India High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

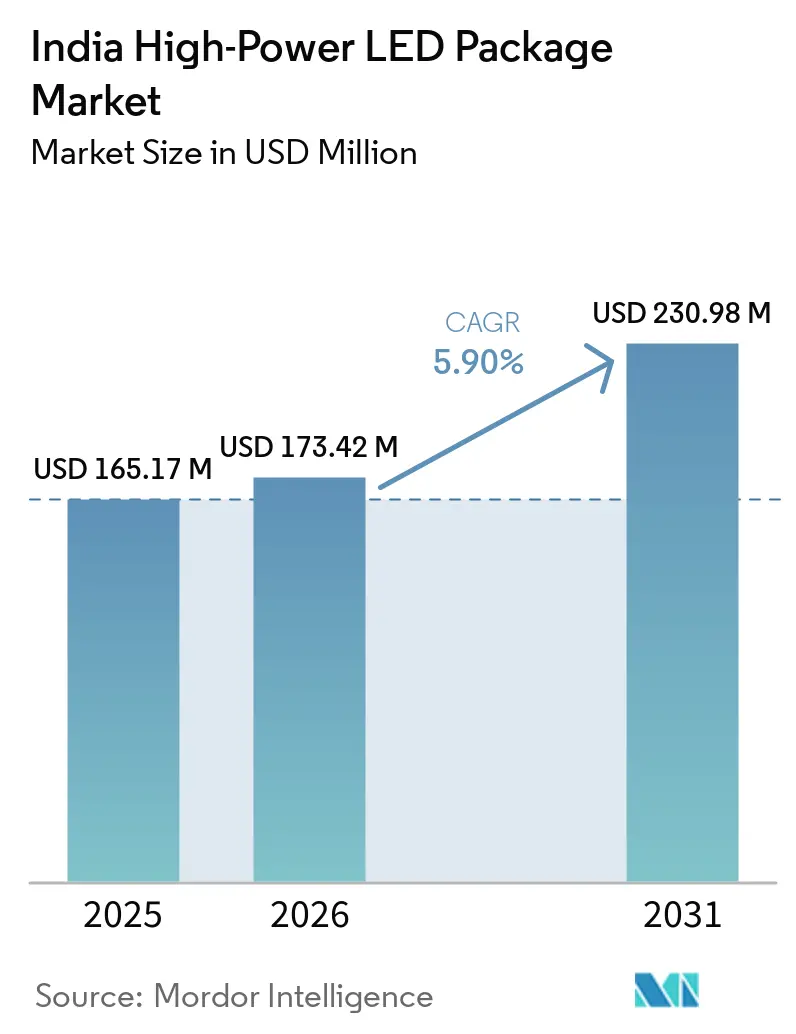

| Base Year Market Size (2025) | USD 165.17 Million |

| Market Size (2026) | USD 173.42 Million |

| Market Size (2031) | USD 230.98 Million |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

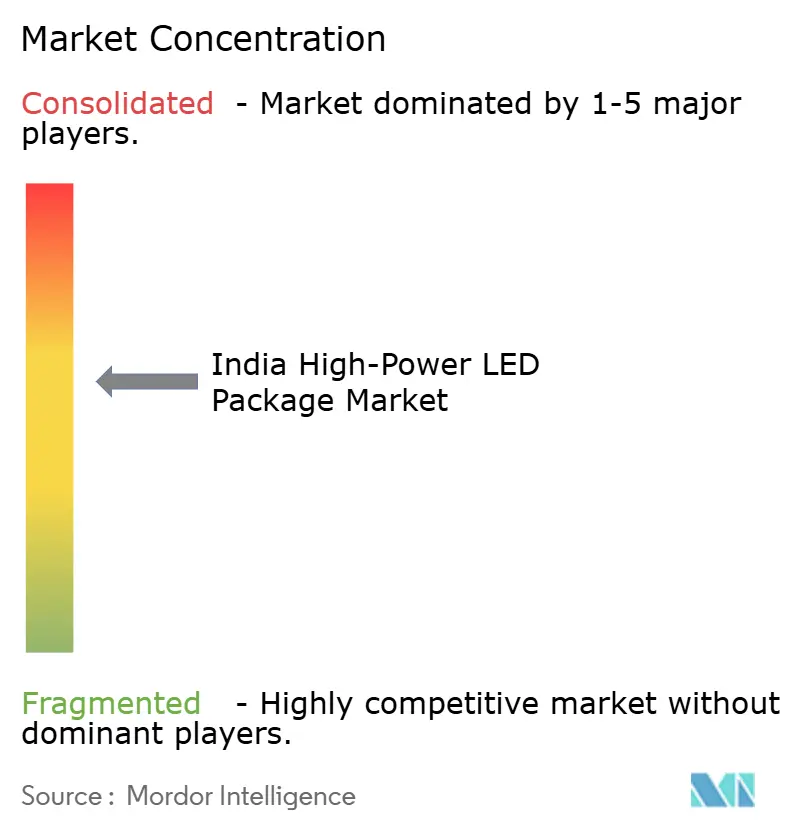

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India High-Power LED Package Market Analysis by Mordor Intelligence

The India High-Power LED package market size is expected to increase from USD 165.17 million in 2025 to USD 173.42 million in 2026 and reach USD 230.98 million by 2031, growing at a CAGR of 5.9% over 2026-2031. Supported by government bulk-procurement programs, falling cost-per-lumen economics, and regulatory mandates in the automotive sector, the market continues to add new demand pockets in municipal infrastructure, industrial lighting, and controlled-environment agriculture. Price erosion in mainstream 1 W-3 W packages is being offset by volume gains and the migration of professional users toward higher-wattage architectures that deliver superior thermal performance. Meanwhile, the Production-Linked Incentive scheme is steering investment toward backward-integrated chip packaging lines, edging the supply base away from assembly-only operations. Intensifying competition around optical tuning, reliability testing, and system-level integration is redefining how suppliers differentiate beyond simple efficacy gains.

Key Report Takeaways

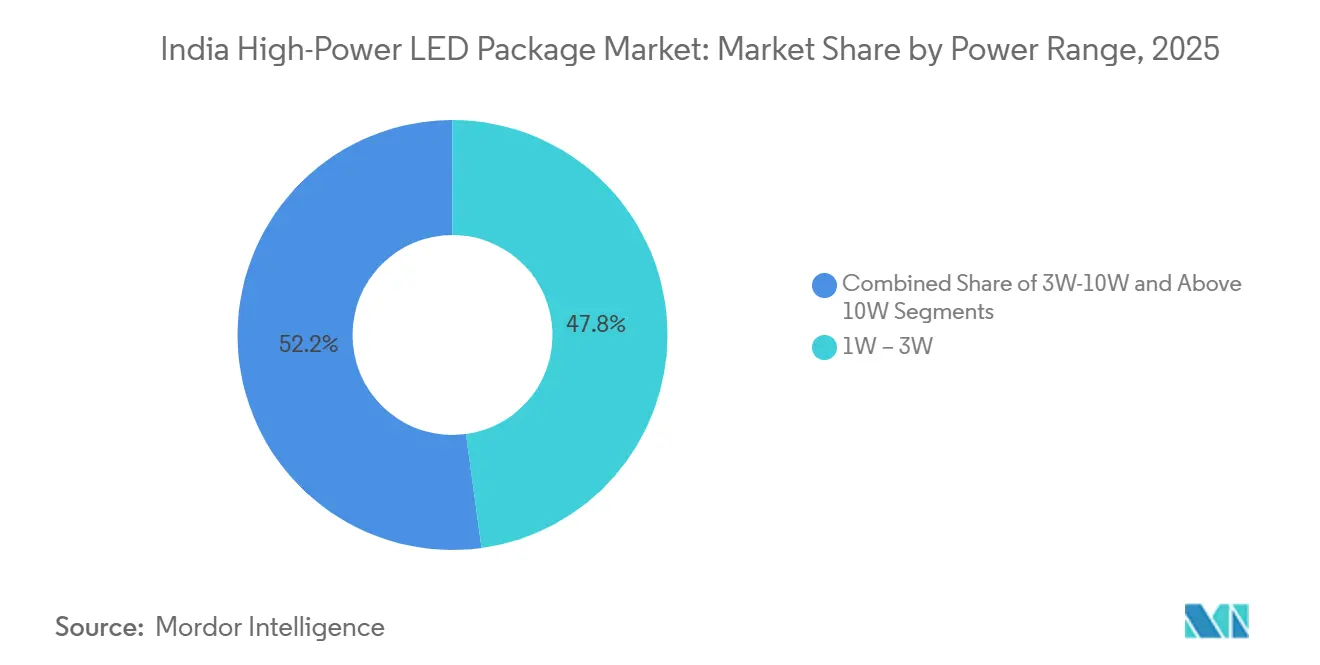

- By power range, the 1 W-3 W class led with 47.84% of the India High-Power LED package market share in 2025, while the Above 10 W segment is projected to expand at a 6.47% CAGR through 2031.

- By architecture, single-die packages accounted for 35.88% of the India High-Power LED package market size in 2025, and chip-on-board packages record the highest forecast CAGR at 6.55% over 2026-2031.

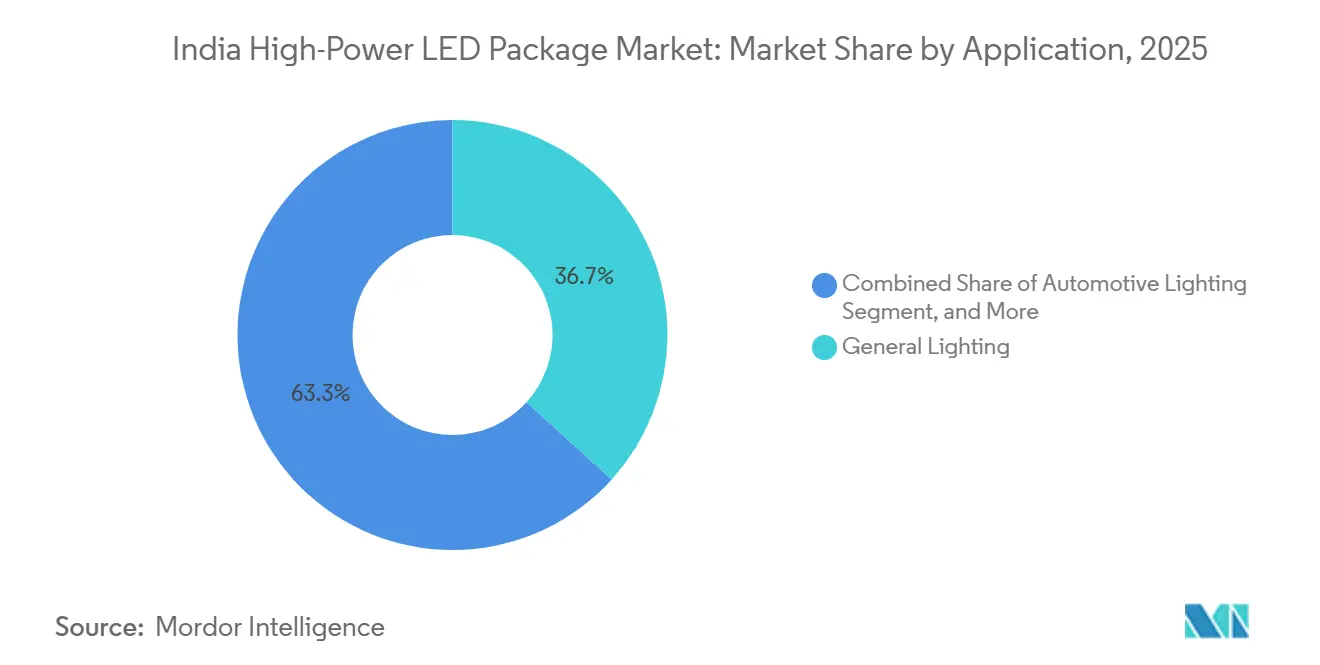

- By application, general lighting accounted for 36.73% of revenue in 2025, whereas automotive lighting is anticipated to grow at a 6.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India High-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Push Through UJALA and SLNP Programs | +1.2% | National, with concentrated deployment in Tier-1 and Tier-2 urban centers | Medium term (2-4 years) |

| Rapid Urban Infrastructure Expansion and Smart City Projects | +1.0% | National, early gains in Delhi, Ahmedabad, Kochi, Guwahati | Medium term (2-4 years) |

| Declining Cost-per-Lumen of High-Power LED Packages | +0.9% | National | Long term (≥ 4 years) |

| Automotive Industry Shift to LED Headlamps | +0.8% | National, concentrated in automotive hubs (Gujarat, Tamil Nadu, Maharashtra) | Medium term (2-4 years) |

| Rise of Horticulture LED Farms in Controlled-Environment Agriculture | +0.5% | National, with early adoption in Maharashtra, Karnataka, Tamil Nadu | Long term (≥ 4 years) |

| Surge in High-Mast Sports Lighting Upgrades for Upcoming Events | +0.4% | National, focused on cricket stadiums in Mumbai, Pune, Rajkot, and metro cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Push Through UJALA and SLNP Programs

Bulk procurement under the Unnat Jyoti by Affordable LEDs for All and Street Lighting National Program has seeded a nationwide installed base of 36.87 crore LED bulbs and 1.34 crore streetlights, creating a predictable aftermarket for high-power replacements.[1]Press Information Bureau, “Distribution of LED Bulbs and Streetlights under UJALA and SLNP,” pib.gov.in Unit prices fell by 75% within the first 16 months of UJALA, normalizing LEDs as the default light source and widening the addressable base for domestic assemblers. As EESL pivots new tenders toward smart, dimmable luminaires, package suppliers must now integrate drivers and IoT controls to stay qualified. Municipalities that adopted SLNP fixtures face seven-to-ten-year replacement cycles, ensuring steady demand for 15 W-50 W packages with higher lumen maintenance. This dynamic favors vertically integrated firms that can meet Bureau of Indian Standards photometric and safety tests while keeping costs aligned with government price ceilings.

Rapid Urban Infrastructure Expansion and Smart City Projects

Smart Cities Mission allocations have financed LED retrofits across 100 cities, with Ahmedabad investing INR 5 billion (USD 56.7 million) to upgrade 210 000 poles and Kochi spending INR 300 million (USD 3.4 million) on 40 000 networked luminaires.[2]Smart Cities Mission, “Guwahati Smart LED Streetlight Project Completion Report,” smartcities.gov.in These large contracts specify lumen maintenance above 50 000 hours and a color rendering index above 80, raising entry barriers for low-cost imports. Guwahati’s 2025 project cut energy use by 60% while stretching maintenance intervals to 50 000 hours, validating the total-cost-of-ownership case for premium packages. Decentralized tendering across states rewards regional distributors that can customize thermal designs for local climate zones. As city contracts increasingly require integrated sensors, suppliers with in-house driver and RF capabilities gain a competitive edge.

Declining Cost-Per-Lumen of High-Power LED Packages

Mainstream packages now deliver more than 100 lm/W, while premium devices exceed 200 lm/W and top laboratory versions approach 230 lm/W, narrowing the economic gap with legacy HID solutions.[3]International Energy Agency, “Solid-State Lighting Annex 2025 Update,” iea.org Flip-chip and chip-scale architectures lower thermal resistance and improve light extraction, allowing a 40 W floodlight in 2026 to match the output of a 50 W unit sold two years earlier. Domestic brands such as Crompton have launched 350 W-400 W fixtures reaching 120 lm/W by leveraging automated COB assembly lines supported by PLI incentives. As efficacy gains plateau near theoretical limits, differentiation is shifting to spectral tuning, dimming linearity, and long-term reliability, attributes that smaller assemblers struggle to fund. Suppliers investing in LM-80 and TM-21 labs are therefore positioned to command margins even when headline efficacy becomes commoditized.

Automotive Industry Shift to LED Headlamps

AIS-034 and AIS-199 standards now mandate LED photometric performance and electromagnetic compatibility on new vehicle platforms launched after 2024. Marelli-Motherson’s 2026 Sanand plant, India’s first single-piece lamp facility, produces 17 mm slim headlamps that integrate 20-40 addressable dies, demonstrating domestic capability for matrix systems. Automotive-grade packages command 30-50% price premiums but also require AEC-Q101 qualification and IATF 16949 processes, which only a handful of Indian suppliers possess. With India’s electric-vehicle sales crossing 1.5 million units in 2025, demand for adaptive lighting and instrument-cluster backlights is set to accelerate. Cross-licensing between Nichia and ams OSRAM underscores the IP complexity in this segment, further raising barriers for late entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Dependence for Epitaxy and Packaging Equipment | -0.7% | National, affecting manufacturers across all regions | Long term (≥ 4 years) |

| Thermal Management Challenges in Tropical Climate | -0.5% | National, acute in coastal and high-humidity regions | Medium term (2-4 years) |

| Fragmented Standards for High-Power LED Reliability Testing | -0.3% | National, impacting export-oriented manufacturers | Medium term (2-4 years) |

| Supply-Chain Volatility for SiC Substrates | -0.4% | National, with global supply-chain dependencies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Import Dependence for Epitaxy and Packaging Equipment

Indian manufacturers still source most MOCVD reactors, lithography lines, and wire-bonders from overseas suppliers such as Aixtron, Veeco, and ASM Pacific, constraining upstream value addition. A single reactor costs USD 3-5 million, while a full fab can exceed USD 100 million, placing such investments beyond the reach of mid-sized lighting firms. Halonix reduced reliance on imports from 60% in FY2021 to 24% in FY2025 by localizing assembly, yet epitaxial wafers and chips still arrive from Taiwan and South Korea. The PLI scheme targets 75-80% domestic value addition by 2029, but achieving this goal will require shared fabrication hubs or joint ventures between equipment vendors. Without such moves, currency volatility and geopolitical risks will continue to pressure margins and supply assurance for high-power packages.

Thermal Management Challenges in Tropical Climate

Ambient temperatures above 40 °C and high coastal humidity accelerate phosphor degradation and solder-joint fatigue in 30 W-100 W outdoor packages. Active cooling can lower junction temperature by 16.667 % and lift lumen output by 5.69 %, yet adds USD 5-10 per luminaire, a premium many municipal buyers resist. Emerging materials, such as graphene-enhanced interfaces and phase-change substrates, improve heat dissipation by up to 30%, but local supply chains for these solutions remain limited. Because Bureau of Indian Standards tests do not mandate elevated-temperature aging representative of tropical conditions, quality gaps persist between certified and real-world performance. Manufacturers pursuing export markets, therefore, run duplicate reliability protocols, stretching product-development cycles and raising total compliance costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Higher-Wattage Packages Anchor New Projects

In 2025, the 1 W-3 W class dominated the India High-Power LED package market, capturing 47.84% share. Meanwhile, the Above 10 W segment is set to grow at a 6.47% CAGR, continuing through 2031. Above 10 W packages now supply high-mast streetlights, industrial bays, and sports venues, where users accept higher purchase costs in exchange for better total cost of ownership. The India High-Power LED package market in this band is benefiting from stadium retrofits that demand 20-30% energy savings and tighter beam angles. Packages exceeding 50 W typically employ ceramic substrates and precision optics, driving collaboration between diode makers and luminaire houses. Installers view longer service intervals as critical because tower-top maintenance remains cost-intensive. Meanwhile, the legacy 1 W-3 W class, once propelled by UJALA bulbs, is entering a slow-replacement phase in urban homes, limiting its growth potential.

Market participants now design modular engines that group six to eight 15 W LED arrays on a single plate, cutting assembly steps for high-mast luminaires. This system-integration trend rewards suppliers that co-design drivers, optics, and thermal paths, not merely diodes. In rural electrification schemes, higher-wattage solar-streetlight kits have begun to specify 20-W to 30-W arrays paired with Li-ion batteries, pushing above 10 W packages further into off-grid applications. Consequently, contract manufacturers expanding PLI-backed capacity are focusing CAPEX on automated assembly lines rated up to 200 W modules.

By Architecture: COB Packages Rise On Performance Advantages

In 2025, single-die packages held a 35.88% share of India's high-power LED package market, while chip-on-board packages are projected to lead with the highest forecast CAGR of 6.55% from 2026 to 2031. Single-die surface-mount devices dominate low-wattage bulbs and tubes, but shifting requirements in automotive and horticulture favor chip-on-board layouts. The India High-Power LED package market share for COBs is rising as headlamp designers seek compact, high-density light sources to streamline optical alignment. Because COBs eliminate bond wires and offer lower thermal resistance, they support 10 W-30 W per square centimeter power densities, ideal for matrix headlamps and spectrum-tuned grow lights. Multi-die SMDs remain relevant in downlights, yet often reach thermal ceilings above 5 W per footprint.

Joint ventures pairing contract assemblers with global patent holders are fast-tracking domestic onboarding of flip-chip and chip-scale packages. Early adopters in plant-factory lighting now demand photon efficacy above 2.5 µmol/J, a level only reachable with high-density COBs. To meet reliability testing requirements, local firms are investing in LM-80 chambers and high-temperature operating-life setups, an expense that smaller assemblers struggle to shoulder. As more tenders specify minimum LM-80 and TM-21 data, market momentum is likely to stay with COB and advanced architectures.

By Application: Automotive Segment Delivers Outsized Growth

In 2025, general lighting made up 36.73% of the revenue, while automotive lighting is projected to expand at a CAGR of 6.93% until 2031. Automotive lighting’s need for photometric precision, ruggedization, and EMC compliance positions it as the fastest-growing segment of the India High-Power LED package market. Passenger-vehicle OEMs are introducing adaptive driving-beam headlamps using 20-40 addressable dies, prompting specialized package designs with AEC-Q101 rating and sulfur-resistant encapsulants. Instrument clusters and interior ambient modules also pivot to energy-efficient LEDs to maximize the range of electric cars.

General lighting remains the revenue leader thanks to retrofit lamps, downlights, and panel fixtures across residential and commercial estates. Yet volume is edging toward price-sensitive replacement cycles, forcing suppliers to add features such as Bluetooth mesh controls to preserve margins. Specialty sectors such as medical phototherapy and UV curing are niche today but offer 2-3× package premiums, encouraging some Chinese-backed entrants to localize micro-UV lines. Together, these shifts underscore that future profitability hinges on capturing automotive and specialty niches rather than defending commoditized bulb insertions.

Geography Analysis

Tier-1 metropolitan clusters account for the largest share of the India High-Power LED package market, driven by dense commercial real estate and aggressive municipal retrofits. Western states such as Maharashtra and Gujarat anchor demand from industrial corridors and automotive hubs, lifting orders for high-wattage streetlights and factory bays. Southern manufacturing zones in Tamil Nadu and Karnataka add mid-power volume for cleanroom, assembly-line, and corporate-campus lighting. Coastal humidity in Chennai and Kochi prompts specifiers to choose ceramic substrates and advanced thermal interface materials to counter high ambient temperatures. North-eastern cities, supported by Smart Cities Mission funds, now pilot connected streetlight networks that integrate 15 W-40 W smart nodes, creating micro-opportunities for package makers that bundle drivers and RF controls.

Volume from Tier-2 and Tier-3 cities is expanding as smart-city corridors move beyond pilot phases and into full rollouts. Municipalities in Uttar Pradesh and Rajasthan are increasingly switching highway poles to solar hybrid kits with 20-W to 30-W arrays, broadening geographic coverage without requiring grid upgrades. Stadium retrofits since 2025 show geographic skew toward western cricket venues, but high-mast sports lighting is beginning to spread to eastern and central arenas ahead of upcoming tournaments. Export-oriented suppliers cluster around special economic zones near Chennai and Pune, enabling quick sea freight of automotive-grade packages to East Asian tier-ones. Localized value-addition targets under the Production-Linked Incentive scheme encourage component sourcing from within each state, fostering small supplier ecosystems around major contract manufacturers.

The northern plains act as a volume buffer during peak summer months when ambient temperatures exceed 40 °C, accelerating replacement of conventional luminaires that cannot withstand thermal stress. In these regions, installers derate lumen output by 10-15% to maintain longevity, which, in turn, boosts shipment counts of higher-wattage packages. Growth pockets are emerging along upcoming freight corridors where new logistics parks require high-bay lighting with integrated motion sensors. Taken together, geographic diversification spreads risk for suppliers and ensures that no single region dominates the India High-Power LED package market share over the forecast window.

Competitive Landscape

The top five global suppliers controlled about 31% of the India High-Power LED package market share in 2025, leaving the remainder to a long tail of domestic brands and contract manufacturers. Nichia, Osram, Samsung, Lumileds, and Cree leverage deep patent portfolios and automotive qualifications, but most still import chips for local module assembly, limiting cost flexibility. Domestic integrators such as Havells, Surya Roshni, Bajaj, and Crompton capitalize on nationwide retail reach and long relationships with municipal utilities to defend their positions in general lighting. Contract manufacturers Calcom Vision and Dixon Technologies ride the Production-Linked Incentive scheme to build automated surface-mount and chip-on-board lines, offering original design manufacturing services to both global and local brands. Cross-licensing agreements among international majors, highlighted by the Nichia-ams Osram deal on matrix headlamps, raise intellectual-property barriers for late entrants.

Competitive tactics now split along end-market lines. Global leaders pursue automotive wins that require AEC-Q101 and IATF 16949 certifications, because those qualifications secure higher gross margins and multi-year platform lifecycles. Domestic brands are doubling down on cost engineering and channel expansion to stay relevant in mid-power retrofit bulbs, which dominate rural sales volumes. Contract manufacturers differentiate by bundling drivers, optics, and heat sinks into single LED engines that shorten luminaire partners' design cycles. Aggressive capital expenditure thresholds in the PLI program compel smaller assemblers to specialize in niche runs, such as UV-C disinfection or horticulture modules, where technical know-how outweighs scale.

Mergers, joint ventures, and capacity expansions are reshaping the field. The Dixon-Signify 50-50 entity aims to fuse manufacturing scale with advanced package intellectual property, targeting both export and domestic automotive OEMs. Calcom Vision’s tie-up with Goldmedal Electricals secures downstream distribution for its enlarged COB output, illustrating how ODM partnerships can offset limited brand equity. Meanwhile, incumbents like Havells and Surya Roshni allocate new capital to backward integration but still rely on imported epitaxy, exposing them to exchange-rate volatility. As larger players lock up patents and quality certifications, market entrants must orchestrate ecosystems of chip suppliers, driver makers, and thermal specialists rather than attempt full vertical integration. Overall, strategic positioning now hinges on securing technology licenses, meeting reliability benchmarks, and aligning with PLI-driven domestic value-addition goals.

India High-Power LED Package Industry Leaders

Nichia Corp.

Osram Opto Semiconductors GmbH

Seoul Semiconductor Co., Ltd.

Lumileds Holding B.V.

Bridgelux, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Calcom Vision formalized a manufacturing partnership with Goldmedal Electricals to produce LED products at its Greater Noida plant, targeting annual revenue of INR 250 million (USD 2.8 million).

- February 2026: Marelli-Motherson opened India’s first single-piece end-to-end automotive lamp facility in Sanand, Gujarat, launching 17 mm slim LED headlamps.

- June 2025: Bajaj Electricals finished installing LED floodlights at MCA Stadium Pune, delivering 30% higher illumination versus metal-halide fixtures.

- May 2025: Calcom Vision secured PLI Large-Investment status, raising committed CAPEX to INR 250 million (USD 2.8 million) for drivers and LED engines.

India High-Power LED Package Market Report Scope

The India High-Power LED Package Market Report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-die Packages (SMD / Discrete), Multi-die Packages (SMD), COB (Chip-on-Board), Other Architectures), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

| 1W-3W |

| 3W-10W |

| Above 10W |

| Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) |

| COB (Chip-on-Board) |

| Other Architectures (CSP, Flip-chip, Hybrid Modules) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| By Power Range | 1W-3W |

| 3W-10W | |

| Above 10W | |

| By Architecture | Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) | |

| COB (Chip-on-Board) | |

| Other Architectures (CSP, Flip-chip, Hybrid Modules) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche |

Key Questions Answered in the Report

What is the forecast size of the India High-Power LED package market by 2031?

The value is projected to reach USD 230.98 million by 2031.

How fast is the automotive lighting segment growing within this space?

Automotive lighting packages are expected to expand at a 6.93% CAGR between 2026-2031.

Which power class currently leads unit shipments?

The 1 W-3 W range held 47.84% shipment share in 2025, largely due to earlier residential bulb programs.

Why are chip-on-board packages gaining traction?

COB layouts lower thermal resistance and support higher power density, making them suited to matrix headlamps and spectrum-tuned horticulture lights.

What policy initiative is driving local manufacturing?

The Production-Linked Incentive scheme provides cash incentives tied to domestic value-addition and has approved 84 companies for LED investments.

Which factor most limits upstream integration?

Heavy reliance on imported epitaxy equipment restricts domestic chip fabrication capability.

Page last updated on: