Executive Compensation Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

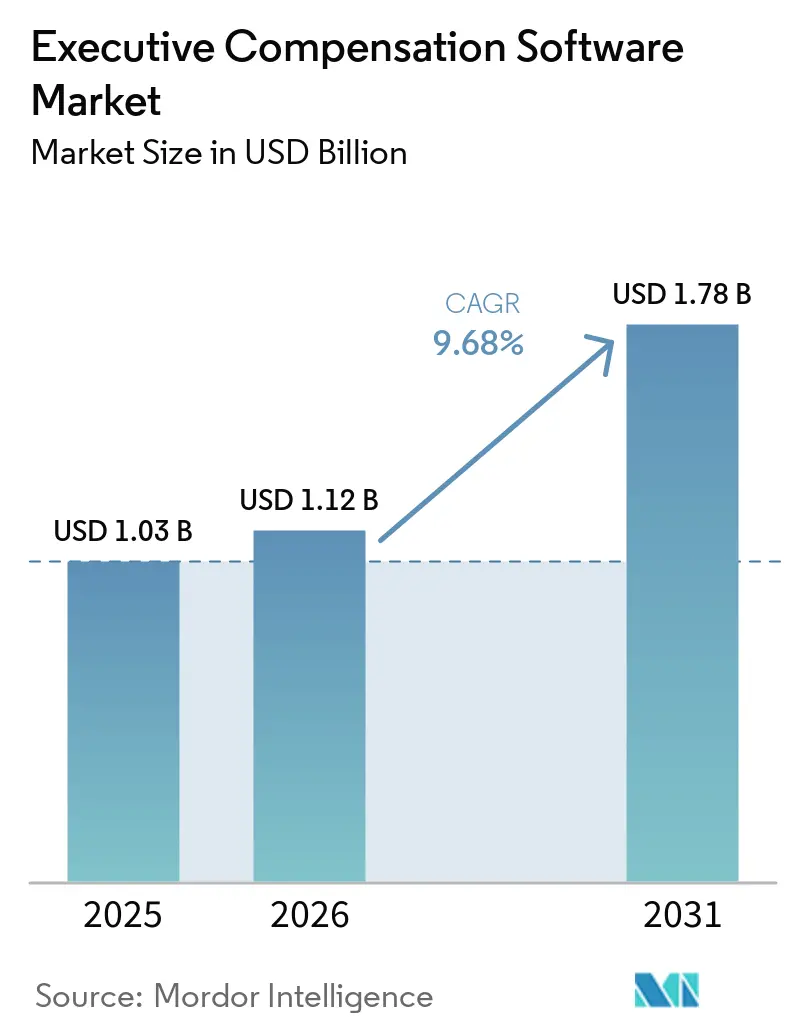

| Market Size (2026) | USD 1.12 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 9.68% CAGR |

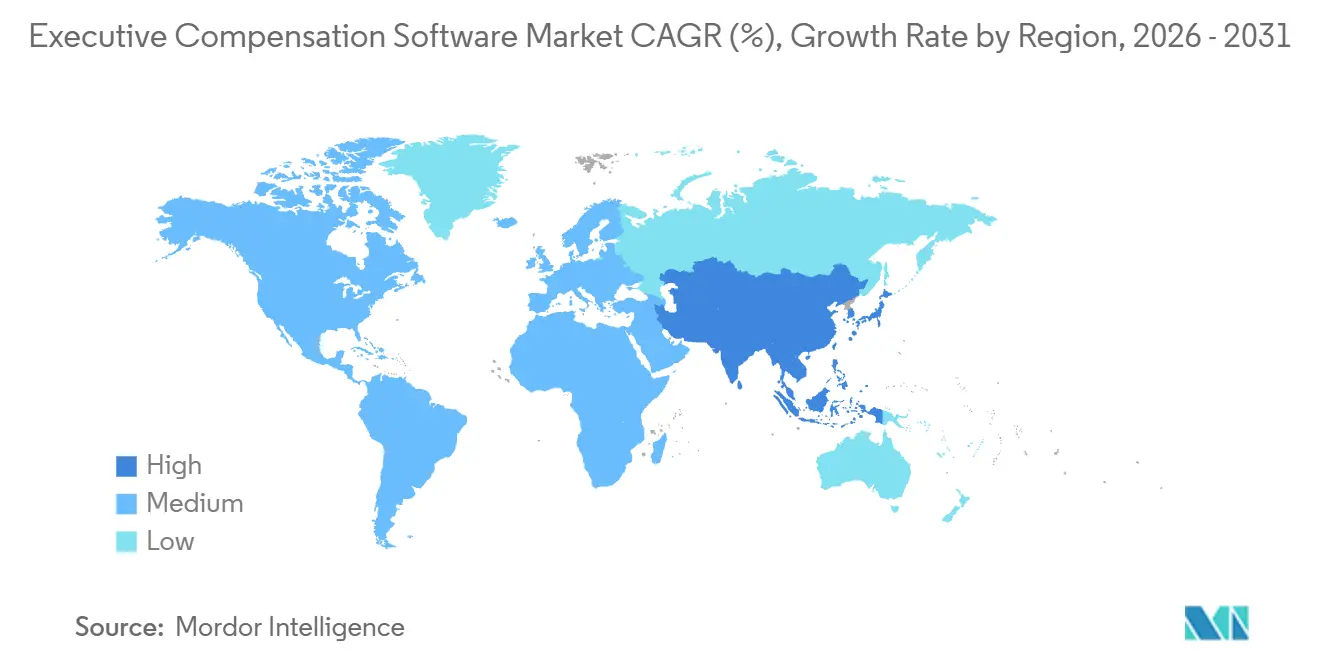

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Executive Compensation Software Market Analysis by Mordor Intelligence

The executive compensation software market was valued at USD 1.03 billion in 2025. It is forecast to reach USD 1.12 billion in 2026 and expand to USD 1.78 billion by 2031, registering a CAGR of 9.68% over the 2026-2031 period. The executive compensation software market is being shaped by a clear shift in how pay decisions are governed, as executive pay now sits closer to board oversight, disclosure risk, and regulatory review than to routine HR processes. Expanding pay transparency rules in the United States, the EU Pay Transparency Directive, and the SEC Pay versus Performance regime are pushing employers to replace periodic manual tracking with systems that can support continuous recordkeeping and defensible reporting. That change is turning one-time compliance work into recurring subscription demand, and it is also raising the value of implementation, integration, and advisory support when employers build compensation workflows for the first time. The executive compensation software market also benefits from a widening buyer base, since large enterprises still account for most spending, while cloud delivery and modular pricing are bringing more mid-sized employers into formal compensation governance. Another near-term opening for vendors comes from readiness gaps, because many employers still lack structured pay data and may need additional investment if disclosure rules or proxy reporting requirements change again.

Key Report Takeaways

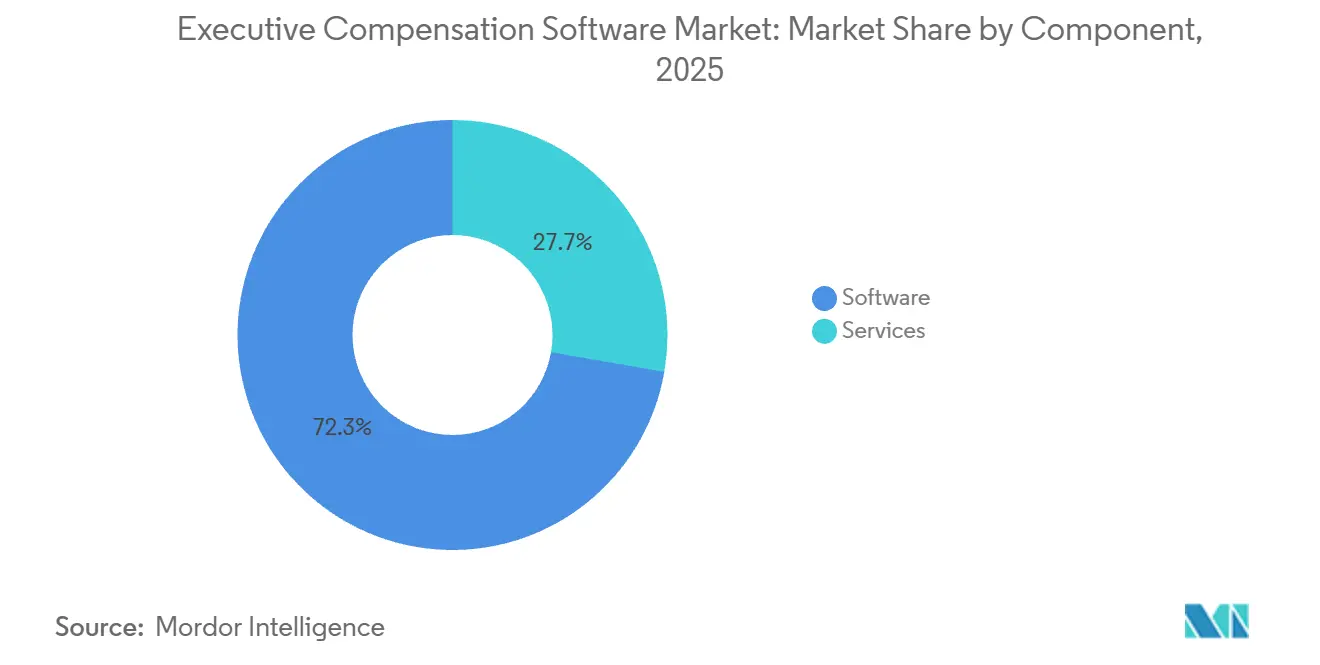

- By component, software held 72.18% of revenue in 2025 of the executive compensation software market, while services is projected to expand at a 10.42% CAGR through 2031.

- By deployment model, cloud-based deployment accounted for 75.44% of revenue in 2025 and is also the fastest-growing model, with a 10.11% CAGR through 2031.

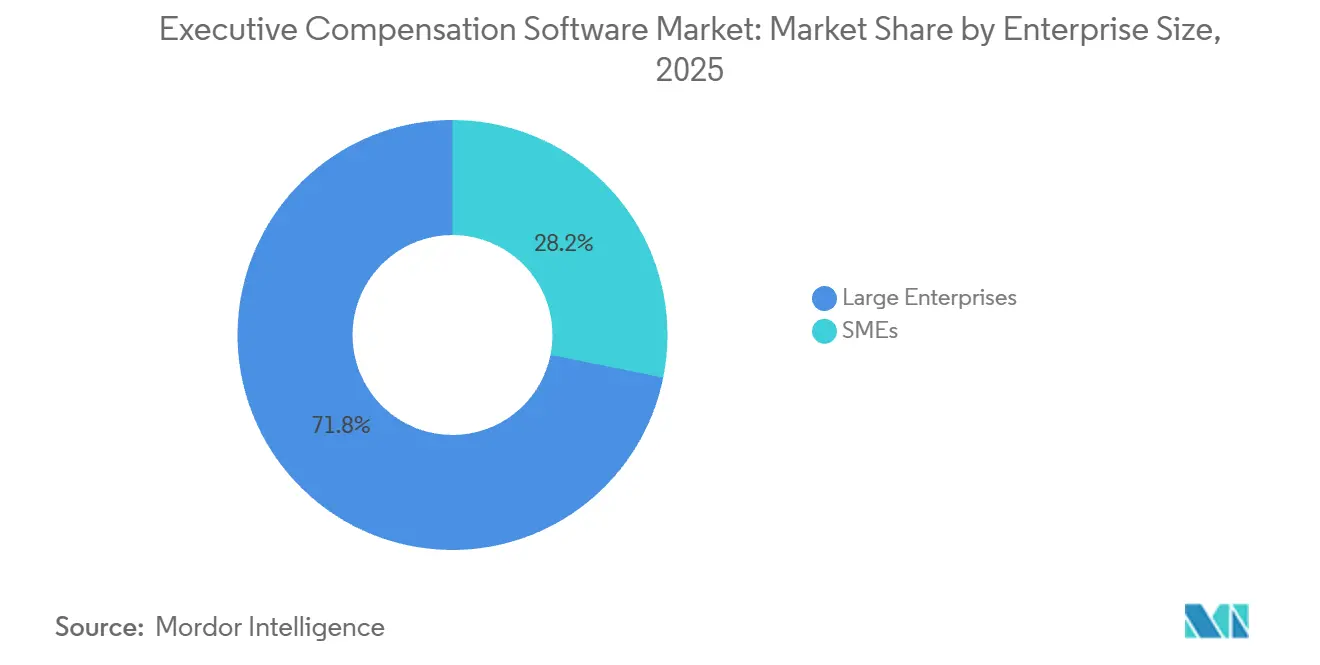

- By enterprise size, large enterprises captured 71.82% of spending in 2025 of the executive compensation software market, while SMEs recorded the highest projected CAGR at 10.86% through 2031.

- By end-user industry, BFSI represented 25.61% of revenue in 2025, while healthcare and lifesciences is forecast to grow at a 10.54% CAGR through 2031.

- By geography, North America held 41.38% of revenue in 2025, while Asia-Pacific is projected to expand at an 11.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Executive Compensation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Pay Transparency and Pay Equity Regulation | +3.2% | Global, with highest intensity in North America and EU | Short term (≤ 2 years) |

| Shift to Audit-Ready Governance from Spreadsheets | +2.4% | Global | Medium term (2-4 years) |

| Cloud-Native Integration with HCM and Finance Systems | +1.8% | Global, with early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Demand for Benchmarking and Retention-Focused Pay Decisions | +1.3% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| SEC Pay Versus Performance and Disclosure Automation | +0.9% | North America, with spillover to cross-listed firms globally | Short term (≤ 2 years) |

| ESG-Linked and Risk-Adjusted Long-Term Incentive Complexity | +0.6% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Pay Transparency and Pay Equity Regulation

Pay transparency rules have moved beyond voluntary practice and into mandatory operating requirements for many employers in the executive compensation software market. As of 2026, 16 US states and Washington, D.C., required salary range disclosure in job postings, and several additional state laws became effective across 2025, which widened the number of employers that had to manage live pay range data across recruiting and rewards workflows. The EU Pay Transparency Directive requires member-state transposition by June 7, 2026, and it sets up annual reporting obligations for employers with 250 or more employees from 2027 using 2026 baseline data, which pulled software planning into the current year rather than a later compliance window.[1]Erika C. Collins and Brooke Razor, “What US Employers Need to Know About the EU Pay Transparency Directive,” Faegre Drinker Biddle and Reath LLP, faegredrinker.com This has changed the buying case in the executive compensation software market, because employers need centralized records, role-based access, and evidence that pay decisions can be explained under review. Multinational employers also face a cascade effect, since hiring into one covered location can force broader policy and data changes across shared compensation systems. That is why regulatory change now supports recurring platform usage instead of a one-off compliance spend.

Shift from Spreadsheet-Led Planning to Audit-Ready Governance

Boards and compensation committees are applying a different standard to executive pay workflows, and that is lifting the executive compensation software market beyond a productivity narrative. Spreadsheet-led planning still works for narrow annual exercises, but it breaks down when employers need multi-level approvals, version history, exception tracking, and evidence that decisions followed policy. A 2026 Silae analysis of 6.7 million payslips found an average executive pay gap of 13.37%, with the gap rising above 45% in financial and insurance activity and widening sharply over the span of a career, which shows how hard it is to detect structural gaps without organized data. beqom reported that 38% of European companies viewed their current systems as inadequate for incoming EU requirements, which points to a readiness gap that extends well beyond headline compliance awareness. The executive compensation software market gains from this shift because governance risk now matters as much as cycle efficiency when employers choose a platform. Vendors that embed approvals, audit trails, and controlled workflows into compensation planning are, therefore, better placed to win enterprise buying decisions.

Cloud-Native Integration with Human Capital Management and Finance Stacks

Integration depth has become a strong purchase filter in the executive compensation software market because compensation decisions rely on current data from HRIS, payroll, ERP, and, in some cases, equity administration systems. Salary.com added a native Paycom connection in January 2026 and extended its list of major HRIS integrations, which reduced manual data handling and helped buyers link compensation planning to a broader system of record. Workday also launched its AI-powered Pay Transparency Analyzer in pilot form with Kainos in October 2025, offering country-specific compliance reports that tie pay transparency work into the existing HCM environment. Payscale reported in 2026 that 75% of executives now frequently request compensation data for strategic decisions, which means HR and finance teams need information that is available in current workflows rather than through delayed manual extracts. In the executive compensation software market, that requirement lifts the value of pre-built connectors and lowers the appeal of platforms that still depend on heavy reconciliation work. It also raises switching costs after implementation, because once data flows are embedded across systems, the platform becomes part of a wider governance process rather than a stand-alone tool.

Rising Demand for Market Benchmarking and Retention-Driven Pay Decisions

Buyer expectations are rising in the executive compensation software market because annual survey data is no longer enough for boards and HR leaders making pay decisions in fast-moving labor markets. Pave stated that its platform manages more than USD 190 billion in total compensation across more than 8,300 companies, and its July 2025 Google Cloud partnership added predictive compensation intelligence through Vertex AI and Gemini models. Equilar reported that median CEO compensation reached USD 29.4 million in 2025, up 23.2% year over year, with stock award values rising 38.8%, which raised the need for reliable peer benchmarking and defensible committee decisions.[2]Amit Batish, “An Early Look at the Highest-Paid CEOs in 2025, Equilar 100,” Equilar, equilar.com Pave and Infinite Equity also found a median net equity burn rate of 3.9% among AI-native private companies, nearly 40% above non-AI technology peers, which shows how quickly equity benchmarking needs can shift in talent-heavy sectors. The executive compensation software market, therefore, benefits from a premium on current benchmarking because retention and executive hiring decisions now require more frequent recalibration than older survey cycles can provide. Vendors with direct system integrations and faster benchmark refresh cycles are taking advantage of that demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration and Implementation Costs Across HRIS, Payroll, And ERP | -0.7% | Global, with highest friction in Asia-pacific and South America | Medium term (2-4 years) |

| Sensitive Pay Data Privacy and Cybersecurity Exposure | -0.5% | Global | Short term (≤ 2 years) |

| Survey Data Fragmentation and Weak Job Architecture | -0.3% | Global, most acute in emerging markets | Long term (≥ 4 years) |

| Cross-Functional Approval Bottlenecks Across HR, Finance, Legal, And Boards | -0.2% | Global, with highest complexity in large multinational enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration and Implementation Costs Across HRIS, Payroll, And ERP

Implementation complexity remains a real brake on the executive compensation software market, especially for buyers moving from spreadsheets to a formal platform for the first time. These deployments often require deep links into HRIS, payroll, ERP, and equity systems, and the work extends beyond technical setup into approvals design, job architecture, security permissions, and change management. In practice, organizations also need to reconcile compensation data that sits across multiple source systems, which adds time and service cost before the platform can support reliable planning or reporting. This burden is heavier in the executive compensation software market for SMEs and first-time buyers, because they usually have fewer internal IT and compensation specialists available to structure the rollout. The continued 10.42% CAGR for services through 2031 reflects that demand for configuration, integration, and support, and it also shows that adoption intent is often stronger than implementation readiness. ISG Software Research noted that platforms without pre-built connectors to major HRIS vendors risk exclusion from enterprise procurement, underscoring why integration readiness has become a gating factor in vendor selection.

Sensitive Pay Data Privacy and Cybersecurity Exposure

Data security concerns limit the executive compensation software market because executive pay records contain some of the most sensitive personal and financial information held by an employer. A 2025 breach at VeriSource Services exposed personal data tied to nearly 4 million people, and the time taken to understand the full scope illustrated how long operational disruption can last after an HR-related incident. Workday also confirmed a breach in August 2025 involving a third-party customer relationship database, which arrived at a time when many employers were increasing scrutiny of cloud-hosted compensation workflows. Buyers in BFSI and healthcare often respond by applying financial-grade vendor reviews that include SOC 2 Type II, ISO 27001, and GDPR-oriented control expectations, which extend sales cycles and narrow the field of acceptable providers. The executive compensation software market feels this restraint most clearly when buyers want AI-enabled pay tools, because the EU AI Act adds another layer of documentation, logging, and risk-management requirements from 2026 onward. As a result, vendors need stronger security programs simply to stay eligible for larger enterprise opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals an Implementation Complexity Premium

Software held 72.18% of the executive compensation software market share in 2025, which kept it as the largest component by a wide margin. That dominance reflects the installed base of platforms already used for compensation planning, benchmarking, pay equity analytics, and disclosure support across larger employers. The software layer remains central in the executive compensation software market because once core modules are deployed, additional users and process extensions can be added with limited incremental delivery cost. It also allows employers to standardize approval paths, scenario modeling, and reporting across compensation cycles that would otherwise sit in separate files and emails. This structural advantage explains why software still anchors revenue even as buyer expectations become more demanding.

The services side of the executive compensation software market is still projected to grow faster, at a 10.42% CAGR through 2031, because implementation work remains intensive. Many buyers underestimate the effort needed to build audit-ready records from fragmented payroll, HRIS, and equity data, and that gap creates recurring demand for configuration and post-go-live support. A second factor is the maturity gap within internal compensation teams, because Payscale found in 2026 that only 45% of organizations had reached an advancing or optimizing state in compensation maturity. That means the executive compensation software industry still depends on outside expertise to convert platform features into controlled governance processes. The result is a market where software provides the revenue base, while services absorb the operational complexity that new buyers and late-stage adopters still struggle to manage.

By Deployment Model: Cloud Consolidates its Lead While On-Premises Holds in Regulated Segments

Cloud-based deployment accounted for 75.44% of revenue in 2025, and it remains both the largest and fastest-growing deployment model with a 10.11% CAGR through 2031. The executive compensation software market favors cloud delivery because compensation planning usually involves HR, finance, legal, and board participants who need access to the same current records across review cycles. This model also supports quicker product updates when reporting rules or pay transparency requirements change. Employers can therefore move from periodic updates to more continuous governance without rebuilding local infrastructure. That convenience has made cloud delivery the default option for the commercial mainstream of the executive compensation software market.

On-premises and private cloud options still hold value in specific regulated settings, particularly in BFSI and government environments where data residency and supervisory expectations remain strict. Germany’s IVV 5.0 framework strengthened the need for documented variable pay controls, multi-year deferral, and malus or clawback tracking in credit institutions, which keeps some banks cautious about fully public cloud deployment.[3]Marcus Michel, “BRUBEG, IVV 5.0 und Entgelttransparenz, Vergütung neu steuern,” FCH AG, fch-gruppe.de That makes the executive compensation software market more nuanced than a simple cloud-only story, because regulated buyers often prefer hybrid configurations that preserve control over the most sensitive records. Vendors with only a basic SaaS offer can still win broad commercial business, but they may struggle in tightly supervised segments. The executive compensation software industry therefore continues to reward cloud-first design while still leaving room for vendors that can support private or hybrid deployment models for complex buyers.

By Enterprise Size: SME Acceleration Reflects Cloud Economics and Regulatory Reach

Large enterprises captured 71.82% of spending in 2025, which reflects the heavier governance demands attached to global workforces, long-term incentive programs, and public disclosure obligations. These organizations have been the natural buyers in the executive compensation software market because they manage more executive layers, more jurisdictions, and more formal committee structures than smaller employers. Their requirements often include SEC proxy support, cross-border pay range control, and board benchmarking, all of which push them toward purpose-built systems. They also have the budgets to absorb integration and advisory work during rollout. This kept large enterprises firmly in the lead on current spend.

The faster growth is coming from SMEs, which are projected to expand at a 10.86% CAGR through 2031 as the executive compensation software market reaches employers that previously relied on manual tools. Pay transparency laws have widened the regulatory net, and some state rules apply at relatively low employee thresholds, which means smaller employers are entering formal compliance cycles sooner than expected. Cloud-native vendors have responded with modular pricing and lighter benchmark products that reduce entry cost for mid-market buyers. Pave’s Market Data Lite offer for companies with 1 to 200 employees illustrates a land-and-expand model built around low-cost benchmark adoption before broader planning and pay equity needs emerge. The executive compensation software market is therefore broadening at the lower end not because the work is simpler, but because affordable delivery models are finally matching the needs of smaller employers.

By End-User Industry: BFSI Anchors Volume While Healthcare and Lifesciences Accelerate

BFSI represented 25.61% of revenue in 2025, making it the largest end-user segment in the executive compensation software market. That position reflects a heavy regulatory load, because financial institutions need to manage material risk taker identification, deferred incentives, malus and clawback rules, and public disclosure expectations in a controlled way. Banks and insurers also face closer scrutiny of how pay links to risk and long-term performance, which increases the value of audit trails and formal approvals. WTW reported that ESG metrics were present in more than 90% of European listed company executive plans and that nearly 70% of those plans used quantitative ESG targets, which adds further design and tracking complexity. In the executive compensation software market, BFSI remains the clearest example of a segment where purpose-built software is closer to a necessity than an optional efficiency tool.

Healthcare and lifesciences is forecast to grow at a 10.54% CAGR through 2031, making it the fastest-growing end-user category. The demand comes from a more formal approach to physician and executive pay, where value-based care, fair market value concerns, and internal pay governance need to be balanced in a documented process. Arthur J. Gallagher introduced a dedicated health plan compensation survey for executive and manager roles in its 2026 healthcare compensation survey cycle, which signals a broader formalization of pay structures in this field. That backdrop supports the executive compensation software market as healthcare employers move toward stronger benchmarking, approval discipline, and role-based compensation controls. Other end users, including IT and telecom, retail and e-commerce, manufacturing, and government, still add meaningful demand through AI talent benchmarking, variable incentive automation, and pay reporting workstreams.

Geography Analysis

North America held 41.38% of the executive compensation software market size in 2025, which made it the largest regional contributor. The region benefits from the concentration of SEC-reporting issuers, an active pay equity legal environment, and widespread use of equity-heavy executive pay structures. In the United States, the executive compensation software market is supported by overlapping requirements that cover SEC Pay versus Performance disclosure, state salary range posting, and clawback-related governance. Canada and Mexico add to regional demand through cross-border governance alignment, especially among multinational employers that want common compensation controls across North American operations.

Asia-Pacific is projected to grow at an 11.76% CAGR through 2031, giving it the fastest regional trajectory in the executive compensation software market. Growth is coming from digital HR modernization in Indian and Southeast Asian firms, stronger executive remuneration oversight in Japan, and expanding multinational payroll governance across China, Singapore, and South Korea. Ravio’s 2026 Compensation Trends report recorded 88% year-over-year growth in AI and ML hiring across Asia-Pacific and European tech markets, with those roles carrying 12% pay premiums, which raises the need for faster benchmark refresh and structured pay decisions.[4]“Compensation Trends 2026, a report by Ravio,” Ravio, ravio.com HRSoft also indicated that APAC, EU, and Middle East financial services verticals were among its fastest-growing customer acquisition areas, reinforcing the region’s momentum in more regulated compensation environments.

Europe remains a high-intensity regulatory region in the executive compensation software market, and it is pulling adoption forward across both large enterprises and parts of the mid-market. The first reporting cycle tied to 2026 data under the EU Pay Transparency Directive is turning general compliance awareness into active procurement work in 2026. Germany adds another layer through IVV 5.0 and related governance expectations for credit institutions, which require more integrated HR, compliance, and risk data in executive pay oversight. South America is still earlier in adoption, while the Middle East and Africa demand is more concentrated among regional headquarters and multinational subsidiaries that need group-level compensation consolidation rather than a fully localized platform footprint.

Competitive Landscape

The executive compensation software market remains fragmented, with no single provider controlling the full competitive field. Competition spans specialist executive compensation vendors, broader total compensation platforms, pay equity and transparency providers, and benchmarking-focused entrants. That mix keeps pricing and product development active, because buyers can choose between deep specialist functionality and wider HCM adjacency depending on their use case. The executive compensation software market is therefore not defined by a single dominant model, but by several overlapping product approaches that continue to converge around governance, analytics, and workflow control. Vendors are now differentiating less on basic planning features and more on integration depth, AI support, security posture, and their ability to fit regulatory use cases.

Several strategic moves show where the executive compensation software market is heading. Salary.com launched Max in March 2026 as an AI layer that combines salary surveys, job posting signals, and enterprise data, pointing to more automated pre-cycle and post-cycle analysis. HRSoft followed its 2025 HRSoft Intelligence launch with a majority investment from Gryphon Investors in April 2026, which strengthened its position as a better-capitalized challenger focused on product expansion and M&A. Syndio launched Syndi in October 2025 with workflow integrations in Microsoft Teams, Slack, and ATS systems, which shows how vendors are pushing compensation decisions closer to the point of action rather than relying on separate platform sessions.

Real-time data architecture is another major line of competition in the executive compensation software market. Ravio and Pave have built benchmark models that draw directly from customer HRIS and equity systems, which reduces the lag associated with traditional survey-based datasets. Workday’s Pay Transparency Analyzer also reflects how large HCM vendors are folding compensation governance into existing enterprise software estates rather than leaving the function to separate tools. At the same time, the executive compensation software market has clearer category boundaries than some adjacent pay tools, because sales commission platforms such as CaptivateIQ, Xactly, Everstage, QuotaPath, and SalesCrew focus on frontline sales incentives rather than board governance, LTI design, proxy disclosure, or pay equity analysis. More relevant adjacent platforms for expansion and substitution include Trusaic, Workiva, Ledgy, Carta, Figures, and Anaplan, which connect more directly to executive pay governance or equity administration. Across all these groups, enterprise security expectations such as SOC 2 Type II and ISO 27001 are setting a minimum procurement standard that can exclude vendors before product fit is even considered.

Executive Compensation Software Industry Leaders

Salary.com, LLC

Payscale, Inc.

beqom SA

Equilar, Inc.

HRsoft, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Equilar published its Q1 2026 Gender Diversity Index and a dedicated analysis of companies disclosing executive pay impacts of tariff-related business disruptions, expanding its benchmarking data set for governance professionals navigating macroeconomic uncertainty in compensation design.

- April 2026: Payscale launched its Intelligence Cloud, a unified suite integrating Payfactors, Marketpay, and Paycycle, designed to deliver contextual compensation intelligence across manager, talent leader, finance, and executive personas simultaneously, based on findings that 75% of executives now regularly request compensation reporting.

- April 2026: Salary.com unveiled Max, a purpose-built AI model featuring autonomous agents and real-time market intelligence within its CompAnalyst AI Suite, reducing multi-week benchmarking and pay structure tasks to minutes and supporting over 10,000 organizations across 140+ countries.

- April 2026: HRSoft announced a majority investment from Gryphon Investors, following the appointment of Larry Dunivan as Executive Chair, with the transaction designed to accelerate product innovation, expand the enterprise customer footprint, and pursue strategic M&A in compensation lifecycle management.

Global Executive Compensation Software Market Report Scope

The executive compensation software market refers to the global market for software platforms and associated services designed to manage, administer, analyze, govern, and optimize compensation programs for senior executives, board members, leadership teams, and key managerial personnel within organizations. These platforms enable enterprises to automate executive pay planning, long-term incentive management, equity compensation administration, performance-linked reward structures, regulatory disclosures, and compensation governance processes while ensuring transparency, compliance, and alignment with corporate performance objectives.

The Executive Compensation Software Market Report is Segmented by Component (Software, and Services), Deployment Model (Cloud-Based, and On-Premises), Enterprise Size (Large Enterprises, and SMEs), End-User Industry (BFSI, IT and Telecommunications, Healthcare and Lifesciences, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector, and Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| SMEs |

| BFSI |

| IT and Telecommunications |

| Healthcare and Lifesciences |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| By Enterprise Size | Large Enterprises | |

| SMEs | ||

| By End-User Industry | BFSI | |

| IT and Telecommunications | ||

| Healthcare and Lifesciences | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Singapore | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the executive compensation software market expected to become by 2031?

The executive compensation software market is expected to reach USD 1.78 billion by 2031, up from USD 1.12 billion in 2026, at a 9.68% CAGR over 2026-2031.

What is driving demand for executive compensation software in 2026?

Demand is being driven by pay transparency rules, SEC disclosure requirements, and the need for audit-ready pay governance. These pressures are turning compensation management into a recurring software and services spend.

Which deployment model is leading adoption?

Cloud-based deployment led with a 75.44% revenue share in 2025 and is also the fastest-growing model, with a 10.11% CAGR through 2031.

Which customer group is expanding fastest?

SMEs are projected to grow the fastest, at a 10.86% CAGR through 2031, as cloud delivery and modular pricing lower adoption barriers for smaller employers.

Which end-user segment contributes the most revenue?

BFSI was the largest end-user segment in 2025 with a 25.61% share, supported by strict pay governance, risk alignment, and disclosure requirements.

Which region offers the strongest growth outlook?

Asia-Pacific has the strongest regional growth outlook, with an 11.76% CAGR through 2031, driven by HR digitization, executive pay formalization, and stronger multinational governance needs.

Page last updated on: