Algeria Molded Case Circuit Breaker Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

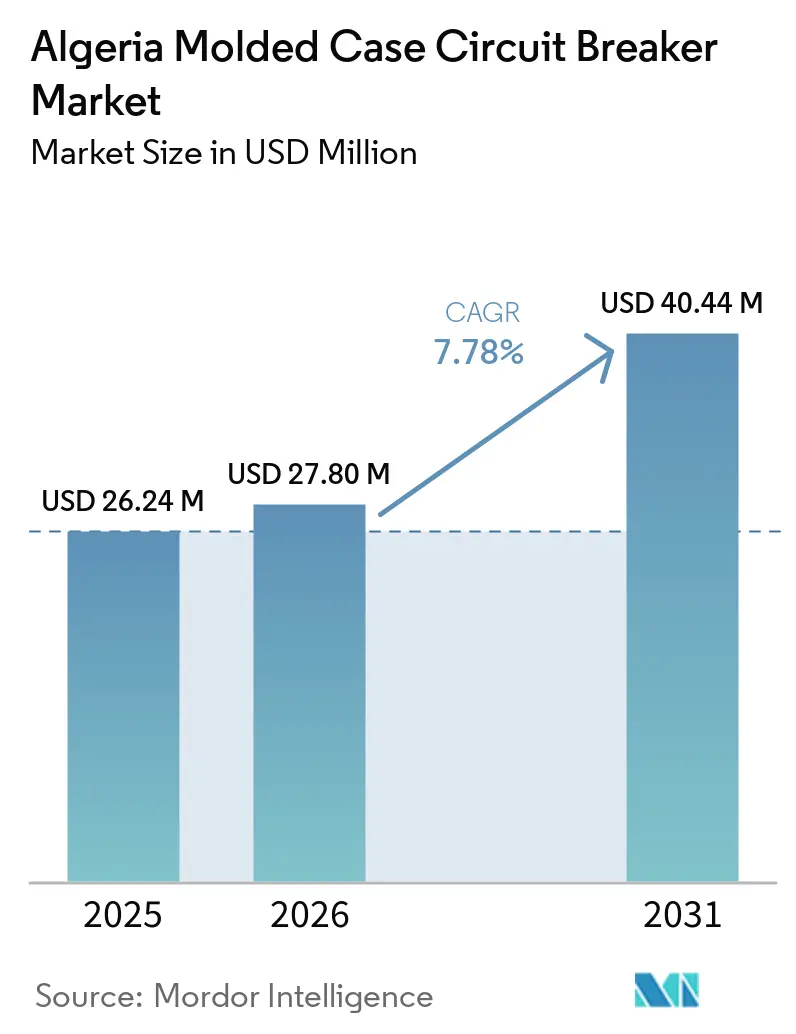

| Base Year Market Size (2025) | USD 26.24 Million |

| Market Size (2026) | USD 27.80 Million |

| Market Size (2031) | USD 40.44 Million |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

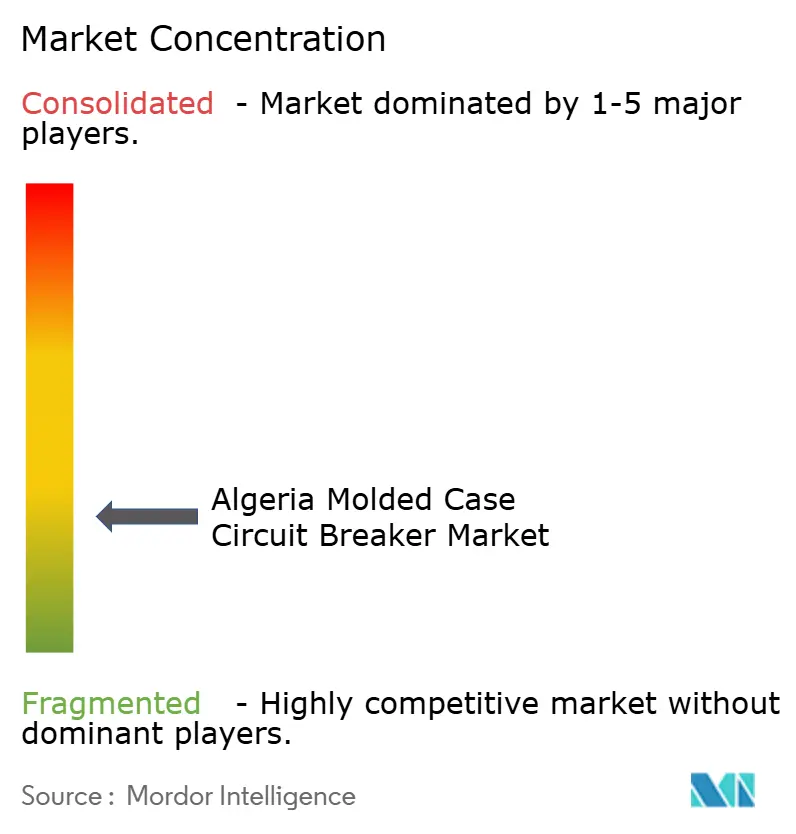

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Molded Case Circuit Breaker Market Analysis by Mordor Intelligence

The Algeria Molded Case Circuit Breaker Market size is expected to grow from USD 26.24 million in 2025 to USD 27.80 million in 2026 and is forecast to reach USD 40.44 million by 2031 at 7.78% CAGR over 2026-2031. The Algeria MCCB market is being supported by a strong cycle of public grid spending, with Sonelgaz having planned DZD 656 billion in 2025, equal to USD 4.84 billion, for network reinforcement, new transmission lines, and substation expansion.[1]Source: Algerie Eco, “Sonelgaz Compte Investir Plus De 650 Milliards De Dinars En 2025,” Algerie Eco, algerie-eco.com Demand is also being lifted by construction activity, as Algeria delivered nearly 450,000 housing units in 2024 and continued to mobilize large housing programs in 2026.[2]Source: Express DZ, “AADL 3, Lancement Des Travaux Pour 73% Des Logements De La 1e Partie Du Programme,” Express DZ, expressdz.dz Algeria’s position as both a major gas producer and an expanding solar developer gives the Algeria MCCB market a broad base of demand across utilities, industry, and new energy installations.[3]Source: pv magazine, “A Turning Point for Algerian Solar,” pv magazine, pv-magazine.com Competition remains split between premium international brands that hold specification strength through International Electrotechnical Commission (IEC) compliance and lower-cost suppliers that gain traction in price-sensitive tenders, while local integration rules are pushing vendors toward partnerships and in-country manufacturing arrangements.[4]Source: Maghreb Émergent, “L'Algérie Mise Sur L'Intégration Industrielle, 50% Minimum, 100% Souhaité,” Maghreb Émergent, maghrebemergent.news Margin pressure still limits the upside because import dependence, volatile metal costs, and aggressive pricing in public procurement continue to shape how distributors and contractors participate in the Algeria MCCB market.

Key Report Takeaways

- By rated current, 75 A-250 A held 41.5% share in 2025, while Above 800 A is forecast to expand at 8.7% CAGR through 2031.

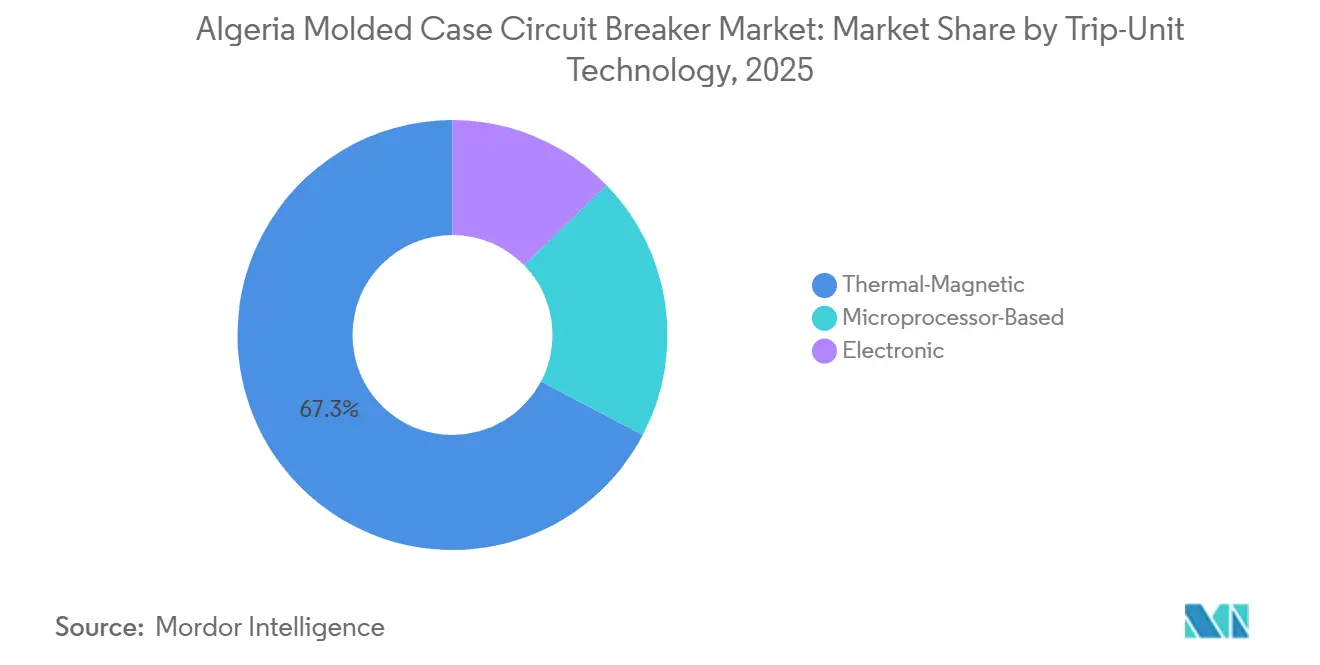

- By trip-unit technology, Thermal-Magnetic held 67.3% share in 2025, while Microprocessor-Based is forecast to expand at 9.2% CAGR through 2031.

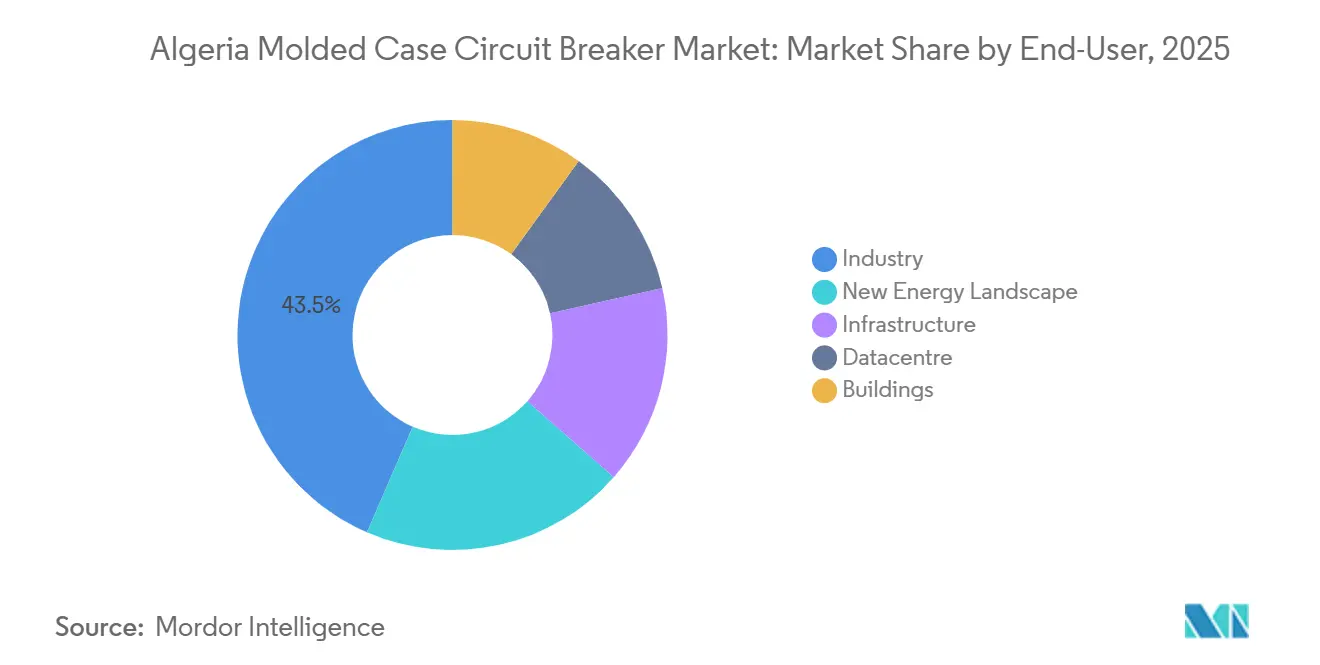

- By end user, Industry held 43.5% share in 2025, while New Energy Landscape is forecast to expand at 10.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Algeria Molded Case Circuit Breaker Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Transmission and Distribution (T&D) networks | +1.8% | National, with stronger pull in southern wilayas and the Algiers to Annaba corridor | Short term (≤ 2 years) |

| Infrastructure-led construction boom | +1.5% | National, with strong activity in Algiers, Oran, Constantine, and new industrial zones | Medium term (2-4 years) |

| Renewable-energy project pipeline growth | +1.4% | National, with concentration in Béchar, Touggourt, Tindouf, Laghouat, and El M'Ghair | Medium term (2-4 years) |

| Stricter energy-efficiency building codes | +0.8% | National, with stronger compliance pressure in Algiers and new urban hubs | Long term (≥ 4 years) |

| Hyperscale data-center build-outs | +0.6% | Oran, Blida, El Mohammedia, with spillover to other large cities | Long term (≥ 4 years) |

| Retrofit switchboard digitalization | +0.9% | National, with stronger activity in Algiers, Oran, and Hassi Messaoud | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of T&D Networks Creates a Structural MCCB Demand Floor

Algeria’s transmission and distribution cycle is at its strongest point in several years, which gives the Algeria MCCB market a stable source of utility demand. In July 2024, GE Vernova secured an order through GE Algeria Turbines SPA to supply high-voltage equipment and grid automation solutions for 134 Sonelgaz substations through 2028. Sonelgaz’s 2025 operating plan also included 35 new high-tension lines across 945 km, 622 medium-voltage transformer stations, and 2,115 km of distribution network, each of which extends low-voltage protection needs at the termination point. The North-South 400 kV interconnection, valued at DZD 200 billion, equal to USD 1.48 billion, is connecting Tamanrasset and Tindouf to the national grid and is widening electrification in the southern part of the country. Because tenders reference IEC 60947-2 through the Algerian compliance framework, the Algeria MCCB market benefits not only from higher project volume but also from a steady need for certified products across distribution tiers.

Infrastructure-Led Construction Boom Multiplies Panel-Level MCCB Installations

Large housing and industrial projects are creating one of the clearest volume channels for the Algeria MCCB market. The Agence Nationale de l'Amélioration et du Développement du Logement 3 (AADL3) rental-purchase program targets 1.4 million dwellings, and 73% of the first 200,000-unit tranche was under active construction as of May 2026. That scale matters because each residential block requires distribution boards and multiple molded case circuit breakers in the mid-current range. The industrial pipeline is also important, with GISB Electric signing a USD 480 million export pact in September 2025, which points to deeper domestic electrical equipment capability around project execution and supply. As these housing, utility, and industrial projects move together, the Algeria MCCB market gains a broad installation base that is less dependent on a single end-use sector.

Renewable-Energy Project Pipeline Unlocks a New Application Tier for High-Current MCCBs

Utility-scale solar is adding a newer and more specialized demand layer to the Algeria MCCB market. Algeria’s 3 GW solar program under Sonelgaz is pushing protection needs from combiner boxes through inverter stages to plant substations, which increases the role of MCCBs in renewable installations. The 362 MW (DC) Hassi Delaa Laghouat project is operational in 2026, and the 80 MW Abadla project in Béchar province began construction in March 2025. Renewable Energy and Energy Efficiency Commission (CEREFE) stated that renewable generation capacity moved past 600 MW by early 2025, up from 437 MW at the end of 2023, which shows that the project pipeline is moving from planning to grid-connected capacity. This shift is favorable for the Algeria MCCB market because higher-current solar applications require stronger breaking performance and support the move toward electronic and microprocessor-based protection.

Stricter Energy-Efficiency Building Codes Accelerate Smart MCCB Specification in New Builds

Energy rules and tariff structures are gradually changing what electrical designers specify in the Algeria MCCB market. Algeria’s DTR C3-2 framework divides the country into 5 climatic zones, which raises the importance of load management and thermal performance in electrical systems, especially in hotter southern areas. Research on housing units in Algiers found that common construction practices remained highly energy-intensive, which supports the case for tighter distribution control and more responsive protection devices. The CREG tariff structure also increases the value of adjustable-trip settings, because developers have more reason to manage loads carefully in new buildings. Over time, this favors the Algeria MCCB market segment that offers monitoring, selectivity, and better operational control rather than basic fixed thermal-magnetic protection alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -1.2% | National, with stronger pressure on Algiers-based importers serving public tenders | Medium term (2-4 years) |

| Commoditization-driven price pressure | -0.9% | National, with stronger impact in the 75 A-250 A range for residential and light industrial use | Medium term (2-4 years) |

| Lengthy IEC and registration cycles | -0.6% | National, with delays concentrated around import registration and approval processes | Medium term (2-4 years) |

| Emergence of solid-state power controllers | -0.4% | Limited to large industrial, renewable, and data-center installations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility Constrains Importer Margins on Fixed-Price Project Contracts

Raw-material volatility remains a practical constraint for the Algeria MCCB market because most supply still depends on imported products and imported components. Copper and aluminum prices have stayed exposed to wide movements, and that matters because they are central to the current-carrying parts inside molded case circuit breakers. This becomes more serious in public tenders, where contractors and distributors often commit to fixed prices long before delivery. When metal costs rise during that window, the ability to protect margins becomes limited in a country without local MCCB manufacturing depth. The result is a more cautious inventory stance, longer lead-time risk, and tighter pricing behavior in the Algeria MCCB market, especially in the fast-moving mid-current bands.

Commoditization Pressure Limits Sustainable Differentiation for Mid-Market Circuit Breaker Products

Price-led competition is another clear restraint on the Algeria MCCB market, especially where products are close substitutes in the 75 A-250 A range. Chinese suppliers have widened their presence by offering IEC-tested products at clear cost advantages over European alternatives, which has weakened sustainable differentiation in value-oriented tenders. This pressure is strongest after the engineering stage, when the purchase decision shifts from specification quality to budget control. The premium zone remains more defensible in renewable energy, heavier industry, and applications that require stronger breaking capacity or advanced trip functions. Even so, the Algeria MCCB market still faces ongoing margin compression in mid-market distribution channels, which limits how much distributors can grow through volume alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rated Current: Mid-Tier Ratings Anchor Volumes While High-Current Bands Accelerate

The 75 A-250 A band held 41.5% of Algeria MCCB market share in 2025, which made it the core volume range across the country. This position reflects the load profile of commercial buildings, AADL housing boards, light industrial facilities, and decentralized panels used across Algeria’s 58 wilayas. The Algeria MCCB market is particularly exposed to this range because it sits at the point where residential-scale protection gives way to larger commercial and industrial applications. The sub-75A tier remains relevant for small installations, but part of that demand is contested by miniature circuit breakers, which limit how much of the protection scope is addressable by MCCBs.

The 250 A-800 A band serves mid-range industrial switchboards, hospital distribution systems, and grid-connection panels for smaller solar sites, which gives the Algeria MCCB market a useful bridge between general construction and heavy industry. The Above 800 A segment of the Algeria MCCB market size is projected to expand at 8.7% CAGR through 2031, which makes it the fastest-growing current band in the forecast period. That growth is tied to refinery, transmission, and steelmaking loads, including the Hassi Messaoud refinery expansion and the Tosyali Oran steel plant’s larger electric arc furnace footprint. Schneider Electric’s EasyPact CVS C4 expansion to 1,600A, launched in Africa in May 2026, also shows that suppliers are now addressing a tier that had a clearer product gap before. Because short-circuit performance requirements are stricter at these ratings, premium suppliers retain stronger pricing power in this part of the Algeria MCCB market.

By Trip-Unit Technology: Thermal-Magnetic Dominance Meets a Digital Disruption Curve

Thermal-Magnetic trip units accounted for 67.3% of Algeria MCCB market share in 2025, which shows how strongly the installed base still favors simple and lower-cost protection. These devices remain attractive in residential, light commercial, and small industrial applications because contractors can install them without complex commissioning. Their operating logic also fits the preferences of panel builders that prioritize reliability and ease of service over digital features. For that reason, the Algeria MCCB market still depends heavily on thermal-magnetic units for mainstream demand.

Electronic trip units serve the middle ground, where selective coordination and better control matter more than the lowest possible upfront price. The Microprocessor-Based segment of the Algeria MCCB market size is projected to expand at 9.2% CAGR through 2031, making it the fastest-growing technology category. Sonelgaz’s Poste de Commande Centralisé program is pushing network supervision toward more connected protection architectures, which increases the value of digital trip units and remote state reporting. ABB’s July 2025 launch of the SACE Emax 3 with IEC 62443 Security Level 2 certification shows how protection devices are moving closer to the cybersecurity and uptime needs of data centers and advanced industrial sites. As the Algeria MCCB market shifts toward monitored switchboards in utilities, critical facilities, and high-value industrial plants, microprocessor-based devices should take a larger role in new specifications and retrofit programs.

By End User: Industry Leads Volumes While New Energy Emerges as the Market’s Long-Run Growth Engine

Industry held 43.5% of the Algeria MCCB market in 2025, which made it the largest end-user group by value. Oil and gas, heavy industry, cement, steel, and emerging manufacturing clusters give this segment a dependable need for switchboard protection and load control. The Algeria MCCB market benefits from this base because industrial investments tend to require larger ratings, stronger compliance, and more recurring replacement demand than standard building installations. Buildings remain a large volume channel, supported by housing programs and commercial construction, but unit values are usually lower than in heavy industrial applications.

Infrastructure demand is tied to transport, utilities, and public projects, including rail-related investment such as Vossloh’s EUR 59 million (equivalent to USD 68 million) contract for rail systems linked to the Ghar Djebilet corridor. Data centers are still small in 2025, but the government-backed AI data center project in Oran shows how critical power environments are beginning to enter the addressable space. New Energy Landscape is projected to grow at 10.4% CAGR through 2031, which is the fastest pace among end users in the Algeria MCCB market. Solar plants, hybrid installations, storage-linked projects, and generator output protection all require protection schemes that go beyond standard building boards. This is why the Algeria MCCB market is likely to see its strongest structural shift at the intersection of industrial electrification and renewable energy deployment.

Geography Analysis

Algeria has a distinct demand profile within North Africa because utility expansion, hydrocarbons, and heavy industry shape purchases more strongly than in markets led mainly by commercial building activity. Sonelgaz planned DZD 656 billion, or USD 4.84 billion, in 2025 for network reinforcement, new transmission lines, and substations, which keeps the Algeria MCCB market closely tied to grid investment. Oran adds industrial weight through steelmaking and related manufacturing, while Hassi Messaoud sustains higher-current protection demand linked to refinery and oilfield assets. This gives the Algeria MCCB market a heavier industrial mix than a standard construction-led profile and supports stronger demand for high-current equipment across utility and process applications.

The northern belt centered on Algiers, Oran, Annaba, and Constantine remains the main installation base for the Algeria MCCB market because it concentrates housing activity, industrial capacity, and new digital infrastructure. Housing construction continues to support this concentration, with 146,640 units already under construction in the first AADL3 tranche as of May 2026. Oran also gained added importance in 2025 and 2026 because the city combines heavy industry with the government-backed AI data center project. This northern corridor therefore continues to generate the country’s broadest volume demand for mid-range commercial and industrial switchboards.

Southern provinces are gaining share of new project activity as solar parks and transmission works move into Béchar, Laghouat, Touggourt, Tindouf, and El M'Ghair. The 80 MW Abadla plant in Béchar and the 362 MWdc Hassi Delaa Laghouat project show how renewable installations are broadening the Algeria MCCB market beyond its historic northern base. The North-South 400 kV interconnection is also extending the grid into Tamanrasset and Tindouf, which supports new switchgear demand across southern substations and local distribution networks. This shift gives Algeria a more balanced geographic demand pattern, with the north driving installation volume and the south adding a rising share of utility-scale and high-current applications. As a result, the next geographic phase of the Algeria MCCB market is likely to come from grid-connected industrial and renewable projects rather than from urban construction alone.

Competitive Landscape

The Algeria MCCB market is fragmented. Schneider Electric, ABB, Siemens, and Eaton dominate the specification tier, serving as the primary reference brands for contractors and utilities. Their stronghold is bolstered by compliance with IEC 60947-2, established distributor relationships, and a deep-seated trust in mission-critical protection applications. New entrants find it challenging to penetrate this segment, as project engineers tend to favor brands with a proven approval history. Conversely, the procurement stage exhibits greater fragmentation than its specification counterpart. This disparity enables lower-cost suppliers to vie for attention, especially when public tenders lean towards price sensitivity post the technical shortlist.

Chinese brands, notably CHINT Group and NADER Electric, have expanded their presence by providing tested products at competitive prices, exerting pressure on premium distributors catering to mid-market applications. However, products with higher currents and digital capabilities resist commoditization in the Algeria MCCB market. Buyers prioritize documentation, fault performance, and after-sales support. Additionally, evolving local integration rules are reshaping the competitive landscape. With the government advocating for heightened domestic integration, suppliers boasting local partnerships or manufacturing ties are poised to strengthen their foothold in public procurement.

Several strategic maneuvers underscore vendor responses in the Algeria MCCB market. In July 2025, Sonelgaz, reflecting the state's broader inclination towards bolstering in-country electrical equipment capabilities, assessed progress with Vijai Electricals on a transformer venture in Azazga. Further cementing this localization trend, Sonelgaz inked a partnership with MATELEC in May 2025 for local transformer fabrication. Schneider Electric's August 2025 debut of the MasterPacT MTZ Active in West Africa holds significance, given its retrofit compatibility with Algeria's legacy switchboards and the nation's utility modernization aspirations. ABB's introduction of the SACE Emax 3 is equally pivotal, aligning with Algeria's shift towards monitored and security-centric protection platforms for data centers and critical infrastructure. Consequently, the Algeria MCCB market is poised to remain a battleground, with trusted global brands at the helm and aggressive price challengers carving out the mid-market space.

Algeria Molded Case Circuit Breaker Industry Leaders

Schneider Electric SE

ABB Ltd.

Siemens AG

Eaton Corp plc

Hager Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Schneider Electric launched the EasyPact CVS C4 MCCB in the African market, bridging the 800A-1,600A product gap in its Easy range. This product directly addresses high-current industrial and utility applications growing across North Africa, with Algeria as a primary addressable market.

- April 2026: ABB revealed the SACE Emax 3 air circuit breaker, the world's first with IEC 62443 Security Level 2 cybersecurity certification, targeting data centres and critical industrial infrastructure. This product enters the Algerian specification cycle as data centre investment accelerates.

- May 2025: Sonelgaz announced its 2025 investment plan of DZD 656 billion, equal to USD 4.84 billion, a 56% increase from the prior year's DZD 420 billion. The plan targets 27,333 MW of generation capacity and includes 35 new high-tension lines spanning 945 km and 622 medium-voltage transformer stations.

- March 2025: Algeria broke ground on an 80 MW solar PV plant in Abadla, Béchar province, developed by Sonelgaz in partnership with China's CWE, with first-phase grid connection expected by January 2026. The facility requires MCCB protection switchgear at the combiner box, inverter, and 30 kV substation levels.

Algeria Molded Case Circuit Breaker Market Report Scope

A Molded Case Circuit Breaker (MCCB) is an electrical protection device used to prevent damage to circuits caused by overloads, short circuits, and ground faults. Enclosed in a robust, insulated housing, MCCBs are commonly utilized in commercial and industrial applications with higher amperage requirements, supporting currents of up to 2,500 Amps.

The Algeria Molded Case Circuit Breaker Market is segmented into rated current, trip-unit technology, end-user, and geography. By rated current, the market is segmented into up to 75A, 75A–250A, 250A–800A, and above 800A. By trip-unit technology, the market is segmented into thermal-magnetic, electronic, and microprocessor-based trip units. By end-user, the market is segmented into buildings, industry, infrastructure, datacentres, and the new energy landscape. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Upto 75 A |

| 75 A - 250 A |

| 250 A - 800 A |

| Above 800 A |

| Thermal-Magnetic |

| Electronic |

| Microprocessor-Based |

| Buildings |

| Industry |

| Infrastructure |

| Data Centre |

| New Energy Landscape |

| By Rated Current | Upto 75 A |

| 75 A - 250 A | |

| 250 A - 800 A | |

| Above 800 A | |

| By Trip-Unit Technology | Thermal-Magnetic |

| Electronic | |

| Microprocessor-Based | |

| By End User | Buildings |

| Industry | |

| Infrastructure | |

| Data Centre | |

| New Energy Landscape |

Key Questions Answered in the Report

What is the projected value of the Algeria molded case circuit breaker business by 2031?

The Algeria Molded Case Circuit Breaker Market size is expected to grow from USD 26.24 million in 2025 to USD 27.80 million in 2026 and is forecast to reach USD 40.44 million by 2031 at 7.78% CAGR over 2026-2031.

Which end-user group generates the highest demand for molded case circuit breakers in Algeria?

Industry is the largest end-user group, holding 43.5% of total market value in 2025 because oil and gas, steel, cement, and manufacturing projects require dependable protection and higher ratings.

Which rated-current segment is the largest in Algeria?

The 75 A-250 A range led the Algeria MCCB market in 2025 with a 41.5% share, supported by housing boards, commercial buildings, and light industrial panels.

What is driving the fastest growth in Algeria's circuit protection demand?

New energy projects are the fastest-growing end-user category at 10.4% CAGR through 2031, while the Above 800 A current band is the fastest-growing rated-current segment at 8.7% CAGR.

Why are digital trip units gaining attention in Algeria?

Microprocessor-based trip units are projected to grow at 9.2% CAGR because utilities, data centers, and critical infrastructure need remote monitoring, better coordination, and stronger operational visibility.

How competitive is supplier participation in Algeria?

The Algeria MCCB market is competitive at the procurement level, with premium global brands holding specification strength while lower-cost suppliers gain traction in price-sensitive tenders.

Page last updated on: