Egypt Molded Case Circuit Breaker Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

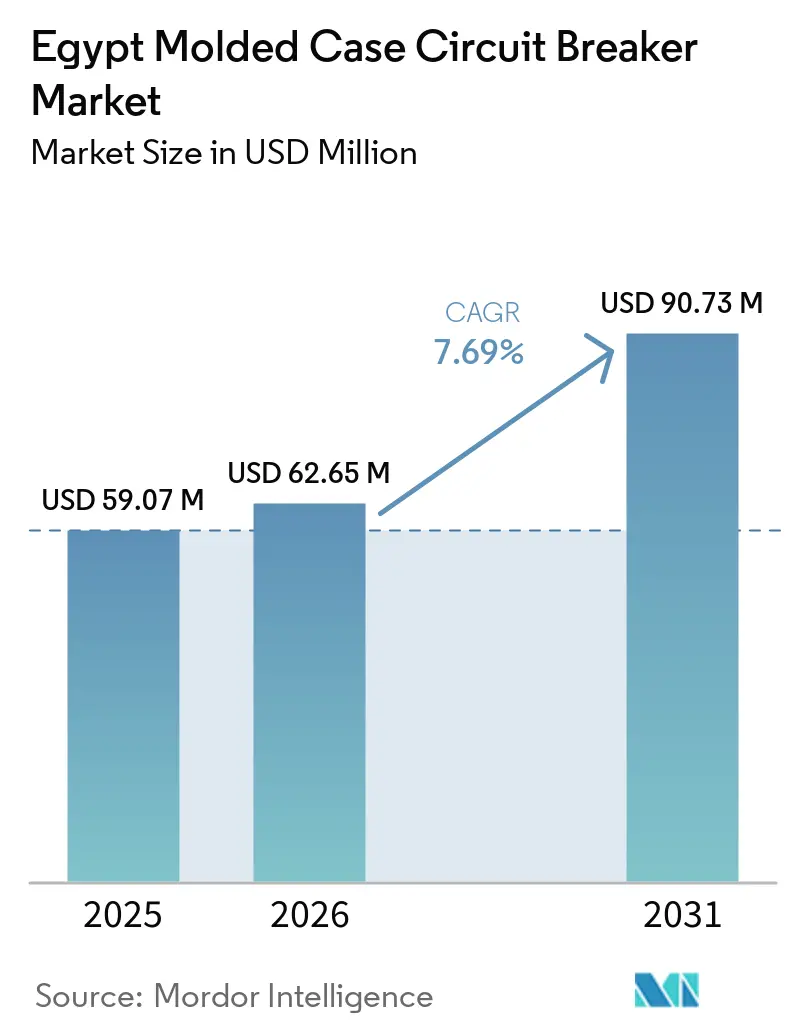

| Base Year Market Size (2025) | USD 59.07 Million |

| Market Size (2026) | USD 62.65 Million |

| Market Size (2031) | USD 90.73 Million |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

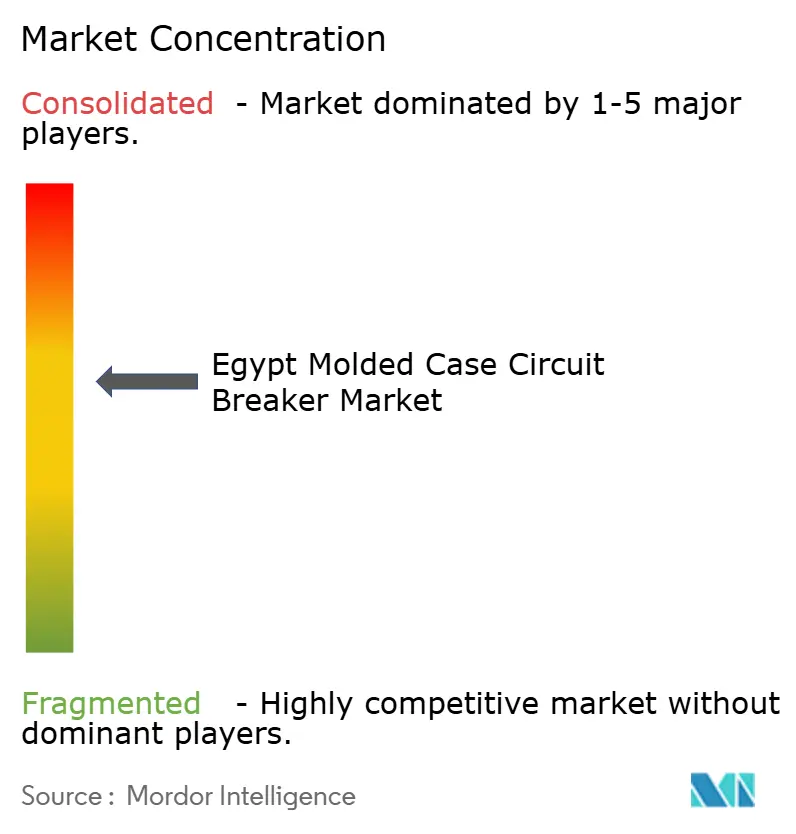

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Molded Case Circuit Breaker Market Analysis by Mordor Intelligence

The Egypt Molded Case Circuit Breaker Market size is expected to grow from USD 59.07 million in 2025 to USD 62.65 million in 2026 and is forecast to reach USD 90.73 million by 2031 at 7.69% CAGR over 2026-2031. The Egypt MCCB market is moving on the back of grid reinforcement, new-city electrification, renewable power integration, and a clear rise in digital infrastructure requirements. Public power projects and planned urban load additions are widening the number of substations, feeder panels, and auxiliary circuits that need low-voltage protection equipment across the country.[1]Source: Engineering Consultants Group, “Infrastructure Facilities for the New Capital City,” Engineering Consultants Group, ecgsa.com Procurement is also shifting toward higher-rated frames and more intelligent trip platforms because larger solar assets, industrial loads, and data center architectures need stronger fault tolerance and better selectivity than standard applications. At the same time, price pressure remains visible in standard ranges, where imported products and contractor margin sensitivity still shape buying decisions. The Egypt MCCB market, therefore, combines volume support from broad construction activity with value support from a gradual move toward higher-frame and digitally enabled protection products.

Key Report Takeaways

- By rated current, the 75 A to 250 A band held 42.6% share of the Egypt MCCB market size in 2025, while above 800 A is forecast to expand at 8.7% CAGR through 2031.

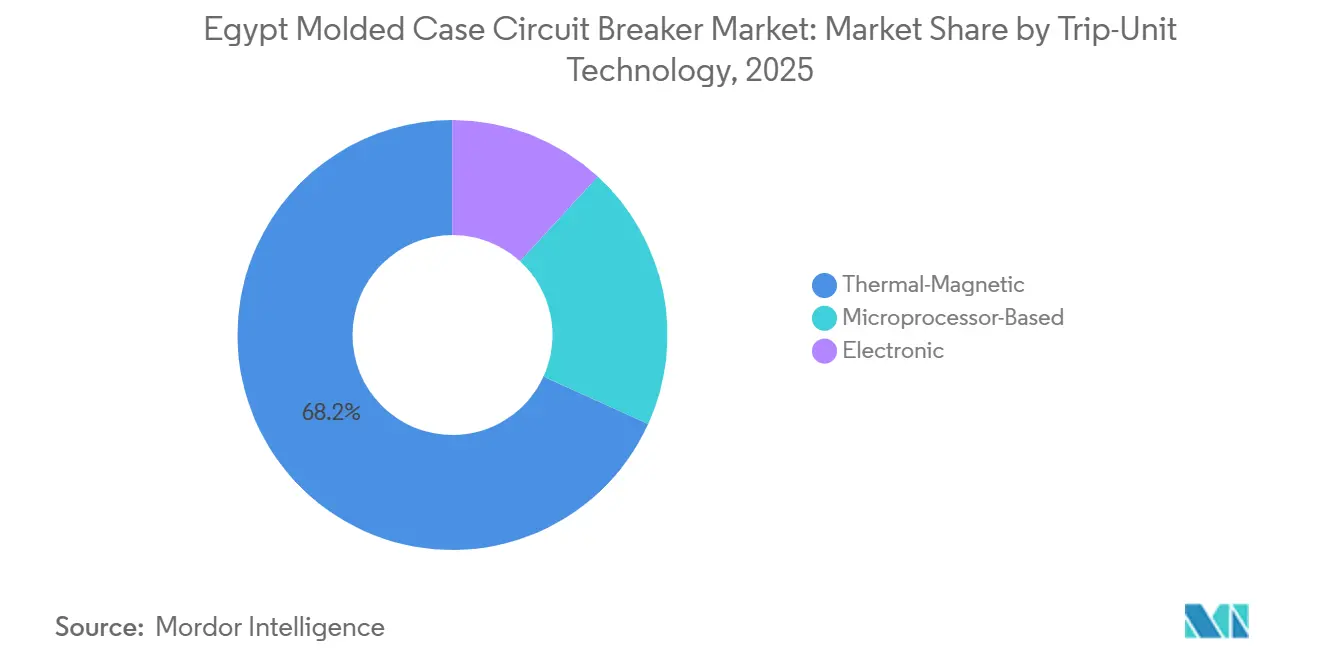

- By trip-unit technology, thermal-magnetic MCCBs held 68.2% of the Egypt MCCB market share in 2025, while microprocessor-based units are projected to grow at 9.1% CAGR through 2031.

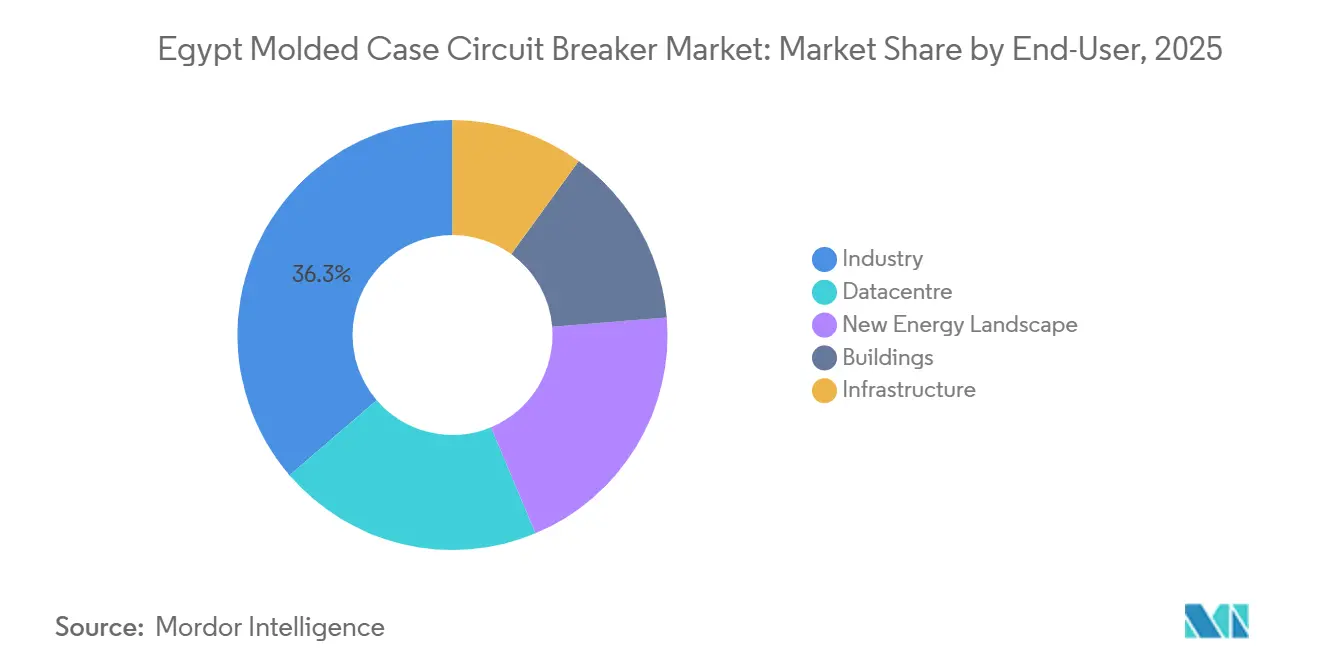

- By end user, industry held 36.3% share of the Egypt MCCB market size in 2025, while data center applications are forecast to advance at 10.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Molded Case Circuit Breaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid Expansion and Substation Upgrades | +2.0% | National, with concentration in Greater Cairo, North Coast, and Upper Egypt corridors | Medium term (2-4 years) |

| New-City and Industrial Construction Pipeline | +1.5% | New Administrative Capital, 10th of Ramadan, 6th of October, Ras El Hekma, New Alamein | Long term (≥ 4 years) |

| Renewable-Energy Integration and Storage-Linked Protection Demand | +1.3% | Upper Egypt solar corridor, including Aswan and Nagaa Hammadi, and Gulf of Suez wind zone | Medium term (2-4 years) |

| Energy-Efficiency and Green-Building Compliance | +0.7% | New cities mandated from January 2026, with Greater Cairo and New Administrative Capital as early adopters | Short term (≤ 2 years) |

| Distribution-Grid Digitalization and Loss-Reduction Retrofits | +0.8% | National, with initial 10-governorate rollout under Egyptian Electricity Holding Company (EEHC) smart-grid activity | Short term (≤ 2 years) |

| Hyperscale and Green Data-Center Load Growth | +1.0% | Greater Cairo, Alexandria, and North Sinai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid Expansion and Substation Upgrades

Grid expansion remains one of the strongest demand supports for the Egypt MCCB market because each new or upgraded substation adds protection needs across feeders, auxiliary panels, and control circuits. The current modernization push is not limited to transmission assets, because distribution grid support and control-center upgrades also widen the installed base for low-voltage switching and protection equipment.[2]Source: CESI, “CESI Signs a Flagship Project to Support Egypt Power Distribution Grids Modernization,” CESI, cesi.it The January 2026 transformer supply contract signed by the Egyptian Electricity Transmission Company (EETC) for multiple electricity regions shows that reinforcement is spread across Cairo, Canal, Alexandria, West Delta, and Central Egypt, rather than being limited to one load pocket.[3]Source: National Media Authority, “المصرية لنقل الكهرباء توقع عقدًا جديدًا لتدعيم الشبكة وتأمين خطة صيف 2026,” Maspero, maspero.eg That national spread matters for the Egypt MCCB market because it supports recurring procurement across both utility-affiliated work and contractor-led panel assembly. It also raises the need for better selectivity at the feeder level, which supports a gradual move from basic protection toward products with greater adjustment and monitoring capability.

New-City and Industrial Construction Pipeline

The new city and industrial buildout is reshaping how demand enters the Egypt MCCB market because the country is adding large, planned load centers rather than relying only on retrofit activity in mature urban districts. Phase 1 of the New Administrative Capital requires 8.3 gigavolt-amperes (GVA) of load through 19 primary high-voltage substations, which creates a deep ladder of protection requirements from primary intake down to secondary and tertiary distribution.[4]Source: Engineering Consultants Group, “Infrastructure Facilities for the New Capital City,” Engineering Consultants Group, ecgsa.com From June 2026, New Cairo, New Damietta, New Alamein, New Mansoura, and the New Administrative Capital are designated as green cities, which strengthens the case for monitored and efficiency-linked protection architectures in new buildings and infrastructure. Industrial load also remains central, because 10th of Ramadan City alone hosts more than 5,000 factories and continues to anchor one of the country’s deepest manufacturing clusters. This combination of planned cities and dense industrial corridors gives the Egypt MCCB market both project-led demand and a more durable replacement cycle once these sites move deeper into operation.

Renewable-Energy Integration and Storage-Linked Protection Demand

Renewable integration is pushing the Egypt MCCB market toward larger frames and tighter performance requirements. Solar and storage projects bring different fault conditions than conventional building loads, especially where battery discharge and photovoltaic reverse current require more precise coordination and stronger interrupting performance. That makes higher-frame MCCBs more relevant in AC output circuits, evacuation infrastructure, and plant-side distribution boards tied to utility-scale renewable assets. It also accelerates the shift away from purely conventional protection choices, because battery-linked systems reward products that can support more refined protection settings and coordination logic. The result is that renewable buildout is not only adding volume to the Egypt MCCB market but also improving the mix toward higher-value configurations.

Hyperscale and Green Data-Center Load Growth

Data center investment is creating a distinct new demand pole inside the Egypt MCCB market because these facilities require larger frame sizes, redundancy, and fast fault clearing. Primary distribution in data centers typically calls for higher-current devices with electronic trip behavior, and that pulls demand away from standard construction-grade products. This matters even when absolute project counts are still limited, because each commissioned facility uses dense power architecture at the main distribution board and critical downstream levels. The user draft points to a pipeline across Greater Cairo, Alexandria, and North Sinai, which suggests that demand is spreading beyond a single metro cluster. As that pipeline turns into orders, the Egypt MCCB market is likely to see stronger growth in the exact product categories that already carry the highest forecast growth rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper, Steel, and Imported Component Cost Volatility | -1.2% | National, with sharper pressure on locally assembled panels that use imported MCCBs | Short term (≤ 2 years) |

| Price Competition from Low-Cost Imports | -0.9% | National, with the strongest effect in the 75 A to 250 A range | Medium term (2-4 years) |

| FX Volatility and Import-Financing Constraints | -1.4% | National, with concentrated impact on importers dependent on USD-denominated procurement | Short term (≤ 2 years) |

| Red Sea Freight Disruptions and Long Component Lead Times | -0.7% | National, with clear impact on imports routed through Suez-linked shipping lanes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FX Volatility and Import-Financing Constraints

FX volatility remains the broadest near-term restraint on the Egypt MCCB market because a large share of products or core components still carry import exposure. When the local currency weakens, land prices rise quickly, while many contractors remain locked into fixed-price project structures that do not fully absorb those increases. Import-financing friction adds to a second layer of pressure because delayed access to trade finance can extend real procurement lead times beyond nominal schedules. That issue becomes more severe in projects with narrow delivery windows, including renewable assets and digital infrastructure builds, where delayed switchgear can slow broader commissioning activity. In practical terms, FX stress can suppress both volume and product quality in the Egypt MCCB market by pushing buyers toward readily available, lower-specification alternatives.

Copper, Steel, and Imported Component Cost Volatility

Raw-material and component cost swings continue to weigh on the Egypt MCCB market, especially for assemblers and panel builders that operate between imported finished devices and locally fabricated enclosures. Copper cost pressure lifts the cost of current-carrying parts and related assemblies, while steel inflation raises the expense of panel structures and supports distribution hardware. These pressures do not hit all suppliers equally, because manufacturers with stronger localization or broader sourcing control can protect margins more effectively than smaller assemblers. Supply chain disruption in Red Sea shipping lanes also adds timing and freight risk for imported electrical equipment and components across the region. This cost imbalance tends to widen the gap between premium brands with operational scale and mid-tier participants that compete mainly on price.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rated Current: High-Frame Demand Reshapes a Mid-Range Market

The 75 A to 250 A band dominated the Egypt MCCB market with a 42.6% share in 2025. Its lead came from the broad mix of commercial buildings, residential blocks, and light-industrial installations that still define a large part of national electrical demand. This range fits feeder and outgoing protection in the types of projects that remain most common across urban Egypt, so its installed base is wide, and replacement demand stays dependable. The Egypt MCCB market, therefore, still rests on a large mid-range volume layer, even as the product mix starts to change. That pattern also explains why price competition is most visible in this brand, where standardization is higher and contractors often compare offers more aggressively.

The above 800 A segment is growing at the fastest pace, with an 8.7% CAGR through 2031, and this is where the Egypt MCCB industry is seeing the clearest shift in value concentration. Demand in this tier is tied to solar evacuation infrastructure, data center primary feeders, and heavy industrial protection duties that require high breaking capacity and stronger coordination. The 250 A to 800 A band remains important as the working middle of the Egypt MCCB market, because it supports industrial panels, infrastructure installations, and larger commercial projects that sit between mass construction and utility-scale applications. Up to 75 A devices continue to serve the residential mass market, but that tier faces the strongest pricing pressure and offers the least room for value expansion. Over time, this split between volume-heavy mid-range demand and faster-growing high-frame demand is likely to shift revenue toward brands that can combine availability, certification, and application support.

By Trip-Unit Technology: Digitalization Erodes the Thermal-Magnetic Incumbent

Thermal-magnetic MCCBs held 68.2% of the Egypt MCCB market share in 2025, which shows how deeply entrenched conventional protection remains. Their lead reflects familiar installation practices, straightforward operation, and a cost profile that still fits residential, commercial, and light-industrial projects. For many contractors, these devices remain the default option where budget control matters more than advanced communication or remote monitoring. That legacy position keeps thermal-magnetic units at the center of the Egypt MCCB market today. It also means change is more likely to happen first in larger or more technically demanding applications, rather than across the full installed base at once.

Microprocessor-based MCCBs are forecast to grow at 9.1% CAGR through 2031, making them the fastest-growing technology segment in the Egypt MCCB market. The shift is linked to grid modernization, monitoring needs, and tighter selectivity requirements in more advanced power architectures. Electronic trip-unit products sit between the low-cost conventional tier and the more advanced microprocessor layer, so they are well placed in renewable and data center specifications where adjustable settings matter. The Egypt MCCB industry is therefore not moving through a sudden replacement cycle, but through a selective upgrade cycle tied to project complexity and performance expectations. This gradual erosion of the thermal-magnetic lead supports higher average selling values without removing the mass-market role of simpler products.

By End User: Industry Anchors the Market While Data Centers Set the Pace

Industry held the largest share of the Egypt MCCB market at 36.3% in 2025. That position reflects the density of manufacturing activity in long-established industrial centers and the continued expansion of factory-linked power distribution infrastructure. 10th of Ramadan City alone hosts more than 5,000 factories, which shows why industrial procurement remains the most stable end-user base for this category. Industrial users support both greenfield demand and replacement demand because older plants also cycle through panel upgrades, motor control changes, and protection replacement over time. This makes industry the deepest demand anchor in the Egypt MCCB market, even when newer applications draw more attention.

Buildings remain the second-largest demand block, supported by residential, commercial, and hospitality projects across Egypt’s main growth corridors. New-city policy is also changing this segment because green-city designation and monitored energy use increase the appeal of smarter protection architectures in new developments. Infrastructure and new energy applications sit in the middle of the Egypt MCCB market, with support from grid reinforcement and renewable interconnection works. Data center demand is smaller by current share, but it is forecast to grow at 10.3% CAGR through 2031, which is the fastest pace among end users. That combination means the Egypt MCCB market will continue to rely on industrial depth for scale, while data centers increasingly influence specification standards and premium product demand.

Geography Analysis

The Egypt MCCB market is a single-country market, so geography analysis centers on where demand is most concentrated inside Egypt rather than across separate national borders. Greater Cairo remains the dominant demand corridor in the Egypt MCCB market because it combines mature urban load, new-city construction, industrial activity, and the country’s deepest contractor and distribution base. The New Administrative Capital is a major part of that concentration, since Phase 1 requires 8.3 GVA of load supplied through 19 primary high-voltage substations. That level of electrical buildout creates demand across primary intake points, secondary distribution, and building-level protection systems. The wider Greater Cairo orbit also includes Badr City, 10th of Ramadan, and 6th of October, which keeps this corridor at the center of both project procurement and after-sales support.

Industrial density strengthens this geography further because the 10th of Ramadan cluster alone supports one of the broadest manufacturing footprints in the country. The Egypt MCCB market is also developing a second strong corridor in Upper Egypt and the adjacent renewable-energy belt, where solar and storage projects are changing the historical map of capital equipment demand. These projects require high-frame protection at the plant level and also support new evacuation and substation infrastructure feeding the national grid. The national transformer supply contract signed in January 2026 shows that reinforcement activity extends across Cairo, Canal, Alexandria, West Delta, and Central Egypt, which helps spread procurement beyond one metropolitan base. As those assets move from construction into operation, the Egypt MCCB market should see a more durable installed base across renewable-linked governorates.

The North Coast is becoming more important as tourism, residential, and utility infrastructure expand around New Alamein, Ras El Hekma, and the East Matrouh area. The East Matrouh 500/220/66/22 kV GIS substation, completed in 2025 as the first 500 kV station on the North Coast, adds a major backbone asset for future downstream distribution demand. The Suez Canal Economic Zone forms another separate demand pocket, driven by industrial, logistics, and port-related electrification. Together, these corridors show that the Egypt MCCB market is moving from a heavily Cairo-centered structure toward a wider multi-corridor pattern, even though Greater Cairo still holds the deepest concentration of demand.

Competitive Landscape

The Egypt MCCB market shows moderate concentration at the premium end and strong fragmentation in standard-specification applications. Schneider Electric, ABB, Siemens, and Eaton are the most visible multinational names in utility-facing and large-industrial procurement because certification, service capability, and project references still matter more than unit price in those tenders. Their position is strongest where buyers need proven compliance, documented performance, and reliable technical support across project execution. That gives leading brands a clear edge in higher-frame, high-breaking-capacity, and digitally enabled portions of the Egypt MCCB market. The same advantage is less secure in standard ranges, where buyers focus more directly on upfront cost.

ABB offers a clear example of premium-tier positioning through its gas-insulated compact switchgear work for the North Cairo Electricity Distribution Company, which strengthens its standing in digital and utility-linked protection environments. That kind of contract matters beyond the immediate equipment supplied, because it supports downstream pull for associated low-voltage protection and reinforces the supplier’s approved-project reputation. Leading international brands are also benefiting from the mix shift inside the Egypt MCCB market, since the fastest-growing demand sits in higher-current and more technically specified applications. Their commercial strength comes from pairing product breadth with engineering support, panel integration, and local distributor or service networks. As project complexity rises, those capabilities become a bigger part of purchasing decisions than they were in purely standard construction tenders.

The lower and mid-specification tiers remain much more contested. Chinese manufacturers such as CHINT, People Electric Appliance Group, NADER Circuit Breaker, and similar players are competing hard on landed price, especially in the 75 A to 250 A range and in value-sensitive panel work. Their role is important because they keep pricing pressure high in the largest-volume layer of the Egypt MCCB market. At the same time, premium suppliers are trying to defend their position by leaning on certification barriers, panel-level compliance expectations, and participation in technically demanding applications where low-cost substitution is harder. The competitive gap is therefore widening between participants that sell mostly on price and those that can combine certification, project support, and higher-performance product portfolios. This leaves the Egypt MCCB market fragmented in overall unit terms, but more concentrated where technical specifications are strict and, procurement risk is high.

Egypt Molded Case Circuit Breaker Industry Leaders

Schneider Electric SE

ABB Ltd.

Siemens AG

Eaton Corp plc

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AIKO has partnered with Infinity Power to supply modules for the 259 MW Nefer Benban solar project in Egypt, featuring 120 MWh battery storage and circuit breaker technology. Expected to power 311,000 homes and cut 349,000 tonnes of CO₂ annually, the project will utilize AIKO’s ABC technology and is set for grid connection by Q4 2026.

- January 2026: Scatec ASA has signed a Power Purchase Agreement (PPA) with the Egyptian Electricity Transmission Company (EETC) for 1.95 GW solar and 3.9 GWh Battery Energy Storage Systems (BESS). The project includes an integrated solar-BESS hybrid system for baseload power, standalone BESS for grid stability, and circuit breaker installations, marking Africa’s largest solar-BESS setup and Scatec’s largest investment.

- December 2025: Infinity Power has started construction on the 200 MW Ras Ghareb wind project in Egypt’s Gulf of Suez. The project, part of Egypt’s renewable energy programme, will power over 300,000 homes, cut 400,000 tons of CO2 annually, and support Infinity Power’s goal of 10 GW renewable capacity in Africa by 2030, supplying 12 million homes.

- December 2025: Egypt and Saudi Arabia will launch the first phase of their electricity interconnection project in January, with a 1,500 MW transmission capacity. The project includes converter stations, subsea cables across the Red Sea, and circuit breakers to ensure system reliability. Egypt’s Minister of Energy, Mahmoud Essmat, announced this during the ninth Al-Ahram Energy Conference.

Egypt Molded Case Circuit Breaker Market Report Scope

A Molded Case Circuit Breaker (MCCB) is an electrical protection device used to prevent damage to circuits caused by overloads, short circuits, and ground faults. Enclosed in a robust, insulated housing, MCCBs are commonly utilized in commercial and industrial applications with higher amperage requirements, supporting currents of up to 2,500 Amps.

The Egypt Molded Case Circuit Breaker Market is segmented into rated current, trip-unit technology, and end-user. By rated current, the market is segmented into up to 75A, 75A–250A, 250A–800A, and above 800A. By trip-unit technology, the market is segmented into thermal-magnetic, electronic, and microprocessor-based trip units. By end-user, the market is segmented into buildings, industry, infrastructure, datacentres, and the new energy landscape. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Upto 75A |

| 75A - 250A |

| 250A - 800A |

| Above 800A |

| Thermal-Magnetic |

| Electronic |

| Microprocessor-Based |

| Buildings |

| Industry |

| Infrastructure |

| Datacentre |

| New Energy Landscape |

| By Rated Current | Upto 75A |

| 75A - 250A | |

| 250A - 800A | |

| Above 800A | |

| By Trip-Unit Technology | Thermal-Magnetic |

| Electronic | |

| Microprocessor-Based | |

| By End User | Buildings |

| Industry | |

| Infrastructure | |

| Datacentre | |

| New Energy Landscape |

Key Questions Answered in the Report

What is the current size of the Egypt MCCB space in 2026?

The Egypt Molded Case Circuit Breaker Market size is expected to grow from USD 59.07 million in 2025 to USD 62.65 million in 2026 and is forecast to reach USD 90.73 million by 2031 at 7.69% CAGR over 2026-2031.

Which rated current segment leads demand in Egypt?

The 75 A to 250 A band led with 42.6% share in 2025 because it serves a wide base of commercial, residential, and light-industrial applications.

Which product category is expanding the fastest through 2031?

Above 800 A MCCBs are forecast to grow at 8.7% CAGR through 2031, supported by solar plants, data center feeders, and heavier industrial loads.

Why are microprocessor-based MCCBs gaining traction in Egypt?

They are growing at 9.1% CAGR because grid modernization, renewable integration, and more selective protection needs favor devices with better control and monitoring.

Which end-user group contributes the most demand today?

Industry led with 36.3% share in 2025, supported by Egypt's deep factory base, including more than 5,000 factories in 10th of Ramadan City.

What are the main risks affecting supplier performance in Egypt?

Foreign exchange (FX) volatility, import-financing constraints, raw-material cost swings, and shipping disruptions remain the main near-term pressures on pricing, lead times, and specification choices.

Page last updated on: