Mobile Learning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

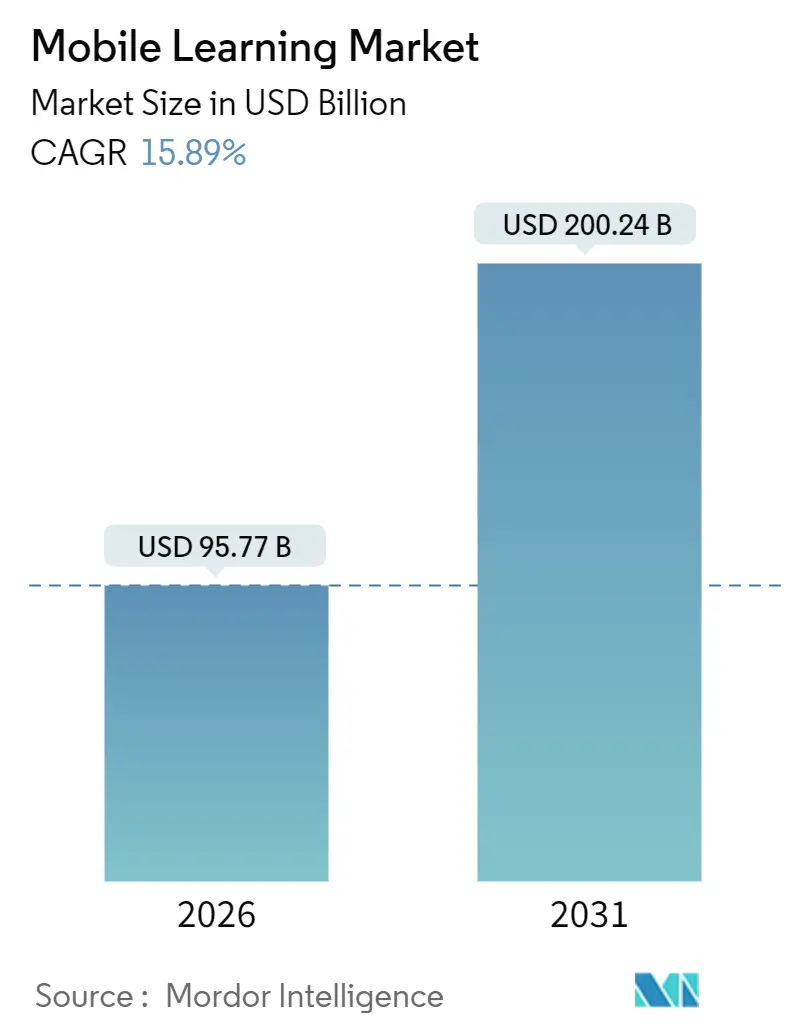

| Market Size (2026) | USD 95.77 Billion |

| Market Size (2031) | USD 200.24 Billion |

| Growth Rate (2026 - 2031) | 15.89% CAGR |

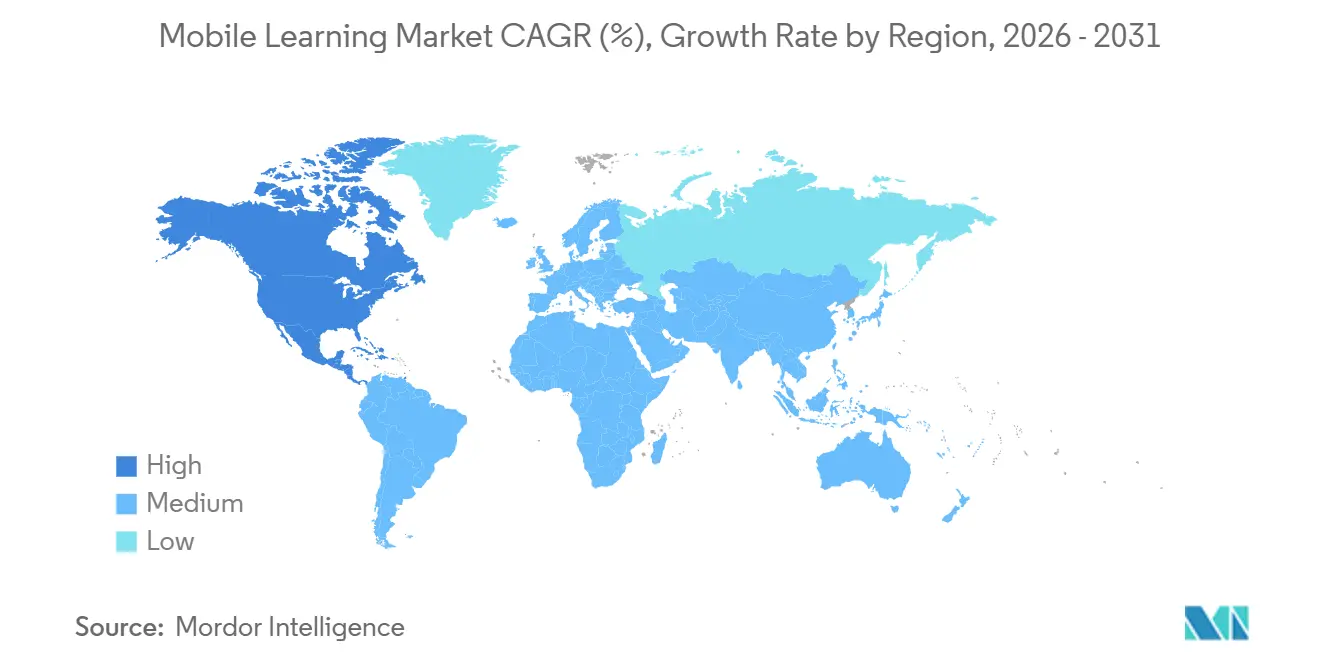

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Learning Market Analysis by Mordor Intelligence

The Mobile Learning Market size is estimated at USD 95.77 billion in 2026, and is expected to reach USD 200.24 billion by 2031, at a CAGR of 15.89% during the forecast period (2026-2031).

This strong trajectory is supported by broad 5G coverage, rapid smartphone adoption, and enterprise-wide bring-your-own-device mandates that reduce hardware expenditures while maintaining security compliance. Generative AI now tailors micro-modules to each learner, raising completion rates and shortening time-to-proficiency, while portable stackable credentials appeal to gig-economy workers who need employer-agnostic proof of skill. Content retrofitting, rather than green-field development, attracts the bulk of near-term capital, as converting existing desktop courses into responsive formats reduces deployment cycles from months to weeks. Vendors that bundle curation, delivery, and analytics into a single subscription have started to gain market share, yet the addressable pool remains fragmented, leaving ample room for niche specialists across highly regulated verticals. Advances in adaptive-bitrate streaming and offline synchronization further widen the audience, reaching learners in bandwidth-constrained regions and ensuring the mobile learning market continues to outpace legacy e-learning alternatives.

Key Report Takeaways

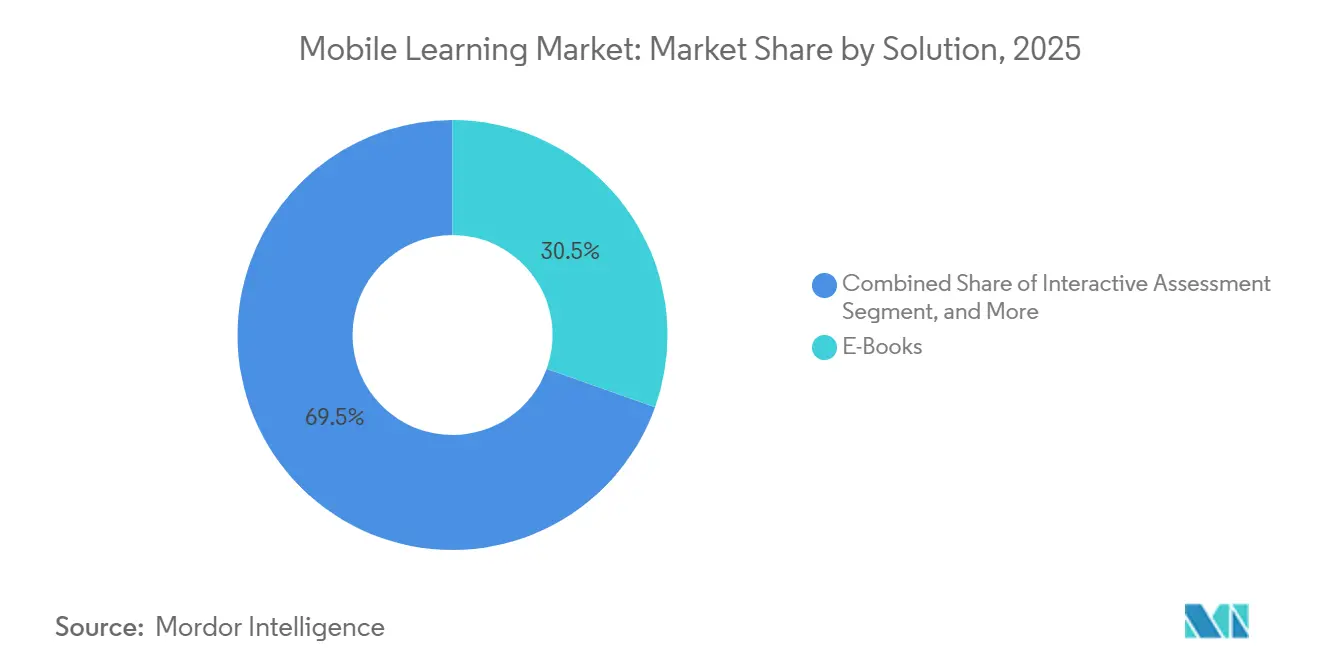

- By solution, e-books led with 30.46% revenue share in 2025, whereas m-enablement is set to grow at a 16.82% CAGR through 2031.

- By application, in-class learning accounted for 36.67% of spending in 2025, while simulation-based learning is forecast to expand at 17.33% CAGR to 2031.

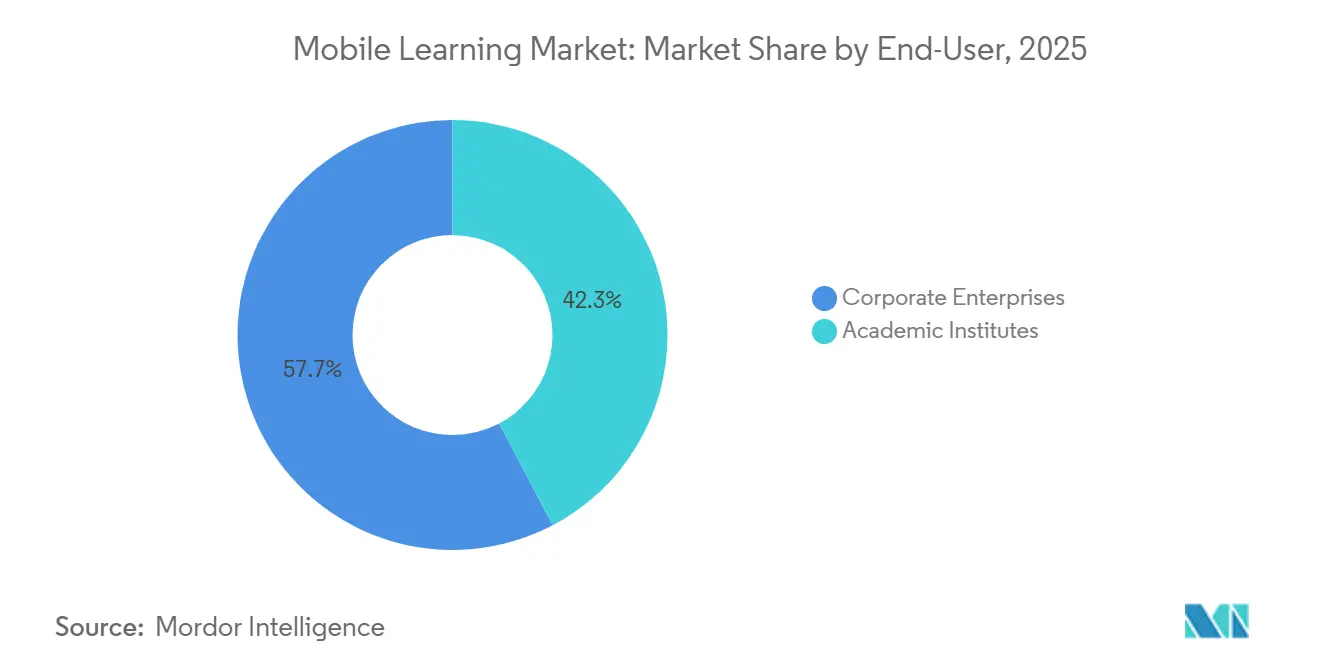

- By end-user, academic institutes held 42.27% of 2025 outlays, whereas corporate enterprises are advancing at a 16.02% CAGR over the forecast horizon.

- By provider type, content providers commanded 36.59% revenue in 2025 and are projected to increase at 17.83% CAGR to 2031.

- By geography, North America held 31.36% of 2025 revenue share, yet Asia Pacific is pacing the field with a 18.15% regional CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Mobile Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Digital Learning Solutions in Corporate L&D | +5.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Bring-Your-Own-Device (BYOD) Policies Across Enterprises | +4.1% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Rising Global Penetration of Smartphones, Tablets and Laptops | +6.3% | Global, with fastest growth in APAC and Middle East | Long term (≥ 4 years) |

| Global 5G Roll-Out Enabling High-Definition Video and AR Mobile Courses | +4.8% | APAC core, North America, selective Middle East markets | Medium term (2-4 years) |

| AI-driven Hyper-Personalised Micro-Learning Analytics Boosting ROI | +3.7% | Global, led by North America and Europe early adopters | Short term (≤ 2 years) |

| Gig-economy Credential Portability Catalysing Mobile Micro-credentials | +2.9% | Global, with highest uptake in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Digital Learning Solutions in Corporate L&D

Corporate budgets pivoted toward mobile-first channels after hybrid work took hold in 2024. Fortune 500 firms now direct most training spend to smartphone-ready modules, a stance validated when LinkedIn Learning registered 78% corporate usage in 2024. Mobile-first programs consistently post higher completion and proficiency metrics than desktop-only equivalents, delivering measurable productivity dividends. Just-in-time learning embedded inside workflow tools drives quota attainment, and the marginal cost of adding each learner approaches zero once the platform is live, letting scale redefine competitive advantage.

Bring-Your-Own-Device Policies Across Enterprises

BYOD acceptance accelerated in 2024 when NIST issued step-by-step security guidelines, reducing chief information officer hesitation. Workers prefer using personal phones on commutes, and enterprises reap 40%-60% hardware savings. Yet, risk shifts to cybersecurity; endpoint vulnerability counts climb, forcing investments in mobile threat defense licenses that average USD 15-25 per user annually. Even with added security spend, the economics remain favorable, supporting wider adoption.

Rising Global Penetration of Smartphones, Tablets and Laptops

The International Telecommunication Union tallied 5.4 billion unique mobile-internet users in 2024, sharply lifting the total reachable learner base.[1]International Telecommunication Union, “Measuring Digital Development 2024,” itu.int Rural learners in India, Nigeria, and Indonesia gained first-time access to structured curricula without desktop infrastructure. Content providers that enable offline downloads thrive in bandwidth-limited regions, broadening the mobile learning market while mitigating cost-of-data headwinds that still curb usage in some low-income territories.

Global 5G Roll-Out Enabling High-Definition Video and AR Mobile Courses

Almost 1.9 billion 5G connections were active at the end of 2024, two-thirds in Asia Pacific. High-bandwidth, low-latency links unlock augmented-reality simulations for complex tasks such as aircraft maintenance and surgical practice. Standard-setting by ETSI ensures cross-vendor compatibility, while enterprise surveys signal mainstream rollouts by 2027 in manufacturing and healthcare. Documented gains, such as Boeing cutting assembly errors by 90% using VR drills, solidify investment cases and push the mobile learning market toward immersive formats.

Restraint Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Investment in Mobile-ready Infrastructure | -3.4% | Global, acute in emerging markets and SMEs | Short term (≤ 2 years) |

| Data-security and Privacy Compliance Risks on Personal Devices | -2.8% | Europe (GDPR), North America (CCPA, FERPA), expanding globally | Medium term (2-4 years) |

| Device/OS Fragmentation Inflating Content-maintenance Costs | -2.1% | Global, most severe in APAC with diverse Android versions | Long term (≥ 4 years) |

| Smartphone Tariff Volatility and Supply-chain Constraints Raising TCO | -1.6% | Global, with acute impact in import-dependent markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Investment in Mobile-Ready Infrastructure

Mid-sized enterprises spend USD 1.2-2.8 million integrating mobile learning management systems with existing HR and authentication stacks. Nearly half of that total funds legacy-system connectors rather than the learning platform itself. Although cloud-native vendors offer pre-built APIs, customization still averages six to nine months, slowing time-to-value. Smaller companies often postpone adoption or rely on consumer-grade tools, deepening skill gaps versus larger peers.

Data-Security and Privacy Compliance Risks on Personal Devices

GDPR and related regimes amplified compliance overhead when regulators imposed EUR 1.8 billion (USD 2 billion) in fines across sectors in 2024 - 7% targeting education and training providers.[2]European Data Protection Board, “GDPR Enforcement Tracker 2024,” edpb.europa.eu California and China layer additional rules, forcing multinationals to juggle varied data-residency demands. Zero-knowledge encryption is emerging as the default safeguard, yet it adds up to USD 0.50 per user each month in hosting costs. The reputational stakes of a breach keep compliance at the forefront of procurement criteria.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Retrofitting Content Outpaces E-Book Dominance

M-enablement is growing at 16.82% CAGR through 2031 as enterprises fast-track desktop-course conversions rather than commission expensive net-new productions. The mobile learning market size attributed to e-books represented 30.46% of overall revenue in 2025, confirming the format’s cost-effectiveness for foundational content. Retrofits slash delivery cycles from 12 months to 3 months, a decisive edge when tech skills now expire in half a decade. E-books, however, remain vital in low-bandwidth settings because learners can download once and study offline, keeping the mobile learning market accessible in data-cost-sensitive geographies.

Interactive assessments, gamified quizzes, and AI-driven adaptive testing supplement core formats. IBM’s Watson-powered formative tools cut grading workloads by 60%, freeing faculty to coach rather than mark. Vendors that support open data standards like xAPI hold an advantage because buyers can mix and match e-books, interactive video, and simulations without vendor lock-in. Platforms forcing proprietary containers risk churn as enterprises favor openness to future-proof their digital libraries.

By Application: Simulations Accelerate Where Errors Are Costly

In-class learning still held 36.67% revenue share in 2025 due to entrenched K-12 and degree programs, yet simulation-based learning is tracking a 17.33% CAGR because it mitigates high-stakes mistakes in healthcare, aviation, and energy. The mobile learning market share of simulations is expected to rise as AR and VR modules become mainstream on 5G networks. Corporate L&D teams value the measurable drop in errors and downtime, and ed-tech vendors now bundle simulation libraries with analytics dashboards, proving ROI in months rather than years.

Mobile homework extensions blur the classroom boundary, turning evenings into continuous learning windows. Retail and hospitality chains deploy bite-sized scenario training that new hires consume within 48 hours, halving ramp-up time. Gig-workers and freelancers meanwhile drive independent learning, often self-funding portable credentials that cross employers, a trend reinforcing mobile platforms over desktop portals.

By End-User: Enterprises Narrow the Spend Gap

Academic institutes accounted for 42.27% of 2025 outlays, supported by government mandates in India and China that require curricula to be mobile‑accessible. These policies have accelerated universities’ adoption of mobile learning platforms to meet compliance standards and broaden access. At the same time, institutions are recognizing that building proprietary systems is costly and slow to scale. As a result, many are partnering with established platform providers to remain relevant, offering degree credits that wrap around modular, stackable micro‑learning units rather than relying on traditional, standalone digital solutions.

Meanwhile, corporate enterprises, projected to grow at a 16.02% CAGR, are positioned to overtake academia by 2029. This shift is driven by organizations embedding skills-oriented micro‑badges directly into promotion criteria and talent‑development frameworks, making mobile learning a strategic component of workforce advancement. Growth is further amplified by HR‑tech integrations, which automate employee enrollment whenever new systems launch or regulatory requirements change. These automations help companies maintain compliance while lowering administrative overhead, strengthening the corporate segment’s momentum in the mobile learning market.

By Provider Type: Content Specialists Hold Share amid Margin Compression

Content providers held 36.59% of mobile learning revenue in 2025 and are projected to grow at a 17.83% CAGR through 2031, but their margins face pressure as generative AI enables enterprises to create internal learning materials at dramatically lower cost. Despite this shift, content curators continue to retain leadership where specialized domain expertise, such as pharmaceutical regulation or nuclear safety, cannot be easily commoditized. Their defensibility rests on deep, compliance‑intensive knowledge that organizations cannot replicate with general-purpose AI models.

Platform suppliers, in turn, are responding to this dynamic by acquiring niche content studios and integrating proprietary libraries with delivery, analytics, and administration features to secure multi‑year bundled contracts. As integration work becomes increasingly automated, service providers are moving up‑market as well, expanding into strategy, measurement, and advisory offerings rather than relying on traditional implementation hours. This repositioning across the ecosystem reflects broader shifts in how mobile learning value is created and captured.

Geography Analysis

North America commanded 31.36% of 2025 global revenue, supported by clear FERPA guidance that eased data-sharing concerns for institutional deployments. Fortune 500 companies spend USD 1,200 per employee annually on mobile L&D, and Canada’s federal directive to migrate all civil-service training to mobile platforms by 2027 adds USD 330 million in incremental procurement. Mexico’s automotive clusters follow suit, rolling out Spanish-language apps for shift workers.

Asia Pacific is the fastest-growing arena at 18.15% CAGR to 2031, powered by India’s DIKSHA platform’s 6 billion sessions in 2024 and China’s upcoming 2027 deadline for mobile-ready K-12 content.[3]Ministry of Education, China, “Digital Education Mandates,” en.moe.gov.cn Japan earmarked JPY 240 billion (USD 1.6 billion) to retrofit public schools, and South Korea leverages domestic OEM strength - Samsung cut new-hire training costs 35% using internal mobile tools. Uneven infrastructure tempers gains in Indonesia and the Philippines, though offline-sync capabilities partly offset network gaps.

Europe trails at mid-teens growth due to GDPR compliance costs that average EUR 2.3 million (USD 2.6 million) per rollout. Germany’s apprenticeship system integrates mobile modules, and the United Kingdom’s visa points regime tied to digital credentials drove a 40% increase in micro-badge enrollments. South America, Middle East, and Africa remain longer-term plays yet reveal pilot momentum: Brazil equips 5,000 rural schools, Saudi Arabia allocates SAR 18 billion (USD 4.8 billion) under Vision 2030, and Nigeria mandates mobile content across 170 universities.

Competitive Landscape

The top ten players, including SAP, Microsoft, Adobe, Coursera, Skillsoft, Cisco, Udemy, Blackboard, Docebo, and Cornerstone OnDemand, hold roughly 40% of revenue, signaling moderate concentration. Platform consolidation intensifies as suites bundle authoring, delivery, and analytics into single subscriptions, curbing churn by raising switching costs. Microsoft embedded Copilot into Viva Learning in 2024, curating courses based on calendar slots, while Coursera’s real-time adaptive micro-courses illustrate a pivot toward active career navigation.

Geographic expansion defines another axis: North American incumbents partner with Asia Pacific distributors to localize content and comply with data residency laws. Technology differentiation now hinges on offline modes and adaptive streaming that sustain the mobile learning market in low-bandwidth regions. Meanwhile, device OEMs such as Apple are patenting context-aware notifications, which threaten to make course delivery a native operating-system feature, potentially commoditizing standalone LMS front-ends.[4]United States Patent and Trademark Office, “Context-Aware Learning Notifications Patent 2024,” uspto.gov To hedge, vendors focus on content curation, compliance analytics, and vertical domain depth that hardware makers cannot replicate easily. Standardization around xAPI shrinks vendor lock-in but widens data-analytics opportunities for providers that turn granular learning records into workforce insights.

Mobile Learning Industry Leaders

SAP SE

Microsoft Corporation

Adobe Inc.

Skillsoft Corporation

Cisco Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft expanded Viva Learning with AI-guided course recommendations that link LinkedIn labor-market data to internal skills gaps, rolling the upgrade out to 400 enterprise tenants.

- September 2025: Coursera introduced GPT-4-generated adaptive micro-courses, signing 2.1 million learners in the initial month as mobile completion rates outperformed desktop by 23 poins.

- August 2025: SAP earmarked USD 250 million to scale SuccessFactors’ mobile infrastructure across India, Indonesia, and Vietnam while securing vernacular-language content partnership.

- July 2025: Learning Technologies Group bought a U.K. mobile-simulation studio for GBP 42 million (USD 53 million) to accelerate immersive manufacturing and healthcare learning portfolios.

- June 2025: Adobe integrated Captivate with Experience Cloud, enabling frontline employee learning paths tailored to customer-journey data, and early adopters recorded 18% higher course completions.

Global Mobile Learning Market Report Scope

Mobile learning is learning by accessing content via the internet or network using personal mobile electronic devices. It is a form of distance education with flexibility where users can learn at their own speed and convenience.

The Mobile Learning Market Report is Segmented by Solution (E-Books, Interactive Assessment, Mobile and Video-Based Courseware, M-Enablement, and Other Solutions), by Application (In-Class Learning, Corporate Learning, Simulation-Based Learning, Online On-the-Job Training, and Independent Learning), by End-User (Academic Institutes, and Corporate Enterprises), by Provider Type (Content Providers, andService Providers), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| E-Books |

| Interactive Assessment |

| Mobile and Video-Based Courseware |

| M-Enablement |

| Other Solutions |

| In-Class Learning |

| Corporate Learning |

| Simulation-Based Learning |

| Online On-the-Job Training |

| Independent Learning |

| Academic Institutes |

| Corporate Enterprises |

| Content Providers |

| Service Providers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Solution | E-Books | |

| Interactive Assessment | ||

| Mobile and Video-Based Courseware | ||

| M-Enablement | ||

| Other Solutions | ||

| By Application | In-Class Learning | |

| Corporate Learning | ||

| Simulation-Based Learning | ||

| Online On-the-Job Training | ||

| Independent Learning | ||

| By End-User | Academic Institutes | |

| Corporate Enterprises | ||

| By Provider Type | Content Providers | |

| Service Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the mobile learning market size in 2026 and its projected value by 2031?

Spending reached USD 95.77 billion in 2026 and is forecast to scale to USD 200.24 billion by 2031, reflecting a 15.89% CAGR.

Which region is expanding fastest in mobile learning between 2026 and 2031?

Asia Pacific is pacing the field with an 18.15% CAGR, led by large-scale national programs in India and China.

How fast is simulation-based learning projected to grow within mobile learning?

Simulation-based use cases are expected to advance at a 17.33% CAGR through 2031, the highest rate among application segments.

What share did e-books hold in the solution category in 2025?

E-books accounted for 30.46% of solution revenue in 2025, remaining the largest single format due to low production and offline-reading benefits.

Who are the leading companies accounting for roughly 40% of mobile learning revenue?

SAP, Microsoft, Adobe, Coursera, Skillsoft, Cisco, Udemy, Blackboard, Docebo, and Cornerstone OnDemand collectively hold about 40% of global revenue.

How does a bring-your-own-device policy influence corporate learning budgets?

BYOD trims hardware outlays by 40%-60%, shifting spend toward mobile threat-defense tools yet still delivering a net cost advantage that accelerates mobile learning adoption.

Page last updated on: