Asia-Pacific Mid-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

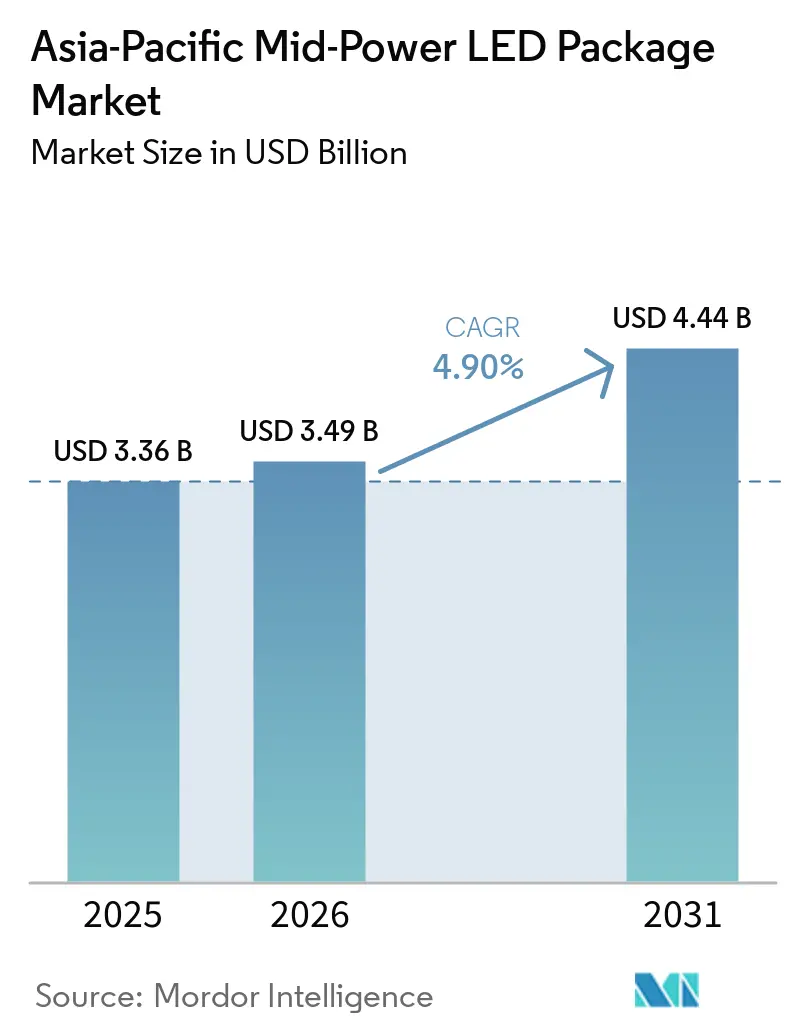

| Base Year Market Size (2025) | USD 3.36 Billion |

| Market Size (2026) | USD 3.49 Billion |

| Market Size (2031) | USD 4.44 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Mid-Power LED Package Market Analysis by Mordor Intelligence

The Asia-Pacific mid-power LED package market size is expected to grow from USD 3.36 billion in 2025 to USD 3.49 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at a 4.9% CAGR over 2026-2031. Constrained growth masks a decisive value shift from commodity lamps to precision pixels that power adaptive headlamps, mini-LED televisions, and machine-readable automotive light bars. Surface-mount formats still dominate volume, yet chip-scale designs capture design-ins where thermal resistance, pixel density, and flicker-free dimming determine qualification. Automotive makers have normalized 25,000-pixel headlamp modules, a density that vaults the Asia-Pacific mid-power LED package market into the broader vehicle sensing stack. Rare-earth supply fears, especially for yttrium phosphors, elevate China’s leverage over global pricing, while India’s production-linked incentives signal a nascent geographic rebalancing away from single-source dependencies.

Key Report Takeaways

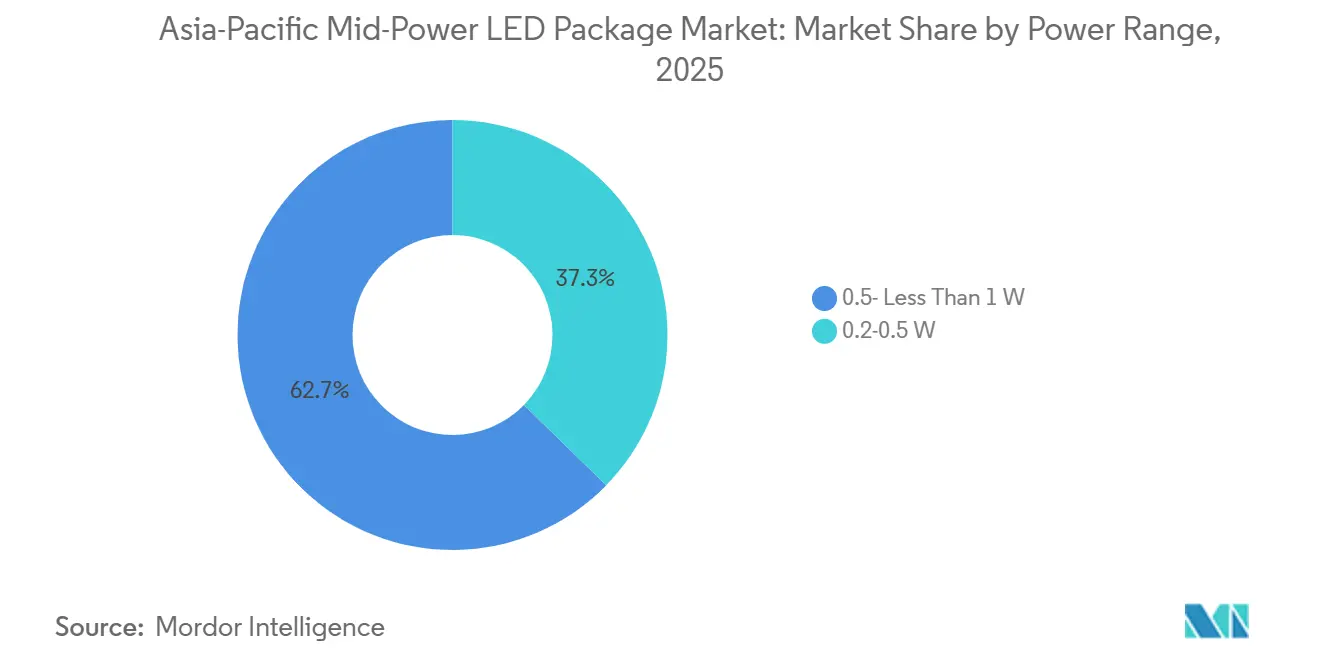

- By power range, the 0.5W- Less Than 1W segment captured 62.68% of the Asia-Pacific mid-power LED package market share in 2025, and 0.5W- Less Than 1W devices are advancing at a 5.55% CAGR through 2031.

- By package architecture, surface-mount devices held 73.38% share of the Asia-Pacific mid-power LED package market in 2025, while chip-scale packages record the highest projected CAGR at 5.38% to 2031.

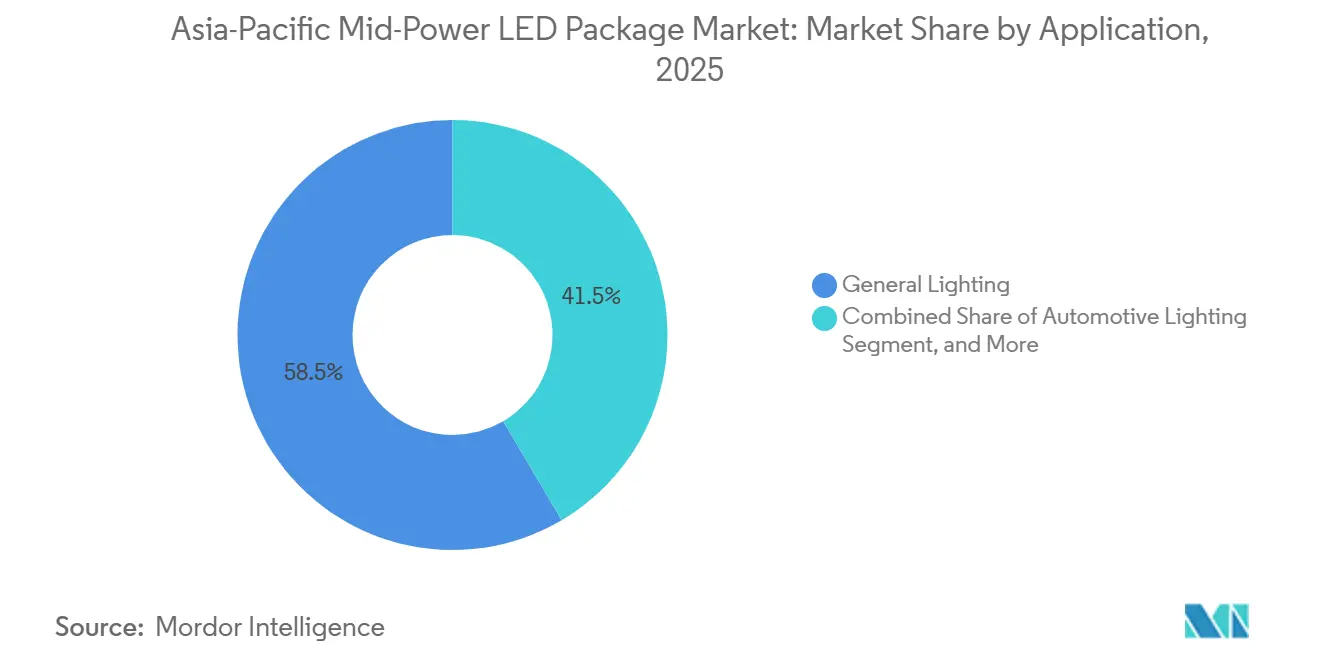

- By application, general lighting led with 58.48% revenue share in 2025; automotive lighting is forecast to expand at a 5.96% CAGR through 2031.

- By geography, China accounted for 57.33% share of the Asia-Pacific mid-power LED package market in 2025, whereas India posts the fastest regional CAGR at 5.78% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Mid-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging Demand for 2835 Mid-Power LEDs in Smart Lighting | +0.8% | China, Southeast Asia, India | Medium term (2–4 years) |

| Automotive OEM Shift Toward Adaptive Pixel Headlamps | +1.2% | Japan, China, India | Long term (≥4 years) |

| Accelerated Mini-LED Backlighting Adoption in TV Panels | +0.9% | China, Japan, South Korea | Short term (≤2 years) |

| Energy-Efficiency Mandates Across Southeast Asia | +0.7% | ASEAN member states | Medium term (2–4 years) |

| Rapid Expansion of Horticultural Lighting | +0.5% | China, Japan, Singapore | Long term (≥4 years) |

| Emerging Micro-Packaging Techniques Lower Cost per Lumen | +0.6% | Global, led by China and Taiwan | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for 2835 Mid-Power LEDs in Smart Lighting

Building owners now specify 2835 packages that integrate thermistors and deep-dimming control, eliminating visible flicker and aligning with wellness codes.[1]Lumileds, “LUXEON 2835 Commercial Deep Dimming,” lumileds.com The 2.8 mm × 3.5 mm footprint allows up to 240 LEDs per meter on flexible strips without breaching thermal limits, creating uniform luminance in retail coves and healthcare wards. Predictive maintenance algorithms tap real-time temperature data to reduce facility operating costs by up to 20%. Adoption accelerates where California Title 24, Singapore’s Green Mark, and Japan’s WELL certification require low-flicker luminaires. As a result, the Asia-Pacific mid-power LED package market increasingly treats the 2835 as a smart-node platform rather than a low-cost commodity.

Automotive OEM Shift Toward Adaptive Pixel Headlamps

Regulators endorse glare-free high beams, prompting carmakers to embrace 25,000-pixel modules that deliver dynamic beam shaping and road-surface projections.[2]CN360LED, “EVIYOS 2.0 Mass Production,” cn360led.com Only suppliers with sub-80 µm pixel pitch and the ability to dissipate 60 watts in a 5 mm × 5 mm envelope qualify, narrowing the vendor pool. Energy savings of 15-20% compared with older matrix lamps translate into extra driving range, an argument that resonates with electric-vehicle buyers across China and Japan. The Asia-Pacific mid-power LED package market thus sees automotive share rising as headlamps evolve from illumination to communication devices.

Accelerated Mini-LED Backlighting Adoption in TV Panels

Premium televisions showcased in 2026 rely on thousands of 0.2-0.3 W packages to hit 2,000 nits peak brightness and greater than 110% NTSC gamut. Panel makers have slashed the cost gap with OLED to roughly USD 100 on 65-inch sets, pressuring package vendors to differentiate by achieving transfer yields above 99.999%. Mass-transfer lines handling more than 1,000 chips per cycle now underpin just-in-time inventory models, trimming rework and elevating the Asia-Pacific mid-power LED package market into display fabs’ strategic cost calculus.

Energy-Efficiency Mandates Across Southeast Asia

Indonesia’s star label at 80 lumens-per-watt and Vietnam’s QCVN 19:2025 compel rapid halogen phase-out, yet uneven enforcement outside Singapore and Malaysia spawns gray-market trade. Suppliers juggle dual-spec lines, fully certified stock for regulated markets, and stripped-down variants for price-sensitive zones, adding complexity to demand planning. Nonetheless, regional targets for a 32% reduction in energy intensity by 2025 anchor LED adoption momentum within the Asia-Pacific mid-power LED package market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| IP Litigation Risk From Dominant Patent Holders | -0.4% | The United States, Germany, Japan | Long term (≥4 years) |

| Supply Chain Disruptions for Key Phosphor Materials | -0.6% | Europe, North America | Medium term (2–4 years) |

| Luminance Degradation Under High-Humidity Asian Climates | -0.3% | Southeast and South Asia | Medium term (2–4 years) |

| Consolidation of Display Backlight Vendors Dampening ASPs | -0.5% | China, Taiwan, South Korea | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

IP Litigation Risk from Dominant Patent Holders

Patent portfolios have become the chief competitive moat. Recent lawsuits in U.S. and German courts underscore that smaller vendors face a binary choice: accept performance trade-offs to avoid infringement, or risk injunctions that stall automotive qualification cycles lasting 3 years. The overhang forces OEMs to favor suppliers offering indemnification backed by royalty pools, thereby concentrating share within the Asia-Pacific mid-power LED package market.

Supply Chain Disruptions for Key Phosphor Materials

China’s April 2025 yttrium export controls spiked European oxide prices by 40x, exposing the reliance on phosphor-converted white LEDs. Alternative RGB or quantum-dot approaches add 20-30% cost and compromise color rendering, limiting substitution. Until Australian or recycled rare-earth streams scale post-2028, package makers must lock multi-year contracts or risk margin erosion, a major brake on the Asia-Pacific mid-power LED package market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Premium Wattages Capture Automotive and Farm Margins

Higher-wattage 0.5W- and Less Than 1W packages dominate the Asia-Pacific mid-power LED package market for vehicle headlamps and horticultural rigs. Pixel beams need 0.7-0.9 W chips to sustain 300-meter reach under −40 °C to 125 °C cycles, while vertical farms drive greater than 1,000 µmol m⁻² s⁻¹ photon flux with fewer fixtures. Gross margins hover near 30% thanks to stringent binning and AEC-Q-grade reliability. Lower 0.2-0.5 W devices still feed strip lights and mini-LED panels, yet price wars compress margins below 12%, nudging vendors toward premium wattages. The Asia-Pacific mid-power LED package market share in the high-power range thus rises despite smaller unit volumes.

Commodity segments lean on incremental efficacy gains and aggressive cost downs to stay relevant. Retail cove lights pack 0.3 W 2835s at densities of 120-160 LEDs per meter, where lumen per dollar rules procurement. Display backlights adopt similar power envelopes, but panel-maker vertical integration now dictates vendor selection, leaving independents with reduced bargaining power inside the Asia-Pacific mid-power LED package market.

By Package Architecture: CSP Wins Design-ins as SMD Holds Volume

Surface-mount devices held a 73.38% share of the Asia-Pacific mid-power LED package market in 2025, while chip-scale packages recorded the highest projected CAGR of 5.38% to 2031. Surface-mount devices remain the installed-base champion with nearly three-quarters of the Asia-Pacific mid-power LED package market share, aided by legacy pick-and-place lines and entrenched 2835 tooling. Deep-dimming SMD variants unlock hospitality retrofits by erasing flicker, while rugged 3030 formats satisfy outdoor façades where IP67 ingress ratings matter.

Chip-scale packages, however, grow faster on the back of adaptive headlamps and mini-LED backlights, where every micron of z-height matters. Eliminating leadframes cuts thermal resistance, permitting 25,000-pixel modules within automotive grille widths. Eutectic ceramic CSPs multiply vibration resilience fivefold, securing heavy-duty vehicle sockets.[3]Refond, “Second-Generation Ceramic CSP,” refond.com As car programs freeze architectures for multi-year lifecycles, CSP wins translate into durable revenue streams for the Asia-Pacific mid-power LED package market.

By Application: Automotive Lighting Outpaces Illumination

General illumination still leads revenue, but matures into a replacement market with slender margins. Automotive advances at nearly 6% CAGR as electric-vehicle OEMs embed dynamic light curtains, cabin ambiance, and pixel headlamps. Each function adds addressable LEDs, elevating bill-of-materials value per vehicle. Premium margins of 25-30% encourage vendors to prioritize AEC-Q qualification even at the cost of three-year validation shoots.

While display backlighting remains a major application, it's facing pricing pressures as OLED technologies narrow the retail price gap. Concurrently, as panel manufacturers bolster their in-house LED capabilities, external suppliers find their opportunities dwindling. In light of these shifts, numerous companies are pivoting towards specialized, high-value segments like UV-C sterilization and medical phototherapy. Though these segments may handle lower project volumes, they promise stronger margins and greater profitability.

Geography Analysis

China’s 57.33% share of the Asia-Pacific mid-power LED package market reflects cradle-to-grave integration from epitaxy to finished lamp, as well as effective control of rare-earth flows. Vertical mergers, exemplified by San’an’s 2025 Lumileds buy, pared chip costs by 30% and plugged the acquirer straight into global cross-licensing alliances. Automation rates above 60% keep labor input minimal, sustaining profitability even as average selling prices slide roughly 6% a year.

India advances at a 5.78% CAGR under production-linked incentives that lure packaging lines to Tamil Nadu and Karnataka. Imported wafers mean value capture still clusters in low-margin backend steps, yet domestic demand from government LED swap programs underwrites capacity. Indian assemblers are now targeting automotive qualification, a leap that could anchor higher-value activity in the Asia-Pacific mid-power LED package market once supply ecosystems mature.

Southeast Asia is sending out mixed signals. In Singapore and Malaysia, stringent efficacy regulations mandate compliance with import requirements, empowering suppliers to charge premium prices. While Indonesia and Vietnam have rolled out similar standards, inconsistent enforcement has allowed gray markets, often sourced from Shenzhen, to thrive. Consequently, suppliers frequently juggle dual inventories, complicating demand forecasting in the Asia-Pacific mid-power LED package market. Meanwhile, vertical farming in Singapore and medicinal cannabis greenhouses in Thailand are driving a surge in demand for high-value horticulture. Yet, despite their promise, these applications still contribute only a modest share to the overall market.

Competitive Landscape

Moderate concentration prevails. The top five firms, Nichia, Samsung LED, Lumileds, ams-OSRAM, and Seoul Semiconductor, collectively account for a significant share of the Asia-Pacific mid-power LED package market. Japanese and European incumbents shelter premium niches through expansive patent pools and 15-20% efficacy advantages, deterring newer entrants. Chinese groups counter with cost leadership; San’an’s 2025 takeover of Lumileds opened patent channels and slimmed the prices of same-spec chips by nearly one-third.[4]Semiconductor Today, “San’an Completes Lumileds Acquisition,” semiconductortoday.com

Strategic thrusts now center on integration and IP. The 2025 ams-OSRAM and Nichia cross-license renewal pooled gallium-nitride lasers and micro-LED know-how, raising barriers for firms bereft of similar portfolios. Refond and Lextar find white-space in interactive vehicle displays, where mini-LED COB backlights and animated grille lights redefine automotive signatures. Yet steep R&D costs and a three-year OEM validation funnel present serious contention for balance-sheet-strong players, locking margins above commodity illumination norms in the Asia-Pacific mid-power LED package market.

Supply rationalization narrows the ranks of TV backlight vendors, with panel makers retaining in-house LED lines to pocket spreads once earned by packagers. Cost-per-lumen curves flatten, pushing independent suppliers to chase automotive, UV-C, and horticulture segments that still reward material science innovation and zero-defect quality.

Asia-Pacific Mid-Power LED Package Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd. (Samsung LED)

Lumileds Holding B.V.

ams-OSRAM AG

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Everlight sued Lumileds and Seoul Semiconductor in Texas federal court over flip-chip electrode IP, seeking injunctions and damages.

- January 2026: CN360LED ranked automotive LED suppliers, spotlighting ams-OSRAM’s 25,600-pixel EVIYOS 2.0 now shipping in the NIO ET9 and Nichia’s DominoPLS mass production.

- October 2025: ams-OSRAM and Nichia expanded their two-decade gallium-nitride cross-license, cementing joint dominance in automotive and micro-LED technologies.

- June 2025: Seoul Semiconductor partnered with OMINSU Vietnam to embed Acrich, nPola, and SunLike technologies in “Made in Vietnam” luminaires.

Asia-Pacific Mid-Power LED Package Market Report Scope

The Asia-Pacific Mid-Power LED Package Market Report is Segmented by Power Range (0.2-0.5 W and 0.5- Less Than 1 W), Package Architecture (SMD including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (China, Japan, India, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| 0.2-0.5 W |

| 0.5- Less Than 1 W |

| SMD (Surface Mount Device) | 2835 |

| 3014 | |

| 3030 | |

| Others (3528, 3020, 5050, etc.) | |

| CSP (Chip Scale Package) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| China |

| Japan |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Power Range | 0.2-0.5 W | |

| 0.5- Less Than 1 W | ||

| By Package Architecture | SMD (Surface Mount Device) | 2835 |

| 3014 | ||

| 3030 | ||

| Others (3528, 3020, 5050, etc.) | ||

| CSP (Chip Scale Package) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the projected value of the Asia-Pacific mid-power LED package market in 2031?

The market is forecast to reach USD 4.44 billion by 2031.

Which power range leads sales in the region?

0.5W–Less Than 1W packages held 62.68% share in 2025 and continue to dominate through 2031.

Why are chip-scale packages gaining traction?

CSPs reduce thermal resistance and enable pixel densities required for adaptive headlamps and mini-LED backlights.

How does China influence regional supply chains?

China controls more than half of regional volume and the bulk of yttrium refining, giving it pricing leverage.

Which application segment is growing fastest?

Automotive lighting is advancing at a 5.96% CAGR thanks to adaptive pixel headlamps and dynamic exterior displays.

What is the main supply risk facing package makers?

Tight yttrium export controls threaten phosphor availability, raising costs for white LED production.

Page last updated on: