Disposable Syringes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.36 Billion |

| Market Size (2031) | USD 24.94 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

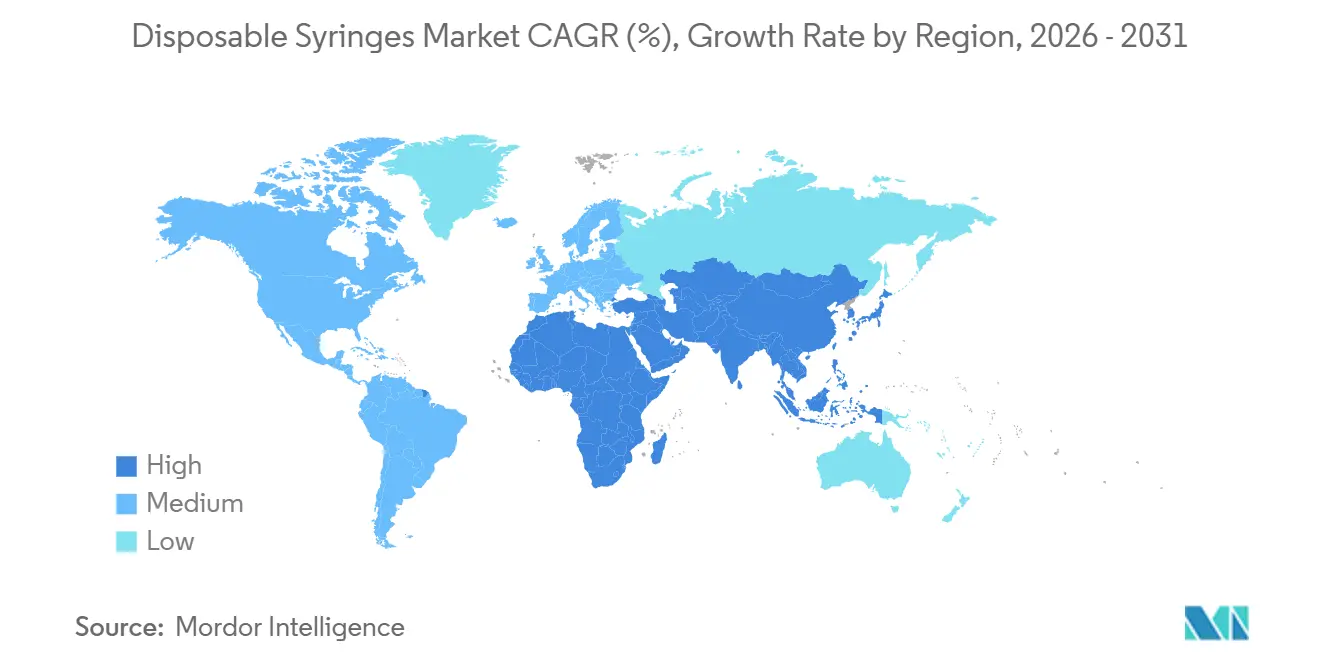

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

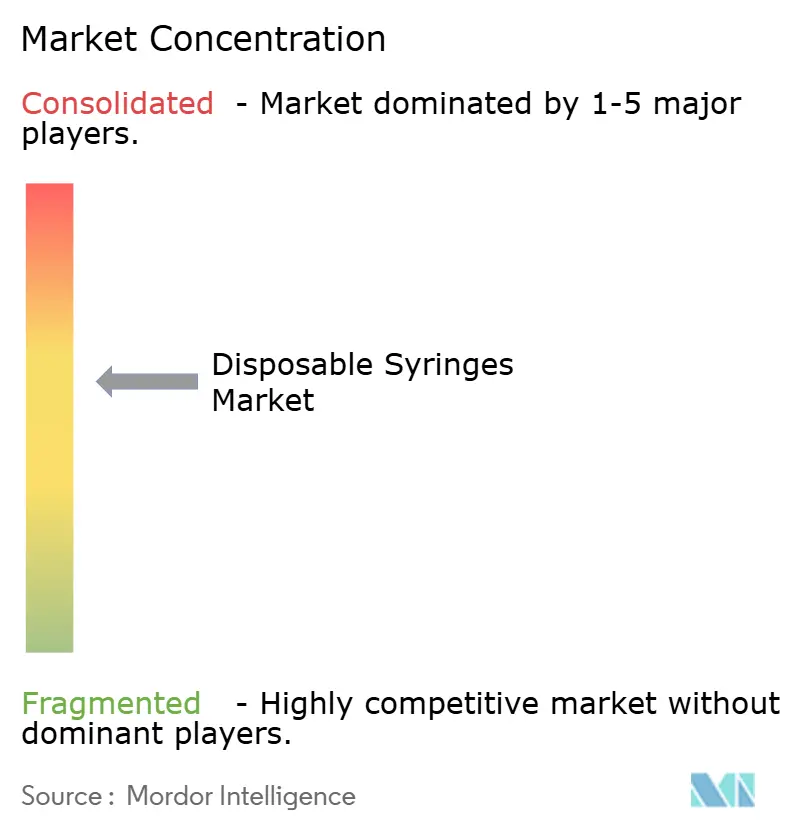

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Syringes Market Analysis by Mordor Intelligence

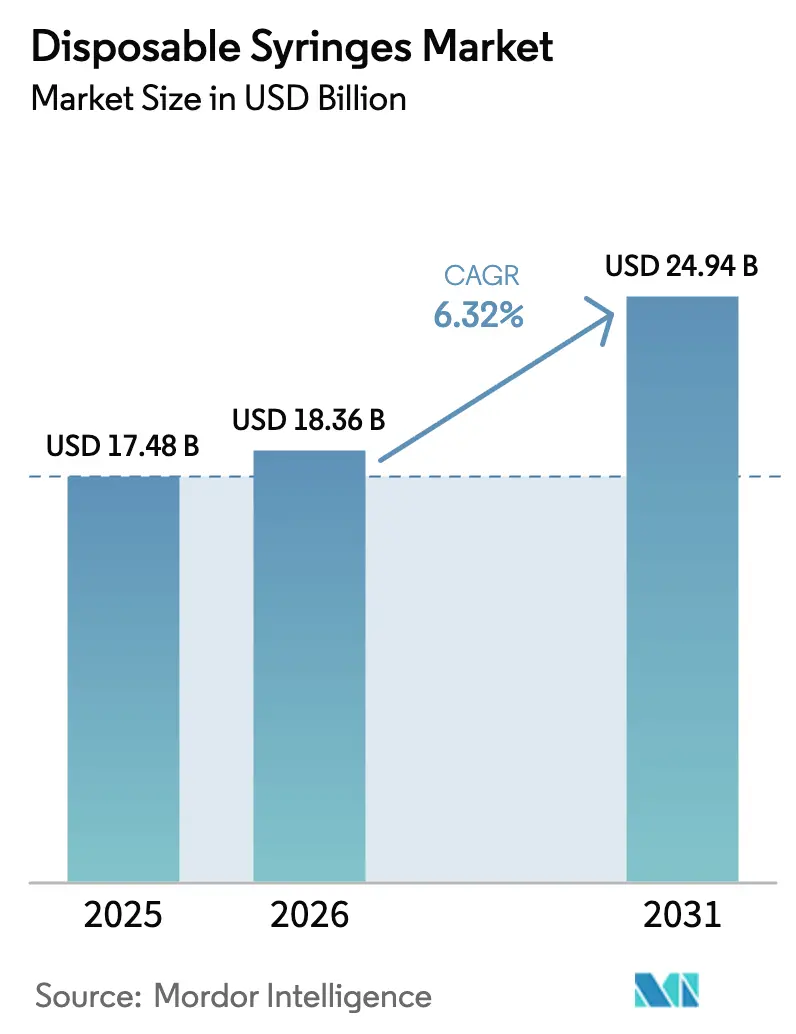

The Disposable Syringes Market size is expected to increase from USD 17.48 billion in 2025 to USD 18.36 billion in 2026 and reach USD 24.94 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

Regulatory mandates that favor single-use safety mechanisms, continuing immunization drives in low- and middle-income countries, and greater use of prefilled formats for biologics and GLP-1 receptor agonists anchor current growth. Hospitals still purchase the largest volumes, yet home-based care is gathering pace as payers reimburse patient self-administration kits and telehealth platforms track adherence. Material selection is also in flux as polypropylene remains dominant on cost grounds while early biodegradable blends enter pilot use. Competitive strategy now centers on capacity expansions, line automation, and differentiated safety technologies that lower needlestick liability and win group-purchasing contracts.

Key Report Takeaways

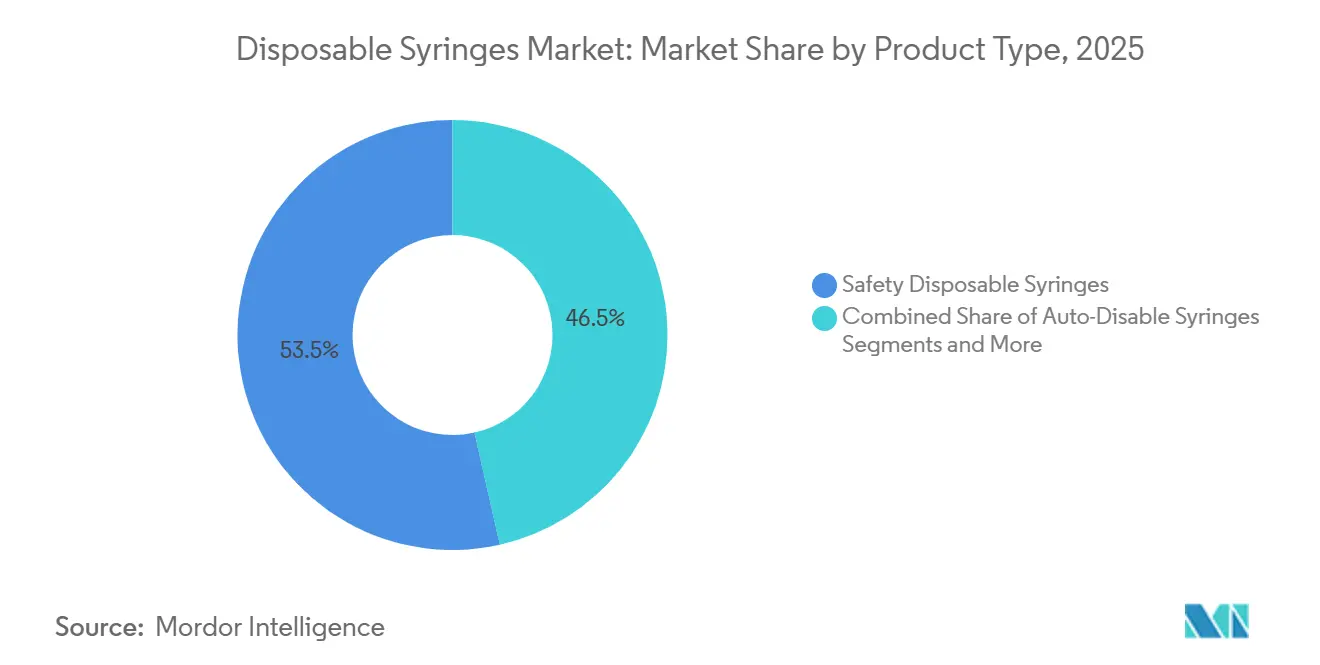

- By product type, safety disposable syringes led with 53.53% revenue share in 2025; auto-disable designs are forecast to grow at a 9.45% CAGR to 2031.

- By application, therapeutic injections accounted for a 62.55% share of the disposable syringes market size in 2025 and are advancing at a 6.1% CAGR through 2031.

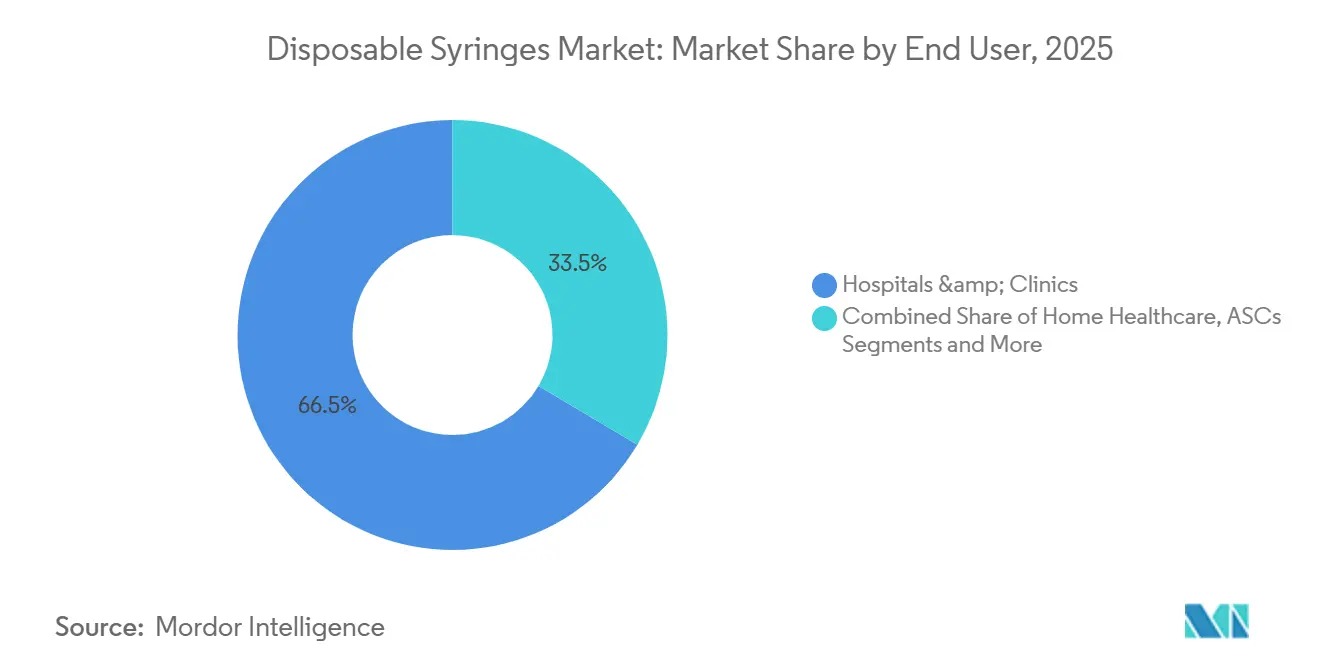

- By end user, hospitals and clinics held 66.48% of disposable syringes market share in 2025, while home healthcare is projected to post the fastest expansion at 10.57% CAGR to 2031.

- By material, plastic syringes captured 86.36% of market revenue in 2025; biodegradable blends are forecast to expand at 9.24% CAGR to 2031.

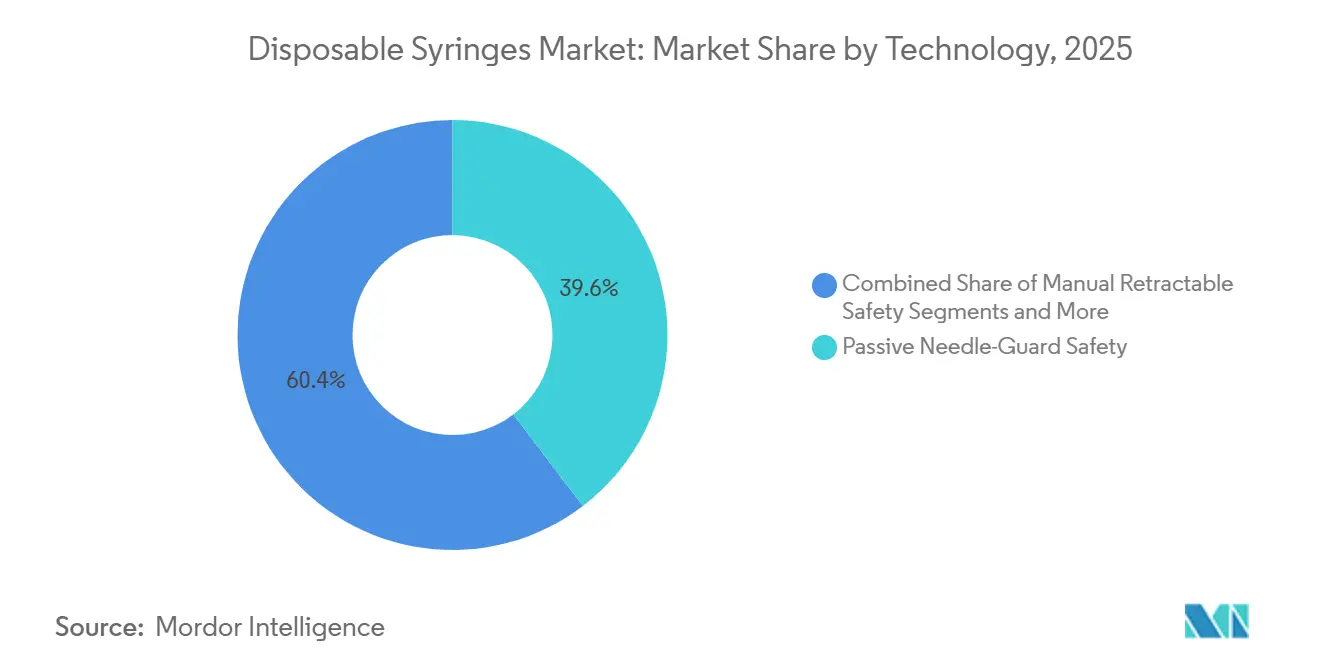

- By technology, passive needle-guard mechanisms represented 39.63% share of the disposable syringes market in 2025; automatic retractable systems will register a 10.45% CAGR through 2031.

- North America contributed 37.12% of global revenue in 2025; Asia-Pacific is positioned for the strongest regional growth at 8.03% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Disposable Syringes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Immunization & Booster Programs | +1.2% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2-4 years) |

| Increasing Prevalence of Chronic Diseases Requiring Injectable Therapies | +1.5% | North America, Europe, Urban Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Mandates Promoting Single-Use Safety-Engineered Devices | +1.0% | North America, EU, Australia | Short term (≤ 2 years) |

| Growing Demand for Prefilled & Self-Administered Syringes | +0.9% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Government Pandemic Stockpiling & Strategic Syringe Reserves | +0.6% | United States, Canada, EU, Select Asia-Pacific | Short term (≤ 2 years) |

| Biodegradable & Smart-Connected Syringe Innovations | +0.4% | EU, Scandinavia, Pilot Sites in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Immunization & Booster Programs

WHO’s Immunization Agenda 2030 targets 90% coverage for essential childhood vaccines, a goal that demands up to 10 billion single-use syringes every year.[1]World Health Organization, “Immunization Agenda 2030,” WHO, who.intThe 2023 “Big Catch-Up” mobilized USD 500 million in donor funding and lifted 2025 auto-disable syringe shipments above 2 billion units.[2]Gavi Secretariat, “The Big Catch-Up,” Gavi, gavi.org Booster programs for COVID-19, influenza, and mpox cement single-use devices as standard practice. UNICEF’s 2025 Supply Division noted a 22% jump in auto-disable orders, with 65% flowing to low- and middle-income countries. Pharmaceutical companies now bundle vaccines in prefilled syringes, reducing reconstitution errors and tightening cold-chain logistics.

Increasing Prevalence of Chronic Diseases Requiring Injectable Therapies

Diabetes, rheumatoid arthritis, multiple sclerosis, and cardiovascular diseases together affect more than 1.5 billion people, and injectables dominate new treatment protocols. GLP-1 agonists generated USD 50 billion in 2025 sales, prompting Novo Nordisk and Eli Lilly to expand prefilled syringe capacity by over one-third. The CDC counted 8.7 million U.S. insulin users in 2024, consuming roughly 3.2 billion syringe units yearly. An aging Japanese, German, and Italian population amplifies demand because patients over 65 now hold 60% of injectable prescriptions.

Regulatory Mandates Promoting Single-Use Safety-Engineered Devices

The U.S. Needlestick Safety and Prevention Act, renewed in 2024, compels federally funded facilities to adopt safety sharps, with OSHA fines up to USD 70,000 per violation.[3]Occupational Safety and Health Administration, “Needlestick Safety and Prevention Act,” OSHA, osha.gov The EU Medical Device Regulation classifies safety syringes as Class IIa and enforces ISO 23908 performance testing. WHO’s 2024 prequalification update requires auto-disable features that lock plungers permanently. Australia’s Therapeutic Goods Administration set 2027 as the cutoff for conventional syringes in public hospitals.

Growing Demand for Prefilled & Self-Administered Syringes

Prefilled formats accounted for 18% of disposable syringe volume but over 30% of revenue in 2025 because drug-device combinations command premiums. BD’s Effivax platform, launched in 2024, integrates a passive needle shield and color-coded plunger to ease mass-vaccination workflows. West Pharmaceutical Services saw a 40% spike in elastomeric stopper orders for high-concentration biologics. CMS broadened reimbursement in 2025 for self-injectable anticoagulants, adding 12 million prefilled units to annual U.S. demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Disposal & Plastic-Waste Regulations | −0.8% | EU, Japan, South Korea, California | Medium term (2-4 years) |

| High-Cost Sensitivity for Safety Syringes in Low-Income Settings | −0.6% | Sub-Saharan Africa, South Asia, Latin America | Short term (≤ 2 years) |

| Gradual Substitution by Glass Syringes for Sensitive Biologics | −0.5% | North America, Western Europe, Japan | Long term (≥ 4 years) |

| Recall Risks from Contaminant Events | −0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Disposal & Plastic-Waste Regulations

The EU’s Single-Use Plastics Directive spurred member states to launch extended producer responsibility schemes; France now makes syringe suppliers fund half of municipal sharps collection programs. Germany’s Packaging Act requires 30% recycled content in polypropylene medical devices by 2028. California passed a Medical Device Stewardship Act in 2025 that obliges manufacturers to run take-back programs. Compliance costs compress margins on high-volume conventional syringes.

High-Cost Sensitivity for Safety Syringes in Low-Income Settings

UNICEF paid USD 0.08-0.12 for auto-disable units in 2025 versus USD 0.05 for conventional designs, a 60% premium that strains budgets where per-capita health spend is under USD 50. Gavi’s co-financing rules force recipient governments to cover 20% of device costs by 2027, delaying safety adoption. Local manufacturers in India and China offer cheaper designs but face 24-month WHO prequalification queues.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safety Mechanisms Command Premium but Auto-Disable Designs Outpace Growth

Safety disposable syringes held 53.53% revenue share in 2025. Auto-disable syringes, insulated from reuse risk and compliant with WHO standards, will post a 9.45% CAGR to 2031, surpassing all other formats. Conventional units persist in cost-sensitive laboratories. Retractable safety designs appeal to emergency departments seeking fast disposal and lower liability. Prefilled devices now capture over 30% of revenue despite lower volumes. Smart connected models remain at pilot scale because cybersecurity validation stretches product timelines.

Producers invest in 64-cavity molds and automated assembly to cut per-unit costs. Becton, Dickinson and Company’s BD Integra has secured 12% of U.S. hospital contracts through group-purchasing deals, illustrating how feature differentiation wins share. Venture funding of USD 120 million in 2024-2025 signals investor confidence in connected devices that may leverage cloud analytics for adherence.

By Application: Therapeutic Injections Dominate but Immunization Volumes Surge

Therapeutic injections controlled 62.55% of 2025 revenue, propelled by diabetes and oncology regimens relying on subcutaneous delivery. Immunization injections will grow 9.22% annually to 2031 as catch-up drives close pandemic gaps. Blood-collection devices account for small value but high frequency.

Subcutaneous reformulation of blockbuster monoclonal antibodies adds an estimated 500 million syringes annually. Point-of-care microsampling may chip away at venous draws, yet adoption remains limited to high-resource clinics.

By End User: Hospitals Anchor Demand but Home Healthcare Accelerates

Hospitals and clinics captured 66.48% revenue in 2025 thanks to procedure volumes and bundled procurement. Home healthcare will expand at 10.57% CAGR as insurers reimburse self-administration kits and remote monitoring.

Telehealth platforms integrate Bluetooth syringe data, improving dose tracking and reducing readmissions. Blood centers and diagnostic labs standardize SKUs nationwide through networks like Quest Diagnostics to lock in pricing.

By Material: Plastic Dominates but Biodegradable Blends Emerge

Plastic maintained 86.36% share in 2025 because polypropylene offers low cost and compatibility with sterilization. Biodegradable blends will grow 9.24% on the back of EU waste rules and NHS sustainability targets. Glass is gaining traction in high-value biologics where stability trumps price.

Gerresheimer and Schott now pilot PLA syringes that compost within 180 days. Cyclic olefin copolymers meanwhile lead prefilled segments due to transparency and low protein adsorption.

By Technology/Safety Mechanism: Passive Guards Lead but Automatic Retraction Gains Momentum

Passive needle-guard devices took 39.63% share in 2025, valued for simplicity. Automatic retractable systems will post a 10.45% CAGR as emergency units seek hands-free activation. Manual retractables lag because they rely on user compliance, which studies peg below the CDC-recommended 95% activation threshold.

Auto-disable syringes already represent 18% of global volume and are mandatory for UNICEF tenders. Passive guards deploy spring sheaths that pass ISO 23908 puncture tests. Automatic retraction reduces disposal volume by 30% and offers an audible click for confirmation.

Geography Analysis

North America contributed 37.12% of global revenue in 2025. Vendor-managed inventory contracts allow the U.S. Strategic National Stockpile to hold 150 million syringes on a rolling basis, creating a stable baseline of orders. CMS reimbursement favors safety-engineered devices and accelerates home-care uptake. Canada expanded its National Emergency Strategic Stockpile to 80 million units in 2024. Mexico’s IMSS procured 120 million syringes in 2025, incorporating local assembly clauses to spur domestic industry.

Asia-Pacific is forecast at an 8.03% CAGR from 2026-2031. Hindustan Syringes & Medical Devices will double auto-disable capacity after a USD 50 million investment, aiming at UNICEF and WHO tenders. Nipro’s Welsh expansion added 1.2 billion units to European supply chains. China’s NMPA harmonized standards with WHO criteria in 2024, opening global markets for local producers. Japan’s aging population encourages prefilled devices for home-based insulin delivery and GLP-1 therapy.

Europe enforces MDR Class IIa conformity, raising barriers for new entrants. Germany, France, the U.K., Italy, and Spain make up two-thirds of European demand. The NHS aims for 25% bio-based devices by 2030. France’s decree obliges suppliers to fund half of sharps collection, increasing per-unit costs. The Middle East and Africa build capacity: GCC states ordered 80 million syringes in 2025, while South Africa inked a 150 million-unit contract with BD. In South America, Brazil’s SUS bought 200 million units and Argentina expanded coverage under its 2024 immunization plan.

Competitive Landscape

Key firms include BD, Terumo, B. Braun, Nipro, and Gerresheimer, confirming a moderately concentrated field. BD’s vertically integrated supply chain spans polymer compounding to automated inspection, achieving defect rates below 10 ppm and securing Vizient and Premier contracts. Novo Nordisk and Eli Lilly are backward-integrating to protect prefilled GLP-1 injector supply. Hindustan Syringes & Medical Devices and Poly Medicure undercut pricing by 20-30% in UNICEF tenders, leveraging low-cost Indian capacity. Gerresheimer’s new 64-cavity mold cuts cycle time 18%, illustrating how automation lowers cost. Patent grants for novel needle-guard springs rose 22% between 2023-2025, signaling sustained R&D. Private equity funds target mid-tier regional players to roll up distribution networks and gain regulatory economies of scale.

Disposable Syringes Industry Leaders

Becton, Dickinson and Company

Terumo Corporation

Nipro Corporation

Cardinal Health, Inc.

Hindustan Syringes & Medical Devices Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Terumo Medical Corporation launched SurTract Safety Syringe with SafeR passive technology for U.S. hospitals, clinics, and emergency settings.

- January 2026: West Pharmaceutical Services introduced the West Synchrony Prefillable Syringe System at CPHI Frankfurt; commercial roll-out slated for January 2026

- April 2025: Gerresheimer agreed with Injecto Group to supply complete silicone-oil- and PFAS-free syringe systems made of glass and COP.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the disposable syringes market as every single-use, sterile hypodermic device, plastic or glass, sold empty to healthcare providers or pre-filled by pharmaceutical companies and discarded immediately after one patient encounter. We count revenues generated from product sales, rentals, and contractual supply agreements.

Scope Note: We exclude reusable metal syringes, pen injectors, auto-injectors, and implantable drug-delivery systems.

Segmentation Overview

- By Product Type

- Conventional Disposable Syringes

- Safety Disposable Syringes

- Non-Retractable Safety Syringes

- Retractable Safety Syringes

- Auto-Disable Syringes

- Prefilled Disposable Syringes

- Smart / Connected Disposable Syringes

- By Application

- Immunization Injections

- Therapeutic Injections

- Blood Collection & Diagnostics

- By End User

- Hospitals & Clinics

- Blood Collection Centres & Diagnostic Labs

- Ambulatory Surgical Centres

- Home Healthcare

- By Material

- Plastic (Polypropylene, Polycarbonate, COP/COC)

- Glass

- Biodegradable / Bio-polymer Blends

- By Technology / Safety Mechanism

- Passive Needle-Guard Safety

- Manual Retractable Safety

- Automatic Retractable Safety

- Auto-Disable Mechanism

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed procurement heads in hospitals, infection-control nurses, and product managers at syringe manufacturers across North America, Europe, and Asia-Pacific. Their inputs on contracted selling prices, the shift toward retractable formats, and average reorder cycles validated secondary findings and closed data gaps.

Desk Research

First, our analysts gathered customs-level shipment lines, WHO and UNICEF immunization dashboards, and procedure volume tables from agencies such as the CDC, Eurostat, and India's MoHFW. These sources anchored injection frequency and vaccination demand. Standards under ISO 7886 and FDA 510(k) listings clarified the regulatory universe, while peer-reviewed studies on needlestick injuries informed safety-syringe adoption curves. Company filings, government budget statements, and medical device trade bodies offered price bands and capacity clues, and paid repositories like D&B Hoovers and Dow Jones Factiva provided producer revenue splits. The sources cited are illustrative; many additional open datasets were reviewed for consistency and validation.

Market-Sizing & Forecasting

We built a top-down and bottom-up hybrid model. Global production and trade volumes were reconstructed from customs data, then converted to value through region-specific average selling prices adjusted for the rising safety-syringe mix. Supplier roll-ups and sampled hospital purchase audits acted as the bottom-up cross-check. Variables such as national immunization doses, inpatient admissions, diabetes prevalence, glass-to-plastic substitution ratios, and quarterly currency movements feed a multivariate regression forecast through 2030. Where unit data were partial, weighted interpolation bridged gaps before final triangulation.

Data Validation & Update Cycle

We run anomaly screens, variance checks, and multi-step peer reviews, then senior analysts sign off. We refresh the model every twelve months, with interim updates when policy changes, recalls, or large acquisitions materially shift market dynamics.

Why Mordor's Disposable Syringes Baseline Inspires Confident Decisions

Estimates often diverge because firms mix reusable pens, apply list rather than transacted prices, or freeze exchange rates for years. By limiting scope to single-use hypodermic devices and updating ASP and currency inputs annually, Mordor Intelligence reduces such distortions.

Key gap drivers include rivals blending pre-filled formats, omitting China's hospital demand, and projecting simple CAGR trends without anchoring to immunization targets or regulatory shifts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 17.27 B (2025) | Mordor Intelligence | None |

| USD 15.81 B (2024) | Global Consultancy A | Includes pre-filled syringes and uses list prices from 2023 |

| USD 11.89 B (2024) | Industry Journal B | Excludes China hospital volumes; straight-line CAGR from 2019 data |

These comparisons show that our disciplined variable selection, yearly refresh, and transparent assumptions deliver a balanced, traceable baseline decision-makers can rely on.

Key Questions Answered in the Report

How large will the disposable syringes market be by 2031?

It is projected to reach USD 24.94 billion by 2031 at a 6.32% CAGR.

Which product segment is growing fastest?

Auto-disable syringes are expected to grow at 9.45% annually to 2031 as immunization agencies favor tamper-proof designs.

Why are prefilled syringes gaining share?

They reduce dosing errors, simplify logistics, and meet rising demand for self-injection of biologics.

What region will see the highest growth?

Asia-Pacific is forecast for the quickest expansion at 8.03% CAGR, driven by manufacturing capacity additions in India, China, and Vietnam.

How are sustainability goals affecting material choices?

EU and U.K. rules are encouraging trials of biodegradable PLA and PHA syringes, although polypropylene remains dominant for now.

Which safety technology is poised for rapid adoption?

Automatic retractable mechanisms are set for a 10.45% CAGR as hospitals seek hands-free needlestick protection.

Page last updated on: