Europe High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

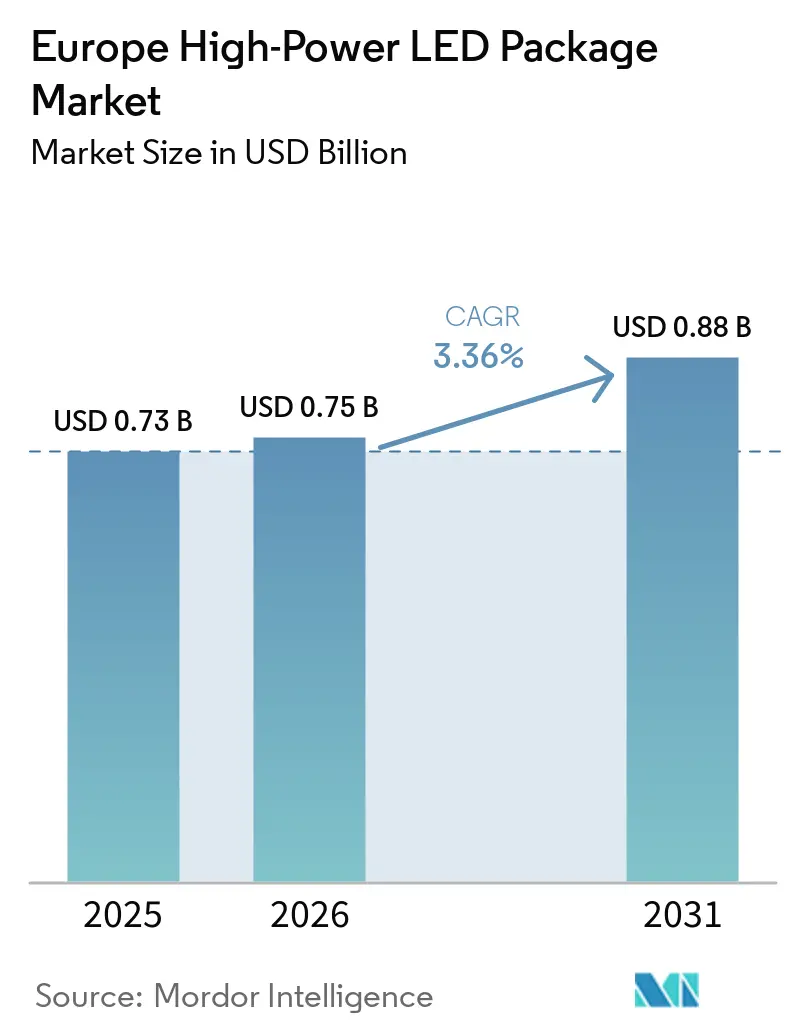

| Base Year Market Size (2025) | USD 0.73 Billion |

| Market Size (2026) | USD 0.75 Billion |

| Market Size (2031) | USD 0.88 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

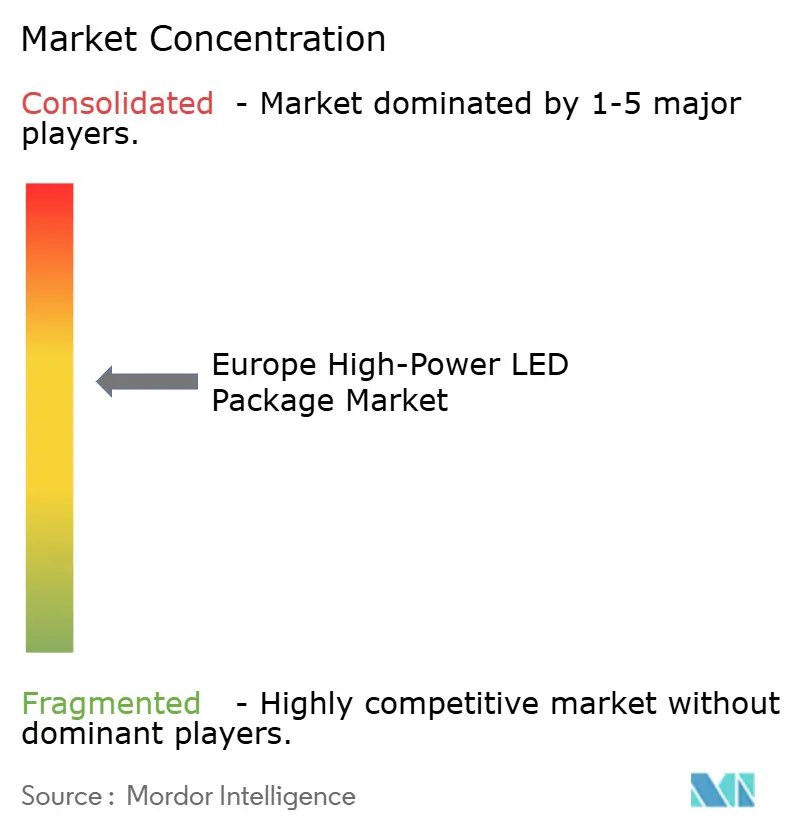

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe High-Power LED Package Market Analysis by Mordor Intelligence

The Europe High-Power LED Package Market size was valued at USD 0.73 billion in 2025 and is estimated to grow from USD 0.75 billion in 2026 to reach USD 0.88 billion by 2031, at a CAGR of 3.36% during the forecast period (2026-2031).

This trajectory reflects the pivot toward chip-on-board architectures, widening automotive demand, and sustained cost-per-lumen deflation that now averages 15% a year. Automotive lighting specifications are transferring rapidly from Asia into European vehicle platforms, compressing development cycles even as photobiological safety rules limit drive current and nudge designers toward amber-shifted phosphors. Thermal-management breakthroughs in gallium-nitride-on-silicon-carbide substrates and vapor-chamber spreaders are enabling 10 W+ packages that displace legacy multi-die arrays. Meanwhile, competitive pressure from Indian and Chinese foundries is squeezing margins and compelling European suppliers to pursue vertical integration, proprietary phosphor IP, and system-level differentiation.

Key Report Takeaways

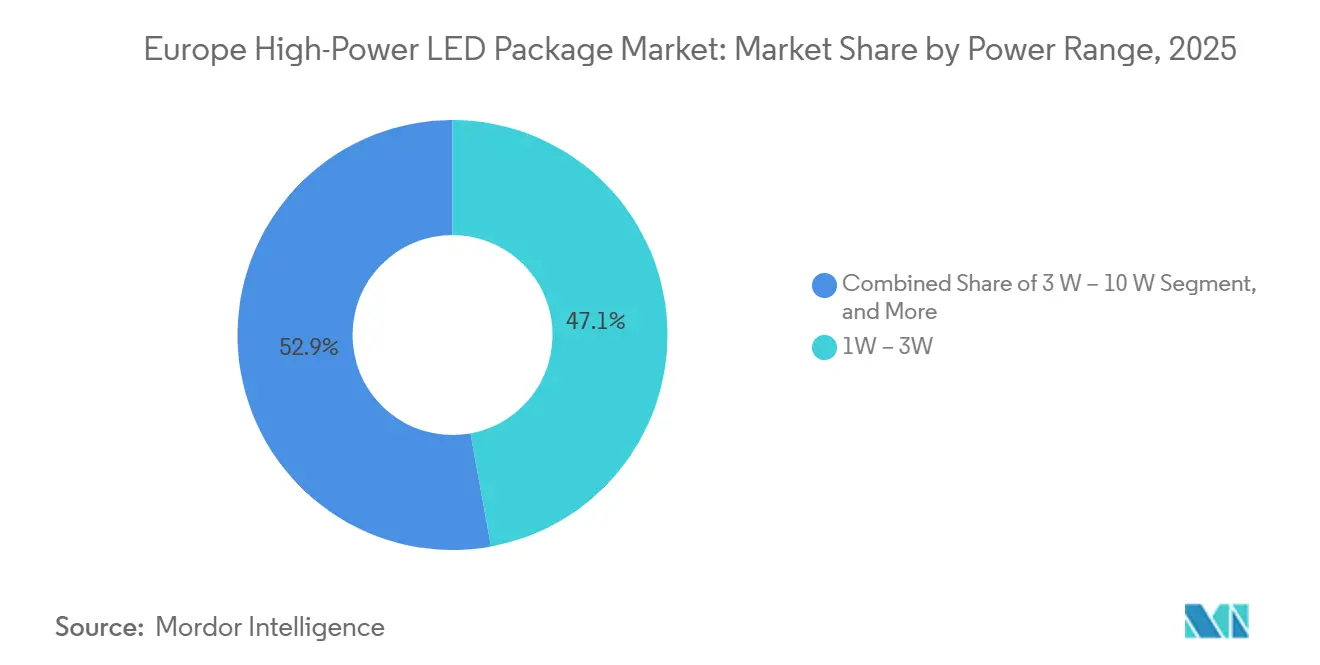

- By power range, 1 W-3 W packages accounted for 47.13% of the Europe high-power LED package market share in 2025, while above-10-W modules are projected to expand at a 3.98% CAGR through 2031.

- By architecture, single-die devices led with 36.84% revenue share in 2025; chip-on-board configurations record the highest forecast CAGR at 4.11% to 2031.

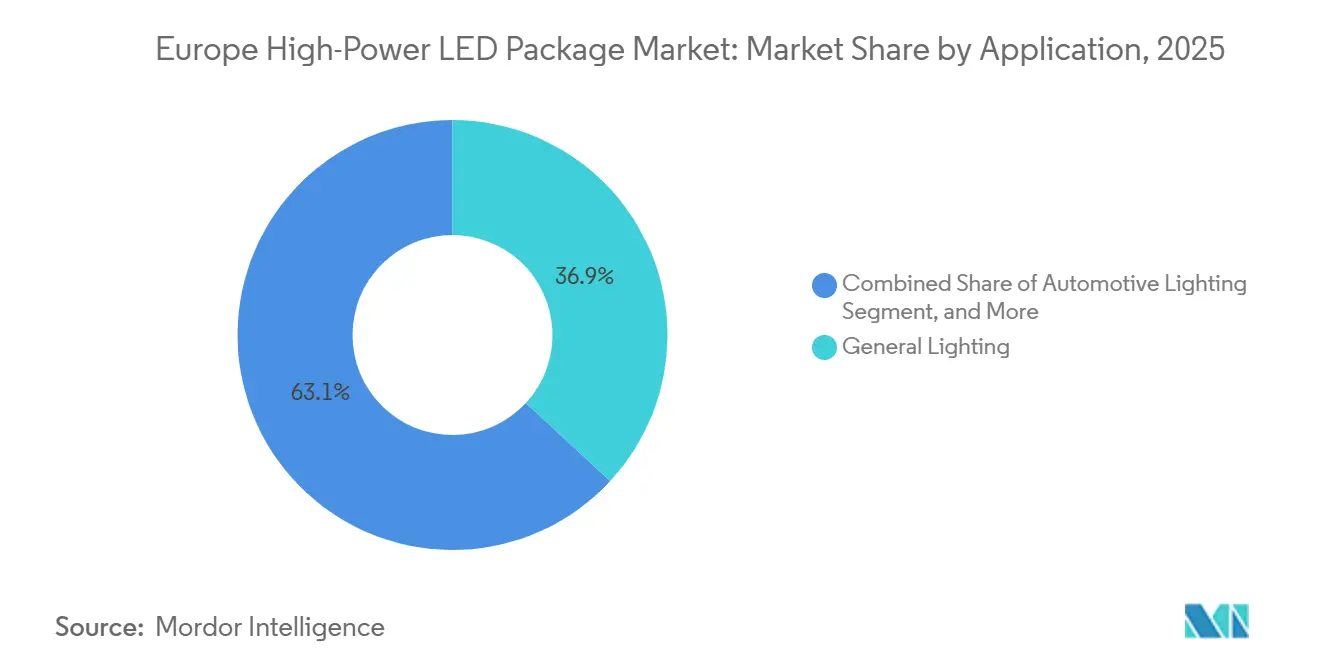

- By application, general lighting held 36.88% share of the Europe high-power LED package market size in 2025, but automotive lighting is advancing at a 3.83% CAGR through 2031.

- By Country, Germany commanded 27.93% regional revenue in 2025, while France is the fastest-growing geography with a 3.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe High-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Decline in $/lm for High-Power Packages | +0.9% | Global, pronounced in Germany and France | Short term (≤ 2 years) |

| Soaring Automotive LED Penetration in China and Japan | +0.7% | Europe-wide spillover from APAC platforms | Medium term (2-4 years) |

| Energy-Efficiency Mandates Across ASEAN | +0.4% | Indirect influence on European exports and standards | Medium term (2-4 years) |

| Industrial Retrofits to High-Bay LED Fixtures | +0.5% | Germany, France, United Kingdom, Nordic corridors | Short term (≤ 2 years) |

| Thermal-Management Breakthroughs Enabling 10 W+ Packages | +0.6% | Germany and France R&D hubs | Long term (≥ 4 years) |

| India’s PLI Incentives for GaN-on-SiC Foundries | +0.3% | Global competitive pressure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in $/lm for High-Power Packages

High-power LED package prices are falling roughly 15% a year as oversupply in China’s gallium-nitride wafer capacity converges with efficiency gains in phosphor conversion. European luminaire makers are redesigning fixtures around fewer, brighter emitters, cutting bill-of-materials costs but shrinking supplier margins. Vertically integrated vendors that own phosphor IP can absorb wafer volatility, whereas merchant assemblers face immediate commoditization. Lumileds’ LUXEON HL2X-V, launched February 2025, underscores this shift by delivering 200 lm W-¹ at 85 °C junction temperature and lowering system cost for industrial high-bay retrofits.[1]European Patent Office, “Lumileds LUXEON HL2X-V Specification,” epo.org Procurement teams increasingly emphasize dollar-per-lumen benchmarks over headline efficacy, tightening contract cycles and accelerating design revisions.

Soaring Automotive LED Penetration in China and Japan

LED penetration in Chinese passenger cars topped 70% in 2025, and Japan cleared micro-LED arrays for ultrathin headlamps in March 2025.[2]Directorate-General for Energy, “Energy-Efficient Lighting in the EU,” europa.eu European automakers are now importing these architectures to meet EU safety rules and differentiate premium trims, bringing chip-on-board modules into regional supply chains. Hella, part of Forvia, cited lighting revenue of EUR 3 billion (USD 3.39 billion) for 2023 and a 25% share of Europe’s premium headlamp segment, on the back of gallium-nitride-on-silicon-carbide packages that cut EV energy draw by 40%. Asian cost baselines, however, frame European negotiations, forcing suppliers to match APAC unit economics while meeting stricter binning and reliability metrics.

Energy-Efficiency Mandates Across ASEAN

Indonesia, Thailand, and Vietnam introduced minimum efficacy thresholds at 85 lm W-¹ and power factors above 0.95 for LED luminaires between 2025 and 2026. Although directed at local markets, the measures form a de facto benchmark for European exporters and harmonize testing protocols that ripple into EU product specifications. European package vendors now license phosphor and thermal materials to ASEAN contract manufacturers, accelerating technology diffusion and eroding home-region production volume. Luminaire brands meanwhile source compliant packages offshore, redirecting price pressure back to European upstream suppliers.

Industrial Retrofits to High-Bay LED Fixtures

Manufacturing and logistics operators across Germany, France, and the United Kingdom have replaced metal-halide lamps with LED high-bay systems, capturing 50%-70% energy savings and securing 12-24 month paybacks. Packages in the 3 W-10 W range dominate these installs, often in chip-on-board form to maximize lumen density for 6-12 m ceiling heights. Compliance with EN 12464-1 workplace standards further favors tight binning and high lumen-maintenance ratings. As retrofit saturation peaks, demand pivots to replacement cycles and specialized cold-storage applications requiring minus-30 °C package ratings, tempering growth yet sustaining a lucrative service market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Erosion from Intense Price Competition | -0.8% | Europe-wide, severe in commodity segments | Short term (≤ 2 years) |

| Volatile Sapphire Substrate Supply | -0.5% | Global supply chain for European assemblers | Short term (≤ 2 years) |

| Photobiological Safety Norms Limiting Drive Current | -0.3% | Europe-wide IEC 62471 enforcement | Medium term (2-4 years) |

| Inadequate End-of-Life Recycling Streams | -0.2% | Regulatory focus in Germany and France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Erosion from Intense Price Competition

Chinese foundries running at 85%+ utilization undercut European pricing by up to 30%, compressing gross margins below sustainable thresholds. Lumileds’ August 2025 sale to San’an Optoelectronics for USD 239 million illustrated the survival advantage of upstream wafer integration. European vendors, therefore, retreat to niches such as AEC-Q102-qualified automotive packages, horticulture spectra, and ultra-high-CRI museum modules. Yet lower volume limits fixed-cost absorption, creating a feedback loop of continuing margin pressure and defensive consolidation.

Volatile Sapphire Substrate Supply

Price swings of 18% for 6-inch sapphire wafers during 2025, driven by episodic oversupply and subsequent export controls, destabilized cost planning for European assemblers lacking captive crystal growth.[3]United States Geological Survey, “Mineral Commodity Summary: Sapphire,” usgs.gov While GaN-on-SiC alternatives deliver superior thermal performance, their threefold cost premium restricts adoption to high-power niches. Long-term offtake contracts with Chinese growers reduce spot risk but can over-index costs when global wafer prices retreat faster than locked-in rates, threatening bid competitiveness on multi-year automotive programs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: High-Flux Modules Push Beyond 10 W

Above-10-W packages are advancing at a 3.98% CAGR to 2031, outpacing lower-power classes that currently dominate the Europe high-power LED package market. The 1 W-3 W bracket, which held a 47.13% share in 2025, remains popular for general lighting retrofits, where cost and form-factor familiarity drive purchasing. Growth, however, is flattening as most large warehouses and offices have completed LED conversions by 2025 and now enter replacement cycles. Packages in the 3 W-10 W tier support automotive daytime running lamps and streetlights, balancing lumen output against manageable heat loads.

Technology breakthroughs in GaN-on-SiC substrates and two-phase vapor chambers now keep junction temperatures below 125 °C at 200 W cm-² flux, enabling above-10-W modules to invade stadium floodlighting and port-crane luminaires. Lumileds’ LUXEON HL2X-V exemplifies this shift, pairing 12% higher efficacy with reduced thermal resistance. IEC 62471 rules that cap drive currents for blue-rich spectra impose limits on absolute efficacy, prompting suppliers to tweak phosphor blends to meet Risk Group 1 while preserving target brightness.

By Architecture: Chip-on-Board Captures Share

Single-die surface-mount devices led in 2025 with 36.84% revenue, yet chip-on-board (COB) assemblies are expanding at 4.11% CAGR and eroding that lead. Single-die packages satisfy residential downlights and linear troffers where modularity and established assembly lines favor incremental updates. Multi-die arrays widen the lumen envelope but confront rising commoditization as COB narrows the cost differential.

COB mounts bare dies directly to thermally conductive substrates, reducing optical losses by up to 15% and enabling tighter beam control. The October 2025 cross-license between Nichia and ams-OSRAM formalized industry alignment on COB as the high-flux standard. Flip-chip variants, which orient the junction toward the board to improve heat spread, are now entering premium segments such as stadium lighting and micro-LED backplanes, though higher process complexity restrains widespread adoption.

By Application: Automotive Lighting Accelerates

General illumination retained 36.88% of the Europe high-power LED package market size in 2025, reflecting decades of retrofit activity across offices, retail, and warehousing. With penetration already high, incremental gains depend on refresh cycles and niche uses like horticulture LEDs tuned for photosynthesis. Automotive lighting, however, is forecast to grow at 3.83% as EU rules phase out halogen bulbs and reward adaptive driving-beam systems. Each matrix headlamp can integrate hundreds of individually addressable emitters, multiplying package counts and elevating average selling prices.

AEC-Q102-qualified devices must withstand –40 °C to 150 °C cycles while preserving color stability over 15,000 hours. European automakers such as Volkswagen and Stellantis deploy micro-LED rear lamps and daytime running modules that integrate driver electronics, enabling sleeker styling and lower harness weight. Display backlighting applications continue their migration toward mini-LED and micro-LED arrays, as Samsung’s December 2025 Micro RGB TV series demonstrates.

Geography Analysis

Germany held 27.93% of regional revenue in 2025 on the back of robust automotive demand and aggressive high-bay retrofits BMWI.DE. Volkswagen, BMW, and Mercedes-Benz integrate matrix LED headlamps across mid-tier models, sourcing AEC-Q102-qualified packages from ams-OSRAM and Lumileds. Industrial corridors near Stuttgart and Munich now require high-efficacy packages to meet EN 12464-1 standards, favoring suppliers that offer tight color binning and 50,000-hour lumen maintenance.

France is projected to post the fastest CAGR at 3.88% to 2031. Stellantis brands Peugeot and Citroën adopt COB modules for weight-conscious EV lighting, while national regulators enforce stricter blue-light hazard criteria under IEC 62471. Logistics hubs near Paris and Lyon are pursuing 24-hour LED retrofits to save energy, amplifying demand for high-flux, high-efficacy packages.

The United Kingdom, navigating post-Brexit UKCA compliance, faces duplicate testing costs, prompting smaller luminaire makers to source pre-certified Asian components. Elsewhere, Italy prioritizes high-CRI museum lighting, Spain links LED streetlamps with photovoltaic microgrids, the Nordics emphasize minus-30 °C performance for outdoor assets, and Eastern Europe staggers retrofits due to energy subsidies, though EU cohesion funds accelerate municipal upgrades. Fragmented regulatory regimes and language differences underscore the need for local technical support and distribution networks.

Competitive Landscape

Five suppliers, Nichia, ams-OSRAM, Seoul Semiconductor, Lumileds, and Samsung Electronics, control about 55%-60% of regional revenues, giving the Europe high-power LED package market a moderate concentration. Rising cost pressures are sparking consolidation, as illustrated by Lumileds’ August 2025 sale to San’an Optoelectronics for USD 239 million. Patent cross-licensing, such as the Nichia-ams-OSRAM COB accord of October 2025, replaces litigation with collaboration to protect R&D budgets.

Strategic differentiation centers on phosphor chemistry, flip-chip bonding, and thermal-interface materials. Suppliers with vertical wafer integration can buffer sapphire volatility and command system-level premiums, while merchant assemblers face the brunt of price erosion. Specialty niches, horticultural lighting with red-blue spectra, UV-C disinfection modules with quartz encapsulation, maintain gross margins above 40% thanks to high regulatory and performance barriers. India’s Semiconductor Mission 2.0 funding, announced February 2026, positions new GaN-on-SiC foundries to challenge established Asian giants and intensify European price compression.

European mid-tier specialists such as BJB and Optoga focus on modular engine boards and quick-connect sockets that simplify retrofit projects for regional OEMs. These firms partner with automotive tier-1 suppliers to co-develop optical simulations and digital twins that shorten homologation cycles by up to 20%. Sustainability credentials have become a competitive lever after the EU’s July 2025 revision of the Ecodesign Regulation, which now requires suppliers to disclose reparability indices at the package level. Nichia responded in January 2026 by launching a take-back scheme for spent automotive modules, targeting 90% material recovery and closed-loop phosphor reuse. Supply-chain resilience also shapes purchasing decisions, with OEMs demanding dual sourcing of sapphire or SiC wafers to avoid the 18% spot-price swings recorded in 2025. Collective R and D under the Horizon Europe “PhotonHub” program pools resources among universities and SMEs, accelerating advances in micro-LED transfer and driver integration.

Europe High-Power LED Package Industry Leaders

Nichia Corporation

ams-OSRAM AG

Seoul Semiconductor Co., Ltd.

Lumileds Holding B.V.

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight Electronics sued Seoul Semiconductor in U.S. federal court over alleged phosphor-conversion patent infringement, highlighting escalating IP battles in an increasingly commoditized field.

- February 2026: Cree LED unveiled OptiLamp intelligent modules with embedded sensors and machine-learning controls that adapt lumen output and CCT to occupancy and daylight, promising 30% incremental energy savings for commercial retrofits.

- February 2026: India’s Ministry of Electronics and Information Technology launched Semiconductor Mission 2.0, earmarking incentives for GaN-on-SiC and InP fabs to create domestic LED capacity for export to Europe.

- December 2025: Samsung Electronics expanded its Micro RGB TV family, using COB micro-LED arrays and quantum-dot filters to push peak luminance over 2,000 nits, lifting demand for high-flux packages.

Europe High-Power LED Package Market Report Scope

The Europe High-Power LED Package Market Report is Segmented by Power Range (1 W to 3 W, 3 W to 10 W, Above 10 W), Architecture (Single-die Packages, Multi-die Packages, COB, Others), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty), and Geography (United Kingdom, Germany, France, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| 1 W – 3 W |

| 3 W – 10 W |

| Above 10 W |

| Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) |

| COB (Chip-on-Board) |

| Others (CSP, Flip-chip, Hybrid Modules) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| United Kingdom |

| Germany |

| France |

| Rest of Europe |

| By Power Range | 1 W – 3 W |

| 3 W – 10 W | |

| Above 10 W | |

| By Architecture | Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) | |

| COB (Chip-on-Board) | |

| Others (CSP, Flip-chip, Hybrid Modules) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche | |

| By Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe |

Key Questions Answered in the Report

What value is Europe’s high-power LED package market projected to reach by 2031?

The market is forecast to reach USD 0.88 billion by 2031.

Which application segment is expected to grow the fastest through 2031?

Automotive lighting leads growth with a 3.83% CAGR to 2031.

How quickly will above-10-W packages expand in the region?

Above-10-W modules are projected to grow at a 3.98% CAGR between 2026 and 2031.

Which European country shows the highest growth outlook?

France posts the fastest trajectory with a 3.88% CAGR to 2031.

Who are the leading suppliers and what share do they hold?

Nichia, ams-OSRAM, Seoul Semiconductor, Lumileds, and Samsung Electronics collectively command about 55%-60% of regional revenue.

Which standard governs photobiological safety for LED packages sold in Europe?

IEC 62471 specifies the photobiological safety limits that LED packages must meet.

Page last updated on: