Modacrylic Fiber Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

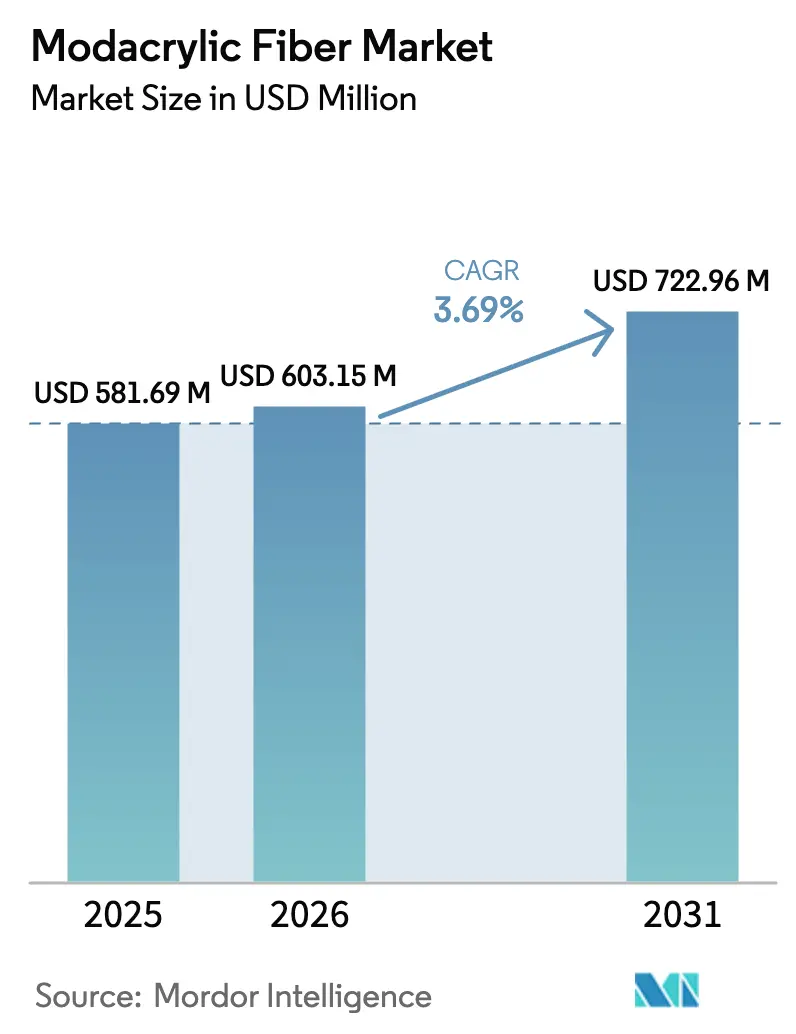

| Market Size (2026) | USD 603.15 Million |

| Market Size (2031) | USD 722.96 Million |

| Growth Rate (2026 - 2031) | 3.69% CAGR |

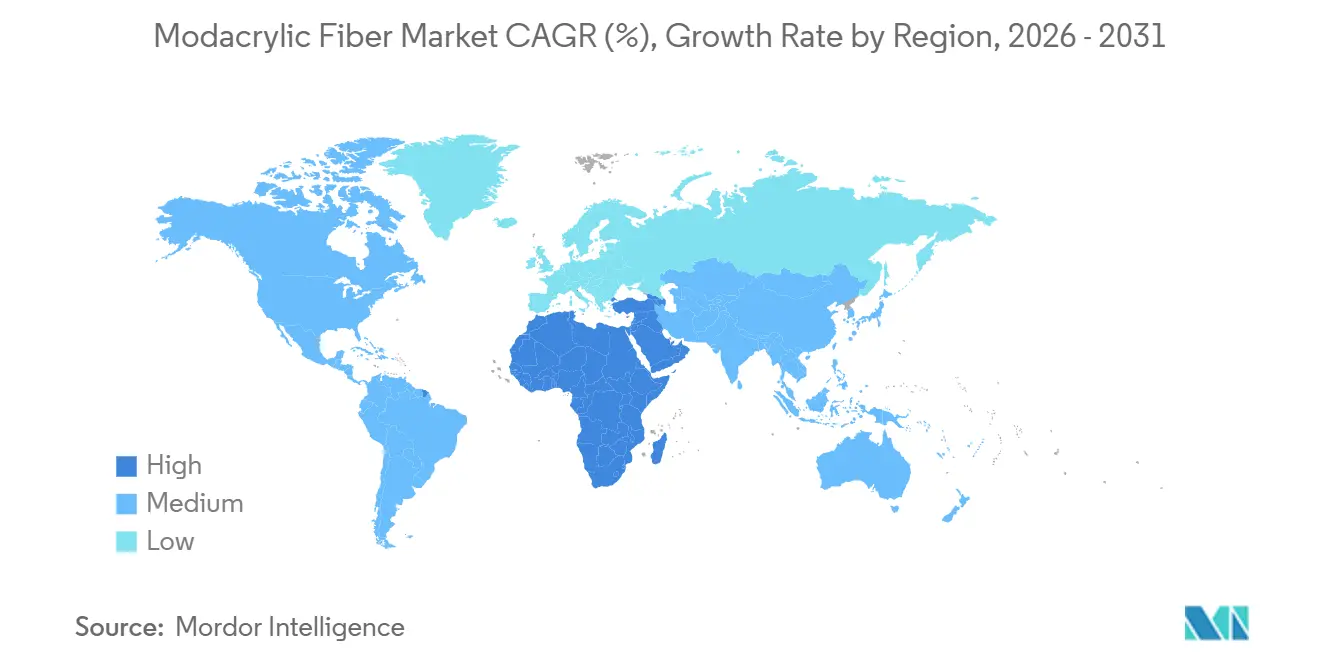

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Middle East and Africa |

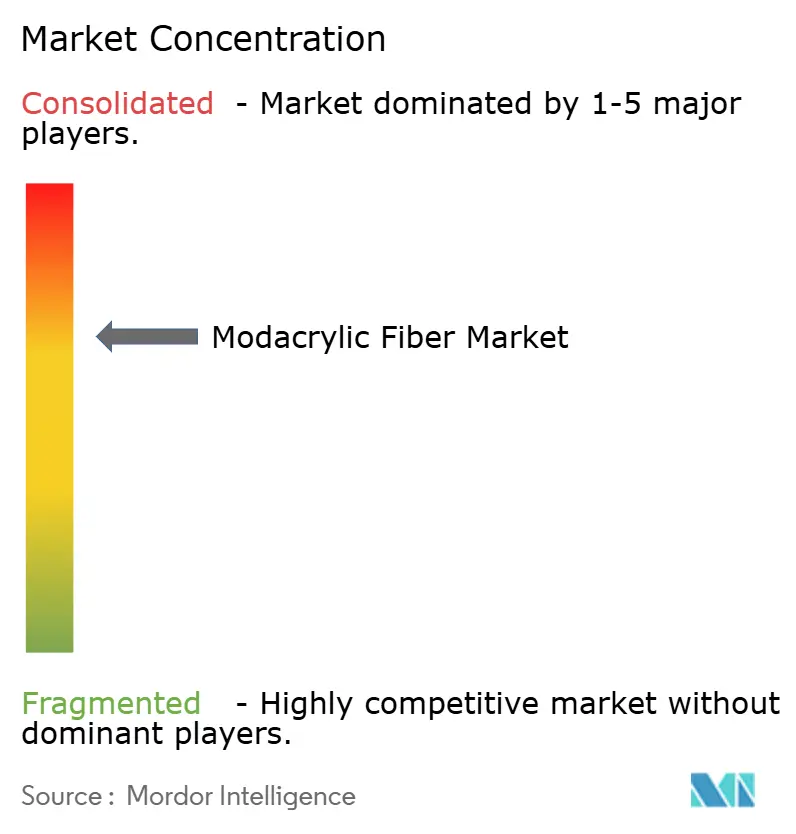

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modacrylic Fiber Market Analysis by Mordor Intelligence

The Modacrylic Fiber Market size is expected to grow from USD 581.69 million in 2025 to USD 603.15 million in 2026 and is forecast to reach USD 722.96 million by 2031 at 3.69% CAGR over 2026-2031. Sub-Saharan Africa's expanding consumer base, coupled with the Middle-East's demand for heat-stable synthetic extensions that endure high styling temperatures, is fueling the surge in hair fiber demand. In the U.K. and North America, stricter fire codes are amplifying the need for protective apparel and upholstery. Suppliers harnessing closed-loop acrylonitrile recovery are effectively shielding their margins from the compliance costs tied to the U.S. EPA's Toxic Substances Control Act. The supply landscape reveals a moderate concentration: the top four producers dominate a substantial share of global capacity, yet smaller innovators are maintaining competitiveness with energy-efficient wet-spinning techniques and low-carbon feedstocks. The forecast period of 2026-2031 presents a promising horizon for the market, particularly in the electric-vehicle acoustic insulation and thermal barriers for lithium-ion batteries. However, for modacrylic to capitalize on these opportunities, it must first align its costs with industry stalwarts such as polyester and aramid.

Key Report Takeaways

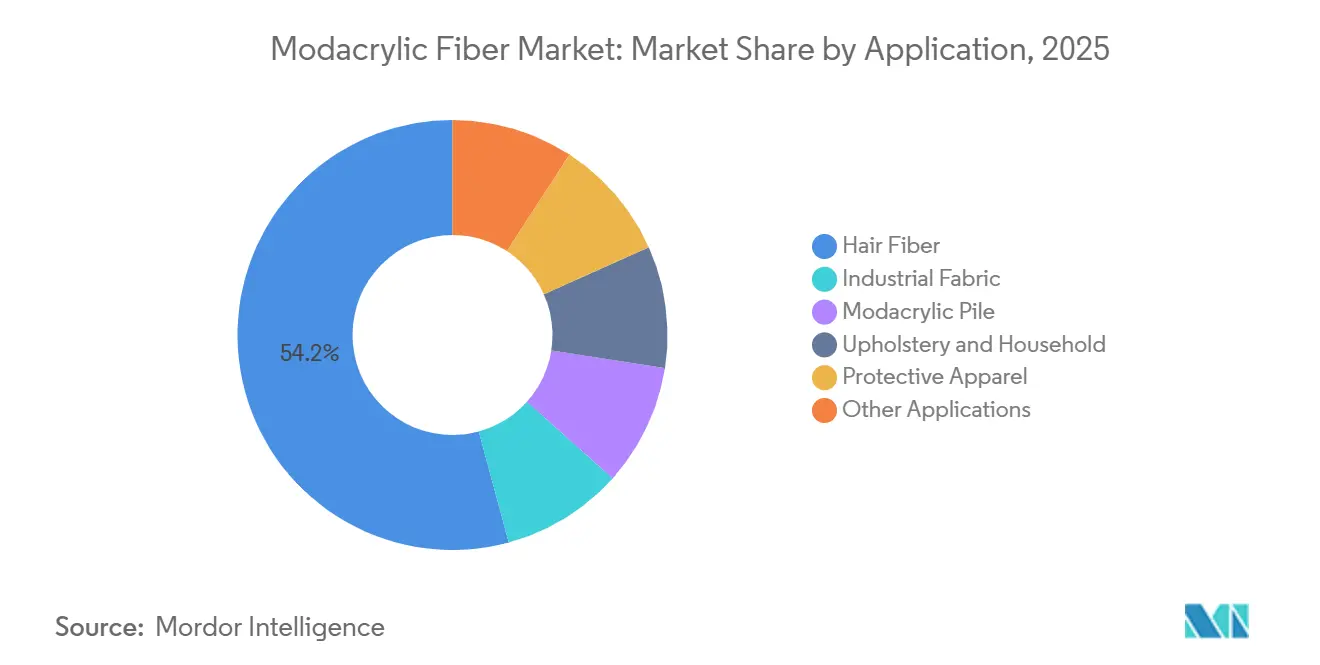

- By application, hair fiber captured 54.22% of the modacrylic fiber market share in 2025 and is advancing at a 6.15% CAGR through 2031.

- By geography, the Middle-East and Africa held 45.67% of 2025 revenue and is projected to lead regional growth with a 6.49% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Modacrylic Fiber Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widening adoption of synthetic hair extensions | +1.80% | Middle-East and Africa, Asia-Pacific | Medium term (2-4 years) |

| Stricter furniture fire codes for upholstery | +0.80% | Europe, North America | Short term (≤ 2 years) |

| Low-cyano bio-acrylonitrile production pathways | +0.40% | North America, Europe (pilot plants) | Long term (≥ 4 years) |

| EV interior acoustic-insulation uptake | +0.30% | Asia-Pacific, Europe | Medium term (2-4 years) |

| Li-ion battery fire-safety felts | +0.20% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift of Upholstery Makers toward Low-Flammability Materials for Stricter Furniture Fire Codes

In 2025, the United Kingdom shifted its domestic furniture regulations, moving from halogenated additives to the inherently flame-resistant modacrylic pile. Massachusetts followed suit, banning organohalogen and organophosphorus retardants, steering North American upholstery makers towards halogen-free alternatives. In 2024, the European Chemicals Agency (ECHA) expanded its list of substances of very high concern (SVHC) to include more flame retardants, further limiting additive choices and reinforcing the regulatory emphasis on modacrylic. However, the uptake of modacrylic faces challenges due to its premium pricing over treated polyester. Suppliers are innovating, creating lighter piles under 400 gsm that achieve NFPA 260 Class I compliance without added finishes, positioning themselves to bridge the cost-performance gap and win favor with furniture OEMs.

Emergence of Low-Cyano Bio-Based Acrylonitrile Routes Cutting Production Toxicity

Trillium Renewables and NREL's pilot plants are at the forefront, converting glycerol and 3-hydroxypropionic acid into acrylonitrile. This innovative approach avoids the cyanide by-products common in propylene ammoxidation and promises a reduction in greenhouse gas emissions. With the EPA flagging acrylonitrile as a high-priority concern in 2024, industry players are keenly exploring these bio-routes to cut compliance costs[1]U.S. Environmental Protection Agency, “Toxic Substances Control Act High-Priority Substances,” epa.gov . Although current yields do not yet meet economic thresholds, the potential for modular construction near existing wet-spinning lines presents an opportunity to lower capital expenditures as catalyst technology progresses. Early adopters can benefit from reduced residual monomer levels, easing the path to REACH authorizations and speeding up audits for apparel brands concerning restricted substances.

Expansion of Modacrylic Acoustic Insulation in Electric-Vehicle Interiors

By 2028, global electric vehicle (EV) production is on track to exceed 20 million units. Amidst this backdrop, automakers are gravitating towards lightweight, non-halogenated acoustic packages that meet UL 94 V-0 standards without secondary chemistries. While polyester nonwovens dominate in cost, they depend on additive retardants that are under growing regulatory scrutiny. Modacrylic, boasting an inherent LOI over 28 percent, not only satisfies crash-test fire simulation benchmarks but, when fashioned into 200-300 gsm felts, achieves a damping coefficient of less than or equal to 0.85 NRC or higher at 1 kHz. Partnering with Tier-1 suppliers to develop automated die-cut panel formats will be crucial for replacing traditional polyester mats. Proving compatibility with high-speed thermoforming lines could be the game-changer.

Rising Use of Modacrylic Felts in Li-Ion Battery Fire-Safety Separators

Next-generation battery modules are now using multi-material thermal shields to address thermal runaway risks. At the cell level, ceramic-coated polyolefin is the preferred choice. Meanwhile, modacrylic felts are emerging as self-extinguishing inter-layer barriers at the module level. These felts not only support IEC 62133 certification but also uphold gravimetric energy density standards. Modacrylics face a challenge in achieving price parity with aramid paper, which is currently priced between USD 15-20 per kilogram. However, modacrylic's lower melting point provides an advantage, simplifying recycling processes, particularly when paired with polyester liners. For modacrylics to secure a position in gigafactory procurement pipelines during the forecast period of 2026-2031, third-party validation against lithium iron phosphate and NMC cathodes will be essential to gain automaker endorsement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPA and REACH limits on residual acrylonitrile | -0.60% | North America, Europe | Short term (≤ 2 years) |

| Viscose-based FR blends competing in PPE | -0.40% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| High energy intensity of wet-spinning | -0.50% | Global, regulatory pressure highest in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Inherently Flame-Retardant Viscose Blends in PPE

In the oil, gas, and utilities sectors, buyers of industrial workwear are increasingly opting for viscose-aramid blends. These blends not only meet NFPA 2112 standards but also come at a reduced fabric cost. While TenCate markets its Tecasafe Plus at a designated weight, it is important to highlight that similar Limiting Oxygen Index (LOI) values can now be achieved using phosphorus-enhanced viscose yarns. These enhanced yarns are durable, withstanding multiple industrial wash cycles. In a strategic response, modacrylic suppliers are co-spinning finer denier with high-tenacity polyamide. This enhancement aims to elevate tear strength and abrasion resistance, ensuring their continued presence in premium garments. However, they are yielding the low-cost commodity coveralls market to viscose alternatives.

High Energy Intensity of Wet-Spinning Raises Scope-3 Emissions Scores

The wet-spinning and dyeing processes for modacrylics emit substantial CO₂e for each kilogram produced. This highlights the pressing need for heat-recovery systems and a transition to renewable electricity. Such initiatives are vital for apparel brands striving to meet Scope-3 emissions targets[2]CDP, “Scope-3 Guidance for Apparel and Footwear,” cdp.net . Toray's launch of a mass-balance acrylic fiber showcases a potential decarbonization route via bio-feedstock attribution. Yet, this comes at a premium price, a burden only brands deeply committed to sustainability are prepared to bear. On the other hand, smaller mills across the Asia-Pacific region are struggling. They face hurdles with the capital outlay required for boiler electrification and wastewater heat recovery. This financial challenge might sideline them from partnerships with Western brands, particularly as carbon-pricing policies tighten.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Hair Fiber Extends Its Lead While Protective Apparel Consolidates

In 2025, hair fiber accounted for 54.22% of total revenue, charting a course with a 6.15% CAGR through the forecast period of 2026-2031. This surge is primarily fueled by Kaneka's Malaysian hub, which is actively supplying vibrant, heat-stable braids to e-commerce platforms across Africa. In the revenue race, protective apparel takes a significant spot, reaping benefits from the stringent NFPA and ISO standards enforced in refineries across North-America and utilities in Europe. However, its growth faces challenges, notably from competition with more budget-friendly viscose-aramid blends.

Growth in the upholstery and household sector remains modest, largely influenced by regulations in the United Kingdom and Massachusetts that ban additive flame retardants. This regulatory push is steering furniture OEMs toward adopting a naturally flame-retardant modacrylic pile. However, the adoption rate is slowed by the modacrylic's price premium compared to treated polyester. Industrial fabric and the modacrylic pile represent a significant share of the revenue, with automotive headliners and contract seating emerging as key niches. Additionally, there is early momentum in electric vehicle (EV) acoustic felts and battery fire-safety pads, signaling potential growth opportunities. Aksa's decision to expand its Armora line highlights industry confidence in multi-hazard garments and industrial fabrics, particularly those combining flame resistance with abrasion durability.

Geography Analysis

In 2025, the Middle-East and Africa accounted for 45.67% of global revenue, driven by a strong demand for premium synthetic hair fiber and a projected CAGR of 6.49% through the forecast period of 2026-2031. Key players, including Nigeria, South Africa, and Kenya, are transitioning from fragmented brick-and-mortar outlets to online retail. Gulf oil exporters, facing high ambient heat, are increasingly adopting flame-resistant workwear, with a preference for modacrylic blends due to their comfort.

The Asia-Pacific region, supported by specialty suppliers in Japan and a robust acrylic value chain in China, emerges as a significant contributor. In China, capacity clusters in Jiangsu and Zhejiang are investing in automation, leading to significant reductions in labor and solvent-recovery costs. Japan's Toray, reporting a year-over-year revenue increase in fibers and textiles for FY 2026, highlights a regional resurgence in demand for higher-margin specialty grades. Looking forward, India's goal to boost man-made fiber penetration is set to drive a rise in protective apparel, even as commodity apparel yarns face a slowdown.

North America and Europe are seeing growth in the low-to-mid single digits, driven by furniture demand and PPE regulations. The U.K. is steering its domestic upholstery producers towards halogen-free solutions, influenced by a mandate for lower ignition propensity and California's TB 117-2013 harmonization. Apparel brands are also tightening their Scope-3 targets, showing a preference for mills that provide mass-balance or renewable-electricity certified modacrylic. In South America, while overall consumption is modest, Brazil's automotive sector is adopting modacrylic headliners, mainly for export models heading to Europe, where fire-testing regulations for interior materials are stringent.

Competitive Landscape

The modacrylic fiber market is moderately consolidated, with the top producers holding a substantial share of global capacity. Aksa Akrilik, leveraging its in-house acrylonitrile plant to mitigate TSCA compliance costs, captured a significant slice of global sales in 2025. Kaneka is strategically focusing on hair fiber, tailoring its Malaysian production to cater to the African and Middle-Eastern markets, thereby enhancing logistics and service efficiency.

Toray's entry into mass-balance acrylics in 2025 not only positions it at the forefront of sustainability but also limits its uptake to brands with eco-conscious values. Smaller players are making their mark: Aksa's OnceDye technology significantly reduces water and energy consumption, while TenCate's Tecasafe Ecogreen, infused with lyocell for moisture management, meets NFPA 2112 compliance. In China, leading state-backed plants are consolidating, sidelining less-capitalized converters. The value chain is evolving, forming alliances with EV component suppliers and battery OEMs. These partnerships come with qualification cycles that can stretch beyond 24 months, favoring established players with substantial research and development and certification investments.

Modacrylic Fiber Industry Leaders

Aditya Birla Management Corporation Pvt. Ltd

Aksa Akrilik Kimya Sanayi AŞ

Dralon

Formosa Plastics Corporation

Kaneka Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Toray Industries has introduced a mass-balance acrylic fiber that utilizes certified renewable feedstock to minimize fossil-carbon intensity. This initiative is expected to strengthen the company's modacrylic fiber portfolio.

- October 2025: California's AB 1059 mandated the International Sleep Products Association to provide a quantitative health risk assessment of modacrylic fiber, free from antimony trioxide, to the bureau.

Global Modacrylic Fiber Market Report Scope

Modacrylic is a synthetic flame-resistant (FR) fiber known for its inherent flame resistance, which is a molecular-level property. It is a chemically modified acrylic fiber, with acrylonitrile units comprising 35% to less than 85% of its composition.

The Modacrylic fiber market is segmented by application and geography. By application, the market is segmented into protective apparel, hair fiber, industrial fabric, modacrylic pile, upholstery and household, and other applications. The report also covers the market size and forecasts for modacrylic fiber in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Protective Apparel |

| Hair Fiber |

| Industrial Fabric |

| Modacrylic Pile |

| Upholstery and Household |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Protective Apparel | |

| Hair Fiber | ||

| Industrial Fabric | ||

| Modacrylic Pile | ||

| Upholstery and Household | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the modacrylic fiber market in 2026 and 2031?

The modacrylic fiber market size stands at USD 603.15 million in 2026, and it is projected to reach USD 722.96 million by 2031 at a 3.69% CAGR.

Which application contributes the most revenue?

Hair fiber accounts for 54.22% of sales and is expanding at a 6.15% CAGR through 2031.

Which region is growing the fastest?

The Middle-East and Africa lead with a 6.49% CAGR over 2026-2031, buoyed by synthetic-hair demand and stricter safety codes.

What regulatory trends affect suppliers?

Tightening EPA and REACH limits on residual acrylonitrile and expanding bans on additive flame retardants are driving investment in closed-loop recovery and inherent FR chemistries.

Where are new growth opportunities emerging?

Electric-vehicle acoustic insulation and lithium-ion battery thermal barriers present white-space niches if modacrylic can match polyester and aramid cost structures.

Page last updated on: