Europe Mid-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

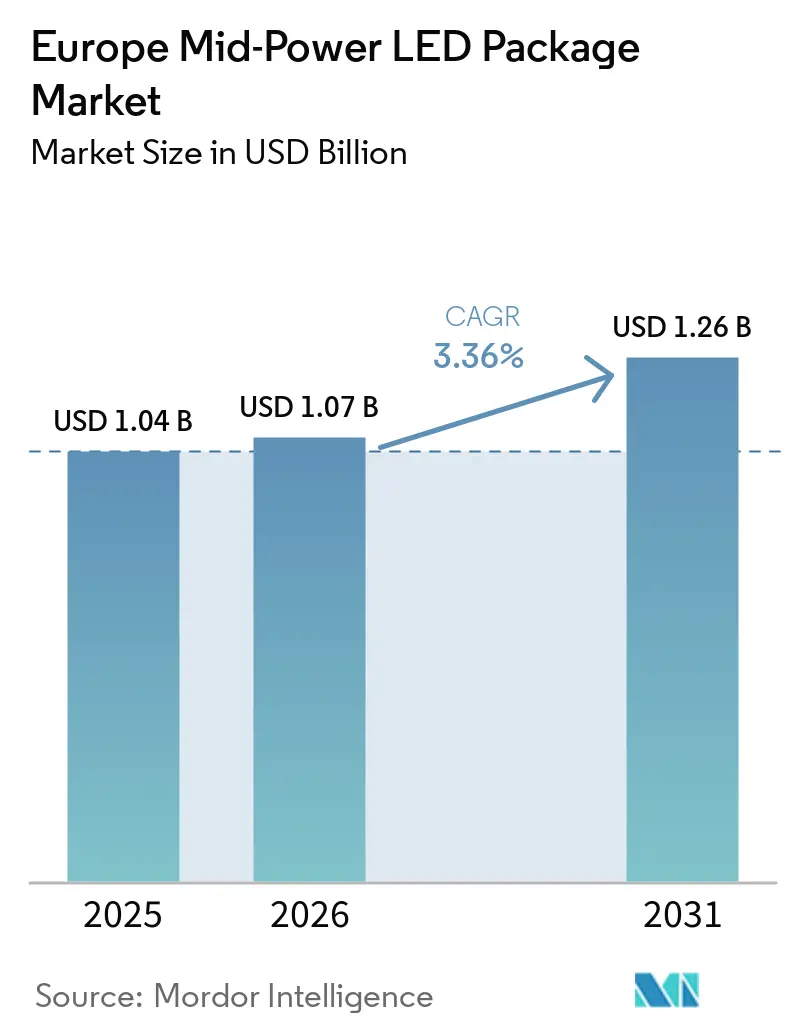

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

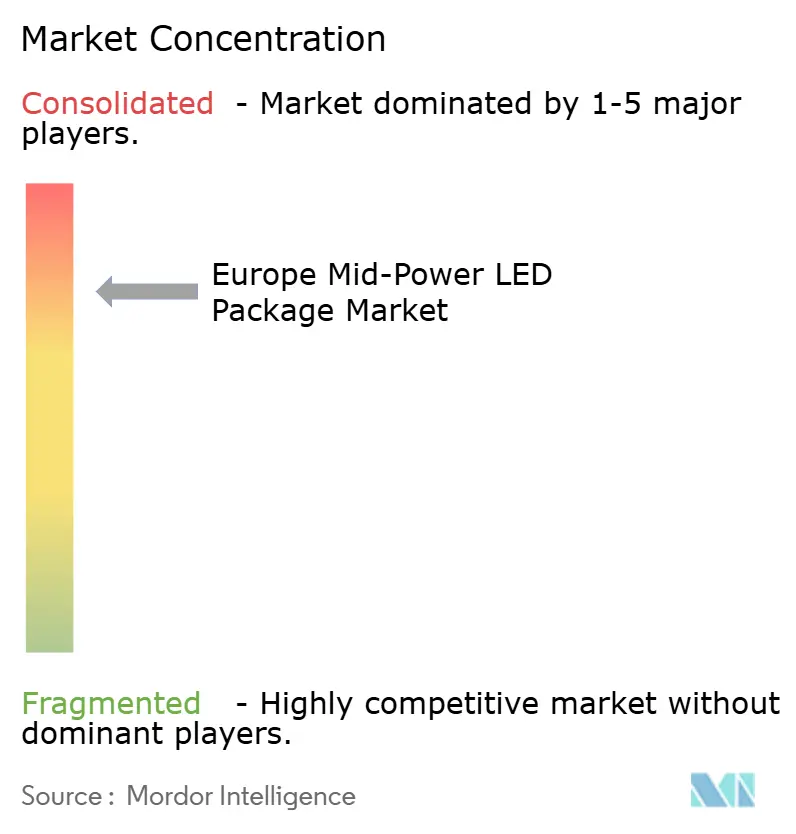

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mid-Power LED Package Market Analysis by Mordor Intelligence

The Europe mid-power LED package market size is expected to increase from USD 1.07 billion in 2026 to reach USD 1.26 billion by 2031, growing at a CAGR of 3.36% over 2026-2031. General lighting retrofits, advanced automotive headlamp designs, and expanding smart-city programs together keep demand on a steady, replacement-cycle-driven path rather than the hyper-growth seen during the first adoption wave of the last decade. Surface-mount device (SMD) formats remain the dominant architecture because municipal and commercial fixture lines are already tooled for them, while chip-scale options gain share in automotive, horticultural, and sensor-dense luminaires that need thin profiles and excellent thermal management. Regulatory pressure from the EU Green Deal and related building-performance mandates locks LED technology in as the only compliance pathway, giving suppliers dependable baseline volumes even as wafer-price shocks narrow margins. Competitive strategies now center on intellectual property enforcement and integration know-how rather than pure cost-cutting, reflecting a maturing technology landscape that rewards patent depth and module-level solutions.

Key Report Takeaways

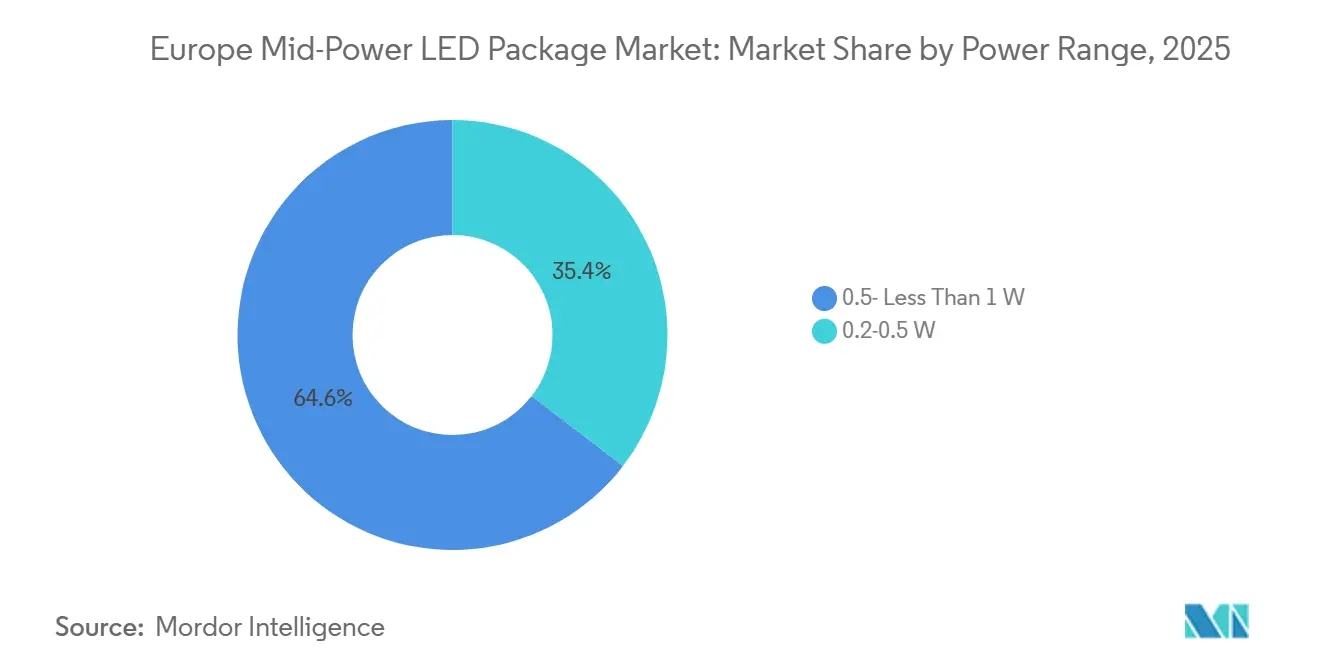

- By power range, the 0.5-watt-to-less-than-1-watt segment accounted for 64.58% of the Europe mid-power LED package market size in 2025 and is set to grow at a 3.91% CAGR during 2026-2031.

- By packaging architecture, SMD devices held 74.84% revenue share in 2025, while chip-scale packages are forecast to expand at a 3.77% CAGR through 2031.

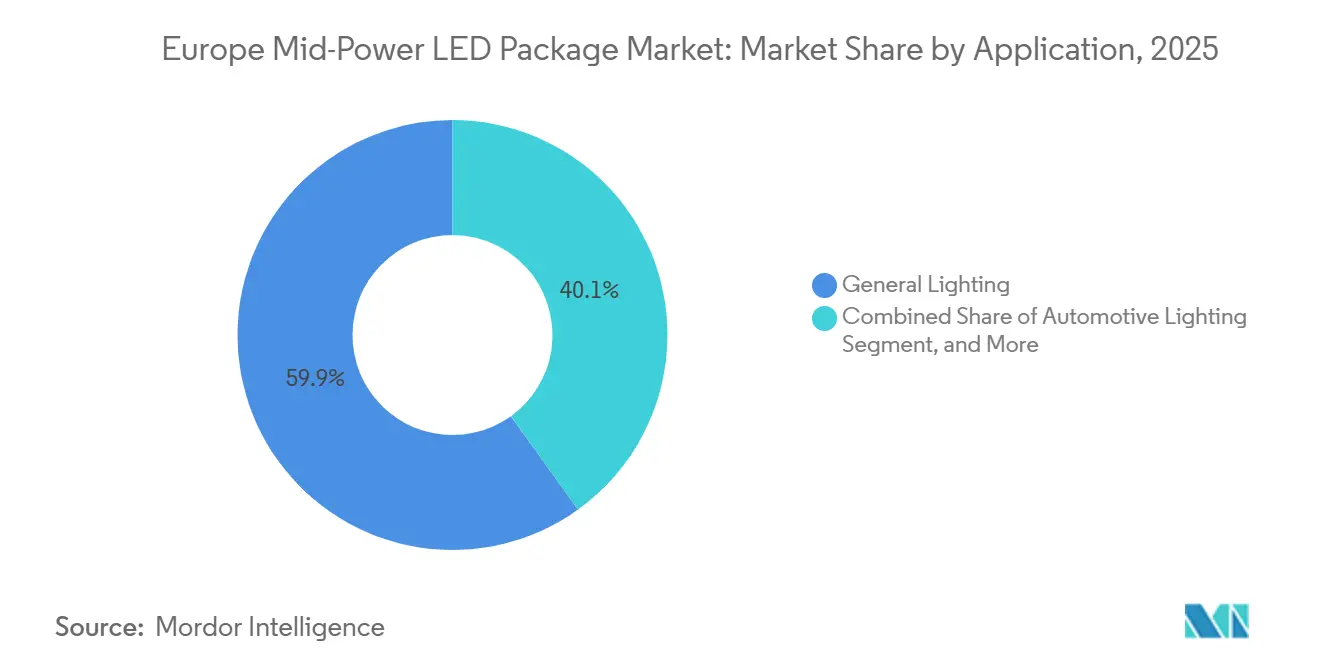

- By application, general lighting accounted for 59.93% of the Europe mid-power LED package market share in 2025, and automotive lighting is projected to advance at a 3.84% CAGR through 2031.

- By country, Germany led with 28.34% of regional revenue in 2025, while France is expected to record the fastest growth at a 3.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Mid-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in Miniaturized Lighting Demand from European Automotive OEMs | +0.9% | Germany, France, Italy, spillover to the UK and Spain | Medium term (2-4 years) |

| Rapid Conversion of Fluorescent Luminaires to LED in Public Infrastructure | +0.8% | Germany, UK, Italy, Spain | Short term (≤ 2 years) |

| Energy-efficiency Mandates Under the EU Green Deal | +0.7% | EU-27, strongest in Northern and Western Europe | Long term (≥ 4 years) |

| Accelerating Build-out of Smart Street-lighting Networks | +0.6% | Germany, UK, France, Central and Eastern Europe | Medium term (2-4 years) |

| Growth of Horticultural Vertical Farms in Northern Europe | +0.3% | UK, Netherlands, Denmark, Norway, and pilot sites in Germany | Long term (≥ 4 years) |

| Emergence of Micro-optics to Boost Mid-power Package Lumen Output | +0.2% | R&D clusters in Germany, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Miniaturized Lighting Demand from European Automotive OEMs

Premium vehicle platforms now ship with tens of thousands of individually addressable LEDs that must fit inside ever-thinner optical chambers. Mercedes-Benz equipped the 2026 S-Class with a 50,000-unit Digital Light system that extends beam reach to 605 m while cutting energy draw by 50%, proving that precision optics can coexist with lower power budgets.[1]Motor 283, “Digital Light System Details,” motor283.com Seoul Semiconductor’s WICOP modules supply 200% higher luminance than prior products and shrink heatsink mass by 75%, meeting automotive duty cycles without wire bonds that can fail under vibration.[2]LEDinside, “Seoul Semiconductor WICOP Production,” ledinside.com The same miniaturization logic extends to transparent foil rear lamps and communication panels introduced by ams OSRAM, expanding the mid-power package pull beyond core headlamp channels.

Rapid Conversion of Fluorescent Luminaires to LED In Public Infrastructure

Municipalities are fast-tracking street-lighting upgrades because the 2025 RoHS mercury bans make fluorescent tubes non-compliant. The IEA 4E SSL Annex measured lifecycle environmental gains of 44%- 61% when T5 and T8 lamps are replaced with LED equivalents.[3]IEA, “4E SSL Annex Life-Cycle Assessment,” iea.orgCities such as Noventa Padovana, Córdoba, and West Sussex documented 50%-plus electricity savings within months of commissioning, with blended EU grants trimming simple payback to fewer than five budget cycles. As cohesion funds expire in 2026, procurement departments are bunching orders, which feeds a temporary demand spike for SMD 2835 and 5630 formats that slot into legacy fixtures.

Energy-Efficiency Mandates Under EU Green Deal

Commission Delegated Regulation (EU) 2024/1781 raises the luminous-efficacy floor to 140 lm/W for directional lamps from 2026, guaranteeing that LED is the only compliant option across commercial and public buildings. The Energy Performance of Buildings Directive further compels upgrades by requiring member states to renovate the poorest-performing 15% of non-residential buildings by 2030. German pilots in Wedemark achieved 80% energy savings and EUR 270,000 in annual cost savings after cloud-managed LEDs replaced sodium lamps, illustrating the financial upside when regulatory push meets digital controls.[4]Enercity, “Wedemark Smart Street-Lighting Pilot,” enercity.de

Accelerating Build-Out of Smart Street-Lighting Networks

Full-scale smart-city deployments now tie luminaire upgrades to sensor platforms, remote-fault alerts, and Wi-Fi backhaul. Dortmund installed 45,000 node-level-controlled LED poles that prevented 2,080 t of CO₂ in only six months while enabling future parking-space and air-quality services.[5]Tvilight, “Dortmund Smart Street-Lighting Case Study,” tvilight.com Brighton and Hove follows with 20,000 posts, suitable for central management, aimed at achieving 61% energy cuts. Municipal buyers specify 100,000-h lifetimes and tight thermal envelopes, tilting preference toward chip-scale packages that can withstand heat trapped in pole enclosures.

Drivers Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Indium Gallium Nitride Wafer Price Swings | -0.5% | Germany and France face the sharpest cost pressure due to their high automotive LED share; ripple effects across the wider region | Short term (≤ 2 years) |

| Cheaper Chinese LED Package Imports Eroding Margins | -0.4% | Southern and Eastern Europe remain most exposed where anti-dumping safeguards are less stringent | Medium term (2-4 years) |

| Shift by Luminaire Makers Toward Integrated Light Engines | -0.4% | Germany, Netherlands, and France lead the move as in-house R&D teams favor board-level modules | Long term (≥ 4 years) |

| Heat-dissipation Limits in Compact Chip-scale Packages | -0.3% | Automotive clusters in Germany, France, UK, plus horticulture projects in Italy and Spain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Indium Gallium Nitride Wafer Supply

China’s August 2023 export quotas pushed gallium prices up by 123% by late 2025, lifting epitaxial wafer costs. European assemblers already operate on approximately 20% gross margins, so pricing shock forces either end-product hikes or throughput rationalization. Recycling loops that could recover gallium at scale remain theoretical, making supply security a near-term strategic risk for German and French automotive LED chains.

Threat of Price Erosion from Chinese Imports

After EU anti-dumping rulings, Chinese exporters still account for a significant inbound LED package volume by routing through tariff-friendly hubs. Unit prices on commodity 2835 and 5630 SMDs remain 20%-30% below European equivalents, especially in Southern and Eastern European fixture shops that accept 2%-3% field-failure rates. Matter certification, obligatory for smart-lighting gear from 2026, raises compliance hurdles, yet leading Shenzhen suppliers clear audits in under one year, limiting the shelter domestic makers expected.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Mid-Tier Wattages, Anchor Volume, and Growth

The 0.5-watt-to-less-than-1-watt slice captured 64.58% of the Europe mid-power LED package market share in 2025. Efficacy-optimized chips in this bracket light residential downlights, commercial troffers, and daytime running lamps, sustaining a 3.91% CAGR that beats the overall market. Lumileds’ Luxeon CS series reaches 174 lm/W while staying within the EU Ecodesign C to E bands, securing specification slots in new build projects.

As smartphone backlights migrate to mini-LED and OLED, sub-0.5-watt packages lose volume. At the opposite end, 1- to 3-watt devices serve high-bay fixtures that demand longer lumen maintenance, and the niche above 5 watts attracts buyers in Nordic horticultural setups that have received public R&D funding for vertical farming. WICOP’s packageless structure blurs classic wattage markers by pushing automotive modules past 200% prior luminance without separate ceramic carriers.

By Packaging Architecture: Chip-Scale Gains Despite SMD Incumbency

SMD formats generated 74.84% of 2025 revenue because pick-and-place lines across Europe were designed around them. Even so, chip-scale alternatives are on track for a 3.77% CAGR through 2031 as automakers, signage builders, and smart-pole integrators reward low z-height and fewer failure points. A 2025 Journal of Optical Microsystems paper proved that wafer-level fan-out on 12-inch glass reduced package area by 42% while achieving 99.8% electrical yield.

Chip-on-board solutions dominate high-density downlights and fine-pixel displays and may migrate into general lighting when aluminum nitride substrates tame thermal spikes. SMD stays relevant when procurement prioritizes the lowest euros per lumen, but every automotive refresh pulls more demand toward wire-bond-free chip-scale devices that survive vibration and deliver pixel-level addressability.

By Application: Automotive Lighting Outpaces General Lighting on OEM Refresh Cycles

General lighting still accounts for 59.93% of 2025 shipments, yet automotive lamps are set for a 3.84% CAGR as brands weaponize lighting signatures for model-year updates. BMW broadened adaptive LEDs and laser rear lights to mainstream trims in late 2025, and Mercedes-Benz rolled star-pattern running lamps into the wider portfolio, both of which consume mid-power chips in the 0.5-watt class.

Horticulture adds incremental pull thanks to vertical farm rollouts in the Netherlands, Denmark, and the UK, where red-blue spectra cut energy use by 40% while improving cucumber yields by 18%. Meanwhile, LCD backlighting fades as mini-LED tablets reach scale. Outdoor signage migrates to chip-on-board modules that deliver higher contrast, cannibalizing discrete mid-power volume.

Geography Analysis

Germany’s leadership rests on a unique mix of premium car production, strict building codes, and municipal appetite for digital infrastructure. The Wedemark pilot that swapped 4,300 sodium lamps for cloud-managed LEDs achieved 80% energy savings and EUR 270,000 in annual utility savings, serving as a template for over 11,000 German towns. Local electricity prices above EUR 0.25 per kWh further shorten the payback period for retrofits.

France gains momentum as cities unlock EU grants covering up to 70% of project capital if carbon milestones are proven. Many municipalities postponed upgrades during the 2020-2022 pandemic, so pent-up demand now coincides with regulatory deadlines that penalize inefficient luminaires.

The UK landscape is characterized by bundled contracts that turn every pole into a multipurpose data node. Brighton and Hove’s 20,000-unit conversion includes Wi-Fi, parking sensors, and air-quality probes, demonstrating how lighting budgets can fund broader smart-city aims. Rising commercial electricity tariffs, which crossed GBP 0.30 per kWh in 2026, accelerate such decisions.

Southern markets like Italy and Spain remain cost-sensitive, yet shared funding windows prompt multiple cities to tender simultaneously. Parma’s 16,000-luminaire roll-out will save EUR 725,000 (USD 8,460,24.25) per year and meet national efficiency targets, while Córdoba’s 4,723-lamp project will deliver EUR 900,000 (USD 10,50,237) in savings with a roughly four-year payback. Central and Eastern Europe trails by about two years but benefits from EU cohesion monies plus manufacturers relocating final module assembly to cut freight time and hedge tariff risk.

Competitive Landscape

Five suppliers, namely ams OSRAM, Samsung, Nichia, Lumileds, and Seoul Semiconductor, together owned a significant share of 2025 revenue, a level that indicates moderate concentration without monopoly power. Signify tilts the field by licensing 1,700-plus EnabLED partners that place dies directly on driver boards, a model that removes discrete package demand but boosts royalty income.

Seoul Semiconductor wields an 18,000-strong patent arsenal, having secured injunctions across nine jurisdictions, and chose the newly effective EU Unified Patent Court to file against Amazon Services Europe in March 2024, an action that covers 17 countries in a single suit. Such litigation raises entry barriers for price-only competitors.

White-space growth sits in horticultural and automotive communication lighting. ams OSRAM’s VegaLED for plant growth and Aliyos transparent-foil pixel strings won early design-ins with European and Chinese automakers, hinting at future royalty-based revenue streams. Taiwanese suppliers retreat from commodity packages toward infrared and photonics niches to defend 20%-plus gross margins, leaving room for Chinese firms to chase high-volume SMD orders despite anti-dumping duties.

Europe Mid-Power LED Package Industry Leaders

ams OSRAM AG

Samsung Electronics Co., Ltd.

Nichia Corporation

Lumileds Holding B.V.

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lumileds released Luxeon CS chip-on-board LEDs with 174 lm/W efficacy, compliant with EU Ecodesign C-E categories, targeting downlights and track fixtures.

- March 2026: West Sussex County Council began a GBP 24.2 million (USD 32.42 million), four-year plan to retrofit 64,000 streetlights with smart-enabled LED heads, aiming to cut 10.7 million kWh annually.

- February 2026: Everlight Electronics sued Lumileds in Europe over LED package patents, underscoring intensified IP enforcement.

- January 2026: Mercedes-Benz launched the Digital Light headlamp with 50,000 micro-LEDs per vehicle, delivering 605 m beam reach and halving power draw.

Europe Mid-Power LED Package Market Report Scope

The Europe Mid-Power LED Package Market Report is Segmented by Power Range (0.2-0.5 W and 0.5- Less Than 1 W), Package Architecture (SMD including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| 0.2-0.5 W |

| 0.5- Less Than 1 W |

| SMD (Surface Mount Device) | 2835 |

| 3014 | |

| 3030 | |

| Others (3528, 3020, 5050, etc.) | |

| CSP (Chip Scale Package) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Power Range | 0.2-0.5 W | |

| 0.5- Less Than 1 W | ||

| By Package Architecture | SMD (Surface Mount Device) | 2835 |

| 3014 | ||

| 3030 | ||

| Others (3528, 3020, 5050, etc.) | ||

| CSP (Chip Scale Package) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the Europe mid-power LED package market in 2026?

The market is estimated at USD 1.07 billion in 2026.

What is the forecast CAGR for Europe mid-power LED packages to 2031?

The market is projected to grow at a 3.36% CAGR during 2026-2031.

Which package type is gaining share the quickest?

Chip-scale packages are expected to post a 3.77% CAGR as automakers and smart-pole projects demand thinner, thermally efficient formats.

Why is France the fastest-growing national market?

Deferred municipal retrofits now align with EU grant deadlines, resulting in a 3.93% CAGR forecast for 2026-2031.

How are EU regulations driving LED adoption?

Minimum efficacy rules of 140 lm/W under Delegated Regulation 2024/1781 and building-performance mandates effectively eliminate fluorescent and halogen options, securing LED as the compliance path.

What risk does gallium price volatility pose?

China’s export quotas pushed gallium costs up 123% in 2025, squeezing wafer margins and pressuring European package assemblers that rely on high-purity indium gallium nitride substrates.

Page last updated on: