China Vitamins Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

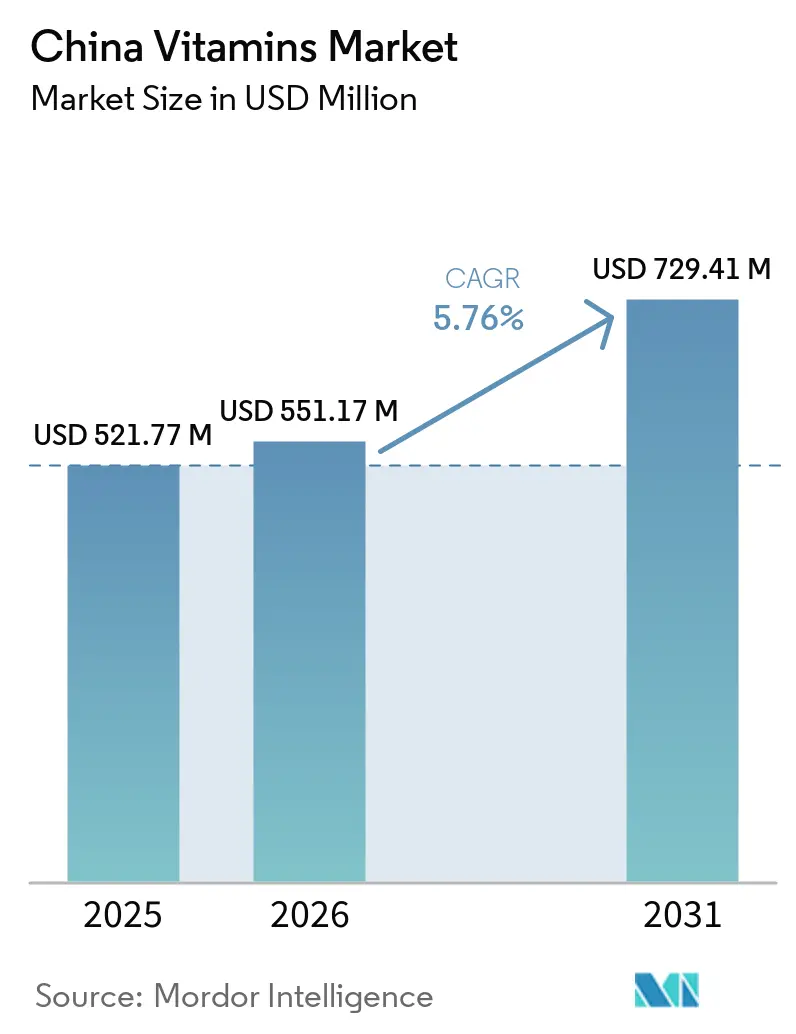

| Base Year Market Size (2025) | USD 521.77 Million |

| Market Size (2026) | USD 551.17 Million |

| Market Size (2031) | USD 729.41 Million |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Vitamins Market Analysis by Mordor Intelligence

The China vitamins market size was valued at USD 521.77 million in 2025 and estimated to grow from USD 551.17 million in 2026 to reach USD 729.41 million by 2031, at a CAGR of 5.76% during the forecast period (2026-2031). The China vitamins market is moving away from its older role as a bulk export base and is gaining more value from specialized ingredients, fortified foods, and consumer wellness products sold for daily use. China still accounts for more than 60% of global production capacity across major vitamins such as A, B, C, and E, but domestic demand is now being shaped more by preventive nutrition, premium formulations, and formal public nutrition priorities than by low-cost commodity supply alone. The February 2025 Food and Nutrition Development Guideline gave this shift stronger policy backing by framing micronutrient shortfalls as a national nutrition issue that requires wider fortification, better diet quality, and more structured nutritional support across population groups. This policy direction supports the long-term position of the China vitamins market by linking demand not only to consumer choice but also to public health, food standards, and product reformulation. At the same time, supply concentration in a limited number of vitamin clusters, recurring swings in precursor availability, and tighter claim compliance are keeping competition active and are pushing producers toward differentiated products, stronger quality systems, and more stable supply chains.

Key Report Takeaways

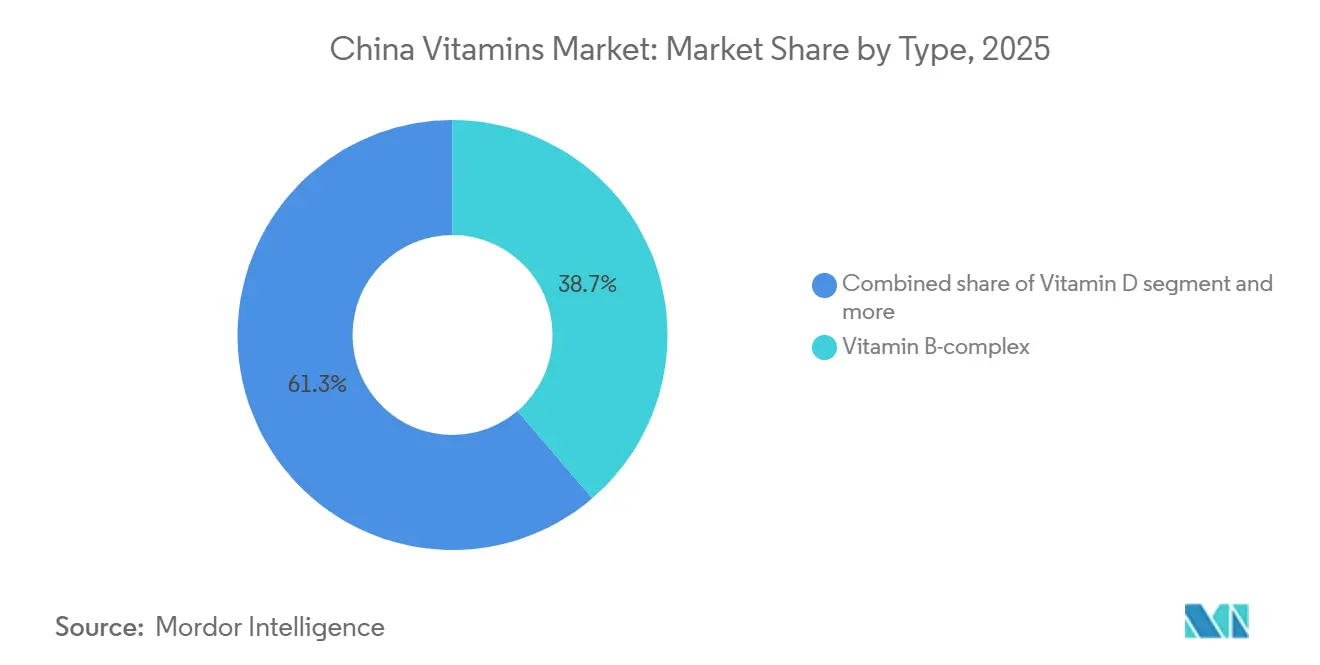

- By type, Vitamin B-complex led the China vitamin market with a 38.73% share in 2025, while Vitamin D is anticipated to register the fastest CAGR of 6.67% during 2026-2031.

- By source, synthetic vitamins held 71.56% of 2025 revenue, but natural vitamins are expected to grow fastest at 6.75% through 2031.

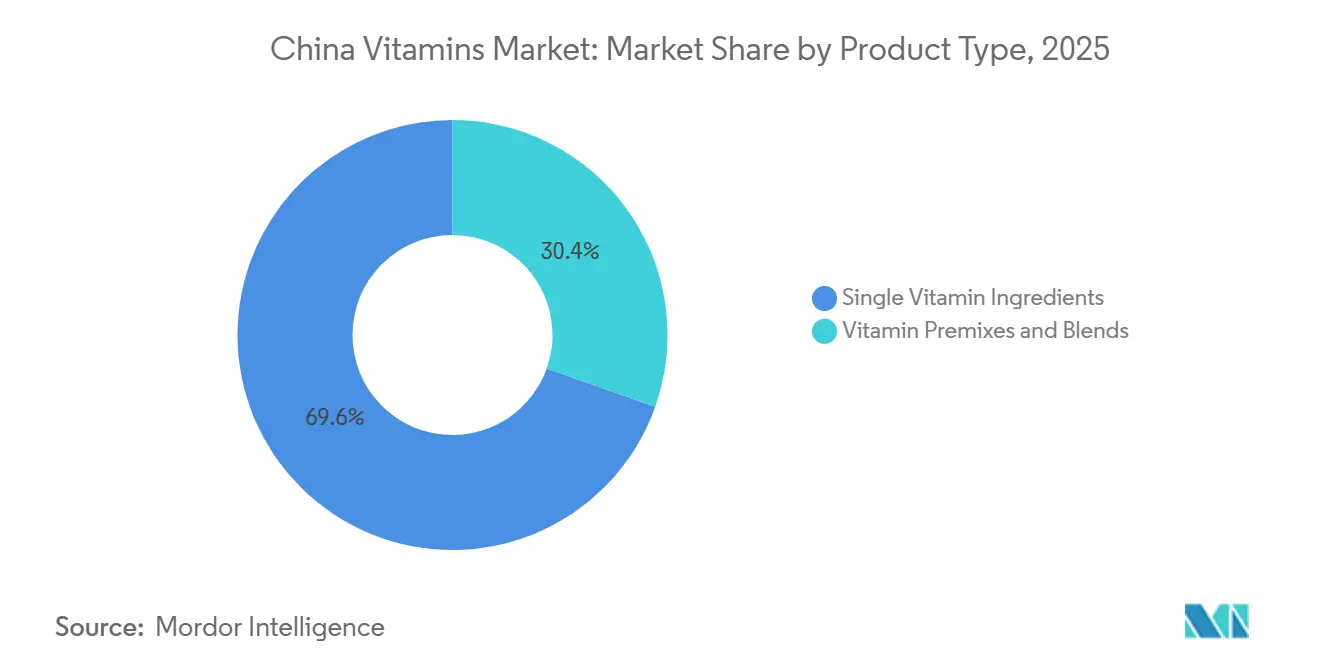

- By product type, single vitamin ingredients represented 69.58% of value in 2025, while vitamin premixes and blends are expected to grow fastest at a 6.19% CAGR through 2031.

- By form, powders held 76.36% of value in 2025, while liquids are projected to advance at a 7.38% CAGR through 2031, supported by the emergence of formal product standards for fortified vitamin beverages.

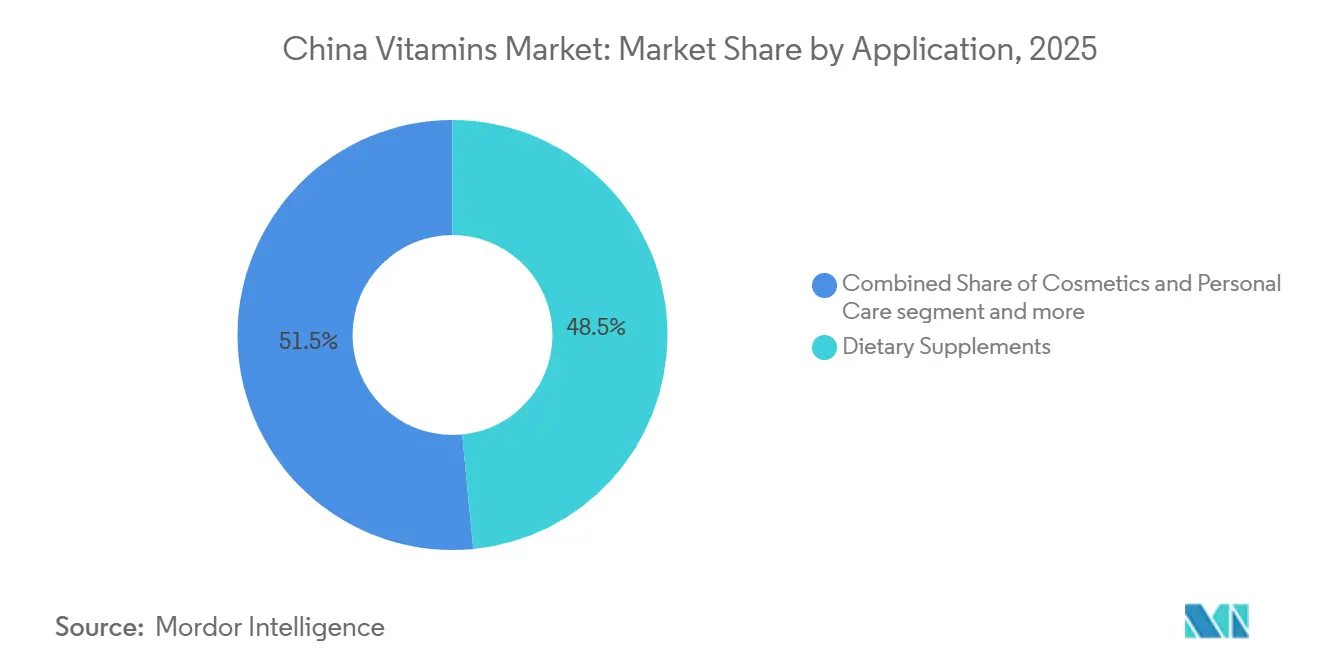

- By application, dietary supplements accounted for 48.46% of the China vitamins market size in 2025, while cosmetics and personal care are forecast to post the highest CAGR at 6.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Vitamins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Preventive Nutrition Adoption Among Urban Consumers | +1.3% | Tier-1 and Tier-2 cities (Beijing, Shanghai, Guangzhou, Chengdu, Hangzhou) | Short term (≤ 2 years) |

| Premium Demand Shift Toward Specialized Vitamin Formulations | +0.9% | National, with strongest uptake in coastal urban centers | Medium term (2–4 years) |

| Rapid E-Commerce Penetration for Daily Supplement Purchases | +1.0% | National, spilling into Tier-3 and Tier-4 cities via Douyin and Pinduoduo | Short term (≤ 2 years) |

| Government Focus on Nutrition Deficiency Reduction | +0.7% | National; with early implementation gains in rural and central provinces | Medium term (2–4 years) |

| Growth in Beauty-From-Within and Bone-Health Use Cases | +0.8% | National; skewed toward 25–45-year-old female urban consumers | Short to medium term |

| Expansion of Functional Food and Beverage Fortification | +0.6% | National, with scale concentration in Guangdong, Zhejiang, and Shandong manufacturing corridors | Medium to long term |

| Source: Mordor Intelligence | |||

Rising preventive nutrition adoption among urban consumers

Urban consumers are treating vitamin intake less as an occasional remedy and more as part of a daily health routine, and that shift is giving the China vitamins market a broader and more stable demand base. Purchase behavior is becoming more consistent because immunity, energy, bone strength, and overall wellness are now more closely tied to work pace, family care, and long-term aging concerns than before. This pattern is strongest in large cities, where consumers are more likely to compare formats, look for targeted use cases, and return for repeat purchases when a product fits a simple daily routine. The policy tone of the 2025 Food and Nutrition Development Guideline also supports this change, as it places greater emphasis on improved nutrient intake, better diet quality, and more active management of deficiency risk across population groups[1]Source: National Health Commission, “Food and Nutrition Development Guideline (2025–2030),” National Health Commission, nhc.gov.cn. As a result, the China vitamins market is gaining not only more users, but also a more disciplined purchase cycle that favors reliable supply, quality assurance, and product formats that feel easy to use every day.

Premium demand shift toward specialized vitamin formulations

Consumers are trading up from low-cost single-nutrient tablets to high-absorption, synergistic, and clinically positioned vitamin formulations, pulling average unit values upward faster than volume growth alone would suggest. The natural vitamin E premium, with natural-source products priced roughly 2× higher than synthetic equivalents, exemplifies this bifurcation, as high-end wellness buyers treat the natural/synthetic distinction as a quality signal even when bioequivalence differences are modest. The China Nutrition Society's bone nutrition division published the 2025 New Era Bone Health and Nutritional White Paper in August 2025, formally endorsing the Ca + Vitamin D + Vitamin K2 synergy protocol for children, pregnant women, and adults over 45, directly catalyzing a wave of premium multi-nutrient bone-health product launches. This clinical endorsement is migrating consumer preference from basic calcium tablets toward liquid calcium formulations with Vitamin D3 and K2 combinations, products that BY-HEALTH (汤臣倍健) launched in September 2025 exclusively on JD Health, debuting at the top of JD's all-category sales ranking on launch day.

Government focus on nutrition deficiency reduction

China's regulatory and policy apparatus is directly stimulating vitamin demand through programs targeting population-level micronutrient gaps. The Food and Nutrition Development Guideline (2025-2030), jointly issued by three ministries in February 2025, explicitly identifies vitamin A deficiency and iron deficiency anemia, particularly among children and pregnant women, as priority public health challenges requiring structured intervention. On September 4, 2025, China notified the WTO (G/SPS/N/CHN/1353) of a draft revision to the National Food Safety Standard for the Use of Food Nutritional Fortifiers (superseding GB 14880-2012), expanding approved categories of fortifiable foods and updating permitted vitamin types and dosage levels[2]Source: U.S. Department of Agriculture Foreign Agricultural Service, “Use of Food Nutritional Fortifier Draft Regulation Notified,” USDA FAS, apps.fas.usda.gov. New GB standards for fortified wheat flour (GB/T 21122-2025, effective May 2026) and vitamin A-enriched edible oils (GB/T 21123-2025, effective July 2026) signal durable regulatory tailwinds for the functional food and beverage fortification channel. A less-noticed mechanism is that the 2025 China Pharmacopeia update (effective October 2025) elevated quality thresholds for pharmaceutical-grade vitamins, effectively raising the barrier for low-cost generic producers and benefiting manufacturers with validated GMP infrastructure.

Expansion of functional food and beverage fortification

Functional food and beverage fortification is translating upstream vitamin ingredient demand into structurally recurring procurement volumes, as manufacturers lock in multi-year supply agreements rather than purchasing spot. China's functional food retail value reached CNY 4,382 billion in 2025, growing at 10.2% year-on-year, with vitamin fortification embedded across beverage, dairy, infant nutrition, and convenience food categories, according to Zhiyancha and ChinabaogaoReport, 2025. The January 2026 publication of the industry standard T/ACCEM 819-2026 for Vitamin Nutrition Water (维生素营养水) by the China Condiment Industry Association provides a product classification framework for what is becoming a distinct and rapidly growing subcategory of fortified beverages[3]Source: National Digital Standards Library, “T/ACCEM 819-2026 Vitamin Nutrition Water Standard,” National Digital Standards Library, ndls.cnis.ac.cn. The revision of the nutritional labeling standard GB 28050-2025, released March 2025 and effective January 2026, mandates declaration of fortified nutrient content and its percentage of daily reference values on prepackaged food labels, making vitamin fortification more visible to consumers and effectively creating a marketing differentiation mechanism for brands that fortify proactively.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Complexity for Health Food and Supplement Claims | -0.5% | National; disproportionate burden on small and mid-size formulators in Tier-2 and Tier-3 cities | Medium term (2–4 years) |

| Price Pressure in Commodity Vitamin Ingredients | -0.6% | National; most acute in Zhejiang, Shandong, and Jiangxi manufacturing provinces | Short to medium term |

| Consumer Skepticism Toward Homogenized Vitamin Products | -0.4% | National; higher in urban Tier-1 cities where product literacy is advanced | Medium to long term |

| Supply Chain Volatility in Imported Specialty Inputs | -0.5% | National, with highest exposure in producers reliant on imported precursors for vitamins A and E | Short to medium term |

| Source: Mordor Intelligence | |||

Regulatory complexity for health food and supplement claims

China's dual-track registration and filing system for health foods, administered by the National Medical Products Administration (NMPA) and the SAMR, imposes compliance costs that small- and mid-tier vitamin brands struggle to absorb, effectively concentrating market power among larger players with dedicated regulatory teams. The 2025 version of the China Pharmacopeia (effective October 2025) introduced more stringent quality specifications for pharmaceutical-grade vitamins, requiring costly process validations that disadvantage manufacturers without GMP-compliant facilities. SAMR's 2024 enforcement data showed a 30% year-on-year increase in penalty cases related to false health claims and non-compliant product labeling, raising legal risk for brands that rely on ambiguous functional language. The second-order constraint is time-to-market: the 5-year transition window for non-nutrient supplement health foods to comply with the 2023 permissible health function directory is forcing formulators to choose between costly reformulation and product discontinuation, disrupting product pipelines across the mid-market segment.

Supply chain volatility in imported specialty inputs

Certain high-value vitamin categories, particularly vitamins A and E, depend on specialty chemical precursors (citral, isophytol) that are produced by a limited set of global manufacturers, creating concentration risk that periodically disrupts Chinese producers' ability to maintain stable output and pricing. In 2024, a force majeure event at a European precursor supplier sharply disrupted vitamin A and E supply; by Q1 2026, these price impacts persisted, Vitamin A prices reached CNY 98,000 per tonne (up 56.80% from early 2026) and Vitamin E reached CNY 96,500 per tonne (up 73.87%), driven in part by Middle East conflict-related logistics disruptions, according to the Shanxi Securities Co., Ltd. Analyst report, DFCFW, April/May 2026. The Xiamen Kingdomway site explosion disrupted vitamin A and D3 production lines, illustrating how geographic concentration of production facilities amplifies the systemic vulnerability of China's vitamin supply chain to single-point failures. Vitamin B12 supply also tightened in 2025 after a key Ningxia-based producer halted operations, highlighting the risk of over-reliance on a limited number of fermentation-based API suppliers for water-soluble vitamins with inelastic pharmaceutical demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vitamin D Momentum Reshaping the B-Complex-Led Market

Vitamin B-complex accounted for 38.73% of the value in 2025, making it the largest type segment in the China vitamins market, while Vitamin D is projected to grow fastest at a 6.67% CAGR through 2031. B-complex has retained its lead because it serves several stable demand pools simultaneously, including pharmaceutical formulations, functional beverages, and routine nutritional products that require widely accepted, cost-effective ingredients. Its position is supported by practical use across daily wellness formats and industrial applications, which gives it broader resilience than more narrowly positioned vitamin categories. The China vitamins industry also continues to rely on B-complex as a familiar and scalable ingredient cluster, which helps explain why it remains large even as newer premium themes gain attention. At the same time, the strongest momentum is moving toward Vitamin D, driven by deficiency awareness, aging concerns, and a stronger consumer focus on bone and immune support.

Vitamin D is gaining ground because clinical evidence of deficiency provides brands and healthcare-linked channels with a clearer basis for recommendations, making the category more actionable for both families and older consumers. The China CDC study cited in the source material showed 41.2% insufficiency and 23.9% deficiency among children aged 3 to 17 across 14 provincial divisions, reinforcing the view that demand growth is tied to a real nutritional gap rather than a passing wellness theme. Vitamins C and E remain important because they continue to serve pharmaceutical, food, and personal care uses, while Vitamin A is becoming more divided between lower-margin commodity grades and more defensible high-purity uses. Vitamin K also benefits indirectly because it is increasingly discussed alongside Vitamin D in bone-support routines, which helps blended products rather than single nutrients alone. Overall, type-level competition in the China vitamins market is no longer defined only by volume scale, because the fastest growth is now moving toward vitamins linked to clear deficiency correction and targeted health outcomes.

By Source: Natural Vitamins Gaining Premium Ground Against Synthetic Dominance

Synthetic vitamins accounted for 71.56% of the value in 2025, which shows how strongly the China vitamins market still depends on scalable, cost-efficient manufacturing for mainstream supply. This dominance is consistent with China’s global production role, as synthetic routes are easier to scale and standardize, and more suitable for large-volume applications in food, feed, pharmaceutical, and supplement manufacturing. Synthetic products also remain central to categories where buyers prioritize consistent specification, price discipline, and reliable industrial output over origin-based positioning. For that reason, synthetic supply should remain the foundation of the China vitamins market through the forecast period, especially in categories tied to mass-market use and export-linked capacity. Even so, the growth pattern is shifting because natural vitamins are expected to expand at a 6.75% CAGR through 2031, which is faster than the market average.

Natural-source vitamins are gaining attention because premium consumers often read source claims as markers of quality, safety, and perceived effectiveness, even when technical differences are not always the main purchase driver. This creates a better pricing environment for companies that can prove traceability, manage natural feedstocks, and keep product consistency high enough for regulated applications and premium finished products. It also supports more value creation in the China vitamins industry because natural-source claims are easier to connect with wellness, beauty, and higher-end nutrition positioning than purely synthetic commodity output. In practice, this means natural vitamins may remain smaller in scale, but they are likely to play a larger role in margins, brand differentiation, and premium product development. The source split therefore shows a China vitamins market that still rests on synthetic scale, while increasingly rewarding natural-origin offerings where consumers are willing to pay more for a stronger quality signal.

By Product Type: Premixes Accelerating as Formulation Complexity Rises

Single-vitamin ingredients accounted for 69.58% of the 2025 value, confirming that the China vitamins market still has a strong base in core ingredient supply for industrial and pharmaceutical use. Their large share reflects the importance of purity, standardization, and high-volume manufacturing in applications where buyers require precise specifications and often formulate finished products themselves. This structure favors producers with strong upstream chemistry, fermentation, and process control because single ingredients remain the core input for a wide range of downstream products. At the same time, this large installed base also shows why product type evolution matters, because the fastest commercial gains are moving toward more integrated solutions rather than raw inputs alone. Vitamin premixes and blends are projected to grow at a 6.19% CAGR through 2031, indicating that the China vitamins market is creating more value by outsourcing formulation complexity.

Premixes are gaining because food companies, clinical nutrition brands, pet nutrition firms, and supplement manufacturers increasingly want ready-to-use nutrient systems that reduce their own blending, testing, and formulation burden. Policy support also matters here, since the nutrient supplement ingredient directory has made combination-based product development easier in some cases and has reduced part of the earlier filing friction around multi-nutrient products. This makes premixes commercially attractive because they offer not only convenience, but also a route to stronger customer stickiness and better technical service relationships. The China vitamins market therefore appears to be moving from a simple ingredient sale toward broader solution selling, where the supplier does more of the formulation work and captures more of the value. That shift will likely help integrated producers the most, especially those that can combine raw material scale with application know-how and tighter customer support.

By Form: Liquid Formats Disrupting Powder-Led Supply Structures

Powders accounted for 76.36% of the value in 2025, indicating that the China vitamins market remains overwhelmingly grounded in formats that are efficient for industrial manufacturing, bulk handling, and standardized distribution. Powdered vitamins fit well with food processing, feed, pharmaceutical, and premix applications because they store efficiently, move easily through existing systems, and support large production runs. This explains why powders remain the dominant form even though much of the visible consumer innovation is now happening elsewhere. Their scale also reflects the older structure of the China vitamins market, where bulk ingredient movement shaped the commercial model more than direct consumer convenience. Still, the fastest growth is clearly in liquids, which are projected to expand at a 7.38% CAGR through 2031 and are becoming one of the most dynamic areas of product development.

Liquid formats benefit from ease of use, more appealing consumption routines, and a stronger fit with targeted health narratives, especially in products positioned for children, women, and older adults. The formal publication of the Vitamin Nutrition Water standard in 2026 provides this shift with additional institutional support by defining classification, quality expectations, and labeling rules for a new fortified beverage subcategory. This matters because standards reduce uncertainty for product developers and encourage more investment in consumer-facing liquid formats. The China vitamins market size for powders remains much larger today, but the incremental value pool is increasingly shifting toward liquids, soft gels, and other formats that make vitamins feel easier to consume and easier to differentiate. In effect, form competition is becoming a useful way to measure where industrial volume still dominates and where consumer-led value creation is starting to take over.

By Application: Consumer Wellness Uses Continue to Set the Pace

Dietary supplements accounted for 48.46% of the value in 2025, giving them the largest application share in the China vitamins market and confirming that direct consumer wellness remains the main revenue center. This lead reflects the strength of urban self-care habits, daily repeat use, and the growing preference for products that fit simple routines focused on immunity, bone support, energy, and long-term wellness. Supplements also address many of the strongest demand drivers simultaneously, including preventive nutrition, premium formulation, online retail visibility, and more targeted product positioning. Because of this, dietary supplements remain the clearest window into how the China vitamins market is changing at the consumer level, even though food, pharmaceutical, and feed demand remain important for volume stability. The largest share, therefore, lies with the most routine and visible consumer application rather than with purely industrial channels.

Cosmetics and personal care are expected to grow fastest at a 6.55% CAGR through 2031, which shows how oral beauty and appearance-linked wellness are widening the addressable space for vitamin ingredients. This is important because it pulls vitamins C, E, and A, along with related nutrients, into a higher-value use context where consumers are often willing to pay more for perceived visible benefits and a better product experience. Food and beverages should also remain important because updated labeling and fortification rules continue to support broader product use and clearer communication of nutrient content on pack. Pharmaceuticals and animal nutrition keep the base demand broad, but the fastest movement is happening where vitamins become part of lifestyle-oriented and premium consumer products. That combination gives the China vitamins market a more balanced application mix, with industrial demand underpinning scale and consumer wellness uses driving most of the visible growth.

Geography Analysis

Eastern China remains the main production anchor for the China vitamins market because the region combines established chemical manufacturing, supporting infrastructure, supplier networks, and the operational experience needed for large-scale vitamin output. Zhejiang stands out within this structure because it hosts major participants such as Zhejiang NHU and Zhejiang Medicine, and the concentration of manufacturing capability there supports efficiency in sourcing, process control, and environmental management. This clustering matters because the China vitamins market depends not only on final vitamin synthesis, but also on a deep supporting chain of intermediates, technical expertise, utilities, and compliance systems that are difficult to rebuild quickly elsewhere. Shandong, Jiangxi, and Hebei also retain importance because they broaden the manufacturing footprint across vitamin categories and reduce the risk of relying on a single province for every major output line. Geographically, the market is still shaped by a strong East Coast production belt that serves as the operational spine of both domestic supply and export-linked manufacturing.

On the demand side, the China vitamins market is becoming more geographically balanced, but consumption is still strongest in coastal urban regions where income levels, health awareness, and online product access are higher. East China and South China remain the most mature consumer zones because they combine stronger purchasing power with faster adoption of premium supplements, convenient formats, and targeted wellness products. North China also has a meaningful role, especially in categories linked to bone support and general deficiency awareness, while central and western regions represent a larger catch-up opportunity as online retail and public nutrition programs extend access. The 2025 Food and Nutrition Development Guideline supports this wider spread because it approaches deficiency reduction as a national issue rather than a narrow urban theme, which should help demand deepen beyond the highest-income cities over time.

Geography also matters in the China vitamins market because the country’s production map is tied to global precursor flows and international company investment decisions. BASF’s start-up of first products at its Zhanjiang Verbund site in Guangdong in November 2025 adds a major specialty chemical node in South China and strengthens the local supply foundation for citral and vitamin value chains. That complements the established eastern clusters and shows that the market is not static, because new investment is gradually widening the strategic importance of southern coastal provinces as well. The result is a geography where eastern provinces remain the core manufacturing base, coastal cities remain the most developed consumer markets, and new specialty investment is making the national footprint of the China vitamins market broader and more resilient.

Competitive Landscape

The China vitamins market has a moderately concentrated upstream structure, with a small group of producers shaping supply conditions across major vitamin categories, while downstream branded supplements remain much more fragmented. Zhejiang NHU, Zhejiang Medicine, CSPC, and Xiamen Kingdomway are central to this structure because they operate at scale, with technical depth, and hold supply chain positions that influence both domestic availability and export economics. The strongest players are not competing only on output volume, because they are also building advantages in process know-how, patent portfolios, compliance systems, and broader nutrition ingredient capabilities. NHU is a good example, with a large patent portfolio and overseas research and development centers that demonstrate a strategy focused on maintaining technical relevance rather than relying solely on commodity scale. This makes the China vitamins market competitive in a layered way, where the ingredient tier is relatively concentrated, but the branded retail tier still allows newer consumer-facing players to challenge older names.

Strategic moves by major companies show where competition is heading. BASF’s launch of production at the Zhanjiang Verbund site in Guangdong is important because it strengthens the precursor base that supports vitamins A and E and gives the company a deeper local position in the broader specialty chemical chain tied to the China vitamins market. DSM-Firmenich’s divestiture of its Jiangshan Vitamin C plant in 2024 points in the opposite direction, showing a deliberate move away from commodity exposure and toward higher-differentiation nutrition positions. These actions suggest that scale alone is no longer enough, because global and domestic companies are increasingly choosing either deeper integration into strategic inputs or sharper focus on premium and specialized categories.

Competition is also being shaped by companies that can link manufacturing credibility with broader market access. Kingdomway’s profile highlights a vertically integrated chain spanning coenzyme Q10 and natural beta-carotene production, along with international manufacturing capabilities, which supports its position in both premium export markets and higher-trust domestic channels. NHU’s 2026 approval for synthetic anethole is not a vitamin expansion by itself, but it shows how leading firms are widening their ingredient portfolios so that they are less exposed to single-category pricing cycles. In practice, the competitive edge in the China vitamins market now comes from a mix of integration, application breadth, compliance readiness, and the ability to move beyond bulk molecules into more defensible nutrition solutions. That is why the market remains moderately concentrated in supply, but still open enough for differentiated players to gain ground where quality, specialization, and strategic positioning matter more than volume alone.

China Vitamins Industry Leaders

Zhejiang NHU Co., Ltd.

Zhejiang Medicine Co., Ltd. / ZMC

CSPC Weisheng Pharmaceutical / CSPC Pharmaceutical Group

Xiamen Kingdomway Group Co., Ltd.

Jiangxi Tianxin Pharmaceutical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Zhejiang Medicine Co. (ZMC) registered the CNY 1.685 billion (approximately USD 237.77 million) Changbei Bio project in Hangzhou Bay for the production of 17,000 tonnes per year of vitamin precursors and derivative series products; construction is planned from January 2026 through December 2028.

- November 2025: BASF commenced production of the first products from the core of its Zhanjiang Verbund site in Guangdong, China, the company's single largest investment at approximately EUR 8.7 billion. The Zhanjiang site's C4-based value chain includes a new citral production facility directly supporting BASF's vitamin A and E ingredient supply.

- September 2025: BY-HEALTH (汤臣倍健) launched a multi-SKU high-content Vitamin K2 liquid calcium series exclusively on JD Health, debuting at No. 1 on JD's all-category sales ranking on launch day. The range features segment-specific formulations for children, pregnant women, and adults over 45, advancing the clinical positioning of Vitamin K2 for bone health.

China Vitamins Market Report Scope

Vitamins are essential micronutrients used as functional ingredients in food, beverages, supplements, pharmaceuticals, animal nutrition, and personal care formulations to support health and product functionality. The China vitamins market is focused on vitamin ingredients and is segmented by type, source, product type, form, and application. By type, the market includes vitamin A, vitamin B-complex, vitamin C, vitamin D, vitamin E, vitamin K, and other vitamins. Based on the source, the market is categorized into synthetic and natural vitamins, with natural vitamins further segmented into plant-derived and animal-derived sources. By product type, the market covers single vitamin ingredients and vitamin premixes and blends. Based on form, the market includes powders, liquids, and other forms. By application, the market is segmented into food and beverages, dietary supplements, animal feed and pet nutrition, pharmaceuticals, and cosmetics and personal care, covering the use of vitamin ingredients across industrial and commercial formulations. The report analyzes the China vitamins ingredients market size and forecasts across these segments. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Vitamin A |

| Vitamin B-complex |

| Vitamin C |

| Vitamin D |

| Vitamin E |

| Vitamin K |

| Others |

| Synthetic | |

| Natural | Plant Derived |

| Animal Derived |

| Single Vitamin Ingredients |

| Vitamin Premixes and Blends |

| Powders |

| Liquids |

| Others |

| Food and Beverages |

| Dietary Supplements |

| Animal Feed and Pet Nutrition |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| By Type | Vitamin A | |

| Vitamin B-complex | ||

| Vitamin C | ||

| Vitamin D | ||

| Vitamin E | ||

| Vitamin K | ||

| Others | ||

| By Source | Synthetic | |

| Natural | Plant Derived | |

| Animal Derived | ||

| By Product Type | Single Vitamin Ingredients | |

| Vitamin Premixes and Blends | ||

| By Form | Powders | |

| Liquids | ||

| Others | ||

| By Application | Food and Beverages | |

| Dietary Supplements | ||

| Animal Feed and Pet Nutrition | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

Key Questions Answered in the Report

What is the 2031 value outlook for vitamins in China?

The China vitamins market is forecast to reach USD 729.41 million by 2031, rising from USD 551.17 million in 2026 at a 5.76% CAGR.

Which vitamin type has the strongest current position?

Vitamin B-complex held the largest share at 38.73% in 2025 because it serves pharmaceutical, beverage, and daily nutrition uses across a broad application base.

Which vitamin category is growing fastest in China?

Vitamin D is projected to grow at a 6.67% CAGR through 2031, supported by documented deficiency levels and stronger demand for bone and immune support.

Why are liquids becoming more important in vitamin products?

Liquids are forecast to grow at a 7.38% CAGR because they offer easier consumption, stronger premium appeal, and a better fit with targeted wellness routines.

What is driving long-term demand in this space?

Preventive nutrition, fortification policy, premium formulations, online access, and demand linked to bone health and beauty support are the main long-term growth factors.

Page last updated on: