Corporate E-Learning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

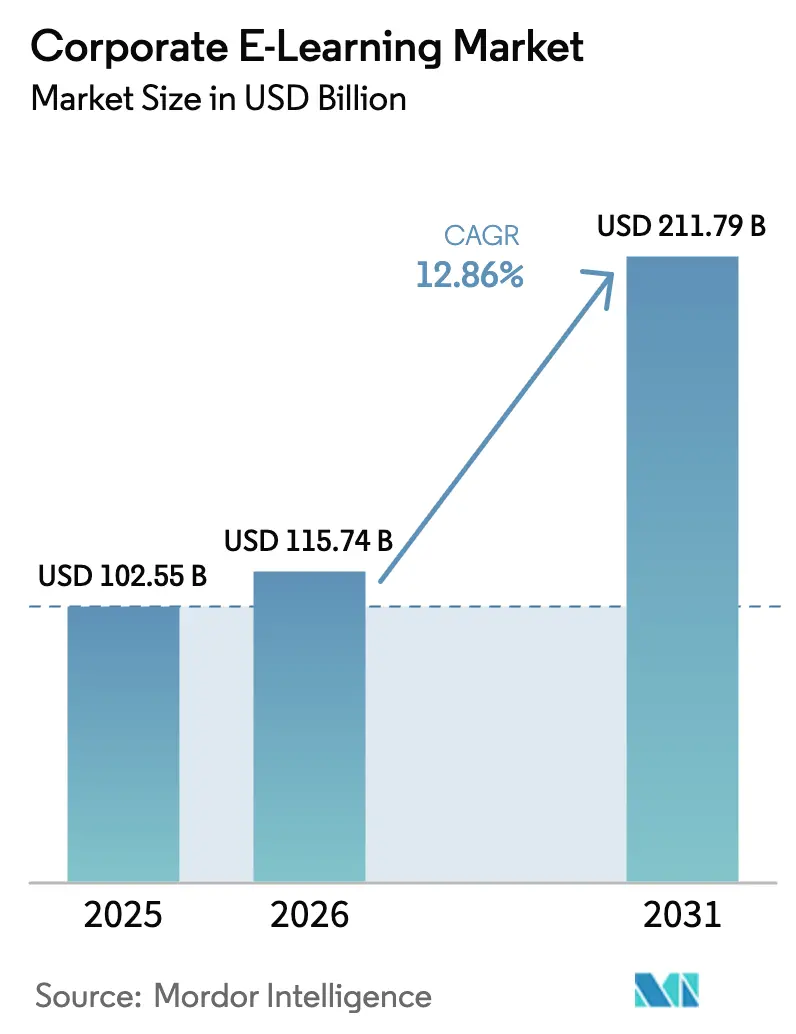

| Market Size (2026) | USD 115.74 Billion |

| Market Size (2031) | USD 211.79 Billion |

| Growth Rate (2026 - 2031) | 12.86% CAGR |

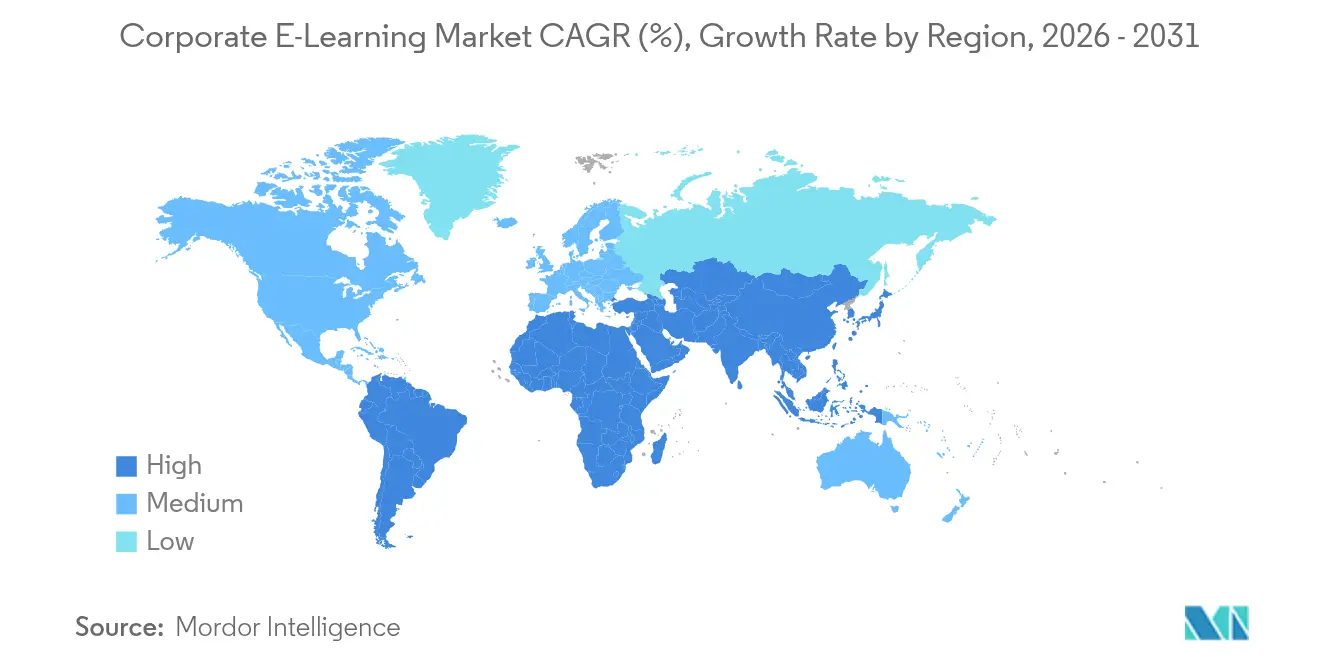

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corporate E-Learning Market Analysis by Mordor Intelligence

The corporate e-learning market size was valued at USD 102.55 billion in 2025 and estimated to grow from USD 115.74 billion in 2026 to reach USD 211.79 billion by 2031, at a CAGR of 12.86% during the forecast period (2026-2031). This strong outlook reflects the strategic priority that companies now place on continuous workforce development as digital transformation accelerates in every sector. Vendors that combine cloud scalability, data-driven personalization, and robust analytics are gaining traction because decision makers increasingly link learning metrics to revenue growth, productivity, and risk reduction. Intense pressure to close AI-related skill gaps, persistent hybrid work patterns, and evidence of double-digit returns on training investments keep demand buoyant across regions and industries. As a result, the corporate e-learning market continues to attract platform innovators, content specialists, and service providers that position learning as a core element of enterprise performance rather than a peripheral HR activity.

Key Report Takeaways

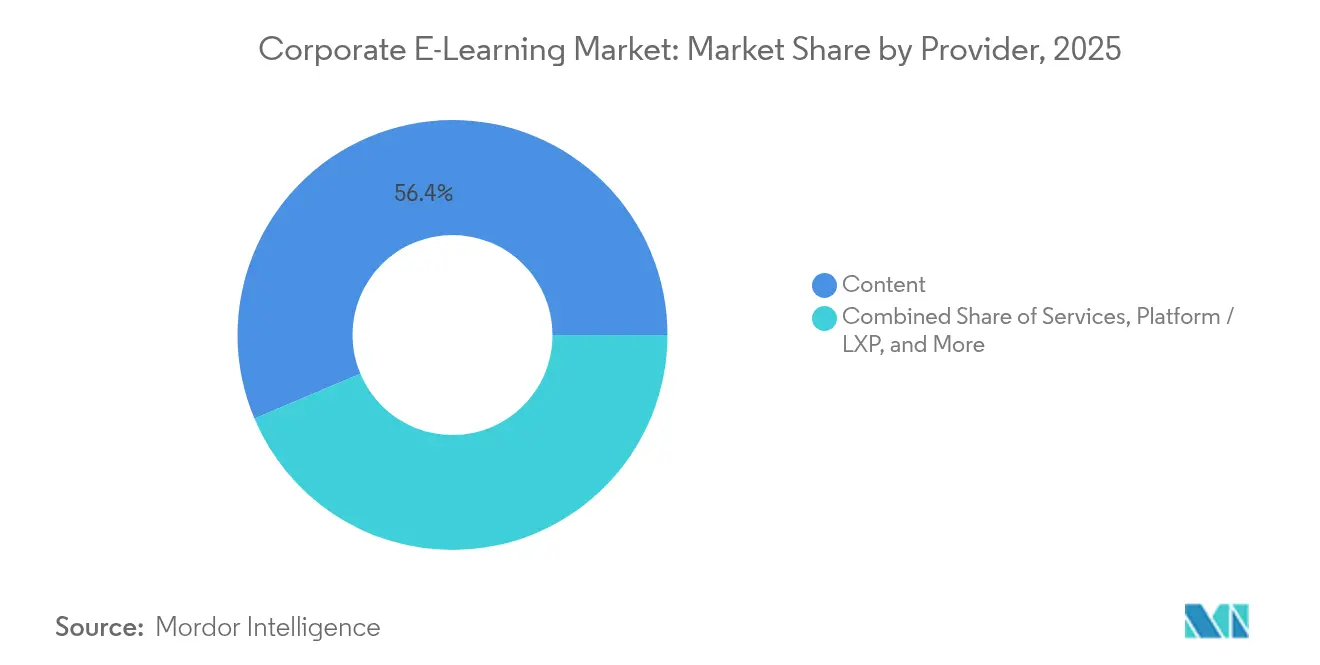

- By provider, the content segment led with 56.35% revenue share in 2025, while the services segment is forecast to expand at a 14.78% CAGR through 2031.

- By deployment, cloud delivery retained 77.45% of the corporate e-learning market share in 2025 and is projected to advance at an 17.42% CAGR to 2031.

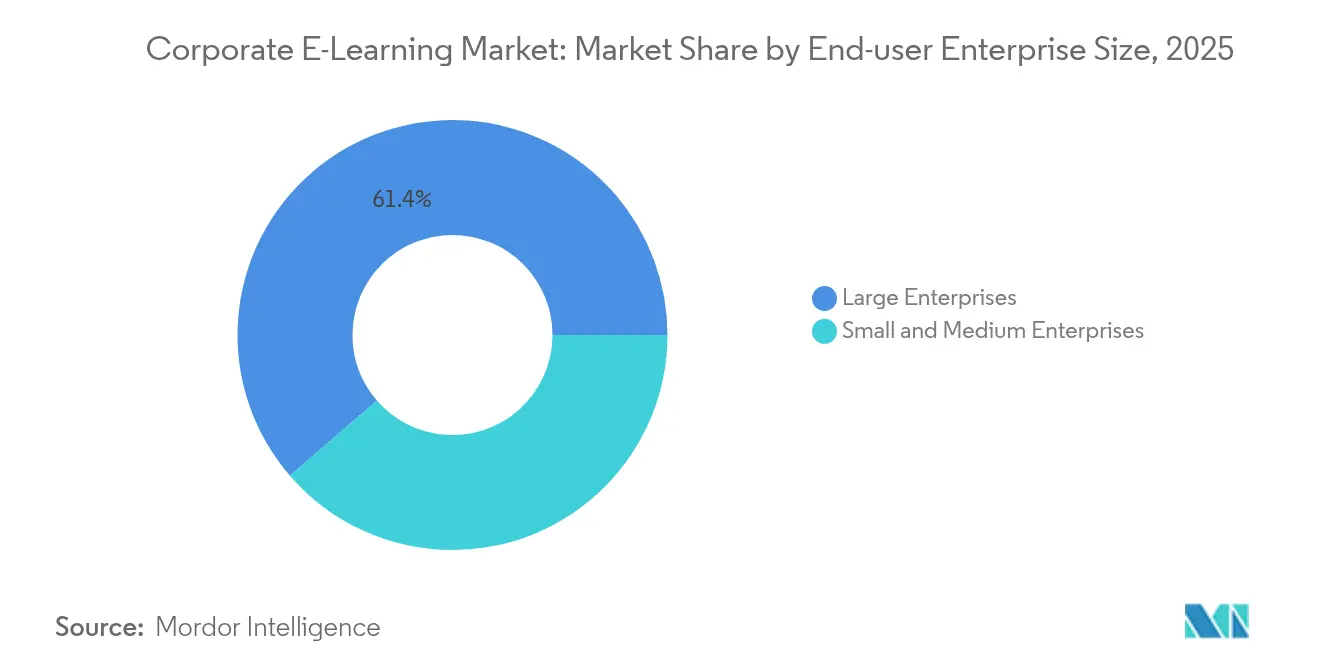

- By end-user enterprise size, large organizations accounted for 61.35% of the corporate e-learning market size in 2025, whereas SMEs are set to grow at a 16.31% CAGR from 2026-2031.

- By technology, online learning platforms captured 47.65% revenue in 2025; mobile/micro-learning is the fastest-growing segment with a 22.7% CAGR through 2031.

- By geography, North America held 33.55% revenue share in 2025, while Asia–Pacific is the fastest-growing region with a 19.12% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Corporate E-Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost savings versus classroom training | +7.3% | Global; strongest in North America and Europe | Short term (≤ 2 years) |

| Unified learning for global workforces | +5.5% | Global multinationals | Medium term (2-4 years) |

| Hybrid work model normalization | +4.6% | Global; mature economies | Short term (≤ 2 years) |

| Continuous up-skilling for AI adoption | +6.4% | Global tech hubs | Long term (≥ 4 years) |

| Gen-AI-powered personalization | +5.5% | North America, Europe, advanced Asia-Pacific | Medium term (2-4 years) |

| Mobile micro-learning for deskless staff | +3.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost savings versus classroom training

Companies that move from instructor-led programs to digital delivery consistently realize 40-60% reductions in travel, venue, and printed-material costs while maintaining or improving learning outcomes. Dow Chemical’s transition generated USD 34 million in savings, demonstrating the scale economies digital training enables when a global workforce is involved. In addition to direct expense reductions, enterprises gain indirect productivity benefits: research shows that every dollar spent on e-learning can return USD 30 in improved performance because employees apply new skills faster [1]Skillsoft, “Workforce Development Through an Era of Skill Disruption,” skillsoft.com. These compelling economics keep budget holders focused on reallocating in-person training budgets toward digital ecosystems. Sectors with heavy compliance mandates—financial services, life sciences, and energy—find particularly large savings because digital modules scale to thousands of employees without proportional cost increases. Consequently, cost efficiency remains the most powerful near-term driver underpinning the corporate e-learning market.

Unified learning for global workforces

Multinational corporations depend on e-learning platforms to standardize competencies across regions while preserving local nuance. Modern cloud suites support dynamic language switching, auto-translation, and cultural adaptation so that employees in 50 countries can complete the same training within a single launch window. AI-guided pathways further customize sequence and pacing, reducing time-to-competency for product roll-outs and regulatory compliance. These capabilities strengthen operational alignment, reinforce corporate culture, and shorten ramp-up periods for green-field facilities. Because learning data feeds directly into enterprise talent analytics, leaders can compare skill readiness across regions in real time and intervene where gaps arise, reinforcing the value proposition of unified global learning initiatives.

Hybrid work model normalization

Remote and hybrid arrangements have become structural, not temporary, features of the modern enterprise workspace. United States employers report that more than 65% of roles now incorporate some remote element, compelling LandD teams to provide anywhere-anytime access to training content [2]OECD, “SME Digitalisation for Competitiveness: 2025 OECD D4SME Survey,” oecd.org.Learning solutions increasingly integrate with collaboration hubs such as Microsoft Teams, embedding micro-lessons within chat channels and calendar flows so that training feels like a natural extension of daily workflows. Simulation-based labs replicate hands-on exercises once limited to physical classrooms, while virtual office-hour sessions give mentors the tools to coach geographically dispersed teams. Soft-skill curricula—virtual communication, remote conflict resolution, and digital delegation—have grown quickly, ensuring managers can sustain engagement without in-person oversight. Thus, hybrid work continues to create a self-reinforcing loop in which cloud learning platforms fulfill both logistical and pedagogical needs, fueling the corporate e-learning market.

Continuous up-skilling for AI adoption

Executives acknowledge that AI literacy now drives competitive advantage: 89% say advanced AI skills are essential, yet only 6% have fully operational up-skilling programs ibm.com. This gap keeps demand high for bite-sized modules on generative-AI use cases, prompt engineering, and data-ethics essentials. Because the half-life of technical skills has shrunk to nearly two years, platforms that push fresh content to learners before skills expire deliver measurable value. Firms with broad AI up-skilling report innovation rates rising by 28% as employees contribute process improvements more frequently [3]Candace Williams, “What’s Next for AI and Digital Skills in the Workforce,” BHEF, bhef.com. This direct link between learning and innovation elevates e-learning to a board-level strategic investment that shields organizations against rapid technological disruption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High up-front platform and content investment | -4.6% | Global; emerging markets | Short term (≤ 2 years) |

| Data-privacy and cyber-security concerns | -3.7% | Global; regulated sectors | Medium term (2-4 years) |

| Digital-fatigue lowers course completion | -2.7% | Global | Medium term (2-4 years) |

| Lack of content-standard interoperability | -1.8% | Global; heterogeneous tech stacks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High up-front platform and content investment

Subscription models and modular roll-outs are easing initial capital hurdles, yet SMEs still grapple with total cost of ownership that includes integration, customization, and governance. Misjudging internal resource requirements can trigger overruns and erode stakeholder confidence, slowing deployment in budget-sensitive regions.

Data-privacy and cyber-security concerns

Learning systems store rich HR metadata, inviting compliance scrutiny under GDPR and similar statutes. Vendors now emphasize SOC 2 certification, data residency options, and end-to-end encryption, but lengthy vendor-risk assessments extend procurement cycles. Highly regulated verticals consequently stage implementations in phases, tempering near-term growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Provider: Content investment anchors learning outcomes

Content governed 56.35% of 2025 revenue, underscoring that compelling material—not platform features—ultimately dictates learning impact. The corporate e-learning market size attributed to content libraries rose steadily as firms licensed curated catalogs across compliance, leadership, and AI domains. Parallel demand for consultation, migration, and change-management services propels a 14.78% CAGR for service specialists through 2031.

Platform vendors are blurring boundaries by embedding authoring tools, analytics, and AI-assisted curation in a single stack. Adobe reported a 73% uplift in field-team enrollments after integrating generative-AI tagging with social learning, illustrating how provider convergence produces closed-loop ecosystems that span needs assessment to outcome measurement.

By Deployment: Cloud flexibility accelerates enterprise scaling

Cloud solutions captured 77.45% corporate e-learning market share in 2025 and retain an 17.42% growth clip. Pay-per-use pricing, zero-hardware overhead, and elastic scalability resonate with HR and CIO functions alike. Organizations shifting from on-premise note as much as 60% savings, reinforcing cloud supremacy in the corporate e-learning market size calculus.

Regulated enterprises still favor hybrid or self-hosted modules for sensitive material, yet most supplement local instances with cloud portals for general curricula. Vendors now bundle offline sync, multiregion hosting, and granular admin controls, eliminating connectivity and governance friction that once constrained cloud adoption.

By End-user Enterprise Size: SMEs narrow the adoption gap

Large organizations controlled 61.35% revenue in 2025, leveraging global roll-outs and deep content budgets. These firms embed learning in integrated talent suites that span recruitment, skills intelligence, and succession planning, thereby translating training metrics directly into workforce analytics.

SMEs, however, are accelerating at a 16.31% CAGR on the back of lightweight, subscription-priced platforms aligned with limited headcount. OECD’s 2025 survey highlights a knowledge gap: only 21% of SMEs know about public digital-skills funding, suggesting latent runway for the corporate e-learning industry once awareness increases.

By Technology: Mobile micro-learning redefines engagement

Traditional online platforms held 47.65% revenue, but mobile micro-learning logs the fastest 22.7% CAGR as bite-sized content meets time-constrained employee preferences. LXPs layer AI-driven recommendations onto these snippets, creating hyper-personalized feeds that heighten relevance and completion.

Virtual and augmented-reality modules add an immersive dimension for high-risk or physically complex tasks. Boeing’s XR initiative achieved a 90% boost in first-time quality, demonstrating how immersive tech anchors advanced use cases while complementing mainstream mobile formats within the corporate e-learning market.

Geography Analysis

North America commanded 33.55% revenue in 2025, thanks to mature cloud infrastructure, high per-capita training budgets, and early adoption of AI-infused platforms. Ninety percent of United States employers now blend digital content into their learning stack, with increasing focus on AI literacy and cybersecurity up-skilling. Robust venture investment nurtures start-ups that commercialize emerging learning science, reinforcing the region’s innovation flywheel.

Asia–Pacific delivers the fastest 19.12% CAGR as China, India, Japan, and South Korea institutionalize digital-skills development. Mobile-first internet cultures propel micro-learning adoption, and government incentives under national skilling missions lower procurement barriers for local firms. Adaptive engines configured for multi-lingual delivery find fertile ground across APAC’s diverse languages, yielding platform innovations later exported to other regions.

Europe sustains steady uptake, balancing strict data-protection frameworks with rising demand for integrated compliance solutions. Blended models that mix self-paced modules and facilitated sessions fit the region’s learning culture, driving vendor investments in seamless offline-online orchestration. EU-funded digital academies further stimulate usage, while micro-learning aligns with the region’s preference for compact workday interventions.

Competitive Landscape

The corporate e-learning market features a tiered structure. Enterprise suites from Cornerstone OnDemand, SAP, and Microsoft anchor large-scale deployments. Specialized vendors such as Docebo, D2L, and Skillsoft carve niches through AI-powered analytics, curated content, or sector focus. Meanwhile, disruptors like mobile-first micro-learning apps and AI content-generation platforms challenge incumbents’ speed of innovation.

Strategic Merger and Acquisitions continues: Cornerstone OnDemand acquired SumTotal and SkyHive to integrate skills intelligence, while Adobe scales its all-in-one proposition by merging content authoring, analytics, and distribution. Private-equity activity, illustrated by H.I.G. Capital and Thoma Bravo’s CompTIA buyout, injects capital aimed at rapid portfolio expansion. Competitive advantage therefore hinges on ecosystem breadth, AI personalization depth, and measurable linkages between learning and business performance.

White-space opp0rtunities persist in industry-specific regulatory training, multilingual personalization, and low-bandwidth mobile delivery. Vendors able to combine these competencies with robust security and analytics will likely consolidate share as adoption accelerates across mid-market segments of the corporate e-learning market.

Corporate E-Learning Industry Leaders

SAP SE

Cornerstone OnDemand

LinkedIn Learning

Microsoft Corporation

Skillsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Auspicious acquired DBLX to blend learning-experience design with portfolio technology, aiming to deliver immersive curricula that improve engagement and knowledge retention.

- November 2024: H.I.G. Capital and Thoma Bravo purchased CompTIA to accelerate global reach for the organization’s IT-skill certifications and expand digital assessment tools.

- May 2024: Accenture closed its acquisition of Udacity, adding large-scale technical-skills programs to support enterprise digital-transformation projects.

- March 2024: Cornerstone OnDemand bought SkyHive, integrating real-time labor-market intelligence into its talent suite for dynamic skill-gap mapping.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the corporate e-learning market as paid digital content, cloud or on-premise learning platforms, and outsourced training services that enterprises of any size purchase to upskill and certify employees through web, mobile, or virtual-classroom delivery. Revenues include subscriptions, authoring tools, virtual facilitation fees, and analytics add-ons, while academic tuition, consumer-oriented MOOCs, and all hardware sales remain outside scope.

Scope Exclusion: Hardware devices and free public learning portals are excluded.

Segmentation Overview

- By Provider

- Content

- Services

- Platform / LXP

- By Deployment

- Cloud

- On-Premise

- Hybrid

- By End-user Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

- By Technology

- Online Learning

- Learning Management System (LMS)

- Mobile / Micro-learning

- Virtual Classroom and Webinar

- AI-driven Learning Experience Platform (LXP)

- AR / VR Immersive Learning

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview chief learning officers, HR-tech suppliers, regional training bodies, and mid-market executives across North America, Europe, and Asia-Pacific. These conversations validate price corridors, renewal rates, and adoption triggers that documents rarely disclose.

Desk Research

We comb open sources such as UNESCO ICT surveys, Eurostat enterprise training spend, US Bureau of Labor Statistics employer training tables, ATD benchmarks, and patent filings, then enrich gaps with paid feeds, D&B Hoovers for company revenues and Dow Jones Factiva for deal news. Shipment signals from Volza and contract alerts from Tenders Info act as proxy checks on platform uptake. The sources named are illustrative only; many additional outlets informed data collection, validation, and clarification.

Market-Sizing & Forecasting

We begin with a top-down construct that multiplies employed workforce, average L&D spend per worker, and verified digital share, followed by regional cloud LMS penetration factors. Bottom-up samples, supplier billings and license counts, stress-test the totals. Key variables include remote-work prevalence, smartphone reach, mandated compliance hours, and course renewal frequency. We project 2025 to 2030 values through multivariate regression blended with ARIMA smoothing for near-term shocks.

Data Validation & Update Cycle

Outputs pass analyst peer review, senior domain oversight, and automated variance checks, and reports refresh yearly with mid-cycle updates whenever major regulations, mergers, or price shifts materially move the market.

Why Mordor's Corporate E-Learning Baseline Deserves Trust

Published estimates often diverge because firms vary scope definitions, currency cut-off dates, and refresh cadence. This is where Mordor Intelligence differentiates; our inclusions are disclosed, drivers revisited annually, and assumptions triangulated through fresh primary evidence, giving clients a stable middle-path figure.

Key gap drivers include whether content services are counted, if smart-learning hardware is folded in, and the breadth of covered industries.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 102.55 B (2025) | Mordor Intelligence | - |

| USD 104.32 B (2024) | Global Consultancy A | Adds hardware and L&D BPO revenues |

| USD 30.8 B (2024) | Global Consultancy B | Limits scope to SaaS platforms and selective sectors |

The comparison shows that Mordor's balanced inclusion of platform, content, and service streams plus its transparent annual refresh offers the most dependable baseline for strategic planning.

Key Questions Answered in the Report

How large is the corporate e-learning market expected to be by 2031?

The market is projected to reach USD 211.79 billion in 2031, growing at a 12.86% CAGR during 2026-2031.

Which delivery model is growing fastest in corporate e-learning?

Mobile micro-learning holds the strongest momentum with a 22.7% CAGR, reflecting employee demand for short, on-demand lessons that fit into daily workflows.

Why do enterprises favor cloud-based learning platforms?

Cloud solutions eliminate infrastructure costs, scale globally in days, and integrate easily with collaboration tools, underpinning their 77.45% market share in 2025.

How is AI reshaping corporate training?

Gen-AI enables platforms to map skills, create adaptive content, and personalize learning paths, contributing to a 73% enrollment surge in some deployments.

What is the primary barrier for SMEs adopting e-learning?

Up-front investment in platforms and tailored content remains the main obstacle, though subscription pricing is gradually lowering entry thresholds.

Which region will contribute most to future growth?

Asia–Pacific is forecast to deliver the fastest expansion at 19.12% CAGR, driven by large populations, government digital-skills programs, and mobile-first learning cultures.

Page last updated on: