Multivitamin And Mineral Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

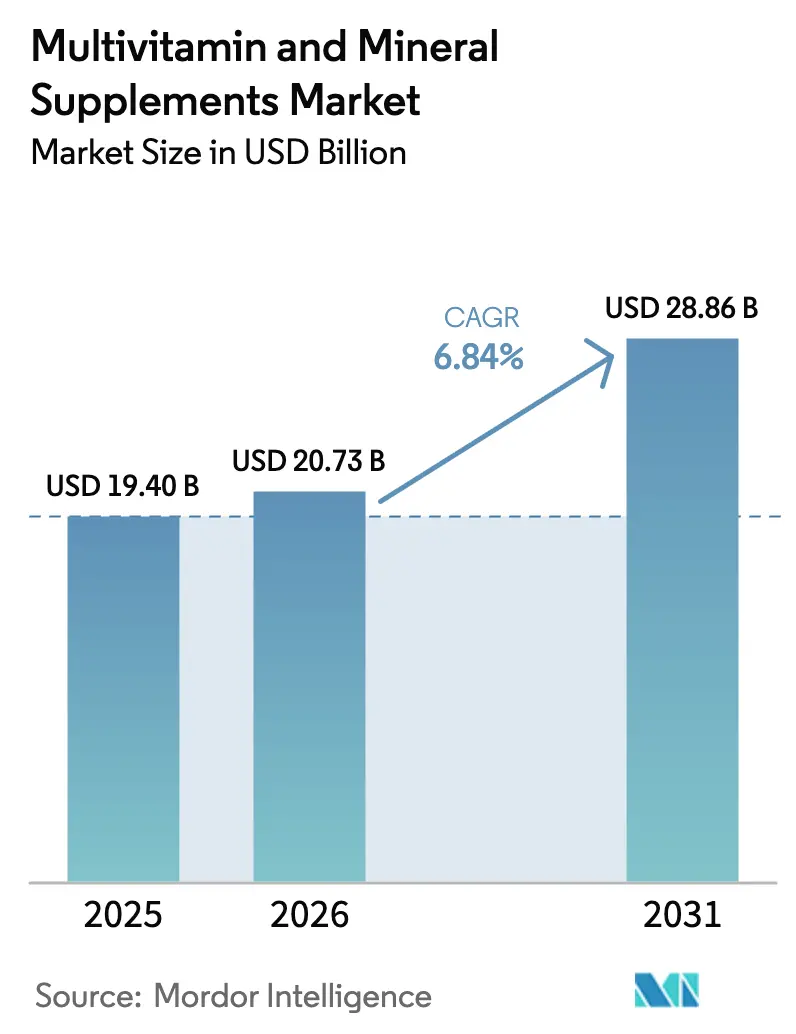

| Market Size (2026) | USD 20.73 Billion |

| Market Size (2031) | USD 28.86 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

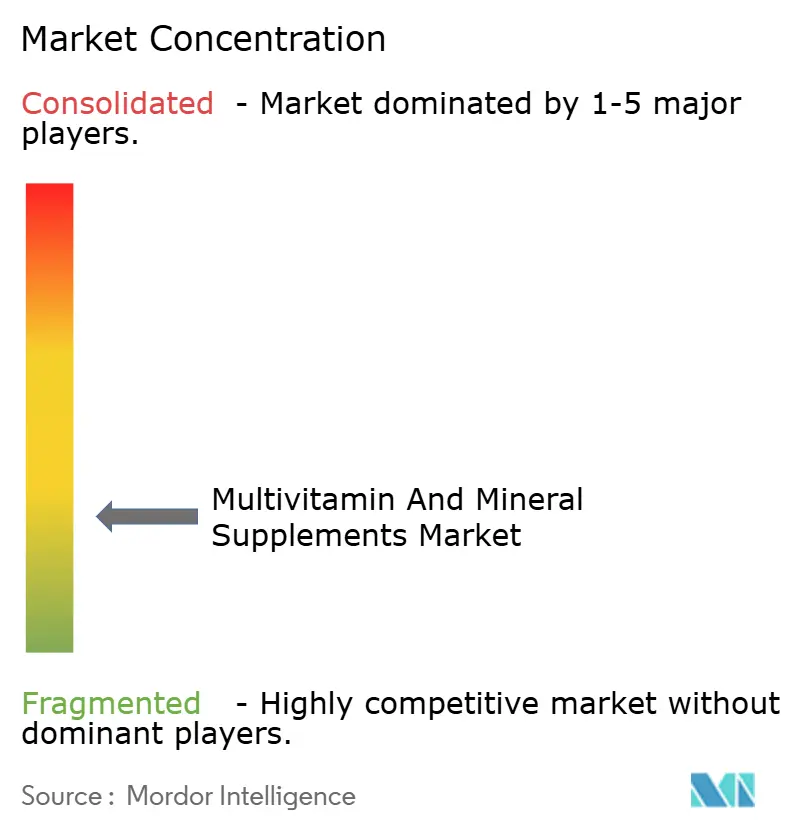

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Multivitamin And Mineral Supplements Market Analysis by Mordor Intelligence

The multivitamin and mineral supplements market size in 2026 is estimated at USD 20.73 billion, growing from 2025 value of USD 19.40 billion with 2031 projections showing USD 28.86 billion, growing at 6.84% CAGR over 2026-2031. Robust growth reflects rising lifestyle-related diseases, advancing product innovation, and widening preventive-health awareness that reposition supplements as everyday essentials instead of discretionary items. For instance, according to the Council for Responsible Nutrition, in 2023, 74% of the adult population in the United States took dietary supplements [1]Source: Council for Responsible Nutrition, "2023 CRN Consumer Survey on Dietary Supplements", crnusa.org. Market resilience is reinforced by diversified positioning across immune health, cognitive support, beauty, and active-aging needs, allowing revenue streams to balance economic swings. Digital retail acceleration and subscription models deepen consumer engagement, while regulatory standardization trims compliance complexity, encouraging product rollouts across regions. Manufacturers harness differentiated delivery formats along with personalized nutrition platforms to secure repeat purchase behavior and protect margins.

Key Report Takeaways

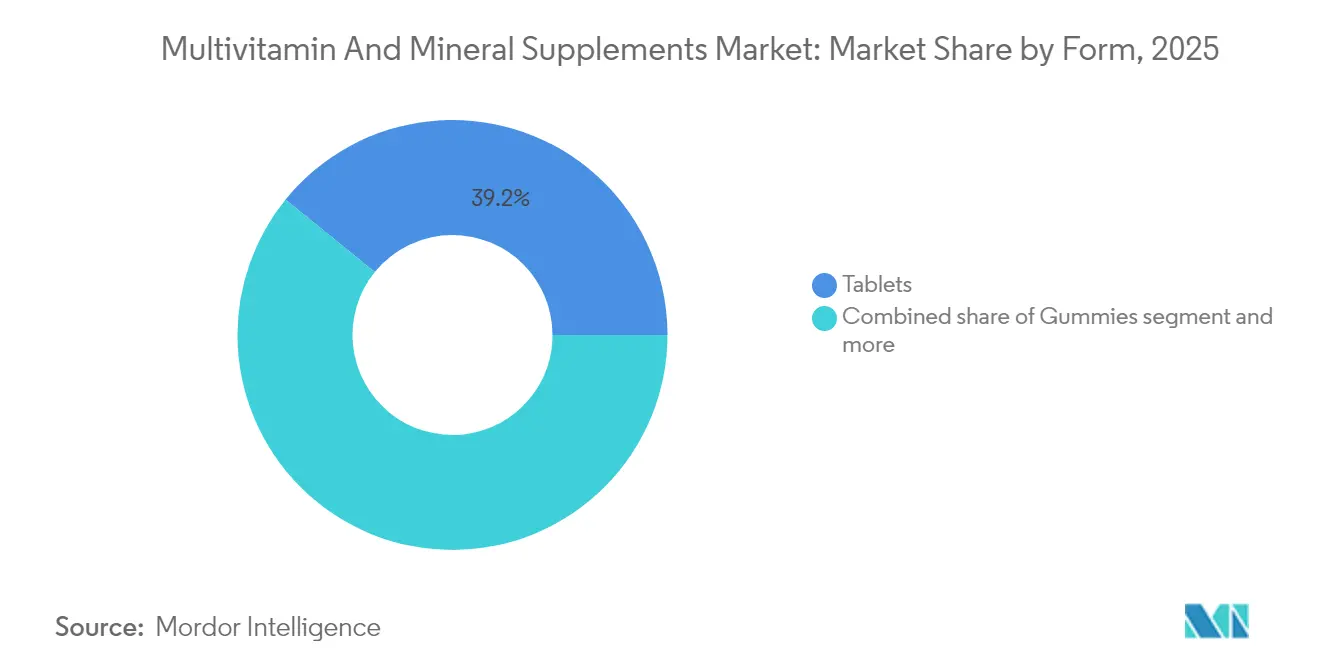

- By form, tablets captured 39.15% of the multivitamin and mineral supplements market share in 2025, while gummies are forecast to post the quickest expansion at a 7.58% CAGR through 2031.

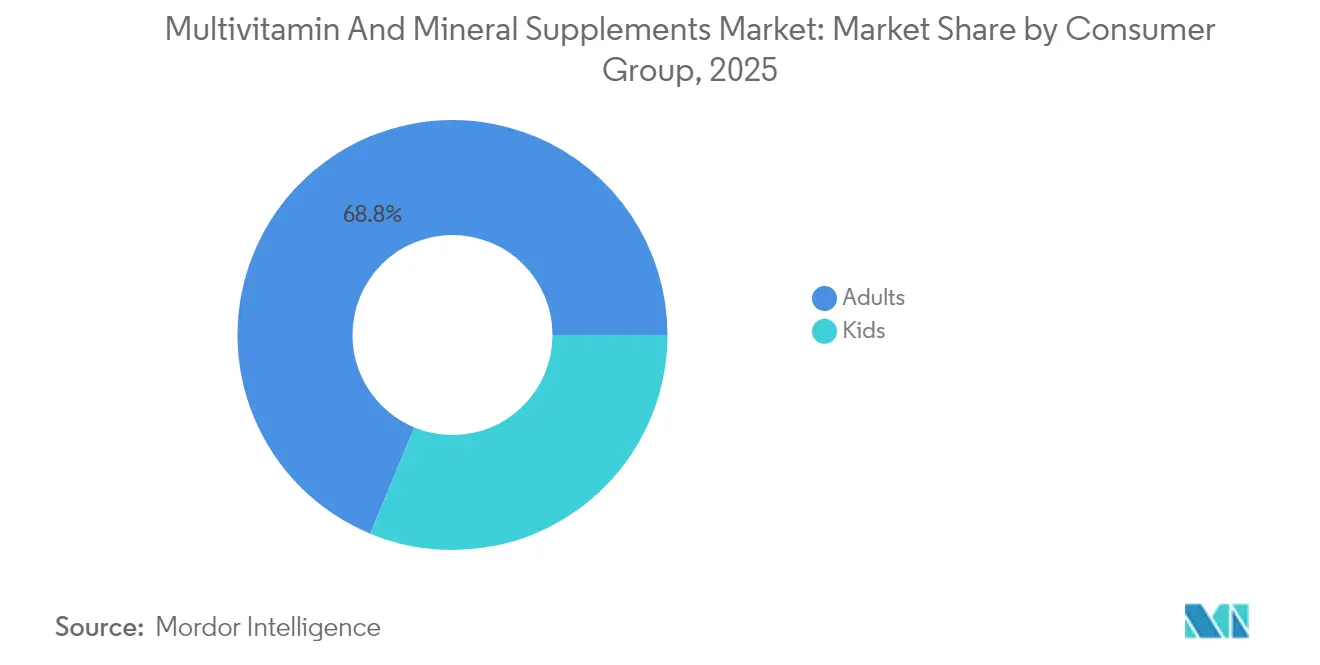

- By consumer group, adults held 68.75% of the multivitamin and mineral supplements market size in 2025, yet the kids segment is advancing at an 7.86% CAGR to 2031.

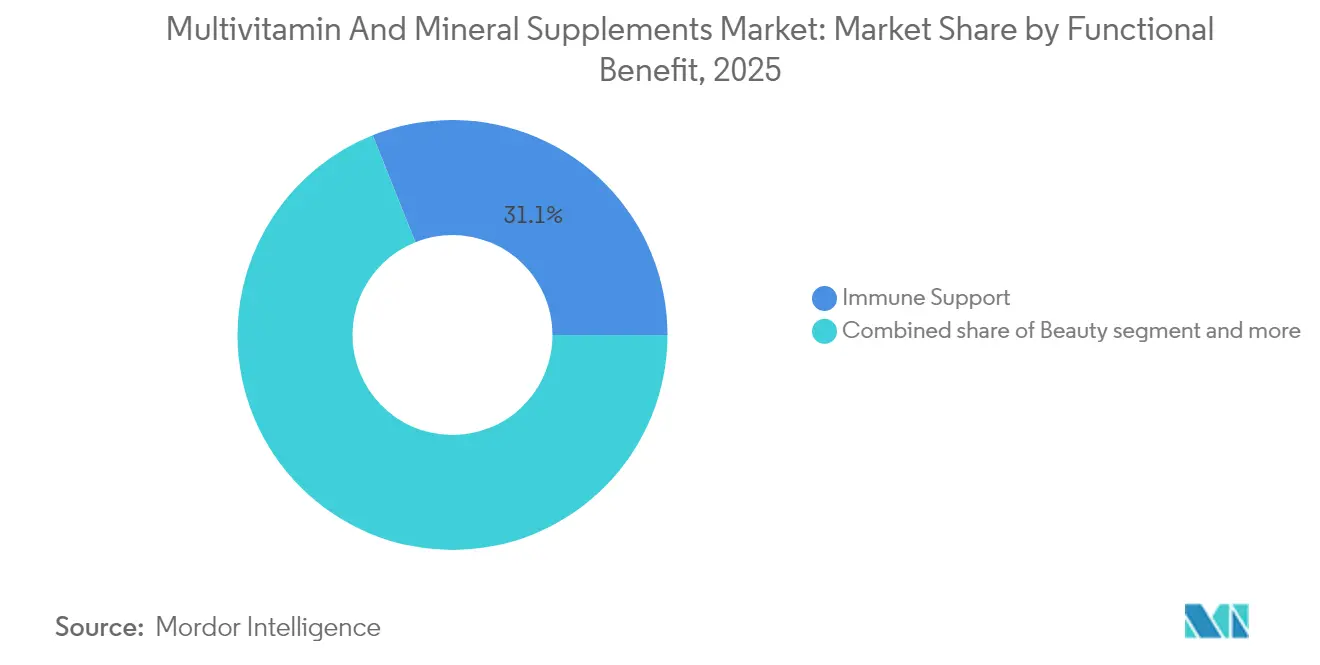

- By functional benefit, immune support led with 31.05% of 2025 revenues; beauty-focused products are projected to climb at an 8.02% CAGR during the same horizon.

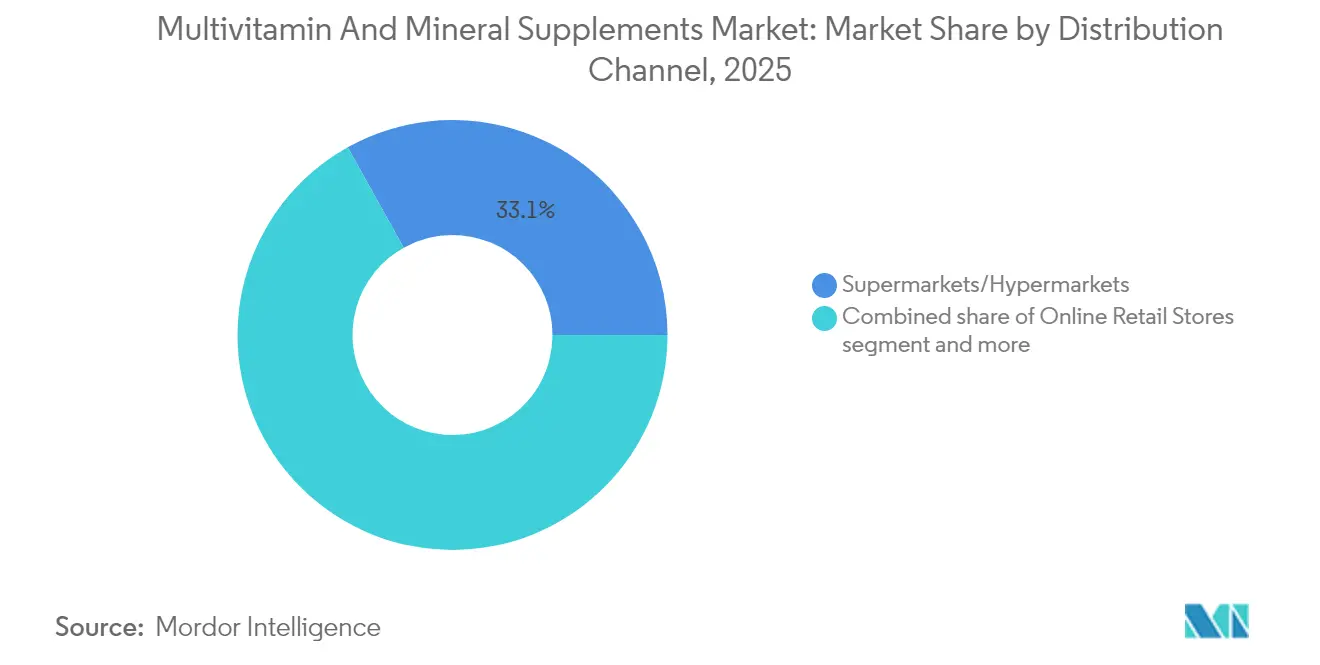

- By distribution channel, supermarkets and hypermarkets accounted for 33.10% of sales in 2025, whereas online retail is expanding at a 10.08% CAGR on the back of data-driven personalization.

- By geography, North America commanded 37.05% revenue share in 2025; Asia-Pacific is poised to rise at a 9.22% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Multivitamin And Mineral Supplements Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of lifestyle-related health issues | +1.2% | Global, with the highest impact in North America and Europe | Medium term (2-4 years) |

| Aging population and elderly health concerns | +0.8% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Innovation in product formulation and delivery | +1.1% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Emphasis on preventive healthcare | +0.9% | Global, accelerating in Asia-Pacific | Medium term (2-4 years) |

| Regulatory support and standardization | +0.7% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Marketing strategies and brand influence | +0.6% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of lifestyle-related health issues

Lifestyle-related health conditions are fundamentally reshaping supplement consumption patterns as consumers seek proactive nutritional interventions. This trend extends beyond basic nutrition gaps to targeted therapeutic applications, where specific vitamin and mineral combinations address metabolic dysfunction, cardiovascular risk, and inflammatory conditions. For instance, according to the Ministry of National Development Planning, Republic of Indonesia (BAPPENAS), the number of patients suffering from heart diseases in Indonesia reached about six million in 2024 [2]Source: Ministry of National Development Planning, Republic of Indonesia (BAPPENAS), "The Consolidated Report on Indonesia's Health Sector", unicef.org. The shift from treatment-focused to prevention-oriented healthcare spending creates sustained demand for supplements that can demonstrate measurable health outcomes. Post-pandemic consumer behavior studies indicate a permanent elevation in health consciousness, with individuals viewing supplements as insurance against lifestyle-induced health deterioration rather than optional wellness products.

Aging population and elderly health concerns

Demographic aging patterns are creating sustained demand for age-specific nutritional formulations, as older adults represent the highest supplement usage cohort. For instance, according to the ChildStats, Forum on Child and Family Statistics, in 2023, about 17.7% of the American population was 65 years old or over; an increase from the last few years and a figure which is expected to reach 22.8% by 2050 [3]Source: ChildStats, Forum on Child and Family Statistics, "POP2 Children as a percentage of the population", childstats.gov. The Administration for Community Living emphasizes that older adults face unique challenges in obtaining adequate nutrients due to dietary restrictions and health conditions, creating a specialized market for senior-focused formulations. This demographic shift drives innovation in bioavailability enhancement, as aging bodies require more efficient nutrient absorption mechanisms. The economic impact extends beyond individual purchases to healthcare cost reduction, as preventive nutrition can delay or reduce the severity of age-related conditions. Companies are responding with targeted products addressing bone health, cognitive function, and immune system support, specifically designed for geriatric populations.

Innovation in product formulation and delivery

Technological advancement in supplement delivery systems is transforming consumer acceptance and market penetration rates across demographic segments. The global gummy market is driven by innovations in reduced-sugar and vegan formulations that maintain nutritional integrity. Patent activity in vitamin formulation technology shows an industry focus on bioavailability enhancement, with water-soluble vitamin E derivatives and nanoparticle-based delivery systems aimed at improving absorption rates. Personalized nutrition platforms are leveraging genomic data and microbiome analysis to create customized formulations, shifting the market from mass production to on-demand manufacturing. These innovations address traditional barriers to supplement adoption, including taste preferences, swallowing difficulties, and dosing convenience, expanding the addressable market beyond traditional health-conscious consumers.

Emphasis on preventive healthcare

Healthcare cost inflation and system strain are driving institutional and individual investment in preventive nutrition strategies that reduce long-term medical expenses. According to the Health System Tracker, in June 2023, the cost of inpatient hospital services in the United States had increased by 3.7% in comparison to June 2022. The FAO's personalized nutrition guidelines emphasize the role of food supplements in preventing chronic diseases, particularly in populations with specific nutritional deficiencies. Government health agencies are increasingly recognizing supplements as cost-effective interventions for population health management, leading to policy support for targeted supplementation programs. Furthermore, healthcare providers are integrating nutritional assessments into routine care, creating clinical validation for supplement recommendations that strengthen consumer confidence. This shift from wellness luxury to healthcare necessity is supported by emerging research demonstrating measurable health outcomes from targeted supplementation programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns about side effects and safety | -0.4% | Global, most pronounced in developed markets | Short term (≤ 2 years) |

| Preference for natural foods | -0.3% | Global, stronger in Europe and North America | Medium term (2-4 years) |

| High cost of innovative products | -0.5% | Global, limiting access in emerging markets | Medium term (2-4 years) |

| Regulatory complexity across different regions | -0.2% | Global, affecting multinational operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Concerns about side effects and safety

Safety incidents and regulatory recalls are creating consumer skepticism that requires sustained industry investment in quality assurance and transparency. The FDA issued multiple recalls in 2024-2025 for supplements containing undeclared pharmaceutical ingredients, including sildenafil and tadalafil, in products marketed as dietary supplements. Nordic Naturals' voluntary recall of Baby's Vitamin D3 Liquid in 2024 due to elevated vitamin D3 levels demonstrates how manufacturing errors can affect even established brands, potentially causing health issues in vulnerable populations. International regulatory actions, including NAFDAC's 2025 alert regarding multivitamin supplements posing a risk of serious injury or death from poisoning, highlight the global nature of safety concerns. These incidents underscore the need for rigorous quality control systems and transparent supply chain management. Consumer surveys indicate that 82% of older adults want information on side effects, and 77% support government review of safety data before marketing, reflecting demand for enhanced regulatory oversight that may slow product launches and increase compliance costs.

High cost of innovative products

Premium pricing for advanced formulations and personalized nutrition solutions is limiting market penetration in price-sensitive segments and emerging economies. The vitamin industry's exposure to raw material price volatility, exemplified by DSM-Firmenich's challenges with unprecedentedly low vitamin prices affecting profitability, creates pressure to maintain margins through premium pricing strategies. Personalized nutrition platforms require significant technology investment and specialized manufacturing capabilities that translate to higher consumer prices, potentially excluding lower-income demographics from accessing optimized formulations. Merger and acquisition activity in the vitamins and supplements sector, with valuations averaging 11.2x EBITDA, reflects investor expectations for premium returns that may pressure companies to focus on high-margin products rather than accessible basic formulations. This pricing dynamic creates market bifurcation between premium wellness products and basic nutritional supplements, potentially limiting overall market expansion. Companies like Haleon are addressing this challenge by offering individual vitamin packs at affordable prices to increase penetration in lower-income demographics, recognizing that accessibility drives volume growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Gummies Drive Innovation Despite Tablet Dominance

Tablets maintain market leadership with 39.15% share in 2025, reflecting established manufacturing economies and consumer familiarity, while gummies emerge as the fastest-growing segment at 7.58% CAGR through 2031. The gummy segment's expansion is driven by technological innovations addressing traditional limitations, including reduced-sugar formulations using natural sweeteners and vegan alternatives to gelatin-based products. Capsules and softgels represent a mature segment focused on bioavailability optimization, particularly for fat-soluble vitamins and specialized delivery systems. Powders cater to specific demographics requiring flexible dosing or mixing capabilities, while other forms include innovative delivery mechanisms such as sublingual strips and effervescent tablets.

The form segmentation reflects broader consumer behavior shifts toward convenience and palatability, with gummies addressing traditional barriers to supplement adoption among children and adults with swallowing difficulties. Manufacturing advances in vitamin stability within gummy matrices, particularly for vitamin C encapsulation techniques, are extending shelf life and maintaining potency. Patent activity in water-soluble vitamin E derivatives for soft gel applications demonstrates ongoing innovation in traditional forms, suggesting that established segments are evolving rather than being displaced. The competitive dynamics favor companies that can offer multiple form factors within integrated product lines, enabling cross-selling and demographic expansion strategies.

By Consumer Group: Kids Segment Outpaces Adult Growth

Adults dominate consumption with 68.75% market share in 2025, driven by established health consciousness and disposable income, while the kids segment exhibits superior growth at 7.86% CAGR through 2031. This growth differential reflects parental prioritization of preventive nutrition for children, supported by pediatric health guidelines emphasizing early intervention for nutritional deficiencies. The adult segment encompasses diverse sub-demographics, from young professionals seeking energy and cognitive support to seniors requiring age-specific formulations for bone health and immune function. Kids' products require specialized formulations addressing taste preferences, appropriate dosing, and safety considerations for developing metabolisms.

Haleon's strategic focus on addressing nutritional deficiencies among Filipino children, where significant deficiencies in iron, folate, and vitamins are prevalent, demonstrates how companies are targeting underserved pediatric populations in emerging markets. The kids' segment benefits from regulatory support for targeted supplementation programs, particularly in regions with documented nutritional deficiencies. Product innovation in this segment focuses on delivery mechanisms that ensure compliance, including gummy formulations and flavoring systems that mask nutrient tastes. The demographic trend toward delayed parenthood and smaller family sizes is creating premium spending patterns where parents invest more per child in health and nutrition products.

By Functional Benefit: Beauty Supplements Emerge as Growth Driver

Immune support maintains the largest functional benefit share at 31.05% in 2025, reflecting sustained post-pandemic health consciousness, while beauty supplements surge at 8.02% CAGR through 2031 as consumers increasingly link internal nutrition to external appearance. Bone and joint health represents a stable segment driven by aging demographics and active lifestyle trends, while cognitive and mental health formulations address growing awareness of nutrition's role in neurological function. Other functional benefits include specialized applications such as sports nutrition, women's health, and digestive support that cater to specific consumer needs.

The beauty supplements surge reflects convergence between cosmetics and nutrition industries, with consumers seeking holistic approaches to skin, hair, and nail health that complement topical treatments. This trend is supported by clinical research demonstrating the efficacy of specific vitamin and mineral combinations for dermatological health, creating scientific validation for premium pricing. Immune support products experienced sustained demand following COVID-19, with research highlighting the immune-boosting roles of vitamins D, C, E, zinc, and selenium. The functional benefit segmentation enables targeted marketing strategies and specialized product development, allowing companies to command premium prices for condition-specific formulations. Cross-functional products that address multiple health concerns simultaneously are gaining traction, reflecting consumer preference for comprehensive wellness solutions.

By Distribution Channel: Online Retail Transforms Market Access

Supermarkets and hypermarkets preserved a 33.10% share in 2025, leveraging store traffic and in-aisle promotions to trigger spontaneous purchases. Pharmacies continue to command consumer confidence for medical-grade brands, aided by pharmacist recommendations. However, online retail accelerates at a 10.08% CAGR, expanding the multivitamin and mineral supplements market through data-driven segmentation and doorstep delivery. Direct-to-consumer sites mine purchase and lifestyle data to propose monthly subscription bundles, boosting retention. Virtual consultations with dietitians and AI chatbots enhance personalization, while same-day shipping removes convenience barriers.

Traditional retailers integrate QR-code access to detailed nutrient information on-shelf and deploy click-and-collect services to harmonize online research with offline pick-up. Cross-border e-commerce flows allow Asian consumers to buy U.S. formulations, bypassing local stock constraints, though parallel import regulation remains a watch point. As smartphone penetration deepens, apps featuring gamified compliance rewards foster habit formation, embedding daily supplementation into routine and expanding lifetime value per customer.

Geography Analysis

North America retains leadership with 37.05% of global sales in 2025, anchored by mature regulatory oversight under DSHEA and sophisticated consumer literacy on micronutrient science. High healthcare expenditure, coupled with employer-sponsored wellness programs, underpins consistent demand. Retailers range from drugstore chains to warehouse clubs, while online pure-plays exploit rapid fulfillment networks. Canadian and Mexican markets benefit from harmonized labeling frameworks, creating a contiguous North American trade corridor that streamlines cross-border inventory movement. The multivitamin and mineral supplements market size for the region is forecast to expand steadily, though growth moderates as penetration nears saturation.

Asia-Pacific registers the highest regional CAGR at 9.22% through 2031, driven by urbanization, rising disposable incomes, and progressive regulatory regimes. China, the second-largest health functional foods market, has nearly 17,000 approved products under its notification system, demonstrating regulatory maturity. Japan’s supplement landscape leverages Foods with Function Claims labeling to communicate benefits openly. India catalyzes volume through government nutrition programs targeting anemia and vitamin D deficiencies. South Korea’s super-premium VMS segment attracts multinational investments, evidenced by Haleon’s Centrum Wellness Packs launch. Regional heterogeneity mandates localized flavors, dosing norms, and cultural branding, but aggregate momentum positions Asia-Pacific as the primary incremental revenue engine.

Europe embodies a mature yet complex environment. The EU Food Supplements Directive sets foundational rules, but member-state implementation discrepancies prolong approval cycles and necessitate country-specific dossiers. Consumers prioritize clean-label, plant-based, and sustainably packaged products, prompting brands to certify supply chains and adopt recyclable materials. German, Italian, and Scandinavian markets emphasize organic sourcing, while Southern Europe leans toward Mediterranean diet supplementation. Sustainable packaging and carbon-neutral manufacturing resonate strongly, shaping procurement strategies. South America and the Middle East and Africa deliver mid-single-digit growth as urbanization amplifies health literacy. Regulatory gaps and lower purchasing power temper uptake, but regional e-commerce penetration is unlocking cross-border access to international brands, hinting at longer-term upside.

Competitive Landscape

The multivitamin and mineral supplements market features high fragmentation, with pharmaceutical majors, consumer-health conglomerates, and agile digital natives vying for shelf space and online attention. Top incumbents such as Bayer, Haleon, Abbott, and Nestlé leverage global manufacturing footprints and legacy brand equity to maintain core volume. However, vitamin price volatility, illustrated by DSM-Firmenich’s earnings pressure, accelerates operational overhauls aimed at boosting EBITDA through efficiency gains. Nestlé’s 2025 review of its vitamins portfolio signals strategic pruning or acquisition to optimize category position.

Consolidation picks up as investors pay an average of 11.2 times EBITDA for bolt-on deals, allowing buyers to integrate production capacity, broaden formulation libraries, and capture digital consumer data. Contract manufacturers such as SCN BestCo evaluate divestiture, offering entry points for private-equity roll-ups. Intellectual property around nanoparticle carriers and water-soluble derivatives becomes a critical moat, enabling premium SKUs that resist commoditization. Personalized nutrition start-ups deploy AI algorithms and subscription models to bypass traditional channels, forcing incumbents to invest in direct-to-consumer platforms and data analytics capabilities.

Strategic moves include Haleon addressing pediatric micronutrient gaps in Southeast Asia, Abbott scaling metabolic-support lines in North America, and Bayer introducing plant-based gummies to align with vegan trends. Digital marketing partnerships with healthcare influencers build authenticity while driving traffic to brand-owned storefronts. Supply-chain transparency programs, encompassing blockchain traceability and third-party potency testing, emerge as competitive differentiators, answering consumer calls for verified quality amid safety incident headlines.

Multivitamin And Mineral Supplements Industry Leaders

-

Haleon plc

-

Bayer AG

-

Pharmavite LLC

-

Amway Corp.

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: New Chapter introduced its first liquid multivitamin formulated for the whole family, delivering 22 essential vitamins and minerals, including fermented B vitamins, vitamins C and K, and superfoods like elderberry and grape seed. It supports heart, bone, brain health, immune function, and digestion. Available in Orange Mango and Mixed Berry flavors, it is vegan, gluten-free, and uses eco-friendly packaging.

- March 2025: Life Time launched NOURISH, a drinkable multivitamin and greens powder featuring 23 vitamins and minerals plus probiotics, digestive enzymes, ashwagandha, CoQ10, and antioxidants. Designed to enhance energy, immune support, focus, and gut health, it offers a robust foundational daily supplement with transparent, third-party tested ingredients.

- January 2025: Nature Made released an improved multivitamin tablet containing 23 key nutrients, including iron. It is designed to meet the general health needs of adults and is recognized for quality and affordability. This tablet supports daily wellness with science-backed nutrient levels and USP verification for potency.

- November 2024: Lily of the Desert introduced EcoSport, a hydration supplement with aloe vera, B vitamins, and potassium to support athletes and active individuals. EcoDrink Nutrient Support contains the patented Aloesorb technology for optimal nutrient absorption and comes in no-sugar, gluten-free, and caffeine-free formulations designed for on-the-go nutrition.

Global Multivitamin And Mineral Supplements Market Report Scope

| Tablets |

| Capsules and Softgels |

| Powders |

| Gummies |

| Others |

| Kids |

| Adults |

| Immune Support |

| Bone and Joint Health |

| Cognitive and Mental Health |

| Beauty |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Tablets | |

| Capsules and Softgels | ||

| Powders | ||

| Gummies | ||

| Others | ||

| By Consumer Group | Kids | |

| Adults | ||

| By Functional Benefit | Immune Support | |

| Bone and Joint Health | ||

| Cognitive and Mental Health | ||

| Beauty | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the multivitamin and mineral supplements market expected to grow by 2031?

The market is projected to expand from USD 20.73 billion in 2026 to USD 28.86 billion by 2031, delivering a 6.84% CAGR.

Which delivery format is gaining ground the quickest?

Gummies are advancing at a 7.58% CAGR, the fastest among all forms, boosted by reduced sugar and vegan innovations.

Why is Asia-Pacific considered the key growth region?

Rising disposable incomes, regulatory modernization, and urban health awareness are pushing the region to a 9.22% CAGR, the highest globally.

Which consumer cohort drives the highest incremental demand?

Kid’s products are expanding at an 7.86% CAGR as parents prioritize preventive nutrition for growth and immunity.

What factors most restrain category expansion?

Safety-related recalls, premium pricing of personalized formats, and regulatory complexity in multi-country operations temper growth momentum.

Page last updated on: