Laptop Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

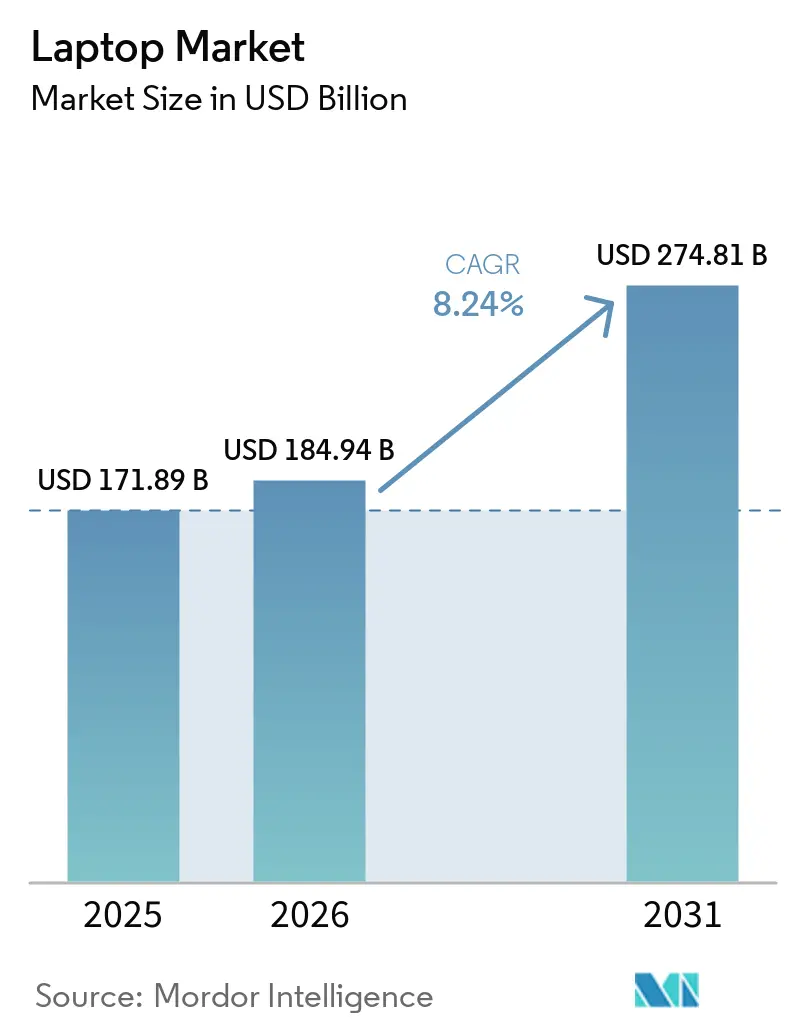

| Market Size (2026) | USD 184.94 Billion |

| Market Size (2031) | USD 274.81 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laptop Market Analysis by Mordor Intelligence

The laptop market size is expected to increase from USD 171.89 billion in 2025 to USD 184.94 billion in 2026 and reach USD 274.81 billion by 2031, growing at a CAGR of 8.24% over 2026-2031. A wave of corporate refreshes triggered by the Windows 10 end-of-support deadline, together with expanding hybrid work patterns, is lifting enterprise demand. Local artificial-intelligence processing is now a mainstream hardware requirement, so buyers view neural processing units as essential rather than optional. Memory shortages that sent DRAM prices up 40-50% in early 2025 pushed average selling prices higher even as unit shipments climbed. Government education programs across the Asia-Pacific created an additional volume backbone, especially for sub-USD 500 Chromebooks. Meanwhile, right-to-repair rules in the United States and Europe are nudging product design toward modular components and extended service life.

Key Report Takeaways

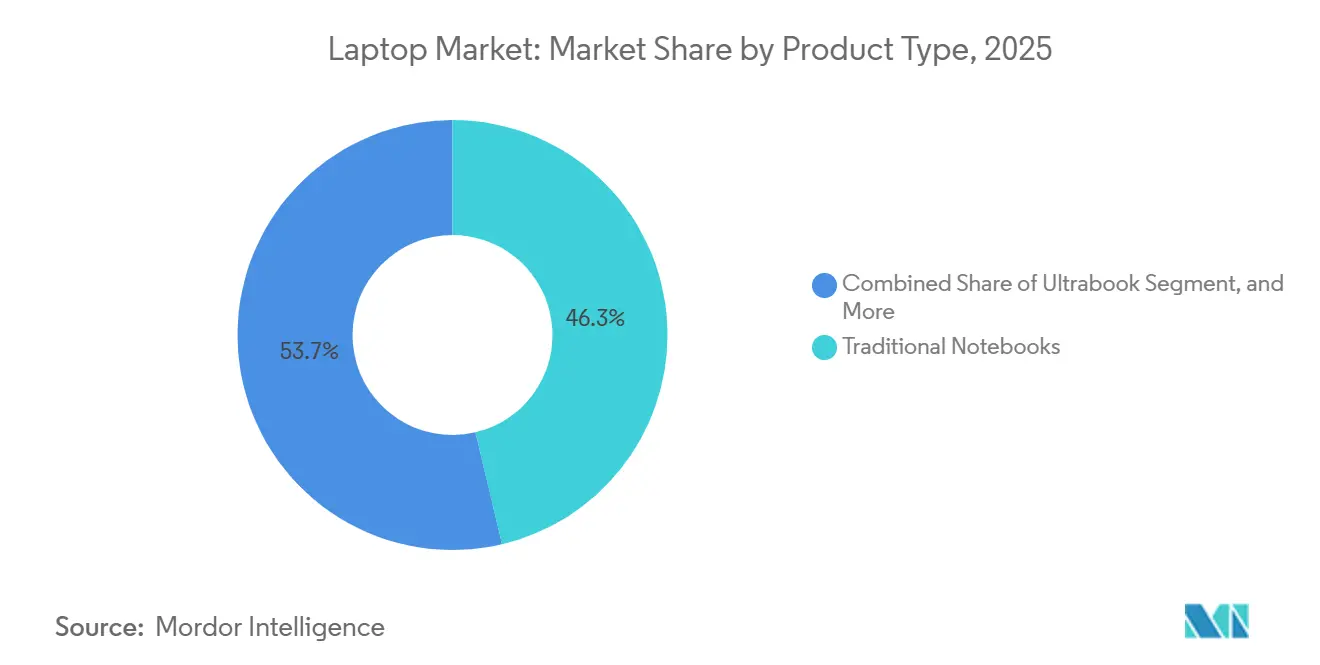

- By product type, traditional notebooks led with 46.31% revenue share in 2025, while 2-in-1 convertibles posted the fastest forecast growth at a 9.24% CAGR through 2031.

- By screen size, the 13–15-inch bracket held 41.24% of the laptop market share in 2025, whereas displays above 17 inches are projected to expand at a 9.04% CAGR through 2031.

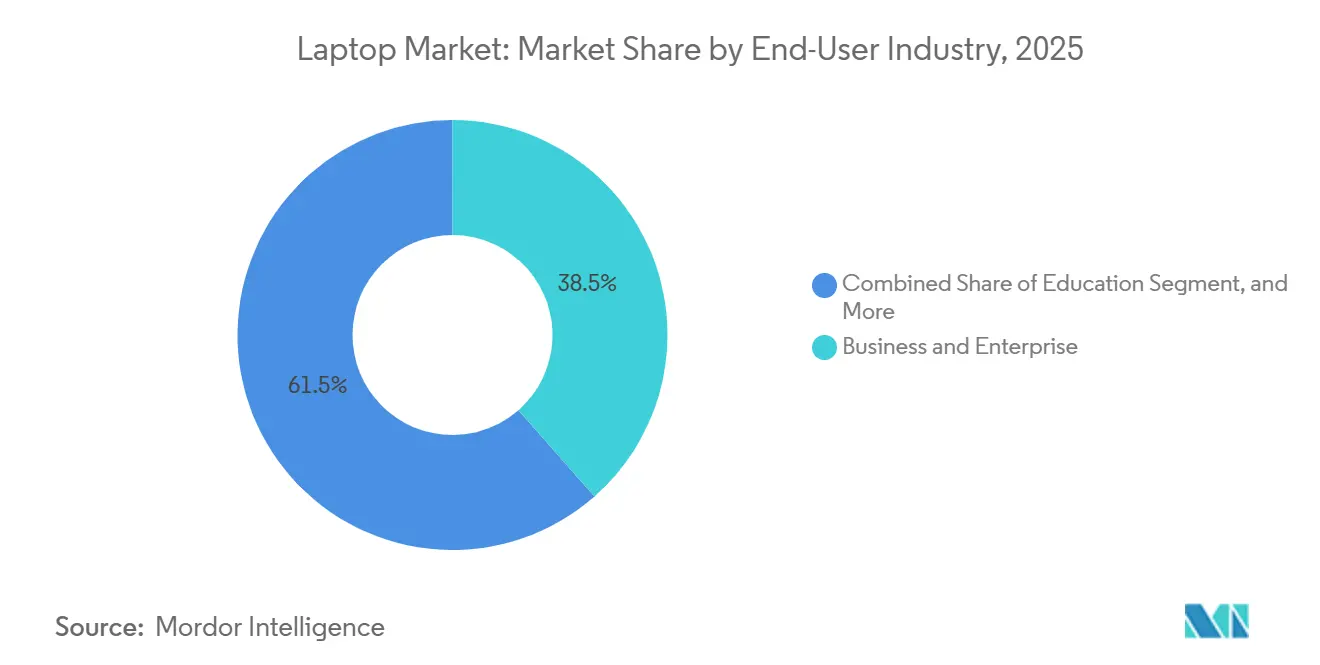

- By end-user industry, business and enterprise buyers delivered 38.53% of 2025 revenue, yet gaming and esports laptops are set to grow at a 9.16% CAGR through 2031.

- By distribution channel, online sales commanded 56.32% of 2025 revenues and are on track for an 8.92% CAGR during 2026-2031.

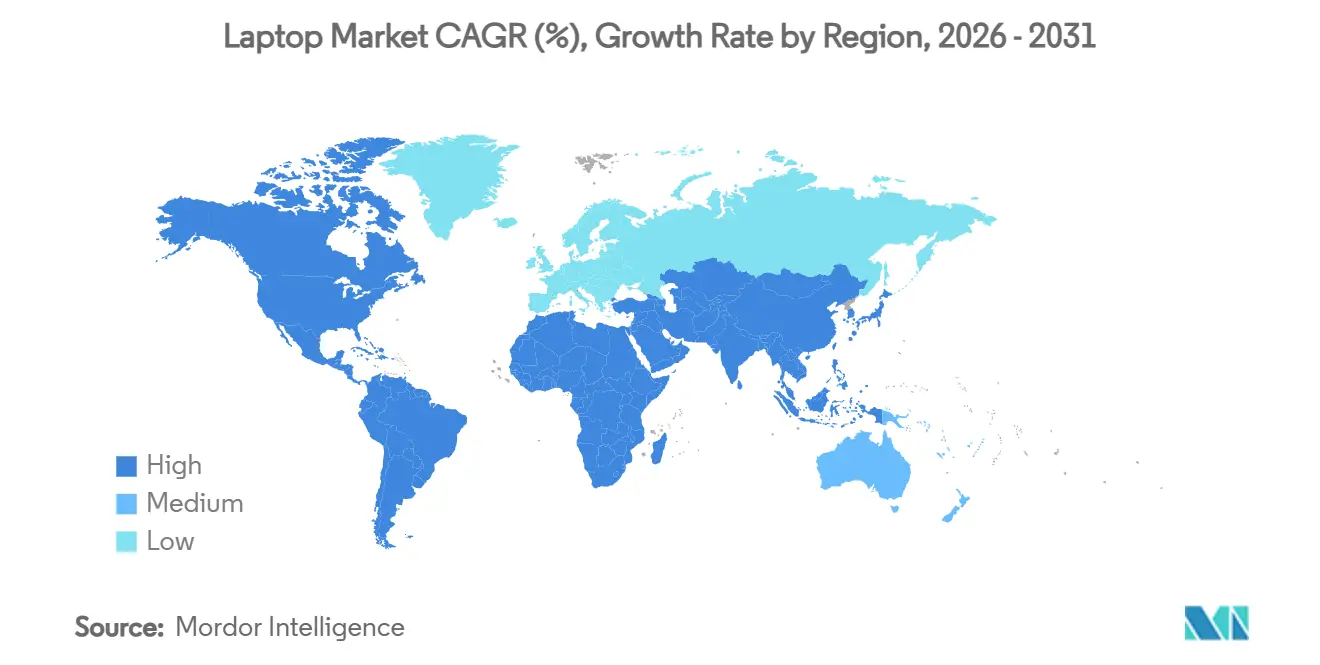

- By geography, North America accounted for 33.19% of the 2025 value, while Asia-Pacific is forecast to be the fastest-growing region at an 8.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laptop Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Corporate Refresh Cycles Post Hybrid Work Adoption | +2.1% | North America and Europe, spill-over global | Short term (≤ 2 years) |

| On-Device Artificial Intelligence Processing Demand | +1.8% | North America, Europe, China, Japan, South Korea | Medium term (2-4 years) |

| Education Digitization Mandates in Asia-Pacific | +1.5% | Philippines, Thailand, India, Hong Kong | Medium term (2-4 years) |

| Gaming Laptops Penetrating Emerging Markets | +1.2% | India, Vietnam, Indonesia, Brazil, Argentina | Long term (≥ 4 years) |

| Battery Density Advances Enabling Ultra-Thin Form Factors | +0.9% | Global, early uptake in North America and Europe | Long term (≥ 4 years) |

| Right-to-Repair Legislation Boosting Upgrade Kits | +0.6% | Europe, California, New York, Minnesota, Oregon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Corporate Refresh Cycles Post Hybrid Work Adoption

The October 2025 Windows 10 end-of-support milestone left enterprises with the choice between escalating Extended Security Update fees and immediate migration to Windows 11. Organizations managing more than 500 endpoints calculated that three-year ESU costs outstripped the capital outlay for new hardware. Hybrid schedules intensified performance demands because employees expect eight hours of video calls without throttling. Fleet buyers, therefore, standardized on 16 GB memory and 512 GB NVMe storage, specifications once reserved for premium tiers.

On-Device Artificial Intelligence Processing Demand

Microsoft’s Copilot+ certification requires at least 40 TOPS of neural throughput, a benchmark that, as of early 2026, is achieved only by the most advanced processors from Intel, AMD, Qualcomm, and Apple. This high-performance requirement underscores the growing demand for cutting-edge hardware capable of supporting complex AI workloads. Enterprises increasingly prefer local inference solutions due to their ability to eliminate cloud latency, which is critical for real-time applications, and to ensure compliance with stringent data-residency regulations, particularly in sectors like finance and healthcare. Although software support for these systems remains in its early stages, the trend of hardware adoption often precedes the optimization of applications. This dynamic creates a positive feedback loop, where the growing installed base of hardware, expected to surpass 30 million units, drives further advancements in software development and application performance, ultimately accelerating the adoption of AI-driven technologies across industries.[1]Intel Corporation, “Core Ultra Series 2 Product Brief,” intel.com

Education Digitization Mandates in Asia-Pacific

Government initiatives promoting one-device-per-student programs have significantly influenced regional procurement strategies. For instance, in the Philippines, the government in Manila allocated funds to procure 64,816 laptops, amounting to PHP 1.913 billion (approximately USD 33.5 million), specifically targeting rural schools to enhance digital education access. Similarly, Thailand has committed THB 29.76 billion (around USD 827 million) for the second phase of its program, which aims to provide devices to 600,000 students, further supporting the country's digital learning infrastructure. In Hong Kong, the government extended its subsidy program, offering HKD 4,900 (equivalent to USD 628) per student annually, ensuring continued support for digital education until 2027. These initiatives predominantly favor Chromebooks and budget-friendly Windows devices, particularly in the sub-USD 400 price segment, driving substantial demand for high-volume, cost-effective solutions in the education market.

Gaming Laptops Penetrating Emerging Markets

Esports viewership has significantly contributed to hardware sales growth, as rising tournament prize pools have legitimized gaming as a viable profession. This trend has driven demand for laptops equipped with NVIDIA RTX 4060 graphics cards and 16 GB of DDR5 memory, available in the USD 800-1,200 price range. These devices are particularly appealing to middle-income consumers in emerging markets such as India, Vietnam, and Brazil. Additionally, the portability of these laptops, which allows them to function as both gaming and study devices, has helped to alleviate parental concerns, further boosting their adoption among younger users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Vulnerability to Rare-Earth Metals | -1.3% | Global exposure, acute in North America and Europe | Medium term (2-4 years) |

| Lengthening Replacement Cycles in Developed Regions | -1.1% | United States, Canada, Western Europe, Japan | Long term (≥ 4 years) |

| Tablet and Smartphone Cannibalization | -0.8% | Global consumer segment | Long term (≥ 4 years) |

| Rising Geopolitical Tariffs on Semiconductors | -0.7% | North America and Europe on imports from Asia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerability to Rare-Earth Metals

China controls approximately 70% of global rare-earth production and 90% of refining, making it a dominant player in the market. In 2025, the country imposed export quotas, significantly tightening the supply of critical rare-earth elements such as neodymium and dysprosium. These materials are essential for manufacturing high-performance magnets, which are integral components in speaker systems and cooling-fan assemblies. The restricted supply has led to increased magnet costs, directly impacting production expenses for original equipment manufacturers (OEMs). While substituting ferrite magnets offers a cost-effective alternative, it compromises audio fidelity, forcing OEMs to balance cost efficiency with product quality. This challenge is expected to persist until alternative refining capacities in regions like the United States and Australia become operational, which could help diversify the supply chain and reduce dependency on China.

Lengthening Replacement Cycles in Developed Regions

Consumer refresh intervals extended from 4.2 years in 2020 to 5.7 years in 2025 as performance needs plateaued for everyday tasks, such as web browsing, video streaming, and basic productivity applications. This trend reflects the diminishing returns of hardware upgrades for non-specialized users. Right-to-repair statutes, introduced to promote sustainability and reduce electronic waste, now compel manufacturers to ensure parts availability for up to a decade. This regulation enables third-party technicians to replace components like batteries, keyboards, and screens at significantly lower costs compared to original equipment manufacturers. Additionally, modular designs, such as Framework’s Laptop 16, allow users to upgrade or replace specific parts, further extending the lifespan of devices. These factors collectively contribute to a slowdown in new-unit sales, particularly in mature economies where consumer demand for cutting-edge performance has stabilized.[2]California Legislative Information, “SB 244 Right to Repair Act,” leginfo.legislature.ca.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Convertibles Close the Gap With Clamshells

Traditional notebooks generated 46.31% of 2025 revenue, anchoring the laptop market size for enterprise fleet buyers. These devices remain a preferred choice for businesses due to their reliability, cost-effectiveness, and compatibility with existing IT infrastructure. However, 2-in-1 convertibles are projected to capture the highest growth at a 9.24% CAGR, driven by the increasing demand for versatile devices that cater to hybrid work environments. As flexible work habits continue to evolve, features such as touch and pen input are becoming more valuable than raw processing power. The laptop market share for convertibles has already seen significant growth in the USD 800-1,200 price band, where factors like hinge durability, stylus latency, and overall build quality heavily influence purchase decisions. This trend highlights a shift in consumer and enterprise preferences toward devices that offer both functionality and adaptability.

Convertibles now replicate tablet convenience without sacrificing keyboard ergonomics, persuading knowledge workers who once juggled two devices. Modular entries like Framework’s Laptop 16 demonstrate user-serviceable concepts, yet high entry prices keep adoption niche for now. Ultrabooks face compression because silicon-anode batteries allow clamshell designs to match their thin-and-light profile without steep premiums. Chromebooks remain an education staple, while rugged laptops depend more on infrastructure spending than consumer appetite.

By Screen Size: Large Panels Ride Content-Creation Momentum

Screens between 13 and 15 inches remained the sweet spot at 41.24% of 2025 revenue, sustaining the core of the laptop market. These screen sizes strike a balance between portability and usability, making them ideal for both professional and personal use. Displays above 17 inches are forecast to expand at a 9.04% CAGR, reflecting the growing demand from creators and analysts who require larger, color-accurate workspaces for tasks such as video editing, graphic design, and data analysis. The laptop market size for these large-panel configurations benefits significantly from advancements like USB-C PD 3.1, which enables mobile workstations to operate without the need for heavy power adapters, enhancing their portability and convenience.

Gaming cafés in tier-2 Asian cities have increasingly shifted toward 17-inch rigs that patrons can carry between venues, driving demand for laptops with reinforced hinges, spill-resistant keyboards, and enhanced durability. This trend highlights the importance of robust design features in catering to the needs of this growing segment. Meanwhile, under-13-inch ultraportables continue to serve niche markets such as healthcare professionals conducting rounds and field sales representatives who prioritize lightweight devices. However, these ultraportables account for less than 10% of total shipments. Recent advancements in battery density have also contributed to the evolution of laptop designs, with even 14-inch models now weighing approximately 1 kg. This development has effectively reduced the traditional trade-off between screen size and portability, making mid-sized laptops more appealing to a broader audience.

By End-User Industry: Gaming Growth Outpaces Corporate Steadiness

Enterprise procurement delivered 38.53% of 2025 spending and is expected to remain a significant driver of the market, as organizations continue to refresh their hardware every three years to ensure compatibility with evolving software requirements and maintain compliance. This segment is particularly critical for industries such as finance, healthcare, and IT services, where performance and security are paramount. Meanwhile, gaming and esports laptops are projected to grow at a robust 9.16% CAGR, outpacing all other verticals. The rise of sponsorship opportunities, collegiate leagues, and professional gaming tournaments has transformed competitive gaming into a viable career path, significantly expanding the total addressable audience, particularly in emerging markets like India, Indonesia, and Brazil.

Consumer and student buyers remain the largest contributors in terms of unit volume; however, the lower average selling prices in these segments dilute their overall revenue share. The education sector, in particular, has seen concentrated demand in regions such as Asia-Pacific and Africa, where affordable, cloud-managed Chromebooks are increasingly adopted by schools and institutions, effectively locking users into specific ecosystems. Additionally, government and defense contracts, while representing a smaller portion of the market, command significantly higher margins. This is due to the specialized requirements for ruggedized designs, enhanced durability, and advanced encryption features, which drive up the bill-of-materials costs well beyond those of standard consumer-grade laptops.

By Distribution Channel: Online Platforms Extend Lead but Services Matter

E-commerce captured 56.32% of 2025 spend and is projected to advance at an 8.92% CAGR. The growing preference for online platforms is driven by the convenience of same-day delivery and configure-to-order options, which allow buyers to customize memory and storage without incurring retail markups. This trend has significantly contributed to the growth of the overall laptop market. While brick-and-mortar showrooms continue to attract customers who prefer to physically test keyboards or displays before purchasing, many of these interactions ultimately result in online transactions, highlighting the shift in consumer behavior.

Direct-to-enterprise contracts have evolved to include additional services such as imaging, asset tagging, and lifecycle recycling, all bundled into predictable per-seat fees. These comprehensive agreements help protect OEM margins from the intense price transparency that dominates consumer channels, ensuring profitability. Offline retail, although still relevant in regions where cash transactions are prevalent, is gradually losing its edge as mobile payment platforms gain traction and reduce the reliance on cash-based purchases. This shift is further reshaping the retail landscape, emphasizing the growing dominance of digital payment systems and e-commerce platforms.

Geography Analysis

North America accounted for 33.19% of total revenue in 2025, driven by fleet migrations associated with Windows 11 upgrades and CHIPS Act sourcing incentives. These factors supported shipments in the region; however, future growth is expected to moderate as consumer replacement cycles extend beyond five years. Additionally, the presence of Mexican assembly plants in Monterrey and Guadalajara has played a crucial role in shortening lead times and reducing tariff exposure for customers in the United States, further strengthening the region's supply chain efficiency.

Asia-Pacific is anticipated to experience the fastest regional growth, with a projected CAGR of 8.78%. Large-scale education deployments and the rapid adoption of esports in secondary cities fuel this growth. Government subsidies that lower device prices to below USD 400 have significantly boosted high-volume orders in the region. Thailand allocated THB 4.21 billion (USD 117 million) initially and committed THB 29.76 billion (USD 827 million) for Phase 2, targeting 600,000 high-school students with preloaded educational software.[3]Ministry of Education Thailand, “Digital Learning Initiative,” moe.go.th While China remains the largest country by unit shipments, its economic slowdown has tempered expansion. In contrast, countries like India, Vietnam, and Indonesia are witnessing accelerated growth due to rising disposable incomes and increasing demand for affordable devices.

Europe is expected to maintain stable mid-single-digit growth rates, supported by ecodesign regulations that mandate spare-part availability, thereby extending device lifespans. Although these regulations curb unit volumes, they increase service revenue. Meanwhile, South America, the Middle East, and Africa are experiencing growth from a smaller base, as consumers who primarily relied on smartphones are now adopting laptops for productivity tasks. The introduction of instant payment systems, such as Brazil's PIX, has reduced friction in online transactions, enabling e-commerce to gain market share from traditional, cash-dominant retail channels in these regions.

Competitive Landscape

The top five brands, Lenovo, HP, Dell, Apple, and ASUS, accounted for approximately 65-70% of 2025 shipments, reflecting a moderately concentrated laptop market. Lenovo capitalizes on its extensive scale in the Asia-Pacific region, while Apple secures the highest revenue per unit by leveraging its macOS ecosystem, which locks in users. HP and Dell stand out by offering device-as-a-service contracts, enabling businesses to shift spending from capital expenditure to operating expenditure, thereby safeguarding corporate margins.[4]Apple Inc., “Apple Introduces M4 Pro and M4 Max,” apple.com Meanwhile, ASUS and Acer focus on delivering competitive price-performance ratios, particularly in the consumer and gaming segments.

Emerging modular challengers, such as Framework, emphasize repairability, aligning with the growing adoption of right-to-repair laws. However, their higher pricing limits their appeal to a broader audience. Additionally, new entrants like System76 and Huawei are targeting niche markets by catering to specific operating system preferences and fostering domestic ecosystems. The ongoing technological race is now centered on the development of integrated neural processors capable of exceeding 50 TOPS while maintaining thermal envelopes below 15 watts, showcasing advancements in efficiency and performance.

Design innovations, particularly in hinges and cooling solutions, suggest that convertible laptops will remain a key area for margin differentiation. These advancements are expected to drive further carket acompetition s brands seek to enhance user experience and functionality. The focus on convertibles underscores the industry's efforts to meet evolving consumer demand for versatile, adaptable devices, ensuring sustained growth in this segment.

Laptop Industry Leaders

Lenovo Group Limited

HP Inc.

Dell Technologies Inc.

Apple Inc.

ASUSTeK Computer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Lenovo began a USD 500 million expansion of its Hefei campus, adding 2 million laptops to its annual capacity and using AI-driven inspection to cut defect rates by 15%.

- February 2026: Dell unveiled the Latitude 7450 with Intel Core Ultra Series 2 processors delivering 48 TOPS NPU performance and a user-replaceable battery compliant with EU repair rules.

- January 2026: HP integrated Amprius silicon-anode batteries into the EliteBook 1040 G11, achieving 18 hours of runtime in a 1.2 kg chassis.

- December 2025: ASUS released the ROG Zephyrus G16 with NVIDIA RTX 5070 graphics and a 240 Hz OLED panel aimed at esports professionals.

Global Laptop Market Report Scope

The Laptop Market refers to the global industry encompassing the design, manufacture, distribution, and sale of portable computing devices that integrate essential hardware components, such as processors, memory, storage, displays, keyboards, and batteries, into a single mobile system. These devices are engineered to provide computing capability across personal, professional, educational, gaming, and industrial applications while enabling mobility and flexibility of use.

The Laptop Market Report is Segmented by Product Type (Traditional Notebook, Ultrabook, 2-in-1 Convertible, Chromebook, and Rugged Laptop), Screen Size (Below 13 Inches, 13-15 Inches, 15-17 Inches, and Above 17 Inches), End-User Industry (Consumer, Business and Enterprise, Gaming and Esports, Education, and Government and Defense), Distribution Channel (Online, Offline Retail, and Direct to Enterprise), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Traditional Notebook |

| Ultrabook |

| 2-in-1 Convertible |

| Chromebook |

| Rugged Laptop |

| Below 13 Inches |

| 13-15 Inches |

| 15-17 Inches |

| Above 17 Inches |

| Consumer |

| Business and Enterprise |

| Gaming and Esports |

| Education |

| Government and Defense |

| Online |

| Offline Retail |

| Direct to Enterprise |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Traditional Notebook | ||

| Ultrabook | |||

| 2-in-1 Convertible | |||

| Chromebook | |||

| Rugged Laptop | |||

| By Screen Size | Below 13 Inches | ||

| 13-15 Inches | |||

| 15-17 Inches | |||

| Above 17 Inches | |||

| By End-User Industry | Consumer | ||

| Business and Enterprise | |||

| Gaming and Esports | |||

| Education | |||

| Government and Defense | |||

| By Distribution Channel | Online | ||

| Offline Retail | |||

| Direct to Enterprise | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the laptop market be by 2031?

The laptop market is projected to reach USD 274.81 billion by 2031, expanding at an 8.24% CAGR from 2026-2031.

What segment is growing fastest in laptops?

2-in-1 convertibles are expected to lead growth with a 9.24% CAGR through 2031 as hybrid work favors flexible form factors.

Which region will see the highest laptop growth?

Asia-Pacific is forecast to post the fastest regional CAGR at 8.78%, driven by government education programs and esports demand.

Why are AI-ready laptops important now?

Microsoft Copilot+ certification demands NPUs that deliver at least 40 TOPS, enabling local AI features that cut latency and protect sensitive data.

How are right-to-repair laws affecting laptop design?

Regulations in California and the European Union require spare-part availability for up to a decade, pushing OEMs toward modular components and longer service life.

Page last updated on: