a 9.23% CAGR projected through 2030. This growth is supported by clinical evidence indicating that plant proteins, when formulated with adequate leucine and essential amino acid ratios, can achieve muscle protein synthesis comparable to animal proteins. Additionally, the FDA's GRAS notifications have expanded the range of plant proteins beyond traditional soy and pea to include hemp, rice, and precision-fermented options.

Vegan and vegetarian consumers, due to lower baseline tissue levels from dietary restrictions, show greater performance improvements from creatine supplementation, creating targeted market opportunities. While plant-based proteins require 20-75% higher intake volumes to match the amino acid delivery of animal sources, this challenge also opens opportunities for premium pricing on concentrated formulations. Environmental sustainability concerns are increasingly influencing younger demographics, with ISO 14001 environmental management compliance emerging as a competitive advantage for institutional buyers.

By Form: Liquid RTD Convenience Drives Format Evolution

Powder formulations hold a leading 56.28% market share in 2024, driven by cost efficiency, dosing flexibility, and established consumer habits stemming from traditional protein powder usage. Their adaptability allows seamless incorporation into smoothies, shakes, and various recipes, meeting diverse consumption preferences. Readily available in gyms, specialty stores, supermarkets, and online platforms, powders cater to a wide consumer base. Meanwhile, Liquid RTD products are experiencing a strong growth rate of 8.96% CAGR through 2030, propelled by convenience trends and advancements in formulation stability that address previous taste and texture challenges.

Capsules and tablets fulfill niche demands by delivering concentrated ingredients like creatine and BCAA, particularly where powder palatability limits adoption. The shift of protein bars towards clean-label formulations not only mitigates concerns about ultra-processed foods but also strengthens their appeal for on-the-go consumers. Emerging formats, such as creatine gummies and effervescent tablets, provide alternatives for those moving away from traditional powder mixing. Technologies like NovaQSpheres encapsulation is improving ingredient stability and bioavailability.

By Distribution Channel: E-commerce Disrupts Traditional Retail

Supermarkets and hypermarkets hold the largest distribution share at 42.71% in 2024, leveraging their wide consumer reach and the appeal of impulse purchases, particularly for mainstream protein and energy products. On the other hand, online retail is experiencing the fastest growth, with a strong 10.18% CAGR projected through 2030. This growth is fueled by subscription models, personalized recommendations, and direct-to-consumer strategies that bypass traditional retail margins. E-commerce platforms are also enabling the discovery of niche products, such as nootropics and customized formulations designed for specific training protocols or dietary requirements.

Specialty stores, while facing competition from online alternatives, remain relevant by offering expert consultations and product education—services that online platforms find difficult to replicate. The market is increasingly adopting an omnichannel approach, with brands maintaining partnerships with specialty retailers while enhancing their direct-to-consumer capabilities, particularly for premium products and subscription services. Additionally, social commerce is gaining traction, with influencer collaborations playing a key role. Platforms like Instagram and TikTok now feature embedded shopping tools that simplify the transition from product discovery to purchase, driving immediate conversion rates.

Geography Analysis

North America holds a significant 38.26% market share in 2024, driven by its deeply ingrained fitness culture, high levels of disposable income, and regulatory frameworks that actively promote product innovation and facilitate market entry. The region benefits from concentrated research and development activities, which allow major ingredient suppliers and product manufacturers to capitalize on their proximity to leading academic and clinical research institutions. Although the FDA's GRAS (Generally Recognized as Safe) notification process increases compliance costs for companies, it simultaneously strengthens the competitive positioning of established players by ensuring product safety and fostering consumer confidence in the market.

Asia-Pacific is anticipated to be the fastest-growing region, with a robust projected CAGR of 9.56% through 2030. This rapid growth is attributed to the expansion of the middle-class population, accelerated urbanization, and the increasing adoption of fitness-oriented lifestyles in major metropolitan areas. The region's high energy drink consumption reflects a strong growth potential for caffeinated performance products, which are gaining popularity among consumers. For instance, THG's strategic partnership with South Korea's CJ Corporation in August 2025 exemplifies efforts to expand internationally by aligning with local market preferences and leveraging established distribution networks. However, while ASEAN's regulatory harmonization efforts simplify the process of regional product registrations, the specific compliance requirements of individual countries continue to add layers of complexity to the overall regulatory landscape.

Europe's growth remains stable, supported by stringent regulatory standards that enhance consumer trust and create significant barriers for low-quality competitors attempting to enter the market. The EFSA's (European Food Safety Authority) regulations on health claims and novel food requirements prioritize scientifically validated formulations, aligning with the growing consumer demand for evidence-based nutritional products. Additionally, Europe's strong focus on environmental sustainability is driving increased demand for plant-based and sustainably sourced ingredients. Compliance with ISO 14001 standards is becoming a critical factor in procurement decisions, particularly among institutional buyers such as professional sports teams and corporate wellness programs, who are increasingly prioritizing environmentally responsible sourcing practices.

Competitive Landscape

The sports supplement market exhibits moderate concentration with established multinational players. These companies leverage vertical integration, advanced research capabilities, and extensive distribution networks to maintain their competitive advantage. The competitive landscape is increasingly shaped by strategic partnerships. For instance, in September 2024, C4 Energy collaborated with Hershey to launch flavored protein powders and energy drinks that combine performance nutrition with the familiar and appealing flavors of popular confectionery products. The market is witnessing a shift towards personalized nutrition, with companies heavily investing in biomarker-driven formulations and genetic testing services. These innovations aim to differentiate their offerings from standard protein and creatine products, providing a unique value proposition to consumers.

Emerging players are disrupting the market by adopting direct-to-consumer business models and developing specialized formulations that cater to underserved demographics. These include women-specific products, vegan alternatives, and supplements designed for cognitive enhancement. Although private label brands are gaining traction, they still represent a relatively small portion of the overall market, primarily targeting cost-conscious consumers. Athletes and bodybuilders continue to be the primary end users of sports supplements. However, there is a growing demand among lifestyle users, particularly younger consumers and women, who represent a rapidly expanding target audience. Prominent companies operating in this market include Glanbia Plc, Abbott Laboratories, PepsiCo Inc., Nestlé S.A., and Otsuka Pharmaceutical, among others.

Technological advancements are driving significant changes in the market, enabling the introduction of subscription-based services, personalized product recommendations, and social commerce functionalities. These innovations provide a competitive edge over traditional retail-focused competitors. As regulatory scrutiny intensifies and consumer awareness of contamination risks grows, especially concerning banned substances and mislabeling in unregulated products, quality assurance and third-party testing have become critical differentiators. Key areas of competition include branding and sponsorships with sports celebrities and teams, product innovation such as plant-based supplements, gummies, and personalized nutrition solutions, as well as robust online sales strategies and social media marketing efforts.

Sports Supplement Industry Leaders

-

Glanbia Plc

-

Abbott Laboratories

-

PepsiCo Inc.

-

Nestlé S.A.

-

Otsuka Pharmaceutical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: THG has formed a strategic partnership with CJ Corporation to expand the distribution of sports nutrition products in South Korea. This partnership leverages CJ's expertise in the local market and its robust retail networks, facilitating the international growth of THG's brands in the region.

- January 2025: Ferrero has broadened its confectionery portfolio by acquiring the Power Crunch protein bar brand, targeting the increasing demand from health-conscious consumers in the functional nutrition category.

- January 2025: The Vitamin Shoppe introduced BodyTech Elite Creatine Beadlets, an innovative supplement featuring Specnova's NovaQSpheres multi-layer encapsulation technology. This technology addresses longstanding challenges with creatine's taste and stability while enhancing bioavailability through advanced delivery systems.

- October 2024: Nutrabolt has expanded its C4 Energy collaboration with The Hershey Company by launching C4 Whey Protein powders in Hershey's milk chocolate and Reese's peanut butter flavors. The company has also introduced C4 Performance Energy drinks in Jolly Rancher varieties, highlighting its successful brand extension strategies.

Global Sports Supplement Market Report Scope

| Protein | Whey and Casein |

| Plant-Based | |

| Others | |

| Non- Protein | BCAA |

| Creatine | |

| Others |

| Animal-based |

| Plant-based |

| Powder |

| Bars |

| Liquid RTD |

| Capsules/Tablets |

| Others |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Protein | Whey and Casein |

| Plant-Based | ||

| Others | ||

| Non- Protein | BCAA | |

| Creatine | ||

| Others | ||

| By Source | Animal-based | |

| Plant-based | ||

| By Form | Powder | |

| Bars | ||

| Liquid RTD | ||

| Capsules/Tablets | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the sports supplement market by 2030?

The sector is expected to reach USD 38.52 billion by 2030, reflecting an 8.33% CAGR from its 2025 base.

Which product type currently leads global sales?

Protein supplements, including whey and casein powders, commanded 72.53% of 2024 revenue.

Which region shows the fastest sales growth?

Asia-Pacific is on track for a 9.56% CAGR, fueled by urban fitness adoption and rising disposable income.

Which distribution channel is growing most quickly?

Online retail is set to expand at a 10.18% CAGR as subscriptions and social commerce gain traction.

Page last updated on: