Higher Education Learning Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

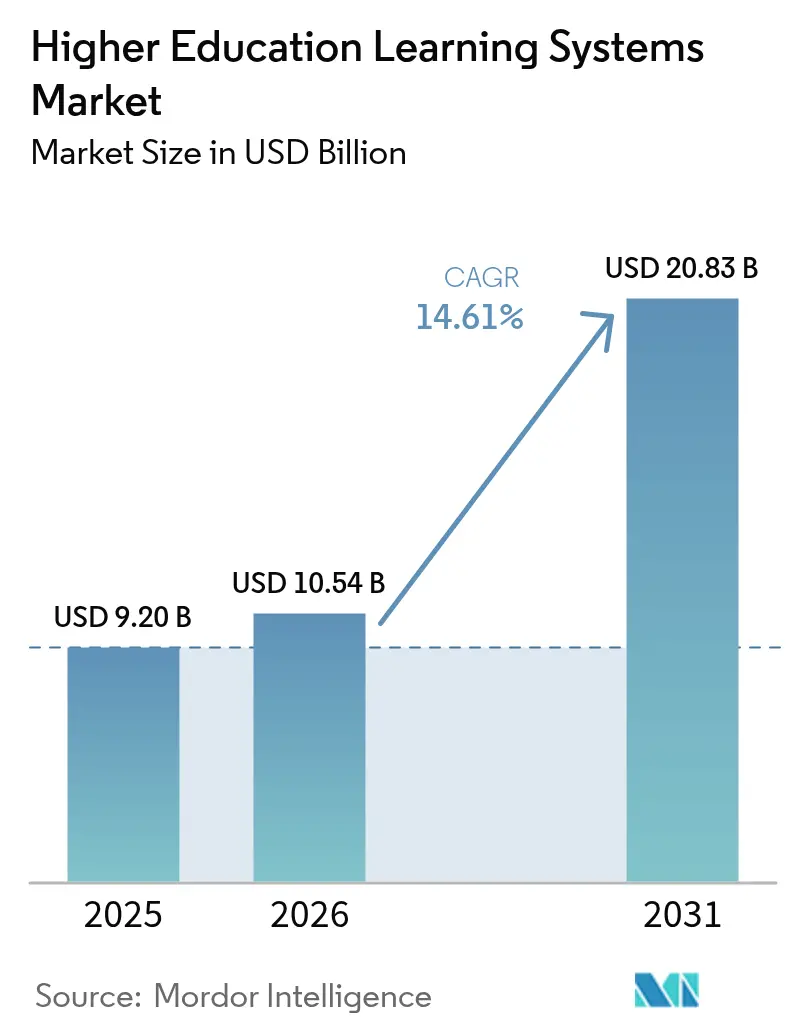

| Market Size (2026) | USD 10.54 Billion |

| Market Size (2031) | USD 20.83 Billion |

| Growth Rate (2026 - 2031) | 14.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Higher Education Learning Systems Market Analysis by Mordor Intelligence

The higher education learning systems market size was valued at USD 9.20 billion in 2025 and estimated to grow from USD 10.54 billion in 2026 to reach USD 20.83 billion by 2031, at a CAGR of 14.61% during the forecast period (2026-2031). Rapid cloud adoption, the mainstreaming of AI-powered personalization, and government stimulus programs are reshaping institutional technology strategies while intensifying competition among platform vendors. Institutions are prioritizing SaaS deployments to curb data center spending, deliver anywhere access for mobile learners, and simplify version management. AI-driven recommendation engines embedded in learning-management platforms are enhancing retention by identifying at-risk students earlier, prompting a shift from focusing on feature quantity to achieving measurable student success outcomes. Meanwhile, tight cybersecurity mandates and widening skills gaps in EdTech administration temper rollout velocity, creating robust demand for specialized services that guide migrations and change management.

Key Report Takeaways

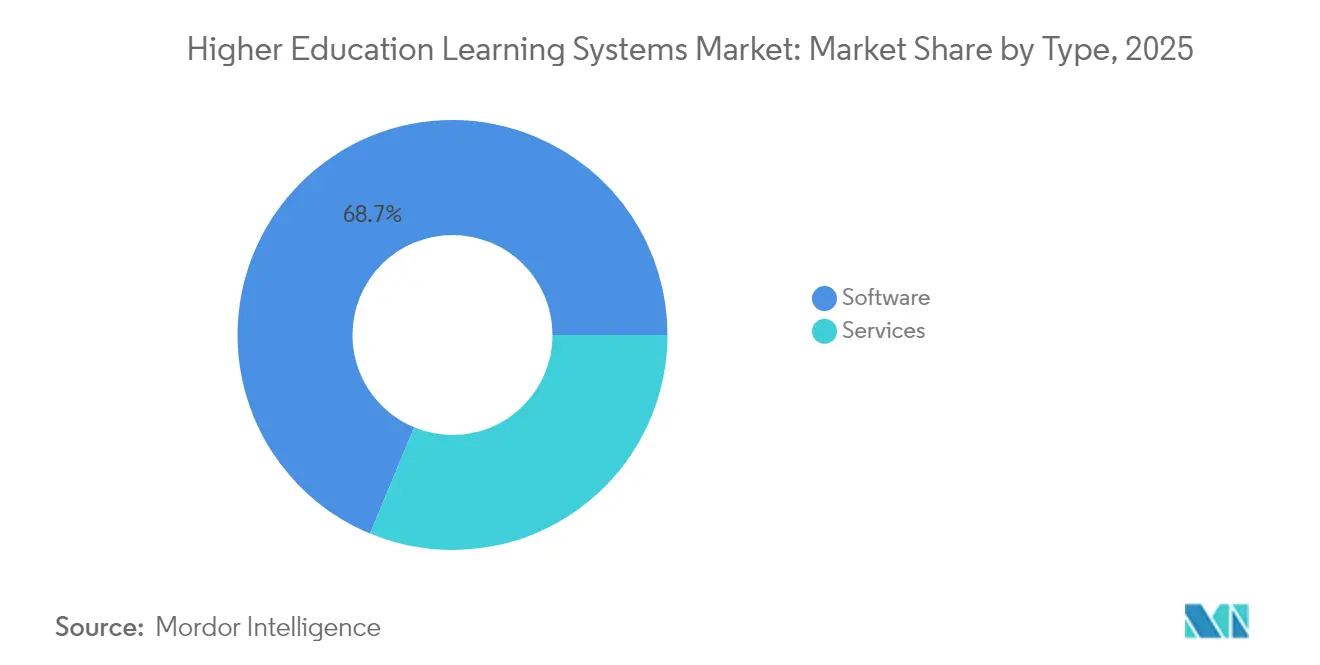

- By type, software accounted for 68.74% of the higher education learning systems market share in 2025, whereas the services segment is forecast to grow at a 15.94% CAGR to 2031, underscoring the mounting complexity of implementation.

- By deployment model, cloud deployments held 72.36% of the higher education learning systems market size in 2025 and are expected to expand at a 15.89% CAGR through 2031, as institutions adopt multi-tenant SaaS platforms.

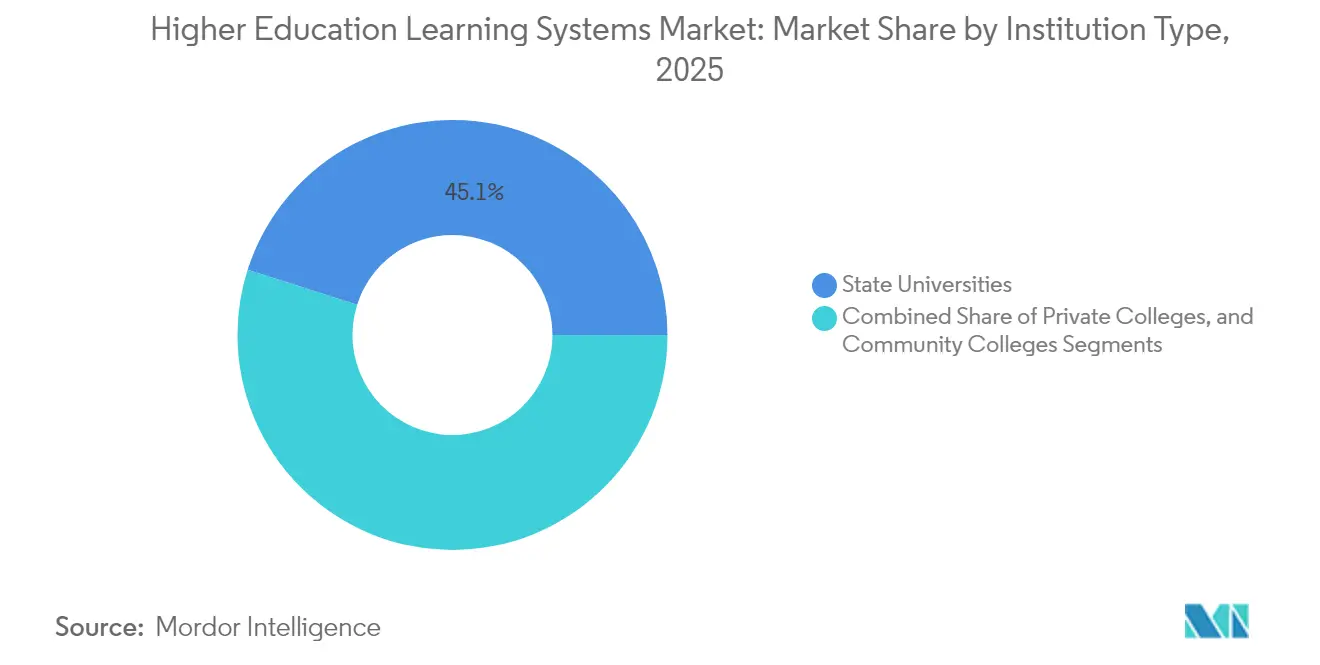

- By institution type, state universities led spending with a 45.10% share in 2025, while community colleges are poised for a 16.63% CAGR on the back of targeted digital equity appropriations.

- By learning mode, hybrid and blended formats captured 40.76% of deployments in 2025 and are projected to grow at a 16.37% CAGR through 2031, reflecting lasting shifts toward flexible pedagogy.

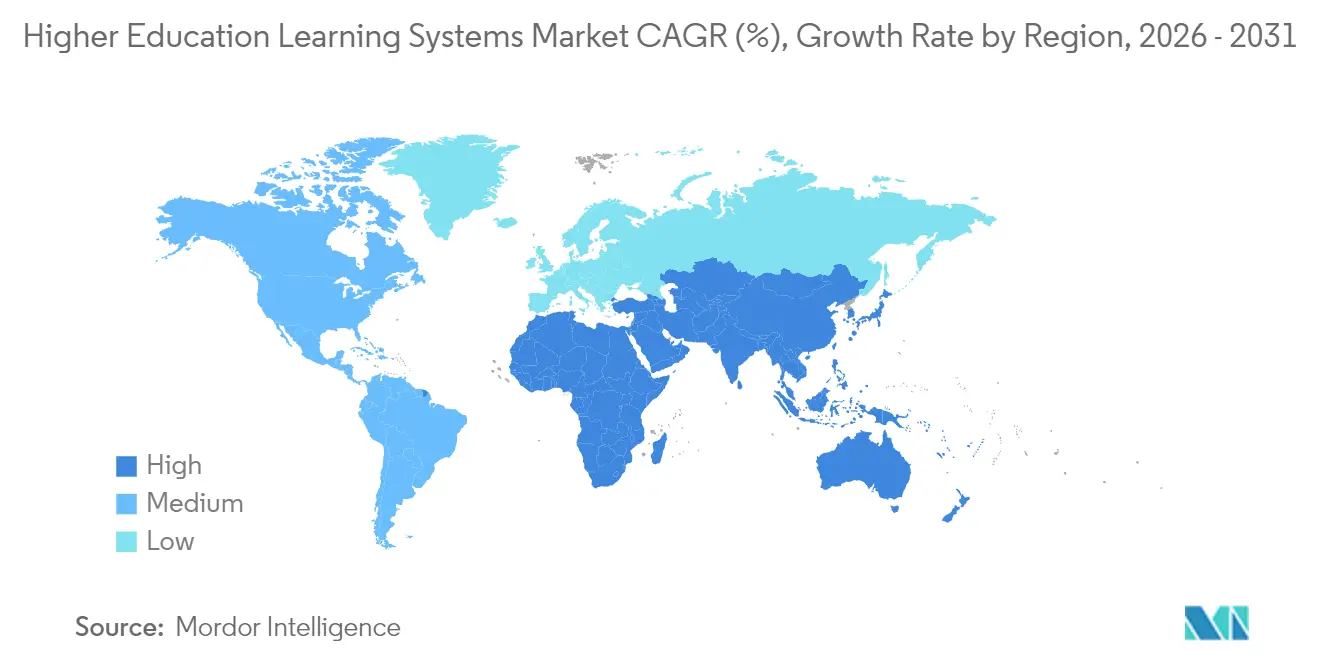

- By geography, North America commanded 39.72% of the 2025 revenue, yet the Asia Pacific is expected to post the fastest regional growth at a 16.94% CAGR through 2031, as China and India scale digital campus initiatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Higher Education Learning Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing cloud-first strategies among higher-ed institutions | +3.2% | Global, with highest adoption in North America and Europe | Short term (≤ 2 years) |

| Proliferation of AI-powered adaptive learning tools | +2.8% | North America, Asia Pacific core, spillover to Europe | Medium term (2-4 years) |

| Government digital-campus stimulus packages | +2.1% | Australia, Ireland, United Kingdom, select US states | Short term (≤ 2 years) |

| Rapid international student mobility driving multi-tenant architectures | +1.7% | North America, United Kingdom, Australia, emerging in Asia Pacific | Medium term (2-4 years) |

| Campus-wide demand for learning analytics dashboards | +1.9% | Global, led by state universities in North America and Europe | Medium term (2-4 years) |

| Sustainability mandates pushing paperless workflows | +1.4% | Europe, North America, select Asia Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Cloud-First Strategies Among Higher-Ed Institutions

Universities are dismantling on-premises data centers in favor of elastic SaaS environments that compress capital outlays, expand uptime, and shorten feature-release cycles. Internet2’s NET+ survey revealed that 78% of member institutions had transitioned at least one core academic system to the cloud by mid-2024, up from 54% in 2022. Australia’s NCRIS fund tied AUD 750 million (USD 488 million) to cloud migration milestones, catalyzing accelerated adoption across the sector.[1]Australian Government Department of Education, “NCRIS 2024 Funding Allocation,” education.gov.au. Cloud platforms also streamline integrations with collaboration and AI services that on-premises stacks struggle to support. Compliance drivers reinforce momentum as ISO/IEC 27001 certification gains de facto status for vendors courting higher education clients. Collectively, these factors contribute more than three percentage points to the higher education learning systems market CAGR during the short term.

Proliferation of AI-Powered Adaptive Learning Tools

AI-driven personalization has moved beyond pilots, scaling across production environments to raise completion metrics. Tel Aviv University’s TAUDT system lowered first-year STEM attrition by 12% in 2024 through natural-language-generated study plans.[2]Tel Aviv University, “TAUDT Impact Report 2024,” tau.ac.il. Pearson’s AI tutor delivered 1.2 million adaptive assessments the same year, lifting remedial-math pass rates by 15%. In early 2025, the University of California deployed predictive early-warning systems system-wide to flag at-risk students, broadening AI reach to 285,000 learners. These successes spur platform vendors to embed machine-learning APIs natively, driving nearly three percentage points of incremental CAGR over the medium term while elevating conversations around algorithmic transparency and IEEE-aligned ethics.

Government Digital-Campus Stimulus Packages

Public-sector infusions are closing funding gaps that tuition revenues cannot bridge. Ireland’s INSPIRE program committed EUR 750 million (USD 848 million) in 2024 to achieve full-cloud adoption by 2027. The U.K. Office for Students distributed GBP 92 million (USD 117 million) to analytics and accessibility projects, contingent on retention improvements. Eighteen U.S. states earmarked FY 2024 appropriations for LMS upgrades and cyber-hardening. These conditional grants hasten procurement cycles, standardize interoperability requirements, and contribute just over two percentage points to forecast expansion.

Campus-Wide Demand for Learning Analytics Dashboards

Real-time data visualizations help faculty track engagement and intervene early. Civitas Learning’s platform, active at 385 institutions in 2024, improved retention by an average of 8%.[3]Civitas Learning, “Deployment Report 2024,” civitaslearning.com. Anthology’s Illuminate logged 42 million dashboard views the same year, facilitating data-informed pacing adjustments. The University of Michigan added a Canvas-based analytics layer in 2025 to alert advisors when submission behaviors deviate from historical norms. These investments add nearly two percentage points to growth as dashboards shift from optional to essential.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cybersecurity and data-privacy compliance costs | -2.3% | Global, with highest burden in North America and Europe due to FERPA and GDPR | Short term (≤ 2 years) |

| Skills gap in EdTech systems administration | -1.8% | Global, acute in community colleges and smaller private institutions | Medium term (2–4 years) |

| Budget freezes at community colleges | -1.4% | United States, select regions in Europe and Latin America | Short term (≤ 2 years) |

| Vendor lock-in concerns over proprietary ecosystems | -1.1% | Global, particularly affecting institutions with legacy on-premises systems | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Cybersecurity and Data-Privacy Compliance Costs

The median security spend per institution reached USD 1.2 million in 2024, a 23% increase from 2022, as FERPA and GDPR audits intensified. European universities faced EUR 1.2 billion in GDPR fines during 2023, driving emergency budget reallocations. The University of California invested USD 14 million in ransomware remediation and monitoring following the 2024 breach. These costs siphon funds from innovation and subtract more than two percentage points from growth during the near term.

Skills Gap in EdTech Systems Administration

In 2024, 62% of IT directors reported difficulty hiring cloud-architecture talent, while 54% cited analytics expertise as a critical gap. Community-college salary disparities exacerbate the shortage, prompting the California Community Colleges system to invest USD 12 million in upskilling 500 staffers.[4]California Community Colleges Chancellor’s Office, “IT Training Initiative 2024,” cccco.edu. Faculty capability gaps persist, dampening feature adoption and dragging CAGR by almost two percentage points over the medium horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Services Address Complexity and Drive Outcomes

Services revenue, including consulting, integration, training, and managed support, is projected to rise at a 15.94% CAGR through 2031, outstripping software, even though the latter captured 68.74% of 2025 spending. Institutions increasingly view platform rollouts as change-management journeys, engaging integrators to migrate legacy content, configure single sign-on, and build custom analytics layers. Accenture’s higher-education practice grew 19% in 2024, driven by demand for cloud-migration roadmaps that align with FERPA and GDPR guardrails. The higher education learning systems market benefits as service providers quantify retention lifts and cost savings, repositioning technology as an outcome driver rather than a procurement checklist.

Ongoing managed-service contracts reduce strain on lean campus IT teams and ensure regulatory patches are applied on schedule. Niche firms specializing in AI-powered tutoring, plagiarism detection, or accessibility remediation monetize open APIs that characterize the higher education learning systems industry. Over the forecast period, institutions will emphasize evidence-based ROI metrics, such as graduation rates, credit completion velocity, and employability, encouraging deeper advisory engagements. As a result, services are set to command a growing slice of the higher education learning systems market by 2031.

By Deployment Model: Cloud Dominance Accelerates

Cloud deployments owned 72.36% of the higher education learning systems market in 2025 and are poised for a 15.89% CAGR through 2031 as SaaS becomes the default for new procurements. The University of Edinburgh completed a three-year migration to AWS in 2025, saving GBP 1.8 million (USD 2.3 million) annually while easing peak-load scaling. FedRAMP, ISO/IEC 27001, and similar attestations are now the minimum entry requirements, boosting confidence in the off-premises storage of sensitive student data. Multi-tenant designs allow vendors to push feature updates without campus downtime, shortening innovation cycles across the higher education learning systems market.

Hybrid models persist where data-residency statutes require local storage or where legacy research compute clusters remain on-site. Nonetheless, even cautious institutions offload compute-intensive tasks, such as video transcoding, to public clouds to manage burst workloads. Reduced maintenance windows, predictable subscription pricing, and automated patching cement cloud’s trajectory, ensuring its share of the higher education learning systems market size widens steadily.

By Institution Type: Community Colleges Lead Growth

Community colleges are forecast to have a 16.63% CAGR through 2031, outpacing their state and private peers as performance-funding policies reward improved completion metrics. California budgeted USD 85 million in 2024 to standardize an LMS across 116 campuses, centralizing analytics and reporting. Affordability pressures are pushing two-year institutions toward SaaS solutions that bundle security, accessibility, and analytics, thereby lowering the total cost of ownership. State universities, which account for 45.10% of the 2025 spending, review technology ROI more rigorously, lengthening procurement cycles while sustaining high absolute expenditures.

Private colleges invest in premium AI coaching and VR labs to differentiate themselves, but face enrollment headwinds that dampen their expansion. The higher education learning systems market share for community colleges is expected to rise as digital equity mandates channel public funds toward underserved learner segments, further diversifying vendor requirements and accelerating volume growth within this customer cohort.

By Learning Mode: Hybrid Models Cement Post-Pandemic Gains

Hybrid and blended courses accounted for 40.76% of deployments in 2025 and are projected to advance at a 16.37% CAGR through 2031, embedding flexible pedagogy into mainstream practice. The University of Central Florida reported hybrid completion rates seven percentage points higher than fully online sections in 2024, demonstrating improved engagement when face-to-face touchpoints are maintained. HyFlex designs empower learners to switch attendance modes each week, necessitating tight video-conferencing integration and real-time polling features within LMS platforms.

Instructor-led formats remain essential for labs and clinical rotations; however, digital simulations now supplement in-person practice, thereby shortening seat-time requirements. Self-paced enrollment surges in continuing education, but higher dropout rates spur institutions to embed AI nudges that prompt steady progress. These dynamics ensure that the higher education learning systems market continues to shift toward modality-agnostic architecture, capable of delivering consistent experiences across synchronous and asynchronous channels.

Geography Analysis

North America generated 39.72% of global revenue in 2025, fueled by large state systems, private endowment spending, and robust IT budgets. Mature platform penetration moderates regional CAGR, yet ongoing refresh cycles and analytics upgrades sustain steady expansion. Stringent FERPA compliance obligations and frequent ransomware incidents also drive sustained cybersecurity spending, adding incremental service opportunities.

The Asia Pacific is forecast to lead growth at a 16.94% CAGR through 2031, as China and India deploy national digitization blueprints. China’s Ministry of Education has earmarked CNY 15 billion (USD 2.1 billion) to modernize 200 universities, aiming for 80% cloud adoption by 2027. India’s National Education Policy aims for a 50% gross enrollment rate by 2035, necessitating a massive expansion of online capacity. Southeast Asian governments emulate these models, leveraging multi-tenant architectures to support multilingual users and variable bandwidth conditions.

Europe maintains steady growth underpinned by Erasmus-style student mobility and strict GDPR mandates that elevate vendor vetting. The U.K. Office for Students’ GBP 92 million grant program links funding to analytics-driven retention improvements, stimulating platform upgrades. South America shows uneven progress; Brazil’s public universities adopt LMS platforms quickly, whereas smaller economies struggle with connectivity. The Middle East, led by Saudi Arabia’s USD 1.3 billion Vision 2030 EdTech plan, prioritizes smart campus rollouts to diversify its economies. Africa remains nascent, yet it records pockets of double-digit growth as distance learning addresses rural access.

Competitive Landscape

The higher education learning systems market exhibits moderate concentration, with the top five vendors capturing approximately 55% of the 2024 software revenue. Instructure, Anthology, and Blackboard defend incumbency through bundled enterprise agreements that integrate LMS, SIS, and analytics, leveraging data lock-in to deter churn. However, interoperability standards like IMS Global’s Learning Tools Interoperability compel providers to open APIs, lowering switching barriers and enabling multi-vendor ecosystems.

Open-source contender Moodle reported 420 million users across 245,000 sites in 2024, underscoring its potential for fragmentation. AI-native upstarts deliver standalone analytics or adaptive-learning engines that can be bolted onto any LMS, exploiting incumbents’ slower innovation cycles. Patent activity in automated grading and natural language processing rose sharply, with IBM, Oracle, and SAP each filing more than 20 education-related patents in 2024. Accessibility compliance to WCAG 2.1 AA and Section 508 emerges as a differentiator, as litigation risk rises for non-conforming platforms.

Strategic moves reinforce competitive intensity. Instructure committed USD 150 million in 2025 to scale its AI assistant across 1,200 institutions. Anthology’s USD 320 million acquisition of Civitas fused LMS and predictive analytics capabilities, serving 40 million students globally. Ellucian partnered with Microsoft Azure to integrate AI services into its ERP suites, enabling the use of chatbots and predictive enrollment models. These maneuvers signal continued convergence of content delivery, analytics, and administrative workflows under unified vendors, even as modular architectures invite specialist plug-ins.

Higher Education Learning Systems Industry Leaders

Cornerstone OnDemand, Inc.

Jenzabar, Inc.

Blackboard Inc.

SAP SE

Desire2Learn Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Instructure announced a USD 150 million investment to extend its AI learning assistant across Canvas LMS, targeting 1,200 institutions by mid-2026.

- April 2025: Moodle released version 4.5 featuring WCAG 2.2 accessibility upgrades and native H5P support.

- March 2025: Workday expanded Workday Student to support competency-based education tracking.

- January 2025: Pearson partnered with Google Cloud to apply generative AI for faster courseware updates.

Global Higher Education Learning Systems Market Report Scope

A Higher Education Learning Systems is a web-based or cloud-based software program which assist in the teaching-learning process and helps in the effective delivery of instruction, training, and development program. The learning system in higher education facilitates learners, instructors, and administrators to use and access to services and is beyond the restriction of time and place in the teaching and learning process.

The Higher Education Learning Systems Market Report is Segmented by Type (Software, Services), Deployment Model (Cloud, On-Premises), Institution Type (State Universities, Private Colleges, Community Colleges), Learning Mode (Instructor-Led, Self-Paced, Hybrid/Blended), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| State Universities |

| Private Colleges |

| Community Colleges |

| Instructor-Led |

| Self-Paced |

| Hybrid/Blended |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Type | Software | ||

| Services | |||

| By Deployment Model | Cloud | ||

| On-Premises | |||

| By Institution Type | State Universities | ||

| Private Colleges | |||

| Community Colleges | |||

| By Learning Mode | Instructor-Led | ||

| Self-Paced | |||

| Hybrid/Blended | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the higher education learning systems market in 2026?

The higher education learning systems market size is USD 10.54 billion in 2026, and it is on track to hit USD 20.83 billion by 2031.

Which deployment model is growing fastest?

Cloud deployments are expanding at a 15.89% CAGR through 2031 as institutions prefer SaaS for cost control and rapid feature updates.

Why are community colleges investing heavily in learning systems?

State-level performance funding and digital-equity mandates are driving a 16.63% CAGR for community colleges, the fastest among institution types.

What is the main driver of hybrid learning adoption?

Higher completion rates and scheduling flexibility push hybrid and blended formats, which already hold 40.76% share and are growing at 16.37% CAGR.

Page last updated on: