Award Management Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

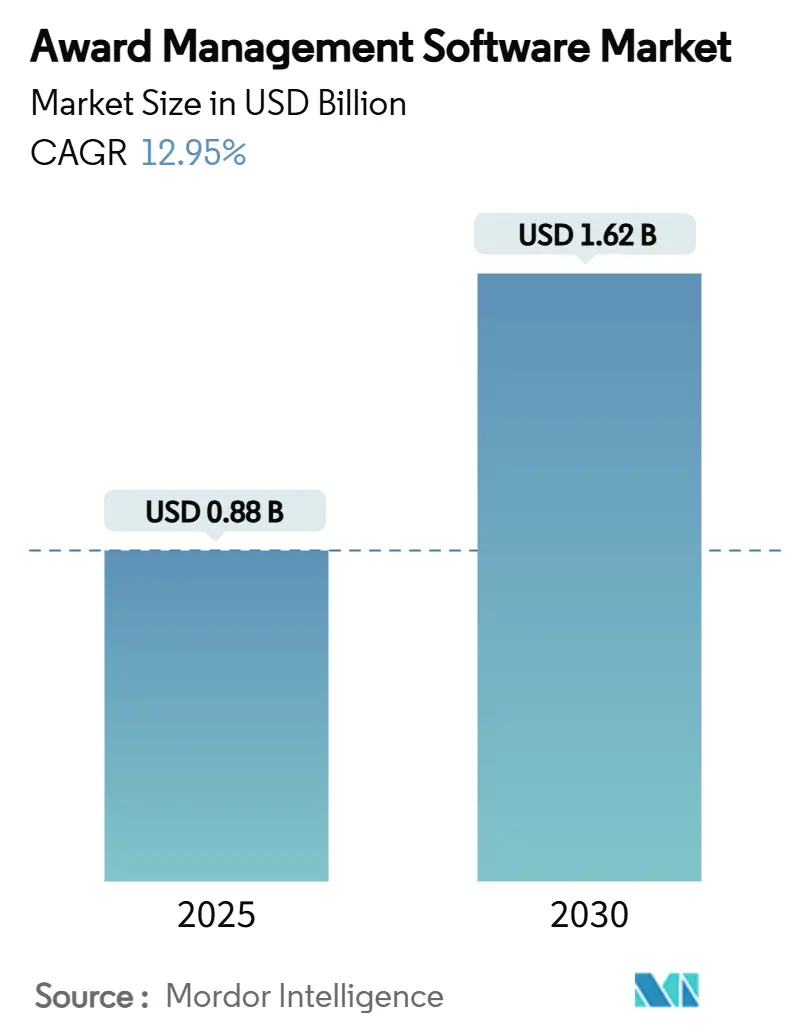

| Market Size (2025) | USD 0.88 Billion |

| Market Size (2030) | USD 1.62 Billion |

| Growth Rate (2025 - 2030) | 12.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Award Management Software Market Analysis by Mordor Intelligence

The award management software market size stands at USD 0.88 billion in 2025 and is forecast to rise to USD 1.62 billion by 2030, reflecting a 12.95% CAGR. Rapid migration from email‐ and spreadsheet‐based workflows to cloud platforms, the embedding of AI scoring engines, and rising compliance demands are the chief accelerators of growth. The market benefits from increasing enterprise preference for SaaS models that remove infrastructure burdens and deliver continuous security updates. API-first architectures also enable seamless connections with HR, finance, and CSR systems, driving ecosystem productivity. M&A activity among mid-tier vendors and private-equity interest in scale plays adds further momentum to platform innovation.

Key Report Takeaways

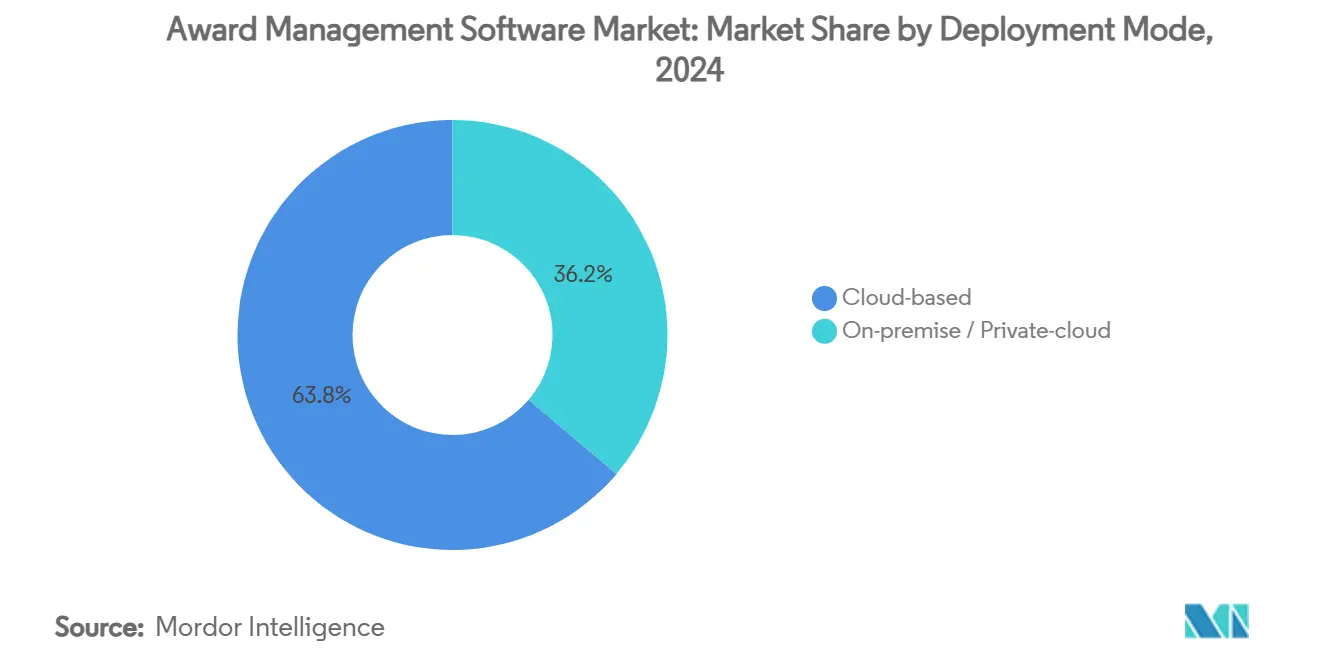

- By deployment mode, cloud solutions captured 63.81% of the award management software market share in 2024, while the cloud segment is expanding at 14.21% CAGR through 2030.

- By organisation size, SMEs held 56.23% revenue share of the award management software market size in 2024 and are growing at 13.04% CAGR through 2030.

- By end-user industry, corporations and enterprises led with 29.61% share in 2024; government agencies are advancing at 14.03% CAGR to 2030.

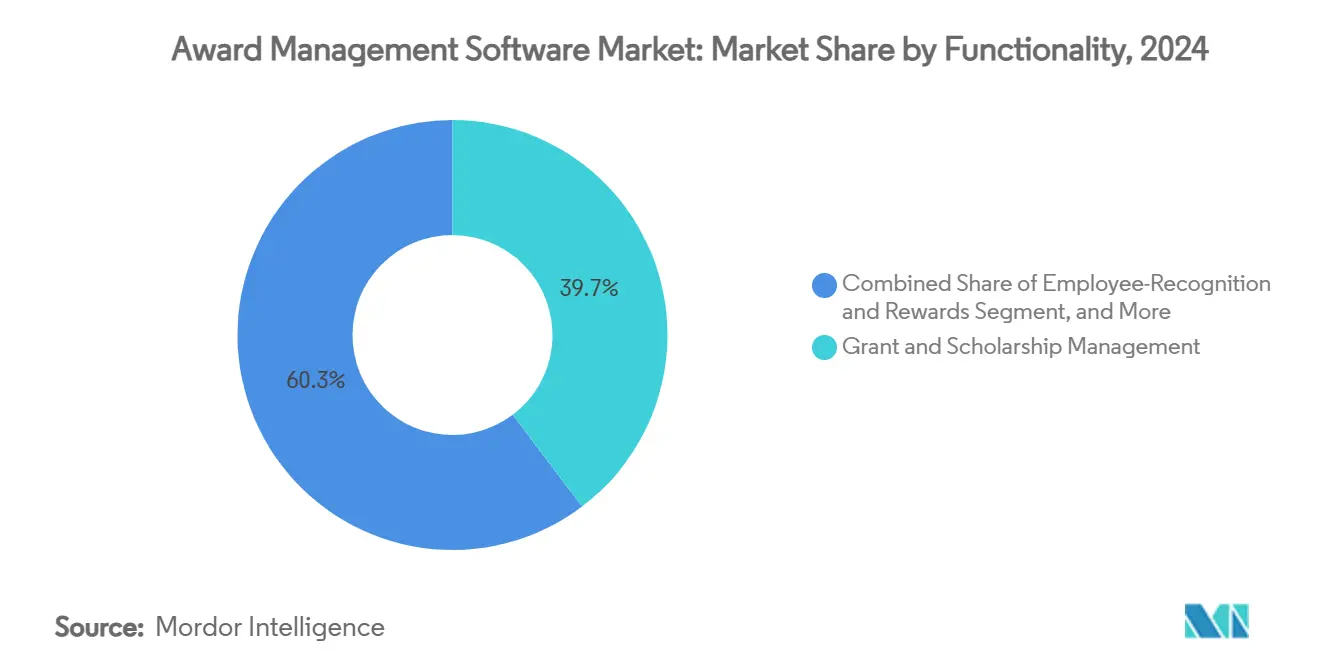

- By functionality, grant and scholarship management commanded 39.71% of the award management software market size in 2024, whereas corporate awards and innovation challenges are forecast to post the fastest 15.68% CAGR to 2030.

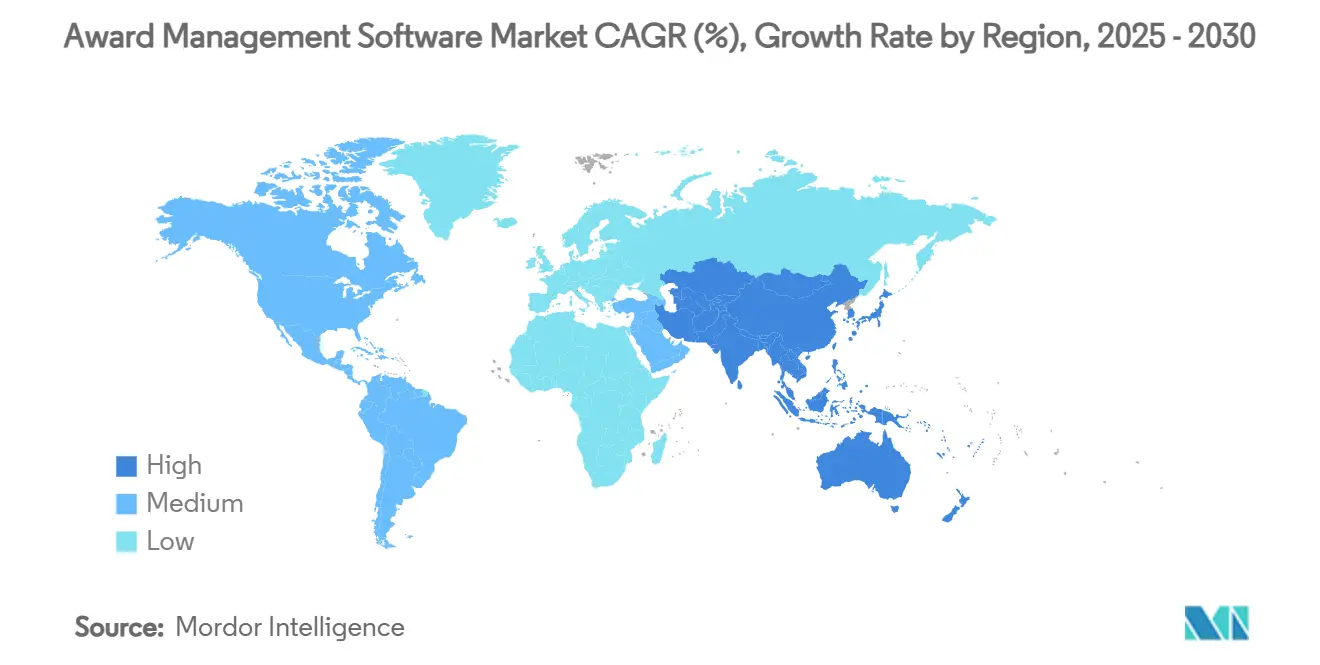

- By geography, North America accounted for 39.67% of the award management software market share in 2024; Asia-Pacific is projected to log a 16.03% CAGR between 2025 and 2030.

Global Award Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift from manual to SaaS-based award workflows | +3.2% | Global, with early adoption in North America & Europe | Short term (≤ 2 years) |

| Growing adoption of employee-recognition programs for DEI goals | +2.8% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Expansion of corporate social-impact and grant programs | +2.1% | Global, particularly strong in developed markets | Long term (≥ 4 years) |

| API-first platforms easing ecosystem integration | +1.9% | Enterprise-focused regions: North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Rising demand for data-driven judging and fraud-detection features | +1.7% | Global, with regulatory compliance drivers in EU | Short term (≤ 2 years) |

| Emergence of AI-powered application scoring and sentiment analytics | +1.4% | Technology-advanced markets: North America, Europe, East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift from Manual to SaaS-based Award Workflows

Award administrators are replacing email chains and spreadsheets because manual methods cannot process growing application volumes or satisfy audit requirements. SaaS platforms deliver instant deployment, automatic upgrades, and granular permission controls that reduce compliance risk. Remote and hybrid working models have normalised digital submission and review, accelerating the switch to cloud solutions. Agencies and foundations also see improved transparency, which is critical for public trust. Vendors that offer low-code configuration further reduce onboarding complexity.[1]Press Office, “Blackbaud Showcases the Future of AI-Powered Fundraising,” Blackbaud, investor.blackbaud.com

Growing Adoption of Employee-Recognition Programs for DEI Goals

Companies link recognition programs to measurable DEI objectives in order to build inclusive culture and improve retention. Platforms provide demographic analytics that help HR teams track participation across groups. AI bias-detection features surface disparities that manual reviews can miss, enabling faster course corrections. Organisations therefore allocate budget to systems that evidence the impact of DEI spend. Rising hybrid work arrangements heighten the value of digital recognition as employees seek visible appreciation.[2]Annual Report Team, “Microsoft 2024 Annual Report,” Microsoft Corporation, microsoft.com

Expansion of Corporate Social-Impact and Grant Programs

Stakeholders demand demonstrable ESG outputs, prompting corporations to increase philanthropic budgets and to professionalise grant workflows. Platforms help enterprises administer community funds, manage compliance, and publish outcome reports. Integrated analytics allow executives to benchmark program effectiveness. The trend widens adoption beyond traditional nonprofit users and supports mid-term revenue stability for vendors.

API-first Platforms Easing Ecosystem Integration

Enterprises require award software that plugs into identity, finance, and HR systems for unified data governance. API-centric products shorten deployment cycles by eliminating custom middleware. Open integration also enables extension through partner marketplaces, which expands platform stickiness. Vendors that expose comprehensive endpoints gain preference in competitive RFPs.[3]Corporate Blog, “SmartSimple Software and Foundant Technologies Announce Strategic Merger,” SmartSimple Software, smartsimple.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints among nonprofits and SMBs | -2.3% | Global, particularly acute in emerging markets and post-DOGE funding disruption areas | Short term (≤ 2 years) |

| Fragmented global regulatory requirements around data privacy | -1.8% | EU core impact with GDPR, spillover to global operations requiring multi-jurisdiction compliance | Medium term (2-4 years) |

| Inertia of legacy email/spreadsheet-based processes | -1.1% | Global, with higher resistance in traditional industries and government agencies | Short term (≤ 2 years) |

| Talent shortage in low-code/No-code configuration skills | -0.9% | North America & Europe primarily, expanding to APAC as adoption increases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints Among Nonprofits and SMBs

Many nonprofits operate on lean operating ratios that prioritise mission delivery over back-office investment. Subscription fees, even when modest, create recurring obligations that boards view as discretionary. Freemium offers lower the entry barrier but organisations often outgrow limited tiers, triggering upgrade friction. Economic uncertainty compounds hesitation in small businesses that compete for limited capital. Vendors are responding with outcome-based pricing that links cost to realised impact.

Fragmented Global Regulatory Requirements Around Data Privacy

GDPR in Europe, state-level rules in the United States, and localisation mandates in Asia require multifaceted compliance features. Smaller vendors struggle to maintain separate data-residency zones and consent frameworks. Buyers in multi-jurisdiction operations therefore extend evaluation cycles, delaying contracts. Compliance costs divert engineering resources from product innovation, which dampens competitive intensity in regional markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Accelerates Digital Transformation

Cloud deployments contributed USD 0.56 billion in 2024, equal to 63.81% of the award management software market size, and are forecast to grow at 14.21% CAGR through 2030. Lower ownership costs, instant scalability, and automatic security patches attract both enterprises and public agencies. Cloud vendors also release AI capabilities sooner because they control update cadence, enhancing value perception. On-premise solutions prevail where policy demands local data control, yet their market share continues to erode as hyperscalers obtain compliance certifications. API marketplaces and single-sign-on integrations further position cloud as the strategic option for digital transformation projects.

Cloud platforms support multi-tenant architectures that pool maintenance costs across customers, freeing product teams to focus on user experience. The ability to spin up test sandboxes encourages rapid workflow prototyping and stakeholder buy-in. Vendors that bundle cloud hosting with managed services capture higher retention because clients depend on vendor expertise for continuous optimisation. Licensing models based on active records rather than user counts also align spend with actual utilisation, easing procurement hurdles for finance departments.

By Organisation Size: SME Adoption Drives Market Expansion

SMEs accounted for 56.23% of the award management software market share in 2024 and are projected to log 13.04% CAGR to 2030. Affordable SaaS tiers and intuitive interfaces turn award programmes into self-service initiatives that fit limited staffing. SMEs leverage templated workflows to launch innovation challenges quickly, using award management software market tools that previously required enterprise budgets. Larger enterprises retain complex use cases such as multi-currency disbursement and cross-brand segmentation, which sustains premium tiers.

Budget-conscious nonprofits contribute to SME momentum, particularly in countries where philanthropic regulation insists on transparent grant adjudication. Peer-to-peer learning communities also influence purchasing decisions, as adjacent organisations showcase operational efficiencies. Vendors nurture these ecosystems through webinars and certification badges that build administrative confidence. The net effect is a virtuous cycle in which SME adoption broadens the installed base and drives word-of-mouth referrals.

By Functionality: Grant Management Dominates as Innovation Challenges Surge

Grant and scholarship management remains the largest functionality slice with 39.71% share of the award management software market share in 2024. This leadership stems from compliance-heavy funding workflows in government and philanthropy that require immutable audit trails. Automation of eligibility checks and budget tracking reduces administrative overhead, which is critical for high-volume grantors.

Corporate awards and innovation challenges are predicted to post 15.68% CAGR through 2030, the swiftest among functional segments. Internal hackathons and external open-innovation contests use AI ranking engines to evaluate ideas at scale, speeding time to product discovery. Employee-recognition and rewards modules sustain steady uptake, primarily as extensions to human-capital strategies aimed at curbing attrition. Marketing-driven loyalty awards compose a niche segment yet benefit from integration with CRM platforms that enrich customer lifetime value analytics.

By End-user Industry: Corporate Sector Leads While Government Accelerates

Corporations and enterprises held 29.61% of the award management software market size in 2024. They deploy platforms to unify employee recognition, innovation challenges, and CSR grants inside a single analytics environment. Standardised data improves cross-programme insights, helping executives demonstrate ROI to investors. Meanwhile, government agencies exhibit the fastest 14.03% CAGR because digital public‐service mandates require transparent and auditable grant processes.

Public-sector modernisation in Asia-Pacific, supported by the ASEAN Digital Masterplan 2025, underpins regional growth by requiring online citizen services that include seamless grant applications. Academia, conferences, and associations form a secondary cluster where recurring scholarship and award cycles create predictable demand. They value configurable review panels and plagiarism detection to maintain academic integrity. Vendors that offer domain-specific templates gain preference in competitive procurements.

Geography Analysis

North America contributed 39.67% of 2024 revenue due to widespread corporate governance standards and mature nonprofit ecosystems that depend on transparent award tracking. Early SaaS adoption culture and strong cloud-infrastructure penetration further solidify regional leadership. Vendors headquartered in the United States often pilot AI features in domestic markets before global release, reinforcing first-mover advantages.

Asia-Pacific is forecast to post the highest 16.03% CAGR from 2025 to 2030. Government digitisation programmes, particularly within ASEAN, compel agencies to shift to online grant portals, which directly stimulates award management software market demand. Rapid SME formation in India and Southeast Asia also boosts subscription volumes because new businesses adopt cloud tools from inception.

Europe records stable growth rooted in stringent ESG and data privacy statutes that favour auditable systems. However, cross-border data rules extend sales cycles as buyers evaluate regional hosting options. Latin America and the Middle East & Africa represent nascent markets where adoption is limited by budget constraints and lower cloud-infrastructure density. Pilot projects funded by multilateral development banks are beginning to showcase measurable efficiency gains, which will likely trigger broader regional uptake over the next five years.

Competitive Landscape

The market remains moderately fragmented yet shows steady consolidation. Blackbaud is the largest player, leveraging a broad product suite that spans fundraising, financial management, and grant administration. Its USD 4.1 billion acquisition proposal from Clearlake Capital underscores private-equity appetite for scale assets. SmartSimple and Foundant merged in 2024 to pool R&D and expand geographic reach, signalling that mid-tier vendors are combining to defend share in the award management software market.

Differentiation revolves around AI integration depth, user-experience simplicity, and the breadth of API connectors. Blackbaud’s Copilot assistant automates donor prospecting and invoice scanning, lowering administrative workload and improving user stickiness. Smaller challengers focus on mobile-first design and rapid onboarding to win price-sensitive clients.

Strategic partnerships with payment processors and HR suites extend platform relevance and create cross-sell opportunities. Vendors also invest in compliance certifications to meet regional data mandates, thereby unlocking regulated verticals such as healthcare and higher education. Continued investor focus on profitable growth suggests that feature roadmaps will prioritise margin-accretive AI modules rather than custom professional-services work.

Award Management Software Industry Leaders

Blackbaud, Inc.

WizeHive, Inc.

Submittable Holdings, Inc.

OpenWater, Inc.

Award Force Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Blackbaud posted Q1 2025 revenue of USD 270.7 million and reaffirmed full-year guidance, indicating durable demand for social-impact software despite divestment of EVERFI. The company stated that AI-based upsell modules will drive margin expansion, aligning with its Rule of 45 ambition.

- February 2025: Blackbaud closed 2024 with USD 1.2 billion GAAP revenue and highlighted operational efficiency initiatives to fuel cash flow for accelerated product innovation.

- November 2024: Blackbaud announced AI enhancements for Raiser's Edge NXT and Financial Edge NXT, showcasing plans to embed machine learning across its portfolio.

- October 2024: Microsoft reported USD 245 billion fiscal 2024 revenue and a 23% rise in Microsoft Cloud, validating enterprise migration to cloud services that underpin award management software market adoption.

Global Award Management Software Market Report Scope

| Cloud-based |

| On-premise / Private-cloud |

| Small and Medium-sized Enterprises (SMEs) |

| Large Enterprises |

| Grant and Scholarship Management |

| Employee-Recognition and Rewards |

| Corporate Awards and Innovation Challenges |

| Marketing / Loyalty Campaign Awards |

| Corporations and Enterprises |

| Non-profit and Philanthropic Foundations |

| Government and Public-sector Agencies |

| Academic and Research Institutions |

| Conference and Event Organisers |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-based | ||

| On-premise / Private-cloud | |||

| By Organisation Size | Small and Medium-sized Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Functionality | Grant and Scholarship Management | ||

| Employee-Recognition and Rewards | |||

| Corporate Awards and Innovation Challenges | |||

| Marketing / Loyalty Campaign Awards | |||

| By End-user Industry | Corporations and Enterprises | ||

| Non-profit and Philanthropic Foundations | |||

| Government and Public-sector Agencies | |||

| Academic and Research Institutions | |||

| Conference and Event Organisers | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the award management software market?

The market is valued at USD 0.88 billion in 2025.

How fast is the award management software market expected to grow by 2030?

It is projected to reach USD 1.62 billion, implying a 12.95% CAGR.

Which deployment model leads adoption?

Cloud platforms hold 63.81% share and are growing at 14.21% CAGR.

Which region will see the fastest growth?

Asia-Pacific is forecast to post a 16.03% CAGR through 2030.

What functionality segment is expanding the quickest?

Corporate awards and innovation challenges are growing at 15.68% CAGR.

How concentrated is vendor competition?

The top five players hold just over 40% share, signalling moderate concentration.

Page last updated on: