China Mid-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

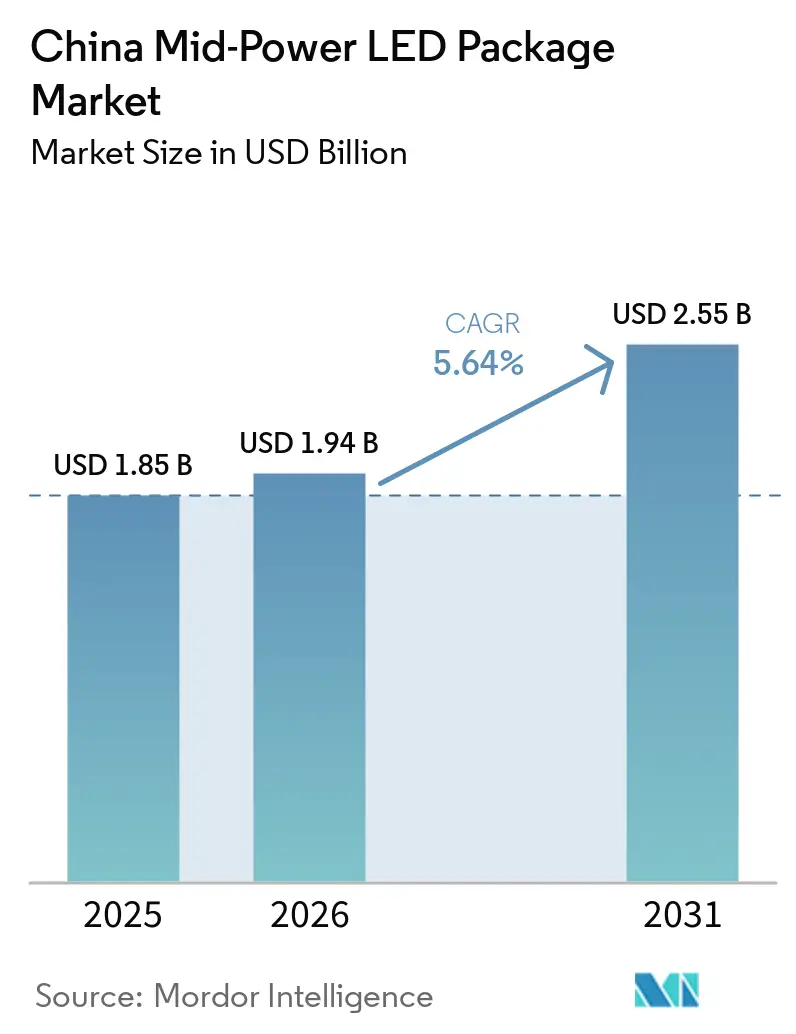

| Base Year Market Size (2025) | USD 1.85 Billion |

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.55 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mid-Power LED Package Market Analysis by Mordor Intelligence

The China mid-power LED package market size is projected to be USD 1.85 billion in 2025, USD 1.94 billion in 2026, and reach USD 2.55 billion by 2031, growing at a CAGR of 5.64% from 2026 to 2031. The structural pricing reset that began in early 2026, after four years of steep price erosion, is restoring margin discipline, while rising raw-material costs have prompted packagers to rebalance contract terms with downstream OEMs. Policy drivers from ultra-long special government bonds for carbon-reduction projects to the forthcoming GB 30255-2026 energy-efficiency mandate are expanding demand for high-efficacy, smart-ready luminaires. Vertical integration by panel makers and large LED manufacturers is concentrating technology and capacity in fewer hands, yet more than 20 domestic suppliers still vie for share, keeping competitive pressure elevated. Automotive-grade, Mini/Micro LED, and horticultural segments now anchor most new capacity plans, signaling a decisive pivot away from commoditized general lighting.

Key Report Takeaways

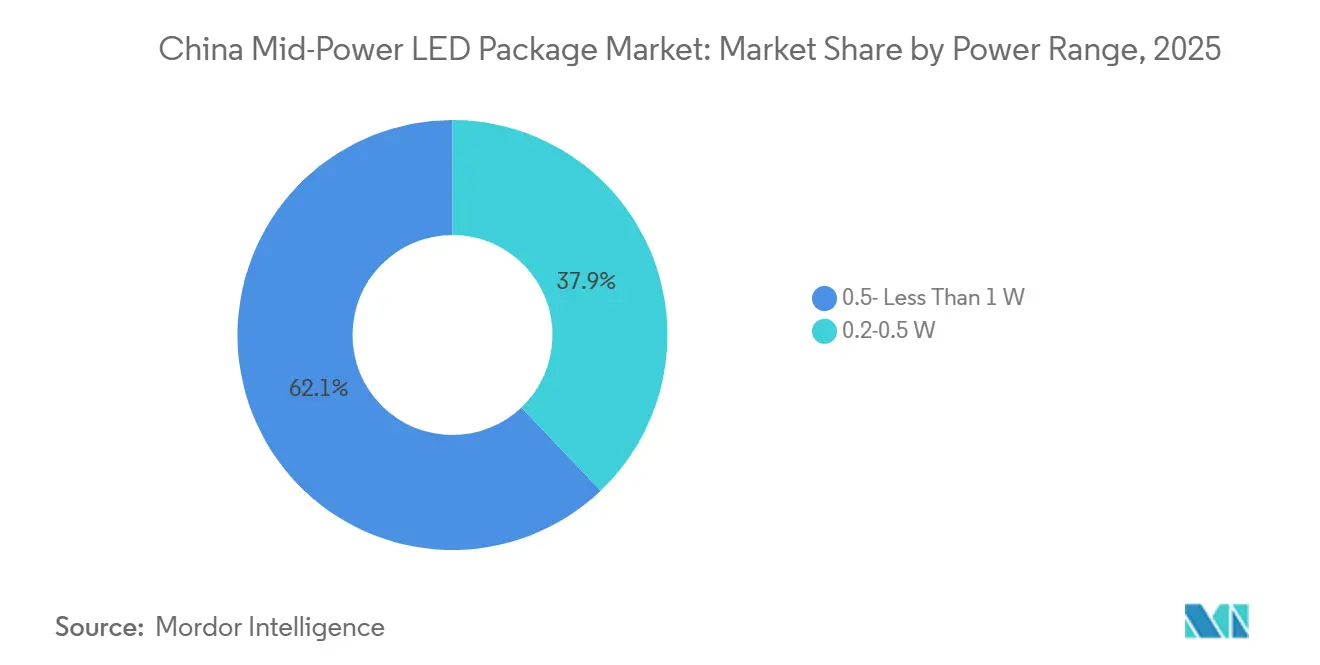

- By power range, the 0.5 W- Less Than 1 W segment captured 62.1% of the China mid-power LED package market share in 2025 and is set to advance at a 5.99% CAGR through 2031.

- By package architecture, surface-mount devices (SMD) held 72.2% of the revenue share in 2025, while chip-scale packages (CSP) are forecast to record the fastest 6.05% CAGR through 2031.

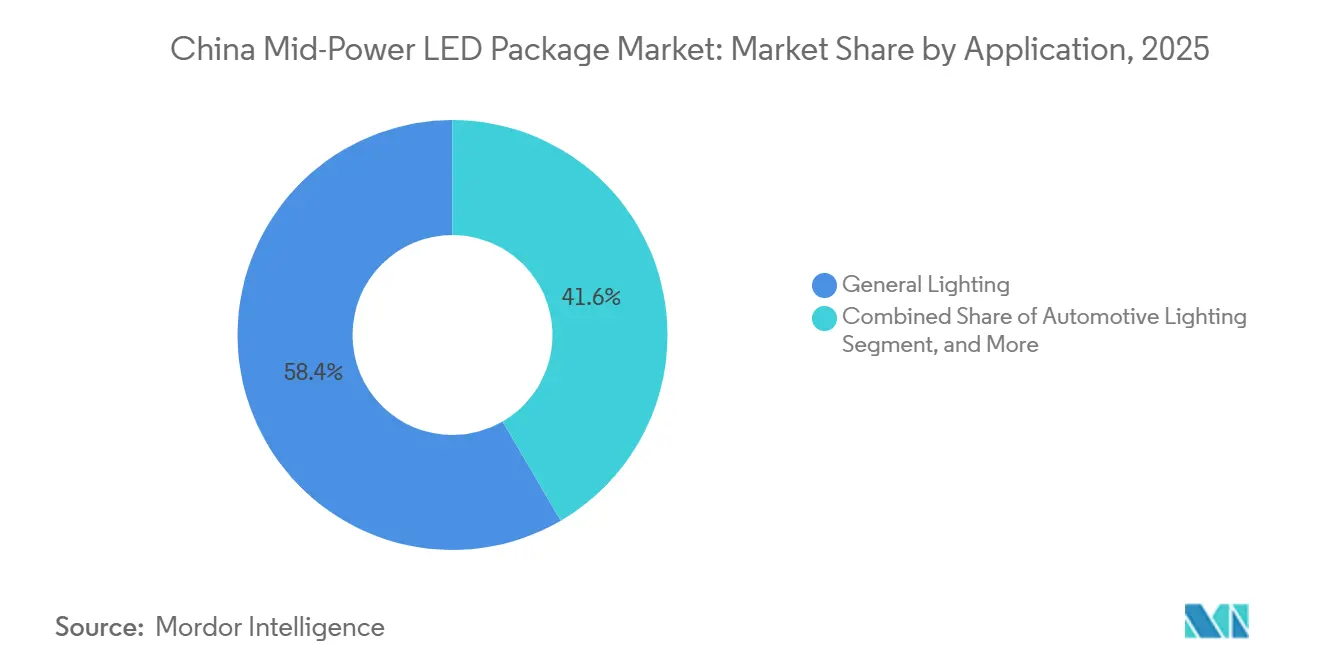

- By application, general lighting accounted for 58.4% of the China mid-power LED package market size in 2025, whereas automotive lighting is projected to rise at a 6.11% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Mid-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing Demand for Energy-Efficient Lighting in China's Tier-2 Cities | +1.2% | National, concentrated in Tier-2 and Tier-3 municipalities | Medium term (2-4 years) |

| Government Subsidy Programs for Industrial Upgrades in LED Manufacturing | +0.9% | National, with emphasis on provincial-level capacity upgrades | Short term (≤ 2 years) |

| Rapid Expansion of Automotive LED Headlamp Adoption | +1.4% | National, driven by NEV production hubs | Medium term (2-4 years) |

| Surge in Mini-LED Backlight Adoption in TVs and Monitors | +1.1% | National and export-oriented panel clusters | Medium term (2-4 years) |

| Rising Investments in Smart City Infrastructure Lighting | +0.6% | Provincial capitals and economically developed municipalities | Long term (≥ 4 years) |

| Localization of LED Supply Chain Due to Geopolitical Tech Self-Reliance | +0.4% | National, upstream epitaxy, and chip sourcing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Energy-Efficient Lighting in China's Tier-2 Cities

Municipal retrofits financed through energy-performance contracts are scaling across Hefei, Qianjiang, Tongling, and Zengcheng, where single-lamp IoT controls cut maintenance response times by as much as 80%.[1]China Daily Staff, “Hefei Accelerates Smart Streetlight Retrofit,” chinadaily.com.cn Verified energy-savings guarantees allow private investors to recover project costs over 9- to 10-year terms, creating a predictable mid-power LED package pull-through. The GB 30255-2026 standard boosts minimum efficacy to 105 lm/W and caps standby power at 0.5 W, thereby favoring high-efficacy 0.5 W- less than 1 W packages for streetlighting retrofits. As more Tier-2 cities commit to carbon-peaking goals before 2030, retrofit pipelines are lengthening, underpinning multi-year demand visibility. The dynamic is reinforcing supplier interest in long-lifetime ceramic and flip-chip SMD formats that meet the new optical and flicker limits.

Government Subsidy Programs for Industrial Upgrades in LED Manufacturing

The Ministry of Finance earmarked RMB 93.6 billion (USD 13 billion) for carbon-reduction projects, while the People’s Bank of China opened RMB 800 billion (USD 111 billion) in low-cost refinancing to accelerate factory upgrades.[2]Ministry of Finance, “Notice on Issuing Ultra-Long Special Government Bonds for Carbon Reduction,” mof.gov.cn These funds are underwriting vertical-integration deals such as TCL CSOT’s purchase of Fuzhou Huazhao Optoelectronics and capacity expansions at NationStar and Leyard. Subsidy criteria favor lines producing Mini/Micro LED, automotive, and horticultural packages that exceed Level 1 China Energy Label thresholds, further tilting market share toward integrated players. Provincial governments add matching grants that offset up to 20% of new equipment costs, hastening adoption of high-speed flip-chip bonders and automated phosphor-spray lines. Smaller packagers lacking capital or automotive-grade qualifications are consequently losing bids for subsidy-linked orders.

Rapid Expansion of Automotive LED Headlamp Adoption

NEV production rose 39.2% year-on-year to 8.23 million units during January-July 2025, pushing LED headlamp fitment above 90% for electric cars.[3]Ministry of Industry and Information Technology, “NEV Production and Sales Monthly Report,” miit.gov.cnAdaptive driving beam and through-type taillight penetration is forecast to increase in 2026, lifting per-vehicle lighting value. GB 4599-2024 introduces stricter UV-emission and photometric-stability tests, making AEC-Q102-qualified 0.5 W- less than 1 W LEDs the default for matrix modules. Domestic packagers such as Jingke, Refond, and Hongli have doubled automotive revenue by tailoring CSP and ceramic packages to 125 °C junction temperatures and zero-defect PPAP requirements. As NEV subsidies taper, lighting differentiation remains a key brand lever, sustaining robust demand for mid-power packages.

Surge In Mini-LED Backlight Adoption in TVs And Monitors

Chinese shipments of Mini LED backlight televisions surpassed 8 million units in 2025 and are on course to exceed 10 million in 2026.[4]MIIT Panel Division, “Mini LED Backlight TV Shipments 2025,” miit.gov.cn Panel makers BOE, TCL, CSOT, and HKC now co-locate COB backlight module lines with captive LED chip capacity, compressing cycle times and lowering cost per zone. RGB-plus-cyan backlights showcased at CES 2026 require narrow-band, high-flux CSP emitters, creating new design wins for suppliers that can meet ±1 nm wavelength tolerances. The government’s appliance trade-in program mandates Level 1 energy labels, further advantaging Mini-LED LCD sets over OLED equivalents on power metrics. Tight binning, phosphor stability, and high reliability at 4,000-6,000 nits drive new specification layers that only a subset of packagers can satisfy, cementing premium pricing despite broader market commoditization.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price Erosion Due to Overcapacity in Chinese LED Packaging Lines | -1.8% | National, commodity general lighting and low-end displays | Short term (≤ 2 years) |

| Supply Chain Disruptions for High-Purity Phosphors | -0.7% | Global, acute for China-based phosphor users | Medium term (2-4 years) |

| Stringent Blue-Light Hazard Regulations Limiting Drive Current | -0.4% | National and key export markets | Long term (≥ 4 years) |

| Competition from Integrated COB and High-Power Packages | -0.5% | National and global specialty segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Erosion Due To Overcapacity in Chinese LED Packaging Lines

Between 2022 and 2025, new entrants ramped up capacity faster than demand, leading to a drop in average selling prices for mid-power packages. While a concerted effort in early 2026 led to a price rebound, the market still grapples with an oversupply of commodity lighting. Retailers tread carefully, hesitant to transfer rising costs to consumers, which in turn elongates working-capital cycles for packagers. In 2025, fluctuations in raw-material prices led to surges in gold, silver, and copper prices, exerting pressure on gross margins. By Q3 2025, this was evident as San’an Optoelectronics, a key market player, reported a dip in its margins. While consolidation in the market promises to bolster pricing power, smaller vendors lacking unique technology face the looming threat of being edged out before market equilibrium is achieved.

Supply Chain Disruptions for High-Purity Phosphors

China widened export controls on 12 rare-earth elements in October 2025, imposing 45-day license requirements on shipments containing more than 0.1% of Chinese-origin processing. The country refines a significant share of global rare-earth production, so packagers reliant on europium- and yttrium-based phosphors face longer lead times and higher inventory costs. LED makers supplying healthcare, broadcast, and premium backlights now scramble to certify alternate sources in Australia or the United States, yet new refining capacity remains two-to-three years away. Temporary work-arounds, including phosphor recycling and synthetic substitutes, lift unit costs and lengthen qualification schedules, weighing on shipment volumes through at least 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: 0.5 W- Less Than 1 W Anchors Multi-Market Demand

The 0.5 W- Less Than 1 W class accounted for 62.1% of the China mid-power LED package market share in 2025, with its market size forecast to expand at a 5.99% CAGR to 2031. This range balances luminous flux, heat dissipation, and cost, making it the workhorse for indoor lamps, streetlights, and Mini LED local-dimming zones. Ceramic and flip-chip 3030 formats rated to 125 °C junction temperature are increasingly displacing plastic packages in automotive side markers and daytime running lamps.

Material advances, such as deep-red 3535 horticultural LEDs with an efficiency of 5.05 µmol J⁻¹, extend the segment into controlled-environment agriculture. Tightening efficacy targets under GB 31831-2025, plus stricter flicker metrics, further entrench the adoption of mid-current 0.5 W emitters. Lower-power 0.2-0.5 W devices keep a niche in decorative strips and portable gadgets, while less than or equal to 1 W packages migrate toward high-bay and UV markets.

By Package Architecture: SMD Dominance Meets CSP Momentum

SMD devices accounted for 72.2% of revenue in 2025, supported by mature 2835 and 3030 supply chains and low cost-per-lumen. CSP, however, is growing fastest at a 6.05% CAGR, enabled by flip-chip die attach, which removes bond wires and plastic frames. Bridgelux’s CSP2727 hits 209 lm W⁻¹ at 350 mA, matching top SMD efficacy while shrinking footprint to 2.7 mm².[5]Bridgelux Engineering, “CSP2727 Performance Data Sheet,” bridgelux.com

Panel makers now specify CSP arrays for 65-inch-plus Mini LED backlights requiring 5,000-zone dimming, and automotive OEMs value the format’s robustness under vibration. Still, conventional SMD keeps control of price-sensitive bulbs and tubes, where existing pick-and-place lines and photometric testers yield scale economies that CSP has yet to match.

By Application: Automotive Lighting Takes Growth Lead

General lighting retained 58.4% of revenue in 2025, yet its volume growth has plateaued as retrofit demand slows and imports of alternative light sources rise. Automotive lighting, in contrast, is on track for a 6.11% CAGR, lifting its China mid-power LED package market size materially by 2031. NEV models adopt matrix headlamps, dynamic taillights, and interactive interior strips that rely heavily on mid-power packages.

Mini LED backlight shipments exceeding 8 million TVs in 2025 fuel a parallel surge in display demand. RGB-plus-cyan backlights quadruple the LED count per set compared to conventional full-array backlights, while maintaining sub-10 mm module thickness. Specialty niches UV disinfection, horticulture, and smart wellness luminaires add incremental pull for spectrum-tuned mid-power LEDs but remain modest in absolute revenue terms.

Geography Analysis

Clustered industrial bases shape regional opportunity within the China mid-power LED package market. Guangdong leads Mini LED adoption because BOE and TCL CSOT co-locate panel fabs and backlight modules, ensuring high local pull for SMD and CSP chips. The province also incubates Refond, NationStar, and Hongli, giving buyers proximity to certified automotive and horticultural lines. Zhejiang and Jiangsu host major NEV assembly plants in Shanghai’s orbit, so ADB-grade package demand concentrates there, with suppliers aligning processes to GB 4599-2024 photometric updates.

Fujian, newly home to TCL-backed Fuzhou Huazhao Optoelectronics, is pivoting from low-margin lighting chips to display backlight nodes, adding diversity to regional supply. Inland Tier-2 cities fund large-scale streetlight retrofits via energy-service contracts, translating policy finance into steady 0.5 W shipment lanes. Hefei’s 27,000-lamp project and Qianjiang’s 6,473-lamp upgrade alone drive annualized demand exceeding 10 million mid-power emitters.

Shenzhen-based video wall manufacturers are now exporting their output to Southeast Asia and the Middle East, helping cushion against domestic oversupply. By adhering to dual certifications, CCC for the domestic market and CE, UKCA, or NHTSA for international markets, manufacturers are distributing qualification tasks across both coastal and inland testing labs. This approach extends the revenue timeline for package suppliers and diversifies their income sources.

Competitive Landscape

Over 15 participants jostle for position in the Chinese mid-power LED package market, yet ownership shifts show rapid consolidation. San’an Optoelectronics expects to fold Lumileds into its books by Q1 2026, vaulting it into the global automotive top three and adding cross-licensing protection for critical phosphor and flip-chip processes. TCL CSOT, meanwhile, secured upstream LED chips through its USD 68 million buyout of Fuzhou Huazhao, mirroring panel peers BOE and HKC, which favor captive supply chains. MLS and LEDVANCE jointly increased their stake in Purui Optoelectronics to 68%, aiming to secure Mini LED backlight capacity for international lamp brands.

Domestic specialists pivot toward higher-margin niches. Refond renews KSF phosphor licenses to target wide-gamut backlights, while Hongli’s agreement with Current opens automotive display channels. Everlight’s patent suit against Seoul Semiconductor underscores lingering IP friction, especially around flip-chip CSP. Verticalized panel makers threaten merchant packagers by in-house sourcing, yet also spin off surplus chips to allied brands, preserving some external demand.

Competition now rests on process capability COB, ultra-thin 0-OD, and automated binning, as well as on access to rare-earth phosphors under new export controls. Players unable to fund automotive-grade reliability labs or maintain 45-day phosphor inventories risk relegation to commodity lamps, where margin recovery remains elusive.

China Mid-Power LED Package Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

Lumileds Holding B.V.

Seoul Semiconductor Co., Ltd.

San'an Optoelectronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: TCL CSOT completed its 80% acquisition of Fuzhou Huazhao Optoelectronics for RMB 490 million (USD 68 million), integrating LED chip supply for its Suzhou Mini LED video wall line.

- February 2026: Everlight Electronics filed a U.S. patent-infringement lawsuit against Seoul Semiconductor covering flip-chip LED packaging processes.

- January 2026: LEDVANCE and MLS agreed to acquire a 34.78% stake in Purui Optoelectronics for RMB 900 million (USD 125 million), boosting their joint ownership to 68%.

- August 2025: San’an Optoelectronics announced plans to take 74.5% control of Lumileds Holding B.V. for USD 239 million, targeting completion by Q1 2026.

China Mid-Power LED Package Market Report Scope

The China Mid-Power LED Package Market Report is Segmented by Power Range (0.2-0.5 W and 0.5- Less Than 1 W), Package Architecture (SMD including 2835, 3014, 3030, Others and CSP), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

| 0.2-0.5 W |

| 0.5- Less Than 1 W |

| SMD (Surface Mount Device) | 2835 |

| 3014 | |

| 3030 | |

| Others (3528, 3020, 5050, etc.) | |

| CSP (Chip Scale Package) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| By Power Range | 0.2-0.5 W | |

| 0.5- Less Than 1 W | ||

| By Package Architecture | SMD (Surface Mount Device) | 2835 |

| 3014 | ||

| 3030 | ||

| Others (3528, 3020, 5050, etc.) | ||

| CSP (Chip Scale Package) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

Key Questions Answered in the Report

What is the current value of the China mid-power LED package market?

The market stands at USD 1.94 billion in 2026 and is on track to reach USD 2.55 billion by 2031.

Which power class leads demand for China’s mid-power LED packages?

Devices rated 0.5 W- Less Than 1 W commanded 62.1% share in 2025 and are forecast to keep the largest slice through 2031.

Why are CSP packages gaining momentum in China?

Chip-scale packages offer smaller footprints, better thermal paths, and high zone densities needed for Mini-LED TV backlights and advanced automotive lighting.

How fast is automotive lighting growing in China?

Automotive lighting LED revenue is projected to rise at a 6.11% CAGR from 2026-2031, the highest among major application segments.

What policies are shaping China’s LED demand outlook?

GB 30255-2026 raises indoor-lighting efficiency thresholds, while ultra-long special government bonds fund municipal retrofits and factory decarbonization, both of which accelerate the uptake of high-efficacy packages.

How are rare-earth export controls affecting LED suppliers?

New 45-day export license rules for lanthanum, europium, and other phosphor elements lengthen lead times and raise costs, prompting suppliers to source alternative materials or expand inventories.

Page last updated on: