Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

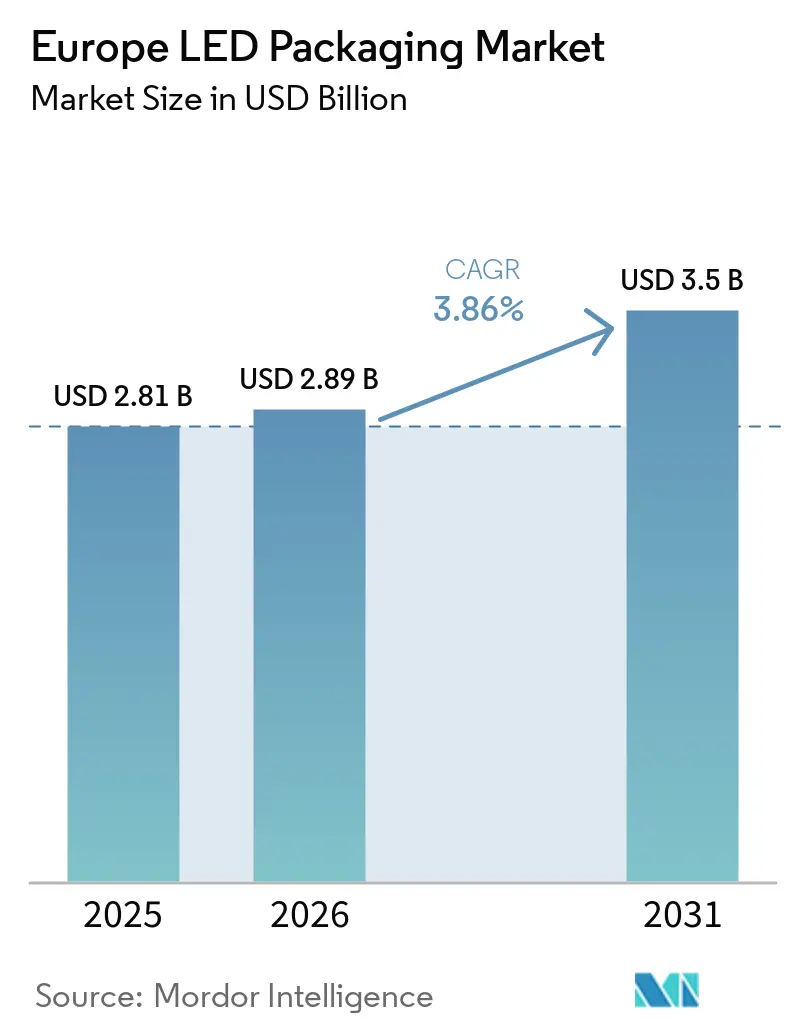

| Base Year Market Size (2025) | USD 2.81 Billion |

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 3.5 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

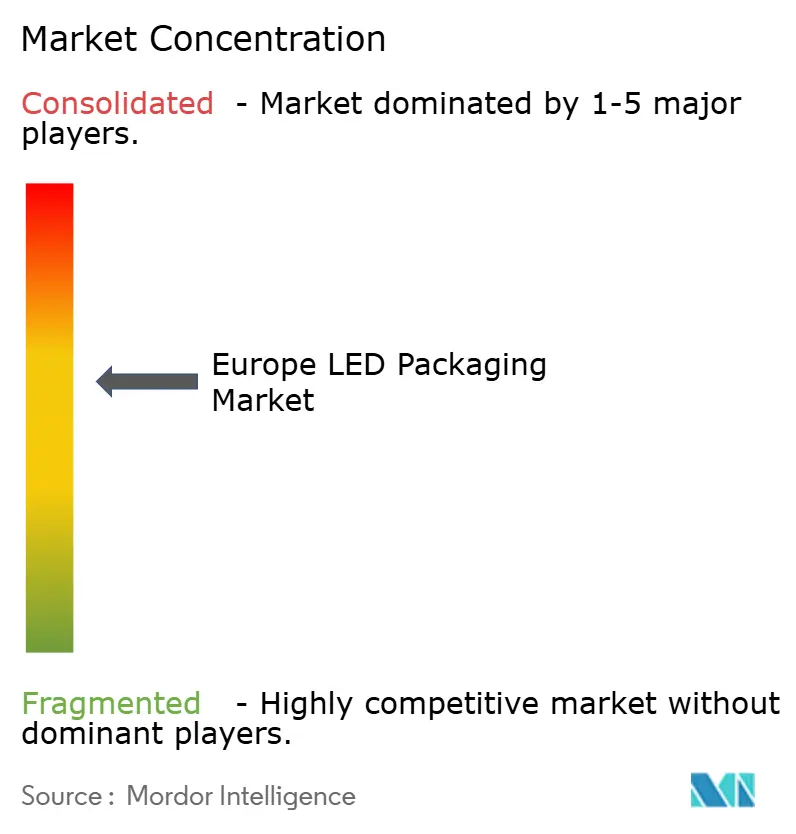

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe LED Packaging Market Analysis by Mordor Intelligence

The Europe LED packaging market size is projected to expand from USD 2.81 billion in 2025 and USD 2.89 billion in 2026 to USD 3.50 billion by 2031, registering a CAGR of 3.86% between 2026 and 2031. Demand momentum stems from automotive pixel-LED headlamps, accelerated phase-outs of halogen and fluorescent fixtures under European Union Ecodesign rules, and rapid adoption of mini-LED backlight televisions. Automotive original equipment manufacturers are embedding sub-100 µm flip-chip arrays that enable adaptive high-beam systems, while municipalities in Germany and France are replacing 320,000 streetlight heads with chip-on-board (COB) modules that cut energy use by 60%. A parallel transition is occurring inside European television plants, where direct-lit mini-LED backlighting now delivers more than 1,000 dimming zones at 30% lower cost per zone, driving stepped-up orders for compact chip-scale packages (CSP). These structural pivots provide head-room for premium-priced, thermally efficient architectures even though headline revenue growth appears modest.

Key Report Takeaways

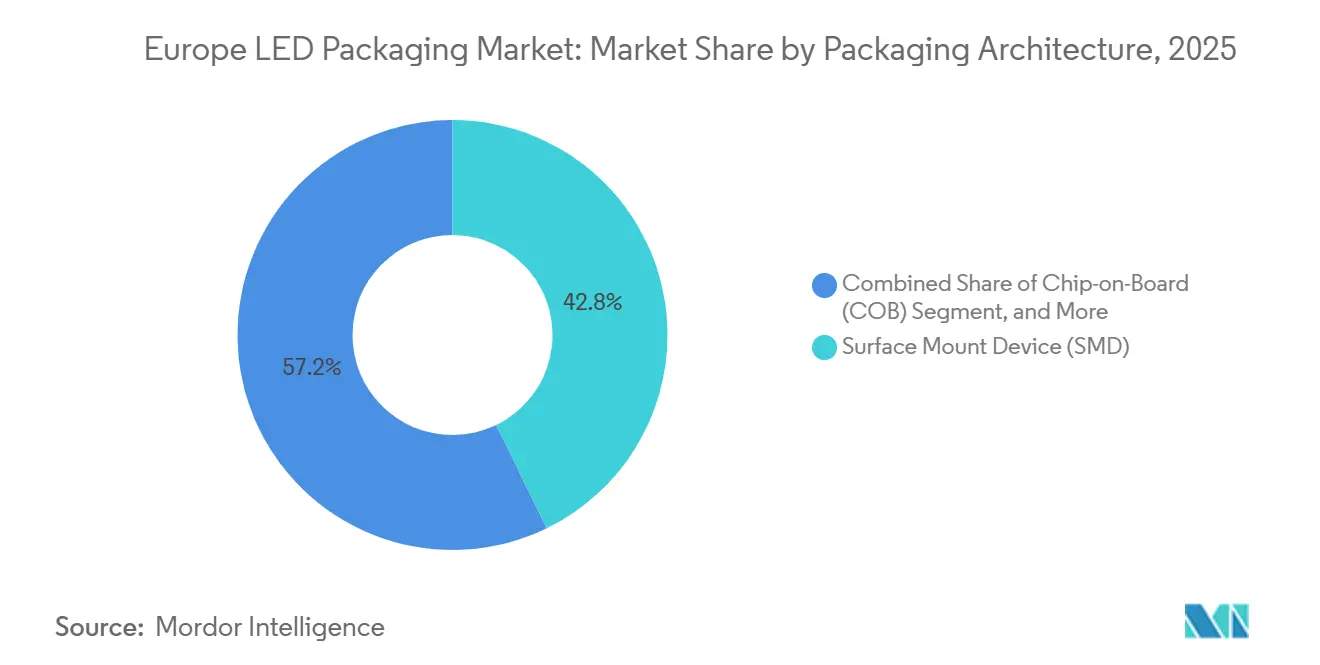

- By packaging architecture, surface-mount devices held 42.78% revenue share in 2025, while chip-scale packages are advancing at a 4.51% CAGR through 2031.

- By power class, mid-power packages captured 39.61% of the Europe LED packaging market share in 2025, whereas high-power variants are set to grow at 4.23% through 2031.

- By emission type, visible-spectrum LEDs accounted for 85.73% of the 2025 value, and ultraviolet packages are forecast to post a 4.19% CAGR to 2031.

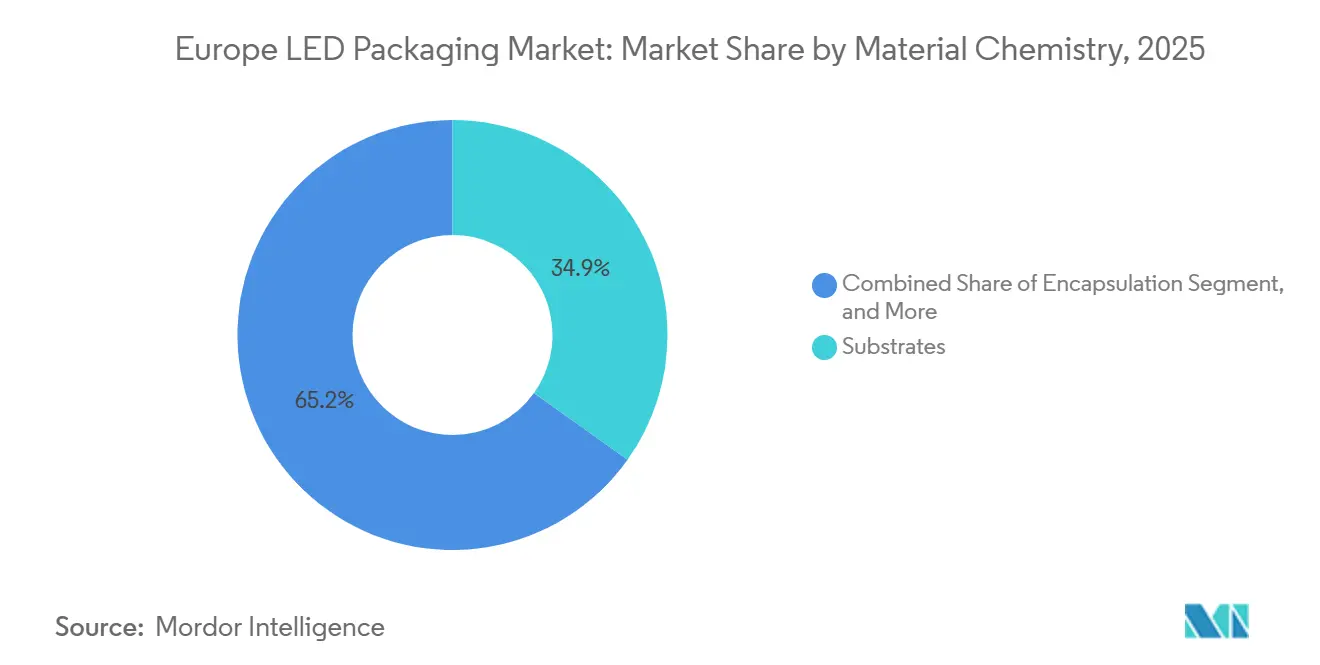

- By material chemistry, substrates represented 34.85% of the 2025 value, yet phosphor and coating formulations will rise at a 4.44% pace through 2031.

- By application, general lighting accounted for 41.48% of the 2025 value, and automotive lighting will rise at a 4.73% rate through 2031.

- By geography, Germany led with 26.37% revenue share in 2025, and France is projected to log the fastest CAGR of 4.65% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe LED Packaging Market Trends and Insights

Surging Mini-LED Backlight Adoption In European TV And Monitor Production

Television brands introduced more than twenty mini-LED models at CES 2026, with European assembly plants in Poland and the Czech Republic ramping module lines that consume CSPs able to endure 260 °C reflow temperatures. Localized dimming zones exceed 1,000 per panel, broadening HDR1400-certified displays and compressing bill-of-materials cost by 30%. These pull-through dynamics elevate unit orders for flip-chip and CSP architectures tailored to direct-lit backlighting.

EU Ecodesign Regulations Phasing-Out Conventional Lighting

The Ecodesign Directive removed T8 fluorescents in 2023 and halogen capsules by September 2025, triggering accelerated retrofit programs such as Berlin’s 220,000-fixture swap-out.[1]European Commission. "EU Ecodesign Directive - Lighting Phase-out Timeline," ec.europa.eu Minimum efficacy thresholds of 120 lm/W disqualify legacy technologies, forcing municipal buyers toward high-power LED modules that comply with RoHS lead-free mandates.

Automotive OEM Shift Toward Pixel-LED Headlamps

Audi, Mercedes-Benz, and BMW have released 2026 model-year vehicles fitted with 25,600-pixel EVIYOS HD25 modules that raise semiconductor content per car by EUR 150 (USD 169). New ECE R48 adaptive-beam regulations permit continuous high-beam operation provided glare zones are masked, cementing demand for sub-100 µm flip-chip packages on ceramic substrates with <5 K/W thermal resistance.

Declining Cost Curve Of Flip-Chip CSP Technology

Wafer-level packaging yields have surpassed 95% and die-attach has migrated to eutectic alloys that lower thermal impedance by 20%. The elimination of wire bonds shrinks footprint 50%, enabling fixture makers to raise lumen density while approaching cost parity with mid-power SMD packages by 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for Advanced Packaging Lines Below 10 µm Pitch | -0.6% | Germany, Austria, France | Medium term (2-4 years) |

| Supply-Chain Exposure to Asian Substrate Vendors | -0.5% | Europe-wide, concentrated in automotive and display | Short term (≤ 2 years) |

| Thermal-Management Limits in Ultra-High Power Packages | -0.3% | Germany, United Kingdom, industrial segments | Long term (≥ 4 years) |

| Competition from Emerging Micro-OLED Displays | -0.2% | France, Germany, premium display segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX For Advanced Packaging Lines Below 10 µm Pitch

A sub-10 µm bump-pitch line requires lithography steppers and mass-transfer tools that together exceed EUR 100 million (USD 113 million), stretching payback beyond five years and consolidating production among a few vertically integrated incumbents.

Supply-Chain Exposure To Asian Substrate Vendors

Europe currently imports more than 70% of its sapphire and silicon-carbide LED substrates. Domestic fabs subsidized under the EU Chips Act will not open until 2028, leaving packagers vulnerable to price spikes and allocation risk during automotive model-year launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Architecture: Chip-Scale Packages Gain Traction

Chip-scale packages are growing at a 4.51% rate as automotive dashboards and consumer devices demand compact footprints and low thermal resistance. The Europe LED packaging market size for CSPs is projected to reach USD 1.11 billion by 2031, while surface-mount devices decline in relative importance as flip-chip designs deliver superior lumen-per-dollar economics. Surface-mount devices accounted for 42.78% of revenue in 2025. Fixture makers increasingly specify CSPs for linear strips where smaller footprints improve heat spreading and enable tighter bend radii. Meanwhile, chip-on-board modules remain favored in stadium floodlights and high-bay industrial luminaires that require uniform beams and simplified optics.

Flip-chip packages bridge the gap between SMD heritage and CSP miniaturization by bonding die directly to ceramic carriers, achieving pixel densities above 10,000 px/cm². Dual in-line and through-hole formats persist in legacy signage, yet their volume share keeps sliding as supply chains pivot to reflow-capable surface-mount alternatives. Component-level integration of driver and health-monitor circuits, as demonstrated by the OptiLamp series, underscores a roadmap in which package boundaries blur with system modules.

By Power Class: High-Power Packages Address Lumen-Dense Applications

High-power packages (1-3 W) are projected to grow 4.23% annually through 2031, fueled by industrial retrofits and municipality streetlighting where reducing fixture count cuts installation labor. The Europe LED packaging market share for mid-power packages stood at 39.61% in 2025, yet their CAGR trails the segment average because CSPs deliver equivalent output in smaller footprints. Ultra-high-power devices above 3 W target stadium and horticulture installations, but thermal-management constraints cap their volumes.

Copper metal-core PCBs with >380 W/mK conductivity, coupled with ceramic substrates, maintain junction temperatures below 125 °C, thereby extending lumen maintenance. Procurement teams favor high-power LEDs on a total-cost-of-ownership basis, accepting higher unit prices in exchange for fewer luminaires and quicker payback periods.

By Emission Type: Ultraviolet Packages Accelerate

Ultraviolet LEDs are slated to post a 4.19% CAGR as municipalities install UV-C disinfection arrays in water and HVAC systems to meet pathogen targets. Visible-spectrum LEDs accounted for 85.73% of the 2025 market share; visible-spectrum devices remain the workhorse of the Europe LED packaging industry, yet their unit dominance masks the outsized growth in UV-A horticultural fixtures that manipulate plant morphology and accelerate photosynthesis. Infrared packages serve surveillance and biometric modules and enjoy steady but modest growth.

Mercury-free mandates are boosting UV-LED traction despite inferior efficacy compared to low-pressure mercury lamps, compelling designers to specify larger arrays or higher drive currents. Ongoing phosphor innovations and aluminum nitride substrates are narrowing that gap, especially in 265-280 nm outputs where disinfection efficacy peaks.

By Material Chemistry: Phosphor Formulations Lift Color Quality

Phosphor and coating materials are expanding at 4.44% per year. Recent nitride-red phosphors based on Sr: Eu elevate color rendering indices above 95, allowing retail and hospitality luminaires to match halogen warmth without energy penalties. Substrates accounted for 34.85% of the 2025 market share, still one-third of the bill, and are increasingly shifting from sapphire to silicon carbide and gallium-nitride-on-silicon to improve heat dissipation. Encapsulation resins are migrating to high-Tg silicones that resist yellowing at drive currents above 700 mA.

Innovations in Si4+/Eu3+ co-doped gallate germanate phosphors raised internal quantum efficiency from 37.8% to 49.0%, setting new baselines for efficacy in warm-white packages. These chemistry advances sustain premium pricing and differentiate suppliers in segments where color fidelity trumps raw flux.

By Application: Automotive Lighting Leads Growth

Automotive lighting is forecast to register a 4.73% CAGR as adaptive pixel headlamps and dynamic turn signals become standard on premium and mid-range vehicles. The Europe LED packaging market for automotive modules is expected to exceed USD 1.02 billion by 2031. General lighting still commands the largest absolute revenue share in 2025, with 41.48%, driven by Ecodesign-induced retrofits, but its growth moderates as replacement cycles taper. Display backlighting receives a boost from mini-LED televisions and instrument panels, while UV-C disinfection arrays carve out an emerging niche in healthcare facilities.

Each new vehicle fitted with pixelated headlamps contains up to 25,600 addressable emitters, boosting package volume and ASPs. Ambient-interior lighting packages that mix RGB or RGBW chips add incremental demand, shifting cabin personalization from optional to default features across multiple brands.

Geography Analysis

Germany accounted for 26.37% of Europe LED packaging revenue in 2025, buoyed by automotive OEM integration of pixel-matrix headlamps and by industrial lighting retrofits across Bavaria and Baden-Württemberg. The Europe LED packaging market share in Germany is set to edge higher as municipal projects and the EU Chips Act funnel EUR 200 million (USD 230.88 million) into domestic substrate lines that shorten lead times and reduce import exposure.[2]European Council, “EU Chips Act Funding Allocations,” consilium.europa.eu

France shows the fastest country-level growth at 4.65% between 2026 and 2031, propelled by national building codes mandating LED-only fixtures and by Paris and Lyon retrofitting streetlights with smart-enabled COB arrays. French projects emphasize dark-sky compliance, requiring lower glare and precise beam control, which favors high-power packages with secondary optics capable of cut-off angles below 15 °.

The United Kingdom and the broader Rest-of-Europe cluster, including Poland and Hungary, absorb volume demand for mid-power SMD modules assembled in regional plants that serve Western European OEMs within 48-hour delivery windows. Poland hosts Samsung and LG Innotek module lines, while Hungary specializes in general-lighting SMDs. Central- and Eastern-European factories also benefit from workforce costs 30% below Western benchmarks, reinforcing their status as on-shoring nodes inside the single market.

Competitive Landscape

The Europe LED packaging market features moderate concentration. ams-OSRAM, Lumileds, and Nichia jointly hold roughly 45-50% of regional sales. Ams-OSRAM has earmarked EUR 588 million (USD 663 million) for Austrian capacity expansion, partly underwritten by EU Chips Act grants, to insource substrate fabrication and packaging formerly sourced from Taiwan.[3]ams-OSRAM, “Investor Presentation Q4 2025,” ams-osram.com San’an Optoelectronics’ USD 239 million acquisition of Lumileds brings a Chinese owner into the European ecosystem, triggering scrutiny under export-control frameworks that govern automotive and defense contracts.

Nichia continues to enforce intellectual-property rights, extending YAG-phosphor litigation against Everlight before the Düsseldorf Higher Regional Court. Patent defense underpins price discipline in commoditizing mid-power segments. Korean and Taiwanese players Samsung, LG Innotek, Seoul Semiconductor, Everlight supplement supply, often through Polish and Hungarian assembly hubs that benefit from customs-free access to Western Europe.

White-space prospects emerge in UV-C disinfection and horticultural UV-A markets, where efficacy hurdles leave room for differentiated phosphor systems and aluminum-nitride substrates. Smaller firms such as Vishay and Cree LED pursue specialization: Vishay targets ultra-compact 0404 RGB packages for micro-mobility dashboards, while Cree integrates driver and monitoring circuits inside each pixel, slashing external component count and easing system integration.

Europe LED Packaging Industry Leaders

-

ams-OSRAM AG

-

Lumileds Holding B.V.

-

Nichia Corporation

-

Seoul Semiconductor Co., Ltd.

-

Cree LED

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Vishay Intertechnology launched the VLMRGB1500 tricolor RGB LED in a 0404 package, 70% smaller than PLCC-4 alternatives, aimed at micro-mobility dashboards and message displays.

- February 2026: Cree LED released OptiLamp pixels with on-board driver and health monitoring, eliminating external ICs and cutting power consumption in large-format displays.

- December 2025: Samsung Electronics expanded its Micro RGB TV lineup to six screen sizes, each achieving 100% BT.2020 gamut with sub-100 µm LEDs.

- August 2025: San’an Optoelectronics completed the USD 239 million acquisition of Lumileds Holding B.V., adding a Chinese-controlled brand to the European supply base.

Europe LED Packaging Market Report Scope

The Europe LED Packaging Market is witnessing significant growth, driven by advancements in LED technology, increasing demand for energy-efficient lighting solutions, and expanding applications across various industries. The market's evolution is further supported by government initiatives promoting sustainable energy usage and the rising adoption of LEDs in automotive, consumer electronics, and industrial sectors.

The Europe LED Packaging Market Report is Segmented by Packaging Architecture (SMD, COB, CSP, Flip-Chip, DIP, Others), Power Class (Low, Mid, High, Ultra-High), Emission Type (Visible, IR, UV), Material Chemistry (Substrates, Encapsulation, Bonding, Phosphors), Application (General Lighting, Automotive, Display, Consumer Electronics, Industrial), and Geography (UK, Germany, France, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

By Packaging Architecture

| Surface Mount Device (SMD) |

| Chip-on-Board (COB) |

| Chip Scale Package (CSP) |

| Flip-Chip LED Packages |

| Dual In-line Package (DIP / Through-hole) |

| Others (IMD, GOB, Mini-LED display packaging) |

By Power Class

| Low Power (Less Than 0.5 W) |

| Mid Power (0.5 - 1 W) |

| High Power (1 - 3 W) |

| Ultra-High Power (Greater Than 3 W) |

By Emission Type

| Visible LED Packages |

| Infrared (IR) LED Packages |

| Ultraviolet (UV) LED Packages |

By Material Chemistry

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

By Application

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Consumer Electronics |

| Industrial and Specialty |

By Geography

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe |

| By Packaging Architecture | Surface Mount Device (SMD) | |

| Chip-on-Board (COB) | ||

| Chip Scale Package (CSP) | ||

| Flip-Chip LED Packages | ||

| Dual In-line Package (DIP / Through-hole) | ||

| Others (IMD, GOB, Mini-LED display packaging) | ||

| By Power Class | Low Power (Less Than 0.5 W) | |

| Mid Power (0.5 - 1 W) | ||

| High Power (1 - 3 W) | ||

| Ultra-High Power (Greater Than 3 W) | ||

| By Emission Type | Visible LED Packages | |

| Infrared (IR) LED Packages | ||

| Ultraviolet (UV) LED Packages | ||

| By Material Chemistry | Substrates | |

| Encapsulation | ||

| Bonding / Die-Attach | ||

| Phosphors / Coatings | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Consumer Electronics | ||

| Industrial and Specialty | ||

| By Geography | Europe | United Kingdom |

| Germany | ||

| France | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will the Europe LED packaging market be by 2031?

It is projected to reach USD 3.50 billion by 2031, growing at a 3.86% CAGR from 2026.

Which segment of the Europe LED packaging industry is expanding the fastest?

Chip-scale packages are advancing at a 4.51% CAGR as miniaturization and flip-chip demand accelerate.

Why are UV-LED packages gaining traction in Europe?

Municipal disinfection mandates and mercury-free regulations are lifting UV-C and UV-A adoption despite lower efficacy than mercury lamps.

Which country will post the quickest growth in LED packaging demand?

France is forecast to record a 4.65% CAGR through 2031, driven by smart-streetlight retrofits and building code mandates.

How is the EU Chips Act influencing supply chains?

Grants exceeding EUR 200 million are financing on-shore substrate and packaging plants, reducing reliance on Asian imports after 2028.

What is the key barrier to micro-LED packaging expansion?

Sub-10 µm bump-pitch lines require capital outlays above EUR 100 million, limiting participation to a few well-capitalized IDMs.

Page last updated on: