Accounting Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

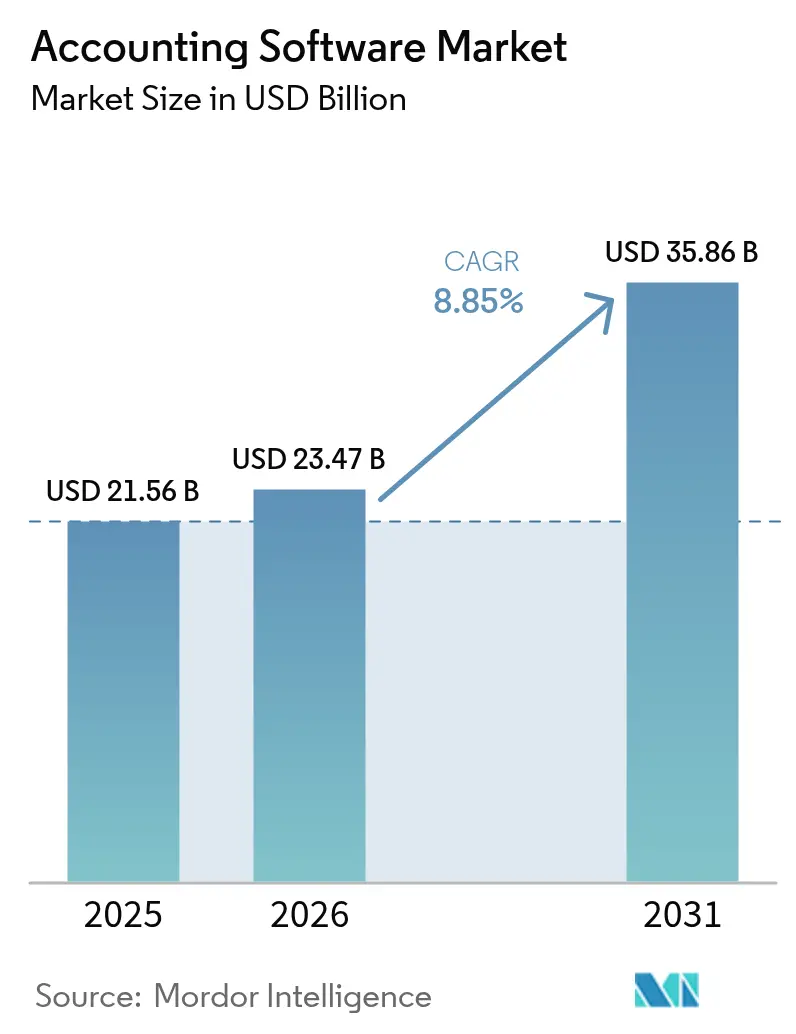

| Market Size (2026) | USD 23.47 Billion |

| Market Size (2031) | USD 35.86 Billion |

| Growth Rate (2026 - 2031) | 8.85% CAGR |

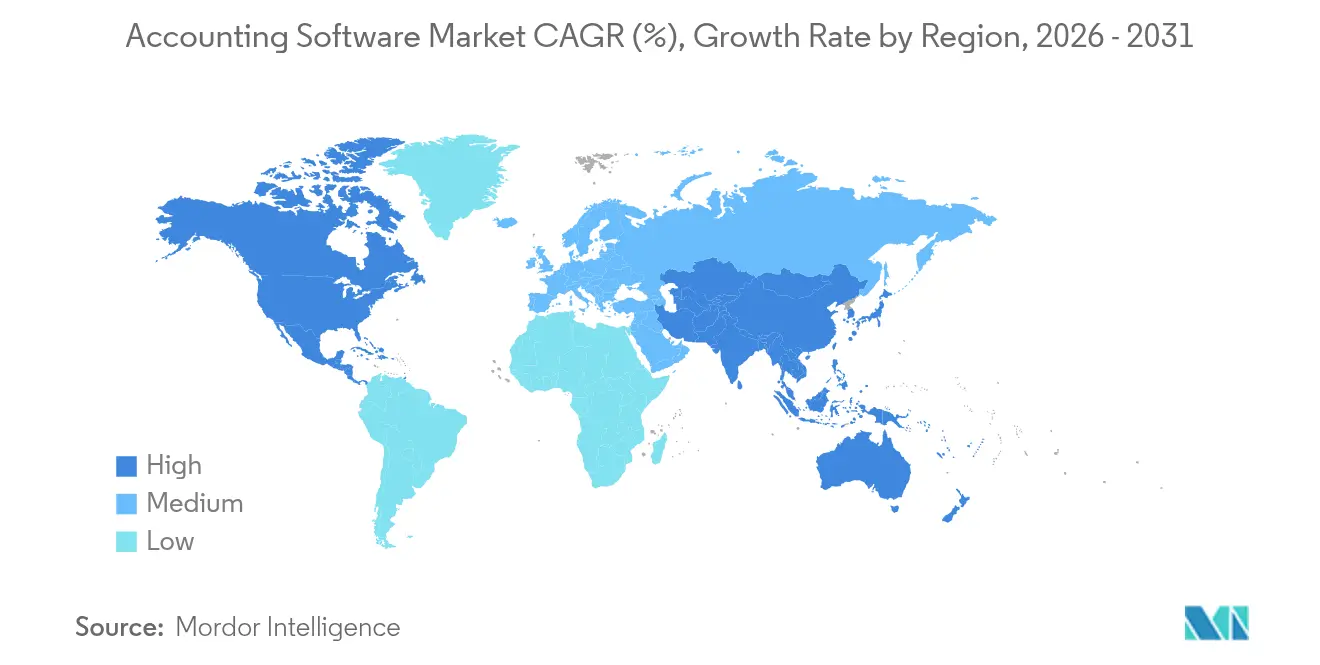

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Accounting Software Market Analysis by Mordor Intelligence

The accounting software market size was valued at USD 21.56 billion in 2025 and estimated to grow from USD 23.47 billion in 2026 to reach USD 35.86 billion by 2031, at a CAGR of 8.85% during the forecast period (2026-2031). Cloud-first strategies, real-time regulatory reporting mandates and embedded artificial-intelligence features continue to redefine competitive advantage, with cloud deployments already anchoring 67.43% of revenue in 2024. Vendors are expanding mobile, API-centric suites that integrate banking, treasury and spend-management functions, helping enterprises compress monthly close cycles and unlock working-capital insights. At the same time, talent shortages inside finance departments accelerate software adoption because automation substitutes repetitive bookkeeping labor. Finally, emerging ESG audit-trail requirements force organizations to refresh legacy systems in favor of solutions that generate immutable environmental and social disclosures.

Key Report Takeaways

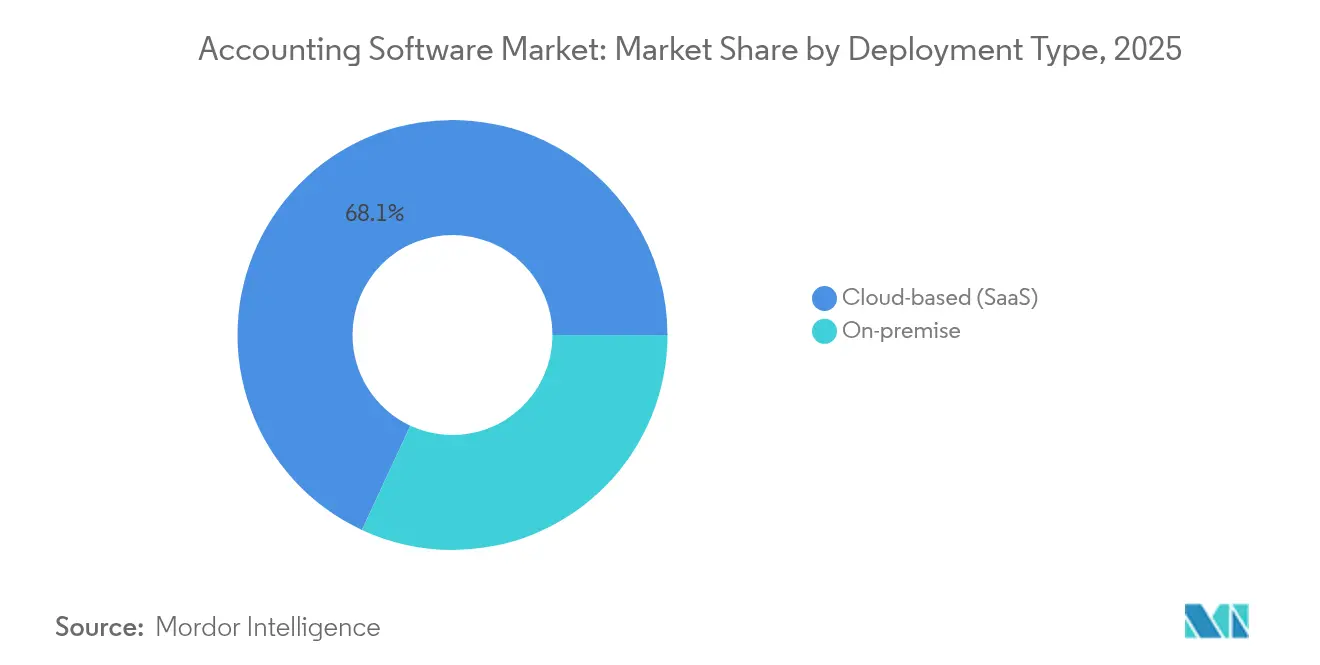

- By deployment type, cloud-based solutions captured 68.08% of accounting software market share in 2025 while advancing at a 10.15% CAGR through 2031.

- By organization size, small and medium enterprises registered the fastest growth at 10.85% CAGR from 2026-2031, whereas large enterprises held 54.10% revenue share in 2025.

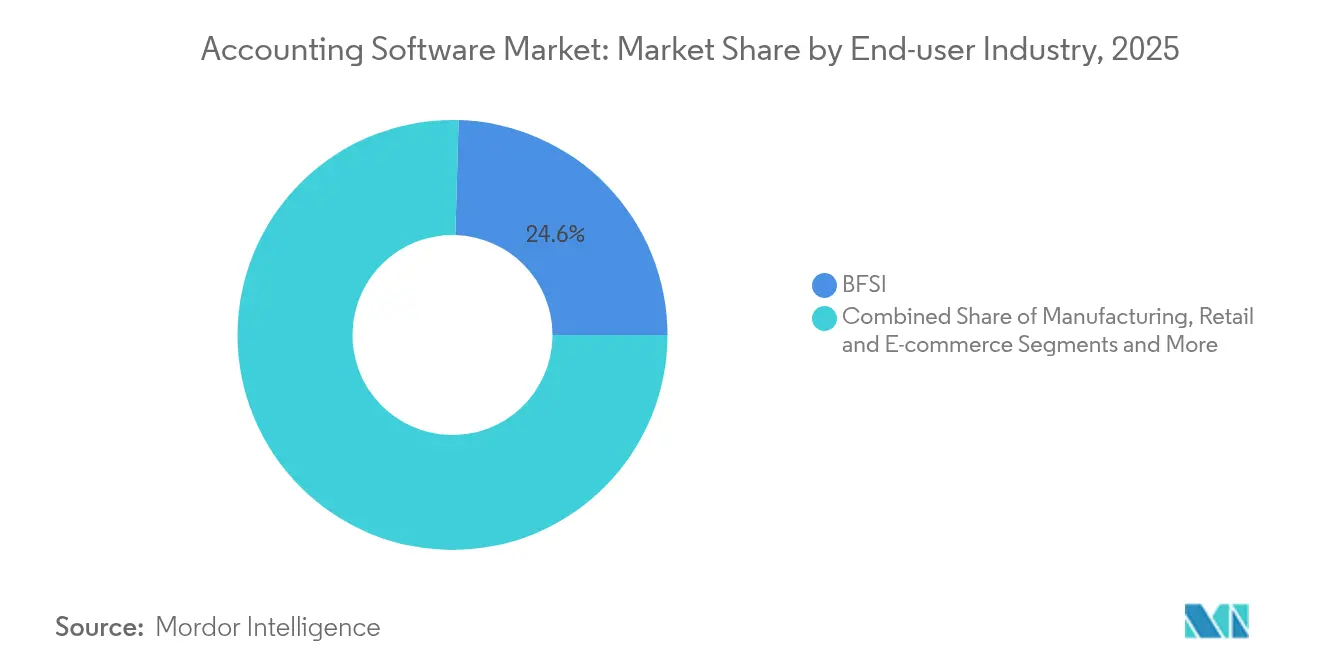

- By end-user industry, the BFSI segment led with 24.55% revenue share in 2025; IT & Telecom is poised for a 10.35% CAGR to 2031.

- By application, payroll management commanded 29.10% of the accounting software market size in 2025 and is expanding at 10.40% CAGR through 2031.

- By geography, North America accounted for 38.35% revenue in 2025, yet Asia-Pacific is projected to grow at 10.45% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Accounting Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first finance-stack adoption | +2.1% | North America, EU | Medium term (2-4 years) |

| Hyper-automation of bookkeeping workflows | +1.8% | Asia-Pacific, MEA | Short term (≤ 2 years) |

| AI-led anomaly detection & compliance | +1.5% | Global | Long term (≥ 4 years) |

| Mobile-first accounting experience | +1.2% | Emerging markets | Short term (≤ 2 years) |

| Real-time A/R-A/P financing via open banking | +0.9% | Europe, Asia-Pacific | Medium term (2-4 years) |

| ESG-grade audit-trail refresh cycles | +0.7% | EU, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Finance-Stack Adoption

Organizations are abandoning on-premise installations in favor of cloud architectures that synchronize accounting, treasury and operational data in real time, cutting infrastructure costs and improving cash-flow visibility. The shift also unlocks seamless fintech integrations—payments, expense cards and short-term liquidity—once unattainable on legacy systems[1]Safra Catz, “Oracle Announces Fiscal 2025 Fourth Quarter and Fiscal Full Year Financial Results,” Oracle Corporation, oracle.com.

Hyper-Automation of Bookkeeping Workflows

Machine-learning extraction and robotic process automation now classify transactions, reconcile banks and process invoices with 98% accuracy, allowing accounting firms to absorb more clients without proportional head-count increases. The resulting productivity gains lower total ownership costs for small businesses and offset the industry-wide talent deficit[2]Sasan Goodarzi, “Intuit Reports Strong Third-Quarter Results and Raises Full-Year Guidance,” Intuit Inc., intuit.com .

AI-Led Anomaly Detection and Compliance

Advanced models continuously scan ledgers for fraud signals, cash-flow gaps and filing errors, triggering proactive alerts that minimize audit exposure. Natural-language interfaces democratize complex analytics, enabling non-finance managers to query books conversationally and strengthening cross-functional decision making.

Mobile-First Accounting Experience Demand

Full-function mobile apps empower owners and finance teams to issue invoices, approve expenses and view KPIs wherever they operate, supporting hybrid workforces and accelerating payment cycles. An API-first design ensures feature parity across devices and simplifies integration with mobile wallets prevalent in Asia-Pacific commerce.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-sovereignty & privacy regulations | -1.4% | EU, North America | Medium term (2-4 years) |

| Legacy-system switching costs | -1.1% | Global | Short term (≤ 2 years) |

| Scarcity of AI-ready accounting talent | -0.8% | Developed markets | Long term (≥ 4 years) |

| Fragmented cross-border e-invoicing rules | -0.6% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Sovereignty and Privacy Regulations

Rules such as GDPR compel local data residency, forcing vendors to maintain multi-region clouds and inflating implementation budgets. Enterprises hesitate to migrate sensitive ledgers until contractual clauses guarantee encryption, access controls and in-country storage options, delaying project timelines [3]heyData GmbH, “GDPR vs. SOC 2: Navigating Compliance in the Digital Age,” heydata.eu.

Scarcity of AI-Ready Accounting Talent

Fewer certified professionals possess the data-analytics and system-integration skills needed to configure modern platforms, leading to deployment bottlenecks and under-utilized feature sets. Vendors respond with low-code configuration tools and embedded training modules, but up-skilling remains a multi-year journey.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Dominance Accelerates

Cloud solutions generated 68.08% revenue in 2025, and their 10.15% CAGR signals that the on-premise share will continue to erode. The model’s pay-as-you-grow pricing eliminates capital expenditure and embeds automatic updates that strengthen security posture. Seamless API connectivity with banks and payroll providers further cements adoption. Large enterprises wedded to legacy ERPs still favor hybrid strategies for latency-sensitive workflows, yet even they pilot cloud subsidiaries to reduce close cycles. Growing data-residency options and regional datacenters mitigate prior compliance objections, suggesting that the cloud slice of the accounting software market will near saturation by decade-end.

On-premise platforms retain niche relevance in highly regulated sectors where offline processing is mandatory or where bespoke customizations lock systems in place. However, maintenance overhead and scarce mainframe skills push CFOs to earmark modernization budgets. Vendors exploit this transition by offering migration toolkits that map historical ledgers into multi-tenant architectures, shortening cut-over periods to weeks. As a result, the accounting software market size tied to on-premise deployments is projected to contract despite overall industry expansion.

By Organization Size: SME Growth Outpaces Enterprise

Large organizations captured 54.10% of 2025 revenue by deploying global-consolidation suites capable of multi-currency and multi-entity reporting. Yet SMEs drive the fastest 10.85% CAGR because intuitive cloud modules and AI-driven data capture reduce the need for dedicated IT staff. Subscription tiers align costs with transaction volume, ensuring affordability even during early growth stages.

Entrepreneurial ecosystems in Asia-Pacific and Latin America further catalyze SME demand as mandatory e-invoicing forces digital upgrades. Vendors releasing starter packages with embedded chatbot support lower adoption barriers and convert manual spreadsheet users into subscribers. Consequently, the accounting software market share commanded by SMEs will steadily rise, narrowing the historic gap with enterprise deployments.

By End-User Industry: BFSI Leads, IT Accelerates

Banks, insurers and fintechs represented 24.55% revenue in 2025. Their compliance burden around capital adequacy, anti-money-laundering and audit trails mandates premium features such as rules-based sub-ledgering and automated statutory filings. Conversely, IT and Telecom chalks up a 10.35% CAGR because subscription billing, recurring revenue and multi-region tax nostalgia require sophisticated recognition engines.

Manufacturing and retail follow by integrating inventory costing and omnichannel sales data, while professional-services firms demand project accounting and time-billing modules. Healthcare entities prioritize claim reconciliation, patient invoicing and HIPAA-aligned data handling. The diversity of use cases fuels vendor specialization and micro-vertical templates that shorten time-to-value.

By Application: Payroll Management Dominates

Payroll systems accounted for 29.10% of the accounting software market size in 2025 and exhibit the strongest 10.40% CAGR. Complex wage regulations, gig-work arrangements and multi-jurisdiction tax tables make automation indispensable. Near-real-time gross-to-net calculations and same-day pay features enhance employee satisfaction and compliance simultaneously.

Billing and invoicing, expense tracking and tax management remain foundational modules and serve as gateway functions for first-time adopters. AI-assisted OCR now classifies receipts in seconds, while predictive tax engines optimize quarterly estimates. Incremental add-ons allow companies to extend functionality without rip-and-replace disruptions, fostering upsell opportunities across the accounting software market.

Geography Analysis

North America contributed 38.35% revenue in 2025 on the back of high cloud readiness, mature payments rails and well-funded technology budgets. United States enterprises allocate larger per-employee spend on finance applications compared with global averages, spurring rapid vendor innovation and partnering ecosystems. Canada mirrors this trend, supported by harmonized taxation frameworks that simplify cross-border deployment.

Europe follows, where GDPR compliance and sustainability-reporting mandates stimulate platform refreshes. Multi-lingual interfaces and European e-invoicing standards such as Peppol drive product localization. However, slower decision cycles temper growth relative to Asia-Pacific.

Asia-Pacific charts the fastest 10.45% CAGR, propelled by India’s and Indonesia’s compulsory e-invoicing rollouts and by Japan’s soft-mandate for electronic preservation of ledgers. SMEs leapfrog desktop software, adopting mobile-first cloud suites that integrate domestic e-wallets and QR code payments. Local datacenter investments by global vendors mitigate data-sovereignty hesitance and unlock public-sector procurements.

Latin America sees momentum in Brazil and Mexico, where real-time invoice clearance has existed for years, leading businesses to extend automation beyond tax reporting to full ERP-finance clouds. Middle East and Africa post steady gains aligned to economic diversification drives and expanding fintech ecosystems, though connectivity and talent shortages moderate adoption pace.

Regulatory Landscape

Digital tax and continuous transaction control regimes are increasingly shaping accounting software requirements, moving compliance from periodic filings to structured, near-real-time data exchange. In Europe, the European Committee for Standardization (CEN) updated EN 16931-1 in February 2026 to better support B2B e-invoicing and digital reporting workflows aligned to the EU policy direction. Country programs are adding urgency, including Poland's Ministry of Finance moving KSeF 2.0 into force for the largest taxpayers from February 1, 2026, and France's Finance Act confirming September 1, 2026 as the go-live date for mandatory B2B e-invoicing for large and intermediate enterprises.

Beyond Europe, phased national rollouts are pushing vendors toward configurable, jurisdiction-specific tax logic and data-residency options. The UAE Federal Tax Authority published e-invoicing guidelines (Version 1.0) in February 2026, with a phased program beginning July 2026 for voluntary adoption and January 2027 for mandatory compliance for large taxpayers. At the global level, OECD work on digital continuous transactional reporting and the broader "Tax Administration 3.0" direction is reinforcing the need for audit-ready data models, API-based transmission, and standardized formats (for example, SAF-T and XML/Peppol) embedded directly in accounting and ERP finance modules.

Value Chain Analysis

The accounting software value chain spans cloud infrastructure and security providers, core accounting and ERP vendors, compliance and data-exchange specialists, implementation and advisory partners, and distribution via marketplaces and channel accountants. Platform vendors such as Oracle, SAP, Intuit, and Sage are increasingly orchestrating ecosystems that include payments, payroll, and tax compliance partners, with differentiation shifting toward embedded automation, certified compliance connectors, and pre-built integrations that reduce time-to-close and manual reconciliation.

In 2025, partnerships showed how compliance and finance services are being pulled into the core ledger workflow. J.P. Morgan Payments and Oracle announced an integrated supply chain finance solution within Oracle Cloud ERP (July 2025), while Sovos partnered with Tungsten Automation to combine automated invoice capture with global tax compliance (July 2025). Similar ecosystem moves, including Sovos' global partnership with Intuit for QuickBooks e-invoicing (August 2025) and Sage and Sovos embedding e-invoicing into Sage applications for SMBs (November 2025), highlight the role of compliance networks, AI-driven document capture, and financial institutions as upstream enablers, with accountants and app marketplaces acting as major downstream routes to customers.

Competitive Landscape

The market exhibits moderate fragmentation: the top five vendors hold roughly 45% combined share, leaving ample room for vertical specialists and regional challengers. Incumbents—including Intuit, Sage, and Oracle—capitalize on installed-base renewal and aggressive R&D, illustrated by Oracle’s 27% fiscal-year cloud revenue jump. They protect share through ecosystem acquisitions, such as IRIS Software’s purchase of Dext that merges practice management with data capture.

Challengers focus on AI-native architectures, consumption-based pricing and mobile interfaces to woo fast-growing SMEs. AccountsIQ’s acquisition of ExpenseIn expands mid-market reach, while Melio’s integration into Xero embeds payments inside accounting workflows, shortening cash-conversion cycles. Product differentiation now centers on embedded analytics, ESG disclosures and open-banking connectivity rather than core double-entry functionality.

Partnerships with payroll processors, BNPL providers and industry-specific SaaS platforms become critical distribution levers. Vendors securing SOC 2, ISO 27001 and regional e-invoicing certifications accelerate enterprise deals, whereas those lacking compliance credentials face elongating sales cycles. Overall, the accounting software market rewards providers that demonstrate quantifiable ROI from automation and regulatory risk mitigation.

Accounting Software Industry Leaders

Oracle Corporation

Microsoft Corporation

SAP SE

Xero Ltd

Intuit Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Government-mandated digital invoicing and bookkeeping are creating near-term whitespace for vendors that can operationalize compliance across multiple jurisdictions within day-to-day accounting workflows. Denmark's mandated digital bookkeeping and e-invoicing regime for businesses above the 300,000 DKK turnover threshold took effect January 1, 2026, and Norway enacted mandatory digital bookkeeping and e-invoicing requirements on June 19, 2026, with provisions effective from January 1, 2027. In Asia-Pacific, Singapore's IRAS extended the GST InvoiceNow requirement with progressive mandatory participation beginning April 2026 for new voluntary registrants and a stated pathway to cover all GST-registered businesses by April 2031, favoring platforms with Peppol-aligned connectivity, e-invoice routing, and audit-ready data retention.

A second opportunity is emerging around AI-native close, bookkeeping, and firm workflow consolidation, as buyers rationalize fragmented point solutions into platforms that centralize data for automation while preserving audit trails. New category entrants and tools launched in July 2026 (for example, Wesley's AI bookkeeping platform for CPA firms and Puzzle's AI Suite with an AI Close tool) point to active product investment in human-in-the-loop automation for transaction categorization, reconciliation, and month-end processes. That, in turn, supports demand for accounting software that embeds agent-style assistance, integrates via APIs into payroll, banking, and spend tools, and produces immutable, reviewable logs suitable for regulated client work and emerging ESG-grade audit trails.

Recent Industry Developments

- July 2026: Xero launched an integration with Microsoft 365 that surfaces live Xero financial data inside Microsoft 365 applications, extending accounting workflows into everyday productivity tools. The release also referenced AI-enabled assistance through the JAX superagent in Microsoft 365 Copilot, raising expectations for agent-style experiences anchored to trusted ledger data.

- May 2026: Intuit introduced QuickBooks Workforce in the United States as an AI-native human capital management system for small and mid-market businesses. Bringing workforce operations closer to the core accounting stack strengthens cross-sell pathways between payroll, time, and financial close workflows.

- June 2025: TPG and Corpay completed the USD 2.2 billion acquisition of AvidXchange to expand payables automation capabilities for mid-market firms. The combination reinforced competitive pressure on accounting platforms to embed AP automation and payments functionality rather than rely on standalone bolt-ons.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the accounting software market covers paid software products used to record, process, and report financial transactions for businesses, including cloud-based and on-premises deployments. Revenues are counted from software license or subscription fees tied to accounting functions.

Scope exclusions: Free basic tools, custom in-house builds not sold commercially, and non-accounting adjacent tools that do not post to core financial records are excluded.

Segmentation Overview

- By Deployment Type

- On-premise

- Cloud-based (SaaS)

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By End-user Industry

- BFSI

- Manufacturing

- Retail and E-commerce

- Professional Services

- IT and Telecom

- Healthcare

- By Application

- Payroll Management

- Billing and Invoicing

- Expense Tracking

- Tax Management

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on how accounting software demand changes by region and business size, then mapping that to revenue pools. We rely on public sources such as US SEC filings, US Bureau of Labor Statistics, US Census Bureau business statistics, Eurostat enterprise ICT usage datasets, and OECD digital economy publications to understand business counts, cloud adoption signals, and wage cost pressure that encourages automation.

We also review company annual reports, earnings call transcripts, investor presentations, association websites, and reputable press coverage to cross-check product direction, pricing changes, and shifts in customer mix. In selected cases, we use paid subscriptions for company financials and intelligence, news and financials, and patent databases to verify revenue splits, M&A timing, and feature investment trends. These examples are illustrative, and many other public sources were referenced to collect, validate, and clarify inputs during the study.

Primary Interviews and Surveys

Primary work is used to test what the desk signals may miss, especially around pricing behavior, buying cycles, and the shift from on-premises to cloud. We spoke with a mix of software providers, implementation partners, accountants, and finance leaders across APAC, EMEA, and the Americas, and then rechecked key assumptions when responses did not match observed adoption and spend patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 22% | APAC: 39% |

| Mid tier: 42% | Functional/Unit leaders: 28% | EMEA: 36% |

| Smaller Players: 22% | Managers: 50% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enterprise counts and accounting-software adoption indicators are used to reconstruct a realistic spend pool for accounting software by region, and then the totals are split by deployment based on observed migration patterns. Once that structure is in place, we corroborate it using selective bottom-up approximations, like sampled average subscription pricing by business size multiplied by estimated active user bases, and supplier revenue direction checks for the larger participants.

A few inputs that matter in this market are the number of active small businesses and employers, the share of firms using cloud applications, accounting and bookkeeping labor cost inflation, typical subscription price bands by seat or module, and the pace of compliance and e-invoicing related process change in key countries. When a bottom-up cross-check cannot cover smaller geographies cleanly, we handle the gap by using validated penetration ranges from interviews and applying them to the same business-count base.

For forecasting, scenario analysis is used around two variables that consistently shift outcomes, cloud migration speed and pricing progression, and then results are sanity checked against expected SMB formation, enterprise digitization spending, and the pace of automation feature adoption that interviewees described.

Data Validation & Update Cycle

Validation is done through multiple passes so the model does not depend on one assumption. Model outputs are compared with independent signals such as reported software revenue trends, cloud adoption datasets, and regional IT spend direction, then large variances are investigated before sign-off. If the checks point to a data break, we re-contact relevant respondents and adjust the assumption with a documented reason.

Each report is refreshed annually, and interim updates are made when material events occur, such as major pricing changes, acquisitions, or regulation-led demand shifts. Before delivery, an analyst performs a fresh review of the latest public information so clients receive an updated view aligned with current market conditions.

Mordor Intelligence's Accounting Software Market Size Compared Against Other Published Estimates

Published market sizes for accounting software can differ even when the topic label looks the same, because the underlying scope and revenue counting rules are not consistent. Differences usually come from what is treated as accounting software versus adjacent finance tools, how services revenue is handled, and how fast pricing and cloud adoption are assumed to change.

Some estimates expand the scope by bundling broader finance applications and related services as one revenue pool. In Mordor Intelligence, the value is limited to accounting software revenue (cloud-based and on-premises) and it is kept separate from wider ERP, payments, or pure services-only revenue lines when they are not sold as software.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 21.56 B (2025) | |

| Global Consultancy A | USD 20.83 B (2025) | Uses a slightly different revenue boundary for accounting tools and may apply a tighter inclusion of add-on modules, which can lower the counted spend for the same year. |

| Trade Journal B | USD 20.03 B (2025) | Often follows a narrower revenue capture approach, with supply-side reporting conventions that can exclude parts of subscription revenue recognized through broader software bundles. |

The spread in the table is small, but it is still meaningful for planning because it mostly comes from scope choices and how bundled revenue is treated. Our approach keeps the sizing tied to clear demand drivers like business counts, cloud usage signals, and realistic pricing bands, which makes the final number easier to replicate and audit over time.

Key Questions Answered in the Report

How large is the global accounting software market in 2026?

The accounting software market size stands at USD 23.47 billion in 2026 and is on track to reach USD 35.86 billion by 2031.

What is driving the rapid shift to cloud-based accounting systems?

Enterprises favor cloud because it cuts infrastructure costs, supports distributed work, and enables continuous regulatory updates, resulting in a 68.08% revenue share for cloud deployments in 2025.

Which segment shows the fastest growth within accounting applications?

Payroll management leads with a 10.40% CAGR through 2031 owing to increasingly complex wage regulations and demand for same-day pay features.

Why is Asia-Pacific the fastest-growing region?

Mandatory e-invoicing programs across India, Japan and Southeast Asia compel businesses to upgrade from manual or legacy systems, driving a 10.45% regional CAGR.

Page last updated on: