Size and Share of Compensation Management Market In Technology Sector

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

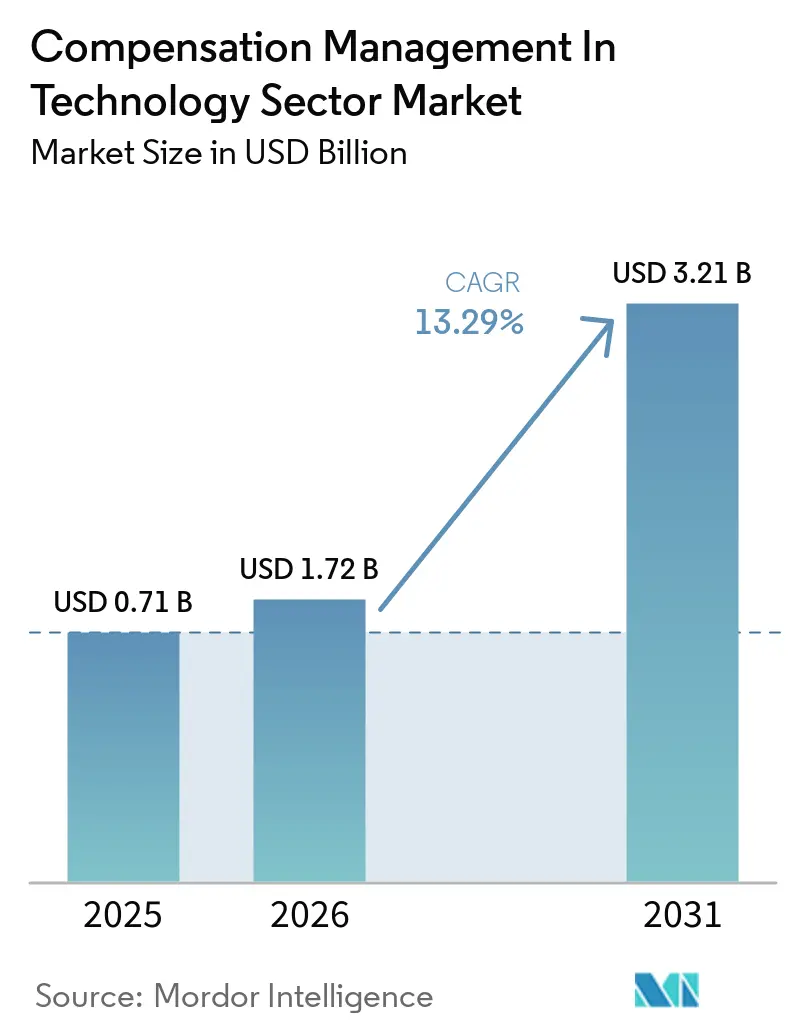

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 3.21 Billion |

| Growth Rate (2026 - 2031) | 13.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Compensation Management Market In Technology Sector by Mordor Intelligence

The Compensation Management Market In Technology Sector is projected to be USD 0.71 billion in 2025, USD 1.72 billion in 2026, and reach USD 3.21 billion by 2031, growing at a CAGR of 13.29% from 2026 to 2031. Compensation management in the technology sector is expanding as employers face tighter pay disclosure rules, more frequent equity reviews, and a greater need for defensible compensation records. The market is also benefiting from a shortage of AI, cloud, and cybersecurity talent, which is forcing employers to revise salary bands, incentive structures, and equity packages more often than annual review cycles allow. Spreadsheet-led compensation cycles are losing relevance because they do not provide the audit trail, workflow control, or cross-system visibility that large technology organizations now need. Vendor competition is increasingly shaped by integration quality, as buyers expect compensation tools to connect in real time with HRIS, payroll, finance, and equity systems. Another change in compensation management in the technology sector is that pay transparency rules are reducing the room for salary differentiation, pushing employers to rely more on equity and non-cash rewards that many older platforms still do not model well.

Key Report Takeaways

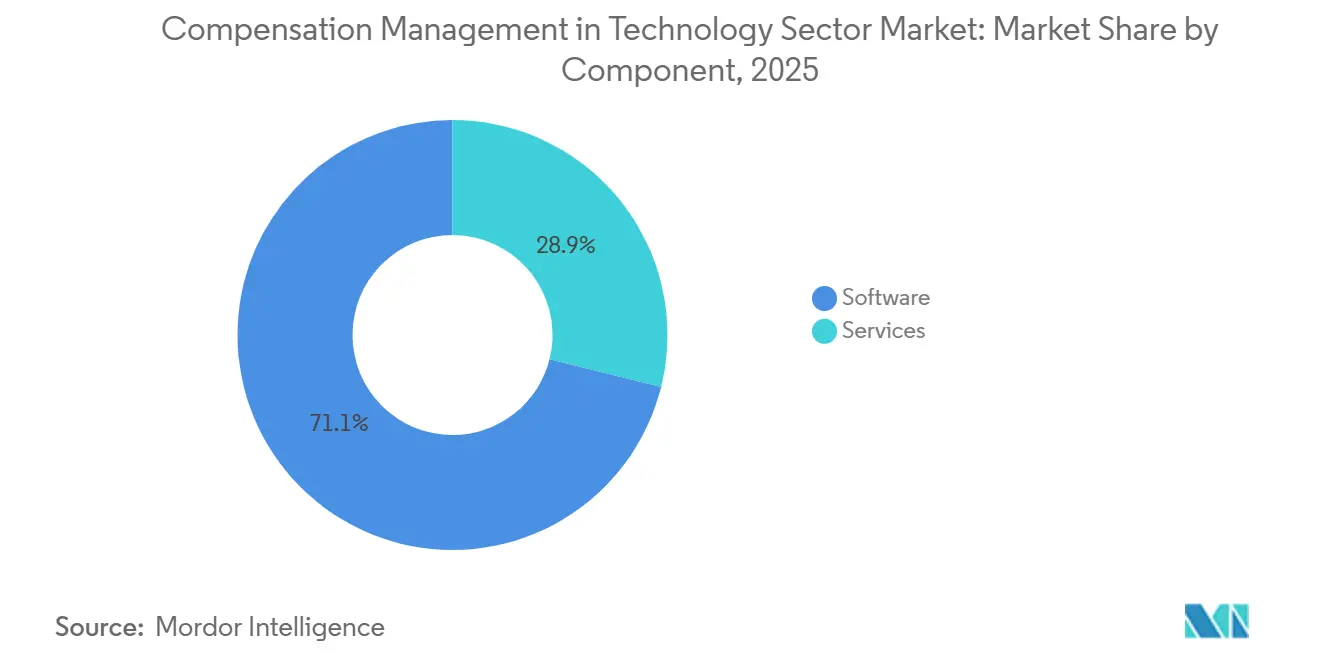

- By component, software led with a 71.12% share in 2025, while services are projected to expand at a 15.23% CAGR through 2031 in the Compensation Management Market In Technology Sector.

- By deployment mode, cloud-based deployment held 68.45% share of the the compensation management in the technology sector marke in 2025, while hybrid deployment is forecast to grow at a 14.89% CAGR through 2031.

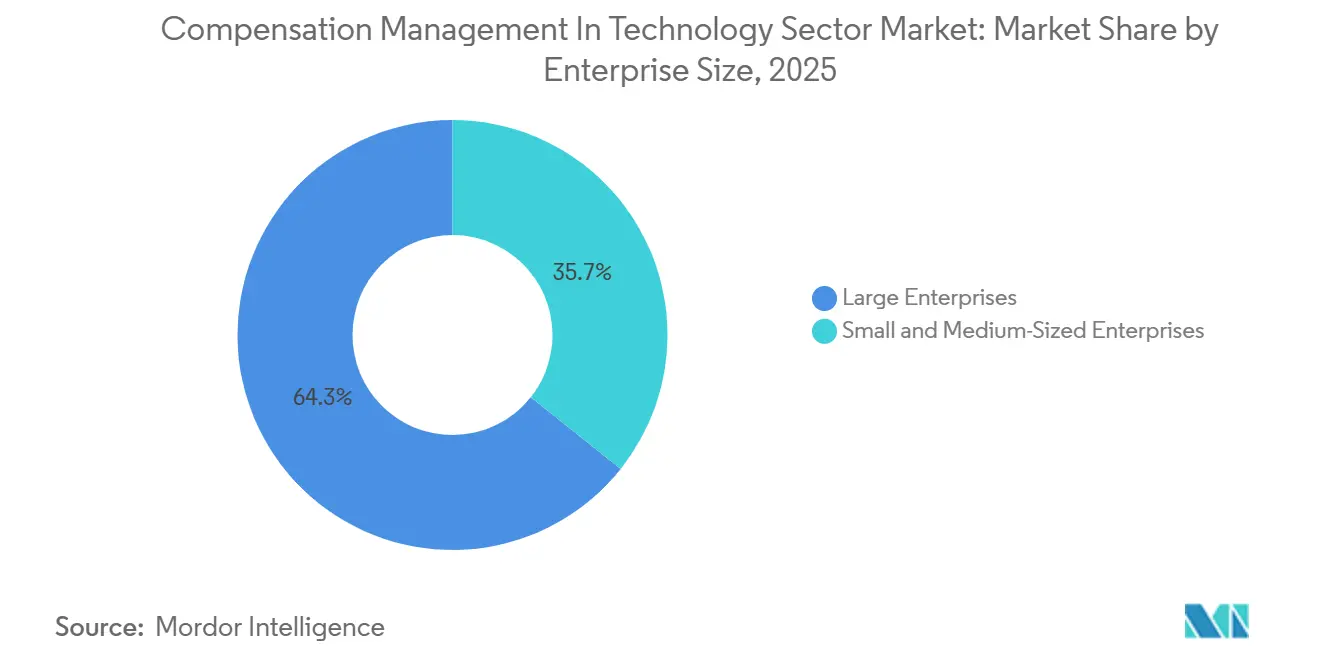

- By enterprise size, large enterprises accounted for 64.30% share of the compensation management market in the technology sector in 2025, while small and medium-sized enterprises are expected to record the fastest CAGR at 16.11% through 2031.

- By functionality, compensation planning captured 24.87% of the Compensation Management Market In Technology Sector in 2025, while compensation analytics and reporting are projected to grow at a 15.67% CAGR through 2031.

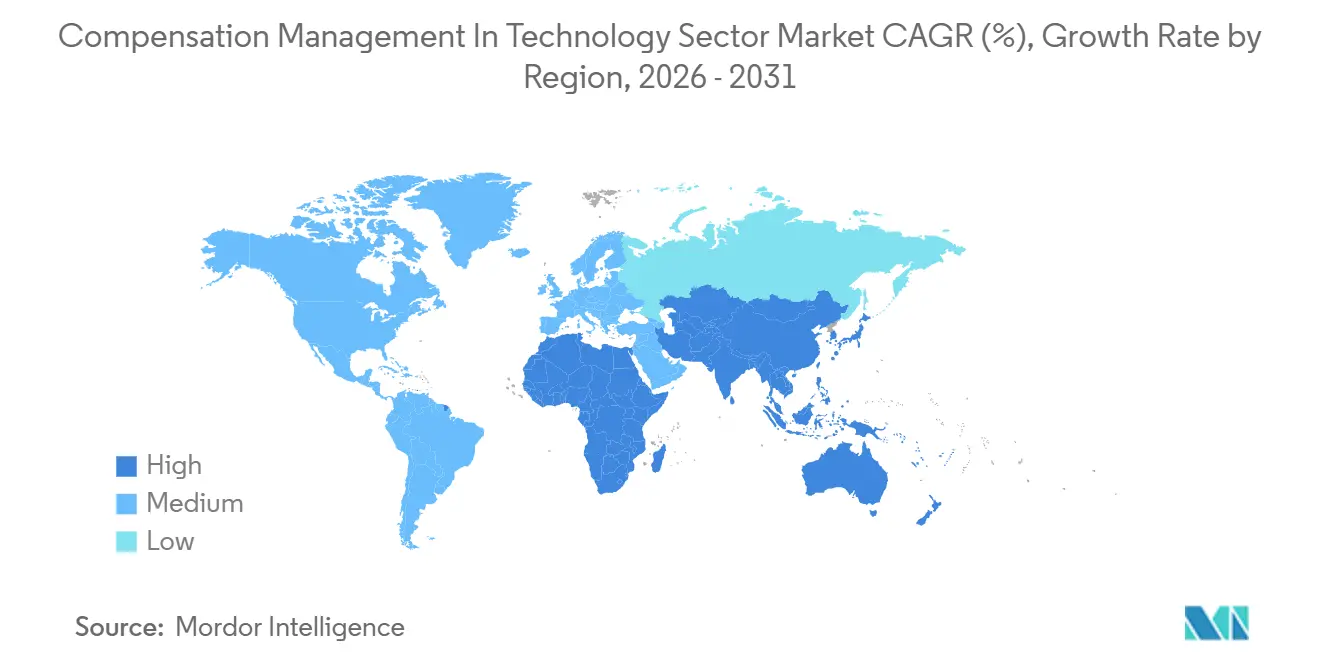

- By geography, North America held 41.05% of the compensation management market share in the technology sector in 2025, while Asia-Pacific is forecast to expand at a 16.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Compensation Management Market In Technology Sector

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pay Transparency and Pay Equity Compliance Deadlines | +3.5% | Global, with highest intensity in North America and EU | Short term (= 2 years) |

| Cloud and AI Adoption In Compensation Workflows | +2.8% | Global, with early gains in North America, EU, and APAC core | Medium term (2-4 years) |

| Competition for Scarce AI, Cloud, And Cybersecurity Talent | +2.2% | North America and EU, spill-over to India and Southeast Asia | Medium term (2-4 years) |

| Enterprise Shift from Spreadsheets to Audit-Ready Compensation Systems | +1.8% | North America, EU, and APAC core | Short term (= 2 years) |

| Growing Need For Multi-Country Compensation Governance In distributed Tech Teams | +1.4% | Global, especially North America with remote hubs in South America and APAC | Medium term (2-4 years) |

| Real-Time Benchmarking Demand as Annual Salary Surveys Age too Quickly | +1.0% | North America and EU, growing relevance in APAC | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Pay Transparency and Pay Equity Compliance Deadlines

The compensation management market in the technology sector is receiving a strong push from compliance deadlines, turning compensation software into a core control system rather than an optional HR tool. The June 7, 2026, deadline under the EU Pay Transparency Directive has forced technology employers to prepare pay-range disclosures, document pay decisions, and review internal pay gaps with much greater discipline. In the United States, pay transparency rules have also expanded across states, and employers posting remote roles must often align a single job opening with multiple disclosure obligations.[1]Colorado Department of Labor and Employment, “Equal Pay for Equal Work Act,” Colorado Department of Labor and Employment, cdle.colorado.gov Illinois has added similar expectations around salary transparency, increasing the pressure on employers that hire across multiple jurisdictions simultaneously. This is making jurisdiction‑aware compensation platforms more valuable for Compensation Management Market In Technology Sector, as they can maintain policy logic, approval history, and posting controls in a single system. The next wave of reporting obligations for employers with larger workforces is likely to keep compliance‑led buying active well beyond the first round of disclosure preparation.

Cloud and AI Adoption In Compensation Workflows

Compensation management in technology sector industry is also being shaped by the shift from annual compensation cycles to continuous decision support. In 2026, 81% of incentive compensation teams reported using AI in some capacity, and extensive users showed a 67% preparedness rate for market shifts, much higher than lighter users.[2]Clare McLeod, “The State of AI in Compensation Management, 2026 Stats and Trends,” Stello AI, getstello.ai One platform highlighted its AI Pay and Compensation Agent, which leverages real-time market data from over 700 enterprises and a large skills graph to support pay recommendations, achieving a 94% offer acceptance rate and a 23% reduction in time-to-offer.[3]Gloat, “AI Pay and Compensation Agent,” Gloat, gloat.com Another vendor added generative AI capabilities for pay equity analysis, budget scenario modeling, and real-time compensation simulation inside a SOC 2 Type II-compliant environment, showing how providers are embedding AI into enterprise control frameworks. In the compensation management market for the technology sector, these launches matter because buyers now expect systems to dynamically guide pay decisions as conditions change, not just summarize results after the cycle closes. Vendors that keep AI tied to auditability, governance, and secure deployment are likely to gain more trust than those positioning AI as a stand-alone feature.

Competition for Scarce AI, Cloud, And Cybersecurity Talent

The Compensation Management Market In Technology Sector is benefiting from the fact that scarce technical talent now forces employers to revisit compensation structures more often and with more precision. Technology employers cannot rely on a single annual salary benchmark when AI, cloud, and cybersecurity roles move faster than traditional review cycles. This is changing compensation from a back-office review process into a frontline tool for offer acceptance, retention, and internal equity management. The issue is not only higher pay levels but also the need to price equity grants, incentive triggers, and geographic differentials consistently across similar roles. In the compensation management in the technology sector market, platforms that can compare cash and equity in a single workflow are becoming increasingly useful, as many high-value candidates evaluate the full reward package rather than base salary alone. The result is steady demand for systems that help employers adjust pay logic quickly without losing governance or creating inconsistent offers across teams and countries.

Enterprise Shift from Spreadsheets to Audit-Ready Compensation Systems

The compensation management market in technology sector continues to benefit from enterprises' move away from spreadsheet-led compensation reviews. Spreadsheet-driven compensation cycles usually take 8–12 weeks, while AI-native platforms can reduce that cycle to 2 weeks or less, which changes the operating case for formal platforms. Spreadsheets also create a weak audit history, fragmented approvals, and limited control over who changed a pay recommendation and why. In compensation management in the technology sector, those weaknesses matter more now because disclosure rules and internal review expectations both require documented reasoning for compensation actions. It has also been reported that 51.4% of organizations still lack formal job architecture, meaning many employers are trying to modernize pay decisions while their role structures remain incomplete. That gap is helping structured compensation systems gain ground because they provide templates, workflows, and data governance that spreadsheets cannot reliably support at scale.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget-Constrained Pay Decisions Delay Suite Expansion | -1.8% | Global, most acute in SME segment and emerging markets | Short term (= 2 years) |

| Integration Complexity Across HRIS, Payroll, Equity, And Finance Systems | -1.5% | Global, particularly complex in large enterprises with multi-system architectures | Medium term (2-4 years) |

| Skill Premium Compression Forces Frequent Repricing of Tech Roles | -1.0% | North America, EU, APAC core | Medium term (2-4 years) |

| Salary-Source Misinformation And Location-Pay Friction Undermine Trust In Formal Pay Programs | -0.7% | North America and EU, where pay transparency laws amplify crowdsourced salary visibility | Long term (= 4 years) |

| Source: Mordor Intelligence | |||

Budget-Constrained Pay Decisions Delay Suite Expansion

The compensation management market in the technology sector still faces slower buying cycles as technology employers move into tighter budget-control periods. Many companies protect the core planning module first and delay spending on analytics, transparency, or equity extensions until headcount and hiring plans become clearer. This is especially visible among smaller technology firms that understand the governance need but cannot always defend a broader platform rollout during periods of hiring caution. The spending pattern does not usually remove compensation software from the roadmap, but it does stretch deployment into phases and reduce short-term module expansion. In the Compensation Management Market In Technology Sector, this favors vendors with bundled pricing and a wider product footprint, as buyers often prefer to deepen an existing relationship rather than add several point tools. That dynamic supports large platforms while making it harder for smaller vendors that cover only one narrow compensation use case.

Integration Complexity Across HRIS, Payroll, Equity, And Finance Systems

Compensation management in the technology sector market is also held back by the difficulty of connecting compensation data across HRIS, payroll, finance, and equity systems. Large technology employers often run compensation processes across multiple systems simultaneously, making it hard to achieve clean, real-time data flow. When market benchmarks, stock grants, payroll changes, and finance approvals are not updated in sync, the value of a compensation platform declines because recommendations become slower and less reliable. This issue is even more serious when employers need audit-ready reporting, because a fragmented system architecture can delay or weaken the evidence supporting a pay decision. In the compensation management market for the technology sector, vendors that offer strong connectors and flexible deployment options gain an advantage because integration quality often determines whether a platform is renewed or replaced. The same factor also explains why hybrid deployment is growing faster than simple cloud-only models among large technology employers with complex inherited system estates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Signals Complexity Beyond The Platform

Software accounted for 71.12% of the compensation management in the technology sector market in 2025, while services are projected to expand at a 15.23% CAGR through 2031. That split shows that software subscriptions remain the revenue base, but it also shows that buyers increasingly need support beyond the platform itself. In the compensation management market in the technology sector, demand for services is rising because multi-country compensation design, workflow setup, data migration, and policy alignment are difficult to execute with internal teams alone. The need for services also reflects the fact that compensation changes within technology firms often affect HR, finance, managers, recruiters, and legal teams simultaneously.

The compensation management in the technology sector is therefore moving toward a model in which software and services reinforce each other rather than compete for budget. Organizations with clean, connected compensation data tend to make faster decisions and adjust to labor shifts with less disruption, which increases the perceived value of implementation and advisory support. That outcome gap matters because many technology employers are not buying a tool alone; they are buying an operating model for compensation governance. Service demand is also supported by the growing use of security and compliance commitments in enterprise contracts, which pushes vendors and implementation partners to stay involved after the initial rollout.

By Deployment Mode: Hybrid Architectures Gain Ground Among Large Enterprises

Cloud-based deployment commanded 68.45% share in 2025, while hybrid deployment is forecast to grow at a 14.89% CAGR through 2031. The leading cloud position reflects the strong preference for managed infrastructure, easier updates, and smoother integration with modern HR systems. Even so, compensation management in the technology sector is not moving in a straight line from on-premises to the cloud, because many large employers still operate systems they cannot quickly replace. Hybrid models are gaining traction where employers want cloud analytics and workflow flexibility but still need local control for sensitive records, data residency requirements, or older enterprise architecture.

The compensation management market in the technology sector is seeing hybrid adoption rise because compensation data rarely resides in a single place. A large employer may use a cloud HRIS, on-premises finance tools, separate equity administration, and regional payroll systems, making a blended compensation layer more practical than a full replacement. The 2026 launch of Compose Insights and Predictive Compensation in a secure, SOC 2 Type II-compliant environment demonstrated that vendors are designing products that meet stricter enterprise governance expectations rather than assuming every buyer wants a simple cloud-only setup.[4]Decusoft, “Decusoft Advances the AI-Powered Future of Compensation Management With Compose Insights and Predictive Compensation,” Decusoft, decusoft.com As a result, hybrid growth is not a temporary transition in Compensation Management Market In Technology Sector; it reflects a durable need to support mixed estates across global technology organizations.

By Enterprise Size: SME Adoption Accelerates As SaaS Pricing Broadens Access

Large enterprises held 64.30% of the Compensation Management Market In Technology Sector share in 2025, while small and medium-sized enterprises are projected to grow at a 16.11% CAGR through 2031. Large employers still lead because their compensation processes are more complex, more regulated, and more likely to include layered merit, bonus, and equity structures. At the same time, compensation management in the technology sector is opening up to smaller technology firms because SaaS pricing, faster deployment, and more focused product design have lowered the entry barrier. This change is important because growth-stage employers now face many of the same compensation pressures as large companies, especially when they hire across states or countries.

Compensation management in the technology sector is also gaining traction among SMEs, as venture-backed and scale-up firms cannot rely on informal pay practices for long. Once hiring expands across multiple locations, manual management of salary bands, promotion logic, and disclosure rules becomes difficult to sustain. Smaller technology employers are also feeling more pressure to standardize skills-based pay, retention grants, and manager approvals, even if their total headcount remains modest. That is why SME growth is outpacing the enterprise tier, not because smaller firms are less complex, but because they are moving quickly from informal compensation practices to formal governance.

By Functionality: Analytics Rises As Boards Demand Pay Intelligence

Compensation planning held the largest share at 24.87% in 2025, while compensation analytics and reporting are projected to advance at a 15.67% CAGR through 2031. Planning remains the main entry point because employers often start by formalizing merit cycles, budget controls, and salary band reviews before expanding into deeper analytics. Still, compensation management in the technology sector is shifting toward broader intelligence, as boards and CFOs want real-time visibility into pay outcomes, not just annual-cycle outputs. This is lifting demand for modules that can track market alignment, scenario changes, internal equity issues, and reporting readiness in one place.

Compensation management in the technology sector is also changing because technology pay packages are no longer easy to assess based on cash compensation alone. Employers need to compare salaries, incentive pay, and equity when evaluating competitiveness for specialized technical roles. That requirement increases the value of analytics tools that can model trade-offs and explain why one package is more effective than another for a given role or geography. The white space remains at the point where equity modeling, real-time benchmarking, and pay transparency controls meet, because many platforms still cover only part of that decision chain.

Geography Analysis

North America accounted for 41.05% of the global compensation management in the technology sector market in 2025. The region leads because the United States combines a large technology employer base with active pay disclosure rules that keep compensation governance high on the agenda. Colorado’s enforcement record, including citation fines issued under the Equal Pay for Equal Work Act, shows that compliance risk is real rather than theoretical. COLORADO CDLE. Canada adds another layer of reporting expectations for cross-border employers, while Mexico is being influenced by compensation governance standards set by U.S. and European parent companies.

Europe was the second-largest regional market in 2025, with Germany, the United Kingdom, and France acting as the main demand centers. The compensation management market in the technology sector is receiving a structural boost in Europe because the EU Pay Transparency Directive has forced employers to prepare for a more formal, documented compensation process. National differences within Europe are also increasing the workload, as employers must adapt their regional compensation strategy to local disclosure, documentation, and employee consultation rules. Germany already had an established pay transparency framework, so many employers there are focused on upgrading existing systems rather than starting from scratch. Across South America, Brazil and Argentina remain the most active markets because multinational technology employers often apply North American and European compensation standards to their operations before local regulations fully require it.

Asia-Pacific is the fastest-growing region, and the compensation management market size in the technology sector is forecast to grow at a 16.73% CAGR through 2031. India, South Korea, and Southeast Asia are driving much of that momentum because technology hiring is expanding and distributed engineering models need stronger pay governance. China remains important, but local data controls and deployment preferences make hybrid or locally adapted models more relevant than simple cloud-only offerings. In the Middle East and Africa, adoption is earlier in the cycle, yet the United Arab Emirates, Saudi Arabia, South Africa, and Nigeria are drawing steady interest as regional technology operations grow under multinational compensation standards.

Competitive Landscape

The compensation management in the technology sector market remains fragmented, with specialized vendors competing alongside compensation modules offered by broader HCM platforms such as Workday, SAP, and Oracle. That structure leaves room for focused vendors to win deals through speed, domain depth, and product flexibility, even when larger suites benefit from existing enterprise relationships. Beqom strengthened its position through a USD 300 million strategic investment from Sumeru, which was directed toward product innovation and global expansion. At the same time, integration debt remains the main churn risk in compensation management in the technology sector, as buyers now expect real-time connectivity across HRIS, payroll, finance, and equity workflows.

Strategy in compensation management in the technology sector market is now clustering around three clear patterns: AI-led workflow automation, deeper ecosystem integration, and broader governance coverage. Xactly’s April 2026 Agent-to-Agent AI integration with ServiceNow demonstrated how vendors are embedding compensation and revenue operations into broader enterprise workflow environments rather than treating them as isolated modules. Decusoft’s March 2026 launch of Compose Insights and Predictive Compensation marked a second path, in which vendors aim to make advanced analytics and scenario modeling easier for HR and finance leaders within secure environments. Beqom’s acquisition of Our Tandem earlier had already pointed to a third path: linking performance, skills, and rewards in a single system so that a broader employee database supports compensation decisions. These moves show that vendor competition is no longer centered solely on compensation planning.

The compensation management market in the technology sector still has clear white space for a platform that brings together multi-country equity modeling, real-time benchmarking, and transparent pay governance. Buyers are raising the bar on security and trust, which means certifications and controlled AI deployment increasingly shape shortlist decisions even before pricing discussions begin. Specialists can still compete well when they solve a sharper problem than the large suites, especially around pay equity, incentive design, or benchmarking depth. The market is therefore likely to stay fragmented until a smaller group of vendors proves that it can combine data connectivity, audit-ready governance, and full rewards modeling better than the rest.

Leaders of Compensation Management Market In Technology Sector

Globoforce, Inc. d/b/a Workhuman

Awardco, Inc.

O.C. Tanner Company

Achievers Solutions Inc.

Reward Gateway UK Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Xactly launched its Fleet of Agents and Intelligence Studio for revenue planning and compensation at its Upside 2026 conference. The Intelligence Studio provides a composability layer enabling Xactly, its customers, and partners to create and configure AI agents based on specific business rules, extending AI capabilities beyond pre-built use cases.

- May 2026: Xactly and ServiceNow launched an Agent-to-Agent AI Integration for Revenue Operations, introducing the Dispute Management AI Agent powered by the Model Context Protocol (MCP). This represents the first of several planned agents within the framework and automates compensation dispute workflows for sales teams and administrators.

- April 2026: Gloat launched its AI Pay and Compensation Agent, integrating real-time market data from 700+ enterprises with a knowledge graph of 2.4 million skill nodes and 18.7 million relationships to generate pay recommendations, achieving a reported 94% offer acceptance rate and a 67% reduction in pay equity exceptions.

- March 2026: Xactly launched its AI Lab, described as an innovation engine for enterprise-ready agentic AI in sales performance management. Early outputs from the Lab include Incent Agents, the Plan Configuration Agent, reducing plan modeling cycle time from weeks to days in simulations, and cross-cloud integration validation via MCP architecture.

Scope of Report on Compensation Management Market In Technology Sector

The Compensation management in the technology sector market involves digital solutions that streamline and optimize employee pay structures, incentive programs, equity compensation, and pay transparency across technology enterprises. These platforms integrate compensation planning, analytics, and reporting to ensure fairness, compliance, and alignment with organizational goals. Available through cloud, on-premises, or hybrid deployments, they serve both large enterprises and SMEs in the technology industry. Their core purpose is to enhance workforce motivation, retention, and equity by connecting compensation strategies with broader HR and business performance objectives.

The Compensation Management Market In Technology Sector report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Functionality (Compensation Planning, Base Pay Management, Incentive Compensation Management, Equity Compensation Management, Pay Equity and Transparency Management, and Compensation Analytics and Reporting), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Compensation Planning |

| Base Pay Management |

| Incentive Compensation Management |

| Equity Compensation Management |

| Pay Equity and Transparency Management |

| Compensation Analytics and Reporting |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Functionality | Compensation Planning | |

| Base Pay Management | ||

| Incentive Compensation Management | ||

| Equity Compensation Management | ||

| Pay Equity and Transparency Management | ||

| Compensation Analytics and Reporting | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the Compensation Management Market In Technology Sector by 2031?

The Compensation Management Market In Technology Sector is projected to reach USD 3.21 billion by 2031, rising from USD 1.72 billion in 2026 at a CAGR of 13.29% over 2026-2031.

What is driving demand for compensation software in technology companies?

The main demand drivers are pay transparency rules, pay equity compliance, talent shortages in specialized roles, and the need to replace spreadsheet-led compensation cycles with audit-ready systems.

Which component leads revenue and which one is growing fastest?

Software held the largest share at 71.12% in 2025, while services is the fastest-growing component with a 15.23% CAGR through 2031.

Why is hybrid deployment growing faster in compensation platforms for technology employers?

Hybrid deployment is growing because large employers often need cloud flexibility while keeping some HR, finance, payroll, or equity data in legacy or locally controlled environments.

Which enterprise size segment is expanding the fastest?

Small and medium-sized enterprises are growing the fastest, with a 16.11% CAGR through 2031, as SaaS pricing and multi-location hiring make formal compensation tools more accessible and more necessary.

Which region leads today and which region is growing the fastest?

North America led with 41.05% share in 2025, while Asia-Pacific is forecast to record the highest growth rate at a 16.73% CAGR through 2031.

Page last updated on: