China High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

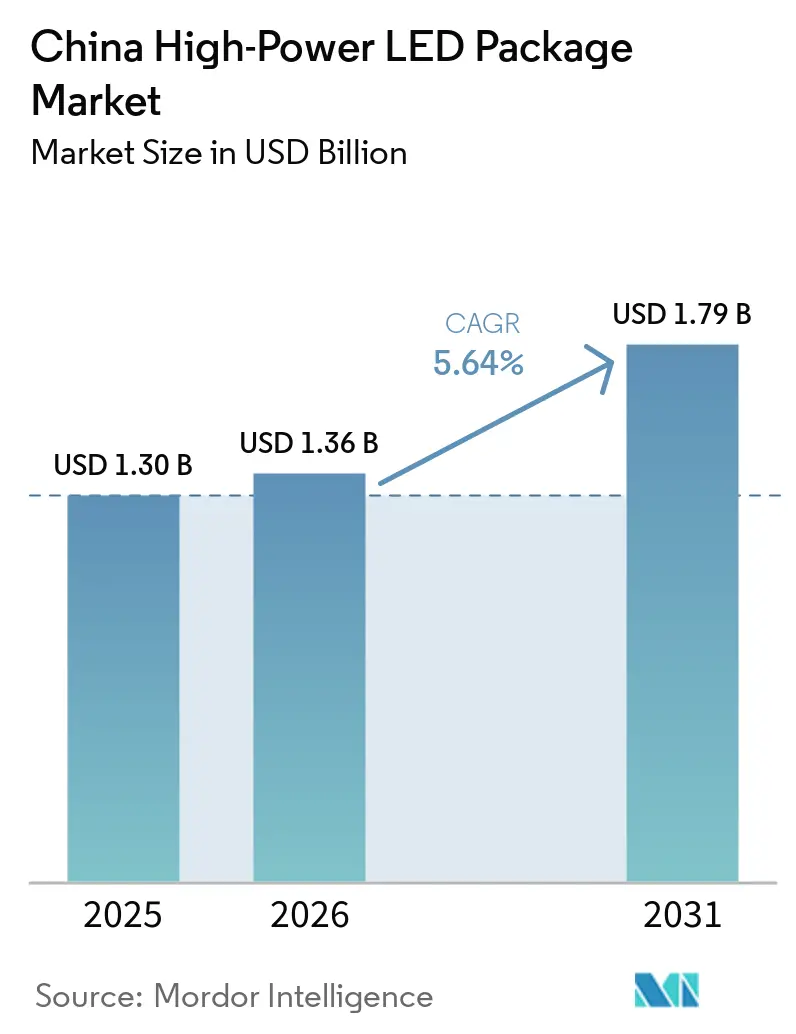

| Base Year Market Size (2025) | USD 1.30 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

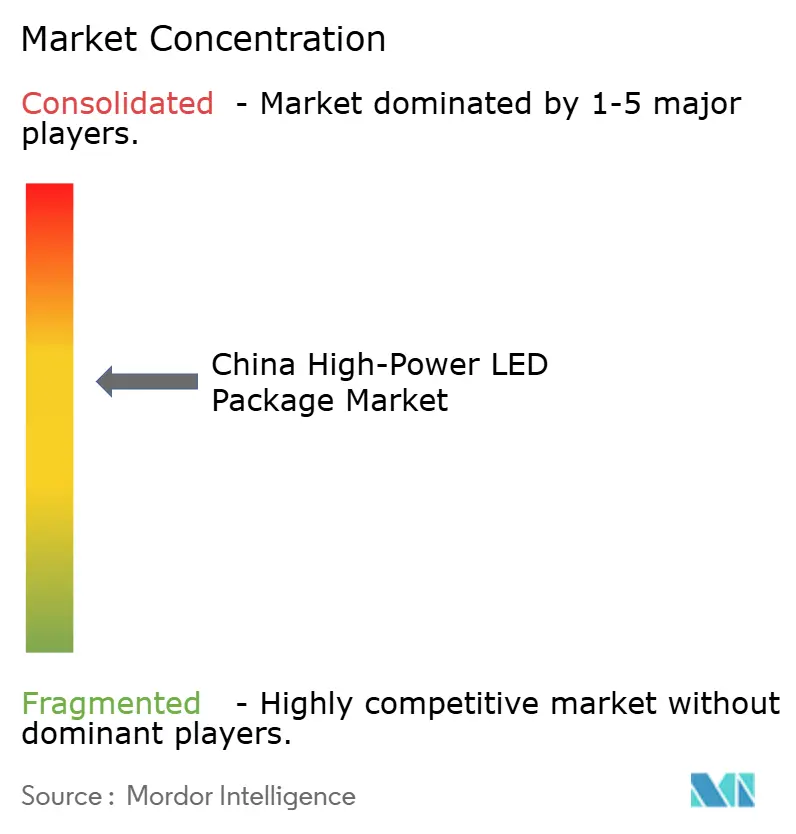

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China High-Power LED Package Market Analysis by Mordor Intelligence

The China high-power LED package market size is projected to expand from USD 1.30 billion in 2025 and USD 1.36 billion in 2026 to USD 1.79 billion by 2031, registering a CAGR of 5.64% between 2026-2031. A structural pivot away from commodity general lighting toward automotive matrix headlamps, Mini and Micro-LED backlights, and specialty UV-C modules is reshaping revenue mix and lifting average selling prices. Raw-material volatility, especially the 70% jump in gold, the 148% surge in silver, and the 36% rise in copper during 2025-2026, drove roughly 60 domestic packagers to raise prices 3-25%, interrupting a three-year stretch of 30-40% price erosion. At the same time, the central government’s RMB 500 billion equipment-upgrade stimulus that began in 2025 is accelerating smart-factory retrofits and public-lighting replacements, rewarding high-efficacy packages that comply with GB/T 31832-2025 for road lighting and GB/T 50034-2024 for building lighting. Competition is therefore realigning around technology capability rather than volume, with domestic suppliers moving into flip-chip bonding, copper-copper interconnects, and ceramic substrates to win automotive and display contracts.

Key Report Takeaways

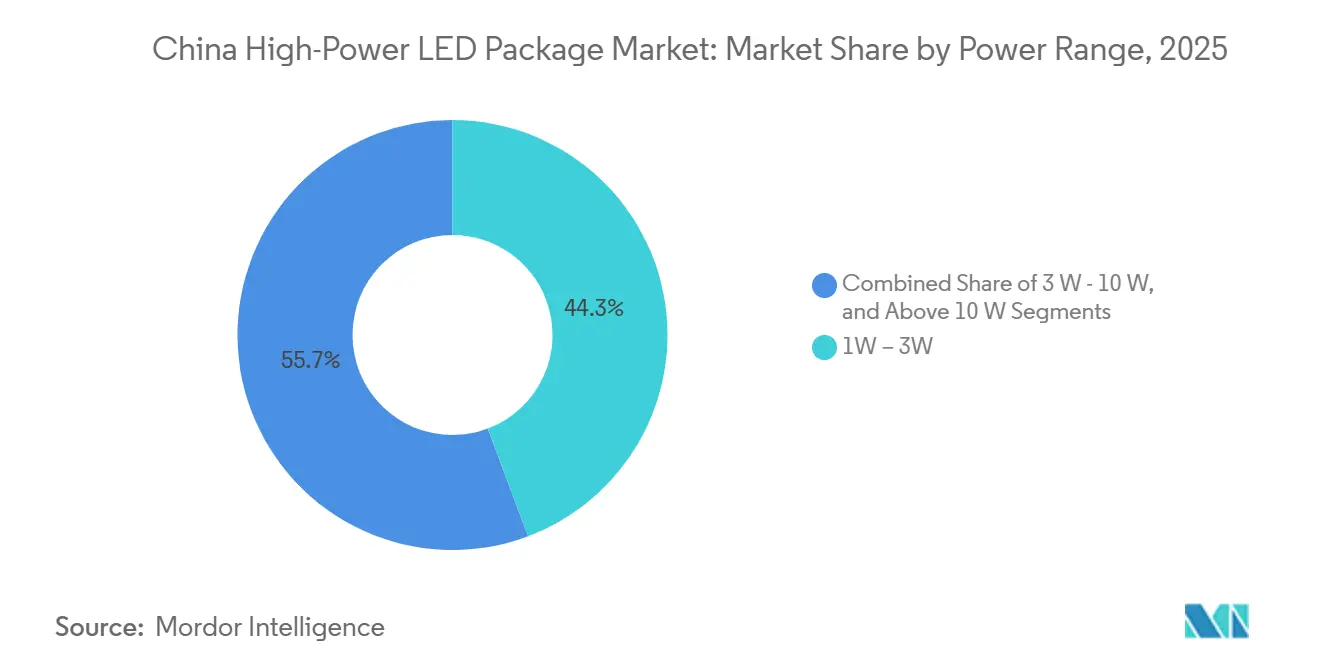

- By power range, the 1 W-3 W tier led with 44.27% of China high-power LED package market share in 2025. The Above 10 W tier is forecast to post the fastest growth at a 5.91% CAGR through 2031.

- By architecture, single-die packages accounted for 35.62% share of the China high-power LED package market size in 2025. Chip-on-board solutions are projected to advance at a 6.06% CAGR to 2031.

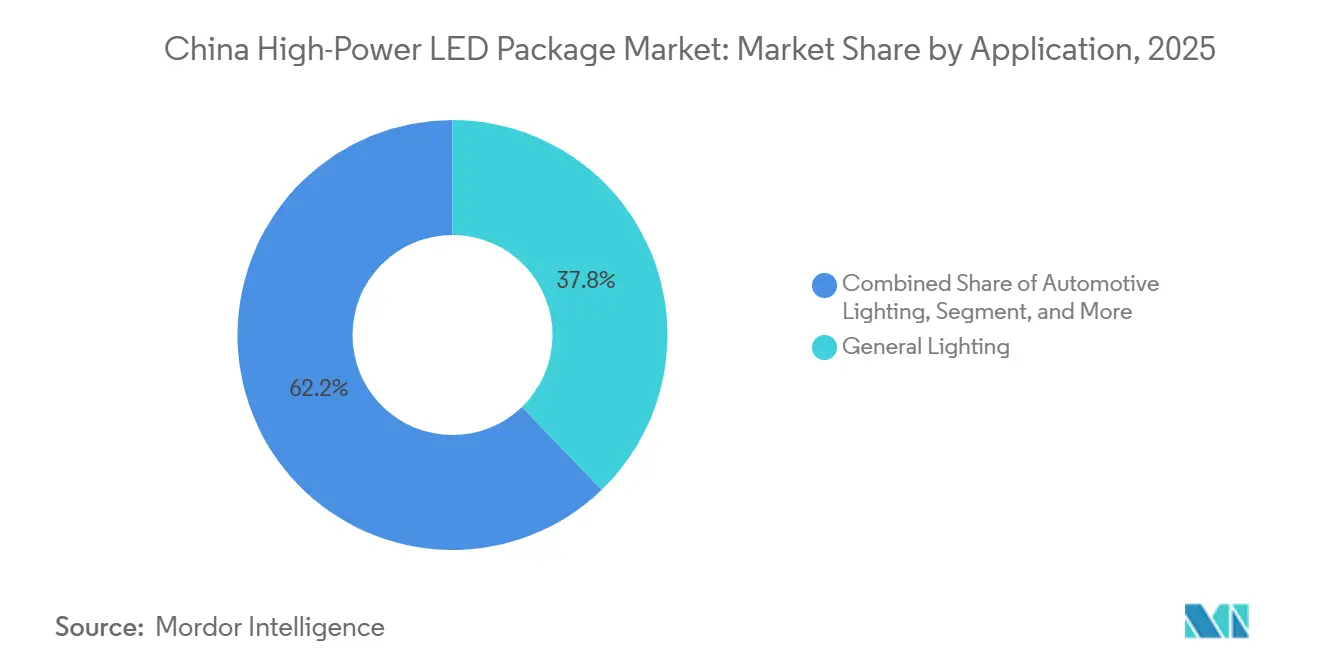

- By application, general lighting held 37.79% of 2025 revenue, while automotive lighting is poised for a 6.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China High-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Mini and Micro-LED adoption demanding higher drive currents | +1.5% | National, spillover to Asia-Pacific display hubs | Medium term (2–4 years) |

| Growth of adaptive matrix headlamps in New Energy Vehicles | +1.2% | Guangdong, Jiangsu, Shanghai NEV clusters | Short term (≤ 2 years) |

| LED subsidy roll-offs steering suppliers toward high-efficiency packages | +0.9% | All provinces | Medium term (2–4 years) |

| ERP standards tightening for public-lighting installations | +0.7% | Tier-1 cities such as Beijing, Shanghai, Shenzhen | Short term (≤ 2 years) |

| Smart-factory retrofits requiring high-lux illumination | +0.5% | Guangdong, Zhejiang, Jiangsu manufacturing belts | Medium term (2–4 years) |

| Surge in UV-C disinfection modules in semiconductor fabs | +0.4% | Jiangsu, Shanghai, Beijing semiconductor zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Mini and Micro-LED Adoption Demanding Higher Drive Currents

Mini and Micro-LED backlights now ship in premium televisions, tablets, and automotive instrument clusters, increasing per-unit LED counts ten-fold compared with edge-lit designs. Bonding tens of millions of sub-100-micrometer chips per panel pushes local heat flux above 20 W cm⁻², so packagers are redesigning thermal interfaces and spreading layers to handle die currents that exceed 1 A in automotive projection modules. Domestic suppliers have installed automated mass-transfer tools and copper-core boards to cut defect density, yet wafer-to-wafer emission-wavelength uniformity remains a hurdle for seamless tiling in ultra-high-definition displays.[1]BOE Technology Group, “Mini LED Capacity Expansion Announcement,” boe.com

Growth of Adaptive Matrix Headlamps in New Energy Vehicles

China sold 12.87 million New Energy Vehicles in 2024, lifting NEV penetration to 40.9% of passenger-car sales. Each mid-range sedan already carries at least 100 controllable pixels per headlamp, and flagship models integrate more than 25,000, driving demand for chip-on-board or single-chip pixelated LEDs qualified to AEC-Q101. Vertical integration moves, such as the Sanan-Lumileds deal, trimmed chip cost nearly 30% and opened European luxury OEM supply chains to Chinese die.

LED Subsidy Roll-Offs Steering Suppliers Toward High-Efficiency Packages

Central and provincial lighting subsidies that once propped up low-efficacy products ended in 2025, shifting procurement toward packages exceeding 130 lm W⁻¹. Municipal tenders in Beijing, Shanghai, and Shenzhen now require whole-luminaire efficacy of 150 lm W⁻¹, forcing adoption of low-thermal-resistance copper-core substrates, high-CRI phosphors, and 95%-efficient drivers. Suppliers lacking ISO 17025-accredited optical and thermal labs exited or consolidated as margin migrated to higher-performance designs.[2]Ministry of Housing and Urban-Rural Development, “Implementation Rules for Public Lighting Standards,” mohurd.gov.cn

ERP Standards Tightening for Public-Lighting Installations

GB/T 31832-2025 and GB/T 50034-2024 mandate fixture-level efficacy and glare limits that effectively ban legacy high-pressure sodium and metal-halide lamps in new public projects starting January 2026. To comply, chip-level efficacy must exceed 180 lm W⁻¹ and junction-to-case thermal resistance must fall below 1.0 K W⁻¹. Domestic COB packages on copper-core boards are meeting the target, but they raise bill-of-materials cost by 10-15% due to premium phosphor and power-factor-correction components.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price compression from over-capacity in Guangdong and Jiangxi | -0.8% | Shenzhen, Foshan, Zhongshan, Nanchang, Ganzhou | Short term (≤ 2 years) |

| Thermal-management limits above 10 W in compact form factors | -0.6% | National automotive and display clusters | Medium term (2–4 years) |

| High import dependence for flip-chip gold-bump equipment | -0.4% | Nationwide | Long term (≥ 4 years) |

| PFAS regulation increasing encapsulation costs | -0.3% | Nationwide, export-oriented suppliers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Price Compression From Over-Capacity in Guangdong and Jiangxi

Large-scale capacity expansions between 2022-2024 created a supply glut that cut average selling prices 30-40%. Although precious-metal cost inflation triggered a brief price rebound in 2025-2026, margin recovery remains fragile as buyers in commodity lighting easily defer purchases or down-spec drive currents. Asset sales and mergers, such as a recent stake purchase in Purui Optoelectronics, illustrate ongoing rationalization.[3]Ministry of Finance, “Provincial Capacity Utilization Report,” cs.mof.gov.cn

Thermal-Management Limits Above 10 W in Compact Form Factors

Packages dissipating more than 10 W inside footprints under 10 mm² risk exceeding the 125 °C junction-temperature ceiling that voids automotive qualification. Ceramic or copper slugs can lower thermal resistance to 0.8 K W⁻¹, yet they add USD 2-5 per unit and extend process cycle time. Until packagers close material-cost gaps or integrate active cooling, lumen density in space-constrained headlamps and industrial fixtures will plateau.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Higher Currents Redraw Market Boundaries

The China high-power LED package market size for the 1 W-3 W tier remained the largest in 2025, buoyed by retrofit downlights and streetlighting. However, improved chip efficacy lets luminaire makers replace several low-watt packages with a single Above 10 W emitter, cutting driver count and assembly labor. Packages at or above 10 W already command the fastest growth, underpinned by adaptive driving-beam modules and industrial high-bay fixtures that operate above 1 A. Ceramic substrates delivering sub-1 K W⁻¹ thermal resistance and gold-tin die attach are becoming standard, even though they raise unit cost, because they enable long-term lumen maintenance at currents that were once impractical.

Thermal innovations are also disrupting the mid-range. Copper-core metal-core boards lower thermal resistance to roughly 1.3 K W⁻¹ at one-third the cost of aluminum-nitride ceramics, but solder-joint fatigue emerges above 12 W during the -40 °C to 125 °C automotive test cycle. The 1 W-3 W tier therefore faces gradual share erosion as designers opt for fewer high-current nodes once thermal hurdles are cleared. The trend amplifies vertical-integration advantages enjoyed by large Chinese packagers that control substrate pressing, phosphor compounding, and driver electronics in-house.

By Architecture: COB Gains Momentum as Optics and Thermal Demands Converge

Single-die packages dominated cost-sensitive general lighting in 2025, yet chip-on-board modules posted the quickest expansion and are on track for a 6.06% CAGR through 2031. COB eliminates bond wires and shortens thermal paths, enabling pixel-dense arrays such as the 25,000-element automotive projector deployed in recent luxury sedans. Because die sit within a 10 mm circle, secondary optics simplify, lens count falls, and optical efficiency improves. Domestic packagers with ISO 17025-certified labs validate AEC-Q101 requirements faster and therefore monetize automotive qualification premiums sooner than smaller rivals.

Chip-scale packages and flip-chip constructions sit at the frontier. By removing lead frames and plastic molds, they reduce package height under 0.5 mm and improve vibration tolerance, critical for NEV tail lamps and interior accent lighting. Equipment availability remains a brake on adoption: bonders capable of sub-10-µm bump pitch are still imported, exposing suppliers to export-control risks and longer delivery cycles. Nevertheless, the architecture mix will continue to tilt toward COB and CSP as Mini and Micro-LED backlights gain traction.

By Application: Automotive Lighting Jumps Ahead of Mature General Illumination

General lighting produced 37.79% of 2025 revenue, but its share will retreat as price erosion persists and subsidy support disappears. Automotive lighting, in contrast, is set to grow at 6.11% CAGR through 2031 on the back of NEV volume and the proliferation of adaptive matrix headlamps. Each new NEV platform mandates pixels capable of microsecond modulation, thermal resistance under 1.0 K W⁻¹, and color-temperature stability across -40 °C to 125 °C. That technical bar creates switching costs that shield margins and reward suppliers equipped for flip-chip bonding, ceramic substrates, and inline optical calibration.

Display backlighting is another growth vector. Direct-lit Mini-LED televisions and high-resolution tablets raise LED counts roughly fifty-fold relative to legacy edge-lit models. Leading panel makers commissioned multiple Gen-8.6 lines in 2025 to address demand, and smart-factory subsidies shaved payback periods for automated mass-transfer tools. Specialty uses, including UV-C disinfection and horticulture lighting, remain niche but lucrative, thanks to mercury-free mandates and controlled-environment agriculture growth in North-China winter greenhouses.

Geography Analysis

Eastern coastal provinces dominate production value. Guangdong alone hosts more than one-third of national LED capacity, with Shenzhen, Foshan, and Zhongshan specializing in commodity packages, while Guangzhou leverages proximity to automakers for AEC-Q-grade production. Jiangsu and Shanghai have shifted capacity toward automotive light engines and Mini-LED backlights, attracted by nearby New Energy Vehicle clusters and display fabs. Zhejiang, historically focused on small-pitch display modules, is upgrading to copper-core boards and flip-chip bonding to capture spill-over Mini-LED orders.

Northern hubs are emerging. Beijing’s semiconductor corridor, anchored by foundries and wafer-level optics labs, spurs demand for UV-C packages used in 130-nanometer cleanroom disinfection, a segment forecast to post high-single-digit growth as fabs incorporate mercury-free sterilization. Tianjin and Hebei, beneficiaries of Jing-Jin-Ji integration, are trialing smart-tunnel lighting that specifies 150 lm W⁻¹ luminaires and low harmonic distortion, creating a regional pull for high-efficacy 3 W-10 W packages.

Inland expansion continues as western provinces seek manufacturing diversification. Chengdu and Chongqing offer tax incentives and lower labor costs, attracting second-tier packagers migrating from the coastal belt. However, supply-chain depth for ceramic substrates and high-power drivers remains shallow inland, so most Above 10 W modules are still assembled in coastal cities where raw-material logistics and reliability testing infrastructure are mature. Long haul rail and highway upgrades under the “Eight Vertical and Eight Horizontal” network are expected to narrow this gap after 2027.

Competitive Landscape

The top five domestic vendors hold roughly 40-45% combined share, giving the China high-power LED package market a moderate concentration score of 6. Industry structure is shifting from pure scale to technology segmentation. Sanan’s integration of Lumileds fused China’s largest epitaxial wafer capacity with long-established AEC-Q qualifications, lowering die cost by about 30% and unlocking European luxury OEM headlamp programs. Nationstar and Hongli accelerated investments in copper-core COB lines to supply Mini-LED backlights, while MLS consolidated overlapping commodity-lighting product families through a minority stake in Purui.

Foreign players defend high-resolution automotive and sensor-fused lighting niches. ams OSRAM’s second-generation pixelated LED embeds more than 25,600 addressable elements on a single chip, adding direct time-of-flight sensing for Level-4 autonomous perception. Nichia’s DominoPLS family delivers 15-20% lower power draw at equivalent lumen output, a decisive attribute for extending battery-electric vehicle range. Seoul Semiconductor leverages its WICOP chip-scale package to win Tesla tail-lamp sockets after a global brand exited the chip business.

Strategic themes center on vertical integration, precious-metal procurement, and equipment localization. Domestic toolmaker AMEC supplies most new MOCVD reactors, yet bump-bonding and gold evaporation systems are still imported. The Ministry of Industry and Information Technology’s PFAS-reduction roadmap further complicates supply chains, pushing encapsulant suppliers to shift from fluorinated resins to silicone chemistries even though the change raises material cost and cures more slowly.

China High-Power LED Package Industry Leaders

Sanan Optoelectronics Co., Ltd.

Nationstar Optoelectronics Co., Ltd.

MLS Co., Ltd.

Hongli Zhihui Group Co., Ltd.

Refond Optoelectronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nichia showcased its upcoming micro Pixel Light Source and laser headlamp technologies at the Automotive Lighting Expo in Kunshan, highlighting higher-resolution front lighting and road projection features.

- March 2026: Osram Opto Semiconductors released new 1-4 chip versions of the Oslon Compact PL family that use ceramic components with electrically insulated pads, enabling 395 lm at 1 A in a 1.9 mm × 1.5 mm × 0.73 mm footprint.

- February 2026: TCL Huaxing acquired an 80% stake in Zhaoyuan Optoelectronics for RMB 490 million (USD 68 million) to integrate Mini and Micro-LED packaging with its Gen-8.6 panel lines.

- January 2026: ALLOS Semiconductors partnered with Ennostar to produce 200 mm GaN-on-Si epiwafers engineered for Micro-LED uniformity, laying groundwork for future 300 mm production.

China High-Power LED Package Market Report Scope

The China High-Power LED Package Market is witnessing significant growth, driven by advancements in LED technology, increasing demand for energy-efficient lighting solutions, and the expanding applications of high-power LEDs across various industries. The market is characterized by innovation and competition among key players, all aiming to cater to the diverse needs of end users.

The China High-Power LED Package Market Report is Segmented by Power Range (1W-3W, 3W-10W, Above 10W), Architecture (Single-die Packages, Multi-die Packages, COB, Others), Application (General Lighting, Automotive Lighting, Display and Backlighting, Specialty/Niche), and Geography (China). The Market Forecasts are Provided in Terms of Value (USD).

| 1 W - 3 W |

| 3 W - 10 W |

| Above 10 W |

| Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) |

| COB (Chip-on-Board) |

| Others (CSP, Flip-chip, Hybrid Modules) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| By Power Range | 1 W - 3 W |

| 3 W - 10 W | |

| Above 10 W | |

| By Architecture | Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) | |

| COB (Chip-on-Board) | |

| Others (CSP, Flip-chip, Hybrid Modules) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche |

Key Questions Answered in the Report

How large is the China high-power LED package market today?

It is valued at USD 1.36 billion in 2026 and is projected to reach USD 1.79 billion by 2031 at a 5.64% CAGR.

Which application area is growing the fastest?

Automotive lighting is expected to advance at a 6.11% CAGR through 2031 as adaptive matrix headlamps become standard on New Energy Vehicles.

Why are Above 10 W packages gaining share?

Higher chip efficacy lets designers replace several low-watt emitters with one high-current device, cutting driver count and meeting rising brightness specs in headlamps and industrial fixtures.

What makes chip-on-board architecture attractive now?

COB removes wire bonds, lowers thermal resistance by 30-50%, and simplifies optics, which is critical for pixel-dense headlamps and Mini-LED backlights.

How are government policies influencing demand?

The RMB 500 billion equipment-upgrade stimulus and new GB/T lighting standards reward packages that deliver ≥130 lm W⁻¹, steering procurement toward high-efficiency high-power LEDs.

Which raw materials most affect package cost?

Gold, silver, and copper drive cost volatility, with prices rising 70%, 148%, and 36% respectively in 2025-2026, prompting suppliers to adjust prices or redesign interconnects.

Page last updated on: