Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.16 Billion |

| Market Size (2031) | USD 21.49 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LED Packaging Market Analysis by Mordor Intelligence

The LED packaging market size is projected to expand from USD 16.50 billion in 2025 and USD 17.16 billion in 2026 to USD 21.49 billion by 2031, registering a CAGR of 4.60% between 2026 and 2031. Mid-power surface-mount device (SMD) packages still anchor the installed base, yet chip-scale package (CSP) formats and flip-chip options are growing at a faster clip as display backlighting, automotive matrix lights, and horticulture luminaires demand thinner profiles, higher luminance, and robust thermal performance. Automotive lighting absorbs the most visible innovation, with adaptive driving beam headlamps moving from premium models into volume segments, while ultraviolet (UV) packages gain momentum as governments phase out mercury lamps. Competitive pressure shifts from simple price wars to patent positioning, cross-licenses, and vertical integration, highlighted by San’an Optoelectronics’ plan to close its USD 239 million purchase of Lumileds in early 2026.

Key Report Takeaways

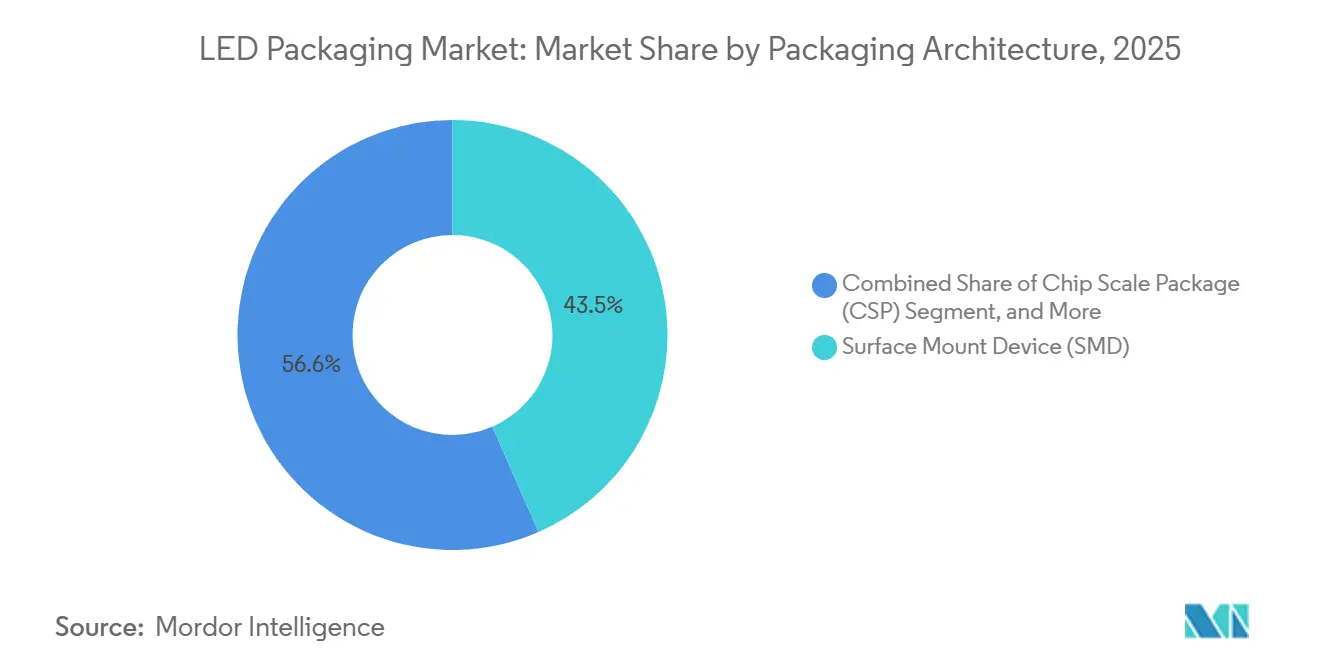

- By packaging architecture, SMD formats commanded 43.45% of the LED packaging market share in 2025, whereas CSP designs are forecast to post the fastest 5.11% CAGR through 2031.

- By power class, the mid-power 0.5-1 W segment accounted for 37.67% of the LED packaging market size in 2025, while high-power 1-3 W packages are projected to expand at a 4.98% CAGR during 2026-2031.

- By emission type, visible packages captured 88.28% of the revenue share in 2025, and UV packages recorded the highest growth with a 4.88% CAGR to 2031.

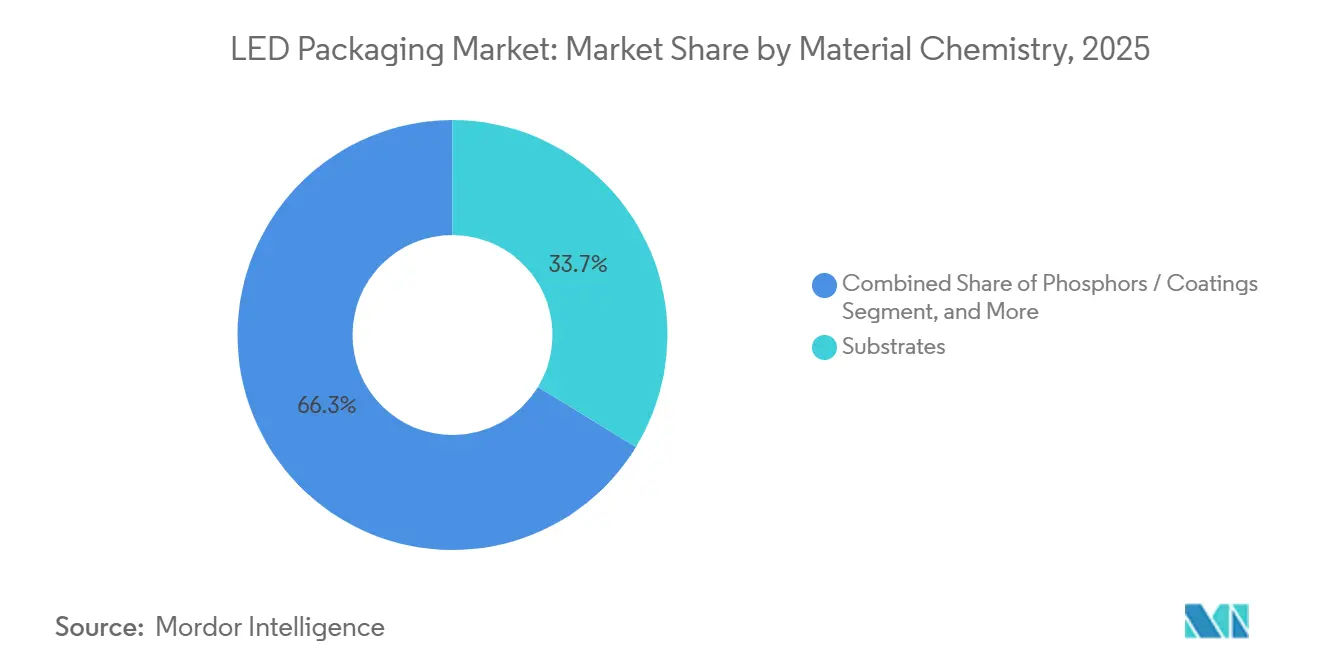

- By material chemistry, substrates represented 33.71% of total component spend in 2025, whereas phosphors and coatings are set to grow the quickest at a 5.28% CAGR over the forecast period.

- By application, general lighting accounted for 41.29% of the LED packaging market share in 2025, while automotive lighting is advancing at the strongest 5.17% CAGR through 2031.

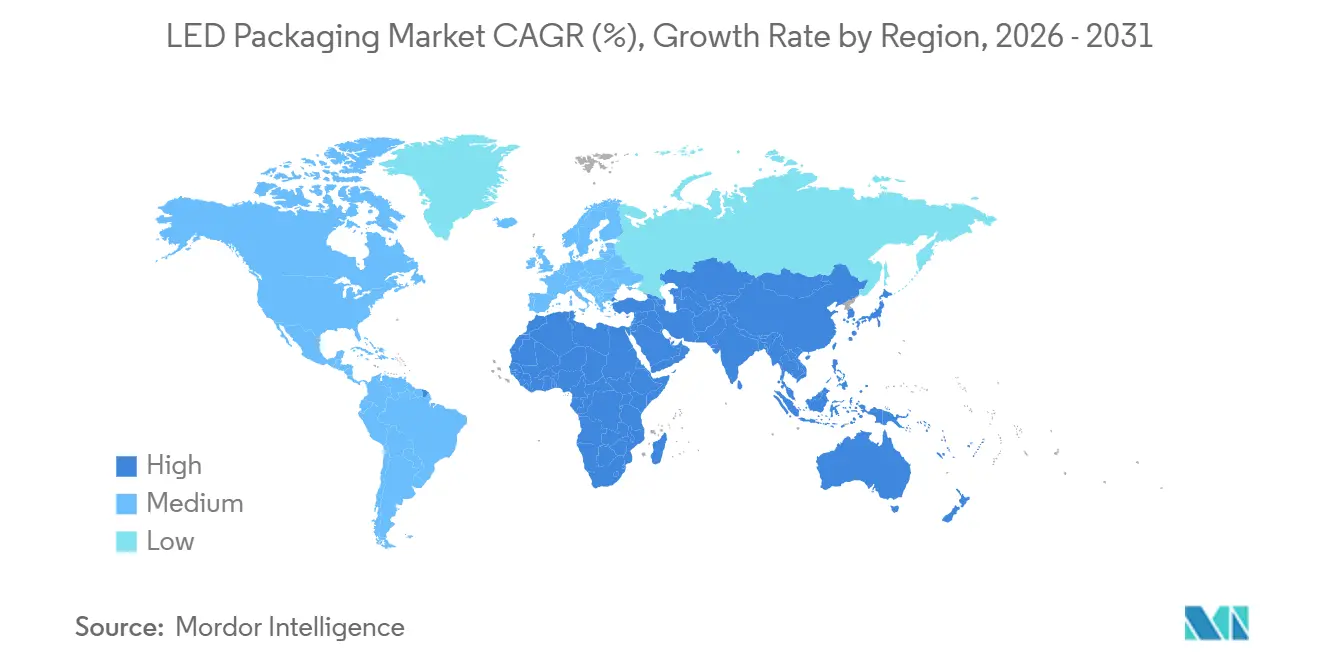

- By geography, Asia-Pacific retained 68.55% revenue share in 2025 and is projected to grow at a leading 5.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global LED Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Adoption of Mini-LED Backlights in IT Products | +1.0% | Global, led by Asia-Pacific and North America | Short to Medium term (≤ 3 years) |

| Accelerated Automotive Shift to Adaptive Matrix LED Headlamps | +0.9% | Global, led by Europe and North America | Medium to Long term (3-5 years) |

| Government Bans on Mercury-Based Lighting Products | +0.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rapid Fab Capacity Build-Out in China for Advanced CSP Lines | +0.6% | Asia-Pacific core, spill-over to global markets | Medium term (2-4 years) |

| On-Device Opto-Biometric Sensors Driving IR LED Demand | +0.5% | Global, concentrated in consumer electronics hubs | Medium term (2-4 years) |

| Emerging Horticulture Solid-State UV-B Illumination Systems | +0.3% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Mini-LED Backlights in IT Products

Demand for thinner laptops, vivid monitors, and high-contrast tablets has vaulted mini-LED backlighting into mainstream production. Each direct-lit panel requires five to ten times as many dies as its edge-lit predecessors, increasing total unit consumption even as average selling prices decline. CSP packages offer sub-millimeter pitch, low z-height, and tight wavelength binning, which premium display brands now specify as baseline. Packaging houses that automate optical inspection at gigapixel throughput and ship pre-binned arrays capture the most value, while legacy SMD suppliers reliant on manual pick-and-place platforms struggle to compete.[1]Consumer Technology Association, “CES 2026 Show Report,” ces.tech

Accelerated Automotive Shift to Adaptive Matrix LED Headlamps

Automotive original equipment manufacturers (OEMs) have prioritized matrix and pixel lighting to improve driver visibility without glare. Audi’s 25,600-pixel headlamp prototype exemplifies the jump in on-board emitter count, pushing high-power CSP and flip-chip packages that withstand −40 °C to +150 °C cycles and meet AEC-Q102. Europe advances fastest under Regulation 123, giving regional suppliers early revenue, while the United States awaits final glare thresholds from the National Highway Traffic Safety Administration. Suppliers with automotive-grade quality systems win design-ins and lock multi-year production contracts.[2]AKE Group, “Global Automotive Lighting Outlook 2026,” ake-lighting.com

Government Bans on Mercury-Based Lighting Products

Canada’s nationwide mercury lamp prohibition, effective January 2026, combined with accelerated Department of Energy phase-outs in the United States, forces commercial and industrial owners to retrofit fluorescent fixtures. Replacement lamps and high-bay luminaires favor mid-power and high-power SMD packages delivering ≥150 lm/W and a color rendering index above 80. Retrofit urgency insulates volumes from broader economic cycles and rewards integrated-module packages that embed driver electronics for fast installation.[3]United States Department of Energy, “Fluorescent Lamp Phase-Out Schedule,” energy.gov

Rapid Fab Capacity Build-Out in China for Advanced CSP Lines

More than USD 390 million of new CSP and mini-LED investment across Jiangsu and Guangdong provinces expands monthly output by hundreds of thousands of wafers. Local clustering of epitaxy, dicing, phosphor coating, and final packaging shortens cycle time and cuts unit cost by 15%-25% compared to dispersed chains. These savings pressure global prices and risk short-term overcapacity, prompting Western and Japanese firms to pivot to niche, high-qualification segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Patent-Thicket Litigation Costs for Flip-Chip Designs | -0.7% | Global, concentrated in United States and Europe | Short to Medium term (≤ 3 years) |

| Supply Tightness of High-CRI Red Phosphors | -0.5% | Global | Short to Medium term (≤ 3 years) |

| Thermal-Management Challenges Above 3 W Ultra-High-Power Class | -0.3% | Global, acute in automotive and industrial segments | Medium to Long term (2-5 years) |

| Price Erosion from Over-Capacity in Low-Power SMD Packaging | -0.6% | Asia-Pacific, affecting global pricing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Patent-Thicket Litigation Costs for Flip-Chip Designs

Everlight, Nichia, Seoul Semiconductor, and Lumileds continue to file cross-border infringement suits, averaging USD 5 million in legal spend per case. Damages debates over lost profits versus reasonable royalties elevate uncertainty and force smaller entrants to allocate reserves rather than fund research and development. Cross-licensing among incumbents creates barriers that slow new entrants and extend monetization for established portfolios.

Supply Tightness of High-CRI Red Phosphors

Next-generation red phosphors such as Li₅MgSrAlB₁₂O₂₄:Eu²⁺, Mn²⁺ achieve 91% internal quantum efficiency and 86.7% output retention at 150 °C, yet batch synthesis at >1,200 °C constrains scaling. Current per-gram costs are three to five times higher than commodity mixes, leading to allocation during peak quarters and disadvantaging small-volume buyers. Color-critical markets like premium retail, galleries, and medical lighting feel the pinch most acutely.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Architecture: CSP Gains on SMD Installed Base

Surface-mount device formats commanded 43.45% of the LED packaging market share in 2025, a lead built on decades of automated assembly infrastructure. CSP alternatives eliminate lead frames and mold compounds, shrinking profiles below 0.5 mm and boosting optical extraction. CSP sales climb on a 5.11% CAGR, pushed by mini-LED backlighting and wearable devices that demand thin modules. Automotive and industrial buyers retain chip-on-board and flip-chip arrangements for superior thermal paths, yet litigation costs temper rapid migration. Integrated-module devices combine driver integrated circuits with the emitter array, reducing the bill of materials and appealing to luminaire OEMs that favor supply-chain simplification.

SMD suppliers defend their share through high-speed pick-and-place throughput and pervasive socket compatibility. Nonetheless, price erosion from surplus Chinese capacity compresses margins, accelerating the shift toward high-reliability niches where CSP and flip-chip packages provide both performance and cost headroom at volume. Legacy through-hole and dual-in-line formats fade in outside indicator and specialty retrofits.

By Power Class: High-Power Packages Ride Automotive and Industrial Demand

Mid-power 0.5-1 W packages captured 37.67% of the LED packaging market size in 2025, buoyed by general lighting retrofits. High-power 1-3 W devices expand at a 4.98% CAGR, reflecting adaptive matrix headlamps and factory machine-vision luminaires that each need individual emitters exceeding 100 lumens with rapid switching. Ultra-high-power units above 3 W penetrate stadium, horticulture, and industrial bays but carry junction-to-case thermal targets under 2 °C/W, steering materials toward copper substrates, diamond-like interface layers, or even microchannel coolers.

Indicators with a power consumption of 0.5 W are increasingly subject to commoditization and substantial price reductions. The automotive sector, characterized by its stringent requirements such as AEC-Q102 certification and the ability to withstand 3,000 thermal cycles, distinctly separates itself from consumer-grade product lines. This differentiation necessitates that manufacturers refine and optimize their production processes to cater to the specific demands of each power category. Consequently, this approach results in the allocation of capital to distinct reliability standards, ensuring compliance with the varying requirements of these markets.

By Emission Type: UV LEDs Carve Specialty Niches

Visible packages held 88.28% share in 2025 and remain dominant across the lighting, signage, and display sectors. UV LEDs, though smaller in volume, post a 4.88% growth rate as water treatment, surface sterilization, and controlled-environment agriculture swap mercury lamps for solid-state emitters. Nichia’s 280 nm deep-UV launch in 2024 at 7.4% wall-plug efficiency exemplifies incremental improvements that unlock regulated markets demanding mercury-free systems.

Infrared packages provide biometric authentication, night vision, and free-space optics, with smartphones and access control systems favoring the 850 nm and 940 nm bands. Controlling wavelength shift with temperature is critical, as a 0.3 nm/°C drift can impair sensor accuracy. Emission segmentation follows fundamental band-gap engineering, granting durable competitive advantage to epitaxy specialists who master specific wavelength stacks.

By Material Chemistry: Phosphor Innovation Drives Value Migration

Substrates accounted for 33.71% of component spend in 2025, with ceramic and metal-core boards governing thermal diffusion. Phosphors and coatings, rising at 5.28%, deliver the spectral tuning that underwrites high-CRI white and specialty wavelengths. Encapsulants, led by high-temperature silicones, shield dies from moisture and UV degradation, but cost two to three times comparable epoxies. Advanced bonding pastes and copper wire die-attach slash thermal resistance and shrink first-level interconnect cost.

Intellectual property fences surrounding YAG: Ce, PFS, and CASN formulations impose licensing fees and create sourcing constraints, significantly influencing market dynamics. Suppliers that adopt vertical integration in phosphor synthesis not only secure their profit margins but also effectively reduce risks associated with allocation. On the other hand, packagers heavily dependent on outsourcing face challenges such as spot shortages and highly volatile pricing, which can disrupt their operations and profitability.

By Application: Automotive Lighting Outpaces General Illumination

General illumination still accounted for 41.29% revenue in 2025 as LED penetration passed 70% in mature economies. Automotive lighting is growing fastest at a 5.17% CAGR, driven by pixelated headlights and expanding rear signature functions. Display backlights embrace mini-LED arrays, swapping edge-lit lightbars for thousands of local dimming zones, which multiply package counts.

Industrial and specialty niches, ranging from horticulture to medical phototherapy, are placing an increasing emphasis on the importance of custom spectra and precise binning. The introduction of innovative product classes, such as intelligent OptiLamp packages integrated with advanced sensors, marks a significant evolution in the industry. These data-ready lighting nodes represent a paradigm shift, where the focus is transitioning from the delivery of raw lumens to enabling advanced diagnostics and facilitating predictive maintenance capabilities.

Geography Analysis

Asia-Pacific retained 68.55% of the LED packaging market share in 2025, led by China’s vertically integrated clusters in Guangdong and Jiangsu, which collocate epitaxy with final module assembly. Investments topping RMB 2 billion (USD 280 million) at BOE Huacan and RMB 215.57 million (USD 30 million) at Qianzhao Optoelectronics illustrate scale economies that lower per-die costs while intensifying regional price competition. Japan focuses on high-efficiency UV and automotive packages, leveraging Nichia’s 280 nm line and its alliance with European OEMs through the Aachen Automotive Innovation Center. South Korea’s Samsung Electronics and LG Innotek channel 600 billion won (USD 450 million) into flip-chip ball-grid-array lines that target premium displays and vehicle modules. Southeast Asia welcomes Malaysia’s USD 83.88 million Aoyang Shunchang plant as firms diversify geographic risk.

North America emphasizes regulatory-driven retrofits and specialty applications. The January 2026 Canadian mercury lamp ban compels rapid LED conversions countrywide, while the United States finalizes adaptive driving beam regulations. Domestic packaging houses focus on automotive, UV-C sterilization, and industrial reliability niches. Europe’s stringent Ecodesign rules and early adaptive headlamp approvals are driving steady demand for high-power, automotive-qualified packages. Germany anchors automotive sourcing, with local Tier-1 lighting firms co-developing modules with Japanese and Korean die suppliers.

South America, the Middle East, and Africa collectively represent modest shares but deliver situational spikes. Brazil’s construction rebound lifts general lighting unit sales, while oil-rich Gulf states deploy high-lumen packages in mega-projects. South Africa mandates ruggedized IP65 modules for mining and industrial zones, while Egypt prefers low-power solar streetlights for grid-constrained rural districts.

Competitive Landscape

The LED packaging arena shows moderate concentration, with the ten largest suppliers accounting for roughly 55%-60% of global revenue, while no single company exceeds a 15% share of sales. Japan’s Nichia, Germany’s Osram, and South Korea’s Samsung Electronics keep epitaxy and chip fabrication in-house, which secures critical intellectual property and material quality. Pure-play packagers such as Everlight, Dominant Opto Technologies, and Refond compete on agile engineering and responsive customer service, sourcing most of their die from merchant foundries. Chinese leaders San’an Optoelectronics, NationStar, and Hongli Zhihui leverage large-scale domestic fabs to drive cost efficiency that smaller rivals struggle to match. Despite cost pressure, niche specialists maintain pricing power by targeting automotive, ultraviolet, and horticulture segments where qualification barriers are high.

Strategic moves in 2025-2026 signal both cooperation and confrontation. San’an Optoelectronics announced a USD 239 million deal to acquire Lumileds in August 2025, a transaction slated to close in the first quarter of 2026 that will merge Chinese scale with strong automotive customer access. Nichia and Osram executed a comprehensive cross-license in October 2025 covering white and colored LEDs, ending several long-running infringement disputes and freeing capital for joint innovation. In contrast, Everlight filed patent suits against Lumileds and Seoul Semiconductor in February 2026, alleging unauthorized use of flip-chip packaging designs and underscoring that litigation remains a cost of doing business in this field. These legal and corporate maneuvers shape access to high-growth niches, influence royalty structures, and determine the pace of new product launches.

Technology differentiation is shifting value toward packages that solve thermal bottlenecks, integrate intelligence, or deliver specialty spectra. Cree LED’s OptiLamp platform, launched in February 2026, embeds temperature sensors and control logic inside the package, enabling predictive maintenance and reducing unplanned downtime for industrial users. LG Innotek is investing 600 billion won (USD 450 million) to boost flip-chip ball-grid-array capacity that targets vehicle headlamps and harsh-environment applications. Meanwhile, Chinese newcomers are flooding low-power SMD categories, pushing established brands to focus on automotive-qualified CSPs, deep-UV emitters, and ultra-high-power stadium lights, where patents and reliability requirements create protective moats. The competitive field, therefore, rewards suppliers that balance cost leadership with specialized performance and that lock in freedom to operate through proactive licensing or vertical integration.

LED Packaging Industry Leaders

Nichia Corporation

Samsung Electronics Co. Ltd.

Seoul Semiconductor Co. Ltd.

Ams-Osram AG

LG Innotek Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight sued Lumileds (Feb 2) and Seoul Semiconductor (Feb 13) in United States courts over flip-chip patent claims.

- February 2026: Cree LED launched OptiLamp LEDs with on-package sensors enabling predictive maintenance and remote diagnostics.

- January 2026: Canada’s federal mercury lamp ban took effect, eliminating sales of fluorescent and high-intensity discharge lamps.

- October 2025: Nichia and Osram executed a comprehensive cross-license covering white and colored LEDs.

Global LED Packaging Market Report Scope

The LED Packaging Market Report is Segmented by Packaging Architecture (Surface Mount Device (SMD), Chip-on-Board (COB), Chip Scale Package (CSP), Flip-Chip LED Packages, Dual In-Line Package (DIP / Through-Hole), Integrated Module Device (IMD), Glass-on-Board (GOB), Mini-LED Display Packaging), Power Class (Low Power (Below 0.5 W), Mid Power (0.5–1 W), High Power (1–3 W), Ultra-High Power (Above 3 W)), Emission Type (Visible LED Packages, Infrared LED Packages, Ultraviolet LED Packages), Material Chemistry (Substrates, Encapsulation, Bonding / Die-Attach, Phosphors / Coatings), Application (General Lighting, Automotive Lighting, Display and Backlighting, Consumer Electronics, Industrial and Specialty), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Packaging Architecture

| Surface Mount Device (SMD) |

| Chip-on-Board (COB) |

| Chip Scale Package (CSP) |

| Flip-Chip LED Packages |

| Dual In-Line Package (DIP / Through-Hole) |

| Integrated Module Device (IMD) |

| Glass-on-Board (GOB) |

| Mini-LED Display Packaging |

By Power Class

| Low Power (Below 0.5 W) |

| Mid Power (0.5–1 W) |

| High Power (1–3 W) |

| Ultra-High Power (Above 3 W) |

By Emission Type

| Visible LED Packages |

| Infrared LED Packages |

| Ultraviolet LED Packages |

By Material Chemistry

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

By Application

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Consumer Electronics |

| Industrial and Specialty |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Packaging Architecture | Surface Mount Device (SMD) | |

| Chip-on-Board (COB) | ||

| Chip Scale Package (CSP) | ||

| Flip-Chip LED Packages | ||

| Dual In-Line Package (DIP / Through-Hole) | ||

| Integrated Module Device (IMD) | ||

| Glass-on-Board (GOB) | ||

| Mini-LED Display Packaging | ||

| By Power Class | Low Power (Below 0.5 W) | |

| Mid Power (0.5–1 W) | ||

| High Power (1–3 W) | ||

| Ultra-High Power (Above 3 W) | ||

| By Emission Type | Visible LED Packages | |

| Infrared LED Packages | ||

| Ultraviolet LED Packages | ||

| By Material Chemistry | Substrates | |

| Encapsulation | ||

| Bonding / Die-Attach | ||

| Phosphors / Coatings | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Consumer Electronics | ||

| Industrial and Specialty | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What compound annual growth rate is projected for global LED packaging from 2026 to 2031?

A 4.60% CAGR is expected for the period.

Which package architecture shows the fastest expansion through 2031?

Chip-scale packages are projected to record the highest 5.11% CAGR.

What key factor is boosting demand for 1-3 W high-power LED packages?

Adaptive matrix headlamps and factory machine-vision systems require emitters delivering >100 lumens with automotive-grade reliability, driving uptake of this power class.

How will bans on mercury lamps affect North American LED package volumes?

Canada’s 2026 prohibition and parallel U.S. phase-outs compel fluorescent retrofits, sharply increasing shipments of mid- and high-power LED packages for linear and high-bay fixtures.

Which region currently dominates LED packaging revenue and capacity?

Asia-Pacific holds 68.55% of 2025 revenue and is forecast to grow at a 5.06% CAGR to 2031, underpinned by extensive Chinese manufacturing hubs.

What strategic moves are reshaping competition among leading suppliers?

Cross-licensing agreements, such as Nichia-Osram’s 2025 deal, and vertical integration efforts like San’an’s planned Lumileds acquisition are redefining intellectual-property access and scale advantages.

Page last updated on: