Consumer Laptop Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

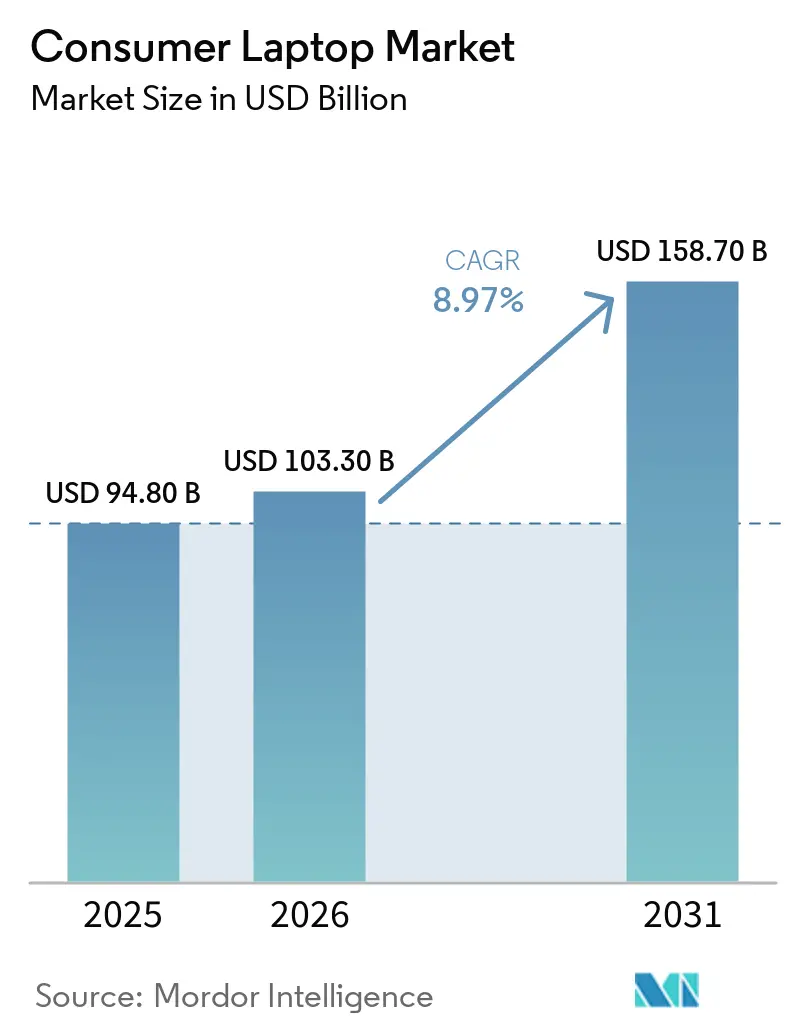

| Market Size (2026) | USD 103.30 Billion |

| Market Size (2031) | USD 158.70 Billion |

| Growth Rate (2026 - 2031) | 8.97% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Middle East |

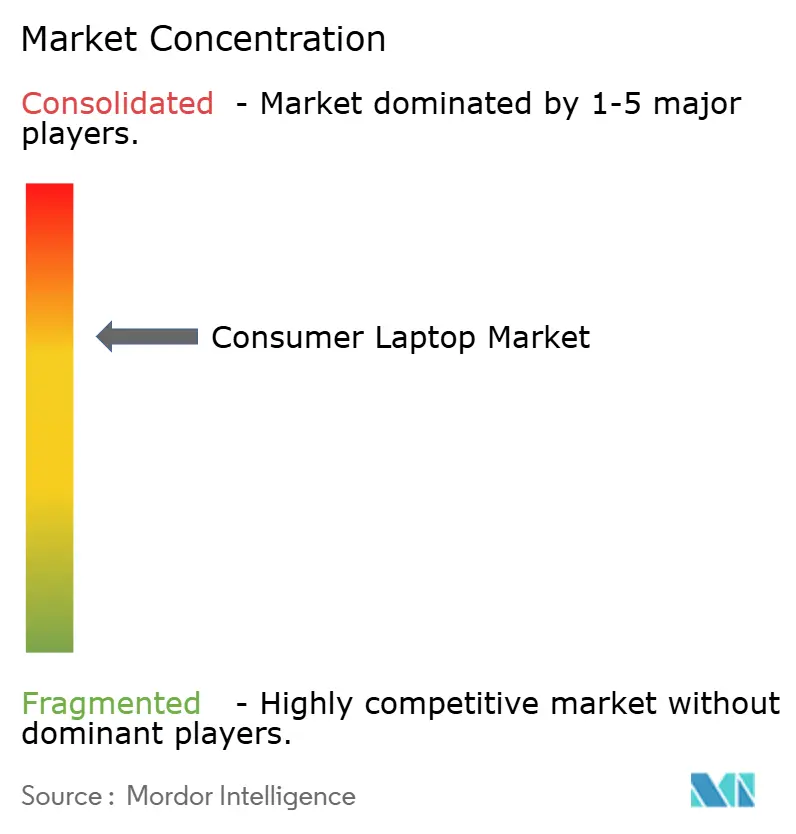

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Laptop Market Analysis by Mordor Intelligence

The consumer laptop market size is expected to be USD 94.8 billion in 2025, USD 103.3 billion in 2026, and reach USD 158.7 billion by 2031, growing at a CAGR of 8.97% from 2026 to 2031. Demand is shifting toward machines with on-device AI capability as neural processing units become a standard requirement, while the Windows 10 sunset in October 2025 has already sparked a replacement wave that is spilling over into personal purchases. Component inflation, especially in memory, is elevating average selling prices and concentrating margins in mature economies. Simultaneously, silicon road-maps from Intel, AMD, and Qualcomm have compressed workstation-class performance into the consumer tier, enabling the consumer laptop market to sustain premium segment growth even as unit demand normalizes. Vendor competition now revolves around who can pair AI-centric silicon with efficient thermals and sustainable materials without eroding price integrity.

Key Report Takeaways

- By geography, Asia-Pacific led with a 38.53% revenue share in 2025, while the Middle East is forecast to record the fastest expansion at a 9.11% CAGR through 2031

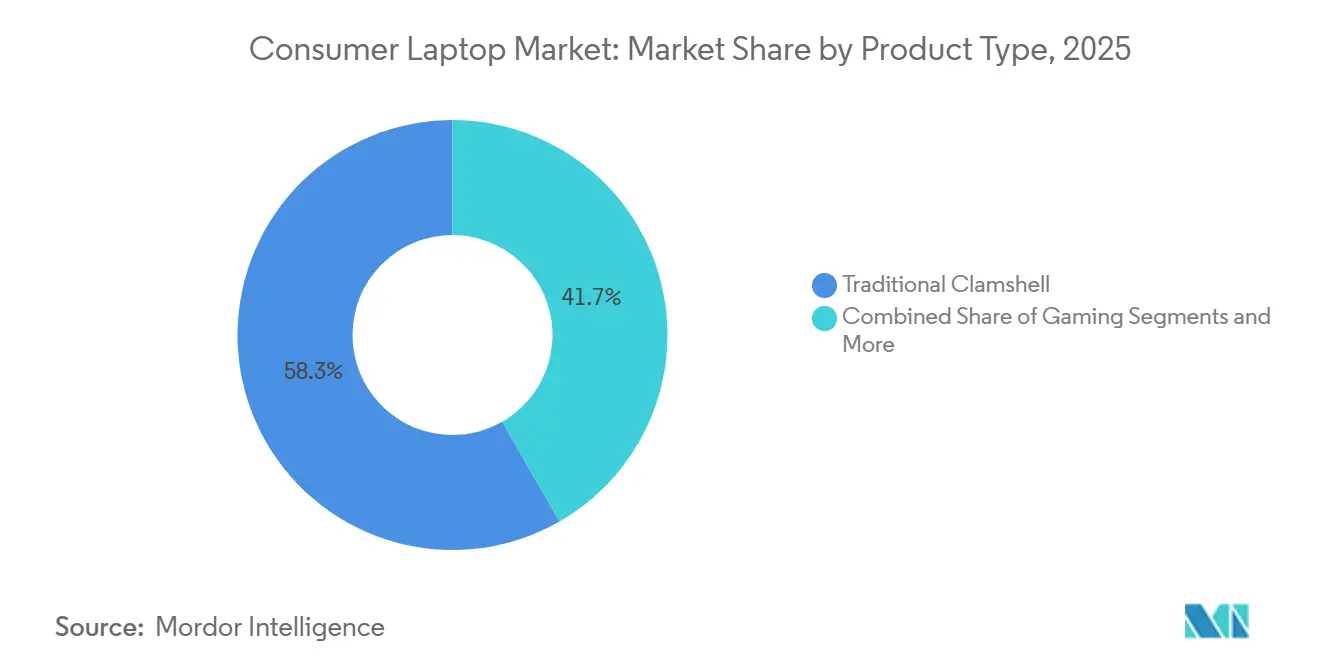

- By product type, traditional clamshells commanded 58.29% of 2025 volume; gaming models are projected to post the highest 9.42% CAGR to 2031

- By end user, home consumers accounted for 46.32% of 2025 revenue, whereas gamers are set to advance at a 9.83% CAGR from 2026 to 2031.

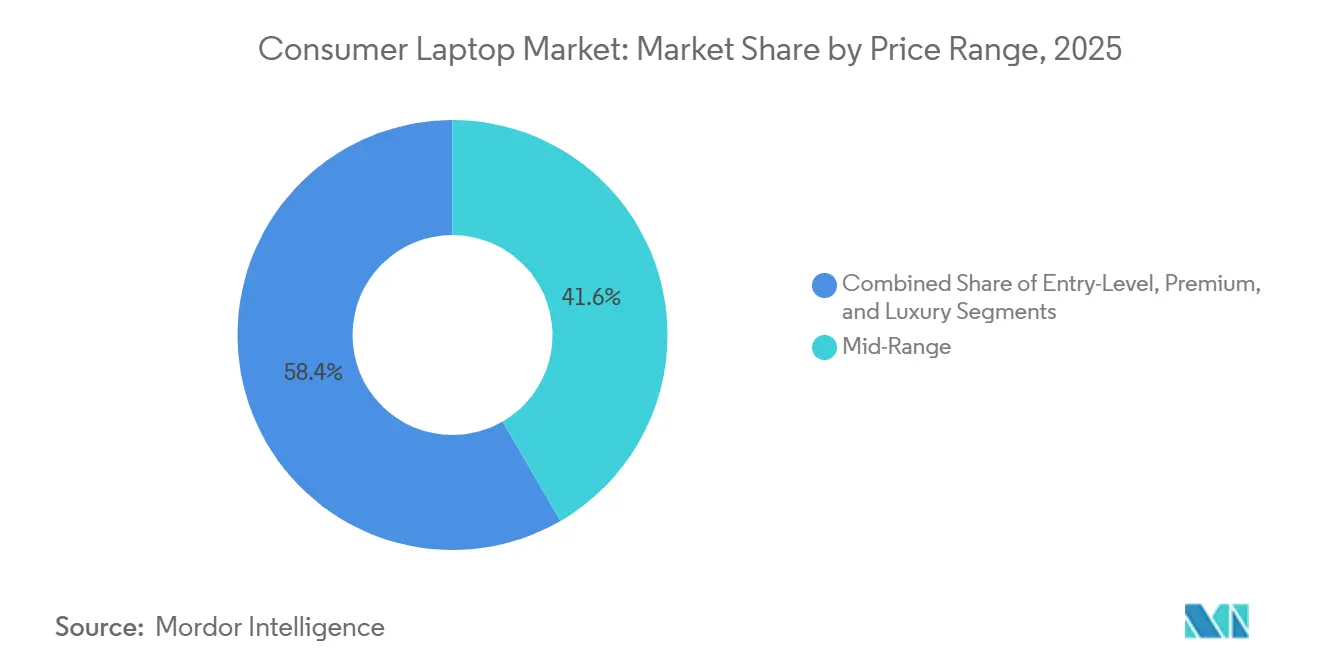

- By price range, mid-range configurations generated 41.62% of 2025 sales, yet the luxury tier is poised for an 11.24% CAGR during 2026-2031.

- By sales channel, offline retail remained slightly ahead at 47.59% of 2025 value, but online platforms are forecast to register a 12.42% CAGR over the same horizon.

- Lenovo, HP, and Dell collectively held roughly 60% of shipments in 2025, underscoring concentrated leadership at the top of the consumer laptop market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Laptop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid Work Culture Sustaining Demand for Portable Computing | +1.80% | North America, Europe, Urban Asia-Pacific | Medium term (2–4 years) |

| Growth of Esports and AAA Gaming Titles | +1.20% | North America, China, South Korea, Western Europe | Medium term (2–4 years) |

| Rising Disposable Income in Developing Countries | +1.50% | India, Southeast Asia, Latin America, Middle East, Africa | Long term (≥ 4 years) |

| Technological Upswing in Processor Efficiency and Battery Life | +2.10% | North America, Europe, Premium Asia-Pacific | Short term (≤ 2 years) |

| Government Subsidies for Student Laptop Procurement in Emerging Markets | +0.90% | India, Indonesia, Latin America, Africa | Short term (≤ 2 years) |

| Expansion of On-device AI Workloads Requiring Higher-spec Laptops | +1.40% | North America, Europe, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Culture Sustaining Demand for Portable Computing

Laptop demand is anchored to corporate refresh cycles prioritizing AI-ready hardware, with enterprises accelerating upgrades ahead of Windows 10 end-of-support timelines. This has driven bulk commercial procurement, indirectly shaping consumer purchasing through pricing signals and improved availability of higher-spec devices. Concurrently, battery efficiency gains, with select models sustaining ~13-hour workloads, are reducing dependence on docking setups and reinforcing the shift toward premium notebooks over desktops. However, the late-2025 demand spike was partly a pull-forward response to concerns about component shortages, masking a structural elongation of replacement cycles. As supply stabilizes, near-term demand may soften before normalizing.[1]Razer PR, “Razer’s Thinnest Gaming Laptop Evolves: Introducing the 2026 Blade 16 With More Cores, Fastest Memory, and Next-Gen Efficiency,” news.razer.com

Growth of Esports and AAA Gaming Titles

Esports viewership and prize pools are pushing desktop-grade specifications into portable systems, with vendors like NVIDIA enabling high-performance mobile GPUs that support 240 Hz QHD+ gaming on laptops. Advances in thermal design are maintaining slim form factors while sustaining performance, narrowing the gap with traditional desktops. Entry pricing near USD 1,000 expands the addressable base to casual gamers, while premium configurations exceeding USD 3,800 target creators and professional users. This bifurcation raises overall ASP and extends revenue potential. However, demand remains discretionary and sensitive to economic cycles, introducing volatility despite strong segment-level growth.[2]“Intel-Nvidia Deal Will Create ‘New Class Of Integrated Graphics Laptops,’ Huang Says,” crn.com

Rising Disposable Income in Developing Countries

Income growth in India, Indonesia, and Brazil is expanding the consumer base beyond metro regions, supported by rapid improvements in e-commerce logistics and last-mile delivery networks. Tier-2 and tier-3 consumers increasingly depend on social commerce and video-led discovery, which are demonstrating measurable conversion efficiency for laptop purchases. Government-led student procurement programs provide a stable demand baseline while incentivizing local manufacturing, reducing import duties, and supply latency. Collectively, these factors support sustained value growth, though affordability constraints and access to consumer financing remain key constraints.[3]Timothy Grant, “Notebook Industry Statistics: Market Data Report 2026,” gitnux.org

Technological Upswing in Processor Efficiency and Battery Life

Hybrid core architectures integrating NPUs are enabling 40–85 TOPS AI performance within passively cooled designs, allowing on-device inference without materially compromising battery life. Vendors such as Intel and Advanced Micro Devices are optimizing heterogeneous compute to balance efficiency and throughput. Devices are also approaching the 99.9 Wh airline limit while supporting 140 W USB-C fast charging, improving mobility economics. Emerging CPU-GPU chiplet designs are expected to narrow the gap between integrated and discrete graphics, enabling thinner high-performance systems. These advancements support ASP expansion, though benefits remain skewed toward premium segments with limited immediate mass-market impact.[4]“CES 2026: MSI Announces Next-Gen Raider, Stealth and Crosshair Gaming Laptops,” ign.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthening Replacement Cycles Due to Incremental Hardware Upgrades | -1.30% | North America, Europe, Japan | Medium term (2–4 years) |

| Competition from Tablets and Smartphones | -0.70% | Global, price-sensitive segments | Long term (≥ 4 years) |

| Supply Chain Localization Policies Adding Cost Complexity | -0.90% | India, Vietnam, Mexico | Short term (≤ 2 years) |

| Rising E-waste Regulations Increasing End-of-life Compliance Costs | -0.60% | EU, India, China | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lengthening Replacement Cycles Due to Incremental Hardware Upgrades

Tool-less upgradeability in memory and storage, combined with firmware-level optimization, is extending device lifecycles by up to 18 months, directly suppressing replacement-driven demand. Rising DRAM prices are shifting economics in favor of component upgrades over full system replacement, particularly for mid-range users. Enterprises are also transitioning toward usage-based refresh triggers rather than fixed three-year cycles, reducing predictable procurement volumes. Concurrently, OEM-led price increases of 18–20% are further delaying consumer purchase decisions. The net effect is structural pressure on unit shipments, even as higher ASPs partially offset revenue impact in the consumer laptop market.

Competition from Tablets and Smartphones

High-end tablets and foldable smartphones increasingly substitute entry-level laptops for casual use cases such as browsing, streaming, and light productivity. Apple Inc. maintains a dominant position in tablets, while Android OEMs are advancing foldables with desktop-style docking capabilities, compressing the functional gap. This creates pricing pressure and feature overlap at the lower end of the laptop market. However, notebooks retain a clear advantage in sustained multitasking, complex workloads such as large spreadsheets, and on-device AI execution. As a result, the consumer laptop market preserves a differentiated value proposition, anchored in performance and productivity rather than convenience.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gaming Laptops Propel Performance Innovation

The gaming segment accounted for a considerable share of the consumer laptop market in 2025 and is projected to grow at a 9.42% CAGR through 2031, outperforming the broader category. Systems from MSI and Razer now combine ~300 W power envelopes with slim ~15 mm chassis, indicating a mature thermal ecosystem. Despite this premium push, traditional clamshell laptops continue to dominate volume, accounting for 58.29% share in 2025, driven by education procurement and enterprise standardization, which anchor baseline demand across price tiers.

Vendors are embedding ~40 TOPS NPUs even in entry-level clamshell devices to align with upcoming AI-driven OS requirements linked to Windows evolution. This ensures compliance and extends lifecycle relevance, particularly for institutional buyers. While gaming drives ASP expansion, clamshells sustain shipment scale due to cost efficiency and familiarity. The coexistence of high-performance gaming systems and mass-market clamshells reflects a bifurcated market structure where innovation at the top end does not immediately translate into volume shifts at the lower end.

Thermal engineering remains the primary differentiator in gaming laptops, with triple-fan configurations and phase-change materials enabling sustained performance under heavy workloads. Convertible 2-in-1s and ultrabooks occupy niche segments, gaining traction where portability below 1.5 kg or stylus functionality is critical. Rugged laptops remain confined to specialized verticals such as defense and construction. Overall, performance gains and esports-driven visibility sustain a premium halo effect, indirectly supporting pricing power and brand positioning across the broader consumer laptop market, even as volume remains concentrated in traditional clamshell form factors with a 58.29% share.

By End User: Gamers Anchor the Premium Upsell Opportunity

Home consumers generated 46.32% of total value in 2025, reflecting strong demand for versatile laptops that support hybrid work, online education, and general productivity. Households increasingly prioritize multi-use devices that balance performance and affordability, reinforcing steady volume demand in mid-range segments. At the same time, gamers are projected to grow at a 9.83% CAGR through 2031, outpacing all other cohorts and driving premiumization. This divergence creates a dual-market structure, where home users anchor volume while gaming and high-performance use cases expand value in higher price bands.

Students benefit from structured procurement programs in markets such as India and Indonesia, ensuring consistent device availability and supporting baseline demand. Meanwhile, professionals and creators are increasingly shifting toward high-spec configurations, including Tandem OLED displays and 32 GB memory baselines, to support content creation and multitasking workloads. This trend aligns hardware expectations across professional and enthusiast segments, gradually narrowing the gap between consumer and workstation-grade devices, while sustaining demand for premium configurations.

The introduction of a lower-cost MacBook variant by Apple Inc. at USD 599 in 2026 intensifies competition in the entry-level segment, putting pressure on Windows OEMs to differentiate through bundled services and flexible financing. At the upper end, demand for local AI inference capabilities and wide-gamut displays continues to rise, particularly among creators and advanced users. This convergence with gaming-grade specifications reinforces the resilience of the luxury segment, ensuring that premium tiers remain a key driver of revenue growth in the consumer laptop market.

By Price Range: Luxury Tier Surges on AI and Sustainable Materials

Mid-range systems accounted for 41.62% of 2025 revenue, reflecting their balance between performance and affordability. However, luxury models priced above USD 2,000 are projected to grow at an 11.24% CAGR over 2026–2031, driven by on-device AI capabilities that elevate perceived value. Vendors such as Dell Technologies and Razer are also embedding sustainability into product design, using recycled materials as a core specification rather than a branding element. This shift supports margin resilience, as both performance and environmental credentials increasingly justify premium pricing.

Entry and premium segments remain critical for sustaining overall volume. Government-backed student procurement programs continue to anchor demand at the entry level, particularly in emerging markets where affordability remains a key constraint. At the same time, premium devices in the USD 1,200–2,000 range strike a balance between discrete graphics performance and thin-and-light portability, appealing to professionals and advanced users. This segment acts as a bridge between mass-market and luxury tiers, ensuring consistent demand across multiple consumer cohorts while maintaining a stable upgrade pathway.

Rising disposable income in developing economies is funneling aspirational buyers toward higher-spec devices, gradually shifting demand from entry-level to mid-range and premium categories. Markets such as India and Southeast Asia are witnessing increased adoption of feature-rich laptops as financing options and e-commerce access improve. This upward mobility supports value growth even if unit expansion moderates. However, sensitivity to pricing and macroeconomic volatility remains a constraint, meaning sustained growth in premium segments depends on continued income expansion and access to consumer credit.

By Sales Channel: Online Platforms Capture Incremental Growth

Offline retail accounted for 47.59% of consumer laptop sales in 2025, reflecting the continued importance of physical touchpoints for evaluation and immediate fulfillment. However, online channels are projected to grow at a 12.42% CAGR, driven by expanding logistics networks beyond metro regions and improved last-mile delivery efficiency. Shoppable video and content-led commerce are increasing conversion rates by 40%, particularly among first-time buyers who require clearer product differentiation. Direct-to-consumer platforms from OEMs such as Dell Technologies further enhance margin control and enable first-party data capture for lifecycle marketing.

Despite digital acceleration, brick-and-mortar stores remain relevant for consumers seeking hands-on experience, configuration guidance, and after-sales support. This is especially critical in higher-value purchases where trust and tactile validation influence decision-making. Retail partners also play a role in financing facilitation and bundling services, which are less effective in purely online environments. As a result, offline channels continue to anchor a significant portion of demand, particularly in emerging markets and among less digitally mature consumer segments

Hybrid fulfillment models are increasingly bridging the gap between online convenience and offline assurance. Approaches such as “order online, pick up in store” optimize inventory utilization while reducing delivery timelines and costs. This omnichannel strategy allows vendors to balance margin efficiency with customer experience. Structurally, the consumer laptop market is converging toward integrated channel ecosystems rather than channel substitution, ensuring flexibility across diverse buyer preferences and reinforcing resilience against shifts in purchasing behavior.

Geography Analysis

Asia-Pacific led the consumer laptop market with a 38.53% share in 2025, supported by strong shipment volumes in India and China. India recorded 15.9 million units, driven by subsidy-backed education programs and rapid e-commerce penetration beyond tier-1 cities, which is expanding the consumer base. China delivered 42.1 million units, maintaining scale leadership, although demand is expected to contract by ~10% in 2026 as government incentives taper. This indicates a transition from policy-driven growth to more normalized demand conditions across the region.

North America and Europe continue to dominate in revenue terms due to higher average selling prices and early adoption of AI-enabled devices. Consumers in these markets are shifting toward premium configurations with enhanced compute and display capabilities. However, rising memory costs and elongating replacement cycles are constraining unit growth, particularly in mature segments. In Japan, demand peaked during the 2025–2026 refresh cycle and is expected to moderate as enterprises adopt usage-based replacement strategies, reducing the frequency of hardware upgrades and stabilizing long-term demand.

The Middle East is emerging as a high-growth region, with a projected 9.11% CAGR supported by localization initiatives such as Lenovo’s USD 2 billion manufacturing investment in Saudi Arabia, aligned with Vision 2030. Latin America and Africa are also showing steady expansion, contingent on scaling local assembly to mitigate import tariffs and improve affordability. Overall, supply chain diversification and region-specific incentives are redistributing manufacturing footprints, reducing dependency on single geographies, and enhancing resilience across the consumer laptop market.

Competitive Landscape

Lenovo, HP Inc., and Dell Technologies together controlled ~60% of global laptop shipments in 2025, indicating moderate concentration with strong scale advantages in procurement and distribution. However, value capture is increasingly shifting upstream as silicon vendors such as Intel and NVIDIA co-develop chiplet architectures that blur the line between integrated and discrete graphics. Simultaneously, Qualcomm’s high-performance ARM-based processors are enabling OEMs to differentiate on efficiency and AI capability rather than traditional x86 performance metrics.

Apple Inc.’s sub-USD 600 MacBook Neo represents a strategic re-entry into the budget segment, directly challenging Chromebook ecosystems and compressing margins at the entry level. This forces Windows OEMs to respond by optimizing costs, localizing manufacturing, and bundling services such as cloud storage and financing. Companies like Acer and Lenovo are expanding regional production footprints in markets such as India and Saudi Arabia to mitigate tariff exposure and reduce logistics costs. This shift toward localized supply chains reflects a broader move toward geopolitical risk management and operational resilience.

Thermal engineering and sustainability are emerging as key brand differentiators, particularly in premium segments. Vendors such as MSI emphasize performance through advanced cooling architectures, such as triple-fan systems, while Dell and Razer focus on recycled materials and reduced packaging footprints to align with environmental regulations. Increasingly stringent extended producer responsibility (EPR) requirements are raising compliance costs, especially for smaller players lacking reverse logistics capabilities. This dynamic may accelerate consolidation or drive strategic partnerships, reshaping competitive intensity within the consumer laptop market.

Consumer Laptop Industry Leaders

Lenovo Group Limited

HP Inc.

Dell Technologies Inc

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2021: Dell released new XPS 14 and XPS 16 models featuring Tandem OLED displays and up to 75% recycled aluminum, signaling sustainability as a luxury attribute.

- February 2026: Dell forged an MoU with Ankabut to deliver GPU-as-a-service for UAE education, expanding its foothold in the Middle East’s digital adoption plans.

- March 2025: Apple launched the MacBook Neo at USD 599 and refreshed the MacBook Pro line with AI-centric M5 chips, escalating competition at both ends of the price spectrum.

- March 2026: Razer introduced the Blade 16 with Intel Core Ultra 9 386H, RTX 50-series GPUs, Thunderbolt 5 ports, and a recycled aluminum body, underscoring portability without sacrificing 300 W headroom.

Global Consumer Laptop Market Report Scope

The consumer PC market comprises desktops, laptops, and hybrid devices purchased by individual users for personal, educational, and home-office use. It includes entry, mid-range, and premium systems, driven by computing needs such as productivity, entertainment, and gaming. Income levels, replacement cycles, technological upgrades, and distribution channels, including online and offline retail, influence demand.

The Consumer Laptop Market Report is Segmented by Product Type (Traditional Clamshell, Convertible 2-in-1, Gaming, Ultrabook/Thin and Light, and Rugged), End User (Home Consumers, Students, Gamers, and Professionals and Content Creators), Price Range (Entry-Level, Mid-Range, Premium, and Luxury), Sales Channel (Online Retail, Offline Retail, and Direct-to-Consumer Brand Stores), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Traditional Clamshell |

| Convertible 2-in-1 |

| Gaming |

| Ultrabook / Thin and Light |

| Rugged |

| Home Consumers |

| Students |

| Gamers |

| Professionals and Content Creators |

| Entry-Level |

| Mid-Range |

| Premium |

| Luxury |

| Online Retail |

| Offline Retail |

| Direct-to-Consumer Brand Stores |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Product Type | Traditional Clamshell | |

| Convertible 2-in-1 | ||

| Gaming | ||

| Ultrabook / Thin and Light | ||

| Rugged | ||

| By End User | Home Consumers | |

| Students | ||

| Gamers | ||

| Professionals and Content Creators | ||

| By Price Range | Entry-Level | |

| Mid-Range | ||

| Premium | ||

| Luxury | ||

| By Sales Channel | Online Retail | |

| Offline Retail | ||

| Direct-to-Consumer Brand Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big will the consumer laptop market be by 2031?

The consumer laptop market size is forecast to reach USD 158.7 billion by 2031, expanding at an 8.97% CAGR from 2026, according to Mordor Intelligence.

Which region will grow fastest in consumer laptop demand?

The Middle East is projected to register the highest regional CAGR at 9.11% through 2031, buoyed by new domestic manufacturing and education-centric digital initiatives.

What drives the premium surge in laptop pricing?

Integrated NPUs enabling local AI workloads, OLED and Tandem OLED displays, and recycled-metal chassis are pushing luxury models to an 11.24% CAGR, per Mordor Intelligence.

Who are the leading consumer laptop vendors?

Lenovo, HP, and Dell together held roughly 60% of global shipments in 2025, placing them at the top of the competitive hierarchy.

Why are gaming laptops outpacing traditional clamshell growth?

Esports popularity and GPUs capable of 240 Hz QHD+ gaming are lifting the gaming sub-segment to a 9.42% CAGR, well above the overall markets rate.

How will Windows 10 end-of-support affect sales?

The October 2025 cutoff accelerated enterprise refreshes in late 2025, providing a tailwind to 2026 consumer demand as users align personal devices with workplace upgrades.

Page last updated on: