Europe AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

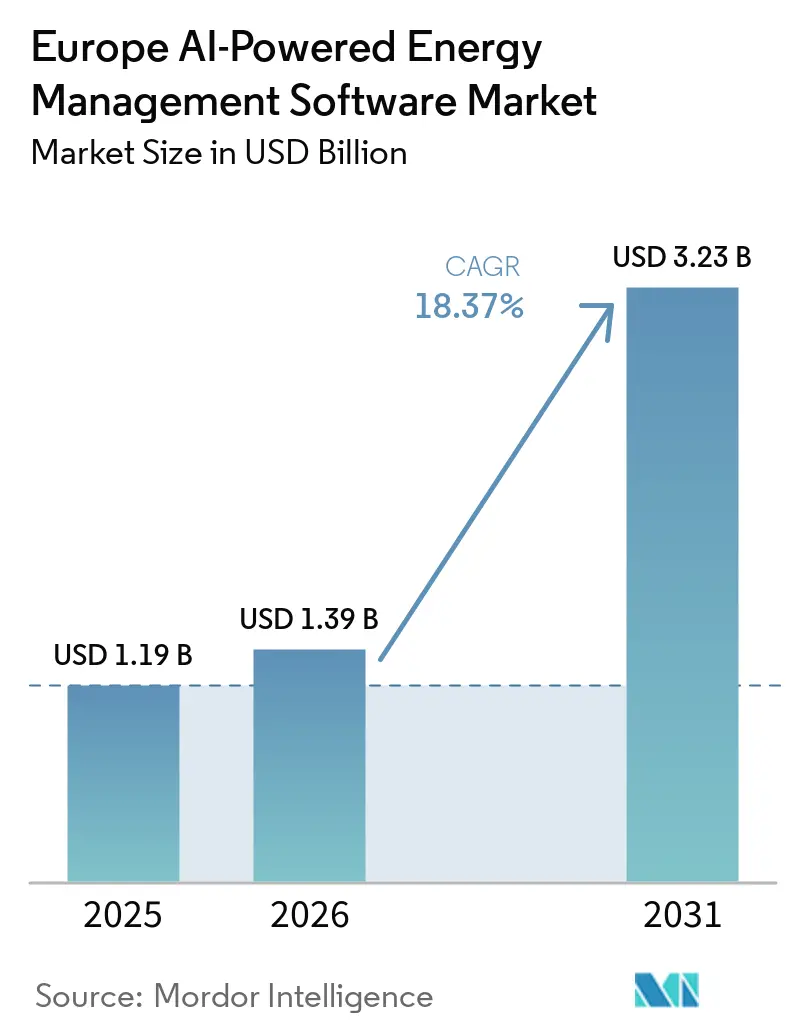

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.39 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 18.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Europe AI-powered energy management software market size was valued at USD 1.19 billion in 2025 and is projected to reach USD 3.23 billion by 2031, growing at a CAGR of 18.37% during 2026-2031. Growth is being supported by sustained electricity price volatility, which has raised the cost of manual energy scheduling for commercial and industrial operators. The market is also benefiting from wider smart meter deployment, because more sites now have access to the detailed consumption data that AI models need for forecasting, load balancing, and automated control. Building efficiency rules, corporate decarbonization targets, and the need for audit-ready emissions records are pushing energy software from a discretionary spend into a core operating system for many enterprises. Utilities are investing in grid balancing and distributed energy resource coordination, while commercial and industrial users are adopting these platforms to lower energy spend, manage operational risk, and improve control over energy-intensive assets. Competition remains moderate at the top end of the market, yet specialist vendors still have room to win in renewable forecasting, industrial optimization, and commercial building intelligence, which keeps the European AI-powered energy management software market active on both product depth and deployment flexibility.

Key Report Takeaways

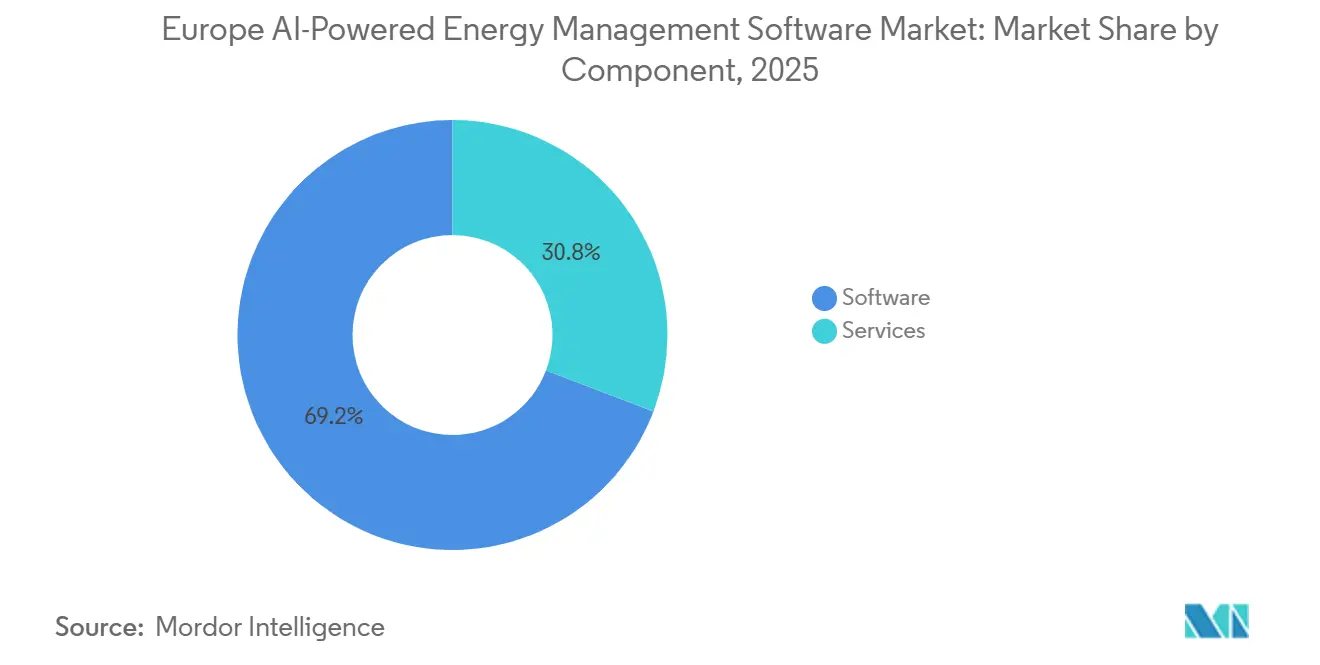

- By component, software accounted for 69.21% of the Europe AI-powered energy management software market in 2025, while services are projected to expand at a 18.44% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 60.17% of the market share in 2025, while hybrid deployment is expected to record the highest CAGR of 18.53% through 2031.

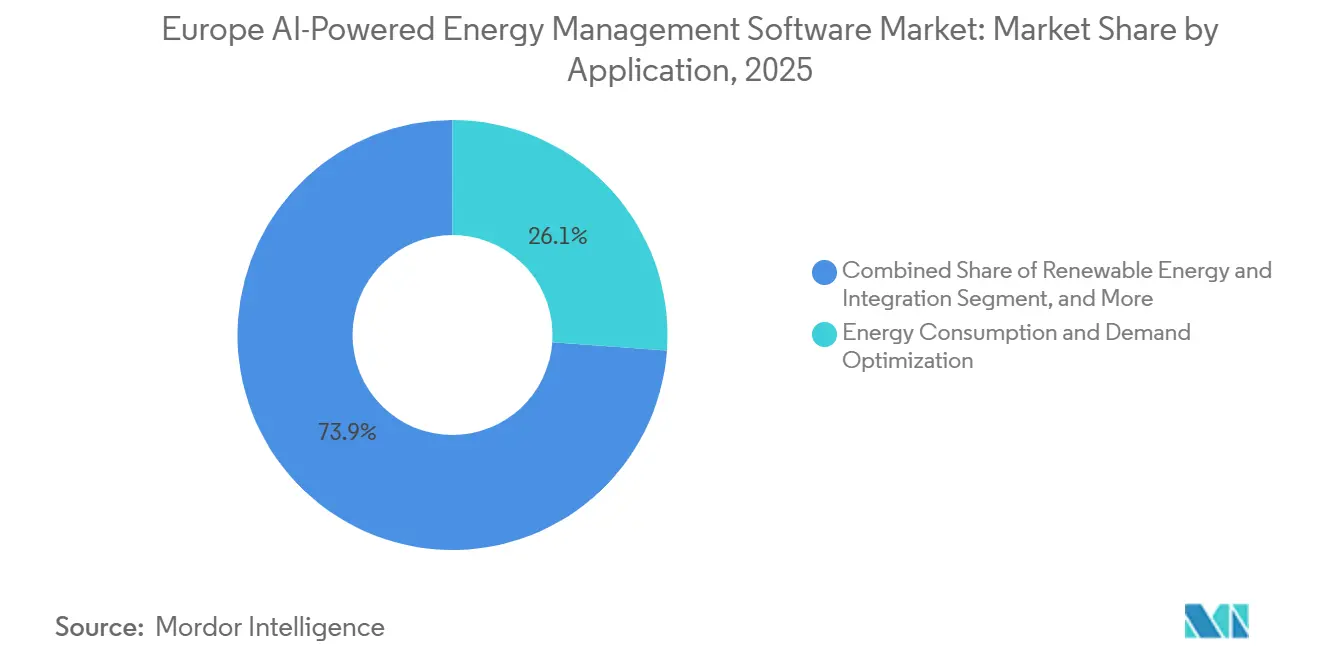

- By application, energy consumption and demand optimization captured 26.14% of the market in 2025, while renewable energy forecasting and integration are projected to grow at an 18.62% CAGR through 2031.

- By end user, utilities held 32.11% of the Europe AI-powered energy management software market share in 2025, while industrial facilities are expected to expand at an 18.71% CAGR through 2031.

- By geography, Germany accounted for 28.16% share in 2025, while the United Kingdom is projected to post the fastest CAGR of 18.79% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Electricity Costs and Load Volatility Across Europe | +3.2% | Germany, Italy, UK, and France | Short term (≤ 2 years) |

| Smart Meter Penetration and Granular Consumption Data Availability | +2.8% | EU-wide, with faster early adoption in Italy, France, and Spain | Medium term (2-4 years) |

| EU Building Efficiency Compliance Pressure on Commercial Portfolios | +2.5% | EU member states, especially non-residential buildings | Medium term (2-4 years) |

| AI-Enabled Forecasting for Demand Response and Peak Shaving | +2.0% | UK, Germany, and France | Short term (≤ 2 years) |

| Faster Return on Investment From Cloud Native Energy Optimization | +1.8% | UK and Germany | Short term (≤ 2 years) |

| Carbon Reporting and Decarbonization Commitments From Large Enterprises | +1.5% | EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Electricity Costs and Load Volatility Across Europe

High and unstable electricity prices have strengthened the commercial case for the Europe AI-powered energy management software market. European wholesale day-ahead electricity averaged EUR 88/MWh (USD 95/MWh) in 2025, and prices exceeded EUR 150/MWh (USD 162/MWh) in 9.3% of trading hours, making manual scheduling harder to justify for large portfolios.[1]Eurelectric, “Electricity in 2025, Solar Surges, Gas Influence Fades, but Volatility and Weak Demand Persist,” Eurelectric, eurelectric.org Buyers are no longer looking only for lower energy bills; they also need tools that can respond to rapid price swings with the discipline manual teams cannot. This shift matters because volatility creates value for forecasting, automated dispatch, and peak avoidance, which are all core functions of the Europe AI-powered energy management software market. Vendors that can support shorter decision cycles and more frequent control actions are moving closer to operational workflows rather than staying in reporting-only roles. The result is that energy optimization software is being treated more like operating infrastructure than an optional analytics layer.

Smart Meter Penetration and Granular Consumption Data Availability

The Europe AI-powered energy management software market is also benefiting from broader access to granular consumption data. Smart meter penetration across the EU27+3 region reached 58% by the end of 2024 and continued to move toward the EU target of 80%, which is steadily enlarging the installed base that can feed AI models with detailed usage signals. The European Commission has also stated that smart meter-enabled energy management can deliver average electricity savings of EUR 270 (USD 292) per metering point, which supports the financial case for wider software adoption.[2]European Commission, “Smart Grids and Meters,” European Commission, energy.ec.europa.eu In markets such as Italy and France, where first-generation rollout has already reached high penetration, the bottleneck has shifted from data collection to data interpretation and control logic. In Germany, smart meter penetration was only 2.8% in Q1 2025, meaning each new installation expands the addressable base for the Europe AI-powered energy management software market over the long term. This pattern supports both near-term adoption in mature meter markets and longer runway growth in late-moving countries.

EU Building Efficiency Compliance Pressure on Commercial Portfolios

Compliance pressure in non-residential buildings is creating another strong demand channel for the European AI-powered energy management software market. The recast Energy Performance of Buildings Directive entered into force in 2024 and sets a national transposition deadline of 2026, while also imposing renovation obligations for the lowest-performing non-residential buildings by 2030 and 2033. These requirements are pushing landlords, asset managers, and facility operators to treat building controls and energy monitoring as much of a compliance issue as a cost issue. Static controls can help with basic monitoring, but they are less effective when building load changes through occupancy, weather, and price conditions across the day. That is why the Europe AI-powered energy management software market is increasingly being pulled into building automation programs as an overlay that improves response quality and reporting discipline. AI-driven energy management platforms can reduce operating costs by up to 30% in industrial settings by improving power quality, reducing waste, and lowering unplanned maintenance, reinforcing the case for broader software-led optimization.[3]ABB, “Energy and Asset Manager, Energy Management,” ABB, abb.com

AI-Enabled Forecasting for Demand Response and Peak Shaving

The Europe AI-powered energy management software market is gaining from the need to forecast and monetize flexibility more accurately. EU solar output exceeded 340 TWh in 2025, reaching a record 12.5% of total EU generation, underscoring the need for better forecasting and faster balancing actions. In this setting, software that can predict short-term generation, load shifts, and dispatch windows has become more valuable to utilities, aggregators, and large power users. It is already being used at scale, with some providers delivering hundreds of millions of forecast data points daily across large installed capacities in multiple countries. Industrial sites have also reported multimillion-pound savings through production-linked load optimization, showing that participation in flexibility programs is becoming financially meaningful. As variable renewable generation continues to grow, the Europe AI-powered energy management software market is likely to benefit from stronger demand for tools that integrate forecasting, dispatch, and asset coordination into a single workflow.[4]GridBeyond, “Demand Response in 2026, From Strategic Advantage to Grid Imperative,” GridBeyond, gridbeyond.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration Complexity With Legacy Building and Industrial Control Systems | -2.0% | EU-wide, with heavier legacy intensity in Germany and Italy | Long term (≥ 4 years) |

| Data Privacy, Cybersecurity, and AI Governance Compliance Burden | -1.5% | EU-wide | Medium term (2-4 years) |

| Fragmented Facility Ownership Slowing Portfolio Scale-Up | -1.0% | France, Germany, and UK | Long term (≥ 4 years) |

| Skilled Implementation Shortage for Energy AI Deployment and Tuning | -0.8% | EU-wide, with stronger pressure in Germany and Central and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity With Legacy Building and Industrial Control Systems

Integration complexity remains one of the clearest limits on how fast the Europe AI-powered energy management software market can scale across large portfolios. Many commercial and industrial sites still rely on older building controls, process systems, and fragmented sensor networks that do not exchange data smoothly. This raises implementation time, increases testing needs, and can weaken model quality if the incoming data is incomplete or inconsistent. It also pushes buyers to spend more on configuration, middleware, and support before they see value at the site level. Some vendors are positioning modular platforms that combine coordinated control with both edge and cloud processing, demonstrating how they aim to reduce this problem through more flexible system design. Even so, integration work remains a significant drag on rollout speed, especially when portfolio owners want a single platform to cover multiple facility types.

Data Privacy, Cybersecurity, and AI Governance Compliance Burden

Governance requirements are also raising the operating burden for the Europe AI-powered energy management software market. Buyers increasingly expect strong access controls, cleaner audit trails, and clearer ownership of operational and sustainability data before they approve software deployment. This is especially important when platforms move from passive reporting into automated recommendations or control actions that affect energy assets. These buyer expectations are shaping product design, with vendors highlighting cross-application security workflows and broader system connectivity improvements. The market is also moving toward more traceable environmental and financial records in software environments that support reporting and verification needs. These added requirements do not stop adoption, but they do lengthen due diligence cycles and raise the bar for smaller vendors that have fewer compliance resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Remained the Core Revenue Base

Software accounted for 69.21% of the Europe AI-powered energy management software market in 2025, confirming that buyers still prefer scalable software subscriptions over hardware-based deployments. This lead reflects the fact that software can be updated more often, rolled out across multiple sites, and adapted to new reporting or optimization tasks without a new equipment cycle. The software layer is where forecasting, anomaly detection, load shaping, and emissions reporting come together, so it remains the center of the buying decision in the Europe AI-powered energy management software market. The software segment also benefits from a broader buyer base, as utilities, commercial buildings, and industrial facilities can all deploy the same core platform with different control logic and reporting views. For many customers, the appeal is not only cost control, but also the ability to standardize energy visibility across geographically dispersed assets.

Services are projected to expand at a 18.44% CAGR through 2031, indicating that the Europe AI-powered energy management software industry is not moving away from software but is adding more implementation and optimization work around it. Large accounts often need system integration, model tuning, training, and managed analytics before internal teams can use the platform effectively at scale. This is especially true in industrial and multi-site building portfolios where operating conditions differ by site, and energy workflows cannot be copied without adjustment. Vendors are responding by combining subscription models with higher-value service layers that support onboarding and long-term performance management. The result is a component mix where software leads revenue and services deepen stickiness, retention, and realized customer value within the Europe AI-powered energy management software market.

By Deployment Mode: Cloud Led Adoption While Hybrid Gained Ground Faster

Cloud-based deployment held a 60.17% share of the European AI-powered energy management software market in 2025, making it the dominant deployment model across buildings and utility analytics use cases. Centralized data access, easier remote updates, and faster scaling across multiple facilities have made cloud models the default choice for moderate real-time control requirements. This preference also aligns with enterprise buying patterns, as many organizations seek lower upfront IT complexity and easier reporting consolidation across sites. In the European AI-powered energy management software market, cloud deployment is particularly attractive for sustainability reporting, cost benchmarking, and consumption analytics that need a broad portfolio view. It also aligns with the push toward subscription pricing and more frequent feature releases.

Hybrid deployment is expected to expand at a 18.53% CAGR through 2031, indicating that the market is balancing cloud economics with site-level operational realities. Critical infrastructure operators and energy-intensive manufacturers often need parts of the control stack to stay closer to the asset because some actions must occur with low latency and with tighter system separation. Hybrid models let them keep deterministic control loops on site while moving forecasting, benchmarking, and portfolio analytics into broader cloud environments. This makes hybrid architecture a practical bridge between legacy site conditions and newer enterprise software strategies in the Europe AI-powered energy management software market. Modular platforms with both edge and cloud processing layers directly support this blended deployment logic. On-premises systems still matter in regulated or connectivity-constrained sites, but their relative role is narrowing as hybrid setups become the preferred compromise for more complex accounts.

By Application: Demand Optimization Stayed Largest While Renewable Forecasting Advanced Fastest

Energy consumption and demand optimization accounted for a 26.14% share in 2025, making it the largest application in the Europe AI-powered energy management software market. This position reflects the basic commercial logic of the category, because most buyers first adopt the software to reduce energy bills, manage peaks, and improve scheduling in response to shifting tariff and wholesale conditions. The use case is broad and immediate, and that gives it a larger addressable base than narrower specialist applications. It also aligns well with both building portfolios and industrial operations, helping vendors scale the same core capabilities across multiple customer groups. In many cases, this application becomes the entry point through which customers later add maintenance, renewable forecasting, and market participation functions.

Renewable energy forecasting and integration is projected to grow at a 18.62% CAGR through 2031, indicating where the next layer of application demand is emerging. EU solar generation rose above 340 TWh in 2025, accounting for 12.5% of total generation, underscoring the value of software that can anticipate output swings and align demand or storage decisions more accurately. Platforms are already processing hundreds of millions of forecast data points each day across large installed capacities, illustrating the scale of forecasting needed in this application set. Asset performance and predictive maintenance also remain important, as operators increasingly want a single platform to support both uptime and energy savings. Smart grid and distributed energy resource management are gaining ground as utilities face a larger mix of batteries, EV chargers, and distributed loads that need coordination. Energy trading, pricing, and market intelligence adds another layer to the Europe AI-powered energy management software market, as some industrial operators now want direct visibility into intraday price signals before shifting production loads or dispatching storage.

By End User: Utilities Held the Lead While Industrial Facilities Set the Pace for Growth

Utilities accounted for 32.11% of the Europe AI-powered energy management software market in 2025 and held the largest share, as they had adopted these platforms earlier for grid balancing, predictive maintenance, and distributed energy resource coordination. Their scale gives software vendors larger contract values, broader meter coverage, and stronger reference cases than many other end users can provide. Utilities also need these tools across more workflows, from demand response to forecasting and outage-related operational planning, which supports deeper platform adoption. In the Europe AI-powered energy management software market, utility demand helps anchor revenue because the buyer group is linked to system-level reliability obligations rather than optional efficiency spending. One utility deployment has even shown how a single relationship can materially expand platform scale by multiplying contracted meter bases.

Industrial facilities are projected to grow at a 18.71% CAGR through 2031, making them the fastest-expanding end-user segment in the Europe AI-powered energy management software market. This growth reflects how manufacturers are no longer treating energy as a passive overhead, but as part of their operating discipline and production economics. Industrial users are increasingly interested in linking plant load, storage, process timing, and maintenance conditions to power price signals within a single control environment. Commercial buildings remain a major user group because they require portfolio monitoring, occupancy-linked HVAC optimization, and support for building compliance across large site estates. Residential buildings still hold the smallest share, but the industry is moving closer to that segment as smart meter infrastructure expands and average savings per metering point continue to be highlighted. This leaves the end-user mix balanced between large institutional adopters that provide scale today and smaller distributed users that can widen the addressable base over time.

Geography Analysis

Germany held 28.16% of the Europe AI-powered energy management software market share in 2025, maintaining its regional leadership thanks to its large industrial energy base and strong need for cost control. Germany also combines mature industrial demand with an early-stage smart meter rollout, since penetration stood at 2.8% in Q1 2025, creating a market where software demand is advancing faster than metering infrastructure in some use cases. This gives vendors room to serve customers through existing SCADA and control data today while preparing for a denser stream of smart meter inputs later. Updates to the eligible energy management software lists have also supported adoption by reducing procurement risk for industrial users that qualify for efficiency-related support. The United Kingdom is projected to record the fastest CAGR of 18.79% through 2031, supported by an active flexibility ecosystem, strong momentum in battery storage, and a visible cluster of AI-energy specialists.

France remains one of the more important markets because of its high smart meter penetration, which has created an AI-ready data layer across residential and commercial settings. The first-generation rollout already exceeds 90%, supporting more advanced analytics and portfolio control use cases. Italy and Spain also remain relevant growth markets in the Europe AI-powered energy management software market because both are seeing stronger interest in combining energy efficiency goals with behind-the-meter optimization and renewable integration. These countries are helping broaden demand beyond the largest Western European markets, especially where commercial buildings and industrial users want more automated responses to intraday energy conditions.

The Rest of Europe segment includes markets such as the Netherlands, Poland, Sweden, Norway, Switzerland, and Belgium, which together add meaningful depth to regional demand. In these countries, the commercial case often depends on a mix of smart meter progress, renewable intensity, and the need for more coordinated flexibility management across distributed assets. The Netherlands stands out for its software activity around utility and prosumer data platforms, while Poland offers a longer demand runway as metering infrastructure builds out across the country. Nordic markets also provide a favorable setting for forecasting and trading applications due to their mature electricity market structures and strong participation in renewable energy. Taken together, these national markets support a broader regional demand base and keep the Europe AI-powered energy management software market from depending only on Germany, the UK, and France.

Competitive Landscape

The Europe AI-powered energy management software market is moderately fragmented, with large automation and software groups leading the upper tier, while specialist firms continue to compete effectively in narrower use cases. Schneider Electric, Siemens, and ABB hold strong positions because they can connect building systems, industrial controls, grid workflows, and energy optimization through broader platform suites. Their advantage is not only scale but also an installed base, existing enterprise relationships, and the ability to support multi-site customers who want fewer vendors. This matters in the Europe AI-powered energy management software market because large buyers increasingly prefer platforms that combine monitoring, forecasting, reporting, and control in a single operating environment. Some vendors have been advancing that position through AI-driven approaches to converged energy, power, and building visibility.

At the same time, specialist vendors continue to win where domain precision and faster implementation matter more than platform breadth. Forecasting firms, flexibility orchestrators, and commercial building optimization specialists can move faster in specific niches and often tailor models more closely to customer conditions. Focused utility partnerships have shown how specialist platforms can gain strong momentum and scale quickly, keeping the competitive field active even as larger incumbents broaden their own software stacks.

Recent product and partnership activity also shows that the Europe AI-powered energy management software market is moving toward more connected, operationally embedded software. Integrations between building management platforms and IoT ecosystems are extending vendor positions inside enterprise environments. Broader multi-site energy and cost monitoring capabilities are being added to commercial operator platforms, while sustainability-focused solutions are connecting environmental and financial data in ways that support more formal reporting workflows. Across the competitive landscape, the winners are likely to be vendors that can combine integration depth, clean reporting, and practical control logic without making deployment too heavy for customers to scale.

Europe AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: ABB and Samsung Electronics announced an integration between ABB Ability BuildingPro and Samsung SmartThings Pro, with proof-of-concept deployments scheduled across three European sites.

- May 2026: Samsung's Business Experience Center in Eschborn, Germany; Samsung's Training Center in Amsterdam, the Netherlands; and ABB's headquarters in Middelfart, Denmark. The integration extends ABB's AI-powered building energy management footprint within enterprise IoT environments.

- May 2026: ABB announced integration of its ABB Genix Industrial IoT and AI Suite with NVIDIA Omniverse and Microsoft Azure at Hannover Messe 2026. The collaboration delivers immersive 3D digital twin visualization for industrial energy systems, combining AI anomaly detection with high-fidelity simulation to improve operator decision-making and system health monitoring across energy-intensive industrial sites.

- March 2026: Siemens released the Building X Energy Manager Standard, completing the platform's Energy Manager offering with expanded multi-site consumption and cost monitoring capabilities. The release includes enhanced cross-application security workflows, improved system connectivity, and support for portfolio-wide sustainability KPI tracking, extending the platform's value proposition for commercial building operators managing large asset portfolios.

- November 2025: GridBeyond and ep Group announced a partnership to deploy GridBeyond's AI-driven energy management system for ep Group's 50 MW battery energy storage system at North Baddesley in the UK. The deployment enables real-time optimization, forecasting, and capacity market enrollment for the 50 MW asset, representing a significant AI energy management contract in the UK's growing grid-scale storage market.

Europe AI-Powered Energy Management Software Market Report Scope

The Europe AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management across the region. These solutions provide advanced capabilities, including predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Europe AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size outlook for Europe AI-powered energy management software through 2031?

The Europe AI-powered energy management software market was valued at USD 1.19 billion in 2025 and is projected to reach USD 3.23 billion by 2031 at an 18.37% CAGR during 2026-2031.

What is driving adoption across Europe?

The main triggers are electricity price volatility, wider smart meter deployment, building efficiency compliance pressure, and stronger demand for forecasting and flexible load control.

Which application area is leading revenue today?

Energy consumption and demand optimization led with 26.14% share in 2025 because it directly addresses energy cost control, peak management, and load scheduling.

Which application area is growing the fastest?

Renewable energy forecasting and integration is projected to grow at an 18.62% CAGR through 2031 as higher solar and renewable penetration raises the value of accurate short-term forecasting.

Which end users are creating the strongest demand?

Utilities led with 32.11% share in 2025, while industrial facilities are projected to grow the fastest at 18.71% CAGR as manufacturers link energy decisions more closely with production scheduling.

Which countries matter most in this regional landscape?

Germany led with 28.16% share in 2025, while the United Kingdom is projected to post the fastest growth at 18.79% CAGR through 2031, with France also remaining important because of its advanced smart meter base.

Page last updated on: