Student Information System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.7 Billion |

| Market Size (2031) | USD 34.97 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

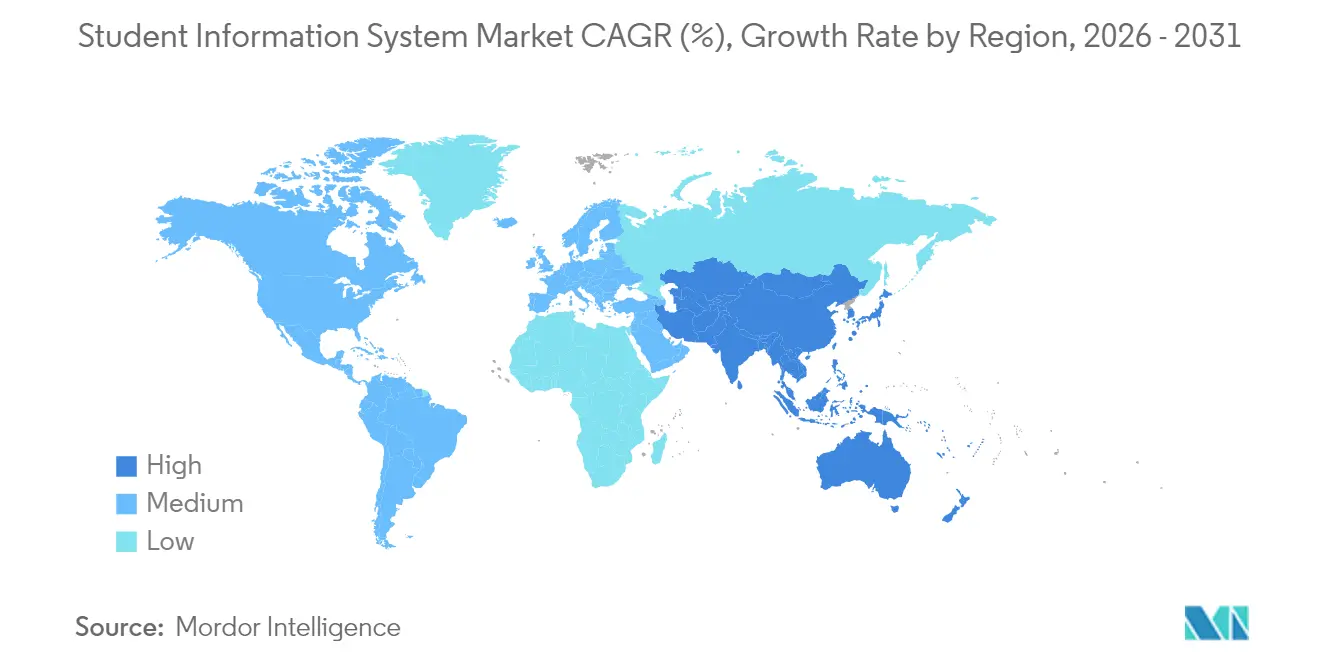

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

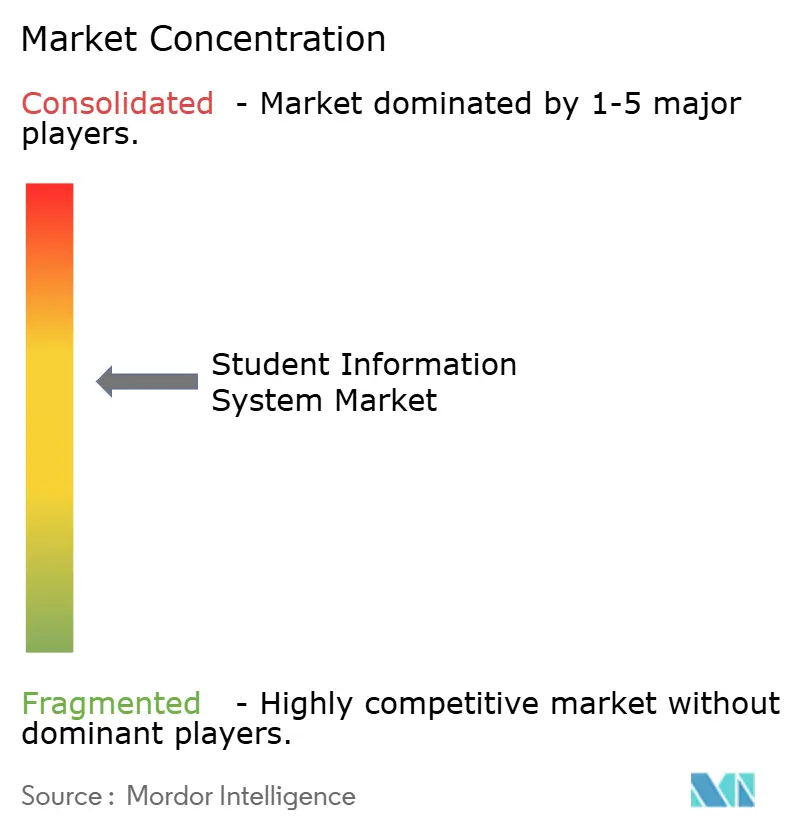

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Student Information System Market Analysis by Mordor Intelligence

The Student Information System Market size was valued at USD 15.44 billion in 2025 and estimated to grow from USD 17.7 billion in 2026 to reach USD 34.97 billion by 2031, at a CAGR of 14.62% during the forecast period (2026-2031). Intensifying cloud-first mandates, growing demand for unified data ecosystems, and heightened compliance requirements are the primary forces propelling this market. Private-equity activity underscores the segment’s attractiveness, with Bain Capital acquiring PowerSchool for USD 5.6 billion and KKR purchasing Instructure for USD 4.8 billion, signalling confidence in long-term fundamentals. [1]Bain Capital, “PowerSchool to be Acquired by Bain Capital in $5.6 Billion Transaction,” baincapital.com Platform vendors continue to consolidate smaller regional players to capture institutional wallet share, while AI-driven analytics differentiate product roadmaps. Institutions are prioritising platforms that embed predictive retention capabilities, streamline regulatory reporting, and integrate seamlessly with the broader EdTech stack.

Key Report Takeaways

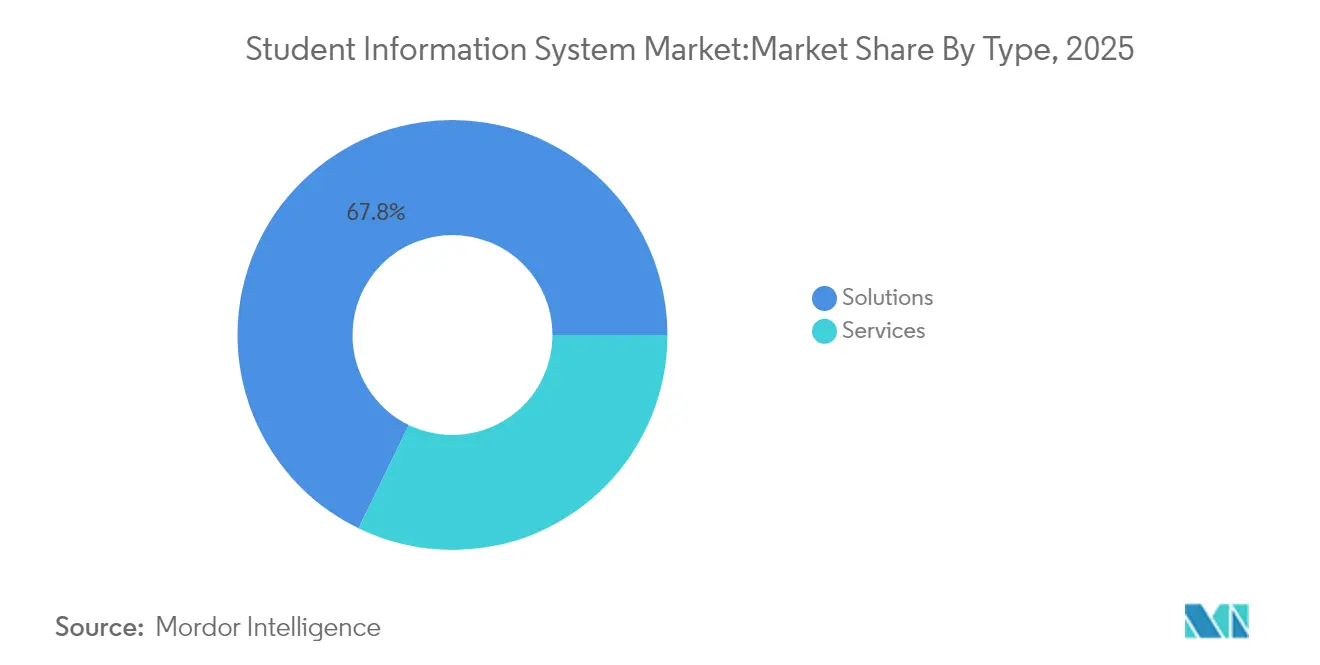

- By type, Solutions held 67.80% of the student information system market share in 2025; Services are projected to record the fastest 16.1% CAGR through 2031.

- By end-user, Higher Education led with 58.20% revenue share in 2025; K-12 Education is expanding at a 16.8% CAGR to 2031.

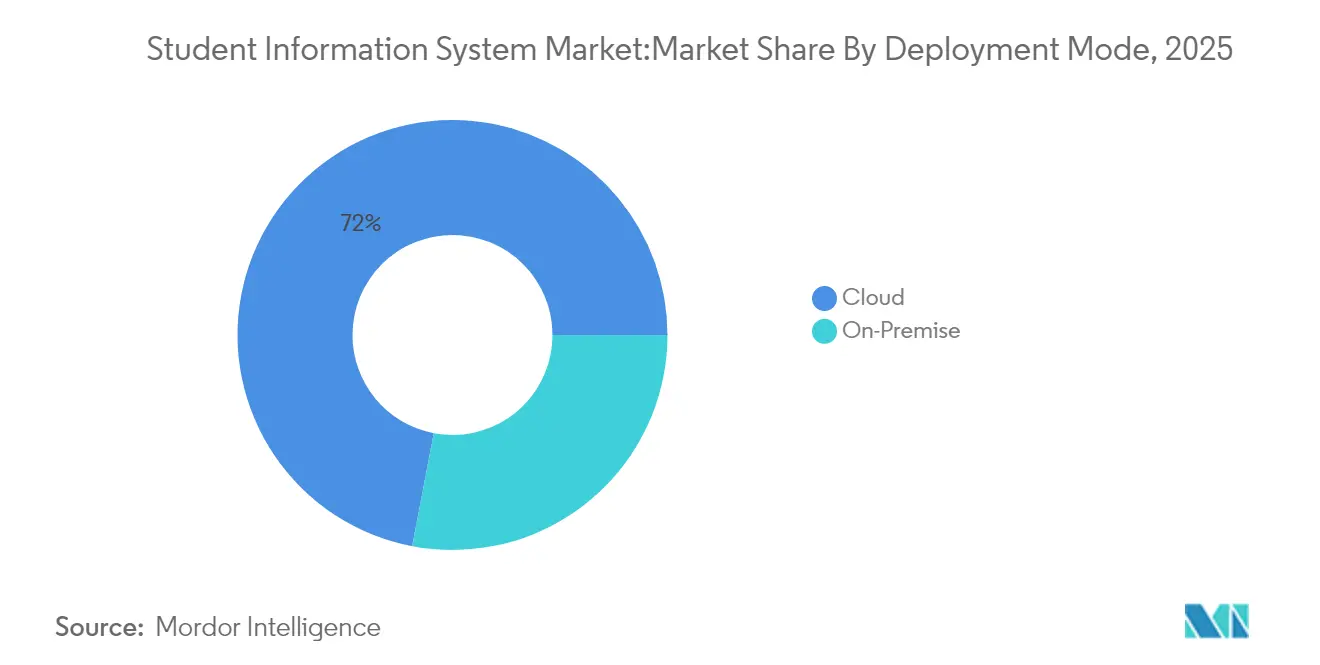

- By deployment mode, cloud platforms commanded a 72.00% share of the student information system market size in 2025 and are growing at a 15.7% CAGR.

- By institution size, medium-sized institutions (5,001–20,000 students) accounted for 43.20% of implementations in 2025; small institutions (≤5,000 students) are advancing at a 15.9% CAGR.

- By geography, North America retained 37.60% revenue share in 2025; Asia-Pacific is forecast to expand at a 16.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Student Information System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cloud-first digital-transformation mandates | +3.2% | Global, strong in North America and EU | Medium term (2-4 years) |

| Mandate for holistic data-driven student-success analytics | +2.8% | Global, concentrated in Higher Education | Long term (≥ 4 years) |

| Heightened compliance and reporting burdens on institutions | +2.1% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Demand for unified EdTech stacks and API-ready SIS platforms | +2.5% | Global, strongest demand in North America | Medium term (2-4 years) |

| Emergence of micro-credentialing/Lifelong-learning models | +1.8% | North America and EU, pilot programmes in Asia-Pacific | Long term (≥ 4 years) |

| AI-powered predictive retention solutions embedded in SIS | +2.6% | Global, led by North America and select EU institutions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud-First Digital-Transformation Mandates

Institutions are shifting wholesale to cloud-native SIS platforms to gain unified data backbones, real-time analytics, and frictionless integrations. Western Sydney University consolidated multiple applications onto Ellucian Banner to support 45,000 students across 10 campuses, replacing disparate on-premises systems with a single cloud environment. [2]Ellucian, “Building an Integrated Experience Across Campuses,” ellucian.com The University of La Verne later increased data-download speed by 50% after layering AI on the same cloud stack. With cloud penetration already at 72.6%, many institutions now deem hybrid models an unnecessary complication. Cloud architectures also lay the groundwork for predictive analytics, an area where legacy systems cannot compete. As a result, vendors are pivoting to subscription models that fund continuous innovation while customers benefit from automatic updates and stronger security postures.

Mandate for Holistic Data-Driven Student-Success Analytics

Universities are migrating from reactive student support toward proactive engagement informed by predictive modelling. Georgia State University improved graduation rates using predictive alerts, and the University of Kentucky used SIS-generated insights to flag and support at-risk learners. To unlock such value, Duke University launched online data-training courses so staff can interpret dashboards effectively. Modern platforms now merge academic records, behavioural signals, and financial data, delivering a 360-degree view of each learner. This shift is transforming the student information system market into a strategic analytics cornerstone that informs institutional resource allocation, financial aid targeting, and curriculum design.

Heightened Compliance and Reporting Burdens on Institutions

Global data-privacy frameworks are tightening, compelling SIS vendors to embed compliance features at the architectural level. Infinite Campus offers a FERPA compliance framework that protects minor data by default. Microsoft’s School Data Sync solution automates GDPR tagging across integrated apps to safeguard personal data during transfers. Real-time regulatory reporting is now essential as funding agencies demand granular performance metrics. Institutions lacking automated compliance functions risk financial penalties, driving them toward platforms with embedded privacy logic and audit-ready reporting modules.

Demand for Unified EdTech Stacks and API-Ready SIS Platforms

Fragmented point solutions create data silos and manual workarounds. The EDU-API standard, spearheaded by the 1EdTech community, is close to launch and promises cleaner interoperability across EdTech products. Instructure’s partnership with Lucid Software eliminated file exports by enabling real-time read-write integration within Canvas. Institutions now evaluate vendors on API depth, out-of-the-box connectors, and marketplace ecosystems rather than on core administrative functionality alone. This demand propels the student information system market toward open architectures, accelerating third-party innovation while lowering institutional integration costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills and change-management gaps among education staff | -1.9% | Global, particularly acute in smaller institutions | Short term (≤ 2 years) |

| Capital-expenditure constraints in low-income regions | -2.3% | Developing markets in Asia-Pacific, MEA, and Latin America | Medium term (2-4 years) |

| Heightened data-privacy/residency regulations | -1.2% | EU leading, expanding to Asia-Pacific and selective US states | Long term (≥ 4 years) |

| Vendor lock-in and legacy-migration complexity | -1.8% | Global, concentrated in institutions with 10+-year-old systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skills and Change-Management Gaps Among Education Staff

Rapid platform evolution demands data literacy and process redesign skills that many institutions lack. Duke University’s staff training programme illustrates the investment needed to close knowledge gaps. Resistance to automated workflows persists among employees accustomed to manual procedures, especially in small schools with limited professional-development budgets. Without upskilling, institutions under-utilise advanced features, diminishing return on investment, and prolonging reliance on obsolete processes. This restraint slows cloud migrations and feature adoption across the student information system market, particularly where staffing resources are thin.

Capital-Expenditure Constraints in Low-Income Regions

The sunset of pandemic-era ESSER funds in 2024 forced many K-12 districts to defer technology upgrades. A separate survey found 68% of school systems delaying replacements due to budget shortfalls. Subscription pricing lowers upfront costs, but recurring fees remain a burden where operating budgets are thin. Consequently, high-capability SIS platforms cluster in wealthier geographies, limiting market penetration in developing regions and widening the digital divide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Momentum Shifts Toward Service-Enhanced Platforms

Solutions captured 67.80% revenue in 2025 as institutions standardised on full-stack platforms. PowerSchool’s 90-day deployment for 40,000 students underscores how vendors refine implementation toolkits to compress timelines. Services, although only 32.20% of spend, are compounding at 16.1% CAGR as campuses need configuration, training, and analytics expertise to unlock advanced features.The lasting appeal of turnkey solutions drives consolidation: platform leaders acquire regional specialists to deepen vertical functionality and scale support teams. Simultaneously, services arms are evolving from basic deployment to continuous optimisation, data-science consulting and AI model tuning. This symbiosis expands the student information system market by embedding long-term vendor-client partnerships that refresh revenue streams beyond licence fees.

By End-user: K-12 Surge Rebalances Institutional Mix

Higher Education maintained a 58.20% share in 2025 due to complex feature requirements and larger average deal sizes. Yet post-pandemic digitisation grants have sparked a sharp rise in K-12 demand, propelling a 16.8% CAGR to 2031. District-wide purchasing consortia negotiate favourable terms that democratise access to advanced functionality.Infinite Campus now serves 10 million learners across 46 states, demonstrating the scale benefits in K-12. Conversely, universities face enrolment headwinds and legacy entanglements that slow migrations. As K-12 adoption expands, vendors tailor UX and compliance modules to the unique workflows of younger learners, further accelerating momentum in this segment of the student information system market.

By Deployment Mode: Cloud Supremacy Drives Subscription Economics

Cloud implementations represented 72.00% of all deployments in 2025 and are advancing at 15.7% CAGR. Western Sydney University reported round-the-clock student access and streamlined administration after moving to the cloud. On-premise footprints continue to erode as boards demand reduced infrastructure risk, automatic feature rollouts, and native security controls.Unit4 disclosed that 95% of new customers in 2024 selected cloud deployments, validating the irreversible shift in buyer preference. Subscription revenue also aligns vendor incentives with customer outcomes, funding faster product iteration cycles that further differentiate cloud solutions within the student information system market.

By Institution Size: Democratisation Opens New Frontiers

Medium-sized universities captured 43.20% of 2025 deployments, sitting at the sweet spot between feature complexity and implementation agility. However, small campuses are the fastest movers, clocking a 15.9% CAGR amid cloud economics that remove historical barriers. Packaged best-practice templates reduce the need for costly customisation, letting smaller teams leverage predictive retention dashboards previously reserved for large universities.Large institutions continue to shape roadmap direction through enterprise-scale requirements such as multi-college governance, but protracted change-management schedules temper adoption speed. Vendors are responding with tiered editions that scale from basic to advanced without compromising data model consistency, thereby widening the total addressable student information system market.

Geography Analysis

North America accounted for 37.60% of 2025 revenue, supported by substantial IT budgets and a dense vendor ecosystem. Yet spending growth is moderating as campuses optimise existing stacks rather than pursue wholesale replacements. The ESSER funding cliff intensifies pressure on K-12 budgets, while universities confront enrolment volatility. Nevertheless, the region remains an innovation test bed, piloting AI-powered retention modules that later roll out globally.Asia-Pacific is the fastest-growing region at a 16.4% CAGR through 2031, benefiting from greenfield cloud deployments that bypass legacy baggage. PowerSchool plans to scale its Indian workforce to 2,000 within five years to capitalise on regional demand. Tribal Group won a USD 3 million AUD contract with British University Vietnam, highlighting rising investment appetite in emerging markets.Europe records steady uptake, driven by GDPR compliance that elevates the value of platforms embedding privacy-by-design. A five-year Ellucian–Interuniversity Services Inc. deal covering Atlantic Canada illustrates cross-border collaboration models that could replicate across European consortia. Middle East and Africa trail in scale but present long-term upside as connectivity projects and workforce-ready education agendas gather momentum. Collectively, these trends reinforce the cross-regional expansion strategy adopted by the major players in the student information system market.

Regulatory Landscape

Student information systems operate under expanding privacy, security, and transparency requirements for education records. In the United States, FERPA (20 U.S.C. 1232g; 34 CFR Part 99) governs access, disclosure, and protection of education records, while institutions that participate in Title IV federal student aid fall under Gramm-Leach-Bliley Act (GLBA) safeguarding expectations and breach reporting to Federal Student Aid (FSA). The US Department of Education also released a 2024 IT PII Processing and Transparency Standard for departmental systems, referencing NIST SP 800-53 controls, which reinforces demand for documented processing transparency and auditable safeguards around student PII.

In Europe, GDPR raises compliance obligations for both SIS vendors and institutions, including data protection by design and by default (Article 25), records of processing activities (Article 30), and processor contracting requirements such as Article 28 data processing agreements. In K-12 contracting, standardized frameworks like the Student Data Privacy Consortium (SDPC) National Data Privacy Agreement (NDPA) help districts standardize vendor terms, pushing SIS providers toward consistent privacy addenda, clearer data-sharing disclosures, and security-aligned implementation practices across jurisdictions.

Value Chain Analysis

The SIS value chain centers on the platform as the institution's system of record for applicant-to-alumni data. Core software vendors, including PowerSchool, Ellucian, Oracle, Workday, Jenzabar, and Anthology, provide the data model, workflows, and reporting layers for enrollment, academics, attendance, and compliance. Around the core platform, implementation and managed-service partners support configuration, migration, training, and ongoing optimization, while cloud and integration partners provide hosting, identity, API management, and connectivity into LMS, ERP, CRM, and analytics tools.

Friction tends to concentrate in integration and migration, where legacy records, proprietary formats, and limited APIs can slow interoperability across the broader EdTech stack. This has increased emphasis on API-ready architectures and shared data standards, alongside governance requirements shaped by FERPA and GDPR, which affect how data is transmitted, audited, and retained across third-party integrations. Vendor marketplaces and connector ecosystems are also functioning as distribution channels for pre-built integrations, reducing custom development and supporting faster time-to-value for institutions running cloud deployments.

Competitive Landscape

Consolidation is accelerating, yet the field remains moderately fragmented. Bain Capital’s takeover of PowerSchool and KKR’s purchase of Instructure injected significant capital for R&D and market entry programmes. Jenzabar secured 134 new institutions in 2024 and deepened ties with Google Cloud to enhance scalability.

Technological moats now depend on AI engines, low-code configuration, and open APIs. The recent USPTO patent on tuning educational data structures emphasises vendor focus on optimising complex schemas for real-time analytics. Disruptors differentiate through niche modules such as micro-credential tracking or advanced retention risk scoring, which larger vendors may later emulate or acquire. Strategic partnerships, exemplified by Instructure integrating Microsoft Reflect for student wellness, extend platform stickiness.

Going forward, platform vendors will balance M&A with ecosystem alliances to cover white-space functionalities without diluting core focus. Market share concentration is therefore likely to increase gradually, but open-API architectures will allow specialised providers to coexist within the broader student information system market.

Student Information System Industry Leaders

PowerSchool Holdings Inc.

Ellucian Company LP

Oracle Corporation (Student Cloud)

Workday Inc.

Skyward Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is the shift from standalone SIS deployments toward unified SaaS platforms that connect student lifecycle processes with finance and human capital workflows. This approach reduces administrative fragmentation and supports more consistent institutional reporting. In April 2026, Ellucian launched Ellucian Student as an AI-native SaaS platform unifying student information, HCM, and finance on a single architecture. The company also reported 26 institutions going live on its SaaS SIS and ERP solutions in Q1 2026, indicating continued buyer willingness to modernize core systems when the deployment path is defined and the operating model supports continuous updates.

Interoperability is another whitespace for institutions operating best-of-breed stacks across SIS, LMS, and adjacent systems. Ellucian became a founding partner of the MortarCAPS Higher Learning Data Standard initiative in 2026, and it launched Ellucian Marketplace to accelerate ready-to-deploy SaaS integrations, pointing to data standards plus packaged connectors as procurement differentiators. For K-12 and independent schools, agentic workflow automation and cross-system synchronization are emerging purchase drivers, illustrated by Blackbaud's July 2026 announcement of an Admissions Agent and real-time data synchronization between its SIS and Raiser Edge NXT via a Common Records Engine.

Recent Industry Developments

- July 2026: Ellucian launched Ellucian Advancement in the United Kingdom, extending its alumni engagement and fundraising capabilities with AI-powered features. The move broadens Ellucian's platform footprint beyond core student records into advancement workflows, which can deepen account penetration across higher education institutions using its SIS and ERP stack.

- May 2026: PowerSchool partnered with the Texas Education Exchange to support secure statewide data sharing across K-12 systems without requiring districts to replace existing tools. The partnership elevates data exchange and interoperability as a competitive differentiator for SIS vendors operating in state-coordinated ecosystems.

- October 2024: Bain Capital closed its USD 5.6 billion acquisition of PowerSchool. The transaction injected private-equity backing into a major SIS provider, supporting continued consolidation and accelerated product investment in areas such as cloud delivery and analytics.

Research Methodology Framework and Report Scope

Market Definition and Coverage

We define the student information system market as the revenues earned from platforms used by education institutions to maintain student records and run core workflows like admissions, enrollment, attendance, grades, and billing, across K-12 and higher education.

Scope exclusions: We exclude stand-alone learning management and classroom tools when they are not the system of record for official student data.

Segmentation Overview

- By Type

- Solutions

- Services

- By End-user

- K-12 Education

- Higher Education

- By Deployment Mode

- On-Premise

- Cloud

- By Institution Size

- ≤5,000 Students (Small)

- 5,001-20,000 Students (Medium)

- >20,000 Students (Large)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Our desk work starts by pinning down the demand pool, meaning how many institutions exist, how many learners are served, and how budgets flow into software and services. For this, we rely on public sources such as the UNESCO Institute for Statistics, National Center for Education Statistics (NCES), OECD education indicators, World Bank education datasets, and the U.S. Integrated Postsecondary Education Data System (IPEDS), which help us ground the count of schools, enrollments, and system needs.

We then review company filings, investor presentations, product documentation, public procurement portals, association websites, and reputable press to map typical buying patterns and contract structures. Where helpful, we also use paid subscriptions for company financials and intelligence, news and financials, and patent databases to confirm revenue context and product direction. The desk sources named above are illustrative and not exhaustive, and we use additional references for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that desk sources cannot fully explain, especially pricing progression, cloud migration timelines, and what buyers treat as part of the SIS versus an adjacent module. We speak with implementation partners, SIS product and sales leaders, IT administrators, and functional owners in registrars and enrollment offices across APAC, EMEA, and the Americas. We then re-check any outlier inputs before finalizing totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 40% | EMEA: 32% |

| Smaller Players: 17% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where institution counts and enrollment by region are translated into an addressable demand pool, and then converted into spending using adoption levels and typical annual contract values. To keep this practical, inputs are anchored to repeatable indicators such as K-12 and higher education enrollment trends, number of active institutions, cloud share versus on-premise footprints, average contract duration, and observed implementation and support intensity.

Totals are subsequently corroborated using selective bottom-up checks, such as sampled pricing by institution size, partner channel checks, and a limited roll-up of vendor revenue disclosures where reporting is clear. When a revenue line is bundled with adjacent education software, we allocate only the portion tied to system-of-record student data workflows, and any remaining gap is handled using conservative ranges agreed in calls with practitioners. For forecasting, we use scenario analysis supported by expert inputs on budget cycles, replacement activity, and cloud migration pace, and then we stress-test the curve against enrollment and institution growth so the result stays realistic.

Data Validation & Update Cycle

Outputs are validated through multiple checks, where model totals are compared with independent signals like public contract awards, reported education IT spending direction, and regional rollout patterns. If a result looks inconsistent, the drivers are reviewed, assumptions are reopened, and experts are re-contacted when the variance cannot be explained with documented evidence.

A second analyst review is completed before sign-off so the logic, arithmetic, and scope treatment stay consistent across years and regions. Reports are refreshed annually, and interim updates are triggered when major policy changes, large contract announcements, or step changes in cloud adoption materially shift the outlook. Right before delivery, we run a final freshness pass to capture any meaningful new information.

Mordor Intelligence's Student Information System Market Size Compared With Other Published Estimates

Published market sizes for student information systems can differ even when multiple reports describe a similar category, because the counting rules are rarely the same. The biggest swings typically come from what is treated as an SIS versus an adjacent education software module, what year is used as the current reference, and how services revenue is included.

In practice, gaps are usually driven by three items: whether learning management and classroom tools are blended into the total, whether implementation and ongoing support are counted in full or only partially, and how cloud subscription pricing is projected as institutions migrate from legacy deployments. The table also shows that currency timing and refresh cadence matter, since fast-moving contract terms and migration speeds can change the current-year number quickly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 17.70 B (2026) | |

| Global Consultancy A | USD 15.33 B (2024) | Anchors to an earlier year and appears to include a wider set of SIS-adjacent tools, and it also applies different cloud subscription price ramps during migrations. |

| Trade Journal B | USD 8.70 B (2024) | Uses a narrower revenue scope that likely focuses on core software only, with limited capture of implementation, support, and bundled services across institution sizes. |

Overall, the spread is largely explained by whether only system-of-record platforms are counted and whether services are included as recurring revenue. Non-system-of-record classroom tools are excluded from the total in the sizing steps used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current student information system market size?

The student information system market size stands at USD 17.7 billion in 2026 and is projected to reach USD 34.97 billion by 2031.

Which deployment model is growing fastest?

Cloud deployments lead with 72.00% share in 2025 and are growing at a 15.7% CAGR due to lower infrastructure overheads and real-time analytics capabilities.

Why is Asia-Pacific considered a high-growth region?

Asia-Pacific is forecast to expand at a 16.4% CAGR because governments are funding large-scale digitisation programmes and institutions can leapfrog legacy systems with cloud-native platforms.

How are private-equity investments affecting the market?

Large buyouts such as Bain Capital’s purchase of PowerSchool are injecting capital that accelerates product innovation, international expansion and further consolidation.

What challenges hinder SIS adoption?

Key barriers include staff skill gaps, capital-expenditure constraints in lower-income regions, stricter data-privacy regulations and the complexity of migrating from decade-old legacy systems.

Which segment is experiencing the fastest growth?

The K-12 end-user segment is growing at a 16.8% CAGR as school districts embrace data-driven decision-making and benefit from group purchasing arrangements.

Page last updated on: