Asia-Pacific High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

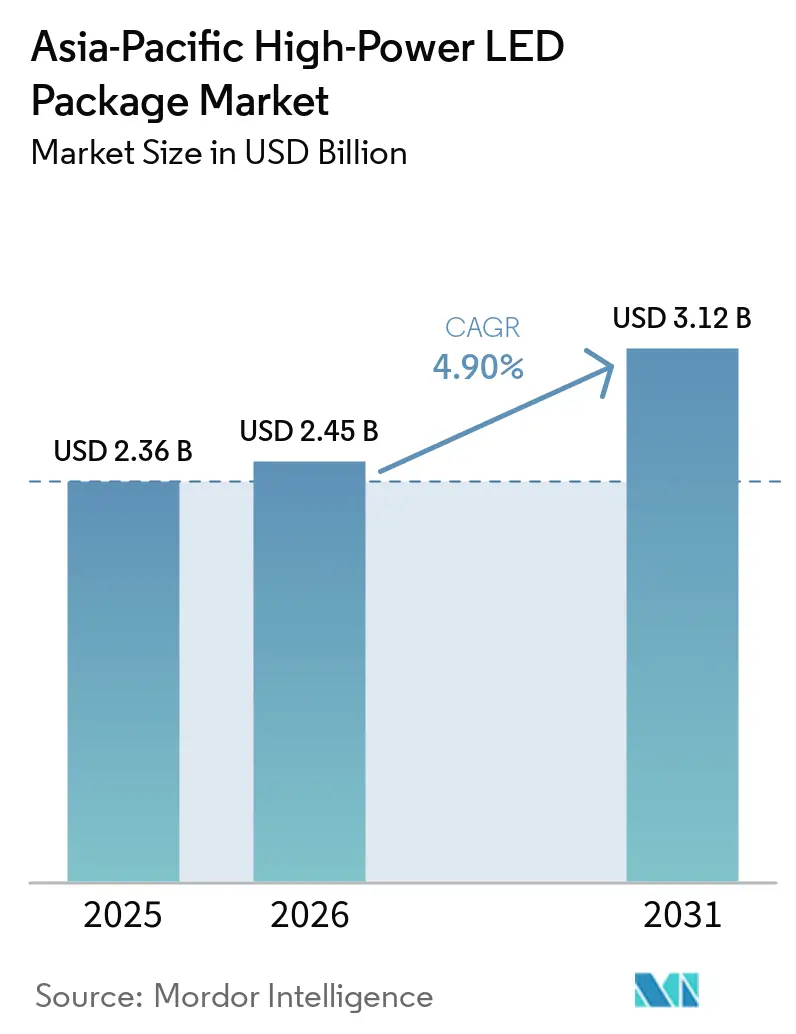

| Base Year Market Size (2025) | USD 2.36 Billion |

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 3.12 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific High-Power LED Package Market Analysis by Mordor Intelligence

The Asia-Pacific High-Power LED Package market size was valued at USD 2.45 billion in 2026 and is projected to expand from USD 2.36 billion in 2025 to reach USD 3.12 billion by 2031, registering a 4.90% CAGR over 2026-2031. Continuous migration toward premium automotive headlamps, mini-LED backlights, and industrial retrofits is redirecting demand away from commodity general-illumination modules. China’s 67.73% revenue dominance in 2025 gave local manufacturers scale advantages, yet margin pressure emerged due to volatility in sapphire substrates and flip-chip patent disputes. India is gaining momentum as Draft AIS-199 headlamp rules accelerate the adoption of adaptive high-power arrays. Regionwide, thermal-management breakthroughs that enable single-package outputs above 60 W are realigning cost curves, narrowing the gap between high-power and mid-power solutions.

Key Report Takeaways

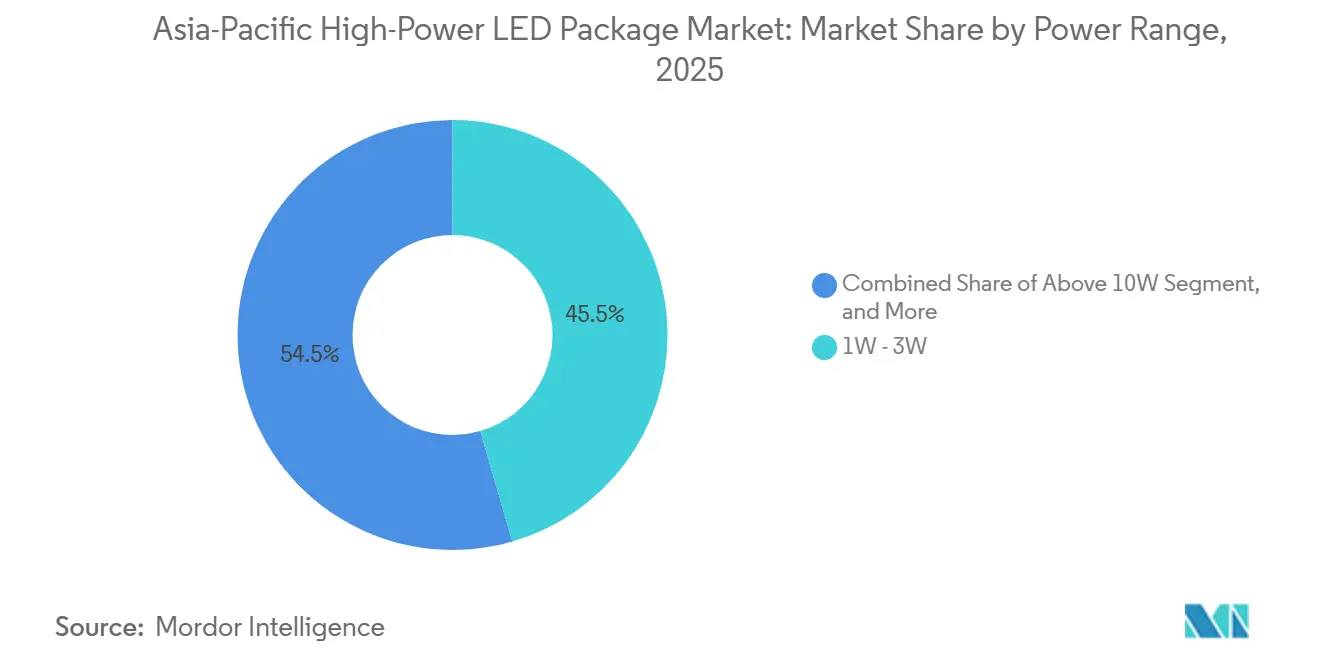

- By power range, the 1 W-3 W tier led with 45.51% High-Power LED Package market share in 2025, while the above 10 W packages recorded the fastest 5.39% CAGR through 2031.

- By architecture, single-die packages held 35.67% revenue share in 2025, whereas chip-on-board designs are forecast to grow at a 5.78% CAGR to 2031.

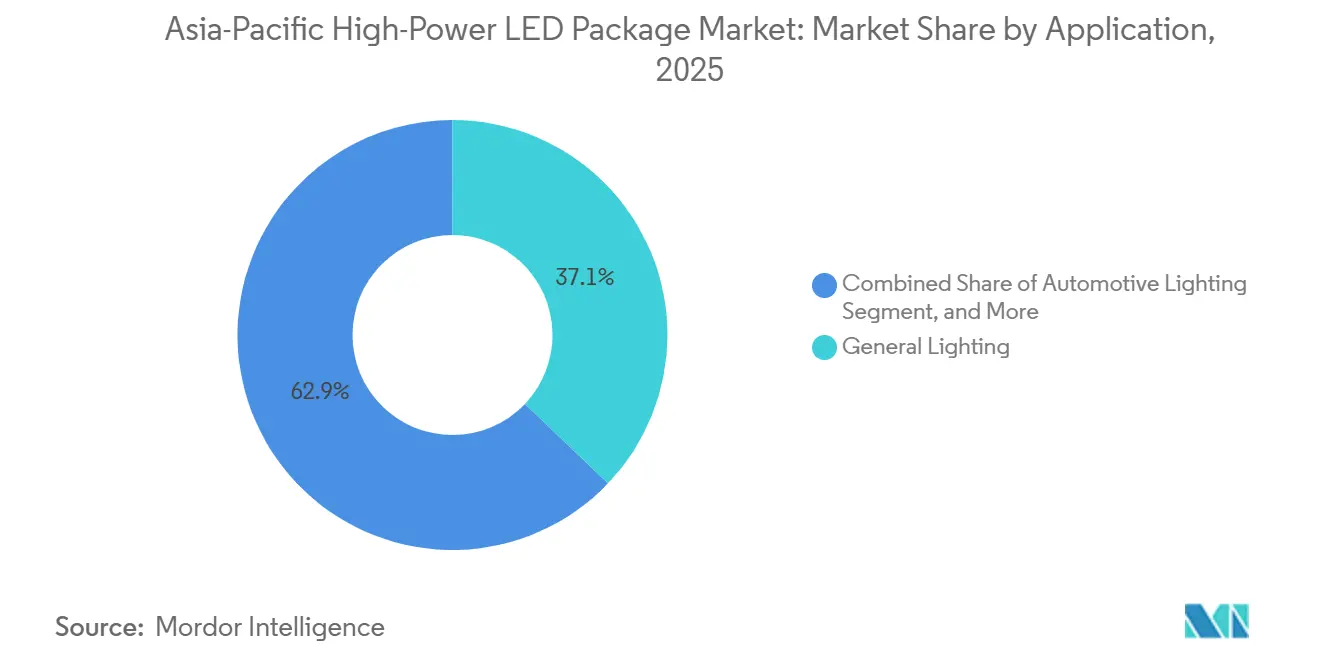

- By application, general lighting accounted for 37.12% of 2025 demand, but automotive lighting is advancing at a 5.71% CAGR over 2026-2031.

- By geography, China contributed 67.73% of 2025 revenue, and India is poised for a 6.81% CAGR between 2025 and 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific High-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Mini-LED Backlight Adoption in Premium Consumer Devices | +1.2% | China, South Korea, Taiwan; spillover to Japan | Medium term (2-4 years) |

| Accelerated Smart-Factory LED Retrofits Across East Asia | +0.9% | China core, Japan secondary, Vietnam emerging | Short term (≤ 2 years) |

| Government-Backed Automotive LED Mandates in China and India | +1.1% | China and India primary, ASEAN secondary | Medium term (2-4 years) |

| Thermal-Management Breakthroughs Enabling Above 5 W Single-Package Output | +0.8% | Global, with early adoption in China and Japan | Long term (≥ 4 years) |

| Rise of Vertical-Integration Models Among Chinese Packaging Houses | +0.6% | China dominant, competitive pressure in Taiwan | Short term (≤ 2 years) |

| Advanced Driver-Assistance Systems Demanding High-Intensity Headlamps | +1.0% | China, India, Japan; gradual ASEAN uptake | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Mini-LED Backlight Adoption in Premium Consumer Devices

Premium televisions and tablets are shifting from edge-lit designs to mini-LED direct backlighting to raise contrast ratios and local dimming precision, a move that directly lifts demand for high-power packages capable of handling elevated current densities without color-shift drift.[1]Samsung Electronics, “Neo QLED 2026 Product Brief,” samsung.com Samsung’s 2026 Neo QLED lineup and MediaTek’s showcase of micro-LED display engines confirm technology migration beyond consumer screens. TrendForce estimates show that mini-LED backlight unit shipments will grow 17% annually from 2024 through 2029, with tablet penetration reaching 15% by 2027. Packages in the 3 W-10 W bracket benefit most because they combine high luminous efficacy with manageable thermal footprints. Suppliers able to maintain sub-5 nm wavelength tolerance, still concentrated in Japan and South Korea, secure margin expansion as OEMs tighten binning specifications.

Accelerated Smart-Factory LED Retrofits Across East Asia

Manufacturing plants in China and Japan are swapping legacy discharge lamps for high-power LED arrays to meet energy-efficiency mandates and improve machine-vision accuracy. Dagu Chemical’s 2025 program integrated smart lighting controls with enterprise resource planning systems to optimize lux levels, achieving operational payback within 2 years.[2]Dagu Chemical, “Smart Lighting Retrofit Case Study,” daguchem.com Packages above 5 W reduce luminaire counts, thereby cutting installation labor and maintenance cycles over a 10-year life. In 2024, China’s Ministry of Industry and Information Technology issued guidance classifying LED retrofits as a qualified carbon-reduction measure. Demand is also rising for tunable white-spectrum products that shift color temperature for night-shift ergonomics.

Government-Backed Automotive LED Mandates in China and India

China’s GB 4599-2024 standard and India’s Draft AIS-199 prescribe luminous-intensity and beam-uniformity thresholds that effectively rule out halogen lamps in new vehicles. Adaptive driving-beam systems, therefore, rely on multi-die or chip-on-board packages that support rapid 1 kHz cycling and precise optical control. Lumileds responded in October 2025 with the 433 µm-height Altilon SMD-A to align with regulatory timelines. India’s automotive LED lighting segment is forecast to grow from USD 1.67 billion in 2025 to USD 2.32 billion by 2030, reflecting a 6.81% CAGR. Localization incentives are attracting joint ventures between global suppliers and Indian tier-two vendors.

Thermal-Management Breakthroughs Enabling Above 5 W Single-Package Output

Refond Optoelectronics commercialized a diamond-substrate platform in 2025 that delivers 60 W and 6,500 lumens by exploiting diamond’s 2,200 W m⁻¹ K⁻¹ thermal conductivity. Lumileds lowered junction-to-case resistance below 0.5 K W⁻¹ across its latest LUXEON series, sustaining 150 °C ambient operation without derating. Fewer high-power packages translate into lower driver counts and simpler optics for stadium floodlights and industrial high bays. Vendors with in-house material science, such as Nichia and OSRAM, command premium pricing, while commodity assemblers face compressed margins as customers demand equivalent thermal performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Tightness of Sapphire Substrates Post-2025 | -0.7% | Global, acute in China and Taiwan | Short term (≤ 2 years) |

| IP Litigation Risks in Flip-Chip Package Designs | -0.5% | Taiwan, China, South Korea; spillover to Japan | Medium term (2-4 years) |

| Persistent Cost Gap Versus Mid-Power Alternatives in General Lighting | -0.4% | Price-sensitive markets: India, Southeast Asia, China tier-3 cities | Long term (≥ 4 years) |

| Regulatory Scrutiny on Blue-Light Hazard in Public Illumination | -0.3% | Gulf Cooperation Council, EU; emerging in China and India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Tightness of Sapphire Substrates Post-2025

As semiconductor fabs reallocated epitaxy lines toward radio-frequency filters for 5G infrastructure, sapphire wafer supply tightened, and spot prices rose by 20% quarter over quarter.[3]Sapphire Technology, “Quarterly Sapphire Wafer Pricing Report 2026Q1,” sapphiretech.com Chinese and Taiwanese packagers without long-term offtake contracts must bid in volatile spot markets, eroding gross margins. Vertically integrated players such as Sanan Optoelectronics, which runs captive sapphire-growth furnaces, maintain cost stability and underprice rivals, driving consolidation. Relief is likely after 2027 when new Malaysian and Vietnamese capacity becomes operational, yet near-term tightness is expected to restrict smaller firms from committing to multi-year automotive contracts.

IP Litigation Risks in Flip-Chip Package Designs

Everlight Electronics filed infringement suits in February 2026 against Lumileds and Seoul Semiconductor over flip-chip bonding patents, resurfacing long-standing IP disputes. For mid-tier packagers, potential injunctions and stacked royalties raise both operational and financial risk. Capital allocation to new flip-chip lines, which need USD 15 million-USD 25 million per facility, now looks less attractive. Large players with cross-licensing portfolios remain insulated, but uncertainty could slow adoption of flip-chip designs in automotive and specialty lighting, indirectly supporting chip-on-board alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Above 10 W Tier Gains Traction

In 2025, the 1 W-3 W bracket captured 45.51% of the High-Power LED Package market, a position rooted in cost-sensitive general lighting. The Above 10 W group is forecast to grow 5.39% annually through 2031, propelled by automotive headlamps, industrial high bays, and stadium floodlights that benefit from luminaires built around fewer yet brighter modules. This structural pivot is possible because diamond substrates and sub-0.5 K W⁻¹ junction-to-case resistance allow packages to exceed earlier thermal ceilings. Automotive original equipment manufacturers value tighter beam control and reduced driver complexity, aligning with Above 10 W adoption with China’s GB 4599-2024 and India’s Draft AIS-199 standards. Suppliers lacking advanced material science risk ceding this high-margin turf to vertically integrated Chinese and Japanese rivals.

The prospects for the 3 W-10 W middle tier remain favorable, driven by its ability to effectively balance lumen output with capital budget constraints, particularly in applications such as municipal street lighting and horticulture lamps. These segments continue to rely on this power range due to its cost-effectiveness and suitability for their specific requirements. However, the declining cost per lumen at higher power ratings poses a potential challenge to the long-term relevance of this tier. This trend could become more pronounced if advancements in smart-factory retrofits and mini-LED backlights persist, as these technologies increasingly emphasize premium efficacy and tighter binning standards, which may shift market preferences toward higher-performing alternatives.

By Architecture: COB Configurations Capture Automotive Design Wins

Single-die packages accounted for 35.67% of 2025 revenue, serving legacy retrofit and low-cost general lighting applications. Chip-on-board solutions, however, should log a 5.78% CAGR to 2031, as headlamps and mini-LED backlights need low z-height and uniform luminance. Harvatek’s February 2026 COBsidian launch showcased 98% uniformity across a 50 mm aperture, an attribute prized by premium automotive original equipment manufacturers. Bridgelux’s DriveLux family, released in March 2025, further validated the suitability of COB for adaptive front-lighting systems.

Flip-chip formats still deliver exceptional thermal paths, yet ongoing litigation elevates licensing uncertainty, nudging some tier-two vendors toward COB. Surface-mount multi-die packages will remain relevant in signage and architectural lighting, where rapid installation outweighs footprint minimization. The High-Power LED Package market, therefore, splits into high-volume single-die commodity supply, fast-growing automotive COB, and specialty niches where performance premiums justify custom formats.

By Application: Automotive Lighting Outpaces General Illumination

General lighting represented roughly 37.12% of demand in 2025 and underpins base-load volumes for many Chinese and Southeast Asian suppliers. Automotive lighting, though smaller, is forecast to accelerate at 5.71% annually over 2026-2031 as adaptive beam patterns become mandatory. Lumileds’ Altilon SMD-A exemplifies how suppliers tailor low z-height, high-frequency, high-intensity packages to meet evolving vehicle standards. The High-Power LED Package market size allocated to automotives is therefore set to expand faster than the overall regional average.

Display and backlighting benefit from mini-LED penetration in premium tablets and televisions. Samsung’s 2026 Neo QLED range and MediaTek’s micro-LED data-center modules underscore widening use cases, helped by a 17% shipment CAGR for mini-LED backlight units through 2029. Specialty verticals such as horticulture and medical devices remain small but command above-average margins because precise spectral performance is critical.

Geography Analysis

China retained the dominant 67.73% High-Power LED Package market share in 2025, a position it defends through vertically integrated giants such as NationStar, Sanan, and Honglitronic, which control sapphire growth, die fabrication, and final assembly. These companies leveraged scale to lift utilization even as sapphire wafer spot prices spiked, then jointly raised package prices 5%-8% in January 2026 to protect margins. The strategy signals disciplined capacity management rather than past price-cutting cycles, and it keeps the regional High-Power LED Package market size anchored in the Pearl and Yangtze River Deltas. However, patent-licensing uncertainty in flip-chip designs and stricter blue-light safety rules are nudging export-oriented Chinese suppliers to diversify into COB and chip-scale formats with lower royalty exposure.

India is emerging as the fastest-growing demand center, propelled by Draft AIS-199 headlamp standards and localization incentives that encourage domestic assembly. India’s automotive LED lighting revenue is projected to rise from USD 1.67 billion in 2025 to USD 2.32 billion by 2030, translating into a 6.81% CAGR that surpasses the broader Asia-Pacific average. Global suppliers are responding with joint-venture proposals that bundle high-power packages with Indian tier-two optics and driver specialists, aiming to satisfy content-requirement thresholds. The ability to qualify products quickly under Bharat Stage VII emissions timelines gives early movers an edge, especially in adaptive driving-beam headlamps, where arrays above 10 W slash module counts.

Southeast Asia is positioning itself as a secondary manufacturing hub as brands seek China-plus-one strategies. Sunlight Lighting committed RMB 324 million (USD 45 million) to a Thailand facility in March 2026, while Seoul Semiconductor transferred WICOP assembly know-how to Vietnam’s OMINSU in June 2025. These moves reduce tariff risk when exporting to the United States and Europe and create localized supply for ASEAN automotive clusters. Japan, meanwhile, is pivoting toward ultraviolet and premium automotive packages; Toyoda Gosei’s launch of its moving-light technology in January 2026 underscores a shift from commodity general lighting to high-spec niches. Australia, New Zealand, and the Pacific islands contribute marginal volumes because limited vehicle production and small industrial footprints constrain large-scale retrofits.

Competitive Landscape

The regional High-Power LED Package market exhibits moderate concentration: Nichia, Samsung, OSRAM, Seoul Semiconductor, and Lumileds account for an estimated 40%-45% of combined revenue, while dozens of Chinese and Taiwanese firms compete on speed and cost. Chinese leaders such as NationStar and Sanan rely on vertical integration to buffer volatility in sapphire substrates, enabling them to underbid rivals during shortages while still funding rapid product refresh cycles. Japanese and South Korean incumbents are exiting low-margin bulbs and reallocating research budgets to ultraviolet disinfection, human-centric luminaires, and automotive-grade modules where patent portfolios sustain pricing power.

Technology differentiation rather than sheer volume now shapes competitive advantage. Refond’s diamond-substrate platform delivers 60 W at 6,500 lumens, a performance level that commodity assemblers cannot match without a multi-million-dollar investment in materials science. Lumileds pairs sub-0.5 K W⁻¹ thermal paths with 1 kHz pulse-width modulation to satisfy adaptive driving-beam requirements and secure design wins with Chinese and European original equipment manufacturers. Harvatek and Bridgelux have carved high-margin niches by supplying chip-on-board arrays that achieve 98% luminance uniformity across 50 mm apertures, a prerequisite for matrix headlamps in premium SUVs.

Legal maneuvering remains a swing factor. Everlight’s February 2026 infringement suits against Lumileds and Seoul Semiconductor over flip-chip bonding patents could force mid-tier suppliers to pay stacked royalties or pause shipments to avoid injunctions. Such uncertainty directs some buyers toward chip-on-board or chip-scale packages that skirt contested claims, indirectly reinforcing the incumbents’ hold on premium automotive and display sockets. As a result, the High-Power LED Package market size tied to specialty applications is likely to consolidate further around players that combine robust IP, captive epitaxy, and advanced thermal materials, while fragmented low-cost vendors cling to price-sensitive general illumination.

Asia-Pacific High-Power LED Package Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

OSRAM Opto Semiconductors GmbH

Seoul Semiconductor Co., Ltd.

LG Innotek Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sunlight Lighting allocated RMB 324 million (USD 45 million) to build a Thailand assembly plant aimed at Southeast Asian automotive and industrial customers. Full capacity is slated for first-quarter 2027.

- February 2026: Everlight Electronics filed United States lawsuits against Lumileds and Seoul Semiconductor over flip-chip patent claims, seeking injunctive relief and damages.

- February 2026: Harvatek Corporation introduced COBsidian, a chip-on-board series delivering 98% luminous uniformity within a 50 mm aperture for matrix LED headlamps.

- January 2026: Toyoda Gosei unveiled moving-light technology that dynamically reshapes beams for premium SUVs, with series production expected in second-half 2027.

Asia-Pacific High-Power LED Package Market Report Scope

The Asia-Pacific High-Power LED Package Market Report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-Die Packages (SMD / Discrete), Multi-Die Packages (SMD), COB (Chip-on-Board), Other Architectures), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty / Niche), and Geography (China, Japan, India, Southeast Asia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| 1 W – 3 W |

| 3 W – 10 W |

| Above 10 W |

| Single-Die Packages (SMD / Discrete) |

| Multi-Die Packages (SMD) |

| COB (Chip-on-Board) |

| Other Architectures (CSP, Flip-Chip, Hybrid Modules) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| China |

| Japan |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Power Range | 1 W – 3 W |

| 3 W – 10 W | |

| Above 10 W | |

| By Architecture | Single-Die Packages (SMD / Discrete) |

| Multi-Die Packages (SMD) | |

| COB (Chip-on-Board) | |

| Other Architectures (CSP, Flip-Chip, Hybrid Modules) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche | |

| By Country | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the High-Power LED Package market in the Asia-Pacific region today?

The market was valued at USD 2.45 billion in 2026.

What CAGR is expected for the High-Power LED Package market from 2026 to 2031?

A 4.90% CAGR is projected for the period.

Which power range holds the biggest share of the High-Power LED Package market?

The 1 W-3 W bracket led with 45.51% share in 2025.

What segment is growing the fastest within the High-Power LED Package market?

Above 10 W packages are forecast to expand at a 5.39% CAGR through 2031.

Which country is the fastest-growing demand center for high-power LED packages?

India is forecast to post a 6.81% CAGR between 2025 and 2030.

Who are the major players in the High-Power LED Package market?

Nichia, Samsung, OSRAM, Seoul Semiconductor, and Lumileds collectively hold about 40%-45% share.

Page last updated on: