United States Dietary Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

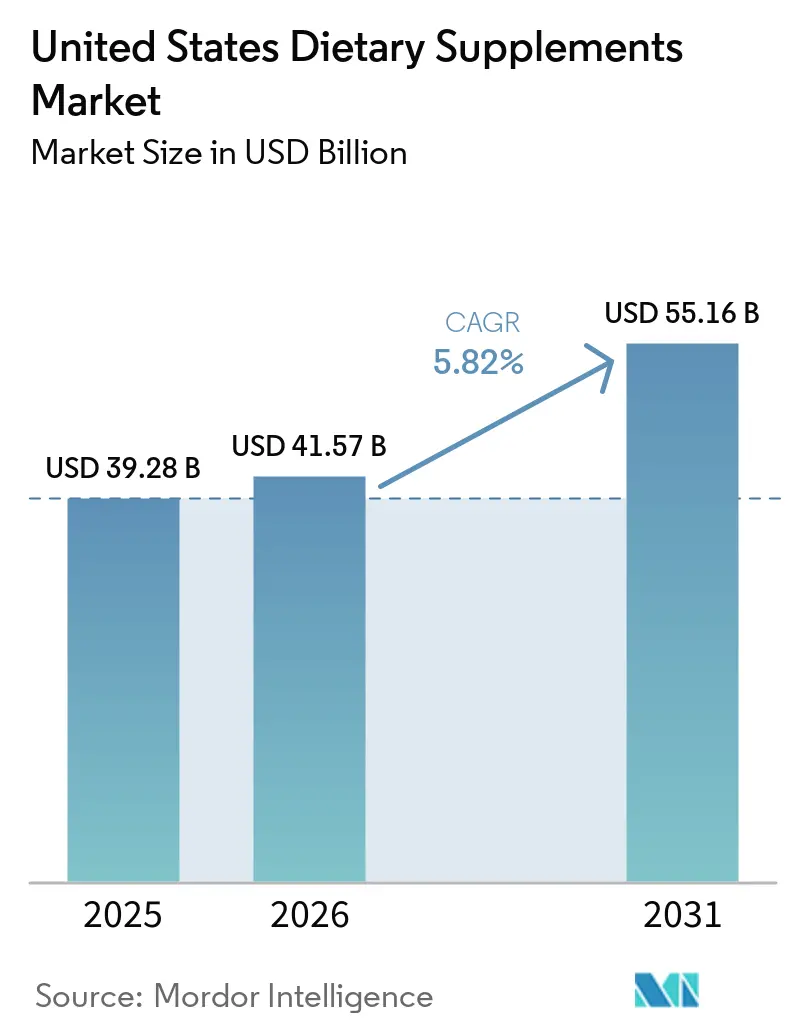

| Base Year Market Size (2025) | USD 39.28 Billion |

| Market Size (2026) | USD 41.57 Billion |

| Market Size (2031) | USD 55.16 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Dietary Supplements Market Analysis by Mordor Intelligence

The United States dietary supplements market size is expected to grow from USD 39.28 billion in 2025 to USD 41.57 billion in 2026 and is forecast to reach USD 55.16 billion by 2031 at 5.82% CAGR over 2026-2031. In the United States, a significant portion of the population relies on dietary supplements, integrating them into daily health routines. This reliance is further underscored by widespread nutrient deficiencies. The 2025 Dietary Guidelines Advisory Committee highlighted that 96% of Americans aged one and older fall short of the Estimated Average Requirement for vitamin D[1]Source: United States Department of Agriculture "Dietary Guidelines for Americans, 2020-2025", usda.gov . Alarmingly, nearly half of these individuals also lack adequate calcium intake. Such deficiencies establish a consistent demand for supplements, even in tighter economic periods. While addressing these fundamental needs, the market is experiencing a surge in innovation. There is a notable emphasis on women-centric and beauty-focused supplements. Gummies are gaining traction, and households are increasingly adopting supplements for children and teenagers. Distribution channels are also evolving. Specialty stores continue to serve as trusted purchase points, but online retail and social commerce are rapidly gaining prominence, enhancing brand visibility and acquisition. This shift particularly benefits agile, digitally native brands. Concurrently, as regulatory scrutiny intensifies, concerns about product integrity have become more prominent. In this environment, transparency, certification, and clinically substantiated claims have become critical to ensuring sustained consumer trust and credibility in the United States market.

Key Report Takeaways

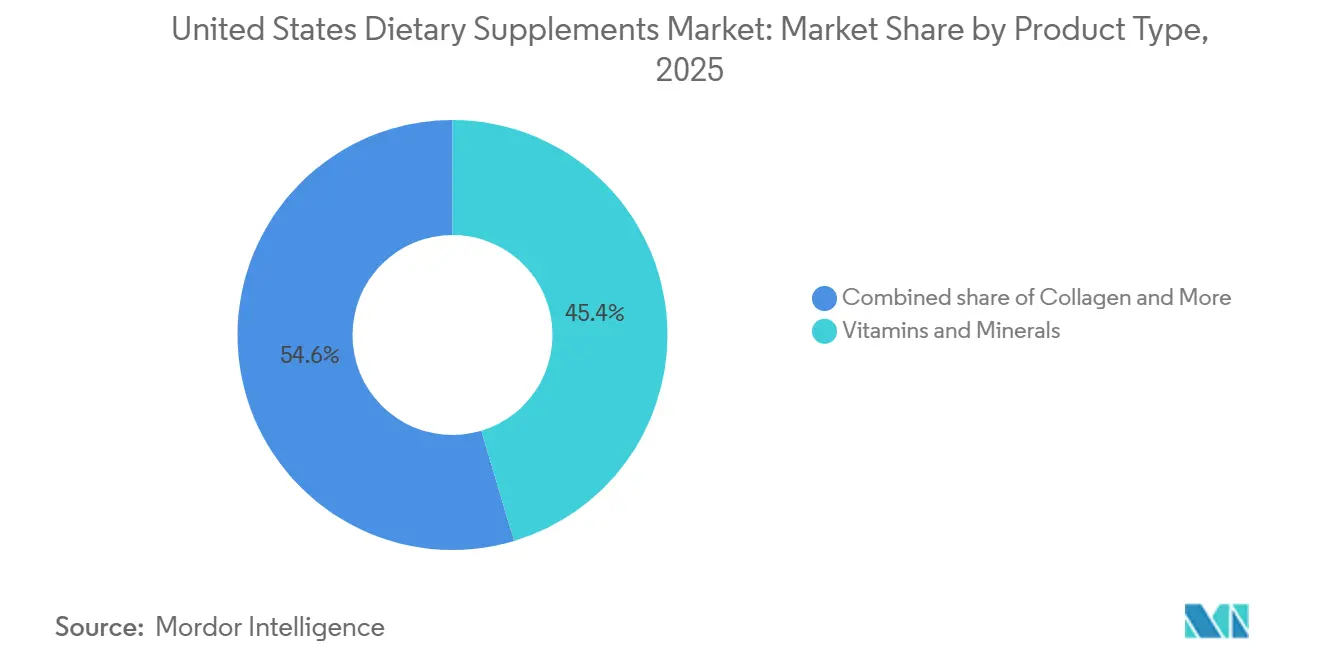

- In 2025, vitamins and minerals led the United States dietary supplements market, accounting for a 45.36% share. The enzymes segment is anticipated to grow at a 7.86% CAGR through 2031.

- In 2025, Tablets captured a 32.56% share of the United States dietary supplements market. However, gummies are expected to emerge as the fastest-growing format, with an 8.08% CAGR projected through 2031.

- In 2025, Adults constituted 86.45% of dietary supplement consumption. Meanwhile, products targeting children are forecasted to achieve the highest growth rate, with a 6.98% CAGR through 2031.

- In 2025, immunity enhancement applications held a 24.15% share of the United States dietary supplements market. Conversely, the skin, hair, and nail care segment is projected to expand at a 7.23% CAGR through 2031.

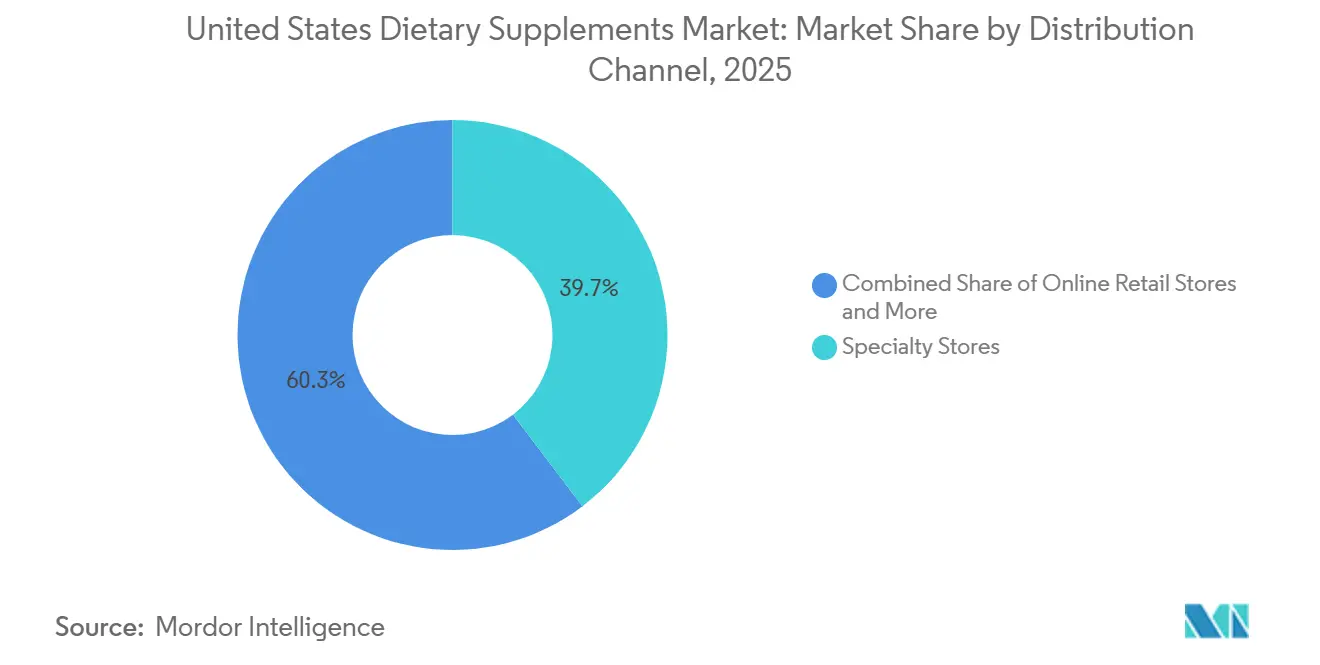

- In 2025, Specialty stores accounted for 39.67% of revenue. However, online retail is expected to be the fastest-growing distribution channel, with a 7.47% CAGR anticipated through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Dietary Supplements Market Trends and Insights

Drivers Impact Table*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer prioritization of preventive health and daily wellness management | +1.6% | National, with highest intensity in urban and suburban markets | Short to Medium term (1–4 years) |

| Supplements targeting women consumers fueling growth | +0.9% | National, concentrated in the 18–44 female demographic | Short term (≤ 2 years) |

| Shift towards natural and organic supplements | +0.7% | National, higher uptake in West Coast and Northeast markets | Medium term (2–4 years) |

| Increasing prevalence of chronic health conditions | +1.0% | National, concentrated in Southeast and Midwest populations | Long term (≥ 4 years) |

| Rapid growth of personalized nutrition solutions | +0.6% | National, early gains in tech-forward urban centers | Medium to Long term (2+ years) |

| Strengthening fitness and sports nutrition culture | +0.5% | National, with strong gains in Sunbelt and coastal metros | Short to Medium term (1–3 years) |

| Source: Mordor Intelligence | |||

Rising consumer prioritization of preventive health and daily wellness management

In the United States, a cultural shift toward preventive health and daily wellness management is driving the growth of the dietary supplements market. Consumers are increasingly incorporating dietary supplements into their daily regimens, transitioning from viewing them as occasional remedies to essential components of their wellness routines. This trend is supported by widespread nutrient deficiencies, particularly in vitamin D and calcium, which establish a consistent baseline demand for supplementation. Additionally, advancements in product innovation are expanding the range of consumer needs addressed by supplements. Beyond traditional areas such as immunity support, emerging categories like gut health, energy enhancement, and stress/mood management are becoming key growth drivers. A survey conducted by NOW Foods in January 2026 indicated that 44% of respondents increased their dietary supplement usage in 2025 compared to 2024[2]Source: NOW Foods "NOW Survey Uncovers 2026 Wellness and Health Priorities", nowfoods.com. These trends collectively highlight the proactive approach of United States consumers in leveraging dietary supplements to support long-term health objectives, mitigate chronic disease risks, and improve overall daily well-being.

Supplements targeting women consumers fueling growth

In the United States dietary supplements market, companies are increasingly focusing on women-centric innovation. These organizations are developing products tailored to address various physiological stages in women, ranging from fertility and premenstrual syndrome (PMS) to perimenopause. Young women represent the fastest-growing consumer segment in this market. Their primary demand centers around beauty-related supplements, particularly for hair, skin, and nail health, while there is also a notable interest in products supporting sleep and mental health. Clinical research highlights substantial nutrient deficiencies in iron and calcium among women and adolescent females, driving the need for targeted formulations. Additionally, supplements addressing mood and stress, such as Withania somnifera (commonly known as ashwagandha), have gained significant traction among female consumers, emphasizing the growing importance of hormonal and emotional wellness. In a strategic development, Herbalife acquired Bioniq in April 2026. Bioniq, a platform specializing in blood-biomarker personalization, enables Herbalife to meet the increasing demand for customized hormonal health solutions across various life stages. These market dynamics underscore the alignment of demographic demand, identified nutritional deficiencies, and the advancement of personalized innovation, establishing women-specific supplementation as a key growth driver in the United States market.

Increasing prevalence of chronic health conditions

Chronic health conditions are increasingly driving growth in the United States dietary supplements market, as consumers incorporate these products into their long-term wellness strategies and disease management plans. Prevalent health challenges such as hypertension, obesity, and prediabetes are encouraging individuals across various age groups to use dietary supplements in conjunction with medical treatments, particularly to support metabolic and cardiovascular health. This trend is further bolstered by a significant rise in adoption among individuals with diabetes. For example, Nestlé Health Science recently launched its Glucagon-Like Peptide-1 (GLP-1) Nutrition Support Platform, highlighting the integration of dietary supplements into patient care pathways, especially for those undergoing GLP-1 medication therapies. Additionally, a peer-reviewed study published in April 2025 in the Journal of the American Heart Association demonstrated that long-term magnesium supplementation is associated with a reduced risk of heart failure among diabetic patients[3]Source: American Heart Association Journals, "Nonprescription Magnesium Supplement Use and Risk of Heart Failure in Patients With Diabetes: A Target Trial Emulation", ahajournals.org. This clinical evidence reinforces the critical role of dietary supplements in chronic disease management. Collectively, these factors emphasize the substantial impact of chronic health conditions on the sustained demand within the United States dietary supplements market.

Rapid growth of personalized nutrition solutions

In the United States, the dietary supplements market is undergoing a significant transformation, primarily driven by the rapid growth of personalized nutrition. Enabled by advancements in technology, mass customization has transitioned from being a luxury to becoming a mainstream offering. Consumers in the United States dietary supplements market are increasingly adopting artificial intelligence (AI)-powered and customized solutions. What was previously considered a premium niche has now emerged as a strategic differentiator, enhancing customer loyalty through biomarker-based feedback mechanisms and subscription-based business models. Recent developments in the industry highlight this progression: GenoPalate introduced "GenoBlend" in 2024, a protein and fiber supplement customized based on deoxyribonucleic acid (DNA), while Bioniq launched formulations tailored using blood biomarker data. These two personalization pathways emphasize the growing demand for individualized protocols within the United States market. This shift not only underscores the critical role of personalization but also signals its potential to disrupt traditional distribution models and pose challenges to established mass-market supplement brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and evolving regulatory environment | -0.4% | National, with state-level regulatory divergence | Long term (≥ 4 years) |

| Growing consumer concerns around product safety, adulteration, and side effect risks | -0.3% | National, disproportionately concentrated in online retail channels | Short to Medium term (1–3 years) |

| Intense market saturation creating high competition | -0.3% | National | Medium term (2–4 years) |

| Ingredient quality and supply chain challenges | -0.2% | Global supply chain impact, concentrated in botanical and marine ingredient categories | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Complex and evolving regulatory environment

In the United States dietary supplements market, a complex and continuously evolving regulatory framework presents a significant challenge. Federal and state-level initiatives contribute to uncertainty and increase compliance costs, particularly impacting smaller manufacturers. The United States Food and Drug Administration's (FDA) Human Foods Program has prioritized finalizing the New Dietary Ingredient (NDI) guidance and advancing Generally Recognized as Safe (GRAS) reform. These developments signal potential changes in regulatory oversight not seen since the introduction of Good Manufacturing Practices (GMP) regulations. Additionally, new legislative proposals, such as the Dietary Supplement Listing Act of 2026 and efforts to preempt state-level restrictions, add further complexity to the regulatory environment. Concurrently, the United States Department of Health and Human Services (HHS) Office of Inspector General is intensifying audits of supplement facilities, while the Federal Trade Commission (FTC) is increasing enforcement actions through civil penalties and substantiation warning campaigns. Collectively, these overlapping regulatory measures are reshaping the compliance landscape in the United States, underscoring the critical importance of transparency and adherence to evolving standards for maintaining credibility and driving growth.

Growing consumer concerns around product safety, adulteration, and side effect risks

Consumer concerns regarding product safety, adulteration, and potential side effects are increasingly influencing purchasing decisions in the United States dietary supplements market. These concerns, highlighted by the United States Food and Drug Administration (FDA) alerts, have significantly undermined consumer trust. The FDA has identified persistent issues with adulterated supplements, particularly those sold through online platforms. Its database on tainted products frequently reports the presence of undeclared pharmaceutical ingredients, especially in categories such as weight-loss and muscle-building supplements. Surveys indicate that a considerable proportion of consumers remain apprehensive about safety and uncertain about which brands to trust. This trust deficit has prompted many consumers to shift their spending toward companies that demonstrate strong quality assurance measures and possess third-party certifications. As a result, product integrity has become a critical factor in establishing brand credibility and fostering consumer loyalty within the United States market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vitamins and Minerals Lead, Enzymes Signal an Under-Appreciated Pivot

In 2025, vitamins and minerals dominated the United States dietary supplements market, holding a 45.36% share. Their leading position was supported by widespread nutrient deficiencies across the population and strong recommendations from healthcare professionals, positioning multivitamins as the primary choice for many consumers. These supplements not only served as the initial entry point for consumers exploring multi-product combinations but also expanded into related categories. These included collagen, which is popular for beauty and joint health, and herbal supplements such as ashwagandha and green tea, which address adaptogenic and mood-enhancing needs. Due to their wide range of applications and clinical importance, vitamins and minerals continue to act as the structural backbone of the United States market.

Conversely, enzymes are projected to be the fastest-growing segment, with a CAGR of 7.86% forecasted for the period 2026–2031. This anticipated growth highlights a significant shift in consumer demand. Increasing awareness of gut health and the straightforward digestive support enzymes provide has positioned them as a preferred solution for many consumers. Their growth trajectory is further strengthened by advancements in multi-enzyme blends and the expanding adoption of prebiotics and probiotics, emphasizing digestion as a critical area for innovation in the supplement industry. As enzymes are expected to outpace all other product types in growth, they are well-positioned to reshape the competitive landscape by appealing to consumers seeking targeted, clinically validated solutions for digestive wellness.

By Form: Tablets Hold Ground, Gummies Reshape Purchase Occasion

In 2025, tablets dominated the United States dietary supplements market, accounting for a 40.39% share. Their popularity was driven by precise dosing, endorsements from healthcare professionals, and institutional purchasing trends, which established them as the preferred format for essential supplementation. Leading industry players reinforced this position through strategic investments in manufacturing capabilities and extensive product portfolios, ensuring tablets remained the cornerstone of supplement consumption. While capsules and softgels addressed the needs of oil-based actives, and powders and liquids gained niche relevance due to their flexibility and rapid absorption, tablets retained their entrenched position as the most widely used format in the United States market.

Conversely, gummies are expected to reshape consumer purchasing behaviors as the fastest-growing format, with a CAGR of 8.12% projected for the period 2026–2031. Their growth is attributed to their appealing taste, convenience, and ability to transform supplementation into an enjoyable daily routine, making them particularly attractive to younger demographics and lifestyle-focused consumers. Initially confined to vitamin products, gummies are now expanding into clinically significant categories such as probiotics and immunity boosters. This expansion is supported by advancements in encapsulation technologies, which enable the effective delivery of sensitive active ingredients. These developments position gummies as a key growth driver, redefining consumer expectations and compelling manufacturers to adapt their innovation pipelines to meet evolving demand in the United States market.

By Consumer Group: Adults Drive Volume, Children Unlock Category Breadth

In the United States dietary supplements market, adults held an 86.45% share in 2025. This dominance highlighted a trend of increased health spending among working-age and older populations. Seniors, in particular, demonstrated significant usage intensity as they relied on supplements to reduce the risks associated with chronic diseases. Beyond single-supplement adoption, adults increasingly incorporated a variety of products, including vitamins, minerals, and specialized formulations, into their routines. This sustained engagement, supported by physician recommendations and a comprehensive base of clinical evidence, positioned adults as the foundational segment driving market volume.

In contrast, children are expected to be the fastest-growing consumer group, with a projected CAGR of 6.78% during the forecast period of 2026–2031. This anticipated growth is driven by parents' growing focus on preventive healthcare and the popularity of innovative formats, such as gummies, which have made pediatric supplementation more accessible and appealing. Additionally, documented nutrient deficiencies among adolescents, particularly in calcium and magnesium, provide a clinical basis for targeted product development. Prenatal supplementation further enhances the relevance of this segment. In response, brands are introducing clean-label and trust-focused offerings, expanding the children's supplement category while reshaping the competitive landscape by addressing family-centered health priorities in the United States market.

By Health Applications: Immunity Enhancement Leads, Skin-Hair-Nail Accelerates

In 2025, immunity enhancement retained the largest share of the United States dietary supplements market, accounting for 24.15% of health applications. This dominance, which was solidified during the pandemic, had been bolstered by consumers' consistent reliance on immune-support products, such as vitamin C and zinc, in their daily wellness routines. The widespread consumer relevance of immune health, viewed as an essential aspect of supplementation, cemented its position as the most established application in the United States market.

Conversely, the skin, hair, and nail care segment is projected to be the fastest-growing application, with a compound annual growth rate (CAGR) of 7.23% forecasted for the period 2026 to 2031. This surge signals a shift in beauty consumer mindset, favoring systemic supplementation over traditional topical solutions. The premiumization of ingredients, especially with clinical endorsements like collagen, coupled with a surge in new product launches, is broadening the category's appeal, particularly among women prioritizing lifestyle wellness. Consequently, skin-hair-nail care is not just a growing segment but a transformative force, merging beauty and nutrition into a unified value proposition in the United States market.

By Distribution Channel: Specialty Stores Anchor Premiumization, Online Redefines Discovery

In 2025, specialty stores accounted for the largest distribution share of 39.67% in the United States dietary supplements market. This performance was driven by their ability to offer knowledgeable staff consultations, a wide range of product assortments, and premium positioning that appealed to health-conscious consumers. These stores established themselves as key platforms for both product discovery and replenishment, particularly for brands emphasizing scientific credibility and professional alignment. By building trust and reinforcing premiumization, specialty stores solidified their position as the foundation of supplement distribution in the United States.

Online retail, however, is projected to be the fastest-growing distribution channel, with a CAGR of 7.47% anticipated for the forecast period of 2026 to 2031. This channel is transforming how consumers discover and purchase dietary supplements. Features such as subscription-based commerce, algorithm-driven product visibility, and social video marketing formats are reducing customer acquisition costs while enabling emerging brands to compete directly with established market players. Although trust-related concerns persist, the convenience and personalization offered by online platforms are driving rapid adoption. This positions e-commerce as a significant disruptor in the dietary supplements distribution landscape. Together, specialty stores and online retail highlight the dual forces of premium credibility and digital accessibility that are shaping the future trajectory of the United States dietary supplements market.

Geography Analysis

The United States dietary supplements market thrives on widespread consumer adoption, daily usage habits, and a robust narrative linking nutrients to chronic disease management. This vast market has shifted supplements from being occasional buys to essential consumables, anchoring global revenues. While the Northeast and West Coast have long been strongholds, states in the Sunbelt are witnessing a surge, driven by a growing emphasis on fitness and lifestyle.

Distinctively, the United States stands out not just for its spending intensity but also as the go-to ground for testing global ingredient innovations. American consumers, with their high habituation rates, often turn to practitioner channels, bolstering trust and premium positioning. This dynamic landscape lures international suppliers, eager to debut their premium-functional ingredients in the United States before taking them worldwide. The interplay of consumer adoption, clinical backing, and physician endorsements fortifies the United States market's dominant stance.

However, this vastness and maturity come with challenges. Rising consumer demands for safety, transparency, and innovation push brands to stand out in a sea of commoditization. Navigating the maze of regulatory complexities and building trust in a fragmented online space pose significant hurdles. Moreover, while brands chase premiumization, they must ensure their offerings remain accessible and backed by solid evidence. These challenges highlight that the United States market, despite its size and clout, must adeptly maneuver through shifting consumer trends, regulatory landscapes, and unique competitive pressures to maintain its leadership.

Competitive Landscape

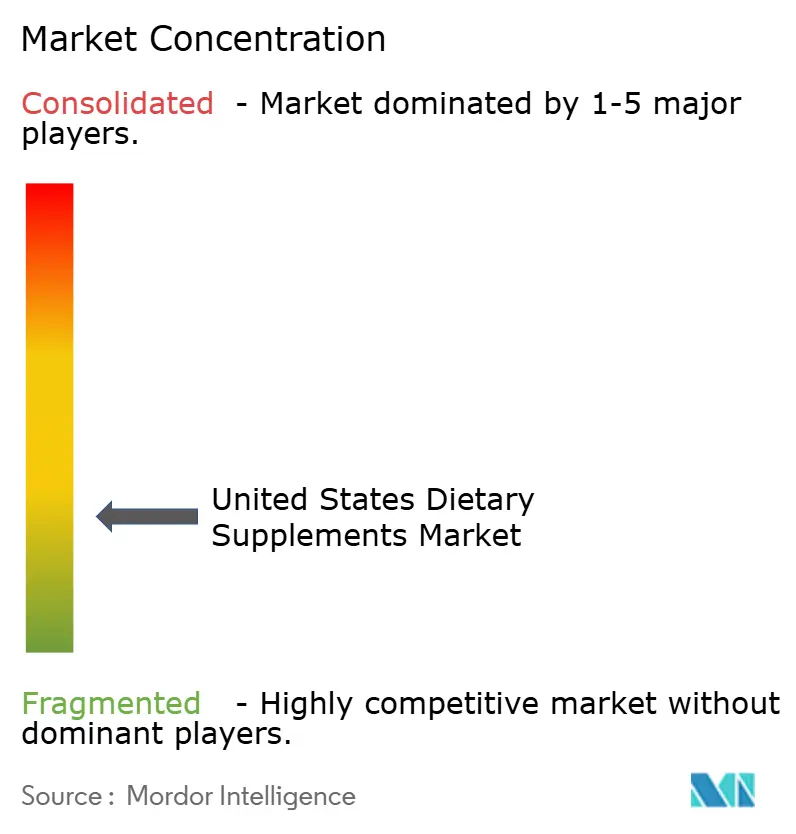

The United States dietary supplements market is fragmented, with multinational corporations competing for dominance alongside specialty brands, practitioner-exclusive lines, and digitally native challengers. No single entity exerts significant control over pricing or distribution, positioning science-backed differentiation as the primary competitive advantage. Leading companies are allocating substantial resources toward clinical validation, certifications, and strategic partnerships to enhance their credibility. Concurrently, other players are adopting personalization and data-driven platforms to move beyond commoditized offerings. This evolving market landscape highlights that brand strength increasingly depends on evidence, exclusivity, and consumer trust rather than sheer scale.

Compliance frameworks are becoming critical competitive differentiators, reshaping market access and positioning strategies. Major retailers and platforms are implementing stricter requirements, effectively filtering out non-compliant sellers. In response, established companies are exceeding regulatory certification standards to demonstrate their commitment to quality and reliability. This emphasis on manufacturing rigor and transparency not only strengthens consumer confidence in established brands but also creates significant barriers to entry for smaller competitors. However, opportunities remain in underdeveloped segments such as cognitive health, pediatric nutrition, and sleep support, where consumer demand continues to outpace product innovation.

Personalization represents the most significant disruption, with artificial intelligence-driven platforms and biomarker-based solutions redefining competitive boundaries. Emerging players are building proprietary data assets capable of delivering clinical-grade personalization at consumer-friendly price points. This innovation threatens the relevance of generic multivitamins and mass-market products. As personalization gains traction, incumbent companies are compelled to adjust their portfolios and distribution strategies to maintain their market position. Consequently, the United States market is characterized by a combination of entrenched credibility, regulatory-driven consolidation, and disruptive innovation, establishing it as a highly competitive and strategically critical arena for global supplement brands.

United States Dietary Supplements Industry Leaders

-

Amway Corp.

-

Nature Made

-

Herbalife Nutrition Ltd.

-

Nestlé S.A.

-

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Amway announced the completion of a United States Dollar (USD) 75 million expansion at its Nutrilite Spaulding Plant located in Ada, Michigan. This investment converted 52,000 square feet of warehouse space into a state-of-the-art facility dedicated to solid dose tablet manufacturing and a quality control laboratory. The upgraded facility was equipped with over 500 pieces of advanced machinery, including high-speed rotary tablet presses and a dual-capsule filling machine

- April 2026: Herbalife completed the acquisition of Bioniq's personalized nutrition business assets for a base consideration of USD 55 million, with potential contingent payments of up to USD 95 million, dependent on future product sales. The transaction added a patented blood-biomarker personalization engine and a call option on Bioniq Laboratory's small-molecules and peptides platform to Herbalife's portfolio. Bioniq-powered personalized supplements were expected to launch through Herbalife distributors in the United States in July 2026, representing the company's most significant capability expansion since its acquisition of Pro2col Health.

- April 2026: USANA Health Sciences launched Glow, its first skin-health supplement. Supported by clinical trials involving 162 women, the research demonstrated a significant 65% improvement in skin uniformity after three months. Glow's formulation included clinically studied ingredients such as Damasty (a rose extract), Bioactive Melon Superoxide Dismutase (SOD), Acerola Cherry Vitamin C, astaxanthin, and grape seed extract. This product was strategically designed to address the rapidly growing health applications sub-segment within the United States market.

United States Dietary Supplements Market Report Scope

Dietary supplements are products taken orally that add nutrients or other beneficial substances to the diet, intended to support overall health but not to treat or cure diseases. They include vitamins, minerals, herbs, amino acids, and other compounds, and are regulated in the United States under specific guidelines that distinguish them from conventional foods and drugs.

The market is segmented by product type, form, consumer group, health applications, and distribution channels. By product type, the market is segmented into vitamins and minerals, collagen, fatty acids, herbal supplements, enzymes, prebiotics and probiotics, and other product types. By form, the market is segmented into tablets, capsules and soft gels, powder, gummies, liquids, and other forms. By consumer group, the market is segmented into adults and children. By health applications, the market is segmented into general health and wellness, bone and joint health, energy and weight management, gastrointestinal and gut health, immunity enhancement, cardiovascular health, diabetes management, cognitive and mental health, skin, hair, and nail care, eye health, and other health applications. By distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online retail stores, direct selling stores, and other distribution channels.

| Vitamins and Minerals |

| Collagen |

| Fatty Acids |

| Herbal Supplements |

| Enzymes |

| Prebiotics and Probiotics |

| Other Product Type |

| Tablets |

| Capsules and Soft gels |

| Powder |

| Gummies |

| Liquids |

| Other Forms |

| Adults |

| Children |

| General Health and Wellness |

| Bone and Joint Health |

| Energy and Weight Management |

| Gastrointestinal and Gut Health |

| Immunity Enhancement |

| Cardiovascular Health |

| Diabetes Management |

| Cognitive and Mental Health |

| Skin, Hair and Nail Care |

| Eye Health |

| Other Health Applications |

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Direct Selling Stores |

| Other Distribution Channels |

| Product Type | Vitamins and Minerals |

| Collagen | |

| Fatty Acids | |

| Herbal Supplements | |

| Enzymes | |

| Prebiotics and Probiotics | |

| Other Product Type | |

| Form | Tablets |

| Capsules and Soft gels | |

| Powder | |

| Gummies | |

| Liquids | |

| Other Forms | |

| By Consumer Group | Adults |

| Children | |

| By Health Applications | General Health and Wellness |

| Bone and Joint Health | |

| Energy and Weight Management | |

| Gastrointestinal and Gut Health | |

| Immunity Enhancement | |

| Cardiovascular Health | |

| Diabetes Management | |

| Cognitive and Mental Health | |

| Skin, Hair and Nail Care | |

| Eye Health | |

| Other Health Applications | |

| Distribution Channel | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Online Retail Stores | |

| Direct Selling Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the size and growth outlook of the United States dietary supplements market?

The market was valued at USD 39.28 billion in 2025 and is projected to reach USD 55.16 billion by 2031, reflecting a CAGR of 5.82% between 2026 and 2031.

Which product type dominates the United States market?

Vitamins and Minerals are the largest product category, accounting for 45.36% of market share in 2025, supported by widespread consumer adoption for preventive health.

Which product type is expected to grow the fastest?

Enzymes are the fastest-growing segment, forecasted to expand at a CAGR of 7.86% from 2026 to 2031, driven by demand for digestive support and specialized formulations.

What is the leading form and the fastest-growing form of supplements?

Tablets held the largest share at 32.56% in 2025, while Gummies are the fastest-growing format, projected to expand at a CAGR of 8.08% from 2026 to 2031 due to consumer preference for convenience and taste.

Which consumer group and health application drive demand?

Adults accounted for 86.45% of consumption in 2025, while Immunity Enhancement was the leading health application at 24.15% share. Looking ahead, Children’s supplements and Skin, Hair, and Nail Care are expected to grow fastest, with CAGRs of 6.98% and 7.23% respectively.

Page last updated on: