LED Packaging Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

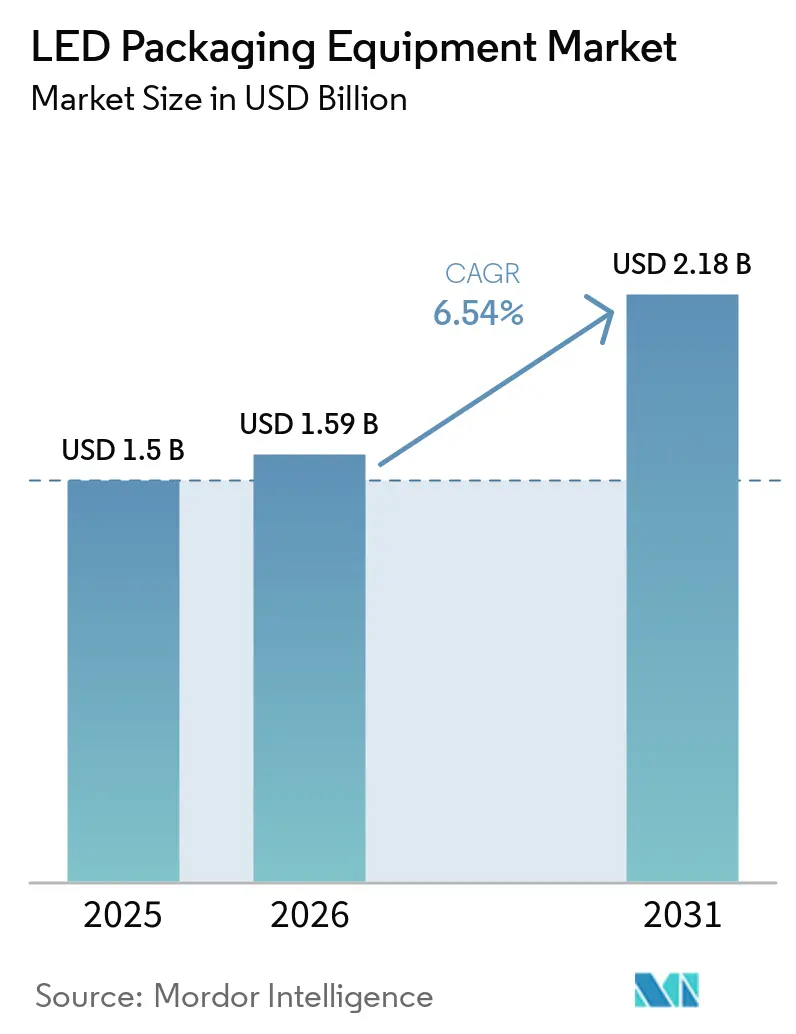

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

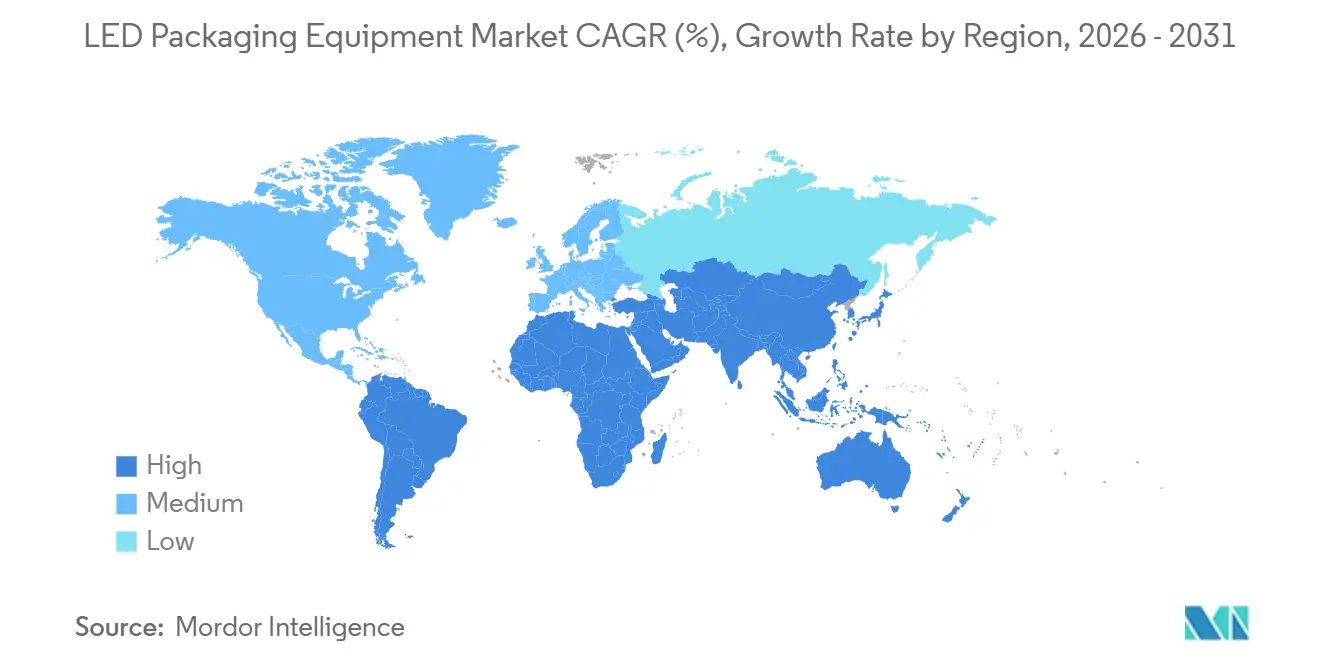

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

LED Packaging Equipment Market Analysis by Mordor Intelligence

The LED packaging equipment market size is expected to increase from USD 1.50 billion in 2025 to USD 1.59 billion in 2026 and reach USD 2.18 billion by 2031, growing at a CAGR of 6.54% over 2026-2031. Solid momentum stems from panel makers shifting to mini-LED backlighting, automotive suppliers embracing adaptive headlamps, and OSATs adopting chip-scale package (CSP) architectures that call for sub-10 micrometer placement precision. Asia-Pacific currently anchors most capacity thanks to China’s 50% domestic-equipment mandate and Japan’s dedicated subsidy for advanced packaging. Parallel traction in inline inspection and sintered-silver die attach is squeezing process windows and raising capital intensity, which, in turn, favors vendors with proven yield credentials. Heightened export-control oversight and a widening skills gap temper near-term expansion but have not derailed new fab construction or the long-term transition to highly automated lines.

Key Report Takeaways

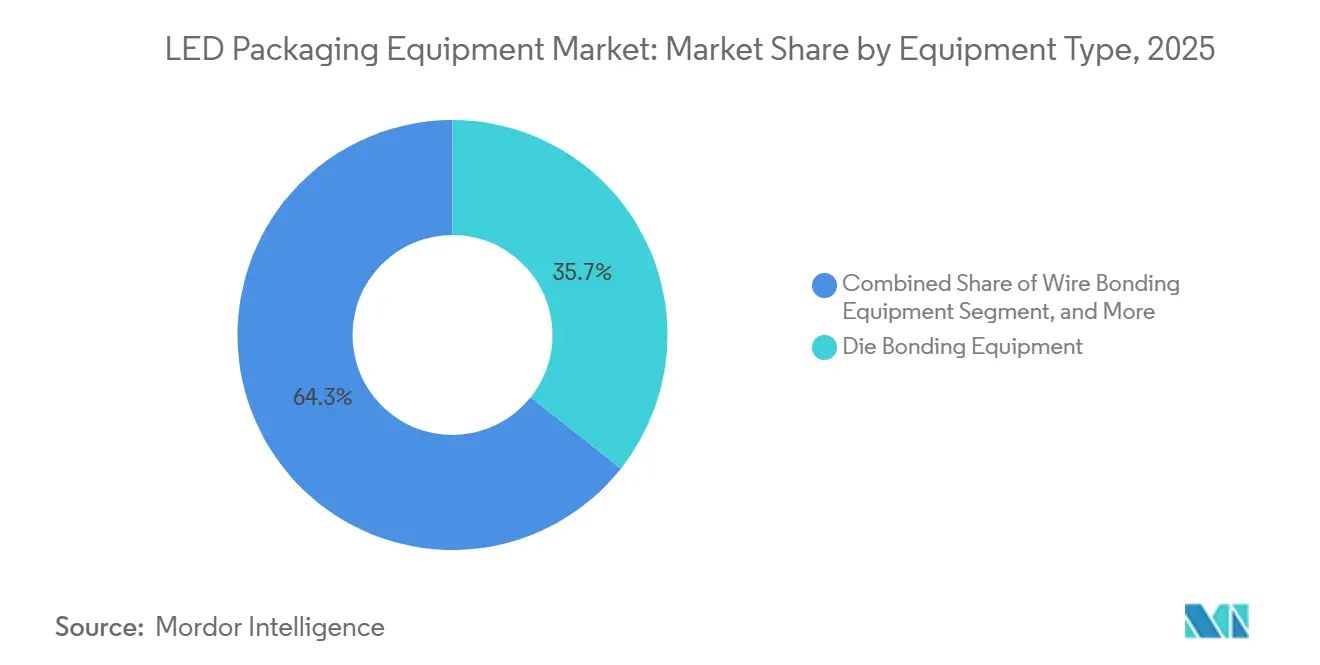

- By equipment type, die bonding equipment held 35.68% of LED packaging equipment market share in 2025, while automated packaging systems are projected to expand at a 6.97% CAGR to 2031.

- By package type, surface-mount device (SMD) platforms led with 42.74% revenue share in 2025; CSP equipment is forecast to log the fastest growth at a 6.91% CAGR through 2031.

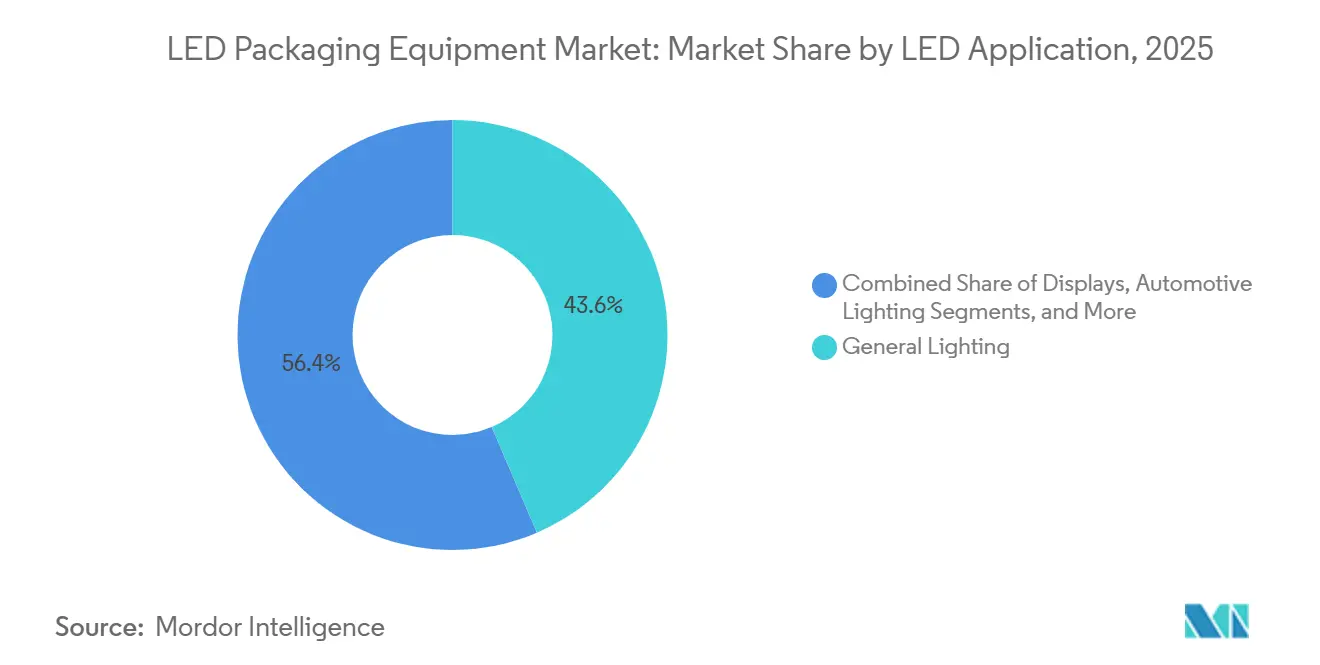

- By application, general lighting represented 43.58% of 2025 demand, whereas display lines are expected to register the highest growth at a 7.11% CAGR over 2026-2031.

- By geography, Asia-Pacific controlled 68.71% of 2025 revenue and is on course to post a 7.17% CAGR, retaining its lead through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global LED Packaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Mini-LED and Micro-LED Capacity Ramp-Up | +1.8% | Global, APAC core with spill-over to North America | Medium term (2–4 years) |

| Rising Adoption of Automotive Adaptive Headlamps | +1.2% | Global, North America and Europe early adopters | Medium term (2–4 years) |

| Line Yield Gains Via Inline AOI/AXI Integration | +0.9% | Global, APAC manufacturing hubs | Short term (≤ 2 years) |

| Demand for Low-Temperature Sintered Silver Die-Attach Pastes | +0.7% | Global, APAC and North America advanced packaging clusters | Medium term (2–4 years) |

| Government Subsidies for Domestic Packaging Lines in Asia-Pacific | +1.1% | APAC core, Japan and China policy-driven | Short term (≤ 2 years) |

| Equipment Refurbishment Market Formalisation in Europe | +0.4% | Europe, North America secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Mini-LED and Micro-LED Capacity Ramp-Up

Segment leaders are scaling full-array local-dimming panels that use tens of thousands of mini-LEDs, forcing equipment to deliver mass-transfer speed without compromising ±10 micrometer accuracy. ASMPT’s Vortex II die bonder hits 99.999% light-up yield for 2 mil × 4 mil dies, raising the performance bar for advanced display deployment. Kulicke and Soffa’s LUMINEX laser system couples sorting and re-pitching in one tool, widening addressable opportunities across direct-view RGB and backlighting workflows. Besi projects its die-attach addressable market to double to USD 1.6 billion by 2026 on the back of photonics and LED adoption. These upgrades lift capital per line by as much as 40%, creating scale advantages for tier-1 panel makers with access to state support. Smaller fabs struggle to match throughput, potentially accelerating industry consolidation.

Rising Adoption of Automotive Adaptive Headlamps

Automakers are migrating to matrix LED systems that enable glare-free high beams and 600-meter reach, pushing packaging tolerances toward ±35 micrometers in z-height. ams OSRAM’s OSLON Compact PL families come with isolated thermal pads that demand precision pick-and-place and controlled thermal-interface materials. Pixelated emitters require sub-pixel placement, so equipment vendors are embedding high-resolution vision systems and auto-recovery loops for misplacement correction. Qualification under AEC-Q102 can last 24 months, elongating the validation pipeline and favoring suppliers with automotive-certified process recipes. As regulatory green lights spread from Europe to North America and Asia, adaptive modules are set to become standard on mid-range trims, stimulating higher unit orders for die bonders and inspection tools.

Line Yield Gains Via Inline AOI/AXI Integration

Forward-looking fabs have started mounting automated optical inspection (AOI) and X-ray inspection (AXI) systems directly on packaging lines, cutting feedback loops from hours to seconds. Nordson’s SQ5000 Pro marries AOI, solder-paste inspection and metrology while its AutoProgram AI trims setup labor, a benefit amid the technician shortage. Coupled with the XM8000 2.5D X-ray tool, operators can flag die-bond voids and encapsulation defects before wafers exit the line. Real-time correction improves first-pass yield by double-digit margins, translating into fewer rework cycles and lower scrap. The trade-off is an added USD 0.5 million per station and terabytes of image storage per shift, a burden that smaller contract manufacturers must weigh against potential savings.

Demand for Low-Temperature Sintered Silver Die-Attach Pastes

High-power LEDs running above 150 °C junction temperatures are switching from high-lead solders to sintered nano-silver pastes that offer higher thermal conductivity and fatigue resistance. IEEE studies confirm robust joints at sub-250 °C sintering, enabling lower thermal stress on substrates.[1]J. Zhang et al., “Pressure-Assisted Sintered Silver for High-Power LEDs,” ieeexplore.ieee.org Equipment adaptation is essential, because pressure-assisted sintering demands tighter atmosphere control and specialty furnace profiles. Besi and ASMPT have integrated sintering-ready modules, but silver pastes cost roughly triple that of solder, limiting adoption to automotive headlamps and premium industrial fixtures. Over time, volume uptick and alloy innovations could narrow the price gap, unlocking broader market penetration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trade-Compliance Audits on US Export-Controlled Wire-Bonders | -0.8% | Global, China and Country Group D:5 restrictions | Short term (≤ 2 years) |

| Thermal Run-Away Risks in High-Power CSP Lines | -0.6% | Global, automotive and industrial lighting segments | Medium term (2–4 years) |

| Skilled Operator Shortage for Sub-10 µm Flip-Chip Bonding | -0.5% | Global, North America and Europe acute | Medium term (2–4 years) |

| CAPEX Freezes at Tier-2 Display Makers | -0.4% | APAC, tier-2 panel fabs in China and Taiwan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Trade-Compliance Audits on US Export-Controlled Wire-Bonders

The U.S. Bureau of Industry and Security added 24 tool categories to its controlled list in December 2024 and extended Foreign Direct Product rules to foreign-made gear containing U.S. ICs.[2]Bureau of Industry and Security, “Export Administration Regulations Amendments 2024,” bis.doc.gov Packaging suppliers now face 60-90 day shipment delays while licenses clear, and Applied Materials’ USD 252 million settlement illustrates the monetary downside of mis-classification. Some vendors contemplate redesigning motion-control boards to rid U.S. content, but engineering costs are steep and performance may slip. Chinese toolmakers free of these constraints are finding an opening to capture share, particularly among fabs racing to meet Beijing’s 50% local-equipment threshold.

Thermal Run-Away Risks in High-Power CSP Lines

CSP architectures cut package height yet localize heat, causing transient spikes during on-off cycles. IEEE thermal simulations reveal that a momentary current surge can create hot spots faster than heat can dissipate through the substrate. Embedding structures or advanced underfills mitigate resistance but require equipment upgrades, as seen in TOWA’s ultra-narrow gap mold underfill platform for HBM4 that can also serve high-density CSP LEDs. Automotive and industrial users often drive LEDs at 1-2 A per die, so active cooling or derating becomes mandatory, adding cost that can dampen CSP uptake in those niches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Automated Lines Emerge as Growth Engine

Die bonders accounted for 35.68% of 2025 revenue, underscoring their central role in the LED packaging equipment market. Wire bonders remain relevant, yet flip-chip and CSP designs erode their volume share as interconnects shift under-bump. Encapsulation dispensers follow die placement in the process flow, coupling silicone or epoxy resins with UV or thermal curing to protect the junction. Automated packaging systems combine all three steps, plus inline inspection, into turnkey cells that shorten takt time. These lines command 20-30% higher throughput and cut labor by roughly 15-20%, giving early adopters a measurable cost-of-ownership edge. ASMPT’s In-Line Linker System synchronizes its Vortex II bonder with upstream and downstream stations, proving the productivity jump. Although automated platforms cost two to three times more than standalone tools, payback compresses when capacity utilization tops 80%. Smaller Asian vendors are now bundling die bond, dispense, and vision modules to court price-sensitive buyers. Consequently, automated lines are projected to capture a larger share of the LED packaging equipment market by the end of the forecast period.

The surge in automation dovetails with Industry 4.0 mandates for data traceability, predictive maintenance and remote diagnostics. European customers lean on refurbished equipment to temper capex, but North American fabs often favor new, fully connected gear to comply with traceability rules tied to government incentives. As both regions wrestle with technician shortages, self-calibrating bonders and auto-programming AOI lessen the skills hurdle. The transition is unlikely to be uniform, tier-2 assemblers may still run semi-automated workcells, whereas tier-1 display and automotive suppliers gravitate toward lights-out factories. Vendors able to offer modular upgrades can cater to both profiles, cushioning revenue volatility across business cycles.

By Package Type: CSP Growth Outpaces SMD Install Base

SMD packaging held 42.74% LED packaging equipment market share in 2025, benefiting from compatibility with mainstream SMT assembly and a vast installed base. Chip-on-board (COB) arrays aggregate die on metal-core PCBs, fitting high-lumen downlights, yet they lack individual addressability. CSP packaging, although representing a smaller portion of LED packaging equipment market size, is forecast to rise at 6.91% CAGR through 2031 as mobile devices, wearables and thin automotive clusters demand sub-0.5 mm profiles. The Vortex II platform’s ±10 µm precision directly caters to CSP deployment in mini-LED matrices. IEEE benchmarks confirm CSP’s lower steady-state thermal resistance, but transient peaks still threaten runaway unless current drivers are programmed conservatively.

COB’s economics shine in fixtures where replacement is rare and lumen density trumps serviceability; yet CSP’s modularity wins in premium devices that value slimmer bezels and lower thermal headroom. Compression molding equipment from TOWA ensures void-free encapsulation at ultrathin layers, a necessity when total package height must stay below 0.3 mm. Going forward, SMD will remain dominant in cost-sensitive bulbs and tubes, but CSP is set to nibble share in automotive dashboards and flagship tablets. Equipment suppliers are therefore maintaining parallel tool lines rather than converging on a single platform, splitting R&D across divergent thermal and optical specifications.

By LED Application: Display Lines Lead the Growth Curve

General lighting accounted for 43.58% of 2025 revenue, supported by ongoing retrofit cycles across residential and commercial estates. However, mini-LED and micro-LED displays are already delivering the fastest order books, with a projected 7.11% CAGR riding premium tablets, monitors, and in-car infotainment. Panel producers require die-placement tolerances an order tighter than bulb manufacturers, favoring suppliers with sub-10 µm bonder specs. Automotive lighting modules, while smaller in volume, command higher ASPs due to AEC-Q102 validation and durability mandates. Adaptive driving beams and signature exterior accents intensify demand for selective die placement and real-time inspection.

Consumer electronics maintain a cost-centric orientation, pushing vendors to refine throughput rather than ultimate precision. Inline laser transfer and automated inspection answer that need, but pricing must clear consumer OEM hurdle rates. The landscape forces equipment makers to segment their portfolios, high-speed mass-transfer for displays, high-reliability bonders for automotive, and cost-optimized lines for bulbs. Those able to cross-pollinate innovation from display throughput to automotive reliability stand best placed to widen share within the LED packaging equipment market.

Geography Analysis

Asia-Pacific dominated with 68.71% of LED packaging equipment market size in 2025 and is on track to register a 7.17% CAGR through 2031. China’s 50% domestic-equipment quota accelerates local procurement from Naura and JT Automation, marginalizing importers unless they form joint ventures. Japan’s JPY 53.5 billion (USD 355 million) subsidy inside the Rapidus scheme aligns with its push to reboot advanced packaging, presenting a fresh customer base for precision tool vendors. South Korea’s Hanmi Semiconductor leveraged localized service to dethrone Shinkawa at Micron, highlighting how equipment uptime and proximity override legacy incumbency.

North America and Europe together accounted for roughly one-quarter of 2025 revenue. The LED packaging equipment market here is shaped by strict export compliance and a labor crunch. The U.S. BIS rulebook slows shipments containing U.S. ICs, prompting some vendors to redesign control boards for de-Americanization. On the upside, the CHIPS and Science Act channels grants toward domestic advanced-packaging lines, partially offsetting compliance drag. Europe shows rising interest in certified refurbished gear; TOWA’s program offers 40-60% price relief but operates without a region-wide quality seal, creating financing uncertainty.

South America, the Middle East and Africa contributed less than 7% of 2025 turnover. Activity centers on assembling imported LED dice into finished lamps or signage modules. Government electrification plans occasionally seed turnkey lines, yet shortage of field engineers and spare-parts logistics hampers large-scale automation. As telco-backed smart-city pilots progress, pockets of demand may emerge for mid-range AOI-equipped lines, but volumes remain too modest to sway global supplier roadmaps.

Competitive Landscape

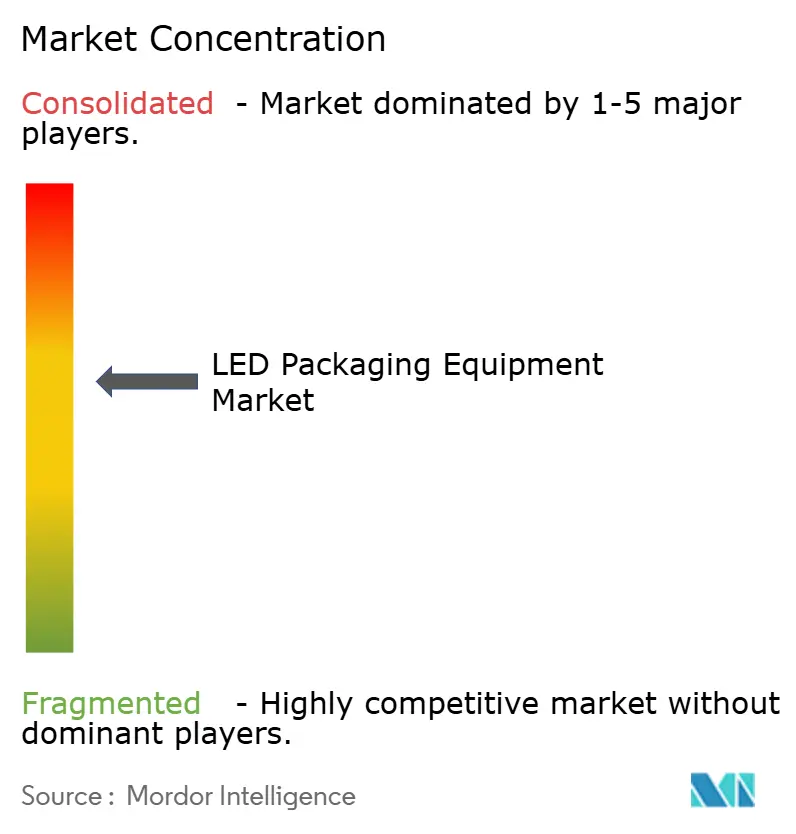

The LED packaging equipment market shows moderate concentration. The top five vendors ASMPT, Kulicke and Soffa, Besi, Hanmi Semiconductor and Shinkawa controlled an estimated 55-60% of 2025 revenue. Strategic stakes and takeover bids underline the scramble for sub-100 nm placement capability.

Applied Materials bought 9% of Besi in April 2025, and by March 2026 both Lam Research and Applied Materials were weighing full buyouts valuing Besi at EUR 14 billion (USD 15.4 billion). ASMPT lifted its thermo-compression bonding total addressable market forecast to USD 1.6 billion by 2028, eyeing a 35-40% slice on the back of AI accelerators.[3]“ASMPT to Shut Shenzhen Site,” asmpt.com Nikon and Oak Seisakusho are developing maskless direct-exposure lithography to address next-wave panel-level packaging, potentially expanding the addressable scope for die-attach and inspection portfolios.

Smaller challengers exploit service agility. Hanmi boosted yields at Micron, winning repeat orders and raising prices at SK Hynix by 25-28%. Nordson courts customers with AOI platforms featuring AI-based auto-programming that mitigate technician shortages. TOWA leverages its 66% share in molding tools by bundling singulation and IoT-enabled support, locking customers into multi-module service contracts. Competitive intensity is therefore poised to escalate as incumbents diversify into adjacent process steps and newcomers scale niche breakthroughs into mainstream production.

LED Packaging Equipment Industry Leaders

ASM Pacific Technology Ltd.

Kulicke and Soffa Industries Inc.

BE Semiconductor Industries N.V.

Hanmi Semiconductor Co., Ltd.

Palomar Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: BE Semiconductor Industries attracted takeover interest from Lam Research and Applied Materials, valuing the firm at EUR 14 billion (USD 15.4 billion).

- March 2026: Kulicke and Soffa unveiled the ASTERION-TW ultrasonic terminal welding system for copper tabs up to 2 mm, targeting power modules with ±40 µm repeatability.

- March 2026: ASMPT reported 2025 revenue of USD 1.76 billion, with advanced-packaging sales up 30.2% and thermo-compression bonding revenue climbing 146%.

- February 2026: BE Semiconductor Industries logged Q4 2025 revenue of EUR 166.4 million (USD 192.25 million) and orders of EUR 250.4 million (USD 289.30 million), proposing a EUR 1.58 dividend per share.

Global LED Packaging Equipment Market Report Scope

The LED Packaging Equipment Market is witnessing significant growth driven by increasing demand for energy-efficient lighting solutions, advancements in LED technology, and the rising adoption of LEDs across applications such as automotive, consumer electronics, and general lighting. The market's expansion is further driven by the growing focus on sustainability and the need for cost-effective production processes.

The LED Packaging Equipment Market Report is Segmented by Equipment Type (Die Bonding Equipment, Wire Bonding Equipment, Encapsulation Equipment, Automated Packaging Systems), Package Type (SMD LED Packaging, COB Packaging, CSP LED Packaging), LED Application (General Lighting, Displays, Automotive Lighting, Consumer Electronics), and Geography (North America, Europe, Asia-Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Die Bonding Equipment |

| Wire Bonding Equipment |

| Encapsulation Equipment |

| Automated Packaging Systems |

| SMD LED Packaging |

| COB Packaging |

| CSP LED Packaging |

| General Lighting |

| Displays |

| Automotive Lighting |

| Consumer Electronics |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Equipment Type | Die Bonding Equipment | |

| Wire Bonding Equipment | ||

| Encapsulation Equipment | ||

| Automated Packaging Systems | ||

| By Package Type | SMD LED Packaging | |

| COB Packaging | ||

| CSP LED Packaging | ||

| By LED Application | General Lighting | |

| Displays | ||

| Automotive Lighting | ||

| Consumer Electronics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the LED packaging equipment market?

The LED packaging equipment market is valued at USD 1.59 billion in 2026 and is forecast to reach USD 2.18 billion by 2031.

Which region leads spending on LED packaging tools?

Asia-Pacific holds nearly 69% of global revenue and is projected to grow at a 7.17% CAGR through 2031.

Which equipment segment is expanding the fastest?

Fully automated packaging lines are set to rise at a 6.97% CAGR as manufacturers chase throughput and yield improvements.

Why are CSP LEDs gaining traction despite thermal hurdles?

CSP designs cut package height and enhance optical density, and new sintered-silver die attach plus advanced underfills alleviate heat concerns enough for high-end devices.

How are export controls influencing equipment suppliers?

U.S. licensing rules slow shipments of wire bonders and die bonders to China, prompting some vendors to redesign for non-U.S. components and opening doors for domestic Chinese competitors.

What level of market concentration characterizes this sector?

The top five vendors command about 58% share, indicating moderate concentration with room for agile newcomers to win share through innovation or service.

Page last updated on: