North America High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

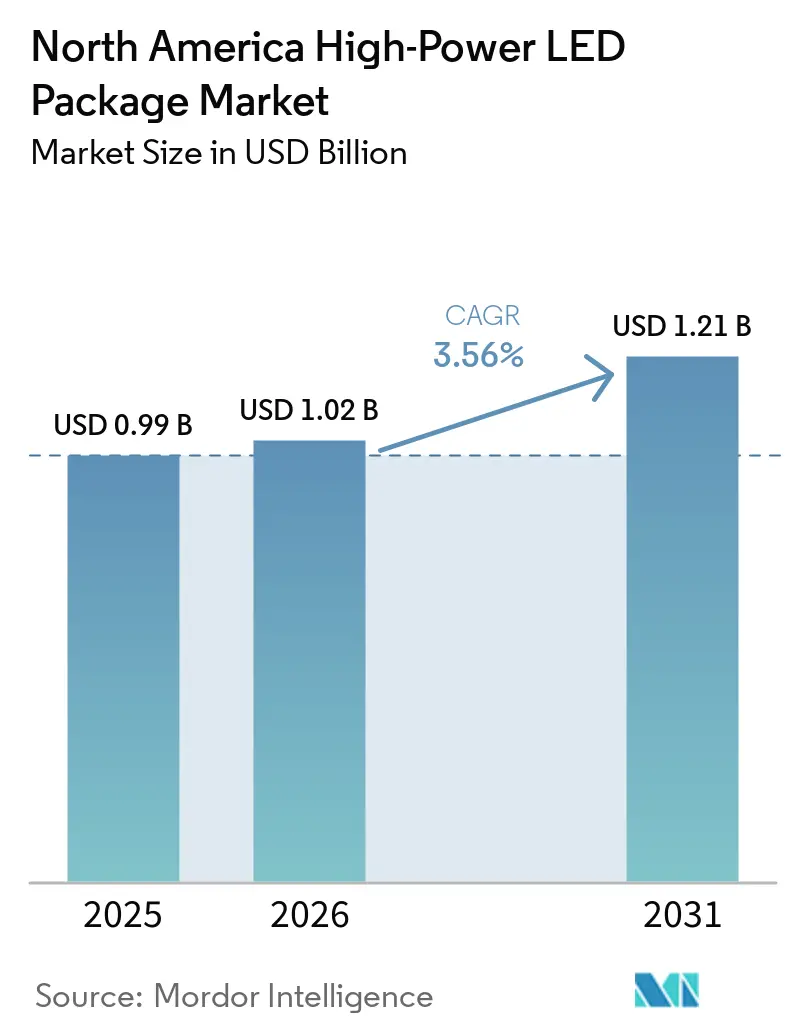

| Base Year Market Size (2025) | USD 0.99 Billion |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

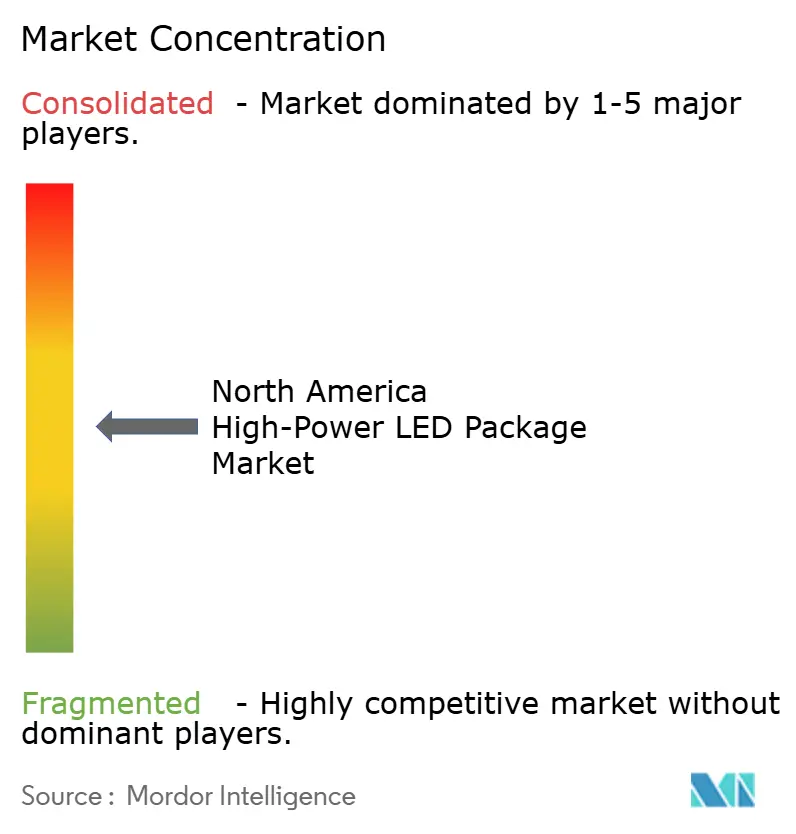

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America High-Power LED Package Market Analysis by Mordor Intelligence

The North America high-power LED package market size is projected to expand from USD 0.99 billion in 2025 and USD 1.02 billion in 2026 to USD 1.21 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031. The growth profile balances a mature retrofit base in commercial lighting with rising demand in automotive headlamps, sports-venue luminaires, and dark-sky compliant outdoor fixtures. Regulatory efficiency mandates, state fluorescent bans, and 8K broadcast requirements are accelerating specification of packages rated above 1 watt. Automotive original equipment manufacturers are migrating to adaptive driving beam modules that incorporate pixel-level dimming, while smart-building integrators prefer high-voltage chip-scale packages compatible with Power-over-Ethernet infrastructure. Supply-chain pressure caused by helium volatility and rare-earth dependence is reinforcing the value of vertically integrated suppliers that control epitaxy, phosphors, and packaging.

Key Report Takeaways

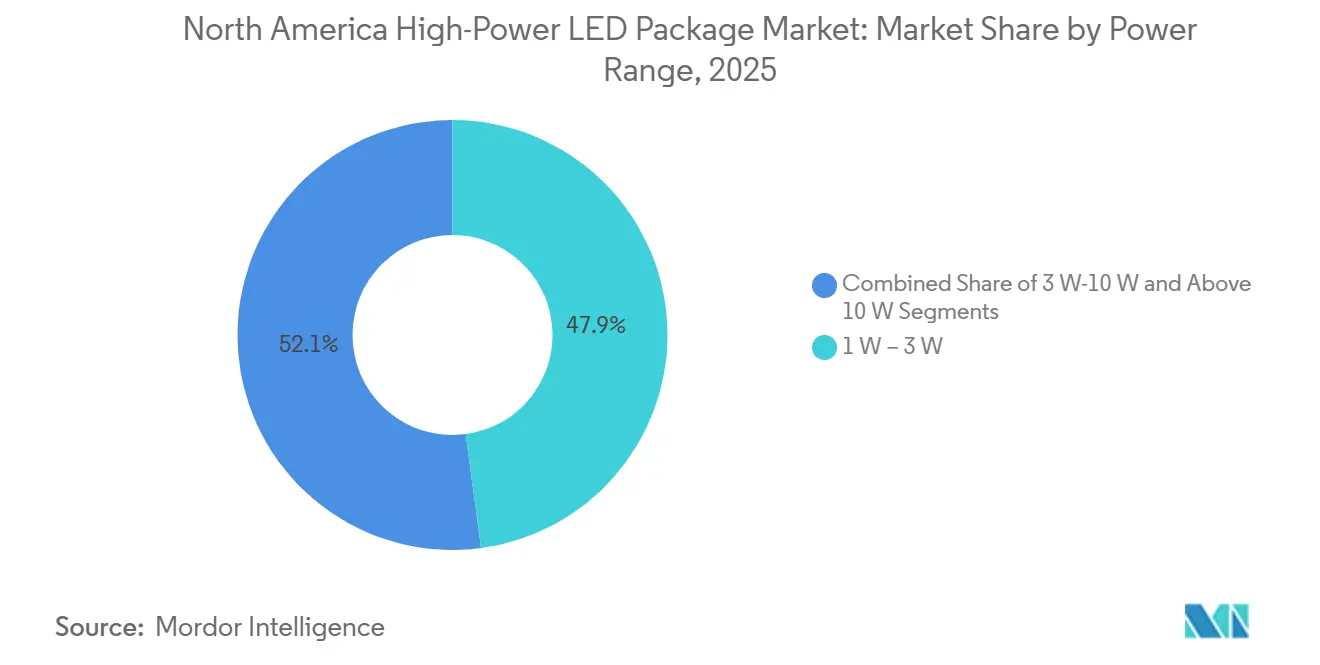

- By power range, the 1 watt to 3 watt tier captured 47.88% of North America high-power LED package market share in 2025, while the above 10 watt segment is advancing at a 4.11% CAGR through 2031.

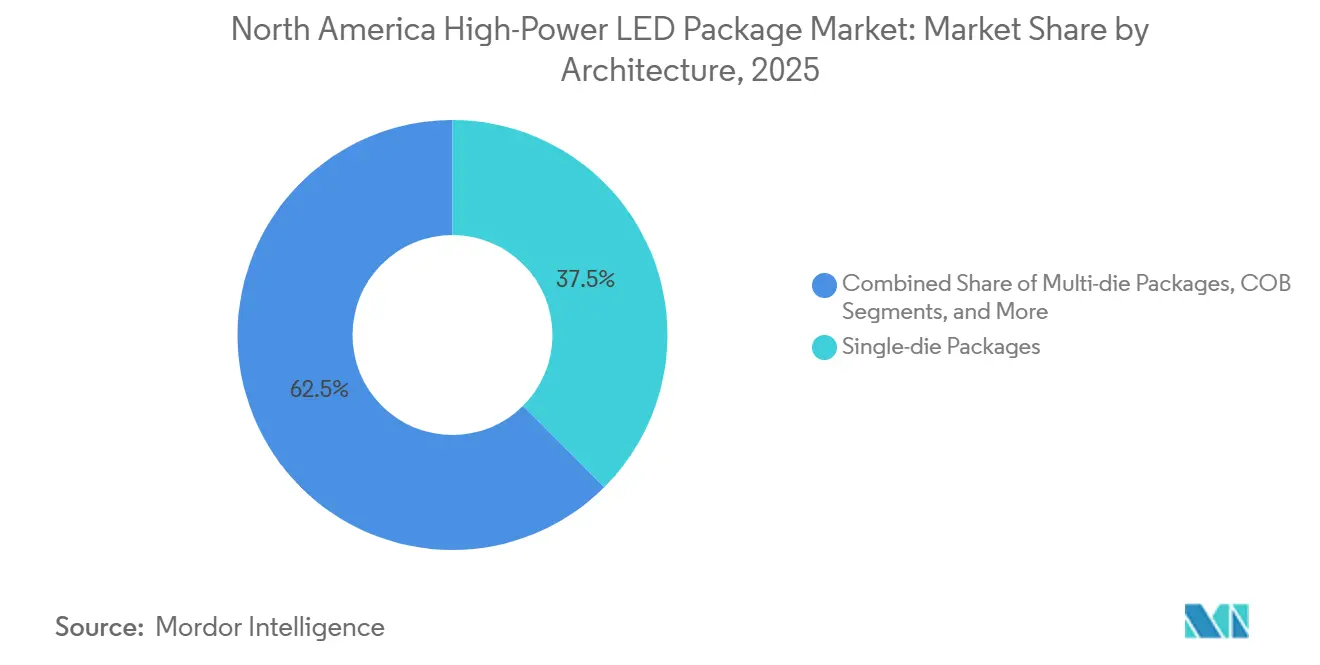

- By architecture, single-die packages led with 37.53% revenue share in 2025, whereas chip-on-board modules record the fastest 4.06% CAGR to 2031.

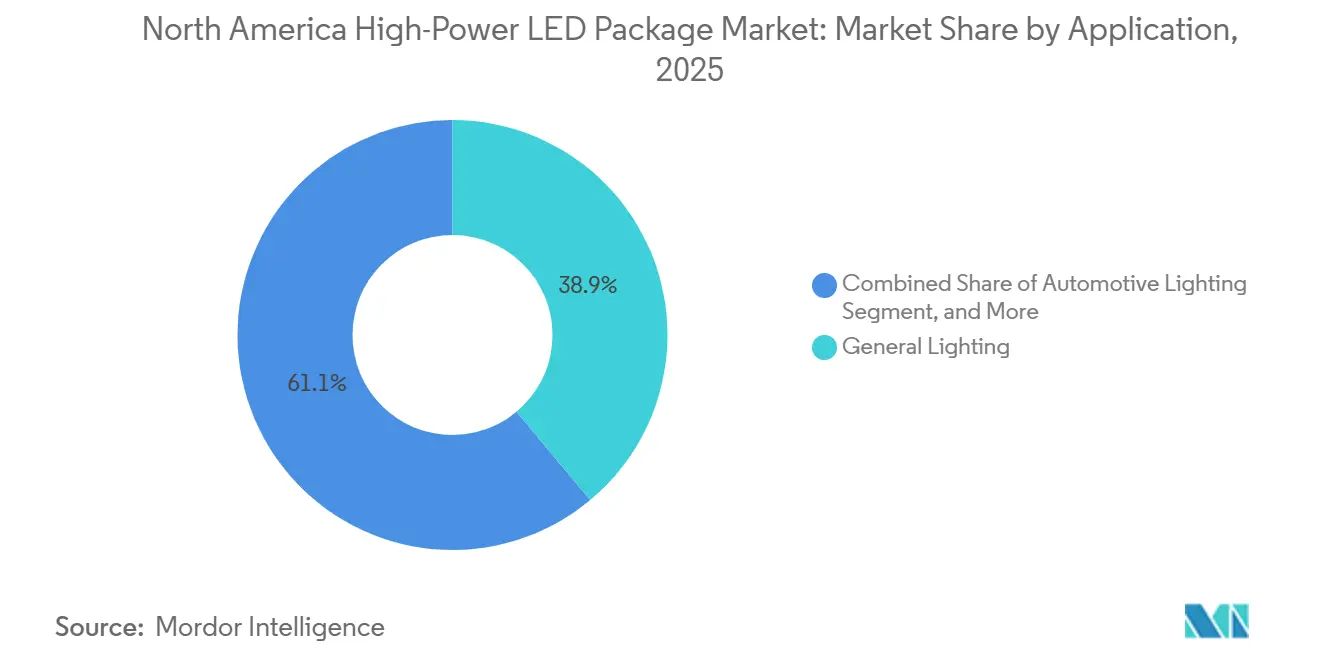

- By application, general lighting accounted for a 38.93% share of the North America high-power LED package market size in 2025 and automotive lighting is expanding at a 4.22% CAGR through 2031.

- By geography, the United States held 87.74% revenue share in 2025, and Canada is growing at a 4.16% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America High-Power LED Package Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-mandated phase-out of inefficient lamps | +1.2% | United States and Canada, with state acceleration in CA, CO, HI, ME, MD, MA | Medium term (2-4 years) |

| Rapid LED penetration in automotive headlamps | +0.9% | U.S. OEM corridors in MI, OH, TN, TX | Short term (≤ 2 years) |

| 8K sports-broadcast lighting standards | +0.5% | Major-league venues and broadcast studios in the United States | Medium term (2-4 years) |

| Dark-sky regulations driving low-blue packages | +0.4% | Early adoption in Maui County, HI, expanding across municipalities in United States and Canada | Long term (≥ 4 years) |

| Stabilization of high-power LED package ASPs | +0.3% | North America | Short term (≤ 2 years) |

| PoE smart-lighting designs favoring high-voltage CSP LEDs | +0.3% | Commercial retrofits and new builds in United States and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Mandated Phase-Out of Inefficient Lamps

Federal and state rules are forcing incandescent and fluorescent products off shelves on a compressed timeline, triggering a sharp pull in demand for high-power packages that can clear 120 lumens per watt within existing fixture envelopes. The U.S. Department of Energy rule, effective July 2028, and six state bans enacted between 2024 and 2027 anchor this shift, making 3-watt to 10-watt emitters the default choice for retrofit downlights and track heads. Distributors are liquidating legacy inventory ahead of cut-off dates, while luminaire brands are fast-tracking chip-on-board and multi-die modules that meet efficacy, lumen density, and color-quality targets. Vendors with in-house phosphor and thermal expertise benefit because compliance audits expose under-performing products to recall risk. The result is a structural growth tailwind that will persist through the middle of the forecast window.[1]U.S. Department of Energy, “Final Rule, General Service Lamps,” energy.gov

Rapid LED Penetration in Automotive Headlamps

Adaptive driving beam approval is reshaping the front-lighting bill of materials. Passenger-car LED penetration already exceeds 70%, and pixel-level systems are moving from luxury to mass-market models under new regulatory headlamp glare rules. Matrix arrays place dozens of individually addressable dice onto compact substrates, favoring high-power packages with low thermal resistance and precise binning. LG Innotek’s ultra-thin pixel module, which won a CES 2026 award, illustrates how shrinking form factors and vehicle-to-everything projections are turning lighting into a safety and communications asset. Tier-one suppliers holding 69.2% automotive share are leveraging patent pools and cross-licenses to secure design wins, locking in multi-year volume ramps as 2027 model launches approach.

8K Sports-Broadcast Lighting Standards Lifting Lumen Demand

Broadcasters migrating to ATSC 3.0 and 8K workflows require flicker below 0.2%, color rendering over 90, and vertical illuminance of 1500 lux or more, specifications that mid-power arrays cannot meet without oversizing fixtures. ITU-R BT.2556, released in 2025, crystallizes these targets for arenas and studios, pushing designers toward chip-on-board modules that concentrate thousands of lumens on a small LES. Stadium retrofits now specify a television lighting consistency index above 95, creating premium demand spikes around National League schedules. Suppliers integrating multi-die stacks with active cooling are capturing orders because fixture counts fall when each unit delivers higher lumen density.[2]International Telecommunication Union, “Recommendation ITU-R BT.2556,” itu.int

Dark-Sky Regulations Driving Low-Blue NightScape Packages

Municipal codes limiting correlated color temperature to 3000 kelvin and blue content to 2% have opened a niche for packages tuned with red and amber phosphors. Maui County’s 2023 ordinance and the 2025 DarkSky Approved program set a template that other jurisdictions are adopting. Lumileds NightScape emitters achieve 1.8% blue at 1900 kelvin and sustain 185 lumens per watt, proving that ecological goals need not sacrifice efficacy. Custom phosphor blends raise material cost but command premium pricing where compliance is mandatory. As wildlife, tourism, and human-health arguments gain traction, low-blue specifications will migrate from coastal resorts to suburban roadways, creating a durable specialty lane for vertically integrated vendors.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal management and reliability challenges above 1 A drive | -0.6% | North America | Medium term (2-4 years) |

| Helium shortage disrupting GaN wafer processing | -0.4% | North America, with supply-chain spillover from global epitaxial capacity constraints | Short term (≤ 2 years) |

| Up-Front Cost Premium Versus Mid-Power LEDs | -0.4% | North America | Medium term (2-4 years) |

| Geopolitical Risk to Rare-Earth Red Phosphors Supply | -0.2% | North America | Long Term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Thermal Management and Reliability Challenges Above 1 A Drive

Driving packages at currents above 1 ampere elevates junction temperatures beyond 150 °C, cutting lifetime in half for every 10 °C rise. Designers must adopt ceramic boards, vapor chambers, or active cooling, which adds cost and weight. Thermal droop reduces efficacy from 150 lumens per watt at 350 mA to near 120 lumens per watt at 1.5 A, negating emitter-count savings. Interface material degradation and solder fatigue under cycling raise warranty exposure, so many luminaires derate to 70% of nameplate current. Until breakthroughs in substrate or phosphor materials lower heat at the source, high-current operation will remain cost-capped in cost-sensitive general lighting.[3]Institute of Electrical and Electronics Engineers, “Thermal Management in High-Power LED Systems,” ieee.org

Helium Shortage Disrupting GaN Wafer Processing

Helium scarcity in 2024-2025 drove up metal-organic chemical vapor deposition costs, delaying capacity expansions and stretching lead times for custom structures. Vertically integrated fabs installed recovery loops, but smaller foundries lacked capital for recycling systems, concentrating wafer supply and shrinking sourcing options for package houses. Although spot prices cooled late in 2025, the episode exposed a non-renewable choke-point and prompted industry groups to pursue alternative carrier gases. Any future geopolitical shock could quickly rekindle volatility and restrain output growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Lumen Density Pushes Growth Above 10 W

The above 10 watt tier of the North America high-power LED package market size is on a 4.11% CAGR path as sports venues, warehouses, and roadway operators favor single-package outputs above 10,000 lumens. Chip-on-board formats dominate because they mount bare dice directly onto metal-core boards, delivering thermal resistance under 2 K/W and supporting smaller heatsinks. In 2025 the 1 watt-3 watt tier retained 47.88% share, serving retrofit downlights that prize footprint compatibility with legacy housings.

Growth momentum is shifting as the DOE efficacy rule and 8K broadcast contracts encourage designers to consolidate flux into fewer optical points, cutting assembly labor and reflector count. Vendors such as Lumileds introduced LUXEON CS in March 2026 to exploit this trend, offering LES diameters from 6.3 mm to 22 mm and CRI options of 90 and 95. The 3 watt-10 watt range remains a transitional bracket for high-bay fixtures but lacks the clear economic edge enjoyed by either extreme.

By Architecture: COB Modules Lead Performance Niches

Chip-on-board modules are expanding at 4.06% over 2026-2031, outstripping single-die packages that held 37.53% North America high-power LED package market share in 2025. Automotive forward lighting and broadcast luminaires value the compact LES and simplified thermal path of COB, which eases pixel-level optical design.

Single-die devices stay prevalent in cost-driven troffers and bulbs where standardized footprints cut qualification effort. Multi-die surface mounts offer incremental power but retain the thermal stack-up of discrete formats. Chip-scale and flip-chip hybrids, though small in revenue today, align well with Power-over-Ethernet smart ceilings because their high voltage lowers copper loss. Lumileds and LG Innotek launches in 2025-2026 illustrate supplier pivot toward mini-packages that can tile densely for dynamic signaling.

By Application: Automotive Lighting Sets the Pace

Automotive lighting is forecast to grow at 4.22% through 2031, fueled by adaptive beam regulation, grill logos, and vehicle-to-everything projection modules. Original equipment manufacturers are integrating dozens of addressable emitters per headlamp, raising per-vehicle package content even as volumes track plateauing car sales.

General lighting, while still commanding 38.93% of 2025 revenue, is maturing as office, retail, and warehouse retrofit cycles taper. Specialty verticals such as horticulture, medical, and UV curing combine tight spectral spec with high willingness to pay, keeping margins healthy despite smaller unit counts. Large-format displays and signage occupy a boutique slice where color gamut and brightness uniformity justify high-power selection.

Geography Analysis

The United States accounted for 87.74% of regional revenue in 2025, driven by commercial retrofits, automotive assembly corridors, and sports-venue upgrades. Federal lamp efficacy rules effective in 2028 compress replacement timelines, while state bans on fluorescent products accelerate uptake in California, Colorado, Hawaii, Maine, Maryland, and Massachusetts.

Canada is projected to grow at 4.16% over 2026-2031 as provincial utilities roll out rebate programs and building codes tighten energy budgets. Natural Resources Canada's minimum performance rules dovetail with these incentives, steering public-sector retrofits toward premium, high-efficacy packages.

Mexico contributes a modest share but is positioned for incremental gains from near-shoring industrial parks that require high-bay and outdoor lighting. Enforcement variance on NOM standards and limited subsidy pools keep the market price-sensitive, leaning toward mid-power arrays until cost curves for high-power packages fall. Divergent codes across the three countries compel suppliers to field region-tailored SKUs and maintain multiple certification tracks.

Competitive Landscape

Market concentration is moderate, with ams OSRAM, Nichia, and Lumileds holding 69.2% share of automotive LED revenues, yet specialty segments remain fragmented. Vertically integrated leaders control epitaxy, phosphor chemistry, and packaging, enabling tighter color bins and faster custom turns. Fabless challengers such as Bridgelux and Luminus outsource wafer work to stay asset-light, pairing agile design cycles with contract capacity.

Patent cross-licensing between Nichia and ams OSRAM in October 2025 broadened freedom-to-operate for matrix headlamps, hinting at consolidation of adaptive beam intellectual property. LG Innotek’s CES award for its 0.12-inch pixel module underscores how proprietary reflector silicones and micro-optics can open premium price lanes.

Supply-chain shocks are reshaping sourcing strategies. Helium volatility favored large fabs with recovery loops, while rare-earth risk around europium and cerium drove some assemblers to trial quantum-dot or nitridosilicate phosphors. Compliance with IEEE 802.3bt and DarkSky Approved programs now acts as a tender gatekeeper, increasing certification spend and squeezing thinly capitalized entrants.

North America High-Power LED Package Industry Leaders

Nichia Corporation

ams OSRAM International GmbH

Lumileds Holding B.V.

Cree LED Inc.

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Luminus Devices and APC Electronics integrated silicon-carbide power semiconductors into the MP-5050 P series, cutting driver weight by 50% in 200-watt systems.

- March 2026: Lumileds released the LUXEON CS COB line with LES options from 6.3 mm to 22 mm and CRI 95, targeting modular automotive lamps.

- February 2026: LG Innotek showcased the NexLide Pixel at the DVN Lighting Workshop, built on more than 700 surface light patents for adaptive headlamps.

- February 2026: Cree Lighting signed a long-term contract manufacturing pact with a U.S. fixture maker to stabilize area and streetlight supply.

North America High-Power LED Package Market Report Scope

The North America High-Power LED Package Market encompasses the design, production, and distribution of high-power LED packages with power ratings from 1 W to above 10 W. These packages are used in various applications, including general lighting, automotive lighting, display and backlighting, and specialty uses.

The North America High-Power LED Package Market Report is Segmented by Power Range (1 W to 3 W, 3 W to 10 W, and Above 10 W), Architecture (Single-die Packages, Multi-die Packages, COB, and Others), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| 1 W - 3 W |

| 3 W - 10 W |

| Above 10 W |

| Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) |

| COB (Chip-on-Board) |

| Others |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| United States |

| Canada |

| Mexico |

| By Power Range | 1 W - 3 W |

| 3 W - 10 W | |

| Above 10 W | |

| By Architecture | Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) | |

| COB (Chip-on-Board) | |

| Others | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Specialty / Niche | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America high-power LED package market today and where is it headed?

It stood at USD 1.02 billion in 2026 and is forecast to reach USD 1.21 billion by 2031 on a 3.56% CAGR trajectory.

Which power range currently dominates shipments?

Devices rated 1 watt to 3 watts held 47.88% of 2025 revenue due to retrofit downlights and track fixtures.

Which segment will grow fastest over the next five years?

Automotive lighting packages are projected to expand at a 4.22% CAGR as adaptive driving beam adoption accelerates.

What regulation is most influencing future demand?

The U.S. DOE rule mandating a minimum 120 lumens per watt for general service lamps effective July 2028 is the key driver.

Which suppliers lead the competitive field?

Ams OSRAM, Nichia, and Lumileds collectively control 69.2% of automotive LED revenues, giving them scale and IP advantages.

Page last updated on: