Education Laptop Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.54 Billion |

| Market Size (2031) | USD 29.66 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

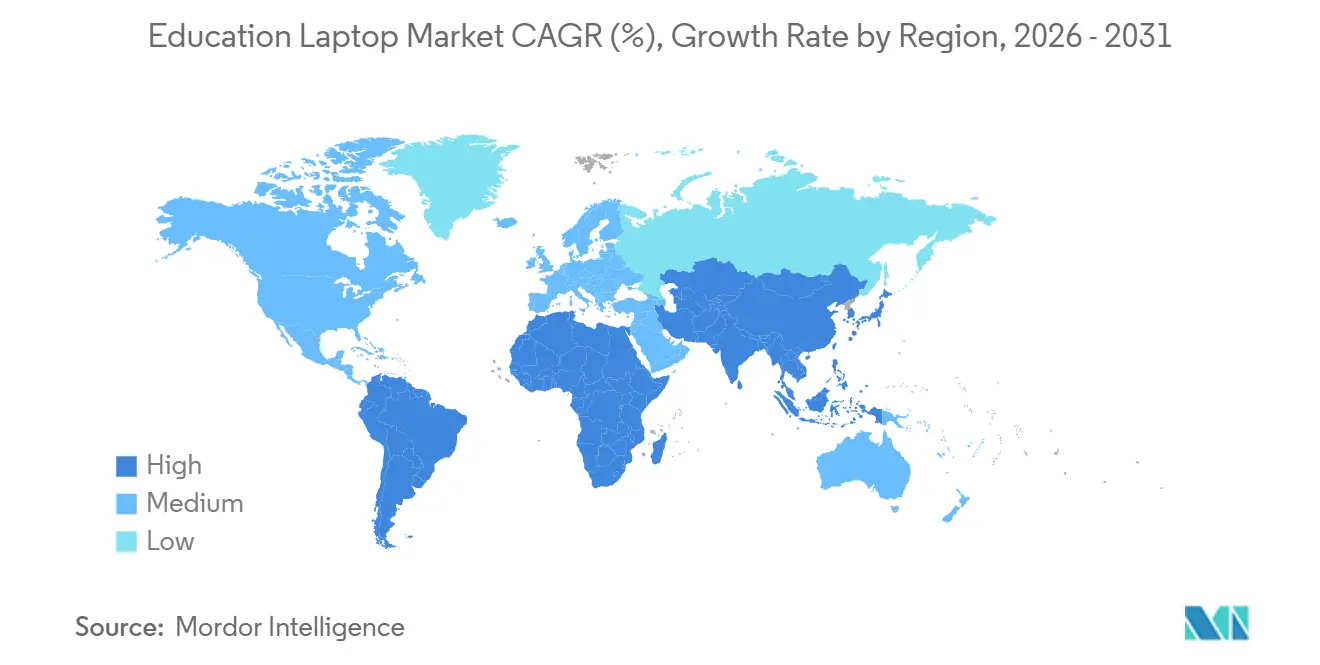

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

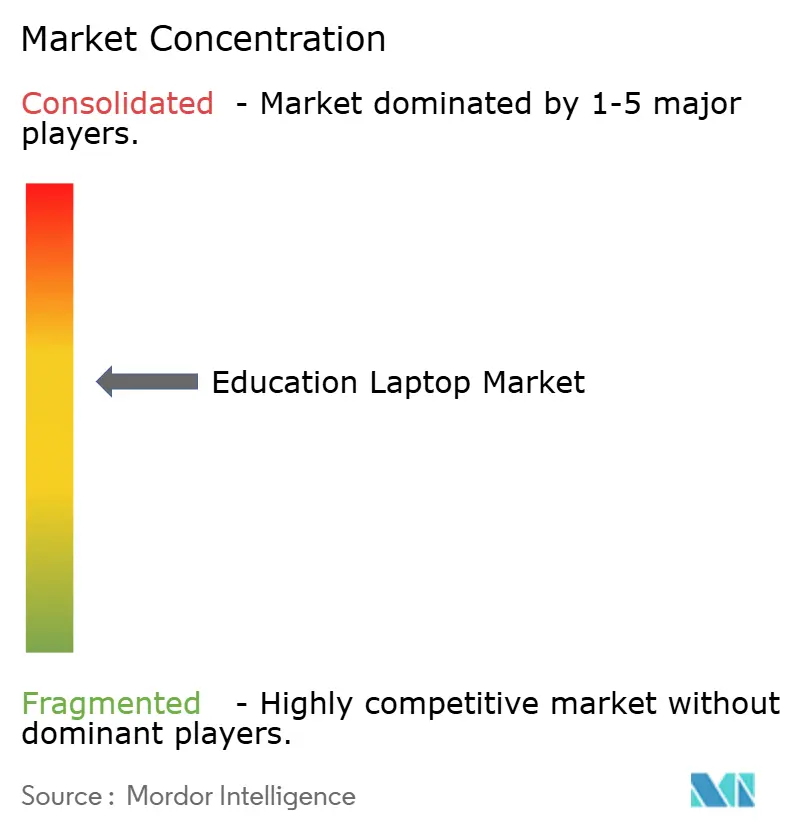

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Education Laptop Market Analysis by Mordor Intelligence

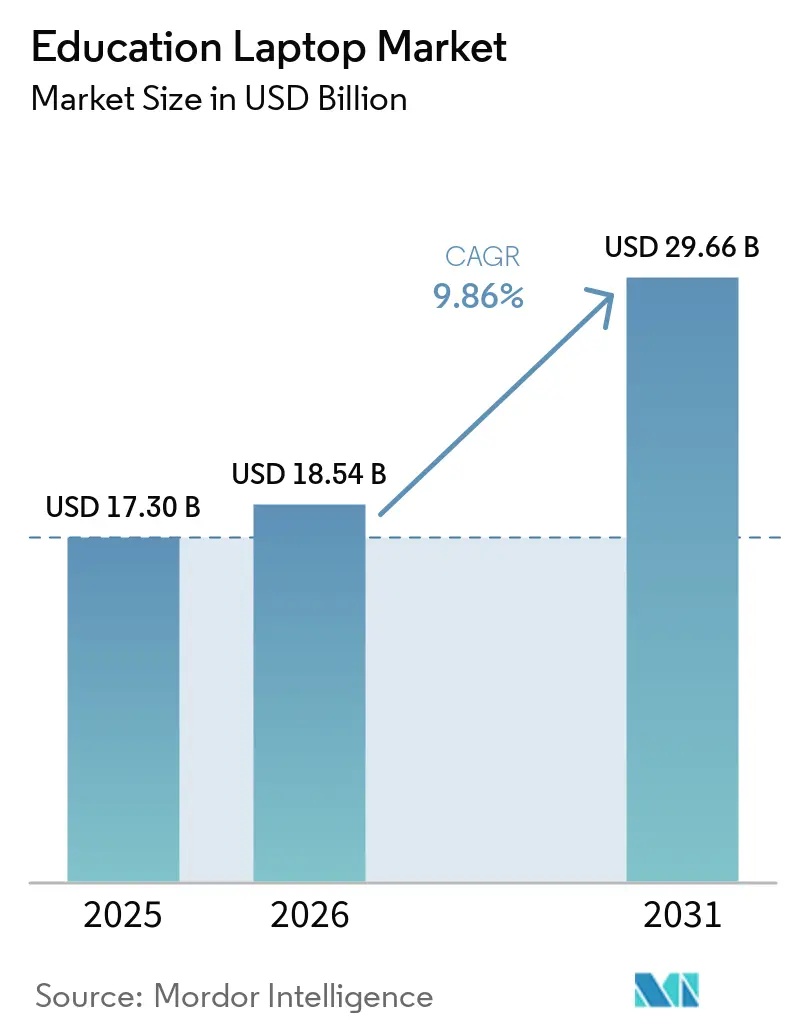

The education laptop market size is expected to be USD 17.30 billion in 2025, USD 18.54 billion in 2026, and reach USD 29.66 billion by 2031, growing at a CAGR of 9.86% from 2026 to 2031. This growth pattern reflects governments reframing device access as critical infrastructure, school districts embracing always-connected instruction, and manufacturers scaling modular designs that cut service downtime. Chrome OS continues to outpace Windows and macOS as administrators choose low-touch fleet management over broad software libraries, while memory and processor shortages temporarily inflate average selling prices. Buyers also weigh total cost of ownership, warranty, repair, and energy consumption, more heavily than headline specifications, a shift that favors vendors offering replaceable components and long-term service contracts. At the same time, data-privacy regulations tighten procurement checklists, driving demand for laptops with embedded encryption, compliant audit logs, and granular access controls.

Key Report Takeaways

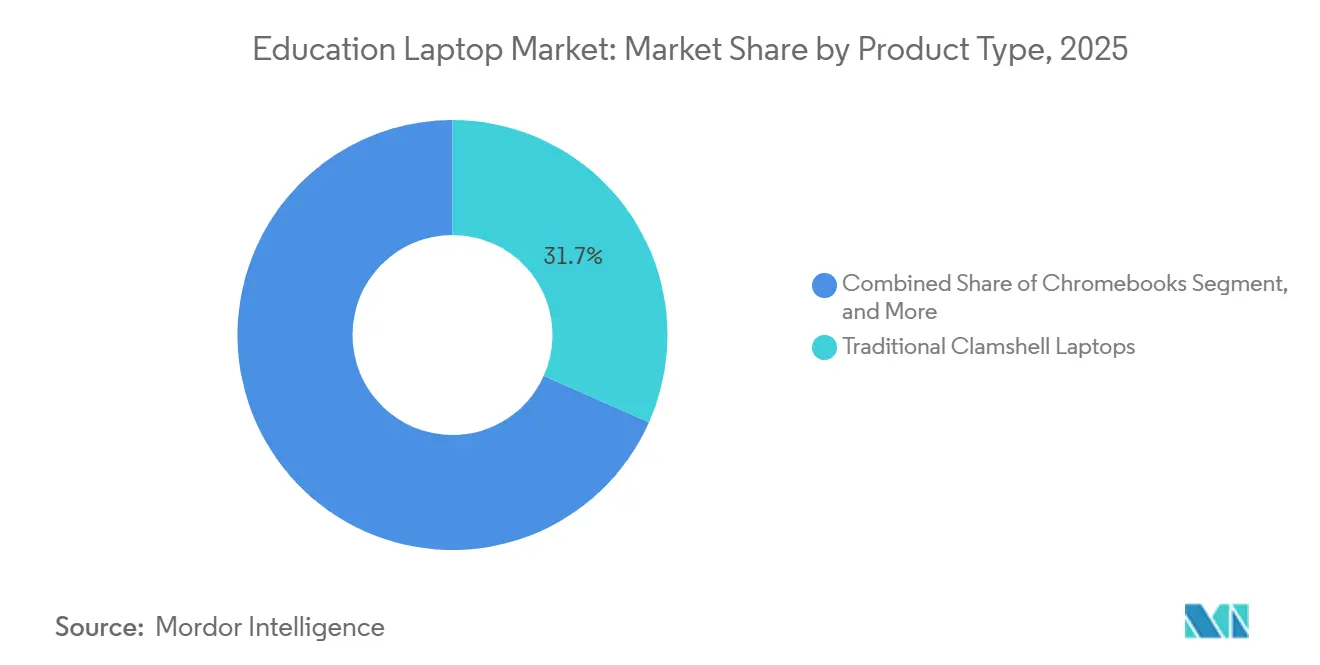

- By product type, 2-in-1 convertibles captured demand previously held by traditional clamshells, expanding at 16.71% CAGR as stylus-driven annotation becomes a core classroom workflow.

- By operating system, Chrome OS led with 38.11% education laptop market share in 2025 and is accelerating at 17.00% annually through 2031, while Windows retains niche strength in vocational institutes that require industry-standard desktop applications.

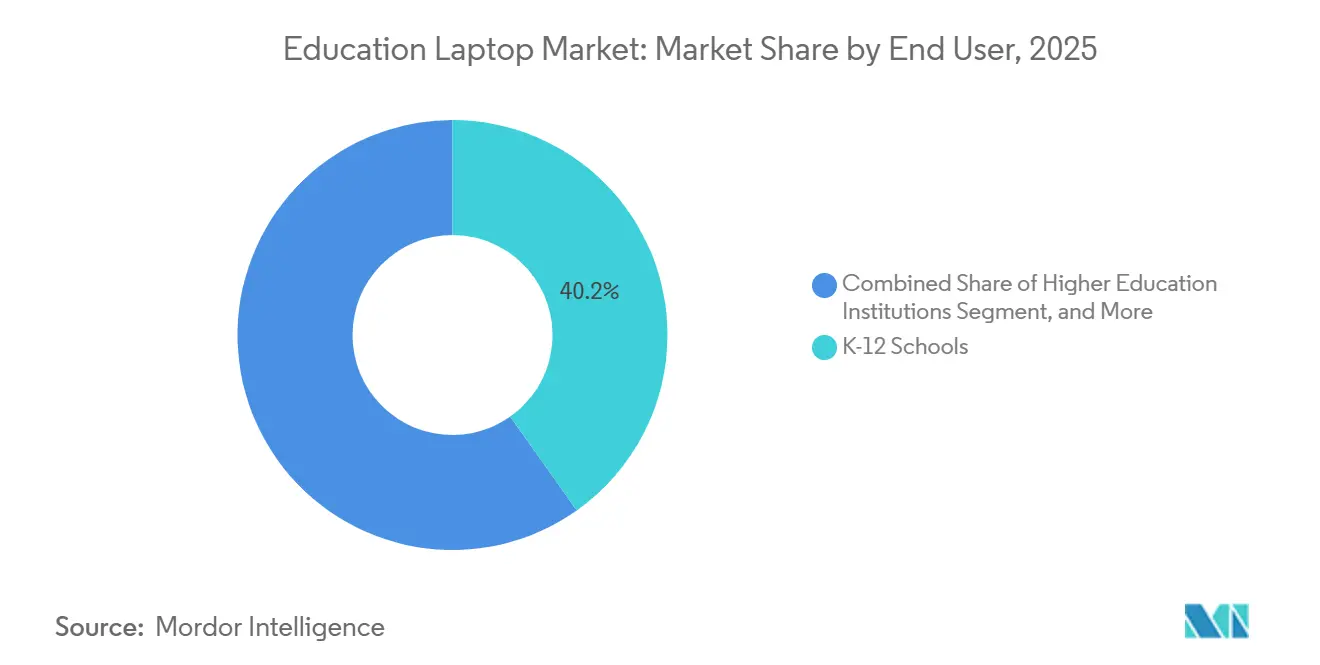

- By end user, higher-education institutions recorded the highest projected CAGR at 15.12% through 2031 as universities dismantle aging desktop labs and roll out bring-your-own-device subsidies.

- By distribution channel, online retail is advancing at 15.67% CAGR as small districts and individual educators bypass formal tenders to secure promotional pricing and rapid delivery.

- By geography, Asia-Pacific is set to expand at a 16.21% CAGR because Japan, India, and China continue funding multi-million-unit refresh cycles, while North America moderates toward steady replacement demand.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Education Laptop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding 1:1 Device Programs in K-12 Schools | +2.1% | Global, strongest in North America, Europe, Asia-Pacific urban areas | Medium term (2-4 years) |

| Government Digital Learning Initiatives | +1.8% | India, Japan, Germany, Nigeria, UAE | Long term (≥ 4 years) |

| Rising Availability of Low-Cost Chromebooks | +1.5% | Price-sensitive markets across Asia-Pacific, South America, Africa | Short term (≤ 2 years) |

| Surge in Hybrid and Distance-Learning Models | +1.3% | North America, Europe, selected Asia-Pacific markets | Medium term (2-4 years) |

| Growing Demand for AI-Ready Edge-Computing Laptops | +0.9% | Early adoption in North America and Europe | Long term (≥ 4 years) |

| Procurement Preferences for Repairable Modular Designs | +0.7% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Digital Learning Initiatives

Multi-year public-sector funding frames hardware and connectivity as universal rights, enabling predictable purchase cycles. Japan’s Next GIGA refresh funds 8 million replacements and channels 60% of orders toward Chrome OS to cut administrative labor. Germany’s Digital Pact 2.0 commits EUR 5 billion (USD 5.65 billion) through 2030 and rings-fences EUR 250 million (USD 282.5 million) for adaptive-learning research. India’s Free Laptop Yojana distributed more than 1 million laptops in Tamil Nadu under a INR 2,000 crore (USD 240 million) line item. Nigeria’s Digital Literacy Network schedules 47 million units and builds local assembly hubs to bypass import tariffs. Such programs convert episodic buying into rolling annual allocations that vendors can forecast with confidence.

Expanding 1:1 Device Programs in K-12 Schools

Surveys show 93% of United States districts planned Chromebook purchases in 2025, pushing the global installed base beyond 38 million. New York City issued 350,000 units to guarantee every grade 3-12 student a personal device. Tokyo’s joint tender pooled 23 wards, saving ¥8.06 billion (USD 54.5 million) through consolidated logistics. These deployments normalize device-per-student ratios and shift competition toward warranty length, spare-device pools, and recycling schemes.

Rising Availability of Low-Cost Chromebooks

Chrome OS shipments reached 22.11 million units and 60.1% education-sector volume in 2025 as cloud storage shaved hardware bills. Acer’s Chromebook 311 line hit USD 499.99 retail in March 2026, balancing power and price for cash-strapped buyers. DRAM shortages spiked module costs 700-800%, eroding headline savings and encouraging designs with user-swappable memory that defers upgrades until prices stabilize. Lifecycle flexibility, not absolute entry price, is emerging as the new affordability metric.

Surge in Hybrid and Distance-Learning Models

Hybrid instruction persists because it lowers absenteeism and supports differentiated pacing. Microsoft’s Elevate for Educators trained 50,000 teachers on AI-assisted lesson plans, and its Learning Zone hosts 2.3 million monthly actives.[1]Microsoft Corporation, “Education Solutions,” microsoft.com Dell’s Pro Education series integrates 1080p cameras and dual-array mics, tailoring hardware to video-centric classes. Universities such as Temple lend devices or sell discounted models to bridge equity gaps. Specifications once viewed as premium, 1080p webcams, WiFi 7, are fast becoming baseline.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget Constraints in Developing-World School Districts | -1.2% | South America, Africa, rural Asia-Pacific | Short term (≤ 2 years) |

| Component Supply-Chain Volatility and Price Spikes | -0.9% | Global, acute where spot purchasing dominates | Short term (≤ 2 years) |

| Device Saturation in Mature Education Markets | -0.6% | North America, Western Europe | Medium term (2-4 years) |

| Data-Privacy Compliance Costs for Student Devices | -0.5% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints in Developing-World School Districts

Fiscal ceilings anchor device rollouts to grants or donor aid rather than recurring budgets. Lesotho accepted 400 UAE-funded laptops in 2025, underscoring dependence on external finance. Currency swings and tariff disputes delay Nigeria’s low-cost imports by up to nine months. Refurbished fleets, priced 40-50% below new, gain traction as 38 million Chromebooks approach end-of-life between 2026 and 2028. Vendors courting these regions adopt lease-to-own models and accept thinner margins to secure volume.

Component Supply-Chain Volatility and Price Spikes

Late-2024 DRAM shortages linger, lifting 8 GB module prices seven-to-eight-fold and stretching lead times to 16 weeks. Education buyers locked into multi-year specifications face 15-20% budget overruns or must accept downgraded builds. Lenovo countered with Chromebook 100e/500e designs featuring customer-replaceable memory, letting schools deploy baseline systems now and upgrade later. Dual-sourcing and modularity are fast becoming competitive prerequisites.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Convertibles Emerge as the Classroom Standard

2-in-1 convertibles accelerated at a 16.71% CAGR through 2031 as teachers lean on stylus annotation for interactive whiteboarding. In 2025, traditional clamshells still accounted for 31.66% of shipments within the education laptop market, mainly because non-touch panels remain cheaper to procure. Chromebooks dominate the low-cost clamshell tier, while rugged laptops with MIL-STD-810H ratings serve vocational courses that expose devices to dust and drops. Dell’s Pro Education 11 and 14 reinforced hinges to survive 30,000 open-close cycles, tackling the 5-7% yearly breakage common in K-12 fleets.

Convertibles increasingly blend touch, pen, and 360-degree hinges into a single configuration that suits both note-taking and group work. ASUS’s BR and CR Chromebook lines launch hot-swap keyboards and tool-less battery modules, cutting service desk wait times. Framework’s Laptop 12 scored a perfect repairability rating but its USD 1,199 entry price limits adoption to sustainability pilots. Over the forecast horizon, the education laptop market size for convertibles is projected to keep outpacing clamshells as curriculum developers embed pen-first activities, while ruggedized builds defend niche workloads that justify premium pricing.

By Operating System: Chrome OS Sustains Its Lead

Chrome OS held 38.11% share of the education laptop market in 2025, expanding at a 17.00% CAGR because zero-touch enrollment slashes IT labor. Windows persists in institutes that need AutoCAD, Adobe, and full Office suites, yet its share erodes as cloud alternatives gain parity. macOS maintains a loyal base in creative arts faculties, while Linux caters to coding bootcamps. Tokyo’s aggregated order showed a 40% administration cost reduction for Chrome OS versus Windows, freeing JPY 8.06 billion (USD 54.5 million) for other priorities.

The education laptop market size tied to Chrome OS is poised to move beyond entry-level hardware. Lenovo’s Chromebook Plus 14 integrates a MediaTek Kompanio Ultra 910 NPU rated at 50 TOPS, enabling on-device inference that historically demanded Windows devices.[2]Lenovo Group, “Education Technology Solutions,” lenovo.com Microsoft counters by bundling Copilot with Windows 11 Education SKUs, pitching AI lesson planning and real-time transcription. Operating-system preference is therefore shorthand for total cost of ownership, security posture, and AI readiness.

By End User: Higher Education Outpaces K-12 Expansion

K-12 still produced 40.19% of 2025 shipments, but universities post the strongest forward momentum at 15.12% CAGR. Campus IT groups are phasing out fixed labs, channeling funds into loaner pools and subsidized personal ownership. The University of North Carolina standardized on Lenovo ThinkPad L13 models with Intel vPro for remote management, embedding support costs into tuition. SUNY Fredonia’s four-year lease-to-own structure folds hardware into semester billing, smoothing affordability.

Higher education’s appetite leans toward mid-spec devices that balance battery life and weight, rather than rugged shells optimized for grade-school abuse. Engineering programs still specify Windows units with discrete GPUs, but liberal-arts faculties accept Chromebooks paired with virtual desktop infrastructure. The education laptop market share for higher education is therefore expected to widen as institutions couple device initiatives with hybrid lecture capture and cloud render farms that de-emphasize local horsepower.

By Distribution Channel: Digital Procurement Accelerates

Offline contracts claimed 55.22% of the education laptop market in 2025 because large districts require site surveys, staging, and on-premise warranty support. Online retail, though, is climbing at 15.67% CAGR. Amazon Business and CDW-G integrate with procurement cards and tax-exempt workflows, allowing sub-500-student schools to finalize orders in days instead of months. ACT Australia’s 8,500-unit ASUS Chromebook award illustrates how tenders still gravitate toward resellers that guarantee local repair depots.

Acer’s direct-to-consumer Chromebook 311 launch gives teachers and small academies immediate access to classroom-ready laptops without negotiating minimum quantities. Hybrid buying journeys are common: districts research SKUs online, obtain quotes through resellers, then loop back to ecommerce to fill accessory gaps. Online’s rising slice signals that the education laptop market will mirror consumer retail patterns, albeit tempered by audit trails and compliance checkpoints unique to public procurement.

Geography Analysis

North America contributed 36.27% of 2025 revenue, buoyed by the Emergency Connectivity Fund and E-Rate extensions that reimbursed USD 7.17 billion in connectivity and devices. Replacement cycles are now lengthening because most districts achieved 1:1 parity, pivoting budgets toward cybersecurity software and teacher professional development. The education laptop market size in the region therefore tracks refurbishment and AI-ready refreshes rather than raw unit expansion.

Asia-Pacific is the fastest growing at a 16.21% CAGR. Japan’s Next GIGA refresh, India’s multi-state Free Laptop Yojanas, and China’s vocational-training mandates combine into multi-million-unit pipelines. Tokyo’s consolidated tender saved ¥8.06 billion (USD 54.5 million) through joint logistics, demonstrating that administrative reforms can free capital for higher-spec models.

Europe advances on the back of Germany’s EUR 5 billion (USD 5.65 billion) Digital Pact 2.0, the United Kingdom’s GBP 325 million (USD 412 million) Connect the Classroom, and Belgium’s EUR 176 million (USD 199 million) Digiplan. GDPR compliance adds 10-15% to lifecycle cost, channeling demand toward vendors offering encrypted storage and data-processing agreements.[3]European Commission, “General Data Protection Regulation,” ec.europa.eu

South America and Africa lag on per-capita spend yet stage blockbuster orders when funding aligns. Nigeria’s 47-million-device roadmap and the UAE’s 46,888-unit rollout highlight how oil revenues and development loans can fast-track digital equity. Saudi Arabia’s USD 2 billion Lenovo-Alat plant, opening late 2026, aims to localize 500,000 units a year and trim import duties. Regional growth therefore hinges on policy resolve more than household purchasing power.

Competitive Landscape

HP, Lenovo, Dell, and Acer capture roughly 60% of shipments, signaling moderately concentrated competition. They lock in share through operating-system alliances, Google with Chrome OS, Microsoft with Windows 11 Education, while investing in neural-processing units and WiFi 7 to future-proof classrooms. Framework positions modularity and a 10-out-of-10 iFixit rating to attract sustainability-minded buyers. ASUS integrates tool-less keyboards and batteries to cut downtime.

White-box assemblers undercut global brands by 20-30% in Africa and parts of Asia, but must now budget for FERPA and GDPR compliance tooling that inflates entry costs. Refurbishment specialists target the 38 million Chromebooks reaching end-of-life by 2028, offering NIST SP 800-88 certified data sanitation and resale into price-sensitive districts. Competitive intensity therefore pivots on lifecycle cost management, regulatory adherence, and in-country service footprints rather than sheer hardware specs.

Education Laptop Industry Leaders

HP Inc.

Lenovo Group Limited

Dell Technologies Inc.

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ASUS introduced the CZ and CR Chromebook series with MIL-STD-810H durability, WiFi 7, and modular keyboards, aiming to minimize field failures in large K-12 fleets.

- March 2026: Acer launched Chromebook 311 C725, C725T, and Spin 311 R725T at USD 499.99, USD 549.99, and USD 579.99, placing MediaTek Kompanio 540 processors into budget-friendly SKUs.

- February 2026: Dell unveiled Pro Education 11 and Pro Education 14 featuring 1080p webcams, dual-array microphones, reinforced hinges, and optional Gorilla Glass touch panels.

- January 2026: ACT Australia awarded ASUS an 8,500-unit Chromebook supply contract focused on rapid delivery and local repair capabilities.

Global Education Laptop Market Report Scope

The Education Laptop Market caters to K-12 schools, higher education institutions, vocational centers, and government-funded programs, offering laptops, Chromebooks, and convertible devices. Demand centers on affordable, durable, and manageable devices that facilitate digital learning and online assessments. Growth is spurred by government digital-classroom initiatives, cloud learning platforms, and the rising trend of 1:1 student devices. Chromebooks, favored for their affordability and centralized management, lead in several regions, especially K-12 settings.

The Education Laptop Market Report is Segmented by Product Type (Traditional Clamshell Laptops, 2-in-1 Convertible Laptops, Chromebooks, Rugged Laptops, and Other Product Types), Operating System (Windows, Chrome OS, macOS, Linux, and Other Operating Systems), End User (K-12 Schools, Higher Education Institutions, Vocational and Technical Institutes, Corporate Training Centers, Government Educational Programs, and Other End Users), Distribution Channel (Online Retail, and Offline Retail), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Traditional Clamshell Laptops |

| 2-in-1 Convertible Laptops |

| Chromebooks |

| Rugged Laptops |

| Other Product Types |

| Windows |

| Chrome OS |

| macOS |

| Linux |

| Other Operating Systems |

| K-12 Schools |

| Higher Education Institutions |

| Vocational and Technical Institutes |

| Corporate Training Centers |

| Government Educational Programs |

| Other End Users |

| Online Retail |

| Offline Retail |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Type | Traditional Clamshell Laptops | |

| 2-in-1 Convertible Laptops | ||

| Chromebooks | ||

| Rugged Laptops | ||

| Other Product Types | ||

| By Operating System | Windows | |

| Chrome OS | ||

| macOS | ||

| Linux | ||

| Other Operating Systems | ||

| By End User | K-12 Schools | |

| Higher Education Institutions | ||

| Vocational and Technical Institutes | ||

| Corporate Training Centers | ||

| Government Educational Programs | ||

| Other End Users | ||

| By Distribution Channel | Online Retail | |

| Offline Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current education laptop market size and growth outlook?

The education laptop market size stands at USD 18.54 billion in 2026 and is forecast to reach USD 29.66 billion by 2031, advancing at a 9.86% CAGR over 2026-2031.

Which product type is expanding fastest in classroom deployments?

2-in-1 convertibles lead growth at a 16.71% CAGR as teachers prioritize stylus-based annotation and flexible tablet-laptop modes.

Why is Chrome OS gaining education laptop market share?

Administrators favor Chrome OS for zero-touch enrollment, centralized policy control, and lower management overhead, helping the platform climb to 38.11% share in 2025.

How are supply-chain shortages affecting device procurement?

Ongoing DRAM shortages push component prices up seven-to-eight-fold, forcing districts either to accept lower specifications or pay 15-20% premiums, though modular designs with user-replaceable memory mitigate the impact.

Which region will contribute most to future education laptop market growth?

Asia-Pacific is projected to advance at a 16.21% CAGR, driven by multi-million-unit government programs in Japan, India, and China.

Page last updated on: