Spain AI-Powered Energy Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

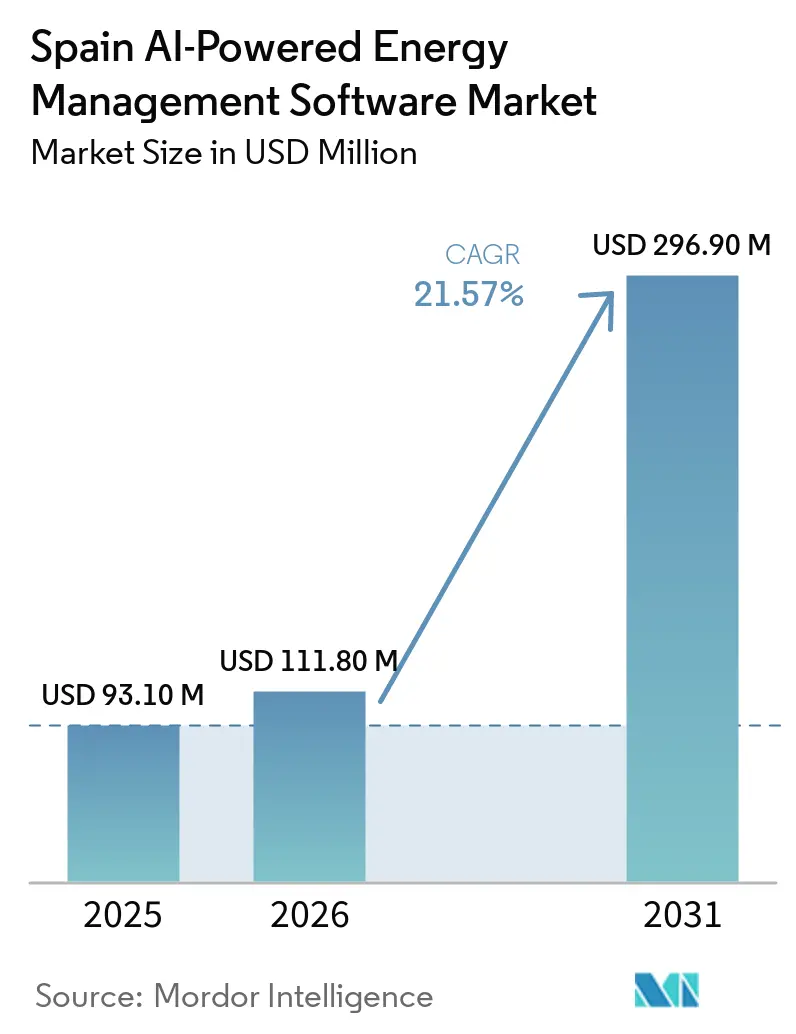

| Base Year Market Size (2025) | USD 93.10 Million |

| Market Size (2026) | USD 111.80 Million |

| Market Size (2031) | USD 296.90 Million |

| Growth Rate (2026 - 2031) | 21.57% CAGR |

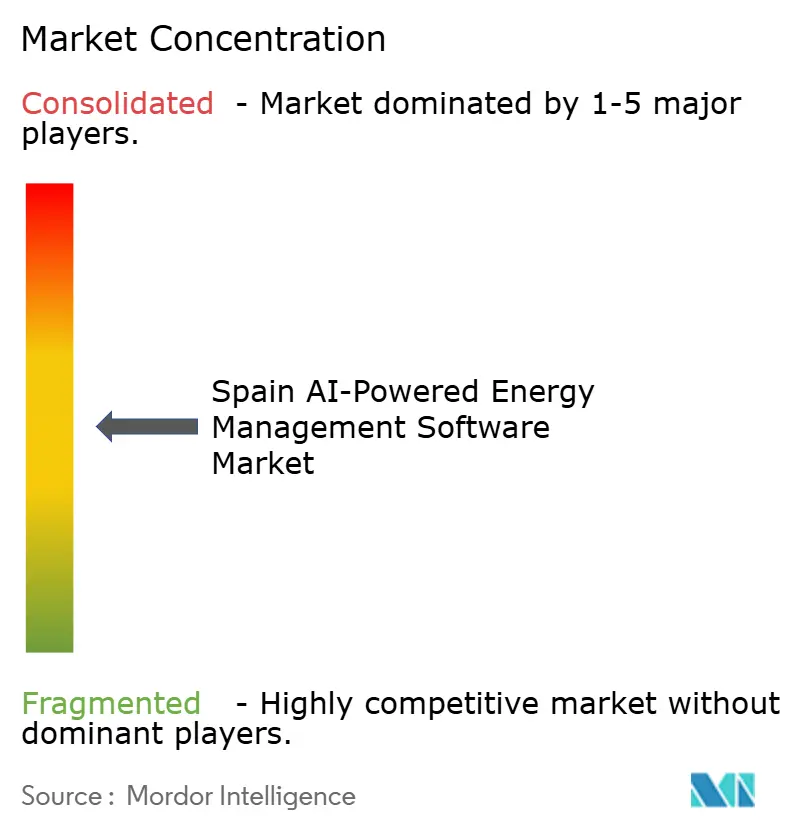

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain AI-Powered Energy Management Software Market Analysis by Mordor Intelligence

The Spain AI-Powered Energy Management Software Market size was valued at USD 93.1 million in 2025 and estimated to grow from USD 111.8 million in 2026 to reach USD 296.9 million by 2031, at a CAGR of 21.57% during the forecast period (2026-2031). The Spain AI-Powered Energy Management Software Market is expanding as Spain’s power system moves deeper into renewable generation, increasing the need for software that can forecast output, balance loads, and support faster decision-making. Regulatory pressure is also strengthening demand, as carbon reporting obligations that began in 2026 are pushing more organizations to connect energy data, emissions records, and operational controls into a single platform. The market is also being shaped by grid conditions that now require better midday balancing, stronger demand response, and more flexible coordination between storage, distributed assets, and electricity consumption. Buyers are placing greater weight on software architectures that can combine cloud-scale with local data control, increasing the appeal of hybrid models in the Spanish AI-Powered Energy Management Software Market. Competitive positioning in the Spanish AI-Powered Energy Management Software Market is therefore moving beyond core monitoring functions and toward broader capabilities in integration, energy intelligence, managed services, and regulatory fit.

Key Report Takeaways

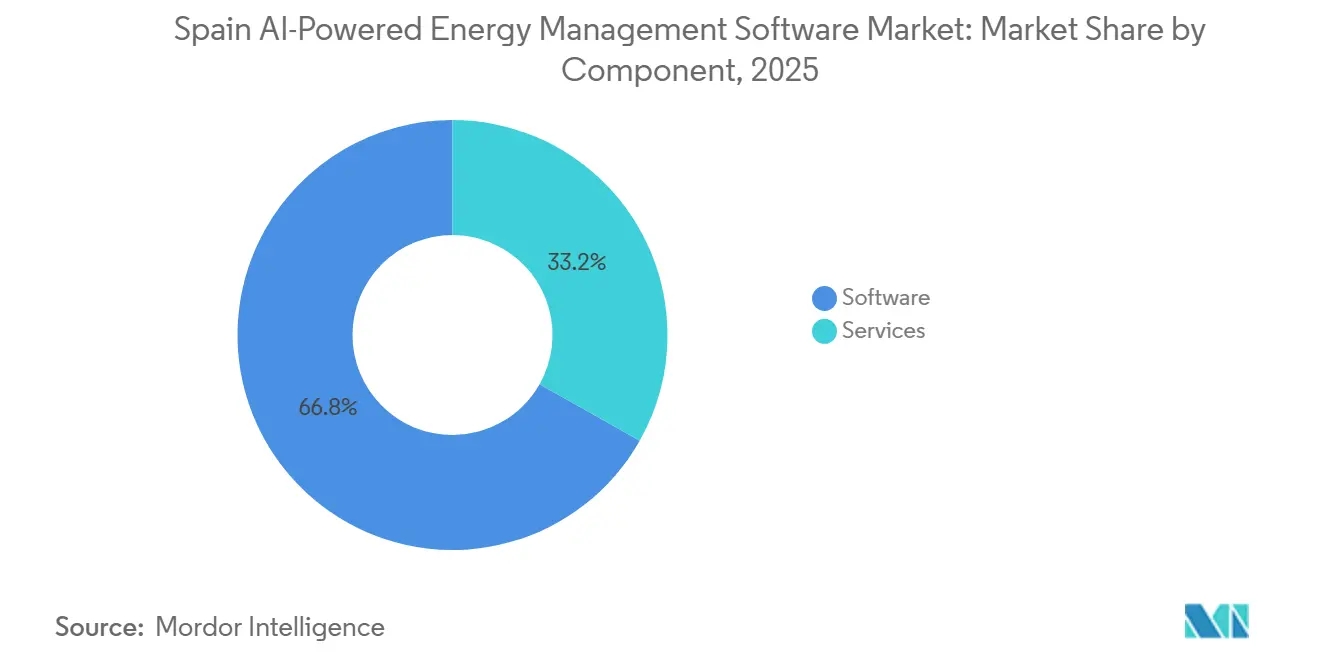

- By component, software held 66.18% share in 2025, while services are projected to expand at a CAGR of 22.61% through 2031 in the Spain AI-Powered Energy Management Software Market.

- By deployment mode, cloud-based deployment held 57.12% share in 2025, while hybrid deployment is projected to grow at a CAGR of 22.73% through 2031.

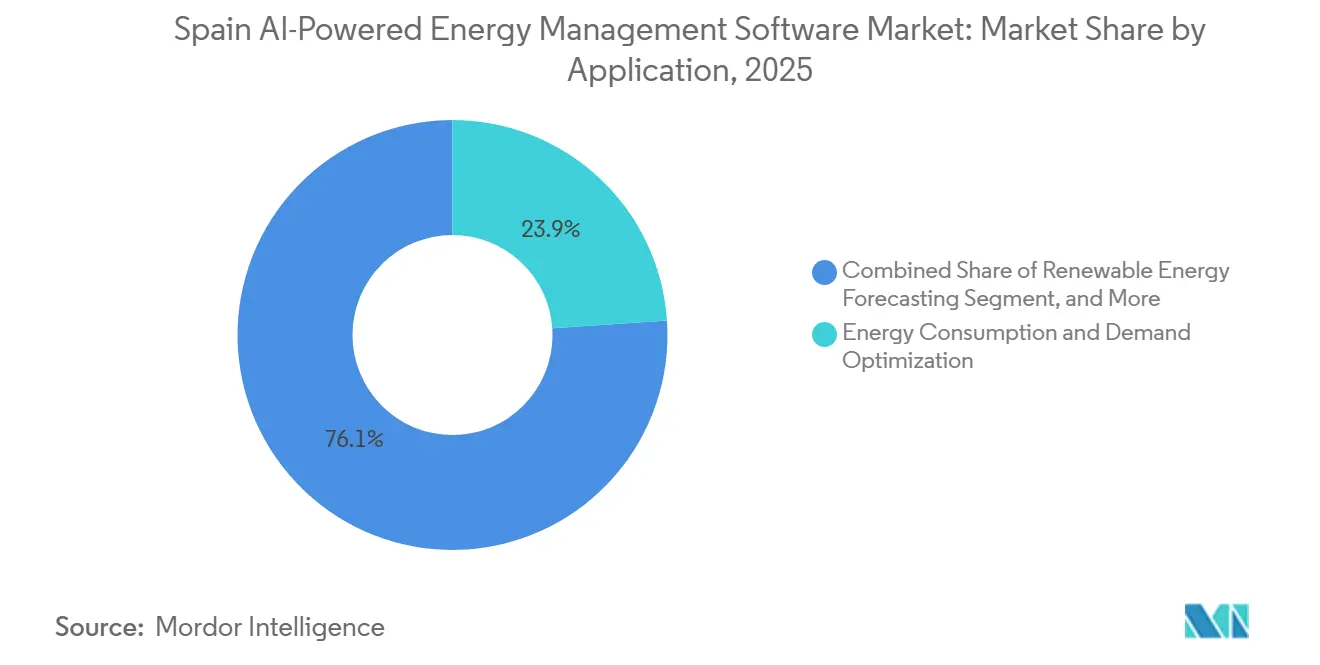

- By application, energy consumption and demand optimization accounted for 24.15% of the market share in 2025, while renewable energy forecasting and integration are projected to register a CAGR of 22.84% through 2031.

- By end user, utilities held 33.19% share of the Spain AI-Powered Energy Management Software Market in 2025, while industrial facilities are projected to register a CAGR of 22.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain AI-Powered Energy Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities | +4.2% | Spain-wide, with stronger demand in Madrid, Barcelona, and Basque Country industrial zones | Medium term (2-4 years) |

| AI Integration With Smart Grids and Distributed Energy Resources | +3.8% | Andalusia, Castile-La Mancha, and Aragón, with spillover across Spain | Medium term (2-4 years) |

| Increasing Demand for Automated Demand Response and Peak Load Management | +3.1% | Spain-wide, especially urban commercial centers and utility operators | Short term (≤ 2 years) |

| Expansion of ESG Reporting and Carbon Accounting Workflows | +2.9% | Spain-wide under national and EU compliance rules | Short term (≤ 2 years) |

| Edge AI Adoption for Site-Level Energy Control and Fault Detection | +2.5% | Industrial zones in Basque Country and Catalonia, with early use at remote renewable sites | Long term (≥ 4 years) |

| Retrofit Demand From Aging Building and Industrial Infrastructure | +1.8% | Spain-wide, with concentration in legacy industrial regions such as Asturias and the Basque Country | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Real-Time Energy Optimization in Commercial and Industrial Facilities

Commercial and industrial operators in Spain have remained under pressure to control energy costs following the price disruptions seen over recent years. That pressure is making real-time monitoring and automated control more useful, because AI platforms can detect peaks, adjust setpoints, and improve daily operating efficiency without waiting for manual review. Large venues have already shown the value of this approach, including the deployment of Sener’s AI platform at Fira de Barcelona, where the target was to reduce energy use by up to 30%. The Spain AI-Powered Energy Management Software Market is also benefiting from the growing need to manage multi-tariff contracts, peak-demand penalties, and reactive power charges through software rather than through manual energy oversight. This is becoming increasingly important as industrial sites add rooftop solar, combined heat and power, and storage, making local energy decisions more complex and strengthening demand for automation.

AI Integration with Smart Grids and Distributed Energy Resources

The Spain AI-Powered Energy Management Software Market is gaining traction amid the country’s need to manage a more complex, renewable-heavy grid. Spain reached 100 GW of installed renewable capacity in 2025, increasing the need for software that can coordinate forecasting, storage dispatch, flexible demand, and distributed assets at much higher speeds. The European Investment Bank and Endesa signed two loans totaling EUR 650 million (USD 702 million) in September 2025 to support smart meters, advanced transformers, and full grid digitalization during 2025-2027, which confirms strong institutional backing for grid intelligence in Spain.[1]European Investment Bank, “Spanish Ministry of Economy, EIB and Endesa Agree EUR 650 Million in Financing to Strengthen and Digitalise Spain's Electricity Networks,” European Investment Bank, eib.org Spain’s S2F project, approved by the Ministry for Ecological Transition and the Demographic Challenge, is also testing flexibility pilots that support nationwide AI-enabled demand aggregation and DER balancing. These developments are pushing utilities toward platforms that combine real-time operational control with market-facing optimization, thereby raising the strategic role of software in the Spain AI-Powered Energy Management Software Market.

Increasing Demand for Automated Demand Response and Peak Load Management

The Spain AI-Powered Energy Management Software Market is also advancing as automated demand response moves from a niche activity to a broader operating priority. The national energy transition plan supports greater flexibility mechanisms, and Spain’s evolving market framework is placing greater value on tools that can shift loads, reduce peaks, and respond to price signals. Royal Decree-Law 7/2026 introduced a flexible demand-side access and connection regime for consumers with adjustable loads, thereby strengthening the commercial case for AI-based peak shaving and load-shifting software.[2]Boletín Oficial del Estado, “Real Decreto 214/2025, de 18 de Marzo, por el que se Crea el Registro de Huella de Carbono,” Boletín Oficial del Estado, boe.es Demand response aggregators are also expanding the use of AI scheduling tools that adjust consumption in response to OMIE intraday pricing, linking energy savings with potential market participation revenue. Large Spanish retail operators using Smarkia’s systems achieved electricity consumption reductions of up to 50%, demonstrating that automation is now judged by measurable operational value rather than basic monitoring alone.

Expansion of ESG Reporting and Carbon Accounting Workflows

Compliance needs are becoming a direct growth driver for the Spain AI-Powered Energy Management Software Market. Royal Decree 214/2025 made carbon footprint calculation, reduction planning, and public disclosure mandatory for approximately 4,000 Spanish organizations from 2026 onward, increasing demand for platforms that connect energy data with audit-ready emissions reporting. This is pushing buyers to favor software that can handle Scope 1 and Scope 2 reporting alongside normal energy optimization tasks. The number of Spanish companies with science-based climate targets rose by 22% in 2025, which suggests that demand extends beyond minimum legal compliance. As a result, many organizations are viewing a single energy platform as a way to support both operational savings and formal sustainability reporting, thereby strengthening adoption across the Spain AI-Powered Energy Management Software Market.[3]ECODES and Pacto Mundial de la ONU España, “Las Empresas Españolas Refuerzan su Posición en los Rankings Climáticos Según el Anuario Climático 2025,” ECODES, ecodes.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity With Legacy OT and IT Systems | -3.2% | Spain-wide, especially in utility infrastructure and legacy industrial control environments | Long term (≥ 4 years) |

| Data Quality and Interoperability Gaps Across Metering and Sensor Layers | -2.4% | Spain-wide, with stronger impact where metering standards vary across autonomous communities | Medium term (2-4 years) |

| Cybersecurity and Data Sovereignty Concerns for Critical Energy Assets | -2.1% | National scope, especially for critical infrastructure run by large utilities | Short term (≤ 2 years) |

| Payback Uncertainty in Small and Mid-Sized Sites With Limited Load Density | -1.5% | Spain-wide, especially in rural and semi-urban commercial sites | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity With Legacy OT and IT Systems

A major challenge in the Spain AI-Powered Energy Management Software Market is the large installed base of older OT, SCADA, and control systems across utilities and industrial sites. These environments were not designed for modern APIs or direct AI integration, so deployments often need middleware, protocol conversion, and long validation cycles. That raises both cost and implementation time, especially for sites with multiple legacy assets and uneven digital readiness. This issue has been highlighted by Spain’s industrial cybersecurity laboratory for strategic energy infrastructure, which reflects how seriously the country is treating the risk posed by OT convergence with newer digital layers.[4]Fundación Ciudad de la Energía, “Joan Groizard Inaugurates the Industrial Cybersecurity Laboratory of CIUDEN and INCIBE to Strengthen Energy Infrastructure,” CIUDEN, ciuden.es The result is that large utilities and multinational operators can often move ahead, while many mid-sized industrial users delay projects until integration risk becomes easier to manage.

Data Quality and Interoperability Gaps Across Metering and Sensor Layers

The Spain AI-Powered Energy Management Software Market also faces a data problem because energy information still comes from multiple metering and sensor systems with varying formats, quality levels, and time intervals. AI models become much less useful when the input data is incomplete, inconsistent, or too slow for real-time decision-making. A 2025 study in Sustainability found that important energy datasets in Spain remain in non-machine-readable formats, limiting the quality and reuse of digital energy information. This issue is especially evident in smaller buildings and secondary industrial sites, where metering is often too coarse for advanced demand-response and load disaggregation. Vendors that can connect directly with DATADIS and automatically clean incoming data are therefore gaining an advantage, as shown by Linkener’s 2025 platform update, which includes direct DATADIS retrieval and automated validation features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Holds the Lead, Services Gain Pace

Software accounted for 66.18% of the Spain AI-Powered Energy Management Software Market in 2025, keeping this segment at the center of customer spending. Buyers continue to prefer software-led solutions because they can combine monitoring, forecasting, DER coordination, and reporting into a single operating layer. This model meets the needs of utilities, industrial groups, and multi-site building operators seeking stronger visibility across dispersed assets. It also supports faster feature updates and easier scaling than hardware-dependent approaches.

The Spain AI-Powered Energy Management Software Market is still seeing faster growth in services, with this segment projected to expand at a CAGR of 22.61% through 2031. Service demand is rising because many deployments now need integration support, AI model maintenance, site onboarding, and managed optimization after the platform goes live. Outcome-based contracts are also becoming more attractive as customers ask vendors to share responsibility for measured savings and system performance. Schneider Electric’s 2025 multi-year initiative to build a next-generation agentic AI ecosystem for sustainability and energy management shows how major suppliers are broadening their revenue focus beyond licenses and into longer service relationships. This shift means service depth is becoming a competitive factor across the Spain AI-Powered Energy Management Software Market, not just an add-on to the initial software sale.

By Deployment Mode: Cloud Leads, Hybrid Builds Faster

Cloud-based deployment held 57.12% of the Spain AI-Powered Energy Management Software Market share in 2025, reflecting its scale, lower upfront costs, and easier remote management. Cloud tools remain attractive for operators with multiple facilities because they simplify updates, enable centralized oversight, and provide access to new AI capabilities. They also align well with digital data sources such as DATADIS, where external connectivity improves the value of continuous analytics. These advantages keep cloud platforms important for commercial buildings, multi-site operators, and mid-sized utilities.

Hybrid deployment is projected to record the fastest CAGR of 22.73% through 2031, indicating that the market is moving toward more flexible architectural choices. This model appeals to utilities and industrial operators that need local control over sensitive operational data while still using cloud analytics, where it adds value. Spain’s NIS2 enforcement environment and broader critical infrastructure requirements are strengthening that preference, because buyers want both performance and local governance. The Spain AI-Powered Energy Management Software Market is, therefore, rewarding vendors that can support edge-plus-cloud deployments rather than a cloud-only approach. That change is important because it shifts the focus to architectural flexibility, cybersecurity fit, and site-specific compliance readiness.

By Application: Demand Optimization Leads, Renewable Forecasting Accelerates

Energy consumption and demand optimization accounted for 24.15% of the Spain AI-Powered Energy Management Software Market size in 2025, making it the broadest revenue base across applications. This segment leads because almost every end user, from office campuses to factories to utilities, can justify spending when the software lowers peak charges and improves daily efficiency. The value is immediate, which makes procurement easier in a market where buyers still closely examine payback. It also creates a stable base for vendors before customers expand into more advanced use cases.

Renewable energy forecasting and integration is projected to grow at a CAGR of 22.84% through 2031, making it the fastest-moving application in the Spain AI-Powered Energy Management Software Market. Spain’s grid now needs better forecasting because solar generation is concentrated around midday, which increases balancing pressure and raises the cost of poor coordination. Smart grid and DER management are also gaining ground as Spain tests flexibility models and distributed asset control through approved pilot work. Asset performance and predictive maintenance are expanding as industrial operators use AI to reduce downtime in electrical systems, especially where interruption costs are high. Energy trading and market intelligence remain a more specialized area, but they are becoming more relevant for prosumers and commercial operators who want to use flexible loads in response to intraday market signals.

By End User: Utilities Hold the Base, Industrial Facilities Advance Fastest

Utilities held 33.19% share of the Spain AI-Powered Energy Management Software Market size in 2025, making them the largest end-user group. Their lead reflects their central role in demand forecasting, grid balancing, asset management, and DER coordination. Utilities also move earlier than most other buyers when national policy and infrastructure investment start to favor digital grid tools. That positioning gives them a strong influence over technology standards and deployment models across the broader market.

Industrial facilities are projected to grow at a CAGR of 22.95% through 2031, making them the fastest-growing end user in the Spain AI-Powered Energy Management Software Market. Factories in Catalonia, the Basque Country, and Andalusia are facing rising electricity costs, carbon reporting obligations, and supply chain pressure from global customers that expect lower emissions intensity. Large energy operators are continuing to invest in the software backbone that supports smarter industrial energy coordination. Commercial buildings remain an important growth area, and building management systems have been shown to reduce energy consumption by up to 25%, supporting wider adoption across hotels, offices, and retail sites. Residential buildings are still the smallest segment, but solar self-consumption and smart home energy tools are keeping them relevant at the edge of future expansion.

Geography Analysis

The Spain AI-Powered Energy Management Software Market size was USD 93.1 million in 2025 and USD 111.8 million in 2026, indicating that demand is already moving beyond early adoption into broader implementation. Spain’s national energy plan, approved through Royal Decree 986/2024, set a large investment path through 2030 and called for 81% of electricity from renewables, 76 GW of solar PV, and 22.5 GW of storage, underscoring the strategic need for intelligent energy software. The same plan requires EUR 308 billion (USD 332.6 billion) in cumulative investment through 2030, with 17% allocated to energy networks and digitalization, which directly supports the operating context for the Spain AI-Powered Energy Management Software Market. Royal Decree-Law 7/2026 widened the scope further through renewable acceleration areas, flexible demand-side connection rules, and sustainability requirements for data centers connected to the grid. Renewables accounted for 55.5% of electricity generation in 2025, which means grid balancing and forecasting needs are now structural rather than temporary in Spain.

Demand inside Spain follows two clear geographic patterns in the Spain AI-Powered Energy Management Software Market. Madrid and Barcelona create strong demand from utility headquarters, financial groups, telecom operators, large offices, and data centers, making them key urban centers for software deployment. Catalonia and the Basque Country stand out on the industrial side because their manufacturing bases make energy optimization and predictive control more valuable at the site level. Andalusia, Castile-La Mancha, and Aragón are more important for renewable forecasting, DER orchestration, and grid software because they carry high renewable penetration and strong generation buildout. Northern regions such as Asturias and Galicia also matter because older industrial assets and legacy grid infrastructure increase the demand for retrofitting digital energy control systems.

The geographic case for the Spain AI-Powered Energy Management Software Market is also reinforced by wider European policy and financing support. The EU network code on cybersecurity for the electricity sector established baseline procurement requirements favoring certified, security-ready software for power infrastructure. Financing commitments are also important, and the European Investment Bank’s September 2025 support for Endesa’s distribution network modernization shows continued confidence in digital grid investment. Academic modeling has also highlighted Spain’s interconnection constraints with France and Portugal, which increase the value of domestic demand flexibility and storage optimization as renewable penetration rises. These factors give the Spain AI-Powered Energy Management Software Market a national growth profile tied to both local operating needs and broader European energy system rules.

Competitive Landscape

The Spain AI-Powered Energy Management Software Market includes a mix of large global automation companies and smaller local specialists, which keeps competition active across utilities, industrial sites, and commercial buildings. Schneider Electric, Siemens, Honeywell, and ABB benefit from broad product portfolios and long-standing customer relationships, especially where buyers want hardware, controls, and software from a small number of suppliers. That bundled approach matters in large projects because it reduces integration risk and simplifies procurement. At the same time, local specialists such as Smarkia, Linkener, and Spacewell Energy compete on Spain-specific integration, faster deployment, and closer alignment with local operating needs. The Spain AI-Powered Energy Management Software Market, therefore, does not favor size alone, because local fit and data connectivity can be just as important as global brand presence.

Several strategic moves show how competition is evolving in the Spanish AI-Powered Energy Management Software Market. Linkener projected revenue above EUR 6 million (USD 6.48 million) for 2025 and launched a new AI-enabled platform version in June 2025 with DATADIS integration and agentic functions, which highlights how local vendors are building around Spanish data access and autonomous optimization. Schneider Electric also announced in 2025 a multi-year initiative to develop a next-generation agentic AI ecosystem for sustainability and energy management, signaling a stronger focus on adaptive workflows and service-led value creation. Edison Next’s October 2025 Ibiza pilot integrated solar generation, storage, and AI-based management in one commercial site, which showed that multi-technology optimization under one software layer is already workable below the utility scale.

White-space opportunity remains visible in mid-market industrial sites and in newer local energy models. Facilities with meaningful electricity use but limited in-house energy teams are still underserved, even though their need for automation is rising. The market also has room for companies that can support prosumers, energy communities, and modular deployment paths as the national flexibility framework matures. Minsait and Naturgy Digital are more closely aligned with Spain’s energy digitalization needs than some overseas billing or consumer engagement platforms that have limited operational relevance in the country. This means the Spain AI-Powered Energy Management Software Market is likely to remain competitive, with no single vendor group fully controlling product design, customer access, or deployment models.

Spain AI-Powered Energy Management Software Industry Leaders

Schneider Electric SE

Siemens AG

Honeywell International Inc.

Johnson Controls International plc

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Fira de Barcelona deployed Sener's AI platform 'Respira' across all 8 pavilions of its Gran Via venue, integrating real-time data from multiple sources to predict and optimize building energy consumption. The deployment targets energy reductions of up to 30%, demonstrating AI energy management viability at large-scale commercial exhibition infrastructure.

- March 2026: Spain published Royal Decree-Law 7/2026, introducing Renewable Acceleration Areas (RAAs) and a flexible demand-side access and connection regime for grid-connected assets. The decree also mandated a royal decree governing energy sustainability and digital sovereignty requirements for data centers connected to Spain's transmission and distribution grids, expanding the regulatory scope for AI energy management software vendors.

- February 2026: Spain's Council of Ministers approved Real Decreto 88/2026, a comprehensive new regulatory framework for electricity supply, commercialization, and aggregation of electrical energy, establishing updated rules for demand aggregators and flexibility service providers that directly shape commercial models for AI demand response platforms.

- February 2026: Schneider Electric launched EcoStruxure Building Activate, a new IoT energy management and automation platform targeting small and medium buildings under 10,000 m², supporting real-time utility data monitoring and automated carbon reduction. The product extends Schneider Electric's commercial reach into the previously underserved small-building segment of Spain's commercial real estate market.

Spain AI-Powered Energy Management Software Market Report Scope

The Spain AI-Powered Energy Management Software market refers to platforms and services that leverage artificial intelligence to optimize energy consumption, enhance asset performance, and enable smarter grid and distributed energy resource (DER) management. These solutions provide advanced capabilities such as predictive maintenance, renewable energy forecasting, demand-side optimization, and market intelligence for energy trading and pricing.

The Spain AI-Powered Energy Management Software market report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Application (Energy Consumption and Demand Optimization, Asset Performance and Predictive Maintenance, Smart Grid and Distributed Energy Resource (DER) Management, Renewable Energy Forecasting and Integration, and Energy Trading, Pricing and Market Intelligence), and End User (Utilities, Commercial Buildings, Industrial Facilities, and Residential Buildings). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance |

| Smart Grid and Distributed Energy Resource (DER) Management |

| Renewable Energy Forecasting and Integration |

| Energy Trading, Pricing and Market Intelligence |

| Utilities |

| Commercial Buildings |

| Industrial Facilities |

| Residential Buildings |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premises | |

| Hybrid | |

| By Application | Energy Consumption and Demand Optimization |

| Asset Performance and Predictive Maintenance | |

| Smart Grid and Distributed Energy Resource (DER) Management | |

| Renewable Energy Forecasting and Integration | |

| Energy Trading, Pricing and Market Intelligence | |

| By End User | Utilities |

| Commercial Buildings | |

| Industrial Facilities | |

| Residential Buildings |

Key Questions Answered in the Report

What is the 2026 value of the Spain AI-powered energy management software space?

It stands at USD 111.8 million in 2026 and is forecast to reach USD 296.9 million by 2031 at a CAGR of 21.57%.

What is driving software adoption across Spain’s energy management platforms?

The main drivers are higher renewable penetration, tighter carbon reporting rules, stronger demand for real-time optimization, and growing use of automated demand response.

Which component category leads spending in Spain?

Software led with a 66.18% share in 2025, while services is projected to grow faster at a 22.61% CAGR through 2031.

Which deployment model is gaining the most momentum?

Hybrid deployment is projected to grow the fastest at a 22.73% CAGR because buyers want cloud analytics with stronger local data control.

Which application area is expanding the fastest?

Renewable energy forecasting and integration is projected to grow at a 22.84% CAGR as Spain’s grid needs better coordination of solar output, storage, and flexible demand.

Which end users are creating the strongest demand?

Utilities remained the largest end-user group with a 33.19% share in 2025, while industrial facilities are projected to grow the fastest at a 22.95% CAGR through 2031.

Page last updated on: