Payroll And Compensation Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

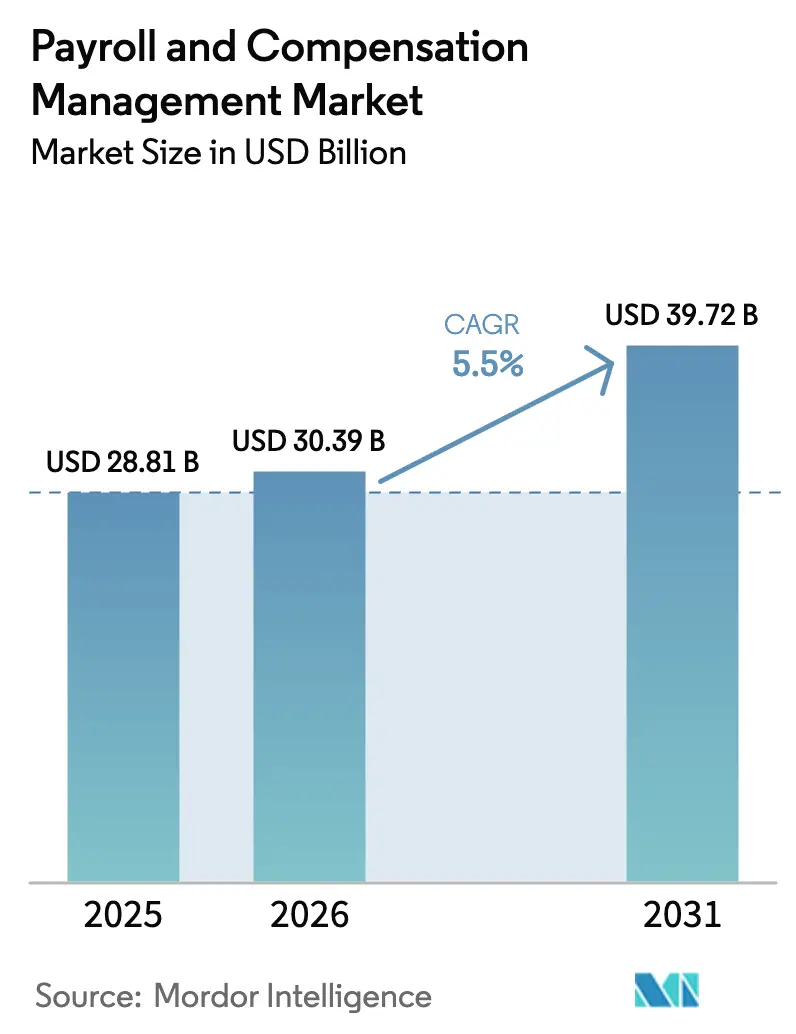

| Market Size (2026) | USD 30.39 Billion |

| Market Size (2031) | USD 39.72 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

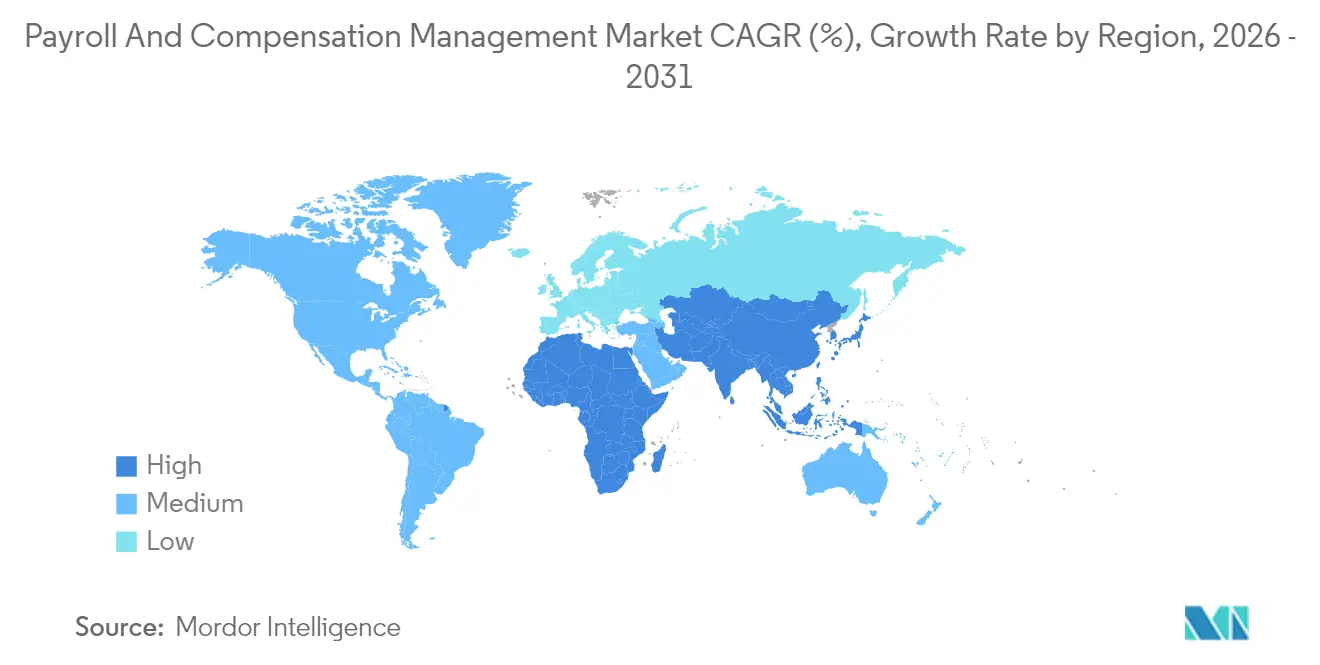

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Payroll And Compensation Management Market Analysis by Mordor Intelligence

The Payroll and Compensation Management market size is expected to grow from USD 28.81 billion in 2025 to USD 30.39 billion in 2026 and is forecast to reach USD 39.72 billion by 2031 at 5.5% CAGR over 2026-2031. Cloud-hosted deployment models command the dominant position, reflecting 71.36% of 2024 revenue, as enterprises pursue scalable platforms that keep pace with frequent tax changes. Services, led by outsourced and employer-of-record (EOR) offerings, hold 62.31% of 2024 spending, confirming that many organizations still rely on expert partners for complex statutory compliance. The BFSI sector delivers the largest end-user contribution thanks to stringent reporting standards, while IT and telecom post the most rapid uptake as remote hiring drives global payroll adoption. Regionally, North America retains leadership through mature outsourcing cultures and intricate tax regimes, whereas Asia Pacific exhibits the strongest medium-term momentum as governments accelerate SME digitization programs.

Key Report Takeaways

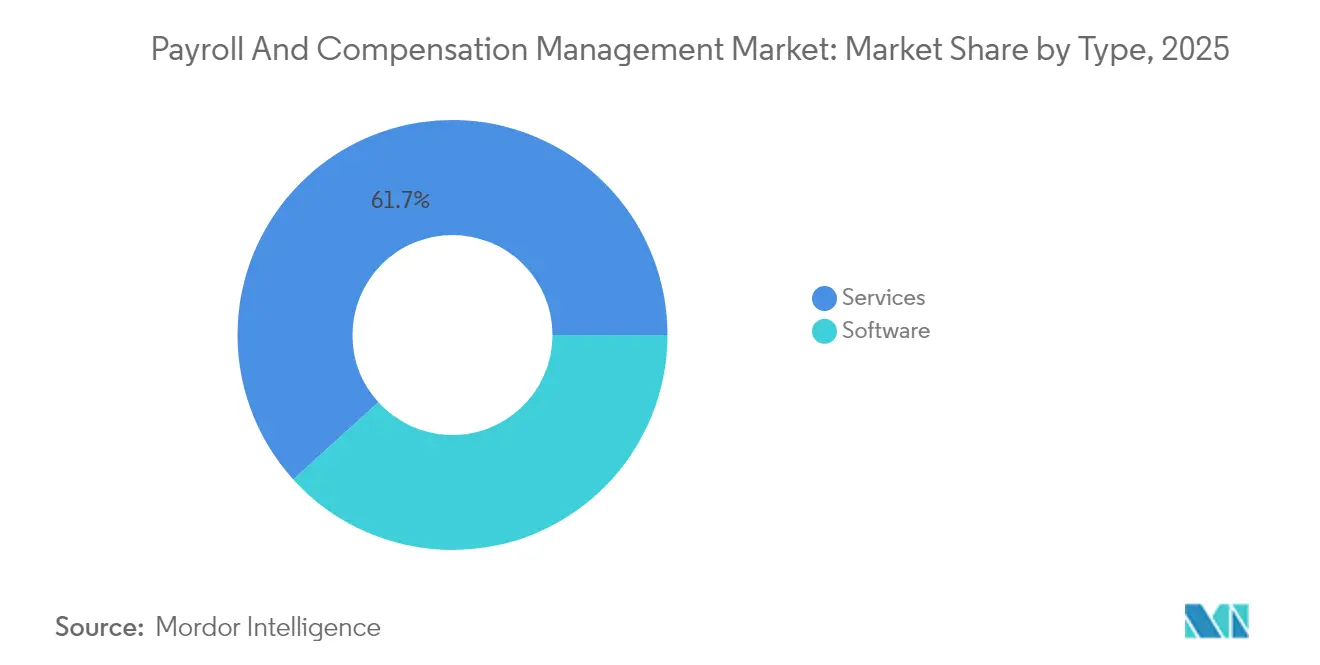

- By type, services led with 61.72% of the Payroll and Compensation Management market share in 2025; software is projected to expand at a 6.32% CAGR through 2031.

- By application, core payroll processing accounted for 46.01% share of the Payroll and Compensation Management market size in 2025 and performance review applications are advancing at a 6.46% CAGR to 2031.

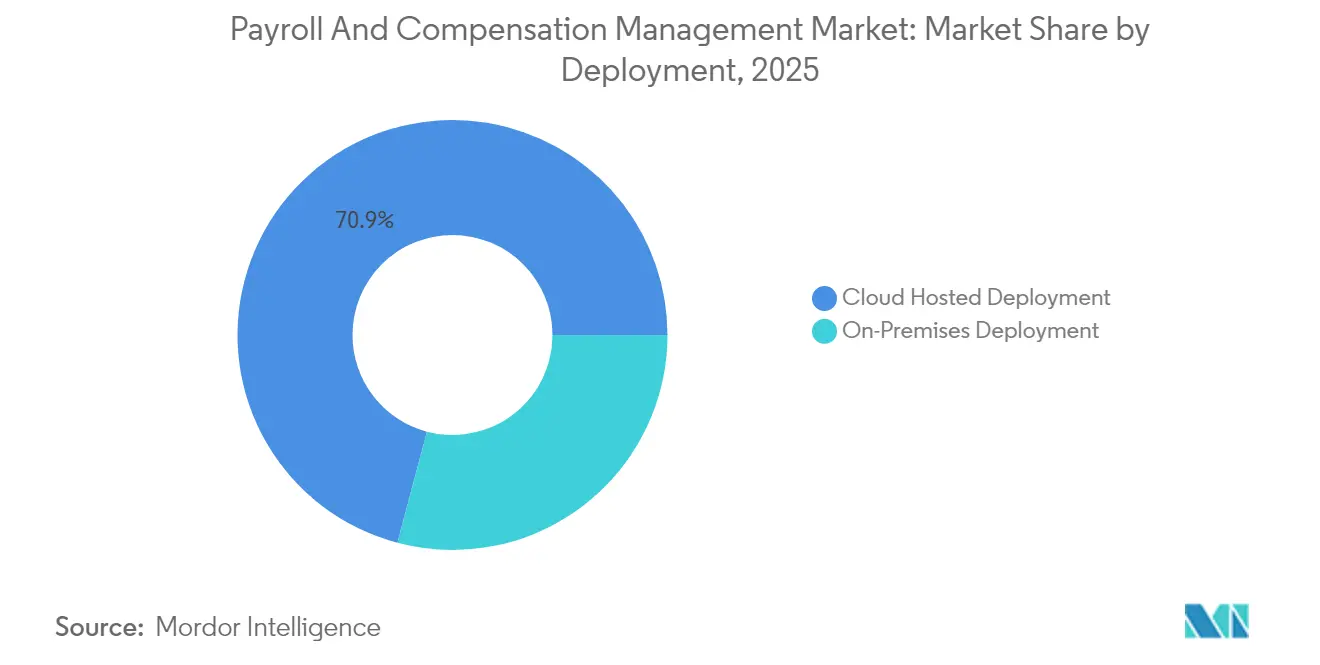

- By deployment, cloud-hosted models captured 70.88% revenue in 2025, and the segment is forecast to grow at a 5.81% CAGR between 2026-2031.

- By end-user industry, BFSI held 22.75% contribution in 2025, while IT and telecom record the highest projected CAGR at 6.12% through 2031.

- By geography, North America retained 35.82% share in 2025; Asia Pacific is forecast to register a 6.20% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Payroll And Compensation Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud-Hosted Global Payroll Platforms | +1.2% | Global (early gains in North America and Europe) | Medium term (2-4 years) |

| Stringent Multi-Country Tax and Labor Compliance Requirements | +1.0% | Global (EU and Asia Pacific focus) | Long term (≥4 years) |

| Expansion of Cross-Border Remote Work and Employer-of-Record Models | +0.8% | North America and Europe core, spill-over to Asia Pacific | Short term (≤2 years) |

| SME Digitization Programs and Government e-Invoicing Mandates | +0.7% | Asia Pacific core (Singapore, Malaysia, Australia) | Medium term (2-4 years) |

| AI-Enabled Autonomous Payroll for Error Reduction and Real-Time Audits | +0.6% | Global (early adoption in North America) | Long term (≥4 years) |

| Earned-Wage Access Integration Driving Payroll Modernization | +0.4% | North America and Europe, expanding to Asia Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud-Hosted Global Payroll Platforms

Cloud solutions already process 71.36% of 2024 transactions, showing that most organizations now value subscription updates over periodic on-premises upgrades. Oracle’s HCM Cloud posted 23% revenue growth during fiscal 2024 in step with multinationals collapsing multiple domestic payroll engines into a single tenant platform. ADP’s GlobalView processes salaries for more than 4 million workers across 140 countries, proving the scale efficiencies cloud affords to complex multi-jurisdiction employers. Automated rule libraries also limit human effort when Singapore or Australia release last-minute tax amendments, enabling near-real-time compliance

Stringent Multi-Country Tax and Labor Compliance Requirements

GDPR, Making Tax Digital, and similar laws force payroll engines to embed privacy-by-design coding while providing real-time submission feeds to revenue agencies.[1]HM Revenue and Customs, “Making Tax Digital,” gov.uk Malaysia’s 2024 e-invoicing law broadens the digital burden, rewarding vendors that field dedicated regional regulatory teams. ISO 27001 certification has become a standard buyer prerequisite because compliance lapses can trigger fines of up to 4% of global revenue in Europe.[2]European Commission, “VAT for Businesses,” ec.europa.eu

Expansion of Cross-Border Remote Work and Employer-of-Record Models

EOR providers fill legal gaps for firms hiring staff where they lack an entity, cutting time-to-hire from months to days. Deel’s USD 1.25 billion purchase of Safeguard Global in 2024 highlighted soaring investor appetite for this segment. More than two-thirds of Fortune 500 enterprises now route some distributed teams through EOR structures, compelling software vendors to embed multi-currency pay, localized benefits and immigration administration.

AI-Enabled Autonomous Payroll for Error Reduction and Real-Time Audits

Pattern-recognition algorithms reduce costly mispayments by flagging duplicate records or out-of-band overtime before payroll is finalized. UKG’s engine already analyzes 30 million paychecks per month to catch anomalies at source. Continuous audits generate digital documentation for regulators, replacing manual sample testing and lifting HR productivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Regional Statutory Reporting Formats | -0.8% | Global (pronounced in EU and Asia Pacific) | Long term (≥4 years) |

| Persistent Payroll Talent Shortage Inside Enterprises | -0.6% | North America and Europe, spreading globally | Medium term (2-4 years) |

| Rising Cyber-Security Breach Costs for Sensitive Pay Data | -0.7% | Global (highest in North America) | Short term (≤2 years) |

| Legacy ERP Lock-In Slowing Cloud Migration | -0.5% | Global (manufacturing and BFSI bias) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Fragmented Regional Statutory Reporting Formats

The European Union manages 27 distinct payroll tax codes that must be filed in unique electronic layouts, compelling vendors to maintain parallel compliance modules and pushing development costs higher. Australia’s Single Touch Payroll and other unilateral frameworks add to the patchwork, hindering the creation of a universally consolidated reporting hub.

Rising Cyber-Security Breach Costs for Sensitive Pay Data

Average breach expenses climbed to USD 4.88 million in 2024, with ransom groups pivoting toward payroll databases because they house bank details and identity numbers.[3]IBM Security, “Cost of a Data Breach Report 2024,” ibm.com GDPR penalties further magnify exposure, driving CFOs to ring-fence cyber budgets that could otherwise fund modernization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Dominate Through Complexity Management

Services retained 61.72% of 2025 revenue, reflecting the enduring appeal of managed offerings when enterprises must reconcile divergent tax schedules, union rules and currency fluctuations. The Payroll Management market size for services still grows at 4.95% despite the maturity of outsourcing deals. In contrast, software posts a faster 6.32% CAGR as AI engines automate validations and shrinks manual interventions. The mix signals that many firms progressively shift from full-outsourcing to technology-led self-service without abandoning expert advisory altogether. Providers including ADP and Paychex now bundle subscription analytics upgrades and on-demand compliance coaching, blurring the historical boundaries between product and service.

Software uptake also benefits from flexible per-employee pricing that appeals to mid-market adopters once locked out of enterprise-grade capabilities. API-first architectures support rapid links to time-tracking, performance and treasury modules, helping payroll teams craft integrated payment strategies. Paychex reported 7% SaaS revenue growth in fiscal 2024, echoing the market’s tilt toward configuration-driven platforms. Hybrid operating models are emerging in which organizations license multi-country suites yet retain a services overlay in the most complex jurisdictions, extending the Payroll Management market momentum.

By Application: Payroll Core Expands Into Performance Integration

Core salary calculation accounted for a 46.01% share in 2025, illustrating that accurate net-pay remains the anchor of the Payroll Management market. However, performance review tools are scaling fastest at a 6.46% CAGR, fueled by merit-based pay schemes that demand instantaneous appraisal data. This shift extends the Payroll Management market share of holistic compensation suites as HR leaders align bonuses to measured behaviors.

Benefits administration continues to grow consistently as employers leverage richer medical plans and retirement perks to woo scarce talent. Time and attendance tools capture demand from shift-based industries, but innovation now resides in AI facial recognition that lowers clock-in fraud. Tax filing modules remain indispensable under persistent legislative change, while earned-wage access options reshape reimbursement workflows. Vendors that fuse these once-separate modules on a single ledger achieve stickier client contracts and stronger cross-sell economics.

By Deployment: Cloud Migration Accelerates Despite Legacy Constraints

Cloud-hosted deployment holds a commanding 70.88% revenue share and will maintain leadership with a 5.81% CAGR to 2031 as firms pursue pay-as-you-go scalability. Automatic updates relieve administrators from downloading country tax patches and ensure audit readiness. The Payroll Management market size derived from on-premises installations contracts as banks and manufacturers gradually rewrite policies that once enforced site-only data residency.

Nevertheless, legacy ERPs with hard-coded pay logic slow total cloud replacement in select unionized plants and defense contractors. Hybrid topologies have emerged, retaining static reference tables on-site while diverting calculation cycles to the cloud for elastic performance bursts. Oracle’s FY 2024 payroll cloud revenue rise of 23% confirms that modular migratory routes are viable even for the most regulated adopters

By End-User Industry: BFSI Leadership Faces IT Sector Challenge

BFSI contributed 22.75% of 2025 spending, driven by daily capital-market compliance filings and complex equity bonus structures that mandate dedicated payroll rules. Big banks also rely on risk dashboards linking pay data with anti-money-laundering controls, reinforcing their premium on specialized platforms. The Payroll Management market size allocated to BFSI continues to rise in low single digits as cost-to-income frameworks remain tight.

Conversely, the IT and telecom sector posts a 6.12% CAGR through 2031 as globally distributed engineering squads demand multi-currency, milestone-linked payroll. Software firms seek instantaneous onboarding and EOR coverage when opening satellite innovation centers, accelerating demand for borderless pay engines. Manufacturing, healthcare, retail and logistics keep stable uptake patterns, each favoring domain-specific features such as shift premiums, credential checks or mileage pay.

Geography Analysis

North America represented 35.82% of global 2025 revenue as intricate federal-state taxation and mature outsourcing cultures bolster platform demand. United States employers face payroll tax at both national and state levels, compelling them to select engines capable of automatic jurisdiction updates. Canadian firms add bilingual payslip mandates and provincial pension contributions that spur reliance on specialized vendors. Mexico’s export-oriented manufacturers link payroll with customs invoicing, requiring cross-border wage reconciliation abilities. ADP generated USD 12.2 billion from the region in fiscal 2024, highlighting its commercial scale.

Asia Pacific posts the swiftest regional CAGR at 6.20% through 2031. Singapore’s SMEs Go Digital vouchers reimburse subscription fees and helped lift micro-business adoption rates above 60% by mid-2025 IMDA. Malaysia’s 2024 e-invoicing rollout pushes companies onto cloud suites that integrate payroll with digital tax ledgers. In India, IT offshoring majors require batch calculations that align variable project bonuses with client billing cycles, spurring demand for highly configurable gross-to-net engines. China’s sheer worker base enforces scale benchmarks, with some domestic vendors now processing in excess of 50 million payslips each month. Japan’s aging labor pool prompts automation to offset HR headcount shortages, while Australia pivots toward analytics overlays rather than base modernization.

Europe maintains stable, compliance-centric growth. GDPR embeds privacy audit reporting into every payslip sequence, encouraging continuous monitoring modules. Fragmented post-Brexit filing divergence raises complexity for firms straddling the English Channel. Germany’s works-council environment necessitates versioning that logs each pay-rule change, and France’s social-security deductions demand extensive arrears recalculation functions. South America and the Middle East and Africa remain nascent yet promising. Brazil’s updated eSocial requirements have driven cloud conversions among multinationals sourcing labor locally, and the UAE’s hub status fuels demand for tri-lingual, multi-currency processing engines to serve expatriate populations.

Regulatory Landscape

Payroll and compensation platforms operate under overlapping labor, tax, and data-protection obligations that increasingly require near-real-time reporting and auditable calculations. In Europe, GDPR continues to shape payroll system design and security controls, and the EU Pay Transparency Directive introduces new compliance requirements with national transposition due by June 7, 2026, including salary-range disclosure and gender pay-gap reporting obligations that expand what payroll and compensation workflows must capture and disclose.

Outside Europe, country-specific e-reporting frameworks continue to drive localization requirements, including the United Kingdom RTI regime and Brazil eSocial, where submission formats and timing can influence payroll processing cycles and error risk. Worker-classification rules (including evolving EU platform-work directives) are also tightening, which raises exposure to back taxes and penalties and reinforces demand for embedded controls, standardized audit trails, and security certifications such as ISO 27001 and SOC 2 Type 2 among large buyers.

Value Chain Analysis

The value chain covers statutory rule content (tax, labor, and benefits updates), payroll and compensation software platforms, implementation and managed services, and adjacent payments and banking rails used to disburse wages and remit taxes. The delivery model is shifting from service-centric offerings toward platform-led ecosystems built on APIs, where vendors connect HCM, time and attendance, performance review, and finance systems to reduce manual handoffs and improve compliance readiness.

Partnership and certification programs are increasingly used to speed integrations and broaden distribution. For example, ADP and SAP announced collaboration in 2025 to elevate global payroll experiences and support unified cloud foundations for multinational payroll operations, while Ramco Payce secured Workday Global Payroll Connect certification to provide prebuilt connectivity with Workday HCM. On the downstream side, embedded payroll models extend distribution through POS and vertical SaaS ecosystems, exemplified by ADP Embedded Payroll positioned for partners. This approach shortens time-to-market for SMB-focused payroll offerings and ties payroll processing more tightly to operational and financial workflows.

Competitive Landscape

The Payroll and Compensation Management market exhibits moderate concentration. Global incumbents such as ADP, Paychex and SAP leverage brand equity, country certifications and integrated HR suites to retain enterprise contracts. Mid-tier challengers including Ceridian and Ultimate Kronos Group pivot to AI-based compliance alerts and shift-centric scheduling analytics to win share among complex hourly workforces. Cloud-native disruptors like Rippling, Deel and Gusto differentiate through friction-less onboarding and transparent pricing geared toward high-growth technology firms. Deel’s USD 1.25 billion Safeguard Global acquisition enlarged its EOR footprint to 180 countries, giving it a turnkey cross-border proposition.

Acquisitions remain the primary route to fill geographic and functional gaps. UKG spent USD 1.2 billion on Immedis to unlock coverage in 160 markets and elevate predictive payroll analytics. Oracle now offers public-sector payroll templates pre-loaded with union deduction tables, shotgunning itself into government tenders that once defaulted to specialist niche players. Strategic tech alliances intensify: Paychex integrates with Microsoft Viva so people analytics can drive automated merit raise triggers. Earned-wage access is another battleground; BambooHR and Gusto already embed early-wage withdrawal, increasing employee engagement and net promoter scores.

Vendors secure ISO 27001 and SOC 2 Type 2 audits to reassure risk-averse buyers amid breach cost escalation. Mobile-first roadmaps, open APIs and partner marketplaces highlight a shift toward payroll as a platform rather than a standalone calculator. With new entrants slicing off EOR or niche geographic segments, established providers respond by adding self-service dashboards, cross-border treasury modules and pay-on-demand rails to neutralize switching incentives. The race increasingly revolves around time-to-compliance updates; whoever posts new statutory tables first typically locks in renewals.

Payroll And Compensation Management Industry Leaders

SAP SE

Paychex, Inc.

Ramco Systems Limited

Automatic Data Processing, Inc. (ADP)

Intuit Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Embedded payroll and pay-disbursement capabilities create whitespace for vendors to distribute payroll through HR, POS, and vertical SaaS platforms instead of selling standalone payroll engines. ADP has positioned embedded payroll for partners, and Paychex expanded employee pay-access options through its Paychex Flex Perks ecosystem by teaming with PayPal in January 2026 for direct-deposit alternatives. Together, these moves reflect a more productized approach to payroll-adjacent payout experiences in SMB accounts.

A second opportunity centers on compliance automation and pay-transparency readiness as reporting obligations expand, especially in Europe with the EU Pay Transparency Directive deadline of June 7, 2026. This is increasing demand for compensation data governance, explainability, and audit trails that connect payroll, performance, and HR master data, aligning with vendor roadmaps such as SAP SuccessFactors Employee Central Payroll updates that add payroll agents and integration enhancements. In parallel, tighter linkage between payroll, treasury, and workforce-cost analytics supports use cases beyond HR, including liquidity planning and operational performance management, particularly in shift-heavy industries where overtime and differentials affect margins.

Recent Industry Developments

- June 2026: Paychex, Inc. reported fiscal 2026 full-year results with heightened compensation-related expenses and technology investments linked to the Paycor acquisition. The results indicate increased capex in payroll tech and potential shifts in competitive positioning post-acquisition.

- May 2026: SAP SE released SAP SuccessFactors 1H 2026 update for Employee Central Payroll, introducing multiple payroll agents and data-integration enhancements. This improves SAP’s payroll platform competitiveness and expands compliance capabilities across markets.

- January 2026: Ramco Systems Limited Ramco Payce certified as a Workday Global Payroll Connect partner, enabling prebuilt integrations with Workday HCM. Broadens Ramco’s cross-border payroll reach and strengthens its end-to-end payroll workflow proposition.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the payroll and compensation management market as the revenue earned from software and services that help employers calculate pay, manage compensation-related records, and complete required payroll workflows, including compliance steps, over a given year.

Scope exclusions: This sizing does not count general HR tools that lack payroll and compensation execution, such as standalone recruiting, learning, or engagement systems.

Segmentation Overview

- By Type

- Software

- Services

- By Application

- Payroll

- Employee Benefits

- Tax Filings

- Performance Review

- Time and Attendance

- Leave Management

- Reimbursement and Loans

- By Deployment

- On-Premises Deployment

- Cloud Hosted Deployment

- By End-User Industry

- BFSI

- Retail

- Manufacturing

- Transportation and Logistics

- IT and Telecom

- Healthcare

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, map the value chain, and build a first pass of regional demand and adoption signals before we spoke to industry participants. For a market like this, we leaned on public and official sources that help explain employment volumes, wage levels, and payroll compliance requirements, such as the US Bureau of Labor Statistics, the US Internal Revenue Service, Eurostat, the International Labour Organization, and the World Bank.

We also reviewed company filings and earnings commentary, product documentation, and large public procurement notices to understand how buyers describe scope and what they purchase over multi-year contracts. Where helpful, we referenced paid subscriptions for company financial intelligence, news and financials, patent databases, and a global contracts and tenders database to cross-check revenue mix and demand signals. This list of desk sources is not exhaustive, and many other public references were used to collect data, validate assumptions, and clarify open points.

Primary Interviews and Surveys

Primary work focused on confirming what is typically included in payroll and compensation management spend, how cloud pricing is structured, and how service components are bundled with software in real buying situations. We spoke with a mix of platform teams, payroll service providers, implementation partners, and enterprise payroll leaders across major regions, so gaps from desk research could be closed and assumptions could be checked in plain language using procurement-like scope descriptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 38% |

| Mid tier: 52% | Functional/Unit leaders: 41% | EMEA: 35% |

| Smaller Players: 18% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up approach, where a demand pool was constructed from the employed workforce by region, then filtered through payroll digitization and outsourcing penetration, and then converted to value using typical per-employee-per-month pricing and service attach assumptions. To keep the totals realistic, we corroborated outputs with selective bottom-up checks, such as sampled supplier revenue splits, channel partner feedback on average contract sizes, and service intensity differences by country complexity.

A few inputs that mattered in the model were the number of active employees on payroll systems, cloud adoption share for HR and payroll workloads, multi-country payroll needs driven by cross-border hiring, the frequency of statutory changes that trigger compliance spend, and the typical split between software subscription and managed services. Where data was thin for smaller countries, we used proxy indicators like formal employment share, wage levels, and regional vendor presence, and then adjusted the results after expert feedback.

For forecasting, we used scenario analysis supported by short multivariate regression tests on drivers like employment growth, cloud migration pace, and outsourcing penetration. The final forecast path was aligned to what practitioners described as the most likely pricing progression and adoption cycle, rather than a single aggressive or conservative case.

Data Validation & Update Cycle

Model outputs were cross-checked against independent signals, including employment and wage series, cloud software spend direction, and public commentary on payroll compliance burden. Variances were reviewed in multiple steps, where a second analyst rechecked scope fit, currency handling, and the logic behind key assumptions before sign-off.

When a large variance or an unexpected regional swing was observed, we re-contacted sources to confirm whether it came from a real demand shift, a pricing change, or a definition mismatch. Reports are refreshed annually, and interim updates are made when material events change the outlook. Before delivery, an analyst performs a final pass so clients receive the latest updated view.

Mordor Intelligence's Payroll and Compensation Management Market Estimate Compared With Other Published Estimates

Published market sizes for payroll and compensation management do not always line up because the scope line is drawn differently and because the underlying price and adoption assumptions vary by publisher. Differences also show up when one estimate mixes software, services, and adjacent HCM spending into a single total, while another keeps the boundary closer to payroll execution.

The table shows a clear spread, and in Mordor Intelligence's model the total includes both payroll software and payroll linked services, but it avoids counting broader HCM suites unless the module is used for payroll or compensation processing and is paid for as part of that use.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 28.81 B (2025) | |

| Industry Publisher A | USD 12.51 B (2025) | Counts mainly payroll software subscriptions and excludes most managed payroll services, which lowers the total and can shift growth rates upward due to a narrower starting base. |

| Research Group B | USD 28.40 B (2024) | Uses a broader HR solutions and services bucket, which can blend payroll with adjacent HR activities, and may apply different currency timing and regional weighting for global rollups. |

Looking across the three figures, the smallest value is explained mostly by a tighter product boundary, while the broader bucket inflates totals by pulling in adjacent HR spend. By keeping assumptions tied to employee counts, adoption, and realistic price ladders, the sizing stays traceable and can be repeated when new signals or contract patterns emerge.

Key Questions Answered in the Report

What is the current value of the Payroll and Compensation Management market?

The market stands at USD 30.39 billion in 2026 and is projected to grow steadily through 2031.

Which deployment model is expanding fastest?

Cloud-hosted payroll tops adoption, covering 70.88% of 2025 revenue and growing at a 5.81% CAGR.

Why are enterprises favoring employer-of-record services?

EOR models let firms hire talent abroad without establishing local entities, speeding onboarding and ensuring compliance across tax jurisdictions.

How does AI improve payroll accuracy?

Machine-learning algorithms flag anomalies before pay is finalized, reducing costly errors and providing real-time audit trails for regulators.

Which region offers the highest growth opportunity?

Asia Pacific is forecast to expand at a 6.20% CAGR to 2031 as governments push SME digitization and mandate e-invoicing.

What is the primary security concern for payroll teams?

Rising cyber-attack costs averaging USD 4.88 million per breach drive urgent investment in encryption, access controls and compliance audits.

Page last updated on: