Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

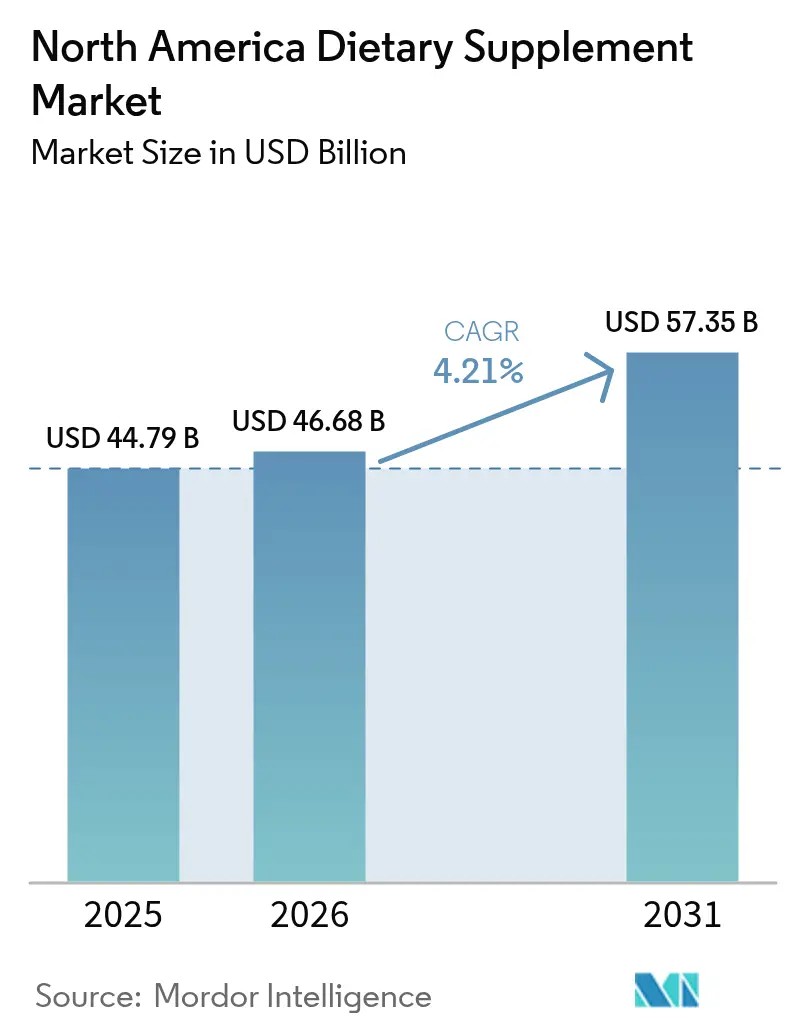

| Base Year Market Size (2025) | USD 44.79 Billion |

| Market Size (2026) | USD 46.68 Billion |

| Market Size (2031) | USD 57.35 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Dietary Supplement Market Analysis by Mordor Intelligence

The North America dietary supplements market size was valued at USD 44.79 billion in 2025 and estimated to grow from USD 46.68 billion in 2026 to reach USD 57.35 billion by 2031, at a CAGR of 4.21% during the forecast period (2026-2031). As the market matures, growth opportunities are increasingly tied to innovations in delivery formats, condition-specific blends, and personalized offerings tailored to individual health needs. The demand for vitamins and minerals continues to dominate revenue generation; however, botanicals are experiencing the fastest growth due to a rising consumer preference for holistic, plant-based solutions. Mexico, supported by a growing middle class and improved retail access, is expanding at a faster pace compared to the United States and Canada, contributing significantly to the region's overall growth. At the same time, regulatory tightening by the U.S. FDA and stricter retailer quality mandates are driving up compliance costs. These changes are pushing brands to adopt higher transparency standards and focus on science-backed claims to maintain consumer trust and market competitiveness.

Key Report Takeaways

- By product type, vitamins and minerals held 31.02% of the North America dietary supplements market share in 2025, while herbal and botanical supplements are projected to grow at a 6.28% CAGR through 2031.

- By form, tablets dominated with 34.11% revenue share in 2025; gummies and chewables are advancing at a 6.74% CAGR to 2031.

- By source, synthetic and fermentation-derived ingredients accounted for 46.74% of the North America dietary supplements market size in 2025, whereas plant-based sources are set to expand at a 5.78% CAGR between 2026 and 2031.

- By consumer group, women represented 55.63% of users in 2025, and products for children are expected to post a 5.41% CAGR to 2031.

- By health application, bone and joint formulas captured 24.54% of the North America dietary supplements market size in 2025; beauty and skin health lines are forecast to rise at an 4.81% CAGR to 2031.

- By distribution channel, specialty stores led with 45.66% revenue share in 2025, while online retail is tracking a 5.57% CAGR through 2031.

- By geography, United States commanded a 77.82% share of the North America dietary supplement market in 2025 and Mexico remains the fastest-growing country at 6.61% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of North America Dietary Supplement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High health consciousness driving consistent use of supplements | +0.7% | North America, with highest impact in U.S. and Canada | Medium term (3-4 years) |

| Supplements Targeting Women Consumers Fueling Growth | +0.8% | North America, particularly U.S. urban centers | Medium term (3-4 years) |

| Strong fitness and wellness culture boosts sports supplement sales | +0.7% | U.S., Canada, urban Mexico | Short term (≤ 2 years) |

| Aging baby boomer population fuels demand for targeted nutrition | +0.5% | U.S., Canada | Long term (≥ 5 years) |

| Prevalence of Chronic Diseases Propelling the market Growth | +0.9% | North America, with spillover to global markets | Long term (≥ 5 years) |

| Increased Focus on Immune Health Driving the Market Growth | +1.6% | Global, with strong impact across North America | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

High Health Consciousness Driving Consistent Use of Supplements

Increasing health consciousness among consumers is a significant driver of consistent supplement usage. The growing awareness of the benefits of dietary supplements, such as improved immunity, enhanced energy levels, and overall well-being, has led to a surge in demand. According to the Council for Responsible Nutrition Survey 2023, nearly 74% of adults in the United States reported using dietary supplements, with multivitamins being the most commonly consumed[1]Source: Council for Responsible Nutrition, "2023 CRN Consumer Survey on Dietary Supplements", www.crnusa.org. This trend is further supported by government initiatives, such as the Dietary Guidelines for Americans, which emphasize the importance of meeting nutritional needs through a combination of food and supplements when necessary. Additionally, the U.S. Food and Drug Administration (FDA) regulates dietary supplements to ensure safety and accurate labeling, further boosting consumer confidence. As consumers increasingly prioritize preventive healthcare and holistic wellness, the consistent use of dietary supplements is expected to remain a key factor driving market growth during the forecast period.

Supplements Targeting Women Consumers Fueling Growth

The increasing demand for dietary supplements targeting women is significantly driving the growth of the market. Women-specific supplements, including prenatal vitamins, calcium, and iron supplements, are gaining traction due to rising awareness about women's health and wellness. According to the Office on Women's Health (OWH), a division of the U.S. Department of Health and Human Services, women have unique nutritional needs at different life stages, such as during pregnancy, lactation, and menopause [2]Source: Office on Women's Health, "Healthy eating and women", www.womenshealth.gov. This has led to a growing emphasis on tailored dietary supplements to address these specific requirements. Additionally, the increasing prevalence of lifestyle-related health issues among women, such as osteoporosis and anemia, further boosts the demand for these products. The trend is supported by government initiatives promoting women's health and nutrition, which are expected to sustain market growth during the forecast period.

Strong Fitness and Wellness Culture Boosts Sports Supplement Sales

The expanding definition of "active consumer" has transformed sports nutrition from a niche category into a mainstream market segment. In North America, the growing emphasis on fitness and wellness has significantly contributed to the rising demand for sports supplements. According to the U.S. Department of Health and Human Services, initiatives such as the "Physical Activity Guidelines for Americans" encourage individuals to engage in regular physical activity, which has led to an increased focus on dietary supplements to enhance performance, recovery, and overall health. Furthermore, the Centers for Disease Control and Prevention (CDC) emphasizes the importance of addressing nutrient gaps in the diet, which has driven consumers to seek sports nutrition products as a convenient solution. Government-backed campaigns promoting healthy eating and active lifestyles, such as "Move Your Way," have also played a pivotal role in raising awareness about the benefits of dietary supplements. This cultural shift toward proactive health management, combined with increasing participation in fitness activities like gym workouts, yoga, and recreational sports, continues to propel the growth of the sports supplement market in the region.

Prevalence of Chronic Disease Propelling the Market Growth

The rising prevalence of chronic diseases, such as diabetes, cardiovascular disorders, and obesity, is significantly driving the growth of the North America dietary supplements market. According to the Centers for Disease Control and Prevention (CDC), approximately 6 in 10 adults in the United States have a chronic disease, and 4 in 10 adults have two or more chronic conditions [3]Source: Centers for Disease Control and Prevention, "About Chronic Diseases-October 2024", www.cdc.gov. This increasing burden of chronic illnesses has led to a growing demand for dietary supplements as consumers seek preventive healthcare solutions and nutritional support. Additionally, government initiatives promoting awareness about the benefits of dietary supplements and their role in managing chronic diseases are further propelling market growth. For instance, the National Institutes of Health (NIH) provides extensive resources and guidelines on dietary supplements, emphasizing their importance in maintaining overall health and preventing disease progression. The growing focus on preventive healthcare, supported by government-backed campaigns and public health programs, is expected to sustain the demand for dietary supplements in the region.

Restraints Impact Analysis of North America Dietary Supplement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit Products Hindering Growth | -0.7% | Global, with significant impact in online channels across North America | Medium term (3-4 years) |

| Growing preference for whole foods over supplements | -0.5% | U.S., Canada, educated urban demographics | Long term (≥ 5 years) |

| Rising scrutiny over unregulated or mislabeled products | -0.4% | U.S., with spillover to Canada and Mexico | Short term (≤ 2 years) |

| Regulatory Compliance Challenges for Exports | -0.3% | Mexico to U.S./Canada exports, cross-border trade | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit Products Hindering Growth

The surge of counterfeit dietary supplements, especially via online platforms, jeopardizes both market expansion and consumer confidence. In the North American Dietary Supplements Market, counterfeit products have emerged as a critical restraint, undermining the credibility of genuine brands and creating significant challenges for regulatory authorities. The ease of access to counterfeit goods through e-commerce channels has further exacerbated the issue, making it difficult for consumers to differentiate between authentic and fake products. This not only impacts the revenue of legitimate manufacturers but also raises concerns about consumer safety, as counterfeit supplements often fail to meet quality and safety standards. Furthermore, the presence of counterfeit goods dilutes brand loyalty and trust, which are essential for the sustained growth of the dietary supplements market. Addressing this issue requires stringent regulatory measures, increased consumer awareness, and collaboration between stakeholders to safeguard the market's integrity. Governments and regulatory bodies in North America are increasingly focusing on implementing advanced tracking and tracing technologies, such as blockchain, to ensure product authenticity.

Growing Preference for Whole Foods Over Supplements

Consumers are increasingly prioritizing nutrient-dense whole foods over pills and powders, signaling a counter-trend to supplement consumption. This trend acts as a significant restraint in the North American Dietary Supplements Market. The U.S. Preventive Services Task Force recently advised against vitamin D supplementation for fall prevention in older adults, highlighting the growing skepticism about the efficacy of supplements. This skepticism is further fueled by increasing awareness among consumers about the potential risks of over-supplementation, such as toxicity or adverse interactions with medications. Additionally, the rising popularity of functional foods, which provide health benefits beyond basic nutrition, is diverting consumer spending away from traditional supplements. As a result, manufacturers in the dietary supplements market may face challenges in sustaining growth, particularly in regions like North America, where consumer preferences are rapidly evolving toward whole-food-based nutrition solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

North America Dietary Supplement Market Segment Analysis

By Product Type:

Vitamins Hold Scale; Botanicals AccelerateVitamins and minerals accounted for 31.02% of the market share in 2025, driven by their widespread acceptance among physicians and the proven efficacy of standardized doses. These products remain a cornerstone of the market, offering consumers reliable and trusted options for their nutritional needs. However, the market is also witnessing a notable shift, as herbal and botanical supplements gain traction. These products are projected to grow at a robust CAGR of 6.28% through 2031, outpacing the overall market growth. This surge is fueled by increasing consumer interest in holistic health solutions, prompting brands to innovate with adaptogens like ashwagandha and functional mushrooms, which are now integral to immune and stress support blends.

Another significant trend shaping the market is the diversification of supplement delivery formats. While capsules remain the dominant choice for vitamin delivery due to their convenience and familiarity, newer formats such as tinctures, shots, and gummies are driving innovation in the botanical segment. These alternative formats cater to consumer preferences for flavor variety and portability, making them particularly appealing for on-the-go lifestyles. This shift reflects the growing demand for products that combine functionality with convenience, allowing consumers to seamlessly integrate dietary supplements into their daily routines. As a result, brands are increasingly focusing on developing products that align with these evolving preferences. Ingredient suppliers are also playing a crucial role in supporting this market transformation.

By Consumer Group:

Women Anchor Volume; Children Drive Incremental GrowthIn 2025, women accounted for 55.63% of all buyers, a trend fueled by the availability of targeted SKUs specifically designed to address their health needs. These SKUs include products enriched with iron, folate, collagen, and hormonal balance supplements, catering to various life stages and health concerns. This focus on women's health has driven significant engagement in the dietary supplements market, highlighting the importance of tailored solutions. Meanwhile, the children's segment, although smaller in size, is projected to grow at an impressive 5.41% CAGR through 2031, surpassing the growth rate of the overall market. This growth is largely attributed to the increasing popularity of gummies fortified with essential nutrients like calcium and DHA, which make daily dosing more convenient and appealing for children. These products address the nutritional gaps in children's diets while ensuring ease of consumption, which is a key factor for parents.

Digital health platforms are playing a pivotal role in enhancing the adoption of dietary supplements for children. By partnering with pediatricians, these platforms provide dosing reminders and educational resources that help parents make informed decisions about their children's health. This collaboration fosters trust among parents, encouraging repeat purchases and long-term brand loyalty. For women, the demand for prenatal and menopausal supplement ranges continues to dominate the market. These ranges include clinically validated formulations such as calcium-magnesium complexes and phytoestrogen supplements, which are positioned as effective non-prescription options. These products are designed to support lifelong bone density and alleviate symptoms associated with menopause, addressing critical health concerns for women. The emphasis on clinically studied ingredients further reinforces consumer confidence, driving sustained growth in this segment.

By Source:

Synthetic Dominance Faces Plant-Based UpswingSynthetic or fermentation-derived actives still constitute 46.74% of the 2025 market. This dominance is attributed to their predictable yields, which ensure consistent production outcomes, and their cost advantages, making them a preferred choice for manufacturers. These actives are widely utilized in dietary supplements due to their reliability in meeting quality standards and their ability to be produced at scale, catering to the growing consumer demand for health and wellness products. The stability and efficiency of synthetic inputs further solidify their position in the market, especially in applications where precision and consistency are critical. Additionally, synthetic actives offer the advantage of controlled production processes, which reduce variability and enhance product uniformity. This level of control is particularly important in the dietary supplements market, where regulatory compliance and product efficacy are paramount. Furthermore, the ability to customize synthetic actives to meet specific functional requirements provides manufacturers with greater flexibility, enabling them to develop innovative formulations that address diverse consumer needs.

On the other hand, plant-based inputs are gaining significant traction in the market, driven by evolving consumer preferences. These inputs are registering a notable compound annual growth rate (CAGR) of 5.78%, projected to continue through 2031. The increasing adoption of vegan lifestyles and the rising demand for clean-label products are key factors propelling this growth. Consumers are increasingly seeking natural and sustainable alternatives, which has led to a surge in the use of plant-based actives in dietary supplements. These inputs are perceived as healthier and more environmentally friendly, aligning with the broader trends of sustainability and transparency in the market. As a result, plant-based actives are expected to play a pivotal role in shaping the future of the dietary supplements industry in North America.

By Form:

Tablets Lead; Gummies Redefine ConvenienceIn 2025, tablets accounted for 34.11% of the revenue in the North America dietary supplements market, driven by their manufacturing efficiency and precise dosing capabilities. Tablets remain a preferred choice among consumers and manufacturers due to their cost-effectiveness, longer shelf life, and ease of storage and transportation. They are also highly versatile, allowing for the incorporation of various active ingredients, including vitamins, minerals, and herbal extracts, in a single dosage form. The ability to produce tablets in different sizes, shapes, and coatings further enhances their appeal, catering to diverse consumer preferences. Additionally, advancements in tablet formulations, such as controlled-release, effervescent, and chewable tablets, have expanded their functionality and improved consumer compliance. These innovations have made tablets a dominant segment in the dietary supplements market, addressing the needs of both health-conscious individuals and those seeking convenience in their daily supplement intake.

Gummies and chewables, favored for their taste and convenience, are projected to grow at an annual rate of 6.74%, which is double the expected growth rate of the North America dietary supplements market. This segment has gained significant traction among consumers, particularly children and older adults, who prefer alternatives to traditional tablets and capsules. The adoption of pectin-based technologies has been a key driver for this growth, as these technologies reduce sugar content and enable vegan label claims, catering to the rising demand for plant-based and health-conscious products. Furthermore, the availability of gummies and chewables in various flavors and shapes has enhanced their consumer appeal, making them a rapidly growing segment in the dietary supplements market.

By Health Application:

Bone and Joint Health Leads; Beauty and Skin Health OutperformIn 2025, bone and joint formulas captured 24.54% of North America's dietary supplements market, highlighting the growing focus among baby boomers on maintaining mobility and joint health as they age. This segment's significant share reflects the increasing demand for targeted nutritional solutions that address age-related concerns, such as bone density, joint flexibility, and overall physical well-being. The aging population, particularly in North America, is increasingly prioritizing preventive healthcare and functional nutrition, driving the adoption of these specialized supplements. The rising prevalence of conditions such as arthritis and osteoporosis has further amplified the need for bone and joint health products, making this category a cornerstone of the dietary supplements market.

Meanwhile, beauty and skin health products, which combine collagen peptides with vitamins A and C, are experiencing a strong growth trajectory with a 4.81% CAGR. This growth is fueled by a rising consumer preference for holistic wellness solutions that promote skin health, elasticity, and overall appearance. The connection between internal nutrition and external skin radiance has gained substantial traction, as consumers increasingly seek products that deliver both functional and aesthetic benefits. These products cater to a broad demographic, including younger consumers focused on preventive skincare and older individuals aiming to reduce visible signs of aging. The integration of scientifically-backed ingredients, such as collagen peptides known for their role in improving skin hydration and reducing wrinkles, has further enhanced the appeal of this category.

By Distribution Channel:

Specialty Stores Dominate; Online Retail Rewires AccessIn 2025, specialty health-nutrition stores held a commanding 45.66% market share, showcasing their strong position in the market. This dominance is largely attributed to their ability to provide expert staff who possess in-depth knowledge of health and nutrition products. These professionals play a crucial role in guiding customers toward making well-informed purchasing decisions, which enhances customer trust and satisfaction. Additionally, these stores offer carefully curated product assortments that cater to the specific health and wellness needs of their target audience. By focusing on quality and relevance, specialty health-nutrition stores have successfully built a loyal customer base, further solidifying their market position. The personalized shopping experience and the assurance of expert advice have made these stores a preferred choice for consumers seeking reliable health and nutrition solutions.

Meanwhile, the online channel has emerged as a rapidly growing segment, achieving an impressive 5.57% CAGR. This growth is fueled by the increasing adoption of auto-replenish subscription services, which provide unmatched convenience by automatically delivering products at regular intervals. These services eliminate the need for customers to place repeated orders, saving time and effort. Additionally, the online channel benefits from rapid delivery services, which ensure that consumers receive their products promptly, meeting their immediate needs. The combination of convenience, speed, and accessibility has made online platforms an attractive option for a growing number of consumers. As a result, the online channel continues to gain traction, reshaping the way health and nutrition products are purchased and consumed.

Geography Analysis

United States Dietary Supplement Market

The North America Dietary Supplements Market is dominated by the United States, which holds a commanding 77.82% share in 2025. This dominance is driven by high disposable incomes, a mature wellness culture, and a strong focus on preventive healthcare. The United States benefits from a well-established distribution network, including both online and offline channels, ensuring widespread availability of dietary supplements. Additionally, the presence of major market players and continuous product innovation, such as personalized nutrition, plant-based supplements, and functional ingredients, further strengthens its position. The growing trend of fitness and wellness, coupled with the increasing prevalence of chronic diseases, has also fueled the consumption of dietary supplements as part of a proactive approach to health management.

Mexico Dietary Supplement Market

Mexico is emerging as the growth engine of the region, with a projected CAGR of 6.61% during the forecast period of 2026-2031. This growth rate is more than double the regional average, driven by rising health consciousness, urbanization, and a growing middle-class population. Government initiatives promoting wellness and the increasing availability of affordable dietary supplements are further boosting the market. The younger population's interest in fitness and nutrition, along with the influence of social media and digital marketing, is expected to sustain growth. Additionally, the entry of international players and the expansion of local manufacturers are enhancing product availability and variety.

Canada Dietary Supplement Market

Canada also plays a significant role in the North America Dietary Supplements Market, supported by a strong regulatory framework ensuring product quality and safety. The increasing consumer preference for natural and organic products is a key driver, as consumers become more conscious of supplement ingredients. The aging population is another factor, with older adults turning to dietary supplements for age-related health concerns. The growing awareness of preventive healthcare and the popularity of e-commerce platforms are making supplements more accessible. Local manufacturers focusing on innovative offerings, such as gummies and powders, are catering to diverse consumer preferences. Together, the United States, Mexico, and Canada shape the dynamics of the North American market through distinct consumer behaviors and market trends.

Regulatory Landscape

United States: Dietary supplements fall under DSHEA and the FD&C Act. The FDA has sharpened its focus on ingredient scope, labeling, and risk-based oversight as novel inputs proliferate. A key anchor is the March 27, 2026 FDA public meeting on defining what qualifies as a dietary substance, including discussions of precision fermentation, peptides, enzymes, and microbials; comments were accepted through April 27, 2026 under docket FDA-2026-N-2047.

Canada: Health Canada continues to apply the Natural Health Products Regulations (SOR/2003-196) with labeling flexibility provided by a Ministerial Exemption Order issued in March 2025, extending labeling timelines to June 21, 2028. Across North America, cross-border compliance remains influenced by policy changes, including a 10% Section 122 import surcharge that remains in effect through July 24, 2026, shaping sourcing for vitamins, botanicals, and excipients.

Competitive Landscape

The North American dietary supplements market, presents a dynamic and competitive landscape. It features a diverse mix of global pharmaceutical giants, specialized nutrition companies, and emerging disruptors. This fragmented structure creates opportunities for niche players to target specific market segments while allowing established leaders to capitalize on their scale and resources. Segments such as gummies, plant-based formulations, and women's health are experiencing significant growth, driven by evolving consumer preferences and rapid innovation cycles. These fast-growing categories are intensifying competition as companies strive to differentiate themselves through unique offerings and advanced formulations.

Major players in the market are focusing on differentiation by emphasizing science-backed formulations and clinical validation to build consumer trust and credibility. Abbott Laboratories and Bayer AG, leveraging their strong pharmaceutical heritage, are positioning dietary supplements as integral components of broader health and wellness solutions. On the other hand, specialized nutrition companies like Glanbia and Herbalife are concentrating on performance-driven and lifestyle-oriented products to cater to specific consumer needs. This strategic positioning enables these companies to maintain a competitive edge in a market where innovation and consumer-centric approaches are critical for success.

Additionally, the market is witnessing a growing presence of private label products, particularly in the mainstream vitamin and mineral categories. These private label offerings are gaining traction among cost-conscious consumers, creating additional pressure on mid-tier brands to innovate and maintain their market share. The increasing competition from private labels is reshaping the competitive dynamics of the market, compelling established players to enhance their value propositions. As a result, the North American dietary supplements market continues to evolve, driven by a combination of innovation, consumer demand, and competitive strategies.

North America Dietary Supplement Industry Leaders

-

Abbott Laboratories

-

Amway Corp.

-

Glanbia PLC

-

Haleon PLC

-

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

North America Dietary Supplement Market Companies Covered in this Report

- Abbott Laboratories

- Amway Corp.

- Glanbia PLC

- Haleon PLC

- Bayer AG

- Nestle S.A.

- Herbalife Nutrition Ltd.

- NOW Foods

- Church & Dwight Co. (Vitafusion)

- Pharmavite LLC

- USANA Health Sciences

- GNC Holdings

- Nature's Way

- Nutraceutical International Corp.

- Jamieson Wellness

- SmartyPants Vitamins

- Plexus Worldwide

- Thorne Research

- Carlson Labs

- Standard Process Inc.

Market Opportunities and Future Outlook

Regulatory scrutiny is driving brands to pair delivery innovation with tighter compliance and transparency. Key 2026 anchors include the FDA public meeting on dietary supplement ingredients on March 27, 2026 and federal proposals such as the Dietary Supplement Listing Act of 2026 and the Dietary Supplement Regulatory Uniformity Act supported by the Council for Responsible Nutrition to standardize oversight and increase product-listing transparency.

Commercial momentum is visible in personalization and condition-specific nutrition for women, children, healthy aging, gut health, and weight management, aligned with delivery innovation and substantiation. A real-world example is Herbalife starting a phased rollout of its Pro2col digital health operating system in February 2026 to generate personalized nutrition and supplement recommendations, reinforcing online channel growth; in Canada labeling extensions to June 21, 2028 support portfolio rationalization for premium lines that rely on clearer substantiation and consistent label execution.

Recent Industry Developments in North America Dietary Supplement Market

- March 2026: Haleon published a peer-reviewed study in Nature Medicine indicating Centrum Silver may slow biological aging in older adults. The publication strengthens Haleon’s science-backed positioning in the healthy aging segment and supports premiumization strategies in vitamins, minerals, and supplements where claims substantiation is increasingly scrutinized.

- July 2025: Bayer launched a pediatric daily multivitamin line to address nutrient gaps in children, expanding its pediatric portfolio and reinforcing competition in child-focused daily nutrition. The launch aligns with dosing convenience and taste as key drivers for consumer adoption in the segment.

- June 2024: Bayer introduced One A Day Age Factor Cell Defense in the United States, targeting cellular health for consumers focused on aging. This product move reinforces the trend toward condition-specific blends and provides additional shelf presence in a category where differentiation increasingly comes from targeted benefits rather than basic multivitamins.

North America Dietary Supplement Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the North America dietary supplement market is the value of finished supplement products sold for human consumption across the United States, Canada, and Mexico, tracked across store-based and online selling routes and priced in USD.

Scope exclusions: We exclude prescription drugs, conventional packaged foods and beverages, and medical nutrition products that are primarily positioned and sold as clinical nutrition.

Segments Covered in This Report

-

By Type

- Vitamins

- Minerals

- Fatty Acids

- Protein and Amino Acids

- Prebiotic & Probiotic Supplements

- Herbal Supplements

- Enzymes

- Blended Supplements

- Others

-

By Form

- Tablets

- Capsules & Softgels

- Powders

- Gummies

- Liquids

- Others

-

By Source

- Plant-based

- Animal-based

- Synthetic/Fermentation-derived

-

By Consumer Group

- Mens

- Womens

- Kids/Childrens

-

By Health Application

- General Health & Wellness

- Bone and Joint Health

- Energy and Weight Management

- Gastrointestinal and Gut Health

- Immunity Enhancement

- Cardiovascular Health

- Diabetes Management

- Cognitive & Mental Health

- Skin, Hair and Nail Care

- Eye Health

- Other Health Applications

-

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Online Retail Channels

- Direct Selling

- Other Distribution Channels

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market guardrails and to keep definitions consistent for supplements, claims, and channels across North America. We relied on public sources such as FDA (DSHEA guidance, warning letters, and labeling rules), NIH Office of Dietary Supplements fact sheets, CDC and National Center for Health Statistics tables, and Health Canada regulatory and compliance information.

To shape the demand context, we also reviewed sources such as Statistics Canada household spending and health tables, Mexico INEGI statistical releases, and UN Comtrade trade flows for relevant ingredient and finished-product categories, where that helped explain supply movements. Company annual reports, investor presentations, and press coverage were used to confirm category priorities and distribution shifts, and paid company financials and intelligence subscription tools were applied selectively to standardize revenue proxies and ownership mapping. These sources are illustrative only, and other public and proprietary references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on cross-checking how sales move by form (capsules, powders, and gummies), which applications are driving repeat purchases, and how channel mix differs between the United States, Canada, and Mexico. We spoke with a mix of brand owners, contract manufacturers, ingredient-focused firms, distributors, and retail-facing experts, then used their inputs to tighten ASP assumptions, split product overlaps, and confirm the practical impact of regulatory actions and claim restrictions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 19% | |

| Mid tier: 47% | Functional/Unit leaders: 24% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up mix, where population, supplement usage rates, and average annual spend were combined to reconstruct the addressable revenue pool for North America, and then allocated across the United States, Canada, and Mexico based on observed consumption and channel intensity. To keep the totals realistic, we corroborated with selective bottom-up approximations, including sampled supplier and brand revenue cues, channel checks, and volume by form multiplied by an implied price band.

Key model inputs included category mix by product type (vitamins, minerals, proteins and amino acids, botanicals, and probiotics), form-factor shifts (especially gummies and powders), channel share changes between store-based and online routes, and application-led demand (immunity, gut health, energy, and weight management). Where a bottom-up signal was incomplete, we used conservative proxy splits and then stress-tested them against trade movement direction and reported company portfolio focus.

For forecasting, we ran scenario analysis using simple multivariate relationships, varying drivers such as consumer wellness intent, price and pack-size moves, and channel expansion within ranges validated through expert feedback. The final forecast was accepted only after the growth path stayed consistent with the category substitution pattern observed across forms, and with the expected pace of regulatory and claim-related constraints.

Data Validation & Update Cycle

Validation relied on triangulation across independent checks, so modeled revenue by country and by broad product families was compared against consumption indicators, company commentary, and channel-level signals. Outliers were flagged early, and assumptions were revisited when a metric moved in a direction the model could not explain using the chosen drivers.

Before sign-off, a second analyst review is completed to re-check formulas, currency handling, and the logic behind each split, and targeted re-contacts are triggered when variance remains high in a specific segment or country. Reports are refreshed annually, and interim updates are made when material events occur, including major regulatory actions, notable category disruptions, or sharp pricing swings. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's North America Dietary Supplement Market Estimate Compared With Other Published Estimates

Published market numbers for dietary supplements in North America can vary widely, even when the same countries are named, because each study sets its own product scope, pricing level, and channel cut-offs. Differences also come from how online growth rates are assumed, how gummies and blended formats are treated, and whether the model is updated after claim enforcement or category re-labeling.

Some estimates appear to include adjacent nutrition products and broader wellness items that sit next to supplements in retail data. In Mordor Intelligence, revenues are counted only for finished dietary supplement products sold for human consumption across the United States, Canada, and Mexico, with cross-checks by product type, form, and application so overlapping sales are not counted twice.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 44.79 B (2025) | |

| Industry Research Publisher A | USD 61.79 B (2024) | Uses a different base year and often aligns closer to a retail sales value view, which can lift totals when markups and a wider capture of channels are applied. Public summaries tend to be less specific on how borderline nutrition products and blended formats are separated from dietary supplements. |

| Global Advisory Publisher B | USD 64.06 B (2025) | Commonly reflects a more aggressive growth setup and may count a broader set of supplement-adjacent nutrition categories sold through similar outlets. In many cases, country splits and price progression steps are not clearly explained, which makes it harder to separate volume growth from ASP changes. |

The spread in published values is mainly explained by what gets counted as a supplement sale, what pricing level is used, and how overlaps between forms and applications are handled. By keeping inputs tied to observable usage, spend patterns, channel mix, and country allocation checks, the total stays traceable to repeatable steps and can be re-run when assumptions change.

Key Questions Answered in the Report

What is the current size of the North America dietary supplements market?

The market is valued at USD 46.68 billion in 2026 and is projected to reach USD 57.35 billion by 2031, growing at a 4.21% CAGR.

Which product category leads revenue?

Vitamins and minerals lead with 31.02% market share in 2025, reflecting long-standing consumer trust and physician endorsement.

Why are gummies gaining popularity?

Gummies combine flavor with convenience; leading to an 6.74% CAGR forecast for the format.

Which geography is growing the fastest?

Mexico is the region’s growth engine, expected to post a 6.61% CAGR through 2031, driven by a rising middle class and broader retail access.

How is regulation affecting manufacturers?

FDA reorganization and retailer-imposed third-party testing raise compliance costs but also enhance product credibility and consumer trust.

Page last updated on: